EC, July 2, 2010, No M.5864

COMMISSION OF THE EUROPEAN COMMUNITIES

Judgment

Avnet/ Bell Micro

Dear Sir/Madam,

Subject: Case No COMP/M.5864 – Avnet/ Bell Micro

Notification of 28/05/2010 pursuant to Article 4 of Council Regulation No 139/20041

1. On 28/05/2010, the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which the undertaking Avnet Inc. ('Avnet', USA) acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the undertaking Bell Micro Products ('Bell Micro', USA) by way of purchase of shares.

I. THE PARTIES

2. Avnet is a US-based distributor of electronic components, computer products and technology services operating worldwide. Through Electronics Marketing ('EM'), Avnet distributes a wide range of electronic components (semiconductors, interconnect devices, etc.) to contract manufacturers ('CMs') and original equipment manufacturers ('OEMs'). Through Technology Solutions ('TS'), Avnet supplies products, services and solutions for value-added resellers ('VARs'), system builders or integrators, OEMs and end-user businesses.

3. Bell Micro is a US-based distributor of data storage and server products and solutions, computer components, software applications, peripherals, as well as a provider of a wide range of services including system configuration, product installation, post-sale service and support and supply chain management. Bell Micro serves OEMs, commercial resellers, VARs, system integrators ('SIs'), CMs, storage, and server and networking infrastructure, end user customers and major retailers.

II. THE OPERATION

4. Pursuant to a Merger Agreement dated 28 March 2010, Avnet will acquire the entire issued and to be issued share capital of Bell Micro through a merger between Bell Micro and AVT Acquisition Corp., a wholly owned subsidiary of Avnet. Bell Micro will survive the merger and become a wholly-owned direct subsidiary of Avnet.

5. The proposed operation therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

III. EU DIMENSION

6. The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (Avnet: EUR 11 836 million; Bell Micro: EUR 2 166 million)2. Each of them has an EU-wide turnover in excess of EUR 250 million (Avnet: EUR […]; Bell Micro: EUR […]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The proposed operation therefore has an EU dimension.

IV. ASSESSMENT

A. INTRODUCTION

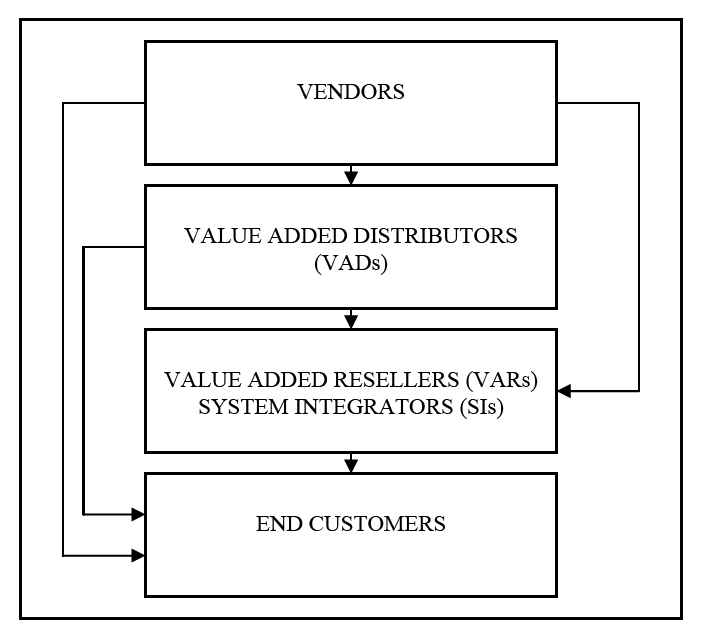

7. The proposed operation concerns the distribution of IT products and related services (referred to in the rest of this decision as 'IT products'). IT products are sold through two main channels: direct sales by the IT manufacturers ('vendors') and indirect sales ('distribution') by numerous intermediaries (value-added distributors ('VADs'), value-added resellers ('VARs'), system integrators ('SIs')).

