EC, July 26, 2007, No M.4706

COMMISSION OF THE EUROPEAN COMMUNITIES

Judgment

SUPERIOR ESSEX/ INVEX

Dear Sir/Madam,

Subject: Case No COMP/M.4706 - SUPERIOR ESSEX/ INVEX

Notification of 21.06.2007 pursuant to Article 4 of Council Regulation No 139/2004[1]

1. On 21.06.2007, the Commission received a notification of a proposed concentration pursuant to Article 4 and following a referral pursuant to Article 4(5) of Council Regulation (EC) No 139/2004 (“Merger Regulation”) by which the undertaking Superior Essex Inc. (hereinafter referred to as “Superior Essex”) acquires within the meaning of Article 3(l)(b) of the Council Regulation control of Invex S.p.A. (hereinafter referred to as “Invex”) by way of purchase of shares.

1. THE PARTIES

2. Superior Essex is a US company active in the manufacture and supply of cable and wires made of copper and other materials for telecommunications purposes, fibre optic cables for use in the telecommunications sector and winding wires for producers of electromagnetic devices. In Europe, Superior Essex operates through a solely controlled subsidiary Essex Nexans Europe SAS ("Essex Nexans"). Superior Essex worldwide sales in 2006 amounted to € 2.3 billion, of which [... ] were achieved in the EEA.

3. Invex is an Italian company active in the manufacture and supply of winding wires. Invex is mainly active in the EEA where it achieved in 2006 [...].

II. THE OPERATION AND THE CONCENTRATION

4. Pursuant to a Sale and Purchase Agreement signed on 30 April 2007, Superior Essex will acquire 100% of the shares of Invex. The notified operation is intended to confer on Superior Essex sole control over Invex. It therefore constitutes a concentration within the meaning of Article 3(l)(b) of the Merger Regulation.

III. COMMUNITY DIMENSION

5. Superior Essex recorded a worldwide turnover of € 2.3 billion and a Community-wide turnover of [... ] in 2006. Invex had a worldwide turnover of [...] and a Community-wide turnover of [...] in the same period. The notified concentration therefore does not have a Community dimension within the meaning of Article 1 of the Merger Regulation.

6. However, on 16 May 2007 the notifying party informed the Commission in a reasoned submission pursuant to Article 4(5) of the Merger Regulation and Article 6(5) of Protocol 24 of the EEA agreement that the concentration was capable of being reviewed under the national competition laws of at least three Member States, namely Germany, Italy, Portugal and the United Kingdom and requested the Commission to examine it. None of the Member States competent to examine the concentration indicated its disagreement with the request for referral within the period laid down by the Merger Regulation.

7. Therefore the concentration is deemed to have a Community dimension pursuant to Article 4(5) of the Merger Regulation.

IV. COMPETITIVE ASSESSMENT

8. Both parties are active in the production and supply of winding wires. Winding wires are used in the production of a variety of electromagnetic devices such as motors, transformers, control devices, relays and generators. These devices are in turn used, among others, in automotive applications, in the manufacture of domestic appliances, pumps, multimedia, computers, insulation and lighting applications.

9. In addition, Superior Essex produces enamels which are used in the production process of enamelled winding wires.

A. Relevant product markets

1. Winding wires

10. Winding wires are manufactured from bare copper wires which are usually coated/enamelled with different types of enamel or other insulating materials such as paper and various textiles according to the application. When enamel is used, it allows the maximum amount of copper to be wound into a given space so as to produce the maximum magnetic field. The main characteristics of a winding wire are determined by its cross-sectioned area and the type of coating.

11. In a previous decision[2], the Commission considered that enamelled wires and winding wires constituted the relevant product market. In line with the Commission previous findings, the notifying party considers that it is not appropriate to sub-segment the market into individual types of winding wire citing inter alia a high degree of supply side substitutability. They do however acknowledge that within the industry it is common to define winding wire into two broad categories: round wire and flat wire (also known as 'winding strips').

