Commission, July 16, 2012, No M.6561

EUROPEAN COMMISSION

Judgment

CYTEC INDUSTRIES/ UMECO

Dear Sir/Madam,

Subject: Case No COMP/M.6561 – Cytec Industries/ Umeco

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041

1. On 11 June 2012, the European Commission received notification of a proposed concentration pursuant to Article 4, and following a referral request pursuant to Article 4(5), of the Merger Regulation by which the undertaking Cytec Industries Inc. ("Cytec", United States of America) acquires, within the meaning of Article 3(1)(b) of the Merger Regulation, sole control of the whole of Umeco Plc ("Umeco", United Kingdom). Cytec is hereinafter designated as the "notifying party" and together with Umeco as the "parties".

1. THE PARTIES

2. Cytec is a US-based global speciality chemicals and materials company listed on the New York Stock Exchange. It develops and supplies value-added products including composite materials and adhesives to a wide range of industries.

3. Umeco is a company registered in England and Wales and listed on the London Stock Exchange. It is a global manufacturer and supplier of composite materials, primarily to the aerospace and defence, industrial, automotive and recreational industries.

2. THE OPERATION AND CONCENTRATION

4. On 12 April 2012, Cytec made a binding offer to acquire the entire issued and to be issued share capital of Umeco. The offer, which was unanimously recommended by Umeco's Board of Directors, was approved by Umeco's shareholders on 28 May 2012.

5. As a result of its acquisition of the entirety of Umeco’s share capital, Cytec will acquire sole control over Umeco. The transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

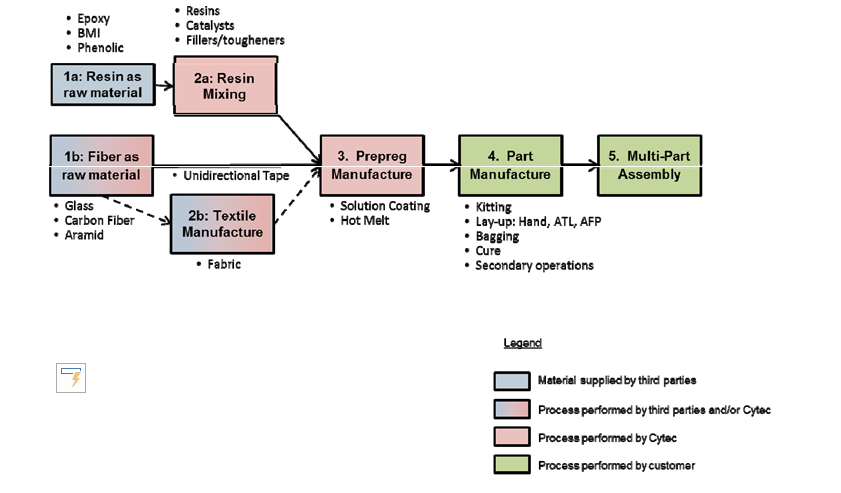

3. EU DIMENSION

6. The operation does not have an EU dimension within the meaning of either Article 1(2) or Article 1(3) of the Merger Regulation because in 2011: (i) Umeco’s EU turnover […] did not exceed EUR 250 million; and (ii) although the combined aggregate turnover of all the undertakings concerned exceeded EUR 100 million in three Member States […], Umeco's turnover exceeded EUR 25 million in only one of these Member States […].

7. However, on 27 April 2012, the Commission received, by means of a reasoned submission, a referral request from Cytec pursuant to Article 4(5) of the Merger Regulation with respect to the transaction. Cytec informed the Commission that the concentration was capable of being reviewed under the national competition laws of three Member States […] and under the national merger control law of […].

8. A copy of this submission was promptly transmitted to the competition authorities of the Member States and the EFTA Surveillance Authority. As none of the Member States competent to review the concentration expressed its disagreement with the request for referral within the period laid down by the Merger Regulation, the notified operation has an EU dimension pursuant to Article 4(5) of the Merger Regulation.

