Commission, March 30, 2011, No M.6124

EUROPEAN COMMISSION

Judgment

SAFRAN / SNPE MATERIAUX ENERGETIQUES / REGULUS

Dear Sir/Madam,

Subject: Case No COMP/M.6104 - SAFRAN / SNPE MATERIAUX ENERGETIQUES / REGULUS

Notification of 23/02/2011 pursuant to Article 4 of Council Regulation No 139/20041

1. On 23 February 2011 the European Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which the undertaking SAFRAN acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of SNPE Matériaux Energétiques ("SME", France) and joint control of REGULUS ("Regulus", France; Regulus and SME are hereinafter referred to together as "the Target"), by way of purchase of shares.

I. THE PARTIES

2. SAFRAN is active mainly in aerospace propulsion, aircraft equipment, defence and security, the three main branches of the group. A number of undertakings exclusively or jointly controlled by SAFRAN are active on the markets concerned by the proposed transaction. These are: Snecma Propulsion Solide (SPS), a wholly owned subsidiary active in solid propulsion and thermostructural composite materials; Europropulsion, a 50/50 joint-venture between SPS and the Italian company AVIO supplying integrated solid rocket motors for space launchers; G2P, an Economic Interest Group in charge of the propulsion of France's fleet of ballistic missiles in which SAFRAN, through its subsidiary SPS holds 75% share, the other 25% being owned by SME. SAFRAN also controls other undertakings which are active on connected or vertically linked markets, as clients or suppliers: Microturbo, a subsidiary specialized in tactical propulsion and turbojet engines for military applications; Aircelle, a subsidiary supplying commercial airplane engine nacelles, thrust reversers, aerostructures and associated services.

3. SME is a wholly-owned subsidiary of SNPE, a French state-owned company. It designs, develops and produces propelling charges and energetic equipment for the defence, aeronautical, space and automotive industries, propellants for military use, as well as composite materials and strategic energetic raw materials related to these applications. These activities are performed directly by SME and through its subsidiaries (i) PyroAlliance which supplies pyrotechnic equipment for the space, defence, aeronautical and industrial sectors, (ii) Structil which is active in high-performance composite materials and intermediate products for the manufacture of technical parts for aeronautics, defence, as well as sports and leisure activities and (iii) Roxel, a 50/50 joint venture between SME and MBDA active in tactical propulsion.

4. Regulus is a French company jointly controlled by AVIO (60%) and SNPE (40%), which operates the solid propellant plant in Guiana where the main segments of the Ariane 5 Solid rocket Motors receive their propellant.

II. THE OPERATION AND CONCENTRATION

5. The proposed transaction consists of the acquisition by SAFRAN of all of the activities of SNPE in the field of solid propulsion and energetic materials.2 Pursuant to the terms of the Financial, Commercial and Industrial Cooperation Agreement and of the Share and Purchase Agreement concluded between SAFRAN and SNPE on 14 February 2011, the transfer of this single business to SAFRAN will take place through the following legal transactions which are interdependent: (i) the acquisition by SAFRAN of 100% of the share capital of SME, which itself owns 50% of the share capital of Roxel, 80.05% of the share capital of Structil, 85% of the share capital of PyroAlliance, and 25% of the Economic Interest Group G2P and (ii) the acquisition by SAFRAN of 40% of the share capital of Regulus currently owned by SNPE.

6. The proposed operation falls within the scope of recital 45 of the Commission's Jurisdiction Notice under Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings3 (hereinafter "the JN").

7. First, the two transactions concern a single economic entity to be managed for common commercial purpose: one same purchaser, SAFRAN, is acquiring control of all of SNPE's solid propulsion activities, comprising a 100% controlling stake in SME and a jointly controlling stake in Regulus.

8. This is confirmed by the Cooperation Agreement signed by the Parties in parallel to the SPA: Regulus is in the perimeter of the solid propulsion business of SNPE. It is in charge of filling the boosters of the Ariane and Vega rockets […]. There is thus a clear economic link between the two parts of SNPE's solid propulsion business.

9. In addition, the acquisitions of the majority and the minority stakes by SAFRAN are interdependent both (i) from an economic point of view as they serve a common purpose, i.e. combining the activities of the parties with regard to solid propulsion and (ii) on a de jure basis as they are subject to the same Share and Purchase Agreement (SPA) and one cannot take place without the other.

10. Therefore, the two transactions constitute one concentration in the form of the acquisition by SAFRAN of a single business constituted by SME and Regulus within the meaning of Article 3 of the Merger Regulation.

III. EU DIMENSION

11. The concentration has EU dimension. The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million5 (SAFRAN: EUR 10 448 million, Target: EUR […]6, AVIO: EUR 1 702 million). SAFRAN and the Target each have an EU wide turnover in excess of EUR 250 million (SAFRAN: EUR […], Target: EUR […]7). Although the Target achieves more than two-thirds of its aggregate EU-wide turnover in one Member State (France), SAFRAN does not. The notified operation therefore has an EU dimension.

IV. OVERVIEW OF THE INDUSTRY

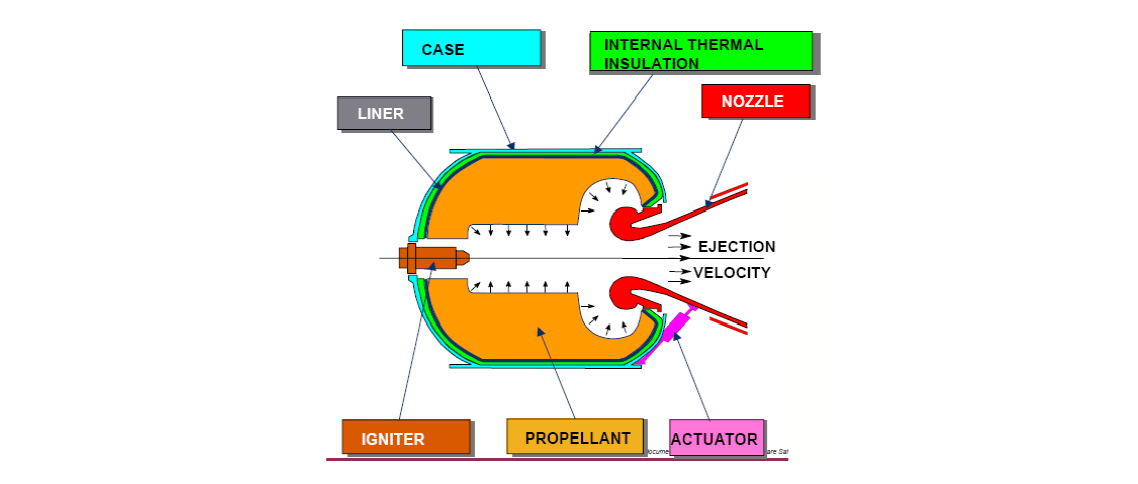

12. The transaction concerns mainly solid propulsion for space launchers, strategic missiles and tactical missiles. Aerospace propulsion and missile propulsion are achieved through rockets. A rocket motor provides the propulsion for the rocket, i.e. it generates the thrust that propels it forwards. The basic principle of operation of a rocket motor is that of action and reaction: the rocket moves forwards because gases (or, more generally, products of combustion) are ejected backwards. Solid propellant propulsion is routinely used to power strategic and tactical missiles and is now the established technology for boosters of heavy space launchers and the main propulsion unit for small launchers. In solid rocket motors ("SRMs"), all the reactive elements – notably Ammonium Perchlorate – that constitute the propellant are pre-mixed in a binder and stored in solid form inside the combustion chamber itself. The components of an SRM are presented graphically in Figure 1.

