EC, November 12, 2007, No M.4735

COMMISSION OF THE EUROPEAN COMMUNITIES

Judgment

OSRAM / Sunny World

Dear Sir/Madam,

Subject: Case No COMP/M.4735 - OSRAM / Sunny World

Notification of 20/09/2007 pursuant to Article 4 of Council Regulation No 139/2004[1]

1. On 20 September 2007, the Commission received a notification of a proposed concentration pursuant to Article 4 and following a referral pursuant to Article 4(5) of Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings (“the Merger Regulation”) by which the undertaking OSRAM GmbH ("OSRAM", Germany) controlled by Siemens AG ("Siemens", Germany) acquires within the meaning of Article 3(l)(b) of the Council Regulation sole control of the undertaking Sunny World (HK) Ltd ("Sunny World", Hong Kong) by way of purchase of shares.

2. After examination of the notification, the Commission has concluded that the notified operation falls within the scope of the Merger Regulation. During the course of the proceeding, the notifying party submitted commitments to address concerns raised during the Commission's market investigation. However, after further analysis and investigation, the Commission concluded that these commitments were not necessary as the transaction does not raise serious doubts as to its compatibility with the common market and the functioning of the EEA Agreement.

I. THE PARTIES

3. OSRAM is active in the development, manufacture and sale of a wide range of lighting products such as lamps (light bulbs), fixtures and electronic ballasts. The parent company Siemens is active in various manufacturing, technology and services business activities.

4. Sunny World, which is registered in Hong Kong, is a newly formed entity for this transaction to control the target's manufacturing activities in mainland China. The target is also active in the development, manufacture and sale of lamps including compact fluorescent lamps with integrated ballast ("CFL-i" or "energy-saving light bulbs") and traditional light bulbs known as general purpose incandescent lamps ('"GLS").

