EC, June 26, 2008, No M.5162

COMMISSION OF THE EUROPEAN COMMUNITIES

Judgment

Avnet/ Horizon Technology

Dear Sir/Madam,

Subject: Case No COMP/M.5162 - Avnet/ Horizon Technology

Notification of 26/05/2008 pursuant to Article 4 of Council Regulation No 139/20041

1. On 26/05/2008, the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which the undertaking Avnet Inc. ("Avnet", USA) acquires within the meaning of Article 3(1)(b) of the Council Regulation control of the whole of Horizon Technology Group plc ("Horizon", Ireland ), by way of purchase of shares.

I. THE PARTIES

2. Avnet is a distributor of electronic components, computer products and technology services based in the USA and operating world-wide. Through Electronics Marketing ("EM"), Avnet distributes a wide range of electronic components (semiconductors, interconnect devices, etc.) to contract electronic manufacturers (CEM) and original equipment manufacturers (OEM); through Technology Solutions ("TS"), Avnet supplies as a distributor technology products, services and solutions for value-added resellers ("VARs"), system builders or integrators, OEM and end-user businesses. Avnet is active worldwide and in almost all EEA States.

3. Horizon is a technical integrator and distributor of IT products in the United Kingdom and Ireland.

II. THE OPERATION

4. Avnet announced a public offer on 18 April 2008 to acquire the entire issued and to be issued share capital of Horizon. The public offer by Avnet has the support of the board of directors of both Avnet and Horizon.

III. CONCENTRATION

5. The operation therefore constitutes a concentration within the meaning of article 3(1)(b) of the EC Merger Regulation

IV. COMMUNITY DIMENSION

6. The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 billion (Avnet: EUR 12.012 billion; Horizon: EUR 288.213 million). The aggregate Community-wide turnover of each of at least two of the undertakings concerned is more than EUR 250 million (Avnet: EUR […]; Horizon: EUR […]) for 2007. Only […] achieves more than two thirds of its Community wide turnover in one Member State (United Kingdom). The notified transaction therefore has a Community dimension within the meaning of article 1(2) of the EC Merger Regulation.

V. RELEVANT MARKETS

V.1. Product market

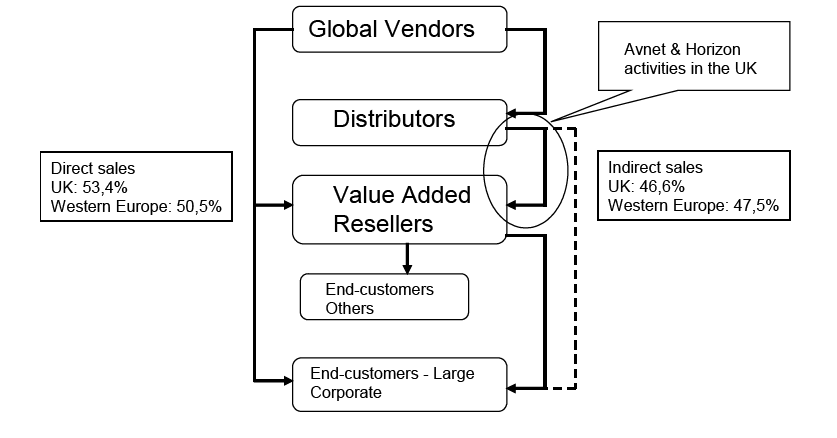

7. Both Avnet and Horizon are wholesale distributors of IT products and services. The wholesale distribution consists in the supply of a broad range of IT products purchased from different IT manufacturers, also called vendors (e.g.: IBM, SUN Microsystems ("SUN")) to a number of re-sellers. The range of products concerned includes personal computers (PCs), servers, printers, routers, storage devices and others. Distributors and resellers can be qualified as "value added distributors" (VADs) or "value added resellers" (VARs) when they provide to their customers also certain services such as consulting support, logistic services, financial solutions, etc. As noted in previous Commission decisions2, distributors essentially provide their customers with a "one stop shop" facility.

8. As noted in a previous decision3, on the one hand vendors can bypass the distributors and supply large corporate accounts and VARs directly (direct sales); on the other hand, the largest VARs also compete directly with distributors for sales to large corporate accounts.

