EC, May 21, 2010, No M.5781

COMMISSION OF THE EUROPEAN COMMUNITIES

Judgment

Total Holdings Europe SAS/ ERG SPA/ JV

Dear Sir/Madam,

Subject: Case No COMP/M.5781 – Total Holdings Europe SAS/ ERG SPA/ JV

Notification of 14 April 2010 pursuant to Article 4 of Council Regulation No 139/20041

1. On 14/04/2010, the European Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which Total Italia Spa. ("Total Italia", Italy) wholly controlled by Total Holdings Europe S.A.S. ("Total", France, collectively "Total Group") and ERG Petroli Spa. ("EGP", Italy) fully owned by ERG Spa. ("ERG", Italy, collectively "ERG Group"), acquire within the meaning of Article 3(1)(b) of the Merger Regulation joint control of JV CO ("the JV"), a newly created joint venture resulting from the merger between EGP and Total Italia.

I. THE PARTIES AND THE OPERATION

2. TOTAL is engaged in all aspects of the petroleum industry, including oil and gas exploration, development and production, as well as refining and marketing business (in Italy, through Total Italia), and trading and shipping of crude oil and petroleum products.

3. ERG Group is active, inter alia, in marketing of petroleum products through its subsidiary EGP, principally in Italy through its retail and wholesale network.

4. The envisaged transaction involves the creation of a full function joint venture, which will combine the refining and marketing activities of Total and ERG Group in Italy through the merger of Total Italia into EGP. The shares of the JV will be held by ERG. (51%) and by Total (49%) respectively. Pursuant to the shareholders agreement each shareholder will appoint respectively 3 members of the Board of Directors where decisions will be validly taken with the affirmative vote of at least 4 Directors out of 6. A majority of 5 Directors will be instead required for the adoption of resolutions on reserved matters such as those relating to the approval of the business plan, budget etc2. As a consequence the JV will be jointly controlled by both parties to the concentration.

5. The joint venture will be fully functional in nature given that it will perform on a lasting basis all the functions of an autonomous economic entity and will have an initial duration of 30 years. It will have its own assets such as its own refineries, logistics and retail networks and sufficient financial resources in order to independently operate on the market. Finally, the joint venture will be economically autonomous from its parents as commercial relations with the parties will be at arm's length3.

6. The transaction does not include (i) ERG Group’s activities in Sicily and Spain, (ii) Total’s aviation fuel activities in Italy, nor (iii) the business unit focused on the sales of motor fuels to large international fleet (the “AS 24” business).

7. It follows from the foregoing, that the operation consists in a concentration within the meaning of Article 3(4) of the Merger Regulation.

II. EU DIMENSION

8. The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4 (TOTAL: EUR 179 976 million; […]), but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension.

III. RELEVANT MARKETS

9. The proposed transaction concerns the upstream and downstream level of refined oil products value chain, namely, (i) ex-refinery/cargo sales of fuels (ii) non-retail sales of fuels (gasoline, diesel, heating oil and fuel oil), (iii) retail sales of motor fuels (diesel, gasoline and automotive liquefied petroleum gas, "LPG"), (iv) sales of LPG in bulk and bottles, (v) sales of bitumen and (vi) sales of automotive lubricants where both parties to the concentration operate.

10. For the purpose of the present decision the assessment will focus on the markets for retail and non-retail sales of fuels, LPG and bitumen. Thus, as the parties' combined market shares with respect to both ex-refinery/cargo sales and sales of lubricants are below 15% under any envisageable market definition5, these markets are not considered to be affected.

A. Product Market Definition

A.1 Non-retail sales of fuels

11. Non-retail sales of fuels consist of smaller volumes compared to ex-refineries/cargo sales usually directed from the supplier's inland storage facilities, which are delivered by secondary transport (generally by truck) to the clients premises. Customers are generally branded and unbranded service stations, independent smaller resellers, industrial and commercial consumers (e.g. transport companies) and public institutions (hospitals, army).

12. In past decisions, the Commission has segmented this market further along the individual types of products, namely, (i) leaded and unleaded gasoline, (ii) diesel, (iii) domestic heating oil and (iv) fuel oil6. The notifying parties consider this segmentation appropriate.

13. The market investigation widely confirmed the Commission market definition in relation to non-retail sales. The majority of respondents also agreed with the precedents of the Italian Competition Authority ("AGCM") distinguishing between two client groups, namely, (i) wholesalers ("B2B" sales) and (ii) end-users (i.e. commercial end-customers, or "B2C" sales).

14. In this respect market players explained that although the products supplied are the same as well as the distribution channel used (truck), wholesalers are usually supplied from both refineries and depots and deliveries are generally free-on truck (i.e. the customers take care of the primary transportation), whereas end-customers are usually supplied from dedicated depots by trucks and transport costs are often borne by the providers.

15. However, the exact market definition can be left open in the present case, as regardless of the market definition no competition concerns would arise as a result of the transaction.

A.2 Retail sales of motor fuel (gasoline, diesel and automotive LPG)

16. Retail sales of motor fuels (gasoline, diesel and automotive LPG) consist of sales made to motorists from branded and unbranded service stations. In line with the Commission’s past practice7, the notifying parties submit that the relevant product market is constituted by the retail sales of all motor fuels with no need for a further segmentation between gasoline and diesel. Their view has been broadly confirmed by the market investigation as at least from a supply-side perspective both fuels are sold at almost every service station in Italy.

17. With respect to retail sales of automotive LPG in Italy, the market investigation was not conclusive on whether this fuel should be considered separately with respect to the other motor fuels usually sold by retail stations. In any event, as it will be explained below, there is no need to conclude on this point as under any alternative market definition the transaction does not raise competition concerns.

