Commission, June 22, 2011, No M.6194

EUROPEAN COMMISSION

Judgment

OSRAM / SITECO LIGHTING

Dear Sir/Madam,

Subject: Case No COMP/M.6194 - Osram / Siteco Lighting

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041

1. On 13 May 2011, following a referral pursuant to Article 4(5) of Council Regulation (EC) No 139/20042, the European Commission received a notification of a proposed concentration by which the undertaking, Osram GmbH ("Osram", Germany, referred to as "the notifying party") controlled by Siemens AG ("Siemens", Germany) acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the undertaking Siteco Lighting GmbH ("Siteco", Germany) by way of purchase of shares. Osram and Siteco are jointly referred to as "the Parties".

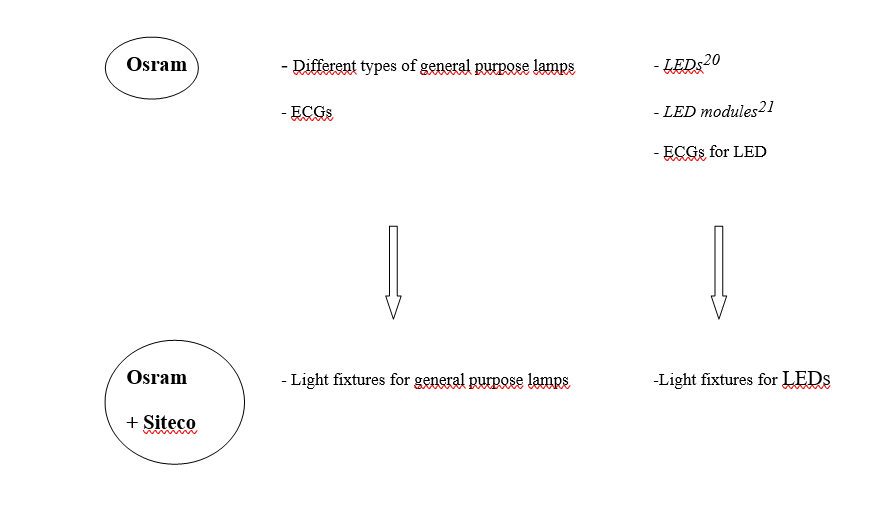

I. THE PARTIES

2. Osram manufactures and markets a wide range of products such as traditional lamps for general purpose lighting, LED light sources, lamps for special purposes as well as light fixtures and electronic control gears, which are components for light fixtures. Its parent company, Siemens, is active in various manufacturing, technology and services business activities. Siemens participates in the lighting industry only through its Osram subsidiary.

3. Siteco is active in the production, development and sale of professional light fixtures and technical lighting solutions. The company focuses on professional indoor and outdoor lighting fixtures, including applications for offices, industry, retail markets, street lighting, sport facilities, and to a minor extent community facilities.

II. THE OPERATION AND THE CONCENTRATION

4. On 26 February 2011, Osram and the current shareholders of Siteco entered into a Share Purchase Agreement to acquire Siteco Lighting GmbH. By means of this agreement Osram will acquire all shares of Siteco’s current shareholders, i.e. private equity funds established by Barclays Bank plc and affiliated companies as well as private shareholders.

5. As a consequence Osram, will acquire sole control of Siteco. The proposed transaction constitutes a concentration within the meaning of Article 3 (1)(b) of the Merger Regulation.

III. EU DIMENSION

6. The operation does not have an EU dimension since Siteco's turnover in 2010 did not exceed EUR 250 million in the EU and Siteco did not achieve a turnover of more than EUR 25 million in three Member States. Thus, the thresholds of Article 1 EU Merger Regulation are not met.

7. However, on 23 March 2011 the notifying party informed the Commission in a reasoned submission that the concentration was capable of being reviewed under the national competition laws of seven Member States (Austria, Cyprus, Germany, Ireland, Italy, Slovakia and Slovenia3) and requested the Commission to examine the transaction. None of the Member States that were competent to examine the concentration indicated its disagreement with the request for referral within the period laid down by the Merger Regulation. The notified operation is therefore deemed to have an EU dimension according to Article 4(5) of the Merger Regulation.

IV. RELEVANT MARKETS

8. The acquisition of Siteco by Osram constitutes mainly a vertical integration between a producer of light sources (Osram) and a producer of fixtures (Siteco).4 This integration aims at enabling Osram to offer fully integrated lighting solutions especially in view of the expected technical shift within the lighting industry from traditional light sources towards more energy efficient lamps, in particular based on light emitting diodes ("LEDs") technology.

9. LEDs constitute a more energy-efficient source of light than traditional general purpose lamps. Another key difference is that LEDs have a much longer life span than traditional lamps and therefore do not require frequent replacement. Accordingly, light fixtures using this new source of light are often integrated products, where LEDs are designed as a part of fixture and not as replaceable consumable good.