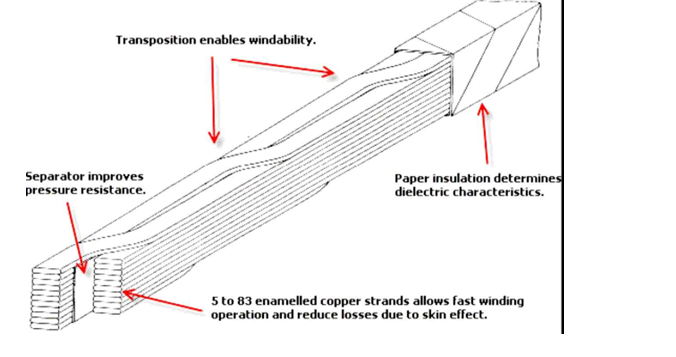

12. Within these broad categories, the notifying party admits that various subsets exist such as fine round wire (of a diameter below 0.15 mm), self bonding wire (either round or flat with a special enamel which allows the customer to bond the wire directly) and CTC (continuously transposed cable) wire. As shown in the drawing below, CTC consists of at least five strands of flat wire twisted together (or transposed) and is primarily used in power transformers.

13. Invex does not have any sales of fine round wire and only minor sales of self-bonding wire. Accordingly, the market investigation focused on the relevance of defining distinct product markets within a wider market for winding wires (including both enamelled, paper covered and uncoated wires), i.e. markets for (i) round winding wires, (ii) flat winding wires and (hi) CTC (a sub-segment of the (flat) winding wire market).

14. On the demand side, the notifying party submits that there are several applications for which the customer may choose between a round and a flat wire. As regards CTC, which represents 5% of the total sales of winding wires[3] and is mainly used for some high power transformer applications, the notifying party submits that the customer may choose between CTC and paper wrapped flat wires which the customer would then transpose himself.

15. Responses of customers to the market investigation show that there are mixed views on the relevant delineation of the product market of winding wires. Indeed about half of the respondents indicate that they view the relevant product as including all types of winding wire, while the other half would rather make a distinction between round and flat, and for some of them, a further distinction for CTC. However a clear majority of customers state that market conditions are roughly the same for winding wires for different applications. As regards CTC, customers explain that CTC was specifically developed to be used in high voltage transformers and substituting CTC with single flat winding wires would lessen the technical possibilities of a transformer and reduce its competitiveness. One customer mentions the use of CTC as a "best practise" in transformer production.

16. The notifying party submits that there is a high degree of supply-side substitutability for the production of wires of the same cross-sectional shape (i.e. round or flat). While round wires of small diameters are usually enamelled on horizontal enamelling machines, larger round wires and flat wires are normally enamelled on vertical enamelling machines to prevent the wire from bowing due to its weight. Therefore while it is possible by changing the shape and size of the dies through which the wire is run, to change the production from large round wires to flat wires, the substitution between small round wires on one hand and large round wires or flat wires on the other hand is more limited. However, it would appear difficult to make a distinction based on this consideration as there is no standard in the industry and the definition of small round wires versus large round wires depends on the equipment used. As regards CTC, its production requires the addition of a specific machine at the end of the flat wire production process for the transposing process. The notifying party submits that this machine would be available from several suppliers and the cost and time needed to install it would not be significant.[4] [5]

17. In the course of the market investigation, winding wire manufacturers acknowledge that while the same process is used for the manufacture of round and flat winding wires, the equipment differs depending on the diameter of the wire. However only some of the competitors state that separate markets for flat and round winding wires should be defined on that basis, and many consider that the product market should encompass round and flat winding wires. Moreover most winding wires manufacturers are active in the supply of both round and flat wires. As regards CTC, competitors explain that while it is true that equipment to transpose the wires is available on the market, CTC production requires more sophisticated know how, which would, in addition to the small volume of demand, partly explain why few suppliers are active in CTC.

18. Based on the above, although there are some indications that separate markets could be defined for round, flat and CTC winding wires, the results of the market investigation do not appear to be conclusive. In any case, the question can be left open for the purposes of the present case since it would not materially change the competitive assessment.