18. The parties also suggest in line with some Commission8 and AGCM9 precedents, that the overall market for retail sales of motor fuels may be segmented further into motorway and non-motorway sales. This distinction has been confirmed by some competitors who explained that different purchasing patterns characterise the two retail segments and that from a supply-side perspective, commercial and marketing offers from oil companies differ between sales on and off-motorways.

19. For the purposes of this decision, there is no need to conclude on the exact product market definition, as under any alternative scenario no competition concerns would arise as a result of the transaction.

A.3 Sales of LPG in bulk and bottles

20. LPG is a mixture of gases which may be sold either in bottles or in bulk. The Commission has previously reviewed the LPG market on the basis of a division between the supply of bulk LPG and the supply of bottled LPG (i.e. cylinders and cartridges)10.

21. For the purpose of the present case, there is no need to conclude on whether LPG in bulk and in bottles belong to the same product market as the transaction does not give rise to competition concerns under any alternative product market definition.

A.4 Sales of bitumen

22. Bitumen is a heavy distillate resulting from the crude oil refining process and primarily used in asphalt production11. In previous decisions the Commission analysed all types of bitumen as constituting one market, mostly due to supply-side substitutability considerations.

23. The parties submit that within the bitumen business three separate products may be distinguished: (i) standard bitumen, (ii) bitumen emulsions and (iii) modified bitumen – as they are not substitutable due to the different production process used for each of them, their inherent characteristics and prices. The market investigation did not contradict this contention.

24. In any case, for the purposes of this decision the exact market definition can be left open, as regardless of the market definition no competition concerns would arise as a result of the transaction.

B. Geographic Market Definition

B. 1 Non-retail sales of fuels

25. With regard to the geographic scope of the markets for non-retail sales of fuels, the Commission found in previous decisions that the markets could be narrower than national in scope as resellers and end-users seek a nearby source of supply in order to economise on transportation costs12. In other decisions, however, the Commission took the view that the geographic market could be national13 or even regional14. However, the Commission ultimately did not take a final position on the geographic market definition for non-retail sales of fuels.

26. The notifying parties submit that the geographic market is as wide as Italy or at least macro-regional-wide (the regions being North-West, North-East, Centre, South and the Islands15) since many customers procure fuels at national level and they usually have nation-wide networks. The AGCM has considered in its decisional practice that sales to (i) wholesalers ("B2B sales") take place within regional/macro-regional areas, while non-retail sales to (ii) end-consumers ("B2C sales") have a narrower geographic scope corresponding to each Italian province or an aggregate of neighbouring provinces16.

27. In the present case, respondents to the market investigation largely confirmed that customers tend to procure refined oil products mainly from suppliers controlling depots and terminals located within a radius of approximately 200 km from the place of delivery. Based on this, a wide majority of respondents (especially customers) pointed to the existence of macro-regional markets for non-retail sales of fuels irrespective of the distinction between (i) end-user and (ii) wholesalers. Given the territorial characteristics of Italy and the locations of the facilities from which fuels are sold, those macro-regions would approximately correspond to (i) North-West, (ii) North-East, (iii) Centre, (iv) South and (v) the Islands.

28. Notwithstanding the above, some competitors equally underlined that the use of terminals located in certain regions is not necessarily an indication of the existence of separate regional markets, since the following four key economic factors constrain suppliers from charging significant price premiums between different regions: (i) the availability of public sources of information (Platts) on fuels prices ex-refinery; (ii) the presence of overlapping supply areas along the national territory; (iii) the extensive use of throughputs agreements between suppliers which allow them to sell fuel in all the country; (iv) and the excess in storage capacity in Italy.

29. In addition, the market investigation also showed that some customers (both wholesalers and end-users) purchase their products nationally from sites based throughout Italy irrespective of their premises' location.

30. Based on the foregoing, the Commission considers it appropriate to examine the competitive impact of the proposed concentration on the Italian market for non-retail sales of fuels from at least a macro-regional perspective irrespective of whether B2B sales or B2C sales are taken into account.

B.2 Retail sales of motor fuel (gasoline, diesel and automotive LPG)

31. In previous Commission decisions, the geographic market for retail sales of motor fuels was defined as national in scope17. However, it has also been pointed out that there is a strong local element to the retail fuel market, as vehicle owners usually resort to service stations in their vicinity. It also appears a common practice in this industry for suppliers to monitor neighbouring retail fuel stations around each of their own retail fuel stations in a given country, region or local area18. For these reasons among others, the AGCM has considered in its past decisions the market for retail sales of motor fuels as wide as each Italian province19.

32. The parties argue that that there are strong indications pointing to the existence of a national market for retail sales of motor fuels in Italy due to the extensive overlaps in the catchment areas of individual service stations in the proximity of each other which would transcend the whole territory of Italy ("knock on effect").

33. In the case at hand, the majority of respondents to the market investigation confirmed that the geographic substitutability among retail stations is limited as motorists are normally supplied by the service stations near to their centre of activity. In addition, pump prices of motor fuels are set at local level based, inter alia, on the observation of prices applied by retail stations close to their fuel outlets.

34. However, several competitors also agreed with the existence of a certain overlap between service stations' catchment areas, which will not only determine the competitive interactions between geographically neighbouring service stations, but will also, to some extent, have a "knock-on" effect on more distant service stations, therefore extending the geographic scope of the relevant market to be considered. In addition, all the respondents interviewed fully agreed with the parties that important parameters of competition, such as range of products, sources of such products, quality, service level (opening hours etc), advertising, promotion etc. are decided at national level rather than locally. Finally, the market investigation also showed that the main suppliers' market positions tend to be broadly similar in the different parts of the country where they operate.