10. Although currently LED technology is not yet widespread, and the parties to the transaction possess higher market shares in the traditional lighting solutions, the industry expects that in the next 5-10 years, LED technology will to a significant extent replace traditional lighting technology. Consequently, the decision also addresses LED technology although it does not lead to technically affected markets.

1. Relevant Product Market

(a) Light Fixtures

11. The activities of Osram and Siteco overlap in light fixtures. Light fixtures control the diffusion of light and heat, ensure the delivery of the correct electricity characteristics and provide the optical assembly, which houses the light bulb.

12. In previous decisions, the Commission has held that the market for light fixtures comprises two different product markets, i.e. consumer/residential and professional/industrial light fixtures.5 As regards the market for professional light fixtures, the Commission has left open whether this could be further segmented into indoor and outdoor light fixtures.

13. The notifying party and the market investigation confirmed these distinctions. Indeed, professional light fixtures are primarily focused on functionality and are usually installed by professional installers because they require additional work before being operational. By contrast, consumer/residential light fixtures are more easy to use given their pre-wire application i.e. can be installed by non-professionals. Also, professional light fixtures are more expensive and are mainly distributed through electric wholesalers, while residential light fixtures are predominantly distributed through retail markets such as "do-it-yourself" stores.

14. Some responses to the market investigation also pointed to the segmentation of the professional light fixtures into indoor and outdoor light fixtures. In addition, a number of respondents pointed out that the outdoor and indoor fixtures differ in terms of technical features (outdoor fixtures being more weather resistant) and price.

15. In addition, some market participants pointed out that a sub-segment of LED light fixtures may be identified within the light fixtures market due to (i) technical specifications (i.e. there is an absence of interchangeability between LEDs and other technologies' lamps); (ii) production specifications (i.e. the materials used in production differ); and (iii) economic reasons (prices, R&D, energy consumption vary). However, in its previous decisions, the Commission has not assessed the market for LED fixtures as a separate segment/market within the overall market for fixtures.

16. According to the notifying party LED fixtures are part of the same product market as other light fixtures since there is a high degree of demand-side substitutability between them. This is because the demand of the end-customers is predominantly driven by the basic purpose of a light fixture, i.e. illumination.

17. At the same time, the notifying party states that fixtures devoted to LED lighting are different from fixtures for general purpose lamps since the first are equipped with an irreplaceable LED module. They also consist of different components (in particular different ECGs) than fixtures for general purpose lamps

18. The responses from the market investigation are not entirely conclusive in this aspect. A narrow majority of respondents (11/20) indicated that LED fixtures are not interchangeable with other general purpose light fixtures because of technical (different types of light source used), production (different components and production method) and economic (different prices) reasons. However a significant number of respondents (8/20) indicated that LED fixtures serve the same purpose (illumination), and are sold via the same channels as the general purpose light fixtures. Moreover, some respondents also indicated that technical barriers to switch from producing one type of fixture to another are not high.

19. A market participant (manufacturer of light fixtures) suggests to segment further the LED light fixtures segment into overlay and spot-by-spot fixtures depending on the positioning of the LEDs in the LED light fixture. In this regard, it is noted that some (6/20) light fixture producers have outlined the difference between customised and standard light fixtures. This distinction has been however suggested in parallel with other possible segmentations of LED fixtures.

20. For the purposes of the present case, the Commission assessed the market shares of the parties in a hypothetical market for LED fixtures. For the purpose of the present decision, it is however not necessary to conclude on the existence such a separate market for LED fixtures, since the transaction does not lead to competition concerns even under the assumption of such a separate market.

21. The Commission did not engage in further hypothetical sub-segmentations since (i) the market shares of the parties in LED fixtures are limited; (ii) the responses to the first phase market investigation did not suggest any further clear delineation between different types of LED fixtures.

(b) General purpose lamps

22. Osram sells general purpose lamps (bulbs), which are normally held by light fixtures. General purpose lamps are sold either directly to the end customer who then incorporates them in the fixture or incorporated into a fixture by the fixture producer. General purpose lamps may be further subdivided according to the basic technology used and the broad characteristics of the lamp, e.g. energy consumption and properties of the light produced.

23. In previous cases, the Commission had excluded lamps for specialty applications such as vehicle lights and sun tanning lights lamps from the general purpose lamps market. This has been confirmed by the market investigation.

24. The Commission has previously considered whether the market for general purpose lamps should be sub-divided into incandescent, halogen, fluorescent, compact fluorescent, and high intensity discharge lamps along the lines of the basic technology used and the broad characteristics of the lamp (e.g. energy consumption and properties of the light produced)6.

25. The notifying party considers that the market for general purpose lamps should not be divided into the above different sub-segments mainly due to a high degree of substitutability from the supply side as all types of general purpose lamps are offered by the same suppliers and are produced based on the same socket technology, hence facilitating switching to other types of lamps in case of a price increase for a certain type of lamp.