Figure 1: Components of a solid rocket motor

Source: Presentation of the Parties to the case team on 2 February 2010

13. In the space sector, the Parties are active on two current European Space Agency programmes: Ariane 5 and Vega. These are multilaterally funded programmes where suppliers are selected at the development stage mainly on the basis of their expertise and of a "juste retour" principle for all national industries at a European level, which reflects each Member State's financial participation in the programme.

14. In the Ariane Programme, the Parties to the transaction have complementary activities that are coordinated by the prime contractor of the rocket, Astrium Space. SAFRAN is active with an Italian company AVIO in a joint venture known as Europropulsion. Europropulsion is the prime contractor for the SRM. It is in charge of performing the final assembly of the motor. It also produces the nozzle and elastomeric thermal insulations material. SME provides the raw materials for the propellant, which is manufactured by AVIO. AVIO is also in charge of the igniters. Through Regulus, a joint venture with AVIO, SME casts the propellant for Ariane 5's SRMs.

15. Regarding the Vega launcher, AVIO is the prime contractor of the SRMs for the second and third stages of the rocket8, while Europropulsion is prime contractor for the first stage. The roles of SME and Regulus are the same as on Ariane.

16. Strategic missiles are dedicated to critical State defence application. They typically have long range and great destructive capabilities relying on nuclear warheads. SAFRAN is only active in the M51 programme, a missile for the French nuclear deterrence force produced under the supervision of the French authorities (Direction Générale de l'Armement). SAFRAN and SME are partners in this field and joint prime contractors for the propulsion system through the economic interest group G2P. SME produces the propellant charge and the liner, while SAFRAN manufactures the combustion chamber and the nozzle.

17. As opposed to strategic missiles, tactical missiles are used for more geographically limited actions and typically carry a conventional high explosive warhead. Tactical missile propulsion includes four sub-segments: SRMs, solid ramjets, turbojets engines and liquid ramjets. The downstream markets are mainly the markets for guided weapons and guided weapons systems.

18. SAFRAN produces SRMs for tactical missiles through its subsidiary SPS and turbojet engines through its subsidiary Microturbo. SME is active through Roxel (a joint venture with MBDA) in the manufacture of SRMs for tactical missiles as well. It also supplies SRMs and propellant charges to manufacturers of unguided rockets9. In addition, Roxel supplies SRMs to Sagem Défense Sécurité ("Sagem"), a subsidiary of the SAFRAN group for modular armaments (also called hybrid weapons or precision bombs). Modular armaments are air-to-ground precision guided ammunitions based on the assembly of a guidance kit (attached at the front of the bomb body), a range-extension kit (attached to the rear of the bomb body), and an aerodynamic unit. The range-extension kit is made of an SRM of the same type as SRMs used for tactical propulsion10.

19. There are a number of markets vertically related to solid propulsion, including (i) pyrotechnic equipment such as initiators, transmission and cutting detonating cords, pyromechanisms, (ii) propellant charges, (iii) inputs for propellant charges and (iv) composite materials.

20. The European defence and space industries have undergone a process of consolidation in the last ten years with the aim of 'establishing a level playing field between European and US companies.11 In 2000, EADS (formed by the merger of DaimlerChrysler Aerospace AG, Aérospatiale-Matra and Construcciones Aeronáuticas SA) and Astrium (a joint EADS/BAE Systems venture) were created12. In 2001, MBDA was founded as a joint venture between BAE Systems, EADS and Finmeccanica. Roxel was formed in 2002 by the merger of Celerg of France and Royal Ordnance Rocket Motors of the UK in the context of the creation of a JV between SNPE and MBDA.13 It acquired Protac (a French company active in solid propulsion) in 200814. In 2007, MBDA acquired Bayern-Chemie, a German company active in solid propulsion.15 SAFRAN itself was created in 2005 by the merger of Snecma and Sagem16.

V. COMPETITIVE ASSESSMENT

A. Horizontal overlaps

1. Space propulsion

21. The Parties submit that there is no open market for SRMs for space propulsion as the Ariane and VEGA programmes – which are the only ones in which SME and SAFRAN are active – are developed through multilateral government funded programmes where the selection of suppliers is based on a "juste retour" principle for various national industries. In addition, once a supplier is qualified, a change of this supplier is very expensive as it requires a new qualification process.

22. In past cases regarding the space sector, the Commission has left open whether markets for certain subsystems (such as SRMs) procured through bidding procedures at European level should be defined17.

23. The market investigation has confirmed that the selection of suppliers for the Ariane and VEGA programmes is based on the "juste retour" principle for various national industries18 and that, once a supplier has been selected, it is very difficult to switch supplier as this would entail a long and costly requalification process. However, the product and geographic market definitions may be left open in this case since it does not affect the competitive assessment.

24. The Parties submit that the transaction will not lead to horizontal issues as SAFRAN and SME are complementary in their involvement in the Ariane and Vega programmes, which are the only space programmes in which they are active. In addition, SRMs for space propulsion such as the Ariane and VEGA programmes are and will continue to be developed through multilateral government funded programmes where the selection of suppliers is based on a "juste retour" principle for various national industries. Therefore, the transaction does not change the prevailing situation in the view of the Parties.

25. The market investigation has confirmed the submission of the Parties. In one respondent's view, there is no critical size to feed competition as only 12-14 boosters are produced each year19. Due to the difficulties associated with a potential requalification and to the "juste retour" principle, it does not make sense from its point of view to switch supplier for the boosters20. Moreover, the allocation of tasks between Italian and French industries concerning solid propulsion will not be affected by the transaction (as SAFRAN and SME are both French). Finally, several respondents to the market investigation indicated that the transaction could create synergies and decrease costs21.