35. As far as motorways are concerned, the market investigation was not conclusive on the geographic market definition that should be retained for Italy, however the same considerations above explained apply also to motor fuel retailing on motorways.

36. Based on the foregoing, the effects of the proposed concentration on the retail level of motor fuels in Italy will be assessed from a national perspective, while taking into account also competition that takes place at the local level.

B.3 Sales of LPG in bulk and bottles

37. The Commission has previously considered that LPG markets appear to be national in scope20. The parties share this view as they consider that each LPG facility is constrained by other facilities in the proximity of each other in such a way to broaden the scope of the market up to the national level.

38. The market investigation showed that while the majority of suppliers generally sell LPG all over Italy on the basis of a national pricing policy, customers tend to source their requirements mainly in the same region where their premises are based. In any event, both customers and competitors fully agree with the existence of a certain overlap among the geographic areas served by the LPG facilities located in Italy.

39. In any case, under any alternative geographic market definition, the transaction would not raise competition concerns. Therefore, in the present case, it is not necessary to conclude on the geographic scope of the LPG market.

B.4 Sales of bitumen

40. In previous decisions, the Commission has never found markets for bitumen to be wider than national, but rather analysed whether the geographic scope of those markets was possibly narrower than national (without ever concluding on the market definition)21.

41. The parties note that advances in bitumen tank technology allow using bitumen within a radius of 300-400 km. Moreover, they also argue that transport costs for modified bitumen and bitumen emulsions have little impact on the final price of these products therefore the relevant geographic market for such products should be considered national-wide.

42. The market investigation showed that the markets for sales of bitumen are at least macro-regional in scope. In this respect, most of the respondents explained that although transport costs are not insignificant they do not represent an obstacle to trade at distances greater than 200 km. Indeed, most customers argued to source a substantial part of bitumen (up to 64% of their requirements) from providers located further than 200 km from their premises.

43. In any event, there is no need to take a final position on the exact geographic market definition, as under any alternative scenario no competition concerns would arise as a result of the transaction.

IV. COMPETITIVE ASSESSMENT

44. The envisaged transaction results in the following horizontally affected markets where both ERG and Total operate: (i) non-retail sales of fuels (gasoline, diesel, heating oil and fuel oil), (ii) retail sales of motor fuels (diesel, gasoline and automotive LPG), (iii) sales of LPG in bulk and bottles and (iv) sales of bitumen.

C. Horizontal overlaps

C.1 Non-retail sales of fuels

45. On a nation-wide market for non-retail sales of fuels the parties' combined market share would be below 15% with respect to each of the fuels they both supply, as showed in the table below. In addition, from the below table it appears that several players would exert competitive pressure over the parties post-transaction. As a consequence the transaction does not raise competition concerns.

Table 1: Market for non-retail sales of fuels in Italy

2008 / Italy | Gasoline | Diesel | Heating oil | Fuel oil |

TOTAL | [5-10]% | [5-10]% | [5-10]% | [0-5]% |

ERG | [0-5]% | [5-10]% | [5-10]% | [5-10]% |

JV CO | [5-10]% | [10-20]% | [10-20]% | [10-20]% |

ENI | [20-30$% | [30-40]% | [30-40]% | [10-20]% |

ESSO | [10-20]% | [5-10]% | [10-20]% | [5-10]% |

TAMOIL | [10-20]% | [5-10]% | [5-10]% | [5-10]% |

Others | [40-50]% | [30-40]% | [30-40]% | [50-60]% |

(Source: Form CO, data based on Unione Petrolifera report)

Table 2: Data supporting the market shares indicated at table 1

2008 / Italy (tons) | Gasoline | Diesel | Heating oil | Fuel oil |

TOTAL | […] | […] | […] | […] |

ERG | […] | […] | […] | […] |

JV CO | […] | […] | […] | […] |

ENI | […] | […] | […] | […] |

ESSO | […] | […] | […] | […] |

TAMOIL | […] | […] | […] | […] |

Total market | 688.413 | 13.755.817 | 2.045.501 | 5.040,713 |

(Source: Form CO)

46. Considering the market for non-retail sales of fuels as macro-regional in scope (North- West, North-East, Centre, South, and the Islands), consistently with the results of the market investigation, the JV's market share would not approach [20-30]% even in North-Western Italy, where the parties' activities overlap the most. The market investigation showed that in each macro-region where the parties operate other oil companies are present (although with a different market presence). Moreover, it appears from the customers' replies to the market investigation that independent refineries may act as wholesalers therefore competing with the parties in the non-retail markets in Italy.

Table 3: Combined market shares of Total and ERG in the market for non-retail sales of fuels (both B2B and B2C)

|

(Source: Parties' estimates on Ministry of Economic Development data)

Table 4: Data supporting the market shares indicated at table 3

|

(Source: Form CO)

47. Notwithstanding the above, the parties argue that any representation of the market at sub-national level does not provide a fully reliable picture of the non-retail sector in Italy as they consider that official statistics on this market (gathered by the Ministry of Economic Development) tend to distort the actual size of the non-retail markets at local level. This is due to the fact that such statistics focus on the registered office of the clients as well as oil companies' subsidiaries irrespective of the final destination of the oil product22. As a result the parties claim that the level of fuels consumption reported at local level is not fully accurate.