26. Companies producing general purpose lamps noted that the different types of lamps are used for the same illumination purpose and as long as the lamp socket is the same, different lamp types can be used interchangeably between fixtures. However, some lamps are designed for specific applications or require adjustment to the fixture. Furthermore, respondents also indicated that it was not easy to switch production between different types of lamps.

27. Therefore for the purpose of this decision, it is proposed to consider different segments of general purpose lamps while leaving open whether they constitute separate product markets since the transaction does not lead to competition concerns under any product market definition.

(c) Solid state lighting - LEDs, LED modules and LED retrofit lamps

28. Solid state lighting ("SSL") is a new lighting technology which surfaced recently in the industry. SSL uses clusters of small semiconductor LEDs (or organic OLEDs) as sources of illumination rather than the electric filaments, plasma or gas used in traditional lamps. A LED is a small single light-emitting diode which comprises a semiconductor chip and its housing. LED lighting is more energy-efficient than lighting based on traditional general purpose lamps.

29. Osram is active in LEDs, organic light-emitting diodes ("OLED"),7 LED retrofit lamps and LED modules.

30. As explained above, LEDs are the small light-emitting diodes used as source of lighting and are the basic component for LED retrofit lamps and LED modules.

31. LED retrofit lamps have a traditional socket and are designed as a replacement for incandescent lamps.

32. LED modules are specifically assembled diodes including electric components. 8

33. In its Philips/PLI decision, the Commission has indicated that LEDs may constitute a separate product market.9

34. In line with this precedent, the notifying party submits that LEDs may constitute a separate product market since they are separately sourced as basic components by manufacturers of LED light fixtures, LED modules and LED retrofit lamps.

35. Similarly, the notifying party considers that also LED modules may constitute a separate market largely because it is not possible to replace the LED module in the light fixture by a general purpose lamp (due to electronic, mechanic and optical incompatibility). Furthermore, LED modules are primarily sold to companies active in the manufacture and sale of light fixtures and not to direct end-customers via retail channels.

36. The market investigation confirms that from the point of view of the fixture producers the LEDs (integrated into LED modules) are not interchangeable with general purpose light since the first are designed for and integrated into LED fixtures whereas the latter could fit into a number of general purpose light fixtures. This implies that contrary to LEDs, general purpose lamps can be replaced directly by the customer after its lifespan has expired.

37. As regards LED retrofit lamps, the notifying party considers that it is a lamp designed as a replacement for incandescent lamps and that most general purpose lamps can be replaced by LED retrofit lamps due to the standardisation of the socket systems.

38. The market investigation suggests that LED retrofit lamps constitute a separate product market. On the supply side, all manufacturers of general purpose lamps which responded to the market investigation also produce LED retrofit lamps. However, all of them stated that it would not be easy to switch production of general purpose lamps to LED retrofit lamps because LED is a different technology. From the demand side, LED retrofit lamps appear to be interchangeable with only some traditional general purpose lamp technologies (incandescent, halogen, compact fluorescent). In any case, LED retrofit lamps are not interchangeable with LEDs or LED modules themselves.

39. As retrofit lamps have all the characteristics of general purpose lamps (i.e. they fit with traditional sockets and can be replaced in general purpose lamps fixtures), the competitive assessment with regards to retrofit lamps will be carried out in the section dealing with general purpose light.

40. In any event, the exact product market definition for LEDs, LED modules and LED retrofit lamps can be left open, since no competition problems arise.

(d) Components for light fixtures - Electronic control gears ("ECGs")10

41. The Commission has previously left open whether there are separate markets for components for light fixtures like fluorescent chokes, HID chokes, electronic transformers, magnetic transformers, igniters and electronic control gears (ECGs).11

42. OSRAM is active in the sale of components for light fixtures. In particular, Osram is active in ECGs.

43. ECGs are one of the components for light fixtures units which continually adjust the lamp voltage and current to keep the lamp power and hence the light output constant, irrespective of the variation in the supply voltage.

44. The notifying party submits that there should be a single product market for ECGs as a whole irrespective of the fact that the ECGs used for light fixtures with LED modules are different from the ECGs for light fixtures in which general purpose lamps are used. According to the notifying party, this is because there is a high degree of supply side substitutability: ECG manufacturers are, in general, able to make ECGs for all types of lighting technologies.

45. However, the responses to the market investigation indicated that there is a difference between ECGs for LED modules and those for light fixtures in which a general purpose lamp is used, mainly due to the different light source used. This is also reflected in the price as the ECGs for LED modules tend to be more expensive probably also because the LED technology is relatively new on the market.

46. On the other hand, the companies active in the production of ECGs noted that they typically use the same technology and production line for all types of ECGs. In this regard, the majority of respondents consider that the ECGs for light fixtures in which a general purpose lamp is used and the ECGs for LED modules constitute one product market. In effect, ECG manufacturers confirmed that they are able to produce ECGs for all types of lighting technologies, thus contributing to a high degree of supply side substitutability in the market.