2, Enamels

19. Enamels are used in the production process of enamelled winding wires to give the wire particular desirable properties such as improved insulation or weather resistance. Enamels used in winding wire applications are generally not appropriate for use in other applications and vice versa. Therefore the notifying party submits that the relevant product market is enamels for winding wires. The notifying party does not consider that it is necessary to further segment the market into different types of enamels as the main enamels suppliers make broadly the same range of enamels and there is no specific enamel type where Superior Essex would enjoy a significant position. The market investigation did not raise any alternative product market definition.

B. Relevant geographic markets

20. The notifying party notes that in the Alcatel/AEG Kabel decision, the Commission considered the market for enamelled and winding wires to be Community-wide as transport costs are not significant and standardised specifications encourage the free flow of products between Member States. For the purposes of the present transaction, the notifying party submits that the geographic scope of the market is at least EEA-wide and could possibly include Turkey. In the course of the market investigation, the notifying party submission has been unanimously confirmed by the competitors and the customers, with the exception of customers located in Italy, which rather consider the winding wire market to have a national dimension.

21. Italian customers' answers can be explained by the fact that Italy is by far the largest producer of winding wires in the EEA and production in Italy exceeds local demand5. However Italy should not be regarded as a separate market as there are no barriers to supply customers in Italy and there are already customers supplied by non-Italian producers. This is reflected by the parties' own experience, when Invex lost customers which switched to non-Italian suppliers.

22. As regards enamels, the notifying party submits that the geographic scope of the market is at least EEA-wide as Superior Essex supplies enamels to winding wire manufacturers located throughout Europe as do its competitors and prices do not vary significantly on a country-by country basis. The market investigation did not contradict this view.

C. Competitive assessment

1. Winding wires

23. The following table presents the market structure at the EEA level (in volume[6], 2006) for all winding wires and according to a segmentation between round and flat winding wires:

Competitor | Total winding wire | Round wire | Flat wire (excluding CTC) | |||

Volume (T) | Market share | Volume (T) | Market share | Volume (T) | Market share | |

Superior Essex | [75.000- 100.000] | [10-20%] | [75.000- 100.000] | [20-30%] | [5.000- 10.000] | [5-10%] |

Invex | [25.000- 50.000] | [5-10%] | [25.000- 50.000] | [5-10%] | [<5.000] | [5-10%] |

Combined | [100.000- 150.000] | [20-30%] | [100.000- 150.000] | [30-40%] | [10.000- 25.000] | [10-20%] |

Elektrokoppar | [50.000- 75.000] | [10-20%] | [25.000- 50.000] | [10-20%] | [5.000- 10.000] | [10-20%] |

IRCE | [25.000- 50.000] | [10-20%] | [25.000- 50.000] | [10-20%] | [<5.000] | [5-10%] |

Schwering | [25.000- 50.000] | [5-10%] | [25.000- 50.000] | [10-20%] | “ | “ |

Acebsa | [25.000- 50.000] | [5-10%] | [25.000- 50.000] | [5-10%] | [<5.000] | [0-5%] |

Ederfil | [25.000- 50.000] | [5-10%] | [25.000- 50.000] | [5-10%] | “ | “ |

Others | [100.000- 150.000] | [20-30%] | [50.000- 75.000] | [20-30%] | [25.000- 50.000] | [60-70%] |

Total market | [250.000- 500.000] |

| [250.000- 500.000] |

| [75.000- 100.000] |

|

24. It appears from the table above that the proposed transaction will increase the pre-existent leading position of Superior Essex in the different markets for winding wires, should it be defined as separate for round and flat or as a sole market. Post merger the combined market shares of the new entity would be [20-30%] (Superior Essex, [10-20%]; Invex, [5- 10%]) on a market including all winding wires, [30-40%] (Superior Essex, [20-30%]; Invex, [5-10%]) on the basis of a narrower market for round wires and [10-20%] (Superior Essex, [5-10%]; Invex, [5-10%]) if a market for flat wires is considered.