48. The market investigation confirmed the parties' arguments as to the difficulty in reconstructing the market for non-retail sales of fuels at sub-national level due to the following reasons. First, it appears that companies use different methods to geographically allocate their volumes of sales, be either the location of the depot/terminal/refinery from which fuels are sold or the delivery point of sales. Moreover, it appears that sometimes oil companies mix in their computations ex- refinery/cargo sales and non-retail sales since in certain cases there is not a clear-cut distinction between the two distribution channels. This is in particular the case when customers buy fuels directly from the refinery site located within a distance of less than 150 Km from their premises and delivery are made by truck. Finally, it can be difficult to identify the final delivery point of the oil products sold at non-retail level as resellers which represent a significant part of the customer's base of companies active in the non- retail sector sell in turns fuels to their clients whose premises are spread in several regions all over Italy. As a consequence, it results difficult to accurately allocate at sub- national level the volumes of sales realized through these intermediary transactions.

49. In the light of the foregoing, the Commission considers it appropriate to use the parties' best estimates of their market shares at macro-regional level for information purposes only and to complement the competitive assessment of the present transaction with the analysis of the infrastructures and storage facilities controlled by the parties in Italy. In this respect, the market investigation fully confirmed the market position of a company on the non-retail market mirrors to a certain extent its position regarding the logistic.

50. The parties submit that in Italy pipelines network has a limited role. None of the pipelines can be considered as a north-south backbone of the country as they essentially serve Northern Italy where they primarily connect storage deposits with refineries either in the interior of the country or on the coasts. To the opposite, Central and South Italy are mainly served from coastal or continental depots by truck. Therefore, as those areas in the Italian territory display different characteristics in their logistic structure, the parties suggest distinguishing four macro-regions (North-West, North-East, Centre and South) also with respect to the provision of logistic services in Italy.

51. The parties' position with respect to the pipelines network, does not result affected by the present transaction as Total only holds a stake together with ERG on the Pantano- Fiumicino pipeline. As a consequence post-merger no horizontal overlap will result from the transaction. In addition, it also appears from the parties' submissions that ENI is the market leader in pipeline transportation.

52. With regards to storage facilities which the market investigation confirmed to be of outmost importance for any successful wholesale activity, the parties control the following depots as displayed in the below table.

Table 5: Storage facilities controlled by the parties in Italy

Shareholders | Import Capacity

000 c.m. | Total Capacity | Type of products stored and lifted from the depot |

Sigemi system (ERG 26% share) (SHELL/ENI/KUWAIT) | […] | […]23 | Gasoline, Automotive Diesel, Heating Oil |

Savona Depot (ERG) | […] | […]24 | Automotive Diesel, Heating Oil and Lubricants |

S. Martino di Trecate Depot (ERG) | […] | […] | Gasoline and Automotive Diesel |

DECO (ERG/TOTAL 50% share)

(SHELL/KUWAIT) | […] | […]25 | Gasoline and Automotive Diesel |

Total parties | […] | […] |

|

(Source: parties' data, 2009)

53. It results from the above that Total has a limited primary logistics network in Italy consisting into the storage and loading facilities dedicated to Rome refinery in Pantano (jointly controlled with ERG) and a 25% stake in a depot connected to this refinery (so- called DECO depot). The other shareholders of DECO are ERG (25%), Q8 (25%) and Shell (25%). As a result, the only increase in market presence brought about by the transaction at hands in relation to the storage facilities controlled by the parties derives from the fact the Total will add its 25% shareholding in DECO to the logistic system of ERG. In any event, post-transaction the JV's share of capacity in storage and import terminals in Italy would be well below 15% in any macro-region in Italy.

Table 6- Parties market shares with respect to storage depots in Italy

Unit of measure

000 c.m. | North West Italy | North East Italy | Centre Italy | South (without Sicily) | Italy |

Total |

|

| 2 |

| 2 |

ERG | 224.5 | - | 2 |

| 226.48 |

Total Market | 5417.2 | 2603.6 | 5432.4 | 3013,2 | 16466.4 |

Market share of JV CO | 4.14% | - | 0.07% | - | 1.39% |

(Source: Form CO, data based on Unione Petrolifera report)

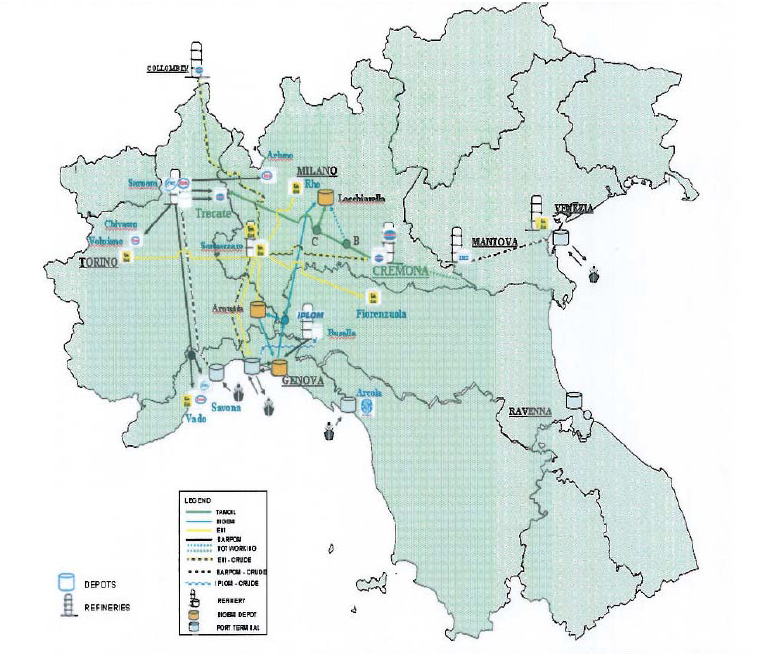

54. The parties also submit that with respect to the Sigemi system, ERG's direct competitors are Kuwait Petroleum, Shell and ENI controlling the remaining 74% of Sygemi capacity. The same consideration applies to DECO depot both controlled by Total and ERG (50%) together with Shell and Q8. In addition, in all the regions covered by JV's logistics there are third parties' depots with sufficient storage capacity to effectively compete with the parties' facilities. The map and tables below display some of the depots controlled by the parties' competitors which are not further than 200 km from the parties' storage facilities.