47. For the purpose of this decision, the exact product market definition can be left open as to whether there are separate markets for ECGs for light fixtures in which a general purpose lamp is used and for ECGs used in LED modules. This is because under all possible market definitions considered, effective competition would not be significantly impeded in the EEA or any substantial part thereof.

2. Relevant Geographic Market

(a) Light Fixtures

48. In previous decisions, the Commission has defined the market for light fixtures for professional use as national in scope.12 However, in subsequent cases the Commission has left open whether the geographic market is national or EEA wide.13

49. The majority of respondents to the market investigation indicate that, irrespective of the segment of fixtures in question, the market for light fixtures is at least EEA wide. Some of the respondents point out that the fixtures sold in the EEA have to fulfil a number of technical requirements which might be different from the requirements in the other parts of the world. Hence, they content that most relevant geographic market for light fixtures is EEA wide.

50. On the other hand, the fixtures manufacturers underline that as only a number of the largest customers would procure fixtures internationally, they consider their national presence and sales teams to be crucial for their light fixtures business.

51. Therefore, in the view of the fact that the proposed transaction does not lead to any competition concerns in the different geographical markets, it is proposed to leave the exact geographic market definition open and analyse the transaction on both, EEA and national level.

(b) General purpose lamps

52. As regards the market for general purpose lamps, the Commission in previous decisions has left it open whether it is national or EEA wide in scope.14

53. In this regard, the notifying party contends that this market is at least EEA-wide particularly given that general purpose lamps are standardized products which are compact in size, use little space in packaging and are rather lightweight. Hence transport costs are low even for shipments between different continents.

54. The market investigation indicated that the geographic scope of the market for general purpose lamps could be either national or EEA-wide. Whereas some producers stated that there are significant price differences across the EEA, others disagreed. Large customers tend to procure lamps internationally but some other producers use EEA price lists as they consider transport costs not to represent a significant proportion of the total production cost. However, smaller customers procure locally with some producers resorting to national price lists. Nonetheless, most of the respondents retained that it was necessary to have local sales forces.

55. However, in the present case, it is not necessary to define the exact geographic market definition as in neither case would the proposed concentration raise competition concerns.

(c) Solid state lighting - LEDs, LED modules and LED retrofit lamps

56. In Philips/PLI, the Commission has also left open whether the market for LEDs is EEA wide or national in scope.15

57. In this regard, the notifying party submits that the market for LEDs would be worldwide in scope as these products are sourced on a global level, although the precise definition may be left open given that even as an EEA wide market for LEDs, this market would not be affected.

58. Similarly, the notifying party notes that the market for LED components such as LED modules may be worldwide in scope largely because these components are sourced on a global level and are currently not sold to ultimate customers via retail channels.

59. The respondents to the market investigation have largely confirmed that all the components for light fixtures, including components for LED light fixtures, are sourced at least on an EEA wide basis.

60. However, for the purpose of the present transaction, the precise geographic market definition can be left open since the transaction does not lead to competition concerns.

(d) Components for light fixtures - Electronic control gears ("ECGs")

61. The Commission in KKR/WASSAL/Zumtobel had left open whether the geographic market for components for light fixtures is EEA wide or worldwide.16

62. The notifying party submits that particularly as regards the market for ECGs (both ECGs in general and ECGs for LED light fixtures) the market is rather worldwide in scope. This is because ECGs are sourced on a global level and are currently not sold to ultimate customers via retail channels.

63. In the context of the investigation at hand, the Commission has found no indications that there are significant restrictions across the countries in the EEA for the market of ECGs. In effect, the majority of customers of ECGs (the vast majority of which are manufacturers of light fixtures) indicated that for their purchases, they typically consider suppliers located within the EEA. The market investigation also confirmed the existence of a developed trade network within the EEA

64. Thereby, in the present case it is proposed to define the geographic scope of the market for ECGs as at least EEA wide.

V. COMPETITIVE ASSESSMENT

1. General Introduction

65. The proposed transaction gives rise to a horizontally affected market in the professional outdoor light fixtures in Norway. In addition, the proposed transaction leads to a number of vertically affected markets as regards components of light fixtures, which include ECGs, various types of traditional general purpose lamps, LED retrofit lamps as well as LED modules, which are all produced by Osram. There also exist a number of supply- relationships between the parties.