II. THE OPERATION

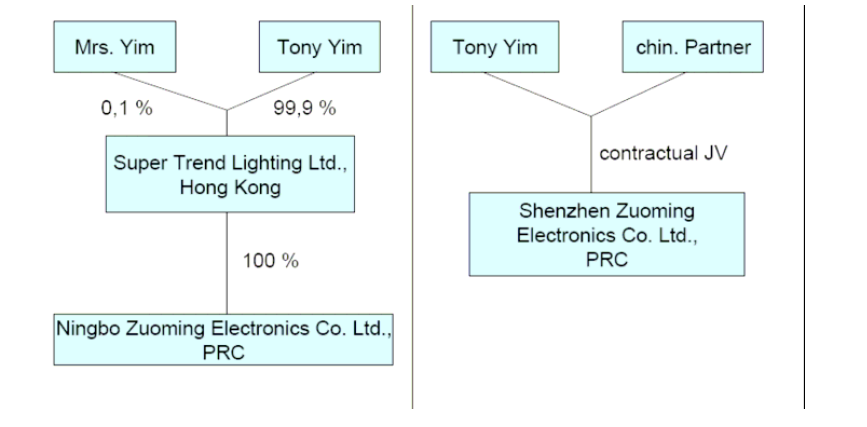

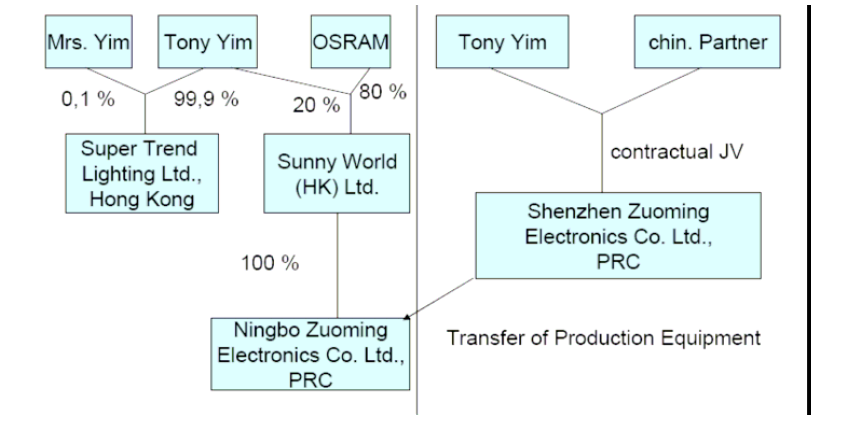

5. The notified concentration relates to the acquisition of sole control over Sunny World by OSRAM. Sunny World is currently controlled by Mr Tony Yim, who is also a 99.99% shareholder of Super Trend Lighting Co. Ltd ("Super Trend", Hong Kong). Prior to the completion of the transaction, Sunny World will acquire 100% of the shares of Ningbo Zuoming Electronics Co. Ltd ("Ningbo", China), one of the plants manufacturing CFL-i and GLS for Super Trend as well as certain assets of Shenzhen Zuoming Electronics Co. Ltd ("Shenzhen", China), which produces CFL-i only. Shenzhen as well as Super Trend will continue their business independently according to the parties as Super Trend is not part of the transaction and Shenzhen's assets will be leased back.

6. The pre and post-merger structure is shown below:

Pre-transaction

Post-transaction

III. CONCENTRATION

7. OSRAM will own 80% of the shares of Sunny World and will have the right to appoint [...] the majority of the Board of Directors. All decisions of the board will be taken by simple majority.

8. The remaining shareholder, Mr Yim, will own 20% of the shares [...]. However, OSRAM has a call option and Mr Yim has a put option for the remaining 20% shareholding of Mr Yim. According to the notifying party, both options are exercisable after three years.

9. OSRAM will thus acquire sole control over Sunny World. The proposed transaction therefore constitutes a concentration within the meaning of Article 3 of the Merger Regulation.

IV. COMMUNITY DIMENSION

10. The operation does not have a Community dimension within the meaning of Article 1 of the Merger Regulation. However, as the proposed transaction was capable of being reviewed in ten Member States[2] the notifying party submitted a request for referral under Article 4(5) of the Merger Regulation on 18 June 2007. None of the Member States competent to examine the concentration indicated its disagreement with the request for referral within the period laid down by the Merger Regulation.

11. The concentration is therefore deemed to have a Community dimension pursuant to Article 4(5) of the Merger Regulation.

V. COMPETITIVE ASSESSMENT

Introduction

12. As noted above, both OSRAM and the target owned by Mr Yim (via his company Super Trend and its subsidiaries) are active in the development, production and sale of lamps. Whilst Super Trend's core focus is CFL-i, OSRAM supplies a broad range of lamps. OSRAM sells its lamps mainly under its own trade name and via its own distribution network; Super Trend primarily supplies lamps to other producers or retail chains which then market the lamps under their own brands. Only the manufacturing activities of CFL-i and GLS and not the sales activities of Super Trend will be transferred to the newly created company, Sunny Worlds. The transaction therefore only concerns the production of CFL-i and GLS.

Relevant product market

13. The Commission has previously left open whether lamps for general purpose lighting4 should be sub-divided into incandescent, halogen, fluorescent, compact fluorescent and high intensity discharge lamps along the lines of the basic technology used and the broad characteristics of the lamp (e.g. energy consumption and properties of the light produced)[3].

14. In the present case, the notifying party submits that CFL-i and GLS each constitute a relevant product market that are distinct from the market for other lamps like noncompact fluorescent lamps, halogen and vehicle lamps.

15. CFL-i were first introduced by OSRAM in 1985 and combine the high energy efficiency of fluorescent lamps with the small size of incandescent lamps. As CFL-i have a built-in electronic ballast they can be used in the same sockets and normally in the same luminaires as GLS. Although the notifying party acknowledges that CFL-i may to a certain extent replace GLS, it maintains that the CFL-i and GLS currently belong to distinct markets and will continue to do so for the next 10-15 years. It argues that not all types of GLS lamps have a comparable CFL-i product available, many consumers still prefer the light colour and starting behaviour of GLS and the manufacturing costs and retail prices of CFL-i are considerably higher than those of GLS. In addition, given the different manufacturing processes, there is no supply side substitutability between GLS and CFL-i.