9. Avnet and Horizon act as intermediaries between vendors of IT products and VARs. They do not realise direct sales to large corporate in the United Kingdom (only affected market). If compared with vendors, distributors sell IT products from multiple sources, and can serve clients that are too small to be considered by vendors. VARs sell IT products and services to end-customers. Sales by distributors and VARs are considered indirect sales.

Direct and indirect sales

10. The notifying party submits that the market of direct sales of IT products and services and the market for indirect sales of IT products and services would be distinct although they would exert competitive constraints on each other. Direct sales of IT products and services account for 53.4%4 of the total sales of IT products and services in the United Kingdom. The notifying party submitted that direct and indirect sales present different characteristics as distributors notably have (i) a broad product offering, (ii) fast delivery systems, and (iii) logistic capabilities.

11. The notifying party notably submitted for the top 10 clients of Avnet and Horizon whether they purchased servers from distributors or from vendors directly (with regard to […] and […], who constitute together [90-100%] of supplies of servers to Avnet and Horizon). All Horizon customers purchase [90-100%] of their […] or […] servers from distributors. One Avnet customer purchases its […] servers directly from […], whereas all Avnet customers purchase […] servers from distributors only. This applies to the largest customers of Avnet and Horizon, and it is likely that smaller customers also buy their servers from distributors and are not served directly by vendors. Such data is therefore indicative that vendors and distributors tend to work on the basis of a clear separation of customers they respectively serve, at least for servers.

12. In TechData/Scribona5, the Commission left open whether direct and indirect sales should belong to the same market, although it recognised that prices in the indirect sales channel are significantly constrained by prices in the direct sales channel. In Arrow Electronics/ Logix6 the Commission also left open this question, although it recognised that direct and indirect sales channels were not fully interchangeable for resellers and retailers active in Denmark.

IT products categories

13. The notifying party also submitted that the relevant product market should be the distribution of all IT products and services, and should not be delineated along different IT products' categories (ex: storage capacity, servers, etc.) or along a narrower segmentation (ex: low-end servers, medium-range servers or high-end servers). It notably submitted that such a narrow segmentation could be appropriate at the manufacturing level, but not at the distribution level, principally because it is the business model of distributors to supply their customers with all kinds of IT products.

14. In TechData/Scribona and Arrow Electronics/ Logix the Commission came to the conclusion that conditions of supply in the indirect sales channel are globally homogeneous across all categories of IT products, but that nevertheless some distributors specialise in certain categories of products. Ultimately, in both cases the Commission left open whether the relevant market should include all IT products or whether distinct markets should be defined on the basis of each IT product category.

Conclusion

15. For the purpose of this decision, the exact market delineation can ultimately be left open, since under all possible alternative definition the proposed transaction does not raise competition concerns.

V.2. Geographic market

16. The notifying party submitted that the distribution of IT products and services has historically been national in focus, but that distribution is increasingly carried out beyond the national scope. There are no technical barriers to the use of IT products in different Member States, no material price differences and vendors in particular tend to distribute direct sales to multinational companies on a Europe-wide basis. Conversely, it could be argued that sales of distributors are achieved via local sales offices.

17. In TechData/Scribona and Arrow Electronics/ Logix, the Commission concluded that a number of elements (language, local presence) constituted indications that the relevant market could be national in scope. However the exact geographic market definition was left open.

18. For the purpose of the present decision, the exact market definition (national, regional or EEA-wide) can be left open as the proposed transaction does not raise competition concerns under any possible definition of the geographic market.

VI. COMPETITVE ASSESSMENT

19. Horizon is active in Ireland and in the United Kingdom only, whereas Avnet is active worldwide, but its activity in Ireland is not related to the relevant market. The merging parties' activities' overlap is therefore limited to the United Kingdom.

20. On a hypothetical EEA-wide market for the distribution of IT products, the combined market share of Avnet and Horizon would not exceed 5%, irrespective of whether direct sales were to be included or not. In view of this insignificant market position, the transaction is unlikely to raise competition concerns at the EEA level, either in the overall market for the distribution of IT products or in any individual product segments of this market.7

21. When considering the market for indirect sales of all IT products and services in the United Kingdom, the aggregate market share of Avnet and Horizon would be [0-5%]8.

