EC, June 25, 2007, No M.4671

COMMISSION OF THE EUROPEAN COMMUNITIES

Judgment

UTC / Initial ESG

Dear Sir/Madam,

Subject: Case No COMP/M. 4671 UTC / Initial ESG

Notification of 16/05/2007 pursuant to Article 4 of Council Regulation No 139/20041

I. INTRODUCTION

1. On May 16, 2007, the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which the undertaking United Technologies Corporation ("UTC", USA) acquires within the meaning of Article 3(1)(b) of the Council Regulation control of the whole of Initial Electronic Security Group ("Initial ESG", United Kingdom) by way of purchase of share.

II. THE PARTIES

2. UTC is a diversified industrial corporation which is active in numerous fields, including manufacturing, technology and services for building systems and aerospace industries. The UTC portfolio of companies includes Otis Elevator Company, Pratt & Whitney, as well as UTC Fire & Security.

3. Initial ESG consists of five companies (together with their subsidiaries) that are currently controlled by the British company Rentokil Initial. Initial ESG offers security and fire protection systems and related services.

III. THE CONCENTRATION

4. The operation consists of the acquisition by UTC of sole control of Initial ESG by way of purchase of shares. The transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

IV. COMMUNITY DIMENSION

5. The concentration has a Community dimension under Article 1(2) of the Merger Regulation. Indeed (i) the combined aggregate worldwide turnover of UTC and Initial ESG in 2006 exceeds EUR 5 billion; (ii) the aggregate Community-wide turnover in 2006 of each of the two undertakings concerned exceeds EUR 250 million; (iii) none of the undertakings concerned achieves more than two-thirds of its aggregate Community- wide turnover within one and the same Member State.

V. COMPETITIVE ASSESSMENT

A. MARKET DEFINITION

6. The parties' activities overlap in alarm monitoring, electronic security systems, and fire detection and alarm systems.

1) RELEVANT PRODUCT MARKETS

Alarm Monitoring

7. Alarm monitoring consists in the provision of alarm monitoring services through a central monitoring office, or Alarm Receiving Centre (ARC). These offices receive incoming signals from connected fire and intrusion alarm systems, interpret and verify them, and notify an appropriate respondent if necessary.

8. In line with previous Commission's decisions2, the notifying party submits that alarm monitoring services constitute a single relevant product market. According to the notifying party, this is warranted by both demand-side and supply-side considerations. From the demand-side, customers have similar alarm monitoring needs and there are generally no differences in the prices charged to comparably sized customers. From the supply-side, monitoring offices usually provide the same range of services from simple monitoring to full-service monitoring requiring various actions to be taken upon receipt of an incoming alarm signal.

9. Monitoring services are purchased by a wide range of customers. Customers include residential users, small and large commercial businesses, multi-national companies, and government entities. The Commission assessed during its investigation whether services to all customers belong to the same relevant product market. Certain respondents to the market investigation indicated that it is necessary to differentiate between alarm monitoring services provided to large customers with many sites / branches and for whom a nation-wide footprint is required3 and alarm monitoring services provided to smaller customers.

10. It is however not necessary to conclude on the question of whether all alarm monitoring services belong to the same relevant product market for the purposes of this decision since the transaction does not raise serious doubts as to its compatibility with the EEA agreement under any alternative.

Electronic Security Systems (ESS)

11. Electronic Security Systems (ESS) are systems designed to provide access security and to detect unauthorized entry and may comprise intrusion alarms, access controls, and closed-circuit TVs, and often include configuration, installation, and maintenance of these devices. End-customers include residential and commercial customers, as well as public and governmental entities.

12. Initial ESG contracts out the manufacture of ESS devices4 and the overlap of activities is limited to the servicing part of the business, that is, configuration, installation and maintenance.

13. In line with previous Commission's decisions, the notifying party submits that installation and service of ESSs constitute a single relevant product market since customers often purchase combined systems and suppliers are capable of supplying each type of system separately or in combination.