8. The chart below illustrates the sales channels of IT products and the relationships between these different actors3.

9. Vendors are IT manufacturers, such as IBM or HP, which develop hardware or software solutions. They can sell either directly to end customers (direct sales, by bypassing distributors and supplying large corporate accounts) or VARs or through the intermediate channel constituted by VADs (indirect sales).

10. VADs are partnered with vendors and sell predominantly to reseller partners (VARs, SIs) and only exceptionally to end-customers. According to the notifying party, the role of VADs is to put together and sell cross-vendor solutions which range from standard products to much higher levels of customisation, configuration and integration. Their technical expertise aims at supporting VARs or end-customers directly on behalf of the reseller.

11. The main factor differentiating VADs from vendors is VADs' ability to provide a one-stop- shop facility to their customers. Indeed, VADs provide a broad range of products. They also provide added-value services such as system configuration, product installation, logistic services, financing, consulting, and support. VADs normally have to be certified by a vendor in order to distribute that vendor's IT products.

12. VARs, and to a certain extent SIs4, are typically partnered with VADs and/or with vendors directly. They sell to end-customers or to smaller VARs. According to the notifying party, the role of VARs is to put together technical solutions for end-customers, install and support.

13. According to the notifying party, although VADs and VARs both sell hardware and services, they do so in varying proportions and importance. The notifying party considers that the qualification of VAD or VAR depends on the proportion that hardware and services represent in their activity. For some companies, the qualification as a VAD or a VAR varies from one year to another.

14. The Commission considers therefore that the distinction between VADs and VARs is blurred. However, this fact has no consequence for the purpose of the assessment of the proposed operation.

15. Both Avnet and Bell Micro are active as VADs.

B. MARKET DEFINITION

1. Product market

(i) Indirect v. direct sales

16. The notifying party submits that direct sales of IT products and indirect sales of IT products ('distribution of IT products') are distinct markets, although the two sales channels exert to some extent competitive constraints on each other.

17. In previous decisions5, the Commission has left open whether direct and indirect sales belong to the same product market. In TechData/Scribona6, the Commission found that prices in the indirect sales channel are significantly constrained by prices in the direct sales channel. However, in Arrow Electronics/Logix7, the Commission found that the direct and indirect sales channels were not fully interchangeable for resellers and retailers active in Denmark.

18. The Commission's market investigation in the present case does not fully support the existence of an overall market for the sale of IT products including both direct sales by vendors and indirect sales through VADs, although half of the respondents consider that prices in the distribution of IT products are significantly constrained by prices and other conditions of supply in the direct sales channel8. Some respondents also indicated that VADs' customers can and do purchase both directly from vendors and indirectly through a distributor. Vendors use VADs to increase market reach and coverage, for their logistics services (such as stocking of products) and their provision of credit and related facilities as well as technical support to VARs. The purchase of IT products through VADs offer their VAR customers advantages in terms of broader range of IT products, better logistics and shorter delivery time, financing services, assistance with integration and marketing.

(ii) All IT products v. IT products categories

19. The notifying party submits that the distribution of IT products is the relevant product market and that this market should not be further segmented by IT products categories.

20. In previous decisions9, the Commission has considered that conditions of supply in the indirect sales channel are globally homogeneous across all categories of IT products, although some distributors specialise in certain categories of products (such as storage capacity and servers).

21. The Commission however left open in those cases whether the relevant market should include all IT products or whether distinct markets should be defined on the basis of each IT product category (including a sub-segmentation according to the servers range).

22. In the present case, the overlap between the activities of Avnet and Bell Micro concerns mainly the distribution of servers and storage products.

23. Servers include industry standard servers and servers with proprietary processor technology using Unix or Linux operating systems. The Commission has in the past further segmented servers into low-end servers, medium-range servers and high-end servers10 based on price band classification used by industry analysts such as IDC.

24. Storage products include disk storage and tape storage systems, as well as hard disk drives (HDDs)11. They are used to support the processing, management, and storage of digital data.

25. The Commission's market investigation in the present case has confirmed that VADs need specific skills and that they have to obtain specific certification from vendors in order to distribute different IT products, including entry-level, mid range and high end servers12. Distributors tend to specialise in specific product ranges, although some respondents indicate that these skills appear transposable through training (maybe less so for higher end products such as high end servers, storage products or networking products).