2. Horizontal relationships

(i) Professional Light Fixtures in Norway

66. Both parties are active in professional light fixtures across all EEA countries

67. In the EEA, the parties' combined market share post transaction will be relatively small, i.e. around [0-10]% for overall professional light fixtures (with increment [0-5]% due to Osram). In the sub-segment for indoor professional light fixtures the parties would achieve around [0- 10]% market share whilst in outdoor light fixtures, the combined market share in the EEA is around [0-10]% (increment [0-5]% due to Osram). This would place the merged entity behind the market leader Philips (with an estimated market share of [10-20]% in 2009) and Zumtobel ([5-10]%). The remaining part of the market is constituted by Trilux ([0-5]%) and a large number of other small players.17

68. In a hypothetical separate segment for LED fixtures in the EEA, the combined market share of the parties would be even smaller at [0-10]% (with increment [0-5]% due to Siteco). This gives the merged entity a minimal presence in the market. The market leaders, Philips and Zumtobel have [0-10]% and [0-10]% market shares respectively.

69. As explained above, the market for light fixtures is not affected on the EEA-wide level. Similarly, on a national level, the proposed transaction does not lead to affected markets with the single exception of Norway.18

70. In effect, the combined market share of the parties within the Norwegian segment for outdoor professional light fixtures is [20-30]% (increment [0-5]% due to Osram).19 As a consequence the proposed transaction will result in the merged entity being the market leader in professional outdoor light fixtures in Norway. However, this strong position on the Norwegian market is largely due to Siteco's relatively high ([20-30]%) market share pre- transaction in the professional outdoor fixtures segment.

71. Moreover, although the merged entity will remain the market leader in the Norwegian segment for outdoor professional light fixtures with [20-30]%, it will still face significant competition from other market participants, namely Defa and Philips with [20-30] % and [10-20]% market share respectively.

72. The respondents of the market investigation (Norwegian customers and competitors of the merging entities) view the transaction as a vertical rather than a horizontal integration. None of the respondents raised competition concerns with regards to the horizontal integration on the market for light fixtures in Norway or any segment thereof. The respondents also confirmed existence of strong competitors for light fixtures in Norway.

73. Hence it is concluded that this transaction does not lead to horizontal competition concerns on the market for professional light fixtures in Norway.

3. Vertical relationships

74. The proposed transaction will also lead to a number of vertically affected markets, notably because, as illustrated below:

· Osram is present in the markets (i) for various types of traditional general purpose lamps and for LED retrofit lamps with a market share above [20-30] % in different segments; and (ii) for components of light fixtures, namely ECGs with market shares above [20-30]%.

· Siteco, and to a limited extent Osram, are present downstream in the market for professional light fixtures.

(i) General purpose lamps as an input to light fixtures

75. Osram is active in the manufacture and sale of numerous types of lamps classified as general purpose lamps. Within the market for general purpose lamps, Osram has market shares of around [30-40]% in the EEA.22

76. If different segments of general purpose lamps were to be considered on the EEA – wide basis, the market shares of Osram would be: for incandescent lamps (GLS) [30-40]%; for halogen lamps (HAL) [40-50]%; for fluorescent lamps (FL) [30-40]%; for compact fluorescent lamps (CFLi) [20-30]%; for compact fluorescent pin lamps (CFL pin) [30-40]%, for high density discharge lamps [20-30]% and for LED retrofit lamps [5-10]%.

77. Osram’s market shares in national markets for general purpose lamps and their segments are listed in the table below:

for CFLi, [30-40%] for CFLpin, and [20-30%] for HID.

Country | Overall General Purpose Lamps (incl. LED retrofit lamps) |

GLS |

HAL |

FL |

CFLi |

CFLpin |

HID |

LED Retrofit Lamps |

Austria | [30-40]% | [40-50]% | [40-50]% | [40-50]% | [30-40]% | [30-40]% | [40-50] % | [10-20]% |

Belgium | [30-40]% | [30-40]% | [50-60]% | [20-30]% | [20-30]% | [50-60]% | [20-30]% | [20-30]% |

Bulgaria | [20-30]% | [20-30]% | [30-40]% | [20-30]% | [20-30]% | [20-30]% | [30-40]% | [40-50]% |

Cyprus | [20-30]% | [20-30]% | [20-30]% | [10-20]% | [10-20]% | [30-40]% | [30-40]% | [40-50]% |

Czech Rep. | [30-40]% | [30-40]% | [30-40]% | [30-40]% | [20-30]% | [20-30]% | [30-40]% | [10-20]% |

Denmark | [30-40]% | [40-50]% | [30-40]% | [40-50]% | [10-20]% | [40-50]% | [40-50]% | [30-40]% |

Estonia | [30-40]% | [30-40]% | [60-70]% | [30-40]% | [40-50]% | [20-30]% | [30-40]% | [30-40] % |

Finland | [20-30]% | [30-40]% | [50-60]% | [20-30]% | [30-40]% | [40-50]% | [20-30]% | [5-10]% |

France | [20-30]% | [20-30]% | [30-40]% | [30-40]% | [20-30]% | [30-40]% | [20-30]% | [10-20]% |

Germany | [40-50]% | [50-60]% | [40-50]% | [40-50]% | [20-30]% | [50-60]% | [30-40]% | [20-30]% |