25. In each of these markets, the new entity will still face a significant number of competitors that for the most part offer a broad range of winding wire products equivalent to the parties' products. Competitors include Elektrokoppar ([10-20%], [10-20%] and [10-20%]), on the markets for all winding wires, round wires and flat wires respectively), IRCE ([10- 20%], [10-20%] and [5-10%]) and Schwering ([5-10%] in all winding wires and [10-20%] in round wires).

26. During the market investigation, some customers of round winding wires expressed their concerns that should the transaction take place, the removal of one player would reduce competition and might lead to a price increase and reduction of capacity. However, after a careful examination of the comments and information received from third parties and the notifying party, the Commission has come to the conclusion that the proposed transaction is unlikely to create competition concerns in the markets for all winding wires, round wires and flat wires (excluding CTC) for the reasons detailed below.

27. As shown in the table above, the new entity will continue to face competition from a significant number of existing competitors. In addition, some of these competitors appear to have plans to increase their production capacity for a total estimated by the notifying party of approximately [50.000-75.000] tonnes in the next one to two years[7].

28. According to the notifying party, there is already an over-capacity in the winding wire industry that is estimated at around 15%[8] by industry experts and at [30-40%] by the notifying party. Data further submitted by the notifying party[9] shows that total production capacity of round and flat winding wires amounted to [500.000-750.000] tonnes in 2006, compared to sales of [250.000-500.000] tonnes. During the market investigation, the main winding wire producers submitted that their capacity utilisation rate was between 85% and 95%.

29. The market investigation has confirmed that there are suppliers that constitute credible alternatives to the parties. Indeed when asked to name Superior Essex's strongest competitors, only one customer out of four cited Invex. As regards Invex's strongest competitors, Superior Essex was cited by only one customer out of five. In total, customers cited a large number of competitors to the parties, some of which were mentioned as often if not more so than the parties themselves as each other's strongest competitor. Therefore, in case of an attempt by the merged entity to increase prices, customers could find substitutable products from other suppliers. In fact, customers unanimously confirmed in the course of the market investigation the notifying party's submission that they already multi-source their requirements of winding wires from several suppliers. Having further examined the list of the largest suppliers of round and flat winding wires, Superior Essex and Invex appear to be both suppliers of the same customer in only less than 25% of the cases.

30. Furthermore the market investigation confirmed the notifying party's submission that contracts with customers are generally short term (one to two years) ant that customers can easily switch suppliers within an average of 6 to 12 months, depending on the final application concerned.

Hypothetical market for CTC

31. As noted above the market investigation did not clearly indicate that a separate market should be delineated for CTC. However the Commission has also considered such a hypothetical market.

32. On the basis of a hypothetical market for CTC, the production capacity in 2007 and the market positions of the parties and their competitors over the last three years are summarized in the table below:

Competitor | Capacity (2007) | Sales (2006) | Sales (2005) | Sales (2004) | ||||

Tonnes | % | Tonnes | % | Tonnes | % | Tonnes | % | |

Superior Essex | [5.000- 10.000] | [10- 20%] | [<5.000] | [10- 20%] | [<5.000] | [10- 20%] | [<5.000] | [20- 30%] |

Invex | [5.000- 10.000] | [20- 30%] | [5.000- 10.000] | [20- 30%] | [5.000- 10.000] | [20- 30%] | [5.000- 10.000] | [20- 30%] |

Combined | [10.000- 25.000] | [30- 40%] | [10.000- 25.000] | [40- 50%] | [5.000- 10.000] | [40- 50%,] | [5.000- 10.000] | [40- 50%,] |

Asta | [10.000- 25.000] | [30- 40%] | [5.000- 10.000] | [30- 40%] | [5.000- 10.000] | [30- 40%] | [5.000- 10.000] | [30- 40%] |