Conclusion

26. For the purpose of the present case, the exact product market definition can be left open, since under all alternative product market definitions the proposed operation does not give rise to serious doubts as regards its compatibility with the internal market.

2. Geographic market

27. The notifying party submits that although the distribution of IT products has historically been national in focus, distribution is increasingly carried out beyond the national scope. The notifying party submits that the relevant geographic markets are regional. It has distinguished between the following geographic markets: (i) the Nordic countries (Denmark, Sweden, Norway and Finland); (ii) the Benelux; (iii) Austria, Germany and the German-speaking part of Switzerland; and (iv) United Kingdom and Ireland.

28. In previous decisions13, the Commission has considered that language and local presence constituted indications that the market for the distribution of IT products could still be national in scope without concluding on its relevant dimension (national, regional or EEA- wide).

29. The Commission's market investigation in the present case has indicated that a majority of the respondents considers that the market for the distribution of IT products is EEA-wide14. Most of the respondents consider also that a local presence (i.e. logistics at a national level) is not a key requirement for a VAD to exercise its activity15, although most VADs do appear to have a local presence. Their respective sales organisations reflect different commercial strategies as the two following quotes from the Commission's market investigation illustrate. One VAD indicated that "[it] generally treat[s] each individual country differently as there are different drivers in each individual country". By contrast, another VAD indicated that "[it] is structured regionally from an internal organisational point of view but this is not a result of a need for country-specific insight."

30. For the purpose of the present case, the exact geographic market definition can be left open as the proposed transaction does not raise competition concerns under any possible definition of the geographic market.

C. COMPETITIVE ASSESSMENT

31. Avnet and Bell Micro are both active in several EEA countries as VADs for a range of IT products. The proposed operation only leads to affected markets if narrow market definitions are retained, namely the distribution of storage products and servers at a regional or national level.

32. On an overall market for the sale of all IT products (comprising both direct and indirect sales), the parties' combined market shares16 would be very limited at an EEA level: [0-5]% (Avnet) and [0-5]% (Bell Micro). The impact of the proposed operation on such a market would be insignificant.

33. This conclusion remains unchanged at the regional or national level, as the assessment below as regards narrower product markets demonstrates.

34. On a market for distribution of all IT products, the merged entity's combined market share remains below [0-5]% at the EEA level, [0-5]% at the regional level, and [5-10]% at the national level.

35. Given these very limited market shares and the existence of numerous significant competitors, such as Arrow, Tech Data and the ALSO group, the proposed operation will not have any effect on the market for the distribution of all IT products in the EEA.

36. On narrower markets for the distribution of specific categories of IT products at the regional level, the merged entity's combined market share does not exceed 15%, except for the following markets:

Region | IT product and service category | Avnet | Bell Micro | Combined market share |

Benelux | Storage products | [0-5]% | [30-40]% | [30-40]% |

Austria, Germany, Switzerland | Mid range servers | [20-30]% | [0-5]% | [20-30]% |

Storage products | [10-20]% | [10-20]% | [20-30]% | |

UK, Ireland | Servers | [10-20]% | [10-20]% | [20-30]% |

Mid range servers | [20-30]% | [5-10]% | [30-40]% | |

Entry level servers | [0-5]% | [10-20]% | [20-30]% | |

Storage products | [5-10]% | [10-20]% | [20-30]% |

37. For those regional markets where the merged entity's combined market share is above 15%, the Commission considers that there are no competition problems for the reasons outlined at paragraphs 41-48 below.

38. At the national level, the parties' activities in the distribution of IT products overlap in the thirteen EEA countries: Austria, Belgium, Czech Republic, France, Germany, Hungary, Ireland, the Netherlands, Poland, Romania, Slovak Republic, Spain and the UK. However, in four of them (namely the Czech Republic, Poland, Romania and Slovak Republic), Bell Micro's sales of IT products remain marginal even though it has been present on these markets for a number of years17. Accordingly, the proposed operation will not change the structure of competition in these countries.