4. ASSESSMENT

4.1. Introduction

4.1.1. Advanced Composite Materials and Prepregs

9. Both Cytec and Umeco manufacture advanced composite materials (“ACMs”).

10. An ACM typically comprises a combination of: (i) a textile i.e. a unidirectional tape or woven fabric made from high performance fibre reinforcement material, typically carbon; and (ii) a formulated resin system used to support and bond the fibres in a composite. A composite is thus a combination of a specific fibre and a formulated resin matrix in calculated proportions resulting in a material with a unique combination of properties.

11. ACMs exhibit, to varying degrees, a number of desirable properties, including light weight, high stiffness, high strength, dimensional stability, configurability into complex shapes, temperature and chemical resistance, flex performance, high corrosion resistance and low thermal expansion.

12. According to the notifying party, ACMs are replacing conventional metal materials such as aluminium and steel in the manufacture of components in a growing number of applications, including: (i) military and civil aerospace applications; (ii) industrial applications (including automotive components); and (iii) recreational applications (including skis and tennis racquets).

13. The main area of competitive overlap between the parties is in the supply of prepregs, one of several product forms/technologies for the delivery of ACM. A prepreg is a composite in which a carbon, aramid or glass fibre reinforcement is impregnated (hence the name prepreg) by a manufacturer at a pre-determined level with a formulated resin system. The prepreg is then delivered to a customer, which moulds it into a finished part.2

14.Figure 1 below3 illustrates the complete value chain in the production of prepregs, from inputs to end use, and highlights Cytec’s own activities in this value chain.

Figure 1: Value chain in the production of prepregs

4.1.2. Other products manufactured by the parties

15. The parties manufacture a number of other products.

16. First, Cytec,4 but not Umeco, manufactures carbon fibre, one of the two main inputs into prepregs.5

17. Second, the parties supply limited volumes of formulated resins for use in Resin Transfer Moulding ("RTM") composites.

18. Third, Umeco,6 but not Cytec, supplies composite moulding tools, for which prepreg materials may be used as an input. There is thus a vertical link between the activities of the parties in relation to the supply of prepregs for use in moulding tools.

19. Fourth, Umeco, but not Cytec, sells process materials7 used by customers in the manufacture of a part (see box 4 of Figure 1 above). The notified operation will not, however, raise any vertical concerns as process materials are not an input in the manufacture of prepregs.

20. Finally, Cytec supplies adhesives used for bonding and surfacing advanced composite components and metal components in structures while Umeco sells limited amounts of structural film adhesives.

4.2. Product market definition

4.2.1. Advanced Composite Materials and prepregs

4.2.1.1. Past Commission decisions

21. In previous decisions, the Commission has assessed the scope of the relevant markets for certain upstream inputs of prepregs, including carbon fibres8 and resins.9 The Commission has also assessed the market for formulated resin system, a neighbouring product to prepregs.10

22. The Commission has, however, never considered in detail the scope of the relevant product market for either ACMs in general or prepregs in particular.

4.2.1.2. The notifying party's submission

23. The notifying party submits that it can be left open whether a relevant market for prepregs exists as the proposed concentration does not raise competition concerns on such a market.

24. Moreover, the notifying party submits that the market for prepregs should not be further sub-segmented by reference to materials (fibres and/or resins), end application and/or prepreg properties and characteristics (e.g. heat resistance). Although prepreg solutions are often interchangeable from the perspective of customers, products originally developed for a given application (e.g. aerospace) can often subsequently be used in a variety of different applications. In addition, while the parties have a focus on certain end-use applications (aerospace applications for Cytec, certain niche industrial applications such as the automotive industry for Umeco), other manufacturers supply a portfolio of prepregs across a range of applications and chemical or physical characteristics.

4.2.1.3. The responses to the market investigation

25. Nearly all of the respondents to the market investigation indicated that a relevant sub- market for prepregs exists within the relevant product market for ACMs.