16. CFL-i are available in different shapes such as stick, globe reflector, spiral and candle versions and life-times such as 6,000, 10,000 and 15,000 hours. In spite of these differences, the notifying party submits that given a high degree of demand and supply- side substitutability, it is not appropriate to sub-divide the CFL-i market.

17. Respondents to the Commission's market investigation in the present case have expressed a range of opinions regarding the product market definition. Whilst competitors broadly agreed that it was not possible to switch production between various types of general purpose lamps (e.g. incandescent, fluorescent, halogen, compact fluorescent) there was less support for the notifying party's claim that all types of CFL-i and GLS respectively could be produced on the same production equipment. At the same time, several competitors indicated that with continued improvements in CFL-i technology and performance and the gradual erosion of the price differential between CFL-i and GLS, the two lamp types form part of one and the same product market. Similarly, whilst all competitors confirmed that lamps for special applications (e.g. vehicle lights and tanning lights) do not belong to the same market as lamps for interior lighting, a minority suggested that lamps for outdoor use (e.g. street and railway lighting and floodlights) would belong to the same market as lamps for interior lighting.

18. Furthermore, the market could be sub-divided into private label and branded product- segments as the price premium for branded products can - according to market participants - reach 20-30%. Nevertheless, a vast majority of customers indicated that branded and private label products are interchangeable from the point of view of the end-consumer. Also, supply-substitutability prevails since light bulbs from the same production line can be sold under private label or a brand as is the case with CFL-i sold by Super Trend (see below).

19. In the present case the precise product market definition, in particular the question whether CFL-i and GLS belong to the same market or constitute separate markets as well as if within the CFL-i market different segments have to be considered can be left open as it would not affect the competitive assessment (see below).

Relevant geographic market

20. In the previous cases dealing with the market for lamps for general purpose lighting, the Commission has left the geographic market definition open[4]. In the present case, the notifying party submits that the markets for CFL-i and GLS are at least EEA wide if not worldwide although it acknowledges that transport costs play a more significant role in the final cost of GLS.

21. The majority of competitors in the market investigation have confirmed that the markets at the production level are at least EEA-wide and possibly worldwide as most of the supply is coming from China. However, there were indications that the distribution of both CFL-i and GLS is carried out at a national level with a majority of customers indicating that they purchase lamps on a national basis and consider that it is important for suppliers to have a sales force especially for the distribution of branded products in each national market where they are active. There were indications from competitors that prices were generally set at a national level. A clear majority of customers with operations in different Member States, however, indicated that these prices did not differ to an appreciable extent.

22. In the present case the precise geographic market definition can be left open as it would not affect the competitive assessment (see below).

Competitive Assessment

23. The EEA wide market for CFL-i amounted, according to the notifying party's estimates, to EUR [...] million for a volume of [...] million pieces. Roughly 70% of the CFL-i sold in the EEA were imported from China, where most of the world-wide production capacity of 1.4 billion pieces is located. The Commission's market

investigation however has given indications that the EEA-wide market for CFL-i is larger than the party's estimate and the following analysis is based on the Commission's findings. For GLS the corresponding figures are EUR [...] million and [...] billion pieces, the vast majority (91% according to the notifying party) produced within the EE A.

24. The activities of OSRAM and Sunny World overlap in the production and supply of CFL-i as well as GLS. Because Sunny World has only a limited presence in the GLS segment with a market share of [0-5]% based on value (and [0-5]% in volume) in 2006, the proposed transaction would not lead to any competition concerns if one were to consider (i) GLS or (ii) GLS plus CFL-i as the relevant product market.[5] The competitive assessment therefore concentrates on the CFL-i segment only.

Market Shares for CFL-i

25. As mentioned above, most of the CFL-i sold in the EEA are imported from China although the main European suppliers OSRAM, Philips, General Electric ("GE"), and Sylvania all have production in Europe. In China - according to the notifying party - between 300 and 400 companies are manufacturing energy saving lamps, but only a limited number of companies export to Europe currently. Imports to the EU of CFL-i originating in China have been subject to anti-dumping duties since February 2001[6], thereby creating a barrier to entry for those Chinese producers that would have to pay the full anti-dumping duties.