39. On a market for the distribution of specific categories of IT products and services at the national level other than those four countries where Bell Micro's sales are marginal, the merged entity's combined market share do not exceed 15%, except for the following markets:

Member State | IT product category | Avnet | Bell Micro | Combined market share |

Austria | Storage products | [10-20]% | [5-10]% | [20-30]% |

Germany | Storage products | [10-20]% | [10-20]% | [20-30]% |

Hungary | Storage products | [20-30]% | [0-5]% | [20-30]% |

Ireland | Storage products | [0-5]% | [10-20]% | [10-20]% |

the Netherlands | Storage products | [5-10]% | [40-50]% | [50-60]% |

UK | Servers | [10-20]% | [10-20]% | [30-40]% |

Mid range servers | [30-40]% | [10-20]% | [40-50]% | |

Entry level servers | [5-10]% | [20-30]% | [20-30]% | |

Storage products | [10-20]% | [10-20]% | [20-30]% |

40. Despite the merged entity's high combined market shares in the distribution of storage products in the Netherlands ([50-60]%) and in the distribution of mid range servers in the UK ([40-50]%), and the relatively high market shares on certain regional markets (see paragraph 36 above) the proposed operation will not lead to any anticompetitive effects due to the characteristics of these markets.

41. First, the Commission's market investigation confirms that the distribution of IT products in these EEA countries and regions is highly competitive with a significant number of distributors competing to supply VARs, SIs and other large accounts. The merged entity will continue to face competition from numerous other VADs. These include generally companies with a pan-European footprint such as Tech Data, Ingram Micro and Arrow, as well as important companies with a more regional or national focus.

42. On the market for the distribution of storage products in the Netherlands, the main competitors of the parties are Ingram Micro (15%-20%), Copaco (10%-15%), ETC (5%- 10%), Magirus (5%-10%) and Tech Data (5%-10%).

43. On the market for the distribution of mid range servers in the UK, the main competitors of the parties are SCH Group (ETC and ISI) (10%-20%), Arrow (10%-20%), Tech Data (10%-20%) and Westcoast (5%-10%).

44. As regards the affected markets (national and regional) indicated above, all respondents to the Commission's market investigation with one exception consider that the distribution of servers and storage products are characterised by substantial intra-brand and inter-brand competition. None of the vendors and clients (VARs, SIs) that replied to the Commission's market investigation expects this proposed operation to have anticompetitive effects on the distribution of servers, as well as on the distribution of storage products in the EEA, in regions within the EEA and in the EEA countries.

45. Second, vendors exert an important competitive constraint on VADs. The Commission's market investigation has confirmed that vendors have contractual relationships with multiple partners in every country, so as to grant VARs, SIs and large accounts a choice of VADs. Contracts between vendors and VADs can be terminated for no cause with a notice period (generally […] days) and at little cost. Vendors do change their distribution arrangements terminating their relationship with some distributors and appointing new ones. Vendors also exert some control over the conditions and price at which distributors can resell their IT products.

46. Third, the Commission's market investigation has confirmed the notifying party's claim that VARs themselves also exert constraints on VADs as VARs can turn directly to vendors if VADs increase their prices, in particular for major VARs (sometimes referred to as 'Tier-1 VARs'). Most VARs indicate that they consider themselves as competitors of certain distributors (4 out of 5 respondents). All of them have switched suppliers (from one distributor to another distributor or from a distributor to a vendor) over the past 3 years. Only one respondent indicated that it cannot turn directly to vendors in case of prices increases.