26. Therefore, the transaction is unlikely to raise competition concerns in relation to SRMs for space propulsion.

2. Defence propulsion

27. The Commission has taken the view in previous decisions that a distinction should be made between propulsion systems for tactical missiles and propulsion systems for strategic missiles22. The market investigation has confirmed that due to technical differences, relating to size, performance and the duration of burn of the propulsion system, there is no possible substitution from the demand-side between the two. In addition, propulsion systems for strategic ballistic missiles are manufactured in dedicated facilities for technical and national security reasons23

27.1. Strategic missile propulsion

28. Each state controls the manufacturing of deterrence missiles and no international market exists. The Parties are active only on the market for the French M51 Programme. Therefore, only France is affected. In any case, the exact market definition can be left open since it does not affect the competitive assessment, even under the narrowest market definition.

29. The Parties submit that the transaction does not raise horizontal issues with regard to strategic missile propulsion for the following reasons: (i) SAFRAN and SME are already partners and jointly prime contractors through the Economic Interest Group G2P; (ii) SAFRAN and SME are and may be involved only in the French deterrence programme (M51) as Ministries of Defence ("MoDs") rely on their domestic industry for strategic missiles propulsion in order to remain autonomous from foreign suppliers; (iii) SAFRAN's and SME's involvement in the French M51 is complementary: SAFRAN is in charge of the combustion chamber and the nozzle while SME supplies the propellant charge and the liner; (iv) SAFRAN and SME cannot be qualified as potential competitors in this market: SAFRAN is not present at all in the sector of propellant charges and the associated raw materials, and SME does not have the capacity to manufacture combustion chambers or thermostructural composite materials used for nozzles.

30. The transaction will therefore not change the existing situation. In addition, the French Ministry of Defence, which is the final customer of the M51 programme, has indicated that it believes that the transaction will have positive effects in relation to strategic missiles propulsion24. Moreover, none of the respondents in the market investigation have raised concerns in relation to strategic missile propulsion.

31. Therefore, the transaction is unlikely to raise competition concerns in relation to strategic missile propulsion.

2.2. Tactical missiles propulsion

2.2.1. Product market definition

Distinction according to technology

32. Different technologies can be used in propulsion systems for tactical missiles: SRMs, ramjets (liquid and solid) and turbo-propulsion. New technologies such as hybrid rocket engines, gel propellant technology and pulse detonation engines remain in the early stages of development25. Whereas both Parties are active in SRMs, only Roxel is active on the market for solid ramjets and only SAFRAN, through its subsidiary Microturbo, is active on the market for turbojets engines.

33. In light of supply-side and demand-side differences, the Parties submit that there are separate markets for SRMs, solid ramjets and turbo-propulsion.

34. The Commission has previously held that there is a separate market for the supply of SRMs but left open the question as to whether the relevant market should include ramjets26 and other technologies.

35. The market investigations has indicated that SRMs and ramjets are not substitutable from both a technical and economic point of view as ramjets are more expensive than SRMs and provide a longer range and higher velocity. SRMs are usually used for short and medium range subsonic missiles (up to 100km) whereas ramjets are used for large, supersonic, long range missiles (more than 100km)27.

Distinction within SRMs

36. As can be seen from Figure 1, a Solid Rocket Motor consists of the following components: (i) a propellant charge28; (ii) an igniter, (iii) a motor case, (iv) possibly a blast pipe, (v) a nozzle, and (vi) insulation. Although not necessarily directly connected with the rocket motor itself, some other devices may also be combined with such propulsion systems to improve the overall capability of tactical weapons or missiles. These components include(i) complex pyrotechnic devices, (ii) gas generators and gas generator sub-systems and (iii) thrusters.

37. In previous cases, the Commission held that it is not necessary to define separate markets for each SRM component as these are not sold on a stand-alone basis, although it noted that the production of propellant charges could, due to demand-side considerations, be considered as a market upstream of SRMs29. The market investigation in the present case has confirmed that SRM components, with the exception of the propellant charges, are not sold on a stand-alone basis to missile manufacturers30. However, some respondents in the market investigation have indicated that SRM components such as pyrotechnical devices, casings, nozzles and insulations may be sold on a stand-alone basis for various applications including SRMs31. However, apart from propellant charges and pyrotechnic equipment which are addressed separately in this decision, the exact market definition for other SRM components can be left open as no affected market arises in relation to these other SRM components32.

38. In the case SNPE/MBDA/JV, the Commission found that it is not necessary to apply a further segmentation of the SRMs market according to the tactical military device’s application (including the different types of tactical missiles and unguided rockets) since the basic technology is applied regardless of the final use of the rocket and there is therefore a high degree of supply-side substitutability33. This has been confirmed by the market investigation in the present case34. The market investigation has also shown that there are no substantial economic or technical differences between SRMs for range extension kits for modular armaments and SRMs for tactical missiles35.

39. For the purpose of this decision, it is therefore considered that SRMs for tactical missiles and range extension kits for modular armaments are part of one relevant product market.

2.2.2. Geographic market definition

40. In the case MBDA/Bayern/Chemie, the Commission pointed to a strong national dimension of the markets for SRMs where a domestic supplier exists in spite of a trend towards internationalisation36. Moreover, the Commission has considered in previous cases that military markets are world markets for countries where there are no domestic suppliers37.

41. The Parties submit that the geographic market for SRMs is at least EEA-wide and probably also includes the USA as well as the other countries of the "free world" (i.e. of North America, Latin-America, Australia and South-Africa). They point to a trend towards internationalisation of the market for SRMs (at least at the European level, and possibly including the US and other countries of the "free world"), driven by the consolidation of the industry, the 2009 European Directive38 and international cooperation programmes.

42. The market investigation has indicated that the geographic scope of the SRM market for countries that do not have an SRM supplier is at least EEA-wide39. Some respondents indicated that certain European customers usually have a preference to buy from European SRM suppliers40 as sourcing parts such as SRMs from US suppliers could limit the export potential of weapons incorporating such parts under the US ITAR regulations41. The turnover achieved by non-European companies, i.e. by US companies (Aerojet and ATK), in the EEA is in fact generated through sales of US propulsion systems for use in US guided weapons and guided weapons systems sold in the EEA42. However, a number of respondents indicate that countries not having SRM capabilities look for worldwide competition.

43. On the other hand, there are indications that the geographic scope of the SRM market is national for countries that have an SRM supplier, as the choice of national suppliers is often supported by the national MoD administration, in some cases in order to maintain a domestic competence for strategic or industrial policy reasons. In addition, MoDs often request offsets for their domestic industry43. Finally, some market players such as SPS are only active in one country.

44. However, the geographic market definition can be left open for the purpose of this decision as it does not affect the competitive assessment, even under the narrowest market definition.