22. When considering the different product categories of IT products in the United Kingdom, and on the basis that direct and indirect sales constitute different markets, the only affected markets would be (a) indirect sales of servers, (b) indirect sales of high- end servers, and (c) indirect sales of mid-range servers.

Avnet and Horizon market shares by product category, via indirect sales (%) United Kingdom – 2007 | |||

| Avnet | Horizon | Combined |

Servers (3 categories) | [10-15%] | [5-10%] | [15-20%] |

· High-end servers | [15-20%] | [0-5%] | [15-20%] |

· Mid-range servers | [15-20%] | [10-15%] | [25-30%] |

· Low-end servers | [5-10%] | [0-5%] | [10-15%] |

Source: notifying parties, IDC

23. In the market for the distribution of servers in the United Kingdom, or in the market for the distribution of high-end servers in the United Kingdom, the market share of the merged entity would be [15-20%], and would not be deemed to give rise to competition concerns.

24. In the market for the distribution of mid-range servers, the combined entity's market share would be [25-30%]. With such a market share the new entity would be the largest player. Its competitors are OpenPSL (10-20%), Intertechnology/DNS (5-10%), Tech Data (5-10%), ISI Interface Solutions (0-5%) and Westcoast (5-10%), followed by a number of smaller distributors with market shares below 10%9. The market is therefore characterised by the presence of a number of companies having limited market shares. These companies nevertheless exert competitive constraints on the market and VARs will continue to have alternative sources of supply for IT products and services.

25. It can be noted that only […] and […] supply Avnet and Horizon with mid-range servers. On the basis of the information provided by the notifying party, […] and […] distribute all categories of servers also through several other distributors in the United Kingdom. Would Avnet/Horizon decide to substantially increase its prices (via an increase of its margin) for […] and […] servers, […] and […] could easily strengthen their business relationships with other distributors10, which could ultimately affect sales of Avnet/Horizon (for instance […] and […] could increase their prices to Avnet/Horizon or give priority to other distributors for new products).

26. In general, direct sales by large IT manufacturers (vendors) account for 45.3%11 of total sales of mid-range servers in the United Kingdom. As noted above, these manufacturers exert a competitive constraint on distributors. In the case Avnet/Horizon would increase its prices for mid-range servers, a proportion of clients that are not currently served by vendors directly could become a profitable target for these vendors.

27. Ultimately, it can also be argued that the market for the distribution of mid-range servers is also constrained by the markets for the distribution of low-end or high-end servers. The frontier between the different markets for servers is indeed changing very rapidly. It is reasonable to assume that the best servers that are available in the low-end category are comparable to the most basic servers available in the mid-range category, and that the same product can fall in the lower segment within a short time frame. For instance, in 2001, IDC defined the mid-range servers as those servers whose price was between 100 000 US$ and 1 000 000 US$. In 2006, IDC defined mid-range servers as priced between 25 000 US$ and 500 000 US$.

28. In view of the above, it can therefore be concluded that the transaction is unlikely to lead to significant impediment of effective competition on any of the alternative product markets in the EEA, or in the United Kingdom.

VII. CONCLUSION

29. For the above reasons, the Commission has decided not to oppose the notified operation and to declare it compatible with the common market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of Council Regulation (EC) No 139/2004.

1 OJ L 24, 29.1.2004 p. 1.

2 See Case No COMP/M.4868. Avnet/ Magirus EID and case COMP/M. 5091 Tech Data/ Scribona.

3 See Case No COMP/M.4868. Avnet/ Magirus EID.

4 Source: IDC Report, May 2006.

5 Case COMP/M. 5091 Tech Data/ Scribona

6 Case COMP/M. 5099 Arrow Electronics/ Logix

7 Source: IDC report 2006, forecast for the year 2007.

8 Source: IDC report 2006.

9 Source: notifying party’s estimate.

10 The notifying party provided information regarding their contracts with the vendors, which are non- exclusive, have liimted duration i.e. annual, and leave the vendors the possibility to appoint as many distributors as they deem necessary.

11 IDC Report 2006, projection for the year 2007.