Map of depots in Northern Italy

Table 7- Depots controlled by third parties in Northern Italy

Northern Italy

Third parties facilities- capacity 000 c.m | |||||

Chivasso (Esso)

[…] | Armani (Tamoil)

[…] | Arluno (Esso)

[…] | Rho/Pregnana (Eni/Q8)

[…] | Fiorenzuola (Eni)

[…] | Vado Ligure (Esso)

[…] |

ERG facilities | |||||

S. Martino di Trecate

[…] | Sigemi system (Lachiarella, Arquata, S.Quirico) […] | Savona depot

[…] |

| ||

(Source: Parties' data)

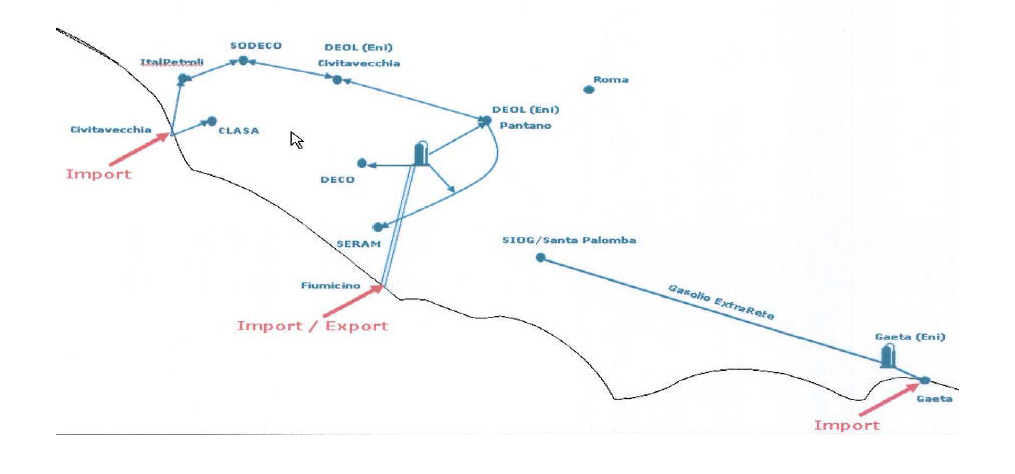

Map of depots in Central Italy

Table 8- Depots controlled by third parties in Central Italy

Centre of Italy

Third parties facilities - capacity 000 c.m | |||||

Civitavecchia (Italpretoli)

[…] | Civitavecchia (Enel)

[…] | Civitavecchia (Eni)

[…] | S. Palomba (Eni)

[…] | Gaeta (Eni)

[…] |

|

ERG and Total facilities | |||||

DECO depot

[…] | |||||

(Source: Parties' data)

55. In addition to the above, the market investigation confirmed that there is an excess of storage capacity in the Italian market and that facilities are easily accessible due to transit agreements in third parties depots, which appear to be common to the this sector. To confirm this, the majority of competitors interviewed argued to be able to sell refined oil products in the whole of Italy partially using third parties depots. Finally, one of the competitors active in the non-retail market in Italy pointed out that in the North-West of Italy where the parties are mostly present, there is a large availability of infrastructures and also some refineries from which wholesalers can easily source their requirements.

56. In this regards the parties also underline even considering their market presence with respect to the refineries they control either at macro-regional level or in the whole Italy the transaction would not give raise to any competition concerns due to the following reasons. In the North-west of Italy ERG only controls Trecate refinery (25.90%) jointly with Exxon Mobil (74.10%). As a consequence, the former owns a refining capacity of […] million tons per year whilst the latter of […] million tons per year. In addition, as displayed in the above map, in North-Western Italy there are Cremona refinery (Tamoil) and Iplom with a respective capacity of […] and […] million tons per year. Total, instead does not control any refinery in the North of Italy. It follows from the foregoing that the parties do not have any competitive advantage with respect to the other oil companies active in both production and non-retail sales of fuels in Italy since there are sufficient refineries from which market players can source oil products.

57. To conclude, it appears from the parties submissions that taking into account the whole of Italy the parties' market presence in terms of refining capacity would be limited as the JV would qualify as only the […] largest refinery in the country with a market share of approximately [5-10]% as opposed to the market leaders ENI ([20-30]%), Esso ([10- 20]%) and Saras ([10-20]%).

Table 9- Refining capacity in Italy

2008 | Effective refining capacity of refineries controlled by the company (Million of tons/year) | Refining capacity at disposal of the company | Market share |

JV CO | […] | […] | [5-10]% |

Erg MED | […] | […] | [5-10]% |

ENI | […] | […] | [30-40]% |

ESSO | […] | […] | [10-20]% |

Saras | […] | […] | [10-20]% |

LUKOIL | […] | […] | [5-10]% |

Iplom | […] | […] | [0-5]% |

API | […] | […] | [0-5]% |

Tamoil | […] | […] | [0-5]% |

IES | […] | […] | [0-5]% |

Q8 | […] | […] | [0-5]% |

TOTAL |

| […] | [90-100]% |

(Source: form CO: data based on Unione Petrolifera report)

58. It follows from the above that the transaction would no significantly impede effective competition neither in Italy nor in any part of it due to the following reasons. There are several oil companies and independent wholesalers active thorough the Italian territory, customers tend to multisource from different suppliers and the market appear unconstrained due to the availability of storage facilities and production capacity from the refineries based in Italy.