2.2.3. Competitive assessment

45. The Parties' market shares estimates in relation to SRMs for tactical missiles are presented in Table 1. These figures have been broadly confirmed by the market investigation44.

Table 1: Market shares of the Parties and their main competitors in respect of SRMs for tactical missile

| Roxel | SPS | AVIO | Nammo - Raufoss | Aerojet | ATK | 45 Others |

World | [20-30]% | [0-5]% | [0-5]% | [0-5]% | [20-30]% | [20-30]% | [20-30]% |

EEA | [50-60]% | [5-10]% | [10-20]% | [10-20]% | [0-5]% | [0-5]% | [0-5]% |

France | [60-70]% | [10-20]% | [0-5]% | [5-10]% | [0-5]% | [0-5]% | [0-5]% |

Germany | [10-20]% | [0-5]% | [0-5]% | [30-40]% | [10-20]% | [10-20]% | [10-20]% |

Italy | [10-20]% | [0-5]% | [40-50]% | [0-5]% | [0-5]% | [0-5]% | [10-20]% |

UK | [70-80]% | [0-5]% | [0-5]% | [5-10]% | [0-5]% | [0-5]% | [5-10]% |

Other EEA Countries | [10-20]% | [0-5]% | [0-5]% | [30-40]% | [10-20]% | [10-20]% | [10-20]% |

Source: best estimates of the Parties

46. Despite SPS and Roxel's high combined market shares in France and at the EEA level, the Parties submit that this overlap will not lead to competition concerns for the following reasons: (i) Roxel is jointly controlled by MBDA (the most important customer of SRMs for tactical missiles in Europe, active in the market for guided weapons and guided weapons systems) and therefore SAFRAN will not be able to determine Roxel's strategy and commercial policy alone; (ii) significant competitors exist at the EEA/global level (Nammo-Raufoss – whose market share is growing 46 –, Aerojet, ATK); (iii) SAFRAN is only providing SRMs for two French programmes (Mistral and MDCN) and is therefore a niche player; (iv) SAFRAN and Roxel have never been the only bidders in the past 10 years and SAFRAN only bid once against Roxel47; (v) new entrants (MKEK and Roketsan from Turkey, Rafael Manor from Israel and Somchen from South Africa) will participate in bids in the next 10 years; (vi) most GW/GWS manufacturers have in-house capacities to manufacture SRMs; (vii) MoDs retain sufficient buyer power (ability to source from many suppliers, monitoring of development and quality), as was evidenced in previous cases (e.g. in Matra BAe Dynamics/DASA/LFK48, Saab/Celsius49, EADS50 and, more recently, in General Dynamics/Alvis51), and they apply the "best value for money" principle; (viii) high market shares are the result from the qualification process and very long product life- cycles (15-20 years) which make supplier's switching costly; (ix) national security considerations may influence the choice of supplier for the defence department.

47. The market investigation has confirmed the Parties' submission that the qualification process is costly and that contracts with customers are long term contracts which make supplier's switching difficult.52 In addition, MoDs retain a decisive influence on the choice of suppliers.53

48. In France, […], the French MoD indicated that it was not concerned about the competitive impact of the transaction on the market for SRM for tactical missiles54. The French MoD also emphasized that it would retain sufficient countervailing buyer power as it has a right to make sure that there is sufficient competition for the components of tactical missiles such as SRMs. This was also confirmed by the market investigation55. In addition, one customer considers that it will retain sufficient buyer power to ensure that the merger will not lead to price increases but will deliver efficiency gains. Such efficiency gains are in its interests as it is under pressure from the French MoD to decrease costs all along the value chain56.

49. SPS was not active in […]. In any event, the market investigation indicated that missile manufacturers systematically invite several suppliers to bid regarding SRMs57 and that a number of credible alternatives exist in the EEA, namely NAMMO, AVIO, Bayern- Chemie and Chemring. Finally, despite certain barriers to entry in the EEA related to capital investment, licensing and qualification costs, a number of potential entrants exist and will replace the limited potential competitive pressure exercised previously by SPS according to one of the most important customers of SRMs for tactical missiles in the EEA58. For instance, the Turkish company Roketsan has already participated in bids organised by two European missile manufacturers (including one successfully)59.

50. Only one customer raised concerns with regard to the market for SRMs for tactical propulsion60. However, these concerns were not related to the proposed concentration, but rather to expected future further reorganization and consolidation of the industry.

51. One competitor also explained that the concentration would make it harder to win bids in the EEA, especially with regard to MBDA61. However, MBDA already has joint control over Roxel before the transaction and does not buy exclusively from Roxel. MBDA confirmed that the transaction will not change its purchasing strategy to procure from other suppliers than Roxel and SPS in order to benefit from their technologies and to apply the 'best value for money' principle62.

52. Therefore, the transaction is unlikely to raise competition concerns on the market for SRMs for tactical missiles and modular armaments.

3. Pyrotechnic equipment

53. Pyrotechnic equipment consists of products performing various functions and using the energy provided by exothermic chemical reactions. In the present case, the pyrotechnic equipment and/or systems manufactured by the Parties include initiators, transmission and cutting detonating cords, pyromechanisms and pyrotechnic equipment for the defence market (mainly missiles), for the space market (mainly launchers) and for the aircraft market (aircraft and helicopters).

3.1. Product market definition

54. The Parties submit that a segmentation by final use sector distinguishing between defence and space applications on the one hand and aeronautical and other industrial applications on the other hand could be established from a demand side point of view since both defence and space applications require specific expertise and qualification procedures for pyrotechnic equipment which is not necessarily the case with aeronautical and other industrial applications. However the Parties also note that on the supply side, most of the players are able to offer and supply a wide range of pyrotechnic components and devices and are able to start the production of a new component or device within a short time frame (less than two years) and without significant costs. As a result, the Parties claim that there is supply-side substitutability on this market and that is not necessary to apply a further segmentation.

55. The market investigation has generally confirmed that pyrotechnic equipment products can be distinguished according to their field of application (defence; space; aeronautical and other industrial applications)63. Indeed, several manufacturers of pyrotechnic equipment are not active in all of these segments. In addition, the defence and space markets are characterized by specific designs for each rocket motor and require high quality standards, special safety characteristics and qualifications. They are produced in low volumes. The aeronautical and other industrial sectors (especially the automotive market) are characterized by much bigger volumes and standard pyrotechnic products.

56. By contrast, the market investigation has not confirmed the Parties' claim that there is supply-side substitution between different sorts of pyrotechnic equipment. Indeed, pyrotechnic equipment for defence and space applications need to be qualified (due to reliability and safety requirements), which is a long and costly process64. In addition, many manufacturers are not producing the complete range of pyrotechnic equipment products.