14. As in the case of alarm monitoring services, the Commission's market investigation provided indications that it may be relevant to further segment the market depending on the size of customers. It is however not necessary to conclude on the question of whether all ESS installation and related services belong to the same relevant product market for the purposes of this decision since the transaction does not raise serious doubts as to its compatibility with the EEA agreement under any alternative.

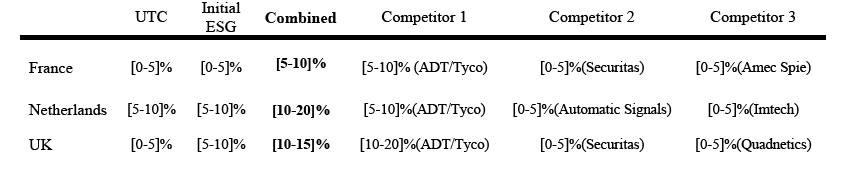

Fire Detection and Alarm Systems

15. Fire protection products and services are designed to protect lives and preserve property in the event of fire. The parties both provide fire detectors and alarms, fire suppression systems, and portable fire extinguishers.

16. As regards fire detectors and alarms, the parties’ activities are predominantly the configuration, installation, and servicing of fire detectors and alarms.5 In line with the Commission’s findings in previous cases6, the notifying party submits that it is appropriate to identify the configuration, supply, installation and service of fire detectors and alarms as a relevant product market.

17. As regards fire suppression systems, they are used to contain or extinguish fires. There exist different types of fire suppression systems: sprinklers, water mist systems, gaseous fire suppression systems (GFSSs), and foam/powder-based systems. While the Commission considered in a previous case7 the existence of a separate market for the sale of GFSSs8 and also of the (narrower) possible markets for GFSSs for land-based applications and for GFSSs for marine-based applications, the parties take the view that there is a single product market encompassing the sale of sprinklers, water mist systems, and GFSSs since all systems are substitutable to a large extent.

18. Finally, portable fire extinguishers (PFEs) are metal cylinders filled with a fire-fighting agent intended to contain and control fire. They can be designed for residential use (RPFEs)—they are then sold to end-customers—or for commercial use (CPFEs) and are then sold to independent fire traders. In line with past Commission's decisions9, the notifying party takes the view that the sale of CPFEs and that of RPFEs are two distinct product markets.

19. It is however not necessary to conclude on the precise scope of the relevant products in the field of fire detection and alarm systems for the purposes of this decision since the transaction does not raise serious doubts as to its compatibility with the EEA agreement under any alternative.

2) RELEVANT GEOGRAPHIC MARKETS

20. As for the geographical scope of the market, the notifying party submits that the relevant geographic markets for all the above-mentioned product markets are national, in line with previous Commission's decisions10. With regards to alarm monitoring this reflects the existence of national regulations and standards, nationally or locally based monitoring, installation and servicing, as well as language differences. National insurance requirements, customer preferences for national, regional or local providers as well as nationally or locally based installation and servicing are also to be considered for Electronic Security Systems and fire detection and alarm systems. The market investigation has confirmed that the above-mentioned markets are national in scope for alarm monitoring services and did not provide any indication that this could be different for Electronic Security Systems or fire detection and alarm systems

21. In view of the above, for the purposes of this decision, the relevant product markets will be considered as national in scope.

B. COMPETITIVE ASSESSMENT

22. In the EEA, the activities of UTC and Initial ESG only overlap to a meaningful extent for alarm monitoring services and Electronic Security Systems in the Netherlands11 and in the UK. Other markets are not further discussed in the present decision.

A. Alarm Monitoring

23. The proposed transaction gives rise to significant horizontal overlaps in the field of alarm monitoring only in the Netherlands and the UK. The table below provides the parties' market shares in value in 2006:

24. Any anti-competitive effects as a result of the merger are unlikely in view of the limited combined market share of the parties. In both the Netherlands and the UK, the new entity would face the competition of large companies (Securitas, ADT/Tyco, Group 4) as well as numerous smaller companies present on these fragmented markets. The notifying party further argues that there is no obstacle to switching for customers.