26. The anti-dumping duties have recently been extended for a period of one year following the conclusion of an expiry review.[7] Certain Chinese producers which cooperated with the anti-dumping investigation have been granted an individual (lower) anti-dumping duty. Companies which did not receive an individual duty are subject to the 'all other companies' rate. This results in the following structure of antidumping duties on imports of CFL-i originating in China :

- Lisheng Electronic and Lighting ('Lisheng') 0%

- Shenzhen (the plant owned by Mr Yim) 8.4%

- Philips and Yarning Lighting Co. Ltd (a Philips IV) 32.3%

- Five other producers with an individual rate[8) 17.1-59.5%

- All other companies (inch the Ningbo plant, the second plant owned by Mr Yim) 66.1%

27. European producers either participate in joint ventures in China and/or source CFL-i directly from Chinese producers. For example, Philips has two joint ventures in China, including Philips & Yarning Lighting Co., Ltd which has an anti-dumping duty of 32.3%. OSRAM, [...] and Sylvania source directly from Chinese suppliers, in particular from Super Trend[9] and sell the production either under their own brand or as a private label. Total imports from China in 2006 were approximately 135 million lamps.

28. Based on the replies to the market investigation and the figures submitted by the notifying party the shares of supplies at the production level (imports plus EU manufacturing) to the EEA are as follows:

Table 1: Volume based market shares on production level for CFL-i sold in EEA (2006)

Source: Estimates based on figures provided by the Parties and replies to the Market Investigation |

29. The proposed transaction would therefore result in the creation of a second strong player in the market behind Philips followed by General Electric, Sylvania and several other suppliers, mainly from China.

30. Taking account of the cross-supplies between producers the market share calculated on the basis of supplies to retailers are as follows[10]

Table 2: Volume based market shares of supplies to the retail level in EEA (2006)

Source: Estimates based on figures provided by the Parties and replies to the Market Investigation

|

31. The proposed transaction would result in the creation of a second strong player in the market in the supply of CFL-i to the retail level behind Philips. Since Sunny World does not sell products under its own brand in the EEA there would be no overlap in the branded segment, whereas in the private label segment the merged entity would create a second strong player behind Lisheng.

Competition concerns raised during the market investigation

32. In view of this market structure, any horizontal effect from the notified transaction would thus appear to be very limited. The market investigation indicated that customers at the retail level do not perceive OSRAM and Super Trend as close substitutes. Nevertheless, in the market investigation several competitors raised concerns about the effects of the merger. The Commission has thoroughly investigated these concerns that focus on different segments of the market.

Horizontal concerns

33. One competitor has argued that the market for CFL-i should be looked at as a differentiated product market with three segments: a "first price" private label segment where hard-discount retailers like Aldi or Lidl offer CFL-i at low prices, a genuine private label segment served by companies like IKEA or Carrefour with their own brand and finally a branded segment, where Philips, GE, OSRAM, Sylvania and Lisheng with its brand Megaman are active. According to the competitor, Super Trend through Shenzhen mainly supplies the "first price" private label segment. Post-merger this competitor argues that OSRAM would have the incentive to redirect Shenzhen's production to the higher end of the market. This would increase the price in the first price segment and reduce the competitive pressure on the higher segments. Since the prices of the genuine private label as well as the branded segment are following price changes on the "first price" private label segment, the competitor argues, an overall price increase would result from the merger.

34. It should be noted that the Commission's investigation did not find evidence to support the three-level segmentation proposed by the above competitor. In addition, the study submitted by the competitor in support of its claim that the "first price" private label segment influences the price level of other CFL-i was not conclusive as in certain instances the price correlation coefficient was either low or indeed negative. Moreover, it should be stressed - as acknowledged in the study - that correlation does not imply causality.