IRCE | [5.000- 10.000] | [10- 20%] | [<5.000] | [10- 20%] | [<5.000] | [10- 20%] | [<5.000] | [10- 20%] |

De Angeli | [<5.000] | [10- 20%] | [<5.000] | [5- 10%] | [<5.000] | [5- 10%] | [<5.000] | [5- 10%] |

Bemka | [<5.000] | [5- 10%] | ” | ” | ” | ” | ” | ” |

Others (imports) |

|

| [<5.000] | [0-5%] | [<5.000] | [0- 5%] | [<5.000] | [0- 5%] |

Total market | [25.000- 50.000] |

| [25.000- 50.000] |

| [10.000- 25.000] |

| [10.000- 25.000] |

|

Non-coordinated effects

33. The proposed transaction will bring together two significant suppliers of CTC. The new entity will have a combined market share of [40-50%] (Superior Essex, [10-20%]; Invex, [20-30%]) and consequently replace the current market leader in the EEA, Asta, which has a market share of [30-40%]. Other competitors include two smaller players, IRCE ([10-20%]) and De Angeli ([5-10%]), which entered the CTC market in 2002 and recently increased its CTC production capacity by [<5.000] tonnes and a new entrant, the Turkish company Bemka, which has plans to enter the market by the end of 2007.

34. Demand for CTC wire in the EEA has increased in the last 5 years from [10.000-25.000] tonnes in 2001 to [25.000-50.000] tonnes in 2006. Despite this increase in demand, the notifying party submits that there is still overcapacity as reflected in the table above. Data collected during the market investigation from CTC competitors confirms that total installed capacity of CTC in the EEA currently exceeds the demand by approximately [30-40%] and that each competitor has free capacity. In addition to the existing capacity, the market investigation has confirmed the notifying party's submission that a company already active in the production of flat winding wires or CTC would need approximately one year and to invest in the range of 1 to 2 M€ to set up a new line for the production of [<5.000] tonnes of CTC.

35. CTC are winding wires used in the production of transformers, in particular of high voltage. Customers of CTC are therefore mainly large companies such as Siemens, Areva and ABB. Indeed the top four CTC customers, namely Siemens, Areva, ABB and SGB account for approximately [70-80%] of total EEA demand for CTC. As for the parties to the transaction, Superior Essex' top three customers (Siemens, Areva and SGB) represent [90-100%] of its European CTC sales whilst Invex' three main customers (ABB, Tamini and Siemens) account for [70-80%] of its CTC sales.

36. The notifying party submits that the strong buying power of these large customers is reflected by the decrease of CTC average prices over the last three years in a context of increased production costs, in particular as regards energy and raw material costs10. The notifying party submits that CTC prices decreased by [...] and [...] for Superior Essex and Invex respectively between 2004 and 2006. In addition, the notifying party has submitted similar evidence of individual price data of Superior Essex, results of annual renegotiations with its main customers[10].

37. In response to the market investigation, CTC customers confirmed the notifying party's claim that they have a multi-sourcing strategy for CTC, and usually source from at least two suppliers. Few customers expressed the concerns that the proposed transaction may result in a short term price increase as they would need from 6 months to 1 year to switch supplier. However these customers acknowledged that the new capacity coming on the market (mainly from Bemka and de Angeli) should defeat any attempt of price increase from the actual large players.

38. In view of this, the Commission concludes that the concentration would not lead to concerns with regard to non-coordinated effects in the EEA market for CTC.

Coordinated effects

39. Post merger, the new entity will have a market share of [40-50%] and its next competitor, Asta, [30-40%] on the EEA market for the sale of CTC. These market shares may suggest prirna facie a symmetrical duopoly consisting of the new entity and Asta. However for the reasons detailed below, the Commission considers that that it is unlikely that the proposed merger would create anti-competitive coordinated effects in the EEA market for CTC.

40. Although CTC could be considered as a relatively homogenous product, CTC is not a standard product and there is a huge variety of available products, usually produced on order, depending on the design of the transformer manufacturer. The different types of CTC can be described by reference to three main technical characteristics: size (thickness, width and radial height), single-strip insulation (e.g. Polyvinylacetal, Polyvinylacetal plus epoxy or Polyesterimide) and external insulation material (Kraft paper, special thermally upgraded paper, Nomex paper, Mylar polyester tape, glass tape or Cordex).