57. For the purpose of this decision, it is considered that the market for pyrotechnic equipment can be segmented according to the field of application (defence; space; aeronautical and other industrial applications). Whether these segments need to be further segmented according to the type of pyrotechnic equipment can be left open since it does not affect the competitive assessment in this case.

3.2. Geographic market definition

58. The Parties submit that the competition in this sector takes place at the European level as pyrotechnic equipment is mainly incorporated in space launchers (in the context of ESA programmes) and tactical missiles (where MBDA, an actor active at European level, is the main player).

59. The market investigation has confirmed that the markets for pyrotechnic equipment are EEA-wide in scope65.

3.3. Competitive assessment

60. The only horizontal overlap in pyrotechnic equipment resulting from the proposed transaction is in the segment for defence applications where both SAFRAN (with a market share of [0-5]% at the EEA level according to the best estimates of the Parties) and SME/PyroAlliance ([10-20]%) are active. However, even in this segment the overlap is minimal and there are several other competitors including Davey-Bickford ([10-20]%), Nexter ([10-20]%) and Chemring ([20-30]%).

61. The market investigation indicated that in a potential EEA market for defence applications, several sizable alternatives exist including Dynitec, Davey Bickford and Chemring66. In addition, the overlap between the parties falls within the scope of recital 18 of the Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (2004/C 31/03). A significant impediment of effective competition is therefore not likely in relation to this potentially relevant market.

62. Should the market for pyrotechnic equipment for defence applications be further segmented, no overlap would arise between the parties as SPS is only active in relation to electro-pyrotechnic initiation, a segment where SME/PyroAlliance is not active as can be seen in the following table (Table 2).

Table 2: Sales of pyrotechnic equipment for defence applications in the EEA (in EUR million, 2009)

| electro- pyrotechnic initiation | bulkhead initiation | deflagrating lines | detonating cords | other energetic materials | Total turnover of the Parties |

SPS | […] | […] | […] | […] | […] | […] |

SME/PyroAlliance | […] | […] | […] | […] | […] | […] |

Total Parties | […] | […] | […] | […] | […] | […] |

Source: Form CO, p. 93.

63. Therefore, the transaction is unlikely to raise competition concerns in relation to horizontal effects in the markets for pyrotechnic equipment.

4. Composite materials

64. Composite materials is a generic term for materials resulting from the combination of two or more materials, a matrix and a reinforcement or fibre, which are combined because of the specific properties their combination produces. SAFRAN is active in thermostructural composite materials whereas SME supplies cold composite materials.

65. The Parties submit that cold composites (which can withstand operating temperatures of up to about 230°C), thermostructural composites (which can withstand operating temperatures of up to 3000°C) and other composites (resisting to temperatures from 200 to 400°C) are not substitutable as they present different characteristics in terms of performance, costs and use.

66. The market investigation has confirmed the submission of the parties67. Indeed, cold composites, thermostructural composites and other composites require different resin/matrix materials which will not work outside of the temperature ranges for which they are designed: they are therefore not used for the same applications.

67. For the purpose of this decision, it is therefore considered that cold composites, thermostructural composites and other composites constitute separate product markets. It can be left open whether these markets need to be further segmented since it does not affect the competitive assessment in this case.

68. The Parties submit that the geographic scope of the market for cold composites is regional while the market for thermostructural composites is worldwide. However, the exact geographic market definition may be left open since it does not affect the competitive assessment in this case.

69. The proposed transaction will not give rise to a horizontal overlap as SAFRAN is active in thermostructural composites only, while SME only supplies cold composite materials. Therefore, the transaction is unlikely to raise competition concerns in relation to composite materials.

B. Vertical overlaps between the Parties' activities in SRMs and in upstream and downstream products

1. Vertical effects in relation to downstream activities in modular armaments

70. Sagem, a SAFRAN subsidiary, manufactures modular armaments and Roxel supplies range extension kits made of SRMs. There is therefore a vertical link between the market for SRMs and the market for modular armaments.

71. Modular armaments are bombs transformed into an air-to-ground precision guided ammunition through guidance and range extension kits. The market investigation has confirmed the Parties' submission that modular armaments constitute a distinct market from conventional bombs on the one hand and tactical missiles on the other hand68. Indeed, conventional bombs have less functions and are less expensive than hybrids weapons. On the contrary, tactical missiles are ready-to-use and far more expensive.

72. The Parties have submitted that the relevant geographic market for modular armaments is worldwide regardless of whether a domestic supplier exists. However, the precise geographic market definition can be left open since it does not affect the competitive assessment in this case.

73. The Parties were not able to provide estimates of Sagem's market shares on such a market. Sagem sales accounted for EUR […] million in 2009 where Boeing, Raytheon and Rafael are also active according to the Parties.

74. In any case, the risk of customer foreclosure in relation to the upstream market of SRMs for tactical missiles and modular armament can be excluded as: (i) […], (ii) Sagem's purchases of SRMs for this programme (EUR […] million a year69) are small compared to the size of the market for SRMs for tactical missiles and modular armaments (roughly EUR […] million in France, EUR […] million in the EEA and EUR […] million in the world). The merged entity will therefore not have the ability to foreclose its competitor in the upstream market for SRMs for tactical missiles and modular armaments as a result of the concentration.

75. The risk of input foreclosure in relation to the downstream market for modular armaments can also be excluded as there are several alternative SRMs suppliers, which have the capacity to take part in new programmes to supply range extension kits. The market investigation has shown that one of them has already taken part in bids for such range extension kits70. The merged entity would therefore not have the ability to foreclose its competitors in the downstream market for modular armaments as a result of the concentration. It should be noted in that regard that none of the respondents in the market investigation active on the market for modular armaments has expressed concerns in relation to the impact of the transaction on this market.

2. Vertical effects in relation to upstream activities in propellants and inputs for propellant charges

Propellant charges

76. Propellants are dense combustible materials that are stable at their service temperature and which, after pyrotechnic initiation, release energy in a controlled manner in the form of gases at high temperatures. Propellants contain, combined chemically or physically, the oxidising and reducing agents necessary for combustion. A distinction is made between homogeneous propellants and composite propellants.

77. In previous cases, the Commission has noted that the production of solid propellant charges could, due to demand-side considerations, be considered as a market upstream of SRMs71.

78. The Parties submit that the question of the possible segmentation of the market for solid propellant charges according to application (i.e. SRMs for tactical missile/strategic missile/aerospace propulsion) would not have any impact on the competitive assessment and can therefore be left open. Indeed, SME is active only in propellant charges for strategic propulsion where the SRM is produced exclusively by G2P (the economic interest group between SME and SAFRAN). The Parties are not active in propellant charges for aerospace propulsion. The transaction only results in one vertical relationship between the market for SRMs for tactical missiles and the market for the solid propellant charges used for SRMs for tactical missiles, where Roxel is active. In addition, the Parties consider that homogenous and composite propellants are fully substitutable for solid propulsion for tactical missiles: they can be both used on SRMs for tactical missiles, all propellant suppliers master both technologies and their price does not significantly differ.