35. Moreover, the competitor's argument that OSRAM will be in a position to influence the sales behaviour of Shenzhen and cause this company to cease selling product to the "first price" private label segment is based on many speculative assumptions. As already noted above Shenzhen is a separate legal entity, controlled by Mr Yim and a Chinese partner, and will remain active in the manufacturing of CFL-i and via Super Trend their export to the EEA. It must be stressed that the anti-dumping duty rate of 8.4% rests with Shenzhen and that Super Trend, the contractual counterpart of its European customers, is not part of the proposed transaction.

36. Even if one were to assume that OSRAM would be able post merger to influence sales of lamps produced in Shenzhen it may not have the ability to influence the market in the way assumed by the complainant. The likely effect of displacing CFL-i from the "first price" private label segment to other segments would be to increase supply, enhance competition and ultimately lower prices in these other segments. Such a price decrease could be expected to have "knock-on effects" on the "first price" private label segment as well.

37. Finally, if the described strategy of redirecting supply from low-margin to high-margin customers was possibly profitable one could expect to observe such behaviour already absent the merger. Suppliers of branded products would have an incentive to acquire Shenzhen's production currently sold to the "first price" private label and sell it to the higher end of the market. Shenzhen as well as the branded supplier could benefit from such a strategy.

Alternative Suppliers and Capacities

38. In addition to the target, Lisheng is the main supplier of CFL-i to the private label segment. It has been granted an anti-dumping duty of 0% and in addition to its brand Megaman it mainly sells to large retail chains that sell lamps situated rather in the low price segment. One of the complainants confirmed that even the lowest price segment of the private label market would be able to source light bulbs with an anti-dumping duty of ca. 20%, which means that there are at least three companies that would also be able to supply even to this low price segment - Lisheng, City Bright and Sanex. The submissions of the complainant have also shown that higher anti-dumping duties can be sustained in the higher priced segments of the private label market and for branded light bulbs. The market investigation confirmed that several companies like SMPIC, Hilight, Brightstar, Sanex and Yankon supplied CFL-i to the EEA in 2006.

39. The Commission has also looked at the capacity situation of the other suppliers. While the notifying party argued that there exists an estimated overcapacity of 300-400 million CFL-i[11] world-wide, most competitors have indicated that because of the growing demand for CFL-i they operate at full capacity. Several suppliers, including OSRAM, Philips and Lisheng have confirmed during the market investigation that they are in the process of increasing capacities. In addition, the owner of Shenzhen confirmed that the company will add new production capacities during 2007 (which are subject to favourable anti- dumping duties and not covered by the current transaction) [...] coming on stream at the beginning of 2008.[12]

40. Moreover, suppliers indicated that increasing capacity within a reasonable time would be possible as in China a number of producers use manual production methods so only a limited amount of investment is necessary.[13] The Commission therefore has concluded that even if OSRAM were to redirect supplies away from the "first price" private label segment, as alleged by the complainant, alternative suppliers with sufficient capacities would exist who would exert a competitive restraint on the merging parties.

Entry

41. When entering a market is sufficiently easy, a merger is unlikely to pose any significant anti-competitive risk. In the present case the existing anti-dumping measures are currently the crucial barrier to entry for new Chinese producers. In this respect the expected evolution of the market should be taken into account.

42. As noted above, the EU Council of Ministers has recently extended the anti-dumping duties for a period of one year following the conclusion of an expiry review. However, in deciding to prolong the duties until October 2008, the Council indicated that an extension beyond this period was not appropriate as "the likely negative effects on consumers and other operators would be disproportionate to the benefits which Community manufacturers would derive from the measures". Therefore, it appears reasonable based on the information currently available to assume that the duties will not be further prolonged. As there are no other major barriers to entry, Chinese producers currently hindered by the high anti-dumping duties are likely to enter the market when the anti-dumping measures expire. Indeed, the majority of respondents to the market test indicated that the ending of the anti-dumping duties would totally change the market functioning adding supply to the EU market.

Conclusion on horizontal concerns

43. In light of the considerations discussed above, the Commission has come to the conclusion that the merger does not raise horizontal concerns.