41. As regards transparency in prices, it appears from the examination of the price setting process, that there is a lack of price transparency. Indeed, in most cases, i.e. for the largest customers, prices are negotiated separately for each individual customer and customer- specific price lists are agreed in the course of supply negotiations. Price lists may be tailored to suit the requirements of a particular customer, in particular as regards the product range. In addition to individual negotiated price lists, quotations to spot market customers are made on a case-by-case basis, either on the basis of a "target price list" or without any reference to price lists. Furthermore, as previously described, customers all multi-source and split their requirements of CTC. This makes it more difficult for a competitor to infer prices negotiated with other suppliers, than in a typical "all or nothing" process.

42. Allocation of customers seems also unlikely as suppliers rely on sales to few large customers that typically multi-source and it would not appear rational for a supplier to give up supply to one of the few customers. Moreover the CTC market has shown a significant growth in the last years, both on the demand and on the supply sides which rather speaks against coordination as suppliers of CTC have increased their capacity and new suppliers have recently entered the market.

2, Enamels

43. Superior Essex supplies enamels to winding wire manufacturers and both parties are active downstream in the manufacture of winding wires.

44. As described above, the combined entity would have a market share of [20-30%] of the downstream market for the supply of winding wires. On the upstream market for the supply of enamels for winding wires, the notifying party submits that Superior Essex's share of merchant sales is [10-20%]. The clear market leader is Altana which has a market share of [60-70%] and the other main competitor is Dupont Herbert with [10-20%]. Unlike Superior Essex, both competitors are not vertically integrated in the production of winding wires.

45. The transaction will not bring about any new vertical integration as Superior Essex is already active pre-merger in the supply of enamels for winding wires. The only change brought about by the transaction is the increased market position of the combined entity in the downstream market for the supply of winding wires. However, as the market position of the new entity on the market for winding wires will be [20-30%] post merger, it is unlikely that the proposed transaction, by increasing Superior Essex's market share by [5- 10%], will provide the new entity with the ability or incentive to restrict the access of competing enamels suppliers to a sufficient base of customers. It seems also unlikely that the new entity will have the ability or incentive to restrict access to enamels to its competitors in the winding wires market given the presence of alternative suppliers which all offer comparable products.

V. CONCLUSION

46. For the above reasons, the Commission has decided not to oppose the notified operation and to declare it compatible with the common market and with the EEA Agreement. This decision is adopted in application of Article 6(l)(b) of Council Regulation (EC) No 139/2004.

[1] OIL 24, 29.1.2004, p. 1.

[2] Decision of 18 December 1991 in Case IV/M.165 Alcatel/AEG Kabel

[3] Round wires represent approximately 80% of the sales of winding wires in the EEA and flat wires (other than CTC) 20%.

[4] According to the Form CO, a machine would cost between € [1-2] million for a capacity of [<5,000] tonnes and its delivery and installation would take [approximately 1 year].

5 In 2005, production of winding wires in Italy amounted to 128,895 t compared to home market

requirements of 85,373 t. Source: EWWG The Winding Wire Business Group of Europacable, meeting -

ROME 8 - 9 June , 2006

[6] Market shares are expressed in volume as the notilying party submits that they are more accurate than in value, for which it would be difficult to compile the data.

[7] Source: parties' market intelligence and Commission's own investigation.

[8] Source: European Winding Wire Business Group.

[9] See notifying party's submission dated 12.07.2007.

10 Data submitted by the notifying party shows that in 2006, electricity and gas costs increased by [...] and

[...] respectively, and in 2007, rod and drawing costs increased by [...].- See notifying party’s submission

dated 12.07.2007.

[11] [...]. It should be noted that the price of the copper is covered by the customer and therefore does not enter into the calculation of these prices per kg (what is known in the industry as the "transformation value").