79. The market investigation did not confirm the substitutability between homogenous and composite propellants for tactical propulsion applications72. Respondents emphasize that the full motor design needs to be different depending on the selected propellant, that qualifying an alternate propellant is very expensive and that the two propellant types offer different performance characteristics (smoke emissions in particular are lower for homogenous propellants, while composite propellants have higher specific impulse, temperature range of application and are less sensitive).

80. However, for the purposes of this decision, it can be left open whether the market for propellant charges needs to be further segmented since it does not affect the competitive assessment in this case.

81. The Parties submit that, to the extent that such a separate product market for the sale of propellant charges to third parties for incorporation into SRM exists, it should be assumed that the geographical scope of this potential market is the same as that for SRMs.

82. The market investigation indicated that the market for propellant charges for SRMs is at least EEA wide73. However, export restrictions limit the ability of EEA prime contractors to onward sell their products, depending on the export country and on the origin of the propellant charges. In particular, if the propellant charges are sourced from the US, it follows from the ITAR regulation that missiles exports must obtain prior US authorisation74.

83. Nevertheless, for the purposes of this decision, it can be left open if the scope of the market for propellant charges is limited to the EEA or if it is wider, as it does not affect the competitive assessment in this case.

84. The Parties were not able to provide estimates of their markets shares either on the potential market for propellant charges for tactical motors or on the possible sub- segments of homogenous and composite propellants for tactical propulsion.

85. The risk of customer foreclosure in relation to the potential markets for propellant charges can be excluded as: (i) SAFRAN already purchases all its propellant charges for SRMs for tactical missiles and modular armaments from Roxel; (ii) SAFRAN is a small player in the SRMs market in the EEA (with a markets share [5-10]%). The merged entity would therefore not have the ability to foreclose.

86. In addition, input foreclosure is also unlikely in relation to the market for SRMs for tactical missiles and modular armaments as: (i) Roxel has very limited sales of propellant charges to be incorporated into SRM programmes of other manufacturers (between […] to […]% of its total sales); (ii) all other significant SRMs suppliers (such as Chemring, Nammo, AVIO, Bayern Chemie, ATK, Aerojet, Roketsan) have a propellant competence75 and propellant charges are therefore very rarely sold on a stand- alone basis; (iii) the market investigation indicated that production capacity can be significantly expanded with regard to propellant charges within 18 months76. The merged entity would therefore not have the ability to foreclose its competitors in the market for SRMs for tactical missiles and modular armaments.

Inputs for propellant charges

87. Energetic materials for propulsion (including missiles and space launchers) are made up of raw materials to be mixed, in order to obtain solid propellant. The Parties submit that, in consideration of the different chemical raw materials they supply, the following materials constitute distinct relevant markets: Ammonium Perchlorate, other solid propellant inputs (methyl bapo, mapo, butacene) and MMH.

88. The market investigation indicated that Ammonium Perchlorate indeed constitutes a separate product market (as there is no existing substitute)77. Butacene, a burning catalyst, has limited substitutability possibilities (extra fine Ammonium Perchlorate or iron oxides). Methyl Bapo and Mapo are bonding agent with limited substitutability possibilities. However, the precise product market definition of inputs for propellant charges can be left open for the purposes of this decision, since it does not affect the competitive assessment.

89. The Parties submit that the geographic markets for Ammonium Perchlorate and other inputs for propellant charges are worldwide in scope, even though export sales may be subject to export controls.

90. The market investigation has not confirmed the Parties' submission that the scope of the geographic market for Ammonium Perchlorate is global. Respondents have indicated that the market for Ammonium Perchlorate is EEA wide in scope for tactical missiles produced by EEA manufacturers hoping to export their products outside the EEA and the US. This is due to the US ITAR rules, which require missile manufacturers to acquire the prior authorisation of the American authorities before they can export missiles carrying American Ammonium Perchlorate78. However, the exact geographic market definition for Ammonium Perchlorate and other inputs for propellant charges may be left open for the purposes of this decision, since it does not affect the competitive assessment in this case.

91. SME is almost a monopolist in the supply of Ammonium Perchlorate at the EEA level. Its main competitor on a global level is AMPAC/WECCO, an American company. With regard to Butacene, which is a very small market in terms of volume and value and a product which is not manufactured and traded on a regular basis, SME only sells to […]79.

92. Some SRMs competitors80 raised the concern that post-transaction SAFRAN/SME could increase the price of the Ammonium Perchlorate and Butacene thereby making them less competitive in the market for SRMs. However, these concerns are not merger specific: SME was already the sole European supplier of Ammonium Perchlorate before the transaction and arguably could have had the incentive to foreclose given its 50% interest in Roxel. Moreover, SPS was already buying its propellant charges from Roxel, which purchased the necessary inputs from SME. In addition, the market investigation has confirmed that SME has not leveraged so far its strength on the market for inputs for propellant charges to weaken its competitors by charging them higher prices81, 82. In addition, should SME abuse of its dominant position in the market for Ammonium Perchlorate, this practice could fall under Article 102 of the Treaty on the Functioning of the European Union.

93. Risks of customer foreclosure can also be excluded as SPS subcontracts the manufacture of propellant charges to Roxel and thus does not source raw materials involved in the manufacturing of propellant charges.

3. Vertical effects in relation to upstream activities in pyrotechnic equipment

94. SRMs typically employ an igniter which requires pyrotechnic ignition to in turn ignite the rocket. The igniter typically consists of an initiator and pyrotechnic charges. The activation is achieved by percussion or by an electrical current. The initiator flame and gases in turn ignite the pyrotechnic charges which in turn ignite the propellant in the rocket. Roxel supplies igniters to SAFRAN. SAFRAN manufactures electrical- pyrotechnic initiators specifically designed for the Mistral missile and used in-house (SAFRAN manufactures the Mistral SRM).

95. Risk of customer foreclosure can be excluded as SAFRAN by itself is a small player in the SRMs market in Europe and was already sourcing its igniters from Roxel or produced them in-house. Risks of input foreclosure can as well be excluded as SME/PyroAlliance sales of igniters to SRM manufacturers are extremely limited. They account for a turnover of approximately EUR […], i.e. […]% of the overall turnover of PyroAlliance. In addition, there are several alternative suppliers of pyrotechnic equipments and systems (such as Nexter, Davey-Bickford, Lacroix or Chemring) which have the capacity to supply igniters and/or electric initiators to SRMs manufacturers, which the market investigation has confirmed. In addition, the market investigation has indicated that pyrotechnic equipment represent a small part (1-2%) of the cost of SRMs for tactical missiles83.