Greece | [20-30]% | [30-40]% | [40-50]% | [20-30]% | [10-20]% | [20-30]% | [30-40]% | [20-30]% |

Hungary | [20-30]% | [20-30]% | [30-40]% | [20-30]% | [30-40]% | [30-40]% | [30-40]% | [30-40]% |

Iceland | [40-50]% | [40-50]% | [40-50]% | [50-60]% | [30-40]% | [40-50]% | [40-50]% | [30-40] % |

Ireland | [10-20]% | [5-10]% | [50-60]% | [20-30]% | [5-10]% | [10-20]% | [10-20]% | [0-5]% |

Italy | [30-40]% | [20-30]% | [40-50]% | [30-40]% | [20-30]% | [50-60]% | [30-40]% | [10-20]% |

Latvia | [30-40]% | [30-40]% | [50-60]% | [20-30]% | [40-50]% | [30-40]% | [30-40]% | [30-40] % |

Lithuania | [30-40]% | [10-20]% | [60-70]% | [30-40]% | [50-60]% | [40-50]% | [30-40]% | [30-40] % |

Malta | [10-20]% | [5-10]% | [40-50]% | [10-20]% | [0-5]% | [20-30]% | [30-40]% | [30-40] % |

Netherlands | [20-30]% | [10-20]% | [30-40]% | [10-20]% | [10-20]% | [20-30]% | [20-30]% | [10-20]% |

Norway | [40-50]% | [60-70]% | [60-70]% | [30-40]% | [30-40]% | [30-40]% | [50-60]% | [50-60]% |

Poland | [30-40]% | [20-30]% | [40-50]% | [20-30]% | [30-40]% | [30-40]% | [30-40]% | [5-10]% |

Portugal | [30-40]% | [30-40]% | [40-50]% | [40-50]% | [30-40]% | [30-40]% | [40-50]% | [20-30]% |

Romania | [20-30]% | [330-40]% | [30-40]% | [20-30]% | [50-60]% | [10-20]% | [10-20]% | [20-30]% |

Slovakia | [30-40]% | [20-30]% | [40-50]% | [30-40]% | [40-50]% | [30-40]% | [30-40]% | [30-40] % |

Slovenia | [30-40]% | [30-40]% | [40-50]% | [30-40]% | [30-40[% | [40-50]% | [10-20]% | [30-40] % |

Spain | [30-40]% | [20-30]% | [50-60]% | [20-30]% | [20-30]% | [20-30]% | [30-40]% | [20-30]% |

Sweden | [30-40]% | [30-40]% | [70-80]% | [20-30]% | [10-20]% | [20-30]% | [30-40]% | [20-30]% |

U.K. | [10-20]% | [5-10]% | [20-30]% | [10-20]% | [5-10]% | [20-30]% | [10-20]% | [5-10]% |

78. As explained above, the merged entity will be active downstream in the market for professional light fixtures with a market share of around [0-5]% in EEA ([0-5]% in the segment of indoor professional fixtures and [5-10] % in the segment of outdoor professional fixtures). In addition, the combined market shares at the national level do not exceed [20- 30]% for professional fixtures and indoor/outdoor segments thereof, except in Norway with [20-30]% in professional fixtures for outdoor lighting.

79. Furthermore, the structure of the market indicates that for general purpose lamps, Philips is the market leader with [30-40]% market share per value and there are a number of other sometimes strong players present in this market including that of LED retrofit lamps such as GE and Havels/SLI with market share of [5-10]% and [0-5]% respectively in the EEA

80. Similarly, the market structure for professional fixtures in the EEA also includes a number of other significant market players like Philips and Zumtobel.

81. In this regard, the parties submit that the existent supply relationships between Osram and Siteco in the market for general purpose lamps are very limited. This is because the volumes of halogen lamps, fluorescent lamps, compact fluorescent lamps and HID lamps sourced by Siteco are very low. These limited amounts are largely attributed to the fact that light fixtures are not sold with an integrated light source and therefore, the general purpose lamps are to a very limited extent sourced by Siteco.

82. As a consequence, Siteco’s purchases of lamps in each general purpose lamp segment represent less than [5-10]% of Osram’s sales.

83. On the other hand, already today Siteco purchases from Osram the following types of general purpose lamps: HAL lamps, FL/CFLpin lamps and HPD lamps. The purchase of these lamps from Osram account for [a significant part] of Siteco’s total purchase in each category.

84. The fact that all producers of general purpose lamps stated that light fixtures are generally not being sold with an integrated light source (except for the light fixtures with LED modules) has been confirmed in the market investigation. A number of respondents have further pointed out that Siteco is too small to consume a significant part of Osram’s sales of general purpose lamps and therefore, the transaction could not lead to input or customer foreclosure for a number of reasons.