26. As regards a possible segmentation of the market for prepregs by production methods, while most suppliers indicated that they offer a range of prepregs suitable for various moulding methods and curing processes, a limited majority of customers indicated that they do not consider prepregs suitable for various moulding methods to be substitutable.11

27. As regards a possible segmentation of prepregs by resin types, a majority of customers indicated that they do not consider prepregs made from different resin types to be substitutable. Rather, these customers would select a particular resin type and production method according to their needs and subsequent switching would be limited.12 As for suppliers, an overwhelming majority of those that responded to the market investigation indicated that while most manufacturers use epoxy in their prepregs and a few also use phenolic and cyanate ester resins, other types of resins are used only by a very limited number of manufacturers.13 A limited majority of suppliers also explained that it was possible for them to switch production from a prepreg based on a given resin type to a prepreg based on another resin type on short notice and without incurring a significant investment.14

28. As regards a possible segmentation of prepregs by production method, while a large majority of prepreg customers in the aerospace sector consider prepregs based on different manufacturing techniques to be substitutable,15 a large majority of customers in the automotive sector do not.16 As for suppliers, a significant majority of those that responded to the market investigation indicated that while most suppliers supply prepregs manufactured according to one of the two main production methods (solution coating and film transfer/hot melt),17 it is not possible for them to switch on short notice from one manufacturing technique to the other without incurring a significant investment.18

29. As regards a possible segmentation of prepregs by application, an overwhelming majority of customers that responded to the market investigation indicated that there are significant price and/or technical differences between: (i) prepregs for the aerospace industry and prepregs for the automotive industry;19 (ii) between prepregs for interiors in the aerospace industry, prepregs for primary structures in the aerospace industry and prepregs for secondary structures in the aerospace industry;20 and (iii) prepregs for racing cars (e.g. Formula One) and prepregs for other for other automotive applications.21

30. As for suppliers, an overwhelming majority of those that responded to the market investigation indicated that they are unable to switch, on short notice and without incurring a significant investment: (i) from the supply of prepregs for automotive applications to the supply of prepregs for aerospace applications;22 (ii) from the supply of prepregs for a given aerospace application (e.g. interiors) to the supply of prepregs for another aerospace application (e.g. primary structures); (iii) from the supply of prepregs for commercial aircraft to the supply of prepregs for military aircraft;23 and (iv) from the supply of prepregs for one type of aerospace applications to the supply of prepregs for another aerospace application.24

31. By contrast, a limited majority of suppliers indicated that they are able to switch, on short notice and without incurring a significant investment: (i) from the supply of prepregs for aerospace applications to the supply of prepregs for automotive applications;25 and (ii) from the supply of prepregs for race cars to the supply of prepregs for other automotive applications.26 These suppliers also indicated that for companies already supplying prepregs for other automotive applications, barriers to expansion into the market for the supply of race cars are low,27 as are barriers to expansion for companies already supplying prepregs for aerospace applications into the market for the supply of prepregs for automotive applications. 28

4.2.1.4. Conclusion

32. Since the concentration does not raise serious doubts under any possible approach, the exact product market definition in this case can be left open.

4.2.2. Moulding tools

4.2.2.1. Past Commission decisions

33. The Commission has never previously considered the scope of the relevant product market for moulding tools.

4.2.2.2. The notifying party's submission

34. The notifying party submits that the majority of prepregs do not require specific types of moulding tools in order to be processed into finished parts by customers. In particular, the notifying party considers that most prepregs can be moulded on any type of composite moulding tool, be they metal or composite moulding tools.

4.2.2.3. The responses to the market investigation

35. A large majority of customers that responded to the market investigation indicated that there are significant price and/or technical differences between metal moulding tools and composite moulding tools.29 This was confirmed by an overwhelming majority of suppliers which consider that faced with a non-transitory 5-10% increase in the price of composite moulding tools, customers would not switch to metal moulding tools.30

4.2.2.4. Conclusion

36. Since the concentration does not raise serious doubts under any possible approach, the exact product market definition in this case can be left open.