4. Vertical effects on relation to activities in Turbojet engines

96. Turbojet engines have been identified by the Commission in the MBDA/Bayern- Chemie84 and the Roxel/Protac cases as a distinct product market from other propulsion technologies as they are based on jet engines. The Parties agree with such a definition.

97. SAFRAN, through its subsidiary Microturbo, is active on the market for turbojet engines and has purchased from PyroAlliance pyrotechnic equipment (flame generators) for its small turboreactors. Flame generators are the igniters of turbojets. They typically consist of an initiator and pyrotechnic charges.

98. The other purchaser of PyroAlliance's flame generators is MBDA. This vertical link represented in 2009 a turnover of EUR […]. These sales have significantly decreased in value between 2000 and 2009 from EUR […] to EUR […].

99. The risk of customer foreclosure can be excluded as (i) Microturbo was already buying its flame generators from PyroAlliance, (ii) these purchases corresponded to a very limited turnover compared to the size of the market for pyrotechnic equipment for defence applications (ca. EUR […] million at the EEA level in 2009) or any of its potential subsegments. The merged entity would therefore not have the ability to foreclose its competitors in relation to flame generators. In addition, the risk of input foreclosure can be excluded as several alternative suppliers of pyrotechnic equipment exist that could produce the flame generators (e.g. Dynitec, Davey Bickford, Chemring or Lacroix). […]. In addition, the French MoD retains significant countervailing buyer power and has an interest in avoiding that cost increase in any segment of the value chain. The merged entity would therefore not have the ability to foreclose its competitors in the market for turbojet engines as a result of the concentration.

C. Coordinated and conglomerate effects

100. Risks of coordinated effects together between the Parties and AVIO will not be increased by the transaction. Indeed, both SAFRAN and SME were already participating with AVIO in common joint ventures before the transaction (respectively Europropulsion and Regulus).

101. The Parties also submit that the risk of conglomerate effects can be excluded. As far as tactical missiles are concerned, guided weapons are composed of a number of sub- systems and equipment, including seekers, proximity fuses, inertial guidance, warhead, rocket motor/propulsion, thermal batteries, etc. The Target is active in the rocket propulsion market. It also supplies pyrotechnic equipments which are incorporated into SRMs and the other subs-systems which compose the missile. However, it is not active in any of these other sub-segments. On the other hand, Sagem offers guidance solutions for all types of missiles. The Parties submit that it cannot be considered that the proposed transaction would provide the Parties with the ability to foreclose competitors in the market of SRMs for tactical missiles and the market of guidance systems (seekers) for tactical missiles by conditioning sales in a way that would link these products together. In particular, they point to the existence of several alternative suppliers of guidance solutions such as Goodrich, Raytheon and Lockheed Martin. In addition, the different sub-systems and equipments that are incorporated in a tactical missile are typically supplied by prime-contractor within the framework of separate bids. Also, the requirements set out by MoDs oblige prime contractor to select all sub-systems and equipment suppliers on the basis of strict technical and financial considerations.

102. One competitor has raised the concern that the merged entity could leverage its position on the SRM market to start selling bundles of pyrotechnic equipment and SRMs to missile manufacturers85. However, this seems unlikely as sub-systems and equipments that are incorporated in a tactical missile are typically supplied by prime-contractor within the framework of separate bids. In addition, Roxel and PyroAlliance, as well as other actors such as Chemring, were already in a position to offer such bundles. Therefore the transaction is not likely to change the ability of the merged entity to bundle. In addition, the market investigation has shown that customers retain significant countervailing buyer power and have the incentive to avoid allowing a practice that would entail increased costs. Finally, the effect of such a foreclosure would be limited as pyrotechnic equipments only represent 2 to 5% of the cost of tactical missiles86

103. As far as the space sector is concerned, space launchers are made up of systems (e.g. stages), sub-systems (e.g. propulsion equipment, attitude control products, etc.) and equipment. Following the proposed transaction, the Parties will be able to supply SRM propulsion systems on a stand alone basis. They will also (via PyroAlliance) supply pyrotechnic equipments to be incorporated in the SRMs and in other sub-systems of the launcher. However, bids will continue to be affected by the “juste retour” rules governing the provision of space infrastructure. Finally, as noted by the Commission in EADS87, customers (ESA and prime contractors) have sufficient countervailing buying power to constrain the competitive behaviour of their suppliers, as well as strong incentives to use this power. For all these reasons, there appears to be no possibility for suppliers to enter into leveraging practices.

VI. CONCLUSION

104. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 SNPE's subsidiary EURENCO is outside the scope of the proposed transaction as it produces gun propellants and high explosives which are activities unrelated to solid propulsion.

3 OJ C 95, 16.4.2008, p. 1.

4 Accord de coopération industrielle, commerciale et financière sur la propulsion solide entre Safran et SNPE en présence de l'Etat, 14 February 2011.

5 Turnover calculated in accordance with Article 5(1) of the Merger Regulation and the Commission ; Consolidated Jurisdictional Notice (OJ C95, 16.4.2008, p.1).

6 This figure corresponds to the turnover of SME and 50% of the turnover of Regulus

7 Ibid.

8 Ariane and Vega are made up of several rocket stages (often three) joined end to end. The stages fire and fall away in turn, ending with the upper stage.

9 Email of Safran of 16 March 2011.

10 Form CO, p.75.

11 Agreed non-confidential minutes of the interview with a third party of 22 February 2011. In addition, the agreement on 14 May 2007 of a strategy for Europe’s Defence Technological and Industrial Base (EDTIB) aims at a less fragmented European Defence Equipment Market.

12 See COMP/M.1636, Astrium, 21 March 2000 and COMP/M.1745, EADS, 11 May 2000.

13 Celerg was jointly controlled by SNPE and EADS France. Royal Ordnance was a wholly-owned subsidiary of BAE Systems. See COMP/M.2938, SNPE / MBDA / JV, 30 October 2002.

14 See COMP/M.5032, Roxel/Protac, 21 April 2008.

15 See COMP/M.4653 MBDA / Bayern-Chemie, 31 July 2007.

16 See COMP/M.3621, SAGEM / SNECMA, 22 December 2004.

17 See COMP/M.1636, Astrium, 21 March 2000, recital 122 and COMP/M.1745, EADS, 11 May 2000, recital 76.

18 Agreed non-confidential minutes of the interview with a third party of 14 February 2011.

19 Agreed non-confidential minutes of the interview with a third party of 14 February 2011.

20 Ibid.

21 Agreed non-confidential minutes of the interview with a third party of 14 February 2011; agreed non- confidential minutes of the interview with a third party of 23 February 2011; agreed non-confidential minutes of the interview with a third party of 24 February 2011.