85. First, given that Siteco's purchase of general purpose lamps represents only [5-10]% of Osram's sales which already accounts for [a significant part] of Siteco's total demand for general purpose lamps, the merged entity would not have the ability for input foreclosure. General purpose lamps are only to a limited extent sourced by the light fixture manufacturers, since they are equally sold to the end customers as a replacement in the fixtures. Therefore the direct supply from Osram to Siteco is not likely to constitute an important input to the downstream product.

86. What is more, Siteco’s presence in a downstream market for light fixtures is relatively limited. Therefore, even if Siteco would start to purchase all its general purpose lamps from Osram, Siteco would not be able to absorb a significant amount of Osram’s supply since currently it accounts for [5-10]% of Osram's supply only. Therefore Siteco's relatively limited market share in the downstream market for light fixtures (around [0-5]% in the EEA) would not enable it to absorb a significant amount of Osram’s total supply of general purpose lamps.

87. Also, there are a number of competitors to Osram present on EEA wide level for general purpose lamps, with significant market shares. These competitors would be able to satisfy additional demand for general purpose lamps if it occurs.

88. Secondly, in this case the merged entity will not have the ability for a customer foreclosure as well. This is because Siteco's presence downstream in limited and currently it does not represent a significant demand for general purpose lamps from Osram's competitors. Therefore the merger would constitute rather an internalisation of the parties existing supply relationship.

89. As a result, the merged entity would not have the ability to engage in input or customer foreclosure strategies with respect to the general purpose light.

(ii) ECGs as an input to light fixture

90. Osram is active in the manufacture and sale of ECGs. The market share realised on an EEA level is [30-40]% and [20-30]% per value and per volume respectively in 2010, hence following a solid [0-5]% yearly increment ever since 2008. According to the market share estimates' of the parties, Philips and Tridonic/Zumtobel are the closest competitors on the EEA level having [20-30]% and [10-20]% market share per value respectively.

91. As previously stated, post transaction the merged entity will be active downstream in the market for professional light fixtures with a market share of around [0-5]% in the EEA ( [0- 5]% in the segment of indoor professional fixtures and [5-10]% in the segment of outdoor professional fixtures).23

92. According to Osram, given that presently Siteco purchases around [significant part] of its total purchases of ECGs from Osram, the transaction would lead to a mere vertical integration of an existent supply relationship. The parties further highlight that as Siteco's share of total purchase of ECGs in the EU amounts to below [5-10]%, the proposed transaction will neither result in customer foreclosure nor input foreclosure.

93. In principle, the merged entity would not have the incentive for input foreclosure for a number of reasons. First, the market investigation has not shown that the market for ECGs is short in capacity. Even if this was the case, the competitors responding to the market investigation have clearly indicated that in case of a shortage of supply or additional demand, they would be able to duly cater for such increase in demand. Moreover, the customers have also confirmed that even post-merger, there would be enough credible market players.

94. Secondly, the overwhelming majority of the respondents to the market investigation observed that Osram does not produce any exclusive and unique type of ECGs which nobody else in the industry can produce. Indeed, the competitors responding to the market investigation highlighted that particularly with respect to the ECGs where a general purpose lamp is used, there is a high degree of interchangeability between the ECGs produced by different manufacturers as these are standardised on the market.24 Indeed, also the customers responding to the market investigation have indicated that Osram's ECGs are of the same type and quality as those produced by the other manufacturers. Thereby, given that the different ECGs produced by Osram do not represent a significant source of product differentiation for the downstream product, input foreclosure does not arise.

95. The proposed merger is also not likely to result in customer foreclosure. This is particularly driven by the structure of the relevant distribution chain in the market for ECGs. As shown by the market investigation, ECGs for light fixtures in which a general purpose lamp is used are predominantly sold to fixture companies and occasionally to distributors.25 On the other hand, the ECGs for LED light fixtures are almost invariably sold to manufacturers of light fixtures. However, in the case at hand, Siteco is the largest customer of Osram for ECGs representing [5-10]% of its total sales within the EEA26 which in turn constitutes around [a significant part] of Siteco's total purchases of ECGs. This implies that the merged entity would not have the ability to foreclose customers in the downstream market for professional light fixtures as evidenced by the minimal market share of [0-5]% in the EEA.

(iii) LED modules as input to light fixtures for LEDs

96. During the market investigation a number of competitors to Siteco raised a possible competitive concern with regards to the components to LED light fixtures (including in particular LED modules) which constitute an immediate input for the light fixtures.

97. However, on the basis of the information provided by the parties, the market for components for LED fixtures would not amount to an affected market since the parties’ market share for each of the components for the LED light fixtures is below [20-30]%

98. In particular Osram estimates its market share to be less than [0-10]% both globally and in the EEA for each of LED modules and LED light engines as well as a market comprising both LED modules. The main competitors of Osram on this market are Philips, Zumtobel, Cree, Samsung, Toshiba and Delta Electronics, each with a market share of less than 10%.27

99. If a market for LEDs which are used for LED lamps, components and fixtures would be taken into account, within the EEA, Osram’s market share would amount approximately to [10-20]% with strong competitors such as Philips (estimated market share of [10-20]%), Cree ([10-20]%), Nichia ([10-20]%) and a number of smaller Asian players.