47. Fourth, the Commission's market investigation has suggested that barriers to entry and expansion in the distribution of specific IT products are relatively low. VADs that replied to the market investigation indicated that they generally would be able to meet an increase in demand for servers and data storage products in the event of a price increase by the merged entity. Existing VADs can also relatively easily extend their product range and would obtain support from vendors to do so. The only potential barrier to entry for a VAD is the need to obtain vendor licences to distribute products within a particular geographic area. As indicated by a respondent, "to the extent that a distributor does seek to obtain licences, this barrier is not significant, as vendors have an interest in maintaining as broad a range of routes to market as possible. Accordingly, they will contract with a number of distributors in any given geographic area and readily change distribution arrangements where they believe one of their existing partners is underperforming". This point has been largely confirmed by the vendors that replied to the market investigation: the great majority of the vendors who replied to the Commission's market investigation explicitly stated that they would appoint additional VADs/VARs if the merged entity increases the prices at which it sells their products

48. The notifying party has provided a list of recent entrants in the markets concerned in the period from 2007 to 2010, such as Arrow, Ingram and Hammer in the UK, Distrilogie, Green Data and Hammer in the Netherlands, Green Data in Germany and Arrow in Austria. Accordingly, the Commission considers that there are relatively low barriers to entry in these markets.

49. In view of all the above, it can therefore be concluded that the proposed operation does not give rise to serious doubts as to compatibility with the internal market on any of the alternative markets for the distribution of IT products.

VI. CONCLUSION

50. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty

on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the

replacement of "Community" by "Union" and "common market" by "internal market". The

terminology of the TFEU will be used throughout this decision.

2 Turnover calculated in accordance with Article 5(1) of the Merger Regulation.

3 See Case COMP/M.5162 - Avnet/Horizon Technology, 26 June 2008, paragraph 9.

4 Some larger SIs only offer services ('pure SIs'), in which case they will then rely on VADs, VARs or

vendors to supply the IT products. All other SIs act as VARs, which offer both products and services.

5 Case COMP/M.5091 - Tech Data/Scribona, 28 April 2008, paragraph 19; Case COMP/M.5099 - Arrow

Electronics/Logix, 19 May 2008, paragraph 17; Case COMP/M.5162 - Avnet/Horizon Technology, 26

June 2008, paragraph 12.

6 COMP/M.5091 - Tech Data/ Scribona, 28 April 2008, paragraph 19.

7 COMP/M.5099 - Arrow Electronics/ Logix, 19 May 2008, paragraph 17.

8 10 out of 19 respondents.

9 COMP/M.5162 - Avnet/Horizon Technology, 26 June 2008, paragraph 14; COMP/M.5099 – Arrow

Electronix/Logix, 19 May 2008, paragraph 19; COMP/M.5091 – Tech Data/Scribona, 28 April 2008,

paragraph 22.

10 COMP/M.5162 – Avnet/Horizon Technology, 26 June 2008, paragraph 13, COMP/M.2223 –

Getronics/Hagemeyer/JV, 2 April 2001, paragraphs 14 to 16.

11 IDC defines "Enterprise Storage Systems" as a set of storage elements, including controllers, cables, and

(in some instances) a host bus adapter associated with three or more mass storage devices (hard disk

drives or solid state drives). IDC Report, Worldwide Enterprise Storage Systems 2009-2013 Forecast:

Economic Crisis Driving Quest for Storage Efficiency and Emerging Architectures.

12 11 out of 13 respondents consider that VADs need specific skills in order to distribute different IT

products. A similar ratio (10 out of 13) considers that VADs need specific skills in order to distribute each

of entry-level, mid range and high end servers.

13 COMP/M.5162 - Avnet/Horizon Technology, 26 June 2008, paragraph 17; COMP/M.5099 – Arrow

Electronix/Logix, 19 May 2008, paragraph 24; COMP/M.5091 – Tech Data/Scribona, 28 April 2008,

paragraph 28.

14 12 out of 19 respondents consider that the geographic scope of the distribution of IT products is EEA-

wide.

15 14 out of 19 respondents consider that a local presence is not a requirement for the distribution of IT

products.

16 The notifying party has provided market shares on the basis of two IDC reports: IDC Report, November

2009, and the IDC Report dated April 2006, entitled "An Overview of IT Distribution in Western Europe

Country Channel Development Forecasts 2005/2010". The data contained in this second report have been

adjusted to take into account the overall market size decrease in server sales in 2009.

17 Bell Micro started its activities in Poland and the Slovak Republic in November 2001, in the Czech

Republic in October 2002, and in Hungary in June 2004.