22 See COMP/M.5032, Roxel/Protac, 21 April 2008, recital 14.

23 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 7. Responses to Article 11 letters of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 7.

24 Response of the French Ministry of Defence (Direction générale de l'armement) to Article 11 letter of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 27.

25 Form CO, p. 52.

26 See COMP/M.2938, SNPE/MBDA/JV, 30 October 2002, recital 11; COMP/M.4653, MBDA/Bayern- Chemie, 31 August 2007, recital 16.

27 Response of the French Ministry of Defence (Direction générale de l'armement) to Article 11 letter of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 27.

28 Form CO, p. 52.

29 See COMP/M.2938, SNPE/MBDA/JV, 30 October 2002, recital 11; COMP/M.4653, MBDA/Bayern- Chemie, 31 August 2007, recital 16.

30 When the propellant charge of a rocket motor is ignited, thrust is created by the combustion process. The propellant charge is made up of an energetic material processed in a specific shape which provides energy by controlled combustion.

31 See COMP/M.2938, SNPE/MBDA/JV, 30 October 2002, recital 11; COMP/M.3205, SNPE/SAAB

/PATRIA /JV (EURENCO), 2 October 2002, recital 20.

32 Responses to Article 11 letters of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 9.

33 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 9.

34 Parties's response to Article 11 Request for information sent on 14 March 2011, question 1.

35 See COMP/M.2938, SNPE/MBDA/JV, 30 October 2002, recital 10.

36 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 10. Responses to Article 11 letters of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 10.

37 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 17.

38 See COMP/M.4653, MBDA/Bayern-Chemie, 31 July 2007, recital 21 and 23.

39 See, for example, Case COMP/M.1745, EADS, 11 May 2000, recitals 129, 137 and 138; Case COMP/M.1797, Saab/Celsius, 4 February 2000, recital 28.

40 Directive 2009/81/EC of the European Parliament and of the Council of 13 July 2009 on the coordination of procedures for the award of certain works contracts, supply contracts and service contracts by contracting authorities or entities in the fields of defence and security, and amending Directives 2004/17/EC and 2004/18/EC

41 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 19. Responses to Article 11 letters of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 11.

42 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 18.

43 US exports regulations (ITAR -Internal Traffic in Arms Regulations and EAR - Export Administration Regulations) limit missile manufacturers' export possibilities if US restricted equipment is used. SRMs are under restricted equipment.

44 Form CO, p.64.

45 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, questions 20 and 32. Responses to Article 11 letters of the Commission to customers of SRMs for tactical missiles of 28 February 2011, questions 12, 22 and 23 .

46 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, questions 5 and 24.

47 Including Bayern-Chemie.

46 Form CO, p.65. This submission of the Parties has been confirmed by the market investigation (responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, questions 5 and 24).

47 Form CO, p.68-69.

48 See Case IV/M.945, Matra BAe Dynamics/DASA/LFK, 27 January 1998, recital 26.

49 See Case COMP/M.1797, Saab/Celsius, 4 February 2000, recital 36.

50 See Case COMP/M.1745, EADS, 11 May 2000, recital 150.

51 See Case COMP/M.3418, General Dynamics/Alvis, 26 May 2004, recital 22.

52 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, questions 30, 34 and 37.

53 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, questions 32 and 33. Response of the French Ministry of Defence (Direction générale de l'armement) to Article 11 letter of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 14.

54 Response of the French Ministry of Defence (Direction générale de l'armement) to Article 11 letter of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 26.

55 Agreed non-confidential minutes of the interview with a third party of 22 February 2011.

56 Agreed non-confidential minutes of the interview with a third party of 22 February 2011.

57 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 29. Responses to Article 11 letters of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 19.

58 Agreed non-confidential minutes of the interview with a third party of 22 February 2011.

59 Non-confidential responses to Article 11 letters of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 18.

60 Responses to Article 11 letters of the Commission to competitors in pyrotechnic equipment of 28 February 2011, question 16.

61 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 56.

62 Agreed non-confidential minutes of the interview with MBDA of 22 February 2011.

63 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 14. Responses to Article 11 letters of the Commission to competitors in pyrotechnic equipment of 28 February 2011, question 7.

64 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 14. Responses to Article 11 letters of the Commission to competitors in pyrotechnic equipment of 28 February 2011, question 6.

65 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 22. Responses to Article 11 letters of the Commission to competitors in pyrotechnic equipment of 28 February 2011, question 8.

66 Responses to Article 11 letters of the Commission to competitors in pyrotechnic equipment of 28 February 2011, question 9.

67 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 15.

68 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 16. Responses to Article 11 letters of the Commission to customers of SRMs for tactical missiles of 28 February 2011, question 15.

69 Form CO, p. 75.

70 Responses to Article 11 letter of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 23.

71 See COMP/M.2938, SNPE/MBDA/JV, 30 October 2002, recital 11; COMP/M.3205, SNPE/SAAB

/PATRIA /JV (EURENCO), 2 October 2002, recital 20.

72 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 11. Responses to Article 11 letters of the Commission to competitors in propellant charges of 28 February 2011, question 8.

73 Responses to Article 11 letters of the Commission to competitors in propellant charges of 28 February 2011, question 11.

74 Responses to Article 11 letters of the Commission to competitors in propellant charges of 28 February 2011, question 12.

75 Form CO, p.107.

76 Responses to Article 11 letter of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 35.

77 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 12. Responses to Article 11 letters of the Commission to competitors in propellant charges of 28 February 2011, question 7.

78 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 21. Responses to Article 11 letters of the Commission to competitors in propellant charges of 28 February 2011, question 13.

79 Form CO, p.114.

80 Responses to Article 11 letter of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 55. Agreed non-confidential minutes of the interview with a third party of 16 February 2011.

81 Agreed non-confidential minutes of the interview with a third party of 16 February 2011. Parties' reply to the Commission' request for information sent on 14 March 2011.

82 This has been confirmed by evidence submitted by the Parties: Parties' response to Article 11 Request for information sent on 14 March 2011, questions 7 and 8.

83 Responses to Article 11 letters of the Commission to competitors in solid propulsion for tactical missiles and modular armaments of 28 February 2011, question 45.

84 See COMP/M.4653, MBDA/Bayern-Chemie, 31 July 2007.

85 Agreed non-confidential minutes of the interview with a third party of 15 March 2011.

86 Agreed non-confidential minutes of the interview with a third party of 15 March 2011.

87 See COMP/M.1745, EADS, 11 May 2000, recital 150.