Commission, August 5, 2011, No M.6230

EUROPEAN COMMISSION

Judgment

SOLVAY/ RHODIA

Dear Sir/Madam,

Subject: Case No COMP/M.6230 – Solvay/ Rhodia

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041

1. On 30 June 2011, the European Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which the undertaking Solvay SA ("Solvay", Belgium) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of the undertaking Rhodia SA ("Rhodia", France) by means of a public bid.2 Solvay is designated hereinafter as the "notifying party", Solvay and Rhodia together as "the parties".

I. THE PARTIES

2. Solvay is the parent of a group of companies that are internationally active in the research, development, production, marketing and sale of chemicals and plastics. It is active worldwide, with a presence in 50 countries, notably in Asia, the Americas and the EEA.

3. Rhodia is an international company active in the development and production of specialty chemicals like solvents, intermediates and polymers.

II. THE OPERATION AND THE CONCENTRATION

4. On 4 April 2011, Solvay announced that it intended to make an offer to acquire the entire common share capital of Rhodia. The proposed offer was recommended unanimously by the Board of Directors of Rhodia and opened on 14 June 2011. If successful, Solvay will acquire sole control over Rhodia.

5. Therefore, the proposed transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

III. EU DIMENSION

6. The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 billion3 (Solvay: EUR 6,796 million, Rhodia EUR 5,226 million). The combined aggregate turnover of each of these undertakings is more than EUR 250 million in the EU (Solvay: EUR […]million Rhodia: EUR […] million). Neither of the undertakings concerned achieves more than two-thirds of its aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

IV. COMPETITIVE ASSESSMENT

1. Introduction

7. According to Solvay, the activities of the parties are complementary in nature. The proposed transaction should allow Solvay to continue its transformation process away from its traditional position as a chemical and pharmaceutical manufacturer towards a provider of speciality chemicals for a variety of applications with a stronger focus on emerging economies.4

8. In spite of the claimed complementarities of the parties’ respective activities, the proposed transaction results in a number of horizontal overlaps and vertical relationships, which are summarised in Table 1.

Table 1: Overview of major horizontal overlaps and vertical relationships –Form CO)5

Product | Horizontal Overlap | Vertical Relationship | |

Yes/No | Yes/No | Markets involved | |

Soda ash |

No |

Yes | Upstream to sodium silicates |

Sodium Silicates |

Yes |

Yes | Downstream to soda ash and upstream to precipitated silicas |

Precipitated Silicas |

No |

Yes | Downstream to sodium silicates |

Hydrogen Peroxide |

No |

Yes | Upstream to diphenols and amine oxide |

Diphenols |

No |

Yes | Downstream to hydrogen peroxide |

Amine Oxides |

No |

Yes | Downstream to hydrogen peroxide |

Organic Fluorinated Intermediate Chemicals |

Yes |

No |

-- |

Polyamides |

No |

Yes | Downstream to adipic acid and hexamethylene diamine |

2. Relevant Markets

2.1 Organic fluorinated intermediate chemicals (OFICs)

Relevant Product Market

9. Both Rhodia and Solvay are active in fluorochemicals, a variety of products derived from hydrofluoric acid. While Solvay is active in all areas of fluorochemicals, Rhodia only produces and sells particular aliphatic molecules, which belong to organic fluorinated intermediate chemicals (OFICs), a specific sub-group of organic fluorinated

chemicals.

10. The OFIC molecules on which both parties are active are trifluoroacetic acid (TFA) manufactured and supplied by Solvay and Rhodia; trifluoroacetic (acid) anhydride (TFAH) and trifluoroacetic acid ethylester (TFAEt), both manufactured by Solvay, whereas Rhodia uses a toll-manufacturer based in […] to have them produced; and trifluoroethyl alcohol (TFE) in which the parties are only active as traders without own production facilities. Furthermore, Solvay produces trifluoroacety chloride(TFAC), which is used as an input for the production of ethyl trifluoroacetoacetate (ETFAA). Rhodia has ETFAA toll-manufactured, using however a process that does not involve TFAC but TFAEt. The potential vertical relations between these three OFIC molecules (TFAC, TFAEt, ETFAA) will be examined in Section 3.1 below.

11. These molecules have different applications in a variety of sectors. TFA is used as a building block, solvent or catalyst for polymerisation and condensation reactions, in particular in the agrochemical industry. TFAH, TFAEt and TFE act as agents for different types of reactions and are used by the pharmaceutical industry.

12. In relation to the relevant product market definition, the notifying party refers to a previous Commission decision6, which distinguished between three types of fluorinated intermediate chemicals – organic, inorganic and polymers – ultimately leaving open the question whether each type represents a separate market.

13. The notifying party further submits that it would not be appropriate to consider the four molecules where the parties' activities overlap as separate products markets, because all of them are used to a large extent for the same purposes in end applications, namely as an active ingredient or an enhancer of another active ingredient. Moreover, supply-side substitutability prevails as all molecules can be produced on multi-purpose equipment.

14. The market investigation, while broadly confirming that OFICs are distinct from inorganic fluorinated intermediate chemicals or fluorinated intermediate polymers, has not generally been able to support Solvay's submission that these molecules can be considered as substitutes. Almost all customers argued that they could not replace TFA, TFAH, TFAEt or TFE with any other OFIC or substance because of their specific properties, which are required in the final product. Competitors responding to the investigation indicated that they rather used dedicated production lines and that switching would not be easy.

15. While the results of the investigation suggest that the relevant product markets are probably separate markets for TFA, TFAH, TFAEt and TFE, respectively, the question can ultimately be left open for the purposes of this decision as even under the narrowest market definition, i.e. by molecule, no competition concerns arise7.

Relevant Geographic Market

16. For the geographic scope, the notifying party argues that the market(s) for OFICs or alternatively for the respective molecules should be defined as worldwide in scope because of significant trade flows, low transport costs (less than [0-5]% of the selling price) and no regulatory barriers. Reference is also made to a previous decision8 where the Commission found strong indications that the market for fluorinated intermediate chemicals is worldwide, but ultimately left the geographic scope open.

17. Almost all responding customers argued that the market is worldwide in scope for the different molecules. Only one customer argued that, because of transport logistics and costs, alternative suppliers of TFA (and to a lesser extent of TFAEt) based in India, China or the US would not be suitable alternatives to Solvay and Rhodia, which are the only suppliers for TFA with manufacturing facilities within the EEA. Other customers based within the EEA – while generally expressing a preference for sourcing nearby – did not view transport costs or logistics as a barrier to imports and some already procure part of their needs from Asia or the US. Several customers also indicated that, in spite of transport costs, Asian suppliers would be able to sell at lower prices than the parties, as the cost base in Asia is significantly lower.

18. These qualitative findings have also been supported by a submission9 of the notifying party in which it details the transport costs necessary to ship TFA from Asia, in particular India and China, to the EEA. The notifying party estimates that transport costs in containers holding 18 tons of TFA amount to roughly EUR [0-5] per kg, a figure confirmed by respondents in the investigation. Finally, for TFAH and TFAEt, Rhodia is selling to EEA customers using a toll-manufacturer based in […], which further supports the ability of Asian suppliers to sell at competitive prices into the EEA.