100. As explained above, the combined market shares of the parties on the LED fixtures market would amount to less than [10-20] % on the EEA wide level. Within this market, the merged entity’s main competitors would be Philips, Zumtobel and Schreder. The parties have further confirmed that they do not exceed [20-30]% in any national market for LED fixtures.

101. Furthermore, the respondents in the market investigation have pointed out that they could switch to alternative suppliers for most of the components. As alternatives, they have indicated Philips, Tridonic, Helvar and GE.

102. Therefore, in the view of relatively limited market shares of the parties in the above markets and the presence of competitors for LED modules the above the competition concerns in this market can be dismissed.

VI. CONCLUSION

103. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 OJ L 24, 29.1.2004, p. 1 (the "Merger Regulation").

3 The transaction was also eligible for notification in one EFTA state – Norway.

4 To a limited extent, the parties also overlap in the light fixtures market.

5 Case No. IV/M.258 – CCIE/GTE, decision of 25 September 1992, para. 16; Case No. COMP/M.1876 – KKR/WASSAL/Zumtobel, decision of 13 April 2000, para. 11; Case No. COMP/M.2917 – Wendel- KKR/Legrand, decision of 14 October 2002, para. 18; and Case No. COMP/M.4509 – Philips/PLI, decision of 29 January 2007, paras. 7-8.

6 Case No. IV/M.258 – CCIE/GTE, para. 15 and Case No. COMP/M.4509 – Philips/PLI, para. 13. Furthermore, in Case No. COMP/M.4735 – Osram/Sunny World, para. 19, the Commission has left the question open whether the market for compact fluorescent lamps with integrated ballast ("CFL-i") constitutes a separate market and whether within the CFL-i market, different segments have to be considered.

7 OLEDs are organic LEDs which serve as a diffuse light emitting source that is typically used in displays rather than in light fixtures given its two-dimensional, transparent and potentially elastic properties. The notifying party submits that the use of OLED for lighting purposes is at a very early stage. For example, Osram started to sell OLED to the market only in financial year 2010/2011 as a prototype product. Therefore this product will not be considered further.

8 LED modules are also sometimes called LED light engines. Although LED modules and LED light engines are similarly used terms, the latter are standardized whereas the former are not. Standards of LED light engines mainly relate to specific characteristics and different interfaces which aim at increasing the market acceptance/attractiveness of lighting products.

9 Op cit, para. 14.

10 ECGs are also known as electronic ballasts.

11 Case No. COMP/M.1876 – KKR/WASSAL/Zumtobel, decision of 13 April 2000, para. 11.

12 Case No. IV/M.258 – CCIE/GTE, decision of 25 September 1992, para 20.

13 Case No. COMP/M.1876 – KKR/WASSAL/Zumtobel, decision of 13 April 2000, para. 14; and Case No. COMP/M.2917 – Wendel-KKR/Legrand, decision of 14 October 2002, paras. 19-20.

14 Case No. COMP/M.4735 – Osram/Sunny World, para. 22, Case No. IV/M.258 – CCIE/GTE, paras. 17-20, Case No. COMP/M.4509 – Philips/PLI, paras. 13 and 16.

15 Op cit, para. 14.

16 Op cit, para. 15.

17 This market data is according to the CSIL study on the European market for light fixtures. Although the market share figures relate to 2009, according to the notifying party, these figures did not change significantly in 2010.

18 Siteco is not active in customer/residential light fixtures.

19 At the same time, in Norway, the parties’ combined market share for fixtures in general does not exceed 15%.

20 This is not an affected market.

21 This is not an affected market.

22 On a worldwide level, Osram market share in the market for general purpose lamps amounts to [20-30%].If the product market definition for general purpose lamps is further segmented according to the lamp technology, Osram would have the following market shares in the EEA: [30-40%] for GLS, [40-50%] for HAL, [30-40%] for FL, [20- 30%]

23 The market shares of Osram/Siteco at national level do not exceed [10-20]% (for professional fixtures and indoor/outdoor segments thereof) except in Norway ([20-30]% in professional fixtures for outdoor) and Iceland ([10-20]% in professional fixtures for outdoor, though only Siteco is present).

24 It is noted that given that this is still a new technology, the ECGs for LED light fixtures are not as yet standardised.

25 The respondents to the market investigation consider that [a significant part] of their total sales in ECGs is made to fixture companies. The remaining percentage is directed to distributors.

26 The total sales of Osram in the ECGs market within the EEA are [20-30]%.

27 The market shares are based on the Parties’ estimates.