25. The market investigation has confirmed that alarm monitoring services offered by different suppliers are generally similar and interchangeable. Accordingly, the majority of the customers interviewed during the market investigation confirmed that they can switch suppliers with relative ease and a limited cost in most cases.

26. As regards specifically the Dutch market for alarm monitoring, no concerns were voiced by customers except for one who expressed the fear that, given the size of the new entity, it would no longer be regarded as an important customer and therefore suffer from a quality drop. However, in view of the existence of several other suppliers of these services which will continue to compete with the new entity in price and quality and the fact that the switching of supplier occurs relatively easily and can be done in a timely fashion12, the risk that the proposed transaction would entail anti-competitive effects seems limited.

27. In the UK, all respondents to the market investigation but one also confirmed that several alternative suppliers would remain on the market after the merger and did not express concerns about the competitive effect of the transaction. One UK customer however raised objections to the proposed acquisition and claimed that the merger would lead to a reduction in the number of national suppliers of alarm monitoring from three to two and this would lead to significantly reduced competition in the UK market. According to this large customer, only the two parties and Tyco/ADT have sufficient scale to meet the need of multi-site customers with hundreds of sites to be monitored over the country.

28. This view was not shared by other large customers in the UK who mentioned the presence of several alternative suppliers capable of providing monitoring services to large national customer, such as Group 4/Securicor, Securitas, Reliance and VSG13. This is confirmed by a submission of the notifying party that lists the suppliers of customers with a large number of sites and wide geographic footprints14.

29. Therefore, in view of the number of alternative suppliers for each category of customers and the limited market position of the new entity on the market for alarm monitoring, the proposed operation does not give raise to competition concern on the Dutch and UK alarm monitoring markets.

B. Electronic Security Systems (ESS)

30. The proposed transaction gives rise to horizontal overlaps in the field of ESS only in France, the Netherlands and the UK. The table below provides the parties' market shares in value in 2006:

31. While these national markets are not affected, the above mentioned large UK customer expressed also its concerns on the impact of the transaction on the market for Electronic Security Systems in the UK on the account that maintenance services for customers with many sites can only source these services from suppliers with a nation-wide footprint. However, other large companies interviewed in the course of the market investigation did not share this concern and it appears that several suppliers with a national coverage remain on the market (ADT, Securitas, Group 4, Kings, Secom, etc.) and will be able to compete with the new entity.

32. Thus, the proposed operation does not give raise to competition concern on the French, Dutch and UK alarm monitoring markets.

VI. CONCLUSION

33. For the above reasons, the Commission has decided not to oppose the notified operation and to declare it compatible with the common market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of Council Regulation (EC) No 139/2004.

1 OJ L 24, 29.1.2004 p. 1.

2 M.3396 – Group 4 Falck/Securicor.

3 According to the market investigation, the nation-wide footprint for monitoring services would be a

requirement for these larger customers who source monitoring services together with installation, and

maintenance services of security systems.

4 UTC has some small ESS component manufacturing activity and thus has to also source most of its components from third parties.

5 However, UTC manufactures some components which generate minor sales to third parties.

6 M.3686 Honeywell/Novar and M.2584 Tyco/Sensormatic.

7 M.3688 UTC/Kidde.

8 This would imply the definition of separate product market for sprinklers and water-mist systems

9 M.3688 UTC/Kidde. A distinction between the market for CPFEs for Independent Fire Traders and for

CPFEs for end-customers was also examined but has no effect on the competitive assessment of this case.

10 With the exception of the markets for fire suppression systems and portable fire extinguishers for which

the notifying party takes the view that it is not necessary to define the precise scope given the marginal

scope of Initial ESG's sales.

11 In the markets for fire detection and alarm systems, the market shares of Initial ESG in all the national

markets are below [0-1]%leading to a negligible increase of the market share already held by UTC and to

combined market shares below[30-40]%.

12 Approximately two months for large companies.

13 Furthermore, many of these companies perform the monitoring of their premises internally.

14 Submission from the notifying party, June 13, 2007