19. Based on the above, it is therefore concluded that the relevant geographic market(s) for OFICs and the respective molecules TFA, TFAH, TFAEt and TFE are, for the purpose of the present decision, worldwide in scope.10

2.2 Hydrogen peroxide (H2O2)

Relevant Product Market

20. Solvay produces and supplies hydrogen peroxide (H2O2), while Rhodia purchases it for the production of diphenols and amine oxides.

21. According to the notifying party, H2O2 is a strong oxidizing agent supplied to the market in the form of aqueous solutions. The largest end market for H2O2 is in the pulp and paper industry where it is widely used to brighten, delignify and address environmental problems. H2O2 is also used by a wide range of industries and as a raw material for the production of other peroxygen products. The production of H2O2 is based on the reduction of oxygen by means of anthrahydroquinone, previously generated by the catalytic hydrogenation of quinone. H2O2 is then extracted with water and in a second step separated by fractional distillation from the water.

22. The notifying party considers that hydrogen peroxide forms a distinct product market, although it is subject to competitive pressures due to the availability of a wide range of alternative products for most applications. The notifying party also submits that H2O2 does not require to be further segmented. The large majority of the H2O2 market is constituted by standard grade H2O2. Since approximately [90-100]% of H2O2 purchased by Rhodia worldwide is used as input for the production of diphenols, for which Rhodia makes use of standard grade H2O2, the notifying party submits that the question as to whether separate markets for specialty grades of H2O2 exist can be left open.

23. In previous decisions11, the Commission considered a distinct market for H2O2. The market investigation in the present case confirmed that competitors and customers consider H2O2 as a separate product market. Furthermore, all competitors have indicated that a further segmentation between standard and specialty grades of H2O2 is not appropriate and most of them produce both grades. In addition, some competitors and customers consider that both standard grade and specialty grades of H2O2 may be suitable for the purpose of producing hydroquinone (HQ), catechol (PC) or amine oxides. In any event, given that no competition concerns arise regarding H2O2, it is not necessary to consider a further product market segmentation into standard and specialty grades. The Commission therefore considers that H2O2 constitutes a distinct product market for the purpose of this decision.

Relevant Geographic Market

24. The notifying party claims that the relevant geographic market for H2O2 is EEA-wide. Solvay points, in particular, to substantial trade between EEA Member States and to the fact that manufacturers and customers are both located throughout the EEA and supply customers and purchase from suppliers, respectively, located throughout the EEA. Furthermore, the notifying party indicates that imports from outside of the EEA are negligible and represent less than [0-5]% of EEA production capacity. Transportation costs account for between [10-20]% and [20-30]% of the selling price. The degree of concentration of the H2O2 (which is sold in liquid form) and the distance between the plant and the customer location contribute to determining transport costs, but the notifying party argues that these differences are not significant within the EEA.

25. The notifying party's submission finds support in the Commission decision Solvay/Montedison-Ausimont12, which concluded that the relevant geographic market for H2O2 was EEA-wide. The investigation in the present case confirmed this as almost all respondents to the Commission’s questionnaires defined the market as being EEA- wide. Furthermore, European producers are present all over Europe, with significant cross-border sales within the EEA. In conclusion, the Commission considers the relevant geographic market for H2O2 to be EEA-wide.

2.3 Amine oxides

Relevant Product Market

26. Amine oxides are surfactants used in cleaning products, in conjunction with other types of surfactants. The major applications are in hand dishwashing liquids, household cleaners and bleach cleaners. Amine oxides are prepared by oxidizing a tertiary amine with hydrogen peroxide. A number of different tertiary amines can be reacted, such as alkyl dimethyl amine or alkyl amidopropyldimethylamine. According to the notifying party, the reaction of a tertiary amine with hydrogen peroxide is a simple reaction not requiring any specialized equipment.

27. In previous decisions13, the Commission subdivided the surfactants sector into four relevant product markets, based on the ionic (electrical charge) properties in water of the different surfactant segments, which is a function of their composition and (indirectly) of the production process used: (i) anionic surfactants (negative charge); (ii) non-ionic surfactants (no charge); (iii) cationic surfactants (positive charge); and (iv) amphoteric surfactants (charge that is either positive or negative, depending on the pH of the solution).

28. Amine oxides are non-ionic surfactants, because the molecule has no formal charge. However, the notifying party submits that the performance profile of amine oxides is far from typical non-ionic surfactants such as alcohol ethoxylates and very close to amphoteric surfactants, notably betaines. Accordingly, the notifying party claims that customers would switch between amine oxides and betaines for the majority of end- applications. Furthermore, manufacturing processes would be similar and cost and time requirements to switch production would be minimal. Therefore, the notifying party submits that amine oxides could be either considered as a separate product market, or be included in a wider market together with amphoteric surfactants.

29. In the BASF/Cognis decision14, the Commission considered the possibility that various sub-segments of non-ionic surfactants could constitute separate product markets, given their apparent lack of demand-side substitutability, as well as different chemical and physical characteristics, performances and prices. Ultimately, the Commission left open the market definition, since no competition concerns arose under any possible market definition.

30. During the market investigation in the present case, competitors have confirmed that amine oxides are non-ionic surfactants, which could be considered close to amphoteric surfactants and notably betaines. However, none of the competitors' customers have recently switched between both products. In any event, there is no need to precisely define the relevant product market as no competition concerns would arise under any alternative definition, i.e. (i) amine oxides (the narrowest possible market definition), (ii) non-ionic surfactants, or (iii) amine oxides plus amphoteric surfactants.

Relevant Geographic Market

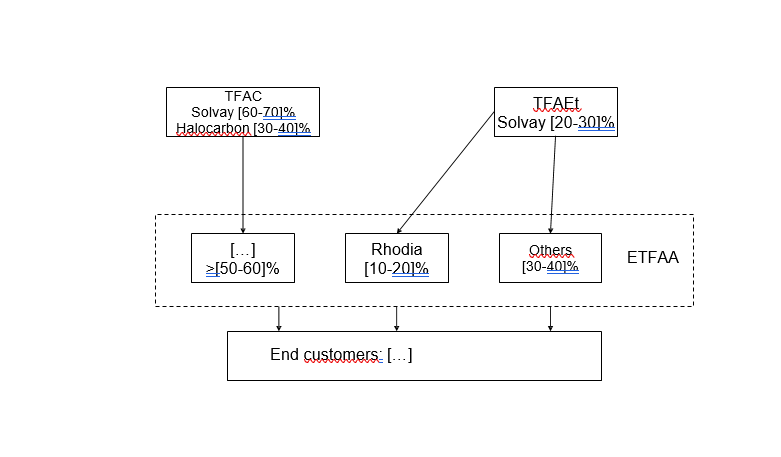

31. In recent decisions15, the Commission has left open the question whether the scope of the geographic markets for surfactants is EEA-wide or larger. The notifying party is also of the view that the geographic market for surfactants is at least EEA-wide in scope. Furthermore, Solvay submits that amine oxides have no distinctive peculiarities in terms of transport costs, barriers to trade or customers’ preferences regarding location of suppliers that would justify distinguishing the scope of the amine oxides geographic market from that of amphoteric or non-ionic surfactants.

32. The market investigation suggests that the market would rather be EEA-wide than larger. Indeed, competitors indicated that transport costs from outside the EEA constitute a significant barrier and that customers expect a quick delivery on short notice. However, for the purposes of this decision it can be left open whether the market is EEA wide or larger, since no competition concerns arise under any market definition.

2.4 Diphenols

Relevant Product Market

33. Diphenols are organic molecules characterized by the presence of two phenol groups in their chemical structure. Rhodia produces two types of diphenols: hydroquinone (HQ) and catechol (PC). HQ and PC are isomeric compounds16 that are jointly produced through the hydroxylation of phenol using H2O2. The main input is therefore phenol, which according to the notifying party covers [60-70]% of production costs. H2O2 accounts for approximately [10-20]%, the remaining [20-30]% being mainly attributed to energy costs.

34. The notifying party submits that although the end-applications for HQ and PC are somewhat different17, there is a certain degree of supply-side substitutability between these two types of diphenols. According to Solvay, HQ and PC are manufactured in the same plants through one and the same chemical reaction involving the use of phenol and H2O2 and the output ratio can be switched from one product to the other. Therefore, Solvay considers that HQ and PC may be viewed as part of a single product market.

35. The market investigation appears to confirm the parties' claim that HQ and PC are produced in the same plants. However, competitors’ replies suggest that it is not possible to change the output ratio from one product to the other. Furthermore, it appears that there is no demand-side substitutability regarding HQ and PC. The product market definition may however be left open since under any possible market definition no competition concerns would arise.

Relevant Geographic Market

36. The notifying party submits that the geographic scope of the HQ/PC market(s) is worldwide. Solvay argues that all main suppliers of HQ and PC are active on a global scale, transport costs are not sufficiently high to put obstacles to worldwide trade, and the price for both products is substantially uniform worldwide.

37. There are indications in the market investigation that diphenols are high value products and transport costs are therefore not a barrier to worldwide trade, which suggests that the market could be worldwide in scope for both HQ and PC. In any event, the precise delineation of the relevant geographic market may be left open, as no competition concerns appear under any plausible alternative.

2.5 Polyamides

Relevant Product Market

38. Solvay and Rhodia are both active in the production and supply of polyamides.18 However, while Solvay is active in high-performance polyamides, in particular polyphthalamide (PPA) and specialty high-performance polyarylamide (PARA), Rhodia supplies medium-performance polyamides, i.e. polyamide 6 (PA6) and polyamide 6.6 (PA6.6).

39. The above materials are used in different applications. PPA is a high performance material used in, for example, automotive and truck parts, appliance parts, electrical and electronics. PARA is a specialty high-performance nylon used for structural applications where aesthetics are an important consideration since it enables to obtain a smooth, resin-rich surface. PARA is used, for instance, in sunroof brackets, louvers and/or electronic connectors. PA6 and PA6.6 are used, among others, in industrial yarns, textile (carpets), cable ties, switches, timers, plugs and door handles.

40. The parties claim, in that regard, that the polyamides Solvay produces (PPA and PARA) belong to different product markets than the polyamides Rhodia produces (PA6 and PA6.6) since the product characteristics, properties and the end-applications thereof vary significantly.

41. In this respect, the parties differentiate between three categories of polyamides: high- performance polyamides (PPA, PA9T and PA4.6), specialty high performance polyamides (PARA, 53G and GVS) and medium-performance polyamides (PA.6 and PA6.6). The parties put forward that these categories contain materials that have similar thermal, chemical resistance and mechanical properties. Therefore, in the view of the parties, the materials placed within each above category are to a large extent substitutable.

42. In particular, the parties claim demand-side substitutability between PPA, PA9T and/or PA4.6. The parties provide examples of substitution between these polyamides by a certain amount of customers in applications such as mobile electronics (connector parts), automotive electronics (bobbins) and automotives (EGR valves and fuel filer tubes).

43. The parties also argue demand-side substitutability between different materials within specialty high-performance polyamides (PARA, 53G and GVS) due to their similar temperature and density properties. The parties provide a number of applications where these materials have been substituted by their customers. These applications are: steering column lock barrels, rear crankshaft, cell phone components and break parts.

44. Furthermore, the parties argue that the above groups of high-performance/high- performance specialty polyamides are different from medium-performance polyamides, since the latter are characterised by lower glass transition temperature, melting points and deflection temperature.

45. In this respect, the parties explain that the prices of high-performance polyamides (including PPA) and specialty high-performance polyamides (including PARA) are almost [70-80]% higher than the prices of medium-performance polyamides PA6 and PA6.6, produced by Rhodia.

46. The market investigation confirmed to a large extent the parties' claims with regard to the lack of demand-side substitutability between polyamides such as PPA/PARA, on the one hand, and polyamides such as PA6 and PA6.6, on the other hand. The respondents indicated that these polyamides have different characteristics, in particular with regards to temperature resistance and strength. Therefore, generally the above-referred groups of polyamides are used in different applications.

47. In the market investigation, a limited number of respondents claimed, though, that in some applications PPA could be replaced by some medium-performance polyamides, in particular PA6.6. However the follow-up investigation confirmed that this substitutability happens only one-way and for a limited number of applications. In particular, it takes place where the product specifications allow the replacement of more expensive PPA by cheaper and less resistant PA6.6. The consistently higher price of PPA confirms that the price of this product is not constrained by that PA6.6, since this cheaper material cannot replace PPA for the generality of applications.

48. On the basis of the above, it can be concluded that the polyamides produced by Solvay (PPA and PARA) belong to different product markets than the polyamides produced by Rhodia (PA6 and PA6.6). Therefore, no horizontal overlaps arise in this respect as a result of the proposed transaction. The exact product market definition of each category of polyamides, in particular whether further segmentations are required according to the different materials involved, can be left open for the purposes of this decision since the transaction does not lead to competition concerns irrespective of the product market definition ultimately adopted.

Relevant Geographic Market

49. The notifying party suggests that the geographic market for the different polyamides is worldwide as transport costs are low, customers source on a global scale and suppliers usually have a single plant supplying to all geographic areas.

50. The market investigation confirmed that the market for the different polymers is at least EEA-wide in scope. While the majority of respondents source polyamides on a worldwide basis, some respondents indicated a narrower sourcing area, limited to the EEA. The market investigation also indicated that transport costs represent a small fraction of the overall price for the above polyamides, that customers tend to source on a global or EEA-wide scale and that producers of polyamides usually supply a number of diverse geographic areas.

51. Based on the above, it is therefore concluded that the relevant geographic market for the different polyamides of the parties, in particular PPA, PARA, PA6 and PA6.6, is at least EEA-wide in scope.

2.6 Adipic acid (AA) and hexamethylene diamine (HMD)

Relevant product market

52. Rhodia is active in the production and supply of adipic acid (AA) and hexamethylene diamine (HMD). AA and HMD constitute inputs to Solvay's production of polyamides.

53. AA is a monomer used, in particular, for the production of different polyamides such as PPA, PARA and PA6.6. AA is also used for the production of polyurethane, flexible foam, plasticizers, TPU thermoplastic and synthetic leather.

54. HMD is an aliphatic diamine, which is used in particular in the production of "nylon salt"19 and of a number of polyamides, including PPA. HMD is also used in a number of other applications such as plastic additives, adhesives, inks, coatings, water treatment and construction.

55. The parties refer to a previous decision where the Commission stated that AA and HMD constitute an input to PA6.620 and submit that each of AA and HMD shall constitute separate relevant product markets. In the market investigation, respondents confirmed that AA and HMD constitute inputs to different substances, such as for instance polyamides PPA, PARA and PA 6.6. The respondents did not point to any possible further segmentation of the materials in question.

56. For the purpose of this decision it is however not necessary to delineate the exact product market definition for AA and HMD since the transaction does not lead to competition concerns in any of the possible market delineations.

Relevant geographic market

57. The parties submit that the relevant geographic market for AA and HMD is global since transport costs are low, customers source AA and HMD on a global scale and suppliers' plants usually serve all geographic areas.

58. In previous decisions, the Commission did not define the geographic market for AA and/or HMD. The respondents to the market investigation in the present case indicated that in principle they source these substances on an EEA or worldwide basis.

59. On the basis of the above, it can be concluded that, for the purpose of the assessment of this transaction, the geographic scope of the markets for AA and HMD is to be considered as at least EEA-wide.

2.7 Soda ash

Relevant Product Market

60. Solvay is active in the production and supply of soda ash, which is used by Rhodia as an input to manufacture sodium silicates.

61. Soda ash (also known as sodium carbonate) is an alkaline chemical commodity that is mainly used as a raw material in the manufacture of glass, but also in the chemical industry for making detergents and in metallurgy. It is produced from common salt and limestone. Soda ash is available in two forms: light or dense.

62. In a previous decision21, the Commission left the exact product market definition for soda ash open. The notifying party submits that soda ash should be viewed as a single product market because of supply and demand-side substitutability.

63. In the market investigation, there were indications that it is possible to switch between the production of light and dense soda ash without any significant costs or delay. However, the market investigation did not generally confirm the submission of the notifying party regarding demand-side substitutability. Indeed, customers claimed that they only use light soda for their production of sodium silicates and that it would be difficult to change to dense soda due either to logistical reasons or switching costs.

64. However the question whether a further distinction of soda ash into light and dense is required can be left open, as the notified operation would not give rise to any competition concern even under the narrowest market definition.

Relevant Geographic Market

65. As regards the relevant geographic scope, the notifying party argues that the market for soda ash should be defined as EEA-wide. The Commission has so far considered the soda ash market to be national or wider, but left the question ultimately open22. The market investigation in the present case did not allow reaching a final conclusion in this respect. A competitor of Solvay considered that the market would be within a radius of 500 kilometres from the production site and that transport costs are EUR 10 per 100 km. While one customer indicated that there are price differences of 10-20% between different Member States due to transport costs, other customers argued that the market is EEA-wide or broader.

66. In any event, the precise scope of the geographic market can be left open for the purpose of this decision, as it would not significantly affect the competitive assessment.

2.8 Sodium silicates

Relevant Product Market

67. Both Solvay and Rhodia are active in the supply of sodium silicates in the EEA.

68. Sodium silicate is a chemical combination of sodium oxide (Na2O), silica (SiO2) and, in case of liquid sodium silicate, water. Sodium silicate is supplied in a wide range of grades (differentiated, for example, by purity, alkalinity and solid content) and in various product forms (aqueous, lump glass, metasilicate, milled glass, powders and granules (spray dried). It is used for the production of silicas and in the manufacture of detergents, pulp/paper and other industrial applications.

69. In line with the Commission's findings in M.4927- Caryle/Ineos/JV, the notifying party submits that sodium silicate constitutes the relevant product market. This was confirmed by the market investigation in the present case, as all competitors claimed that they produce different types of sodium silicates and they can easily switch between the production of different grades or forms depending upon customers demand. Therefore, for the purpose of the present decision, the relevant product market is represented by sodium silicate.

Relevant Geographic Market

70. The notifying party also agrees with the Commission's conclusion in M.4927- Carlyle/Ineos/JV that the relevant geographic scope of this product market is EEA-wide. The present market investigation generally confirmed this delineation. While some competitors argued that the scope of the geographic of the sodium silicate market for precipitated silica is national due to transport costs, they also claimed that there are not significant price differences in sodium silicates between different Member States within the EEA. Moreover, most of the customers purchase sodium silicates on the merchant market across the EEA. Therefore, for the purpose of the present decision, the geographic market is the EEA.

2.9 Precipitated silicates

Relevant Product Market

71. Rhodia produces precipitated silicas in the EEA, America and Asia.

72. Precipitated silica is produced by neutralising a solution of sodium silicate usually with a sulphuric acid. It is principally used in the manufacture of rubber and for food, healthcare and personal/oral care products.

73. In a previous case23 the Commission classified silicas according to their method of preparation into (i) precipitated silica; (ii) silica gel; and (iii) silica sol (colloidal silica) and concluded that, from a demand and supply-side perspective, the three forms of silicas form separate product markets. The notifying party and competitors agree in general to this finding. Although some competitors pointed that there are some minor segments of the overall market where those forms can be used almost interchangeably, the replies also indicate that there are still differences in performance, quality and cost. Therefore, for the purpose of the present decision, the product market is precipitated silica.

Relevant Geographic Market

74. In line with a previous Commission's decision concluding that the geographic scope of the silica gel market was at least EEA-wide,24 the notifying party claims that the same relevant geographic delineation shall apply to the market for precipitated silicates, since around [80-90]% of the European sales are manufactured within Europe and the prices are homogenous across the EEA.

75. The Commission’s investigation in the present case confirmed the parties’ proposed geographic market definition. Competitors have indicated that that the geographic scope of the market could be either EEA or worldwide, but, on the other hand, their replies suggest that there are significant price differences between the EEA and the rest of the world. Therefore, the precise scope of the geographic market can be left open for the purpose of this decision, as it would not significantly affect the competitive assessment.

3. Competitive Assessment

3.1 Organic fluorinated intermediate chemicals (OFICs)

76. Concerning the impact of the proposed transaction on competition (horizontal effects), on an overall market for all OFICs, the combined share of the parties is low and with a worldwide [5-10]% market share does not result in an affected market. If the relevant product markets were to be defined by molecule, the proposed transaction would result in affected markets for TFA ([20-30]% combined market share), TFAH ([50-60]% combined market share) and TFAEt ([20-30]% combined market share). For TFA as well as TFAEt, the combined market share is below 25%, the level under which, in the absence of other factors, the Commission normally presumes an absence of anti-competitive effects.25 Only for TFAH is the combined market share relatively high, namely of [50-60]%, with an increment of [20-30]% – see Table 2.

Table 2: Market Shares of Rhodia and Solvay for OFIC molecules – worldwide market – Form CO

2010 in % |

Solvay |

Rhodia |

Combined |

Market size in EUR million |

TFA | [0-5] | [10-20] | [20-30] | [30-40] |

TFAH | [30-40] | [20-30] | [50-60] | [5-10] |

TFAEt | [20-30] | [0-5] | [20-30[ | [5-10] |

TFE | [0-5] | [10-20] | [10-20] | [20-30] |

77. The notifying party submits that, in spite of a combined market share of [50-60]% in TFAH, the proposed transaction does not result in any competition concerns because customers would have sufficient supply alternatives for this molecule. In particular, Halcocarbon (USA) with a market share of [20-30]%, Shunkai ([10-20]% market share) and Jinan ([5-10]% market share) will be able to exert a competitive constraint post- transaction.

78. Indeed, the wide majority of responding customers expects no impact on their business and indicate that several suppliers in addition to the parties are available and refer to Halocarbon, SRF and Navin (India) and several Chinese suppliers like Shunkai and Jinan as potential alternatives. They also indicated that switching to another supplier is not difficult since TFAH is a commodity product with no particular differentiation. In that respect, competitors responding to the investigation confirmed that spare capacity for the different OFIC molecules, in particular TFAH, is available.

79. Moreover, some customers indicated that in the coming years additional suppliers might enter the market, in particular in China. Finally, Rhodia is currently supplying TFAH by using a toll-manufacturer in […]. […] thus existing toll-manufacturers could enter the market themselves in case of a price increase post-transaction.

80. In conclusion, the proposed transaction does not result in any horizontal concerns for the four molecules in question.

81. In relation to potential vertical effects, market respondents pointed at a vertical link between trifluoroacety chloride (TFAC) and ethyl trifluoroacetoacetate (ETFAA), which are both OFIC molecules. The latter is a product used as a building block in the synthesis of agricultural and pharmaceutically active intermediates. Respondents explained that Solvay is currently supplying TFAC to ETFAA producers, while Rhodia is a competitor in ETFAA with a limited market share between [10-20]%. ETFAA can also be produced using TFAEt as an input. It is thus necessary to examine whether, post- transaction, Solvay might have the incentive to stop supplying these customers to allow Rhodia to gain market share downstream.

82. In response, the notifying party submitted more detailed information on these potential vertical links – see Figure 1

Figure 1: Vertical Relationships between TFAC, TFAEt and ETFAA.

83. According to the parties, two possibilities exist indeed to produce ETFAA: to use TFAC and Ketene or, alternatively, to use TFAEt. Solvay is active in both upstream marketswith respective market shares of [60-70]% in TFAC and [20-30]% in TFAEt. Solvay submits that the only other supplier of TFAC is Halocarbon. Rhodia is using a […] toll- manufacturer for ETFAA, using TFAEt as an input, and sells it on to […]: these sales […] resulted in a turnover of EUR [1-10] million.

84. Solvay submits that it has neither the ability nor the incentive to engage into input foreclosure post-transaction. First, […], active in ETFAA using TFAC, could source this input from Halocarbon or alternatively start manufacturing ETFAA from TFAEt, which following Solvay is an easy to implement technology which costs around EUR [100,000-500,00] and takes a few weeks to be set up. Second, Solvay has only a small share in the market for TFAEt ([20-30]%) and does currently not supply any ETFAA producers with it. In consequence, all ETFAA manufacturers can continue supplying to the market and could even expand output in case of a reduction in the supply of ETFAA produced using TFAC as an input. Third, Solvay does not have the incentive to engage in such behaviour as it would lose its […] client for TFAC and increase its average production costs for the TFAC used captively. Solvay estimates that this margin loss would amount to EUR […] million. To be compensated for it downstream, Solvay estimates that Rhodia would have to increase its sales of ETFAA by [200-300]% to [400-500]%, which is more than unlikely in Solvay's view, notably as […] could revert to the other technology and that, even if […] were to lose sales, other competitors would capture such sales. Finally, Solvay claims that the transaction will not result either in customer foreclosure regarding TFAC and/or TFAEt for the production of ETFAA because of Rhodia's limited market share on this market.

85. On the basis of the information received, it can be concluded that Solvay post- transaction is not likely to engage in an input foreclose of ETFAA manufacturers because: (i) alternative suppliers of TFAC like Halocarbon or a different production technology using TFAEt (for which alternative suppliers to Solvay also exist) are available; (ii) there is a lack of incentive given that Rhodia has not sufficient market size downstream to be able to capture lost sales by competitors to such an extent to make an input foreclosure strategy profitable; and (iii) other competitors not using TFAC as an input may supply ETFAA to end-customers, thus making a harm for the latter unlikely to occur. Similarly, given notably that Rhodia represents a small share of demand of TFAEt (and does not source TFAC at all) for the production of ETFAA, the transaction is not liable to result in customer foreclosure in these markets.

86. Therefore, the proposed transaction does not raise serious doubts with respect to OFICs or the respective molecules TFA, TFAH, TFAEt or TFE, or with respect to the potential vertical links between TFAC/TFAEt and ETFAA.

3.2 Hydrogen peroxide (H2O2) and amine oxides

87. Rhodia currently purchases the whole of its H2O2 requirements for the production of amine oxides in the EEA from Solvay. At the EEA level, Solvay has a market share of approximately [20-30]% for H2O2. Thus, although Rhodia’s market shares in the EEA for amine oxides under all alternative product market definitions are below 25%, this vertical relationship gives rise to an affected market.

88. Solvay submits that it lacks the ability or the incentive to engage into customer or input foreclosure. Although it is the market leader for H2O2 in the EEA, several sizeable competitors with available capacity could supply the market in case of input foreclosure. Moreover, Rhodia represents a very small share of demand on the merchant market for H2O2.

89. In 2010, Solvay sold approximately [100-500] kt of H2O2 on the merchant market in the EEA resulting, as indicated, in a market share of [20-30]%. It faces indeed significant competition from producers like Evonik ([10-20]% market share), Akzo Nobel ([10- 20]% market share), Arkema ([10-20[% market share) or Kemira ([10-20]% market share).

90. Rhodia had a market share in amine oxides of [5-10]% on the EEA and [0-5]% worldwide in 2010.26 In that year, Rhodia procured [100-500] tonnes of H2O2 for amine oxides (and [1-10] kt for diphenols) in the EEA.27 This was equivalent to less than [0- 5]% of EEA overall demand of H2O2. Rhodia is not, thus, a significant purchaser of H2O2.

91. Furthermore, the wide majority of responding competitors and customers has confirmed that they expect no effects on their business or any impact on competition as a result of the acquisition of Rhodia by Solvay.

92. Therefore, the proposed transaction does not raise any serious doubts for H2O2 and amine oxides.

3.3 Hydrogen peroxide (H2O2) and diphenols

93. H2O2 is also used as an input for Rhodia's production of diphenols. At the EEA level, Solvay has a market share of approximately [20-30]% for H2O2, as previously noted. Rhodia’s market shares in the EEA and worldwide markets for PC and HQ are also above 25% under any possibly market definition. Hence, this vertical relationship gives rise as well to an affected market.

94. In particular, Rhodia's market share in diphenols in 2010 on an EEA-wide market was [50-60]% for HQ,[80-90]% for PC and [50-60]% in a combined market for HQ and PC.28 Other competitors are Mitsui, Eastman and Borregaard.

95. Solvay argues however that it will have no ability or incentive to foreclose competitors. First, sizeable competitors exist in the supply of H2O2, who could immediately step in case of an attempt of input foreclosure. Second, Rhodia's requirement of H2O2 is small compared to the overall size of the market, so that suppliers of H2O2 could easily find new customers for their products.

96. Indeed, diphenols represent a very small share of demand for H2O2: Rhodia procured only [1-10] kt of H2O2 for diphenols in the EEA, which, together with its demand for H2O2 for the production of amine oxides, is equivalent to less than [0-5]% of EEA demand. As indicated, Rhodia is thus not a significant customer for H2O2.

97. The market investigation has confirmed that competitors and customers in the markets for H2O2, HQ and PC expect no effects on their businesses. Respondents have indicated that there are alternative H2O2 suppliers as well as spare capacity. H2O2 competitors have also confirmed that, given Rhodia's limited purchases of H2O2, the transaction would have no significant impact on the market.

98. Therefore, no anticompetitive vertical concerns seem to arise from the transaction in these markets.

3.4 PA6.6 and PARA (Kalix)

99. As indicated above, Rhodia produces PA6.6. Solvay purchases PA6.6 as an additive to produce a newly developed sub-brand of PARA, called Kalix, which is marketed specifically for to the mobile electronics market.

100. Under the narrowest hypothetical product market definition, i.e. encompassing only a specific type of polyamide, Rhodia's market shares in PA6.6 are [10-20] % at the worldwide level and [20-30] % in the EEA. The main competitors of Rhodia for the supply of PA6.6 are Invista (with [20-30]% worldwide and [40-50]% EEA), Ascend ([20-30] % worldwide, [10-20]% EEA-wide), Radici ([5-10]% worldwide and [10- 20]% EEA-wide) and DuPont ([0-5]% worldwide and [0-5]% EEA-wide).

101. Solvay's market shares in a hypothetical market encompassing only PARA would amount to [20-30]% in the world and [80-90]% in the EEA. The competitor of Solvay in PARA is Mitsubishi Gas Chemical, which has market shares of [70-80]% on a worldwide level and [20-30]% in the EEA. On a wider product market encompassing specialty high-performance polyamides, such as 53G produced by DuPont and/or GVS produced by Ems Chemie, Solvay's market shares would be [10-20]% worldwide and [50-60]% in the EEA, respectively.

102. Solvay purchases however only small amounts of PA6.6. For instance, in 2010 Solvay purchased [1,000-5,000] tonnes of PA6.6 from Radici and DuPont for a value of approximately EUR [1-10] million, which represents less than [0-5]% of the worldwide sales of PA6.6 and approximately [0-5]% in the EEA.29

103. As explained, the market shares of Rhodia worldwide and in the EEA for PA6.6 are below 25%, and Rhodia faces a number of strong competitors producing this polyamide. The merged entity would therefore not have the ability to foreclose access to PA6.6 post-transaction, since in case Rhodia would stop supplying its current customers, these would simply turn to alternative producers of PA6.6, such as Invista, Ascend, Radici and DuPont. Moreover, the main competitor of the merged entity downstream, Mitsubishi Gas Chemical, does not use PA6.6 for the production of its polyamide PARA, which reduces the merged entity's incentive to foreclose access to PA6.6.

104. In this regard, the market investigation confirmed the lack of competitive concerns with regards to the supply of PA6.6 and also the presence of alternative suppliers of this polyamide, such as DuPont and Radici.

105. The market investigation did not reveal concerns with regards to customer foreclosure for PA6.6 either. Solvay is not a major customer of PA6.6, since its demand of this polyamide is not significant compared to the size of the market for this polyamide. Therefore, even if Solvay would direct all PA6.6 demand to Rhodia post-transaction, the merged entity would not have the ability to foreclose competitors active in PA6.6 from access to a sufficient customer base.

106. Therefore, no serious doubts with respect to this vertical relationship are likely to arise from the transaction in these markets.

3.5 Adipic acid (AA) and PPA/PARA

107. Rhodia is active in adipic acid (AA) which is used as an input in Solvay's production of PPA and PARA.

108. Rhodia's market shares for AA are [10-20]% worldwide and [10-20]% in the EEA. Rhodia faces a number of strong competitors for the supply of AA such as Invista (with market shares of [10-20]% worldwide and [10-20]% in the EEA) or BASF ([10- 20]% worldwide and [40-50]% in the EEA). On a broader market encompassing the AA and the HMD, the market shares are even lower.

109. On a hypothetical market encompassing only polyamide PPA, Solvay's market shares are [20-30]% worldwide and [20-30]% in the EEA. The main competitors of Solvay for PPA would be Ems Chemie ([40-50]% worldwide and [60-70]% in the EEA) and DuPont ([20-30]% worldwide and [10-20] % in the EEA). On a broader market, i.e. for high-performance polyamides30, Solvay's market shares would be [10-20]% worldwide and [10-20]% in the EEA.

110. As explained above, Solvay's market shares in a hypothetical market encompassing only polyamide PARA would amount to [20-30]% worldwide and [80-90]% in the EEA. Solvay would face Mitsubishi Gas Chemical as main competitor ([70-80]% worldwide and [20-30]% in the EEA). On a broader product market encompassing specialty high-performance polyamides, Solvay's market shares would be [10-20]% worldwide and 50% in the EEA, respectively.

111. Solvay's sources however only small amounts of AA. In 2010, its total requirements of this material amounted to [1,000-5,000] tonnes which, according to the parties, represents less than [0-5]% of the total AA volumes sold on the merchant market worldwide and approximately [0-5]% of the overall volumes sold on the merchant market in the EEA.

112. The transaction shall not give rise, thus, to input foreclosure since Rhodia's market share upstream is not significant and, in any event, alternative AA suppliers exist such as Invista or BASF. The existence of these suppliers and the availability of AA post- transaction have been confirmed by respondents to the market investigation.

113. The transaction shall also not lead to customer foreclosure since the volumes sourced by Solvay on the market for AA are insignificant. The market investigation did not reveal concerns in this regard either.

114. On the basis of the above it is concluded that the transaction is not likely to result in input and/or customer foreclosure in these markets.

3.6 Hexamethylene diamine (HMD) and PPA

115. Rhodia is active in hexamethylene diamine (HMD), which is used as an input in Solvay's production of PPA.

116. Rhodia's market shares on HMD are [10-20]% worldwide and [20-30]% in the EEA. Rhodia faces the following competitors on the HMD market: Invista ([50-60]% worldwide and [60-70]% EEA-wide) and BASF ([5-10]% worldwide and [10-20]% EEA-wide). On a broader market encompassing the AA and the HMD, the market shares are even lower.

117. As listed above, Solvay has market shares of [20-30]% worldwide and [20-30]% EEA- wide in the production of PPA. Solvay's main competitors for PPA are Ems Chemie and DuPont. On a wider market, i.e. high-performance polyamides,31 Solvay's market shares are [10-20]% worldwide and [10-20]% in the EEA.

118. Solvay's requirements of HMD for use in the production of PPA represented [0-5]% of total worldwide sales of HMD and [5-10]% of total EEA sales in terms of volume. Currently Solvay sources its HMD requirements from Rhodia's competitor […].

119. The parties submit that the transaction will not result in input foreclosure with regards to HMD since Rhodia's market shares with regards to this material are not high and it faces a number of strong competitors. Therefore, according to the parties, the merged will not have sufficient market power upstream regarding HMD to be able to foreclose its competitors downstream on the market for PPA.

120. While, during the market investigation, some concerns have been raised with regards to a perceived general shortage of HMD on the market and the possibility for the merged entity to restrict access to this product post-transaction, respondents have generally indicated a number of alternative suppliers for HMD, such as Invista, Ascend, BASF, and Asahi, active in the EEA and/or outside the EEA. Some respondents also mentioned the possibility to source HMD on a worldwide basis.

121. Overall, the merged entity does not seem to be able to foreclose its competitors downstream since it does not hold a significant market power on the upstream market for HMD and post-transaction there would still be a number of large HMD suppliers. Furthermore, in case Solvay would redirect its purchases of HMD from […], its current supplier, there would be a spare amount of HMD available on the market, which could be redirected to Solvay's competitors.

122. As regards customer foreclosure, the merged entity will not have the ability to successfully engage in such a strategy with respect to Rhodia's competitors in HMD. This is because the requirements of Solvay for HMD are relatively low and therefore there would be no foreclosure to a sufficient customer base to actual or potential rivals to Rhodia upstream. In that respect, no concerns with regards to customer foreclosure have been raised in the market investigation.

123. Therefore, no serious doubts with respect to this vertical relationship are likely to arise from the transaction in these markets.

3.7 Soda ash and sodium silicates

124. Solvay is active in the production and supply of soda ash, which is used by Rhodia as an input to manufacture sodium silicates.

125. Solvay's market share in the EEA for soda ash is [30-40]%, with less than [0-5]% of its sales going to producers of sodium silicates. Competitors are Ciech ([20-30]%), Tata ([10-20]%), Eti Soda ([5-10]%), Sisecam ([5-10]%) and Novacarb ([5-10]%)32.

126. Rhodia produces sodium silicates as a raw material for use in precipitated silicas at its plant in Livorno in Italy. In addition, Rhodia sold approximately [1,000-10,000] tonnes of sodium silicates on the merchant market for the first time in 2010, giving rise to revenues of approximately €[0-5] million. Rhodia estimates that its market share is less than [0-5]% of total volumes sold on the merchant market in the EEA

127. In turn, Rhodia's purchases of soda ash for the production of sodium silicates in the EEA in 2010 ([1-100] kt) represent less than [0-5]% of the total EEA sales of soda ash.

128. Solvay submits that, based on this market structure and the presence of alternative suppliers of soda ash with sufficient spare capacity, it lacks the incentive to engage into input foreclosure. In addition, Solvay claims that it also lacks the incentive to foreclosure other competitors from access to Rhodia, as Rhodia’s total soda ash requirements represent only [0-5]% of Solvay’s European soda ash sales by volume and only [0-5]% of the total sales of soda ash in Europe. Even if post-merger, Rhodia would obtain all of its supplies of soda ash from Solvay, this would not be a sufficiently important drop in demand to result in customer foreclosure of other soda ash suppliers.

129. On the basis of the information received during the market investigation, it can be concluded that post-transaction Solvay would not engage in input or customer foreclose because (i) Rhodia is too small a customer for soda ash and does not constitute a significant share of demand thereof, (ii) all customers and competitors confirmed that there is sufficient spare capacity for soda ash in the EEA and (iii) all customers stated that they will be able to find alternative suppliers of soda ash for their sodium silicates production in case Solvay stops supplying them.

130. Therefore, the proposed transaction does not result in any serious doubts with respect to the above vertical relationship.

3.8 Sodium silicates

131. Solvay and Rhodia are both active in the supply of sodium silicates in the EEA.

132. The combined merchant market share of Solvay and Rhodia will amount however to less than [0-5]% in the EEA, with an increment of less than [0-5]%.33 The combined market share of the parties is thus well below 25%, the level under which, in the absence of other factors, the Commission normally presumes that no anti-competitive effects arise from a transaction.34

133. Indeed, the majority of the competitors indicated that the transaction will not have an effect on the market for sodium silicate and all customers considered that there is sufficient spare capacity for sodium silicates in the EEA and they do not have any difficulties to find alternative suppliers of sodium silicates.

134. In conclusion, the proposed transaction does not raise serious doubts with respect to this horizontal overlap with respect to this market.

3.9 Sodium silicates and precipitated silicas

135. In 2010, Solvay sold approximately [10-20] kt (EUR [1-10] million) of sodium silicates on the merchant market in the EEA resulting in a market share of less than [0- 5]%.35

136. In 2010 Rhodia procured [10-50] kt of sodium silicates, equivalent to less than [5- 10]% of the EEA sales. In precipitated silicas, Rhodia had a market share of [30-40]% on the EEA (and [20-30]% worldwide) achieving a turnover of EUR [100-200] million.

137. Solvay submits that based on these market shares and the presence of alternative suppliers of sodium silicates, it lacks the ability to engage into customer or input foreclosure. Solvay is hardly active on the market for sodium silicates and has not sufficient capacity to supply Rhodia's current demand, which is already limited compared to the overall size of the market.

138. The market investigation generally confirmed the submissions of the parties and did not reveal concerns about this vertical relation. All customers of sodium silicates considered that there is sufficient spare capacity in the EEA for sodium silicates and the majority of them have a multi-sourcing policy to purchase sodium silicates at least from two suppliers. Moreover, Rhodia’s share of demand of sodium silicates is not particularly significant.

139. On this basis, it can be concluded that the proposed transaction does not result in any serious doubts with respect to the vertical relationship between these markets.

3.10 Conglomerate effects

140. Solvay and Rhodia sell a number of products to the same group of customers within the same industry, in particular polyamides to the automotive industry. Currently, some of these customers are sourcing different types of polyamides from both suppliers.

141. The parties submit however that no conglomerate issues will arise post-transaction in any industry sectors because the products concerned are not complementary and are not used for the same end-use. Moreover, the set of common customers is limited and other suppliers are available with a similar product portfolio.

142. The market investigation generally confirms the parties' claims with regard to polyamides. Customers explained that the polyamides offered by the parties are designed for different, independent end-use applications for which they undergo a specific approval process. Respondents did not indicate that the use of the polyamide of one party would imply the use of another polyamide from the other party and no customer raised concerns in relation to possible conglomerate effects.

143. Therefore, it can be concluded that the proposed transaction will not result in any serious doubts with respect to its possible conglomerate effects.

V. CONCLUSION

144. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the

Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of

"Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will

be used throughout this decision.

2 Publication in the Official Journal of the European Union No C 200, 08.07.2011, p.12.

3 Turnover calculated in accordance with Article 5(1) of the Merger Regulation and the Commission

Consolidated Jurisdictional Notice (OJ C95, 16.04.2008, p1).

4 See presentation to investors dated 4 April 2011 at

http://www.solvay.com/EN/NewsPress/Documents/2011/20110404_Rhodia_Analyst_EN.pdf.

5 In addition, there are minor vertical relationships addressed in the Form CO, namely hydrogen fluoride

and perchloroethylene with organic fluorinated intermediate chemicals, epichlorohydrin and amphoteric

surfactants and biocides. In the case of the Organic Fluorinated Intermediate Chemicals (OFIC), besides

the horizontal overlaps concerning some molecules (namely TFA, TFAH, TFAEt and TFE), respondents

to the market investigation pointed as well at a vertical link between some molecules, namely TFAC and

TFAEt (produced by Solvay), on the one hand, and ETFAA (produced by Rhodia using a process that

involves TFAEt but not TFAC), on the other hand. Furthermore, it should be noted that, while Solvay and

Rhodia are both active in the production and supply of different polyamides, Solvay produces high-

performance polyamides and Rhodia supplies medium-performance polyamides. Finally, it is observed

that Rhodia produces polyamide PA6.6, which is used by Solvay as an additive to produce a newly

developed sub-brand of polyamide PARA.

6 Case COMP/JV.42 - Asahi Glass / Mitsubishi / F2 Chemicals; European Commission decision of 21

March 2000.

7 Similarly, the question of whether separate markets exist for TFAC and ETFAA (see paragraph 10 above)

can be left open for the purposes of the assessment of the present case.

8 Case COMP/JV.42 - Asahi Glass / Mitsubishi / F2 Chemicals; European Commission decision of 21

March 2000.

9 "Solvay/Rhodia: Quantitative Evidence on Geographic Scope of the OFIC Market", 19 July 2011.

10 The same conclusion, namely the existence of a worldwide market, and for the same reasons indicated

above, is valid for potential separate product markets for TFAC and ETFAA.

11 Case IV/M.197 - Solvay/Laporte, European Commission decision of 30 April 1992, paragraph 25, and

Case COMP/M.2690 - Solvay/Montedison-Ausimont, European Commission decision of 9 April 2002,

paragraph 70.

12 Case COMP/M.2690 - Solvay/Montedison-Ausimont, European Commission decision of 9 April 2002,

paragraph 73.

13 Case COMP/M.1517 - Rhodia Donau Chemie/Albright & Wilson, European Commission decision of 13

July 1999, Case COMP/M.2231 - Huntsman International/Albright & Wilson Surfactants Europe,

European Commission decision of 30 March 2001, Case COMP/M.4179 - Huntsman/Ciba TE Business,

European Commission decision of 30 June 2006, and Case COMP/M.5927 - BASF/Cognis, European

Commission decision of 30 November 2010.

14 Case COMP/M.5927 – BASF/Cognis, European Commission decision of 30 November 2010.

15 Case COMP/M.4179 - Huntsman/Ciba TE Business, European Commission decision of 30 June 2006,

Case COMP/M.4972 - Permira/Arysta, European Commission decision of 25 February 2008, Case

COMP/M.5243 - CVC/RAG/Evonik, European Commission decision of 8 September 2008, and Case

COMP/M.5927 BASF / Cognis, European Commission decision of 30 November 2010. Previously, in

Case COMP/M.1517 - Rhodia Donau Chemie/Albright & Wilson, European Commission decision of 13

July 1999, the Commission had considered that the markets for surfactants were EEA-wide.

16 HQ and PC share the same chemical composition, C6H4(OH)2.

17 HQ is mainly used as an additive in the manufacture of monomers and as antioxidant building blocks for

food and tyres. It can be also used, for example, in the photographic industry and the agrochemical sector.

PC is used for a number of electronic applications, agrochemicals, pharmaceuticals, flavours and

fragrances.

18 Polyamides are polymers that have an amide linkage in the polymer backbone

19 Nylon salt is also called AH salt.

20 Case IV/M.214 - DuPont/ICI, European Commission decision of 30 September 1992.

21 Case COMP/M.3024 - Bain Capital/Rhodia, European Commission decision of 19 December 2002.

22 Case COMP/M.3024 - Bain Capital/Rhodia, European Commission decision of 19 December 2002.

23 Case COMP/M. 4927 – Carlyle/Ineos/JV, European Commission decision of 20 December 2007.

24 Case COMP/M. 4927 – Carlyle/Ineos/JV, European Commission decision of 20 December 2007.

25 Horizontal Merger Guidelines (OJ 2004 C 31/5, 05.02.2004), para. 18.

26 Using the alternative product market definitions proposed by the notifying party, the 2010 market shares

would be: (i) for non-ionic surfactants, less than [0-5]% both in the EEA and worldwide; and (ii) for

amine oxides plus amphoteric surfactants,[5-10]% in the EEA and [10-20]% worldwide.

27 On a worldwide level, Rhodia procured around [0-5] kt of H2O2 for amine oxides and [15-25] kt for

diphenols in 2010, representing less than 1% of the overall worldwide demand.

28 On a worldwide level, Rhodia's market shares in 2010 were [30-40]% for HQ, [50-60]% for PC and [40-

50]% in a combined market for HQ and PC

29 The parties estimate the overall size of the market for PA6.6 as [500-1,000] kt in the world and [100-500]

kt in the EEA.

30 According to the parties this market would encompass polyamides PA4.6 and PA9T

31 According to the parties this market would encompass polyamides PA4.6 and PA9T.

32 Solvay's market share in the EEA for light soda ash is [30-40]% and competitors are Ciech ([20-30]%),

Tata ([10-20]%), Sisecam ([5-10]%) and Novacarb ([0-5]%). Solvay's market share in the EEA for dense

soda ash is [30-40]% and competitors are Ciech ([20-30]%), Tata ([10-20]%), Eti Soda ([10-20]%),

Sisecam ([5-10]%) and Novacarb ([5-10]%).

33 In 2010, Solvay’s sales of sodium silicate in the EEA were approximately [10,000-20,000] tonnes, giving

rise to revenues of approximately €[1-10] million. Solvay estimates that its market share is less than [0-5]% of total volumes sold on the merchant market in the EEA. Rhodia estimates that its market share is

less than [0-5]%.

34 Horizontal Merger Guidelines (OJ 2004 C 31/5, 05.02.2004), para. 18.

35 As already indicated, the parties combined share of supply for sodium silicate is insignificant (less than

[0-5]% in the EEA).