Vertical concerns

44. Two competitors who currently source some of their supplies from Super Trend expressed a different type of concern. They fear that the proposed transaction could result in reduced import opportunities assuming that OSRAM would prevent competitors from sourcing high-quality CFL-i from China either by terminating Super Trend's existing contracts or changing product quality, prices or availability to the detriment of competitors.

45. As noted above, Super Trend, which is not covered by the transaction, is the contractual party to the EEA importers. It is speculative to assume that OSRAM would be able to control the commercial behaviour of Super Trend. In any case, even assuming that OSRAM would be able to do so this is unlikely to harm European consumers. According to the market investigation, Super Trend accounts for [45-55]% of the (outsourced) supplies (in volume) to the main OEMs (GE, OSRAM, Philips and Sylvania). However, its share of total EEA-supplies to all customers is only [15-25]%. OSRAM's ability to raise its rivals' costs is thus limited by the merged firm's relatively low share of upstream production ([25-35]%), which limits its ability to affect prices to any significant extent. Furthermore it should be noted that the other OEMs also have their own in-house production, which would prevent them from being marginalised or excluded from the downstream market.

46. At the same time, OSRAM's incentive to sacrifice profits upstream (by restricting Super Trend's supplies to rival OEMs, thereby raising their costs and diverting sales to its own downstream unit) appears low in view of its low market share downstream, which would not increase and which amounts to only [15-25]% post-merger. Hence, in view of the merged entity's limited combined market share both at the upstream production level and at the retail level, the transaction does not raise serious doubts that consumers will be harmed as a result of a possible input foreclosure strategy by OSRAM.

47. In addition to the elements mentioned above, it should be considered that Mr Yim, the owner of Super Trend, has already invested in additional production capacity [...] in Shenzhen which will come on stream in early 2008. These assets are not subject to the transaction. Given Shenzhen's favourable anti-dumping duty Mr Yim has an economic interest not only to fulfil current supply contracts, but also to seek new customers within the EEA as long as the anti-dumping measures grant his company a competitive advantage.

48. Therefore in view of the above considerations, the Commission has concluded that the risk of foreclosure is not likely by the proposed transaction.

VI. CONCLUSION

49. For the above reasons, the Commission has decided not to oppose the notified operation and to declare it compatible with the common market and with the EEA Agreement. This decision is adopted in application of Article 6(l)(b) of Council Regulation (EC) No 139/2004.

[1] OIL 24, 29.1.2004, p. 1.

[2] Austria, Bulgaria, Cyprus, Genuany, Latvia, Malta, Portugal, Slovakia, Slovenia and Spain.

3 Super Trend also sells halogen lamps but this activity will not be transferred to Sunny World.

4 The general purpose lighting market excludes lamp products designed specifically for outdoor use, such

as street and railway lighting and floodlights, It also excludes lamps for special applications such as

vehicle lights and sun tanning lights.

[5] Case IV/M.258-CCIE/GTE, para. 15 and COMP/M.4509-Philips/PLI.

[6] Case IV/M.258-CCIE/GTE, paras. 17-20 and COMP/M.4509-Philips/PLI, paras. 12-13.

[8] See Commission Regulation (EC) No 255/2001, OJ L 38, 8.2.2001, p. 8.

[9] See Council Regulation (EC) No 1205/2007, OJ L 272, 17.10.2007, p. 1.

[10] These suppliers are: Changzhou Hailong, Sanex, City Bright Lighting, Deluxe Well, Zhejiang Sunlight.

[11] [...], Sylvania [...] and OSRAM [...] pieces in 2006 (Source Form CO).

[12] To distinguish between production and supplies, supplies will be called the "retail level". Strictly speaking all the producers are not active at the retail level, instead they are selling their production to retail chains like IKEA, Tesco, Carrefour, Aldi, Lidl etc..

[13] See Form CO page 47.

[14] See statement of Mr Yim submitted to the European Commission dated 15.10.2007.

[15] In this respect it should also be noted that the recent anti-dumping decision (Council Regulation (EC) No 1205/2007, OJ L 272, 17.10.2007, p. 13) found that "capacity of Chinese exporters is significant and can be easily increased".