4.2.3. Film adhesives used in association with prepregs tools

4.2.3.1. Past Commission decisions

37. The Commission has never previously considered the scope of the relevant product market for film adhesives used in association with prepregs.

4.2.3.2. The notifying party's submission

38. The notifying party submits that four different types of adhesive are used in association with prepregs: (i) film adhesives; (ii) paste adhesives; (iii) sealants; and (iv) potting compounds.

39. The notifying party considers that the relevant product market is not narrower than the market for all film adhesives. Although at customer level, film adhesives are not substitutable for other types of adhesives, manufacturers of film adhesives also manufacture other types of adhesives (although the reverse is not necessarily true).

40. In addition, the notifying party considers that it would not be appropriate to further sub-segment the market for film adhesives by application or end use because the same film adhesives are used, for example, in aerospace, construction and automotive applications.

4.2.3.3. The responses to the market investigation

41. An overwhelming majority of respondents to the market investigation confirmed the notifying party’s claim that different adhesives are not substitutable from the point of view of customers. First, film adhesives, paste adhesives and potting compounds have a structural function31 and are not substitutable. Second, sealants are less expensive, have no structural function and are used to get water or air tightness.32 Third, variations in price and technical equipment appear to be significant.

42. As for adhesive manufacturers, they highlighted the difficulty of switching from the production of one type of adhesive to another as this requires specific manufacturing lines. Adhesives are qualified on a suite of physical, mechanical and chemical characteristics which are difficult to replicate from one to the other.33

4.2.3.4. Conclusion

43. Since the concentration does not raise serious doubts under any possible approach, the exact product market definition in this case can be left open.

4.3. Geographic market definition

4.3.1. Advanced Composite Materials and prepregs

44. In previous decisions the Commission has assessed the scope of the relevant geographic markets for certain upstream inputs of prepregs, including carbon fibres34 and resins.35 The Commission has also assessed the relevant geographic market for formulated resin system, a neighbouring product to prepregs.36

45. The Commission has, however, never considered in detail the scope of the relevant geographic market for ACMs in general or prepregs in particular.

46. The notifying party considers that the geographic scope of the market for the supply of ACMs/prepregs to be worldwide or, at the very least, EEA-wide, in line with the Commission’s findings in relation to formulated resin systems in Hexion/Huntsman. The notifying party emphasises that: (i) the main prepreg suppliers operate globally and sell to customers throughout the world; (ii) transport costs are low as a proportion of product value; and (iii) prices do not vary significantly between regions.

47. While a minority of customers that responded to the market investigation, in particular customers for Formula One applications, consider it important for a prepreg supplier to have a production plant located close to its customers,37 the vast majority of respondents, particularly aerospace customers, indicated that they source within the EEA or even globally.38 As for suppliers, an overwhelming majority of those that responded to the market investigation indicated that given transportation costs and tariffs, prepregs can be viably supplied to customers at least throughout the EEA, if not globally.39

48. Since the concentration does not raise serious doubts under any possible approach, the exact geographic market definition in this case can be left open.

4.3.2. Moulding tools

49. The notifying party submits that the proposed transaction does not raise any competition concerns even on the basis of a geographic market that is EEA-wide in scope.

50. For the purposes of the decision, however, as the concentration does not raise serious doubts under any possible approach (i.e. EEA-wide or worldwide), the exact geographic market definition can be left open.

4.3.3. Film adhesives used in association with prepregs tools

51. The Commission has never considered in detail the scope of the relevant geographic market for film adhesives used in association with prepregs tools.

52. The notifying party considers the scope of the relevant geographic market for film adhesives used in association with prepregs tools to be at least EEA-wide, if not worldwide, on the basis that adhesives are sold on a global basis and can be quickly and cheaply transported between regions.

53. A significant majority of the respondents to the market investigation indicated that distribution and logistics for adhesives and film adhesives used in association with prepregs are organised on a worldwide basis. They also stated that film adhesives can be viably supplied to customers on a worldwide basis. Finally, they noted that prices appear to be negotiated at least on an EEA-wide basis, if not globally.40

54. Since the concentration does not raise serious doubts under any possible approach, the exact geographic market definition in this case can be left open.