C.2 Retail sales motor fuel (gasoline, diesel and automotive LPG)

59. At national level the transaction would lead to a combined market share below 15% with respect to gasoline and diesel sold on ordinary roads in Italy. The market leaders are ENI and Esso displaying higher market shares than the parties. Therefore, no competition concerns arise from the envisaged operation.

Table 10-Market for retail sales of motor fuels (gasoline and diesel) -off-motorways- in Italy

Players | Volumes (tons) | Market shares |

TOTAL | […] | [5-10]% |

ERG | […] | [5-10]% |

JV CO | […] | [10-20]% |

ENI | […] | [30-40]% |

ESSO | […] | [10-20]% |

TAMOIL | […] | [5-10]% |

KUWAIT | […] | [10-20]% |

Shell | […] | [5-10]% |

Others | […] | [10-20]% |

Total market | […] |

|

(Source: Parties' estimates based on Ministry of Economic Development and Unione Petrolifera data)

60. With respect to retail sales of LPG on ordinary roads, the market investigation showed that in Italy revenues from LPG sales made at retail level by oil companies constitutes a modest part of their turnover compared to those stemming from other motor fuels. On average, in fact, retail sales of LPG account for no more than [0-5]% of all oil companies' sales of motor fuels. A number of other competitors, in fact, not present with respect to sales of gasoline and diesel, is active in the supply of LPG in Italy (see table below). Therefore, competition concerns with respect to LPG sales can reasonably be dismissed. In any event, as below displayed, even on a separate market for sales of automotive LPG the parties would be constrain post transaction by a number of competitors.

Table 11- Market for automotive LPG in Italy26

Players | Volumes (tons) | Market shares |

TOTAL | […] | [5-10]% |

ERG | […] | [5-10]% |

JV CO | […] | [10-20]% |

ENI | […] | [20-30]% |

ESSO | […] | [10-20]% |

TAMOIL | […] | [5-10] % |

Shell | […] | [0-5]% |

Others | - | [50-60]% |

Total Market | […] |

|

(Source: Parties' estimates based on Unione Petrolifera data)

61. Considering the impact of the transaction at local level, it results that three Italian provinces would be mostly affected by the merger as the parties joint market shares for motor fuels sold of-motorways would exceed [20-30]% but the joint market share would in all cases stay well under [50-60]%.

Table 12- Market for retail sales of gasoline –off-motorways- in some Italian provinces

| ERG | Total | Combined | ENI | Shell | Esso | Tamoil |

La Spezia | [5-10]% | [20-30]% | [30-40]% | [30-40]% | [5-10]% | [0-5]% | [5-10]% |

Massa | [10-20]% | [10-20]% | [30-40]% | [20-30]% | [5-10]% | [10-20]% | [0-5]% |

Viterbo | [20-30]% | [10-20]% | [40-50]% | [10-20]% | [0-5]% | [5-10]% | [5-10]% |

(Parties' estimates)

Table 13- Market for retail sales of diesel-off-motorways- in some Italian provinces

| ERG | Total | Combined | ENI | Shell | Esso | Tamoil |

La Spezia | [0-5]% | [20-30]% | [20-30]% | [30-40]% | [5-10]% | [0-5]% | [5-10]% |

Massa | [10-20]% | [10-20]% | [20-30]% | [20-30]% | [10-20]% | [10-20]% | [0-5]% |

Viterbo | [20-30]% | [10-20]% | [30-40]% | [20-30]% | [5-10]% | [5-10]% | [5-10]% |

(Parties' estimates)

62. However, the market investigation confirmed, in line with the parties' submissions that in each of the provinces above displayed there are other competitors which exert competitive pressure on the parties. In fact, those provinces are relatively small Moreover, those provinces are relatively small27 and crossed by important inter- regional roads through which an important part of their population commutes with the neighbouring provinces (where the parties' joint market shares are below [20-30]%). In particular, Viterbo's inhabitants commute with Rome, La Spezia's inhabitants with Genova and Massa's inhabitants with Pisa and Lucca. As a consequence, the "knock on effect" among retail stations located along the roads connecting these provinces would extend the scope of the relevant geographic market to be taken into account for the assessment of the present transaction with the effect of diluting the parties' combined market presence.

63. Additionally, the parties point out that in the provinces concerned there is a significant number of stations directly owned or operated by dealers ("DO-DOs") which could easily switch to other suppliers at the expiration of the contracts with ERG or Total. Furthermore, they argue that Viterbo for historical reasons is characterised by the presence of several independent retailers ("white pumps") strongly competing with oil companies. The market investigation has confirmed this contention. Therefore, no competition concerns seem to arise from the envisaged transaction under a local perspective too.

64. The same conclusion applies assessing the effects of the merger with respect to LPG sold off-motorways under a local analysis. According to the parties' estimates, the only province where the parties' activities overlap the most is Naples (ERG [5-10]%, Total, [20-30]%). However, the market investigation widely confirmed that non oil companies specialised in the sale of LPG are very well positioned on the Italian market (for sales of both automotive and heating) therefore strongly constraining oil companies (including ERG and Total). In this respect, the parties argue that non-oil companies account for approximately [20-30]% of the market. The market investigation showed that other vertically integrated oil companies sell LPG in the province of Naples. Finally, it appears from the parties' submissions that in all the neighbouring provinces around Naples ERG is not present therefore taking into account the geographical expansion of the scope for competition due to the possible "knock on effect" which apply to the retail stations' catchment areas around Naples, the parties' market presence would be significantly diluted. It follows from the foregoing that the transaction does not raise competition concerns.

65. Finally, the parties' market position on a national market for retail sales of fuels on- motorways would not be much different as compared their market presence on the retail market on ordinary roads. Also in this case the market leaders would be ENI and Esso as displayed in the below table. As a consequence, the transaction would not have any adverse effect on competition in Italian market.

Table 14- Market for retail sales of motor fuels- on-motorways- in Italy

Company (2008) | No. Stations | Volume (tons) | Market Share |

Total |

|

| [5-10]% |

Erg |

|

| [0-5]% |

JV CO |

|

| [10-20]% |

ENI. |

|

| [40-50]% |

Esso |

|

| [10-20]% |

Tamoil |

|

| [5-10]% |

Shell |

|

| [5-10]% |

Total market |

|

| 100.00% |

(Source: Form CO, data based on Unione Petrolifera

66. The same contention holds true assessing the effects of the merger in each motorway where the parties are present. Thus, even considering the highway (A26) where the parties' retail stations are mostly present (7 stations out of 17) no restriction of competition would result from the transaction due to the following reasons. This motorways is only 200 km long (thus, a car can easily drive for the entire length of it without refuelling) and it is located on a junction of two different motorways (A4 and A8) where retail stations belonging to the parties' competitors are strongly present. Therefore, motorists crossing this motorway would have plenty of choice to refuel their cars. Based on this, it can be concluded that the transaction does not raise competition concerns.

67. An assessment of the potential of the transaction to give rise to coordinated effects in the retail markets of auto-motive fuels has also been made by the Commission.

68. In 2007, an AGCM investigation on an alleged exchange of information concerning the recommended prices by some oil companies concluded by the companies concerned committing to restrict the scope of their communication and modify the way in which such price was computed. The investigation also identified ENI as the price-setting entity. The strong competition exerted by independent dealers ("white pumps"), which usually supply refined products from independent wholesalers or directly from refineries, also appears to constitute a significant threat to the establishment of supra- competitive prices, at least in several parts of Italy. Furthermore, with respect to the present merger, neither the relatively high number of independent companies' post- merger (seven), nor the moderate market presence of the merging parties, constitutes per se hard evidence of the fact that co-ordinated effect can be completely excluded. On the other hand, the replies from customers, as well as the overall investigation, do not seem to provide any affirmative evidence that the establishment, or reinforcement, of co- ordination among Italian oil companies might be the outcome to the present transaction. Therefore, the risk that the merger might give rise to coordinated effects, by means of establishing the ground or increasing the likelihood of co-ordination in the non-retail and retail markets of auto-motive fuels, can reasonably be dismissed.

69. In the light of the arguments above explained the Commission concludes that, under any alternative scenario the transaction does not raise serious doubts with respect to retail sales of motor fuels in Italy.

C.3 Sales of LPG in bulk and bottles

70. With respect to sales of LPG, the parties' combined market share would be well below [10-20]% in Italy (ERG: [0-5]%, Total [0-5]%) as well as at regional level. The only exceptions would be Umbria and Piemonte where the parties' joint market shares would be [10-20]% and [10-20]% (with an increment of [0-5]% and [0-5]%, respectively).

71. The parties' position on the LPG market would not change even segmenting the market between bulk and bottled LPG since both ERG and Total are barely present on the bottled market (respectively less than [0-5]% and [0-5]% nationally).

72. The other players active on the Italian market are: ENI ([10-20]%), Api ([0-5]%, Esso ([0-5]%) and other specialized companies in LPG sales such as Liquigas ([10-20]%). The market investigation showed that some of these companies are also active in both regions of Umbria and Piemonte exerting competitive pressure on the parties.

73. Consequently, the Commission concludes that the transaction does not raise serious doubts with regard to the LPG market in Italy.

C.4 Sales of bitumen

74. In relation to the sales of bitumen, the parties' activities overlap only with respect to the supply of standard bitumen as ERG does not supply bitumen emulsions and has minimal sales of modified bitumen ([0-5]% nationally).

75. On a nation-wide market for sale of standard bitumen the parties' joint market share would be [10-20]% (ERG: [5-10]%, Total: [0-5]%) while on a macro-regional level their market shares would exceed [10-20]% only in the Centre (ERG: [5-10]%, Total: [10-20]%) and the South of Italy (ERG: [5-10]%, Total: [10-20]%). In any case, the JV would face competitive pressure from other market players with similar or larger market shares such as Api and ENI28.

76. Consequently, the Commission concludes that the transaction does not raise serious doubts in the market for sales bitumen in Italy.

D. Co-ordinated effects

77. The parties consider that the only market on which both of them will continue to operate individually and independently from the joint venture is the market for ex-refinery/cargo sales of oil products on a worldwide basis. However, the parties stress that their position on such market – as well as the position of JV CO – are significantly different.

78. JV CO has limited refining capacity at the Mediterranean level, accounting for less than [0- 5]% of the total market. ERG Med, a subsidiary of ERG group has currently a modest presence on the market for ex-refineries/cargo sales in the Mediterranean, accounting for approximately [0-5]% of the total refining capacity of the Mediterranean. Finally, Total's refineries, account for [5-10]% of the total refining capacity in the same geographic area, (i.e. three times the refining capacity of ERG or of JV CO). Moreover, taking into account the whole Europe, Total's refining capacity would represent more than 6 times the refining capacity of respectively ERG and JV CO.

79. In view of the above, and considering the asymmetries between the parties’ positions on the ex-refinery/cargo market any risk of coordination between the parties and the JV can reasonably be ruled out.

80. In the worst case scenario, even if the Parties were to coordinate their activities on the market for ex-refinery/cargo sales, this would not lead to any significant restriction of competition since the parties' market position is modest compared to that of other players such as ENI or Exxon and others.

81. In can be concluded from the above that the transaction does not raise serous doubts in this respect either.

V. CONCLUSION

82. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty

on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the

replacement of "Community" by "Union" and "common market" by "internal market". The

terminology of the TFEU will be used throughout this decision.

2 Section 7.3.4 of the Shareholders Agreement.

3 The JV will produce internally […] that it will sell on the Italian market while its remaining requirements

will be purchased from either its parent companies or third parties at market conditions.

4 Turnover calculated in accordance with Article 5(1) of the Merger Regulation.

5 COMP/M.4926 - Basell/ Berre L’Etang Refinery, COMP/M.1383 - Exxon/Mobil, COMP/M.727 -

BP/Mobil, COMP/M.3291 - Preem / Skandinaviska Raffinaderi, COMP/M.4348-PKN/Mazeikiu,

CMP/M.1891-BP AMOCO/CASTROL; COMP/M.3543-PKN Orlen/Unipetrol; COMP/M.3375-

Statoil/SDS.

6 COMP/M.3516 -Repsol / Shell Portugal, COMP/M.5637MOTOR OIL (HELLAS) CORINTH

REFINERIES / SHELL OVERSEAS HOLDINGS

7 Case No M.1383 – Exxon/Mobil; case No M.3516 – Repsol YPF / Shell Portugal; M.3291 – Preem /

Skandinaviska Raffinaderi.

8 Case IV/M.1383 – Exxon/Mobil, recital 437; case COMP/M.1628 – TotalFina/Elf.

9 AGCM decision of 30 October 2008, n. 19083, C9713 - SHELL ITALIA/RAMO D’AZIENDA DI

AUTOSTRADE PER L’ITALIA, in Bulletin n. 41/2008

10 COMP/M.5005 –Galp Energia/ExxonMobil Iberia

11 It is also applied by other industries (industrial bitumen), such as the construction (for the manufacture of

waterproof dams and roofing material)11 and the paper industry.

12 Case No M.1383 Exxon/Mobil, recitals 443, 445.

13 Case No COMP/M.3375 – Statoil/SDS; case No COMP/M.3543 – PKN Orlen/Unipetrol, case No

COMP/M.3516 – Repsol/Shell Portugal, COMP/M.5005 –Galp Energia/ExxonMobil Iberia.

14 Case No M.3291 Preem/ Skandinavska Raffineradi, recitals: 16 and 17

15 North-West includes the following regions: Piemonte, Valle d'Aosta, Liguria, Lombardia; North-East:

Trentino Alto Adige, Venezia Giulia, Veneto, Emilia Romagna; Centre: Toscana, Marche, Umbria,

Lazio, Molise, Abruzzo; South: Campania, Puglia, Basilicata, Calabria; Islands: Sicilia, Sardegna.

16 AGCM, decision of April 7 2004 n.13080-IPLOM/RAMO DI AZIENDA DI SOCIATA' DI PERSONE,

provvedimento C10132 - EUROPAM/RAMO DI AZIENDA DI NEW ENERGY.

17 Case No IV/M.1383 – Exxon/Mobil; case No COMP/M.3516 – Repsol/Shell Portugal, case No

COMP/M.5005 – Galp Energia/ExxonMobil Iberia.

18 This is often done by defining a list, also called "cluster" or "trade area", of stations around each of

their own station where prices are monitored regularly, the prices of these neighbouring competitors'

stations being used in order to adjust their own prices to locally competitive levels.

19 Provvedimento n. 17824 ,C9029 – Esso Italiana/ Serenissima Trading.

20 See case COMP/M.1628 TotalFina/Elf.

21 COMP/M.3516 – Repsol Ypf/Shell Portugal, para. 13, COMP/M.2533 – BP/EON para. 43.

22 As a matter of example ERG explains that Europam, a company jointly controlled by ERG has its

registered office in Milan. Europam unlike ERG does not declare its volumes of sales to the Ministry of

Economic Development. Thus, all the sales of Europam are reported by ERG (its parent company) as

having made in Milan and are added by the Ministry in its estimate of the market for the province of

Milan. In effect,[…]. This situation leads therefore to a distortion of the level of fuels consumption in

certain Italian provinces.

23 […].

24 Savona depot handles both fuels and lubricants, therefore out of its total capacity of […] c.m. […] c.m

are used to store fuels and […] c.m. to store lubricants.

25 This figure refers to the capacity at disposal of ERG and Total whilst the total capacity of DECO

corresponds to […] c.m

26 The parties submit that data reported at table 7 are based on the official data of the Ministry of Economic

Development which relate to sales of automotive LPG made through both the retail and non-retail

channels (meaning sales of LPG to independent companies reselling this fuel through their petrol stations,

generally unbranded). In any event, the parties' estimate that even considering the segment of retail sales

of LPG separately from the non-retail channel, the parties market presence would be even lower

corresponding to a market share of [5-10]% (ERG:[0-5]%, Total [0-5]%). Therefore, no competition

concerns would arise from the transaction under any alternative scenario.

27 Assuming that the average size of all the Italian provinces is approximately 2.740 sq km, La Spezia (882),

Massa-Carrara (1.156) and Viterbo (3.612) are respectively the 9th, 14th and 88th smallest provinces out of

105 Italian provinces.

28 Api has a market share of [20-30]% and [30-40]% respectively in the Centre and South of Italy, ENI: [20-

30]% and [30-40]% in each of these macro-regions.