4.4. Competitive Assessment

4.4.1. Prepregs

55. The notified operation gives rise to a potentially horizontally affected product market with regard to the hypothetical market for all prepregs, as the combined 2011 market share of the parties was [30-40]% worldwide and [20-30]% at EEA-level.

56. The notified operation also gives rise to potentially horizontally affected markets with regard to the following hypothetical sub-segments: (i) all aerospace applications (worldwide [30-40]%, EEA [30-40]%); (ii) aerospace secondary structures (worldwide [40-50]%, EEA [30-40]%); (iii) aerospace interiors41 (worldwide [30- 40]%) (iv) all automotive applications (worldwide [20-30]%, EEA [30-40]%); and (v) automotive Formula One (worldwide [90-100]%, EEA [90-100]%).

4.4.1.1. The market for all prepregs

57. The overlap between the activities of the parties on the hypothetical market for all prepregs does not give rise to serious doubts, both on an EEA-wide and worldwide basis.

58. First, the EEA and worldwide markets for all prepregs are characterised by the presence of several suppliers,42 including recent entrants, the majority of whom are capable of supplying a wide range of prepregs for use in different applications.

59. Second, major prepreg manufacturers are able to produce a wide range of products responsive to customer demand. Suppliers are also able to compete across the range of constituent components and of end-use applications, even if at a given time, certain suppliers may focus on specific prepreg applications rather than others.

60. Finally, there is a degree of complementarity between the activities of the parties, as Cytec has its main focus in aerospace while Umeco focuses especially on the supply of certain niche industrial applications such as the automotive industry.

4.4.1.2. The market for prepreg aerospace applications and its possible further sub-segments

61. The overlap between the activities of the parties on the hypothetical market for prepreg aerospace applications and its possible sub-segments (prepregs for aerospace interiors, prepregs for aerospace primary structures and prepregs for aerospace secondary structures) does not give rise to serious doubts, both on an EEA-wide and worldwide basis.

62. First, the increment on the market for prepreg aerospace applications is relatively low due to Umeco's limited presence in this market (worldwide [0-5]%, EEA: [0-5]%).

63. Second, the market for prepreg aerospace applications and its possible sub-segments are characterised by the presence of a number of competing suppliers.43

64. Third, Umeco is not present in aerospace primary structures and is only a marginal player in aerospace secondary structures (worldwide [0-5]%, EEA: [0-5]%).

65. Fourth, an overwhelming majority of respondents to the market investigation indicated that Cytec's closest competitor on the market for prepreg aerospace applications is not Umeco but Hexcel and Toray.44

66. Fifth, the majority of supply is determined by tenders organised by large customers such as […] and […]. These customers thus enjoy a certain degree of buyer power vis-à-vis suppliers of prepregs for aerospace applications. This buyer power will not change post- transaction.

67. Finally, two respondents to market investigation considered that the transaction may have positive effects on competition as it will result in the emergence of a supplier that will better be able to meet customer needs.45

4.4.1.3. The overall market for prepreg automotive applications

68. The overlap between the activities of the parties on the hypothetical overall market for prepreg automotive applications does not give rise to serious doubts, both on an EEA- wide and worldwide basis.

69. First, the overall market for prepreg automotive applications is characterised by the presence of a number of competing suppliers.46

70. Second, no supplier of prepregs for automotive applications appears to enjoy a particular technical advantage over the others and all are capable of responding to the requirements of customers. In particular, all major prepreg manufacturers, even those not currently focused on automotive applications, have the technology platforms and existing prepreg product ranges to supply prepregs to automotive customers.47

71. Third, automotive customers enjoy a certain degree of buyer power vis-à-vis suppliers of prepregs for automotive applications and this will not change post-transaction.48

4.4.1.4. The sub-segment of prepregs for Formula One applications

72. The overlap between the activities of the parties on the hypothetical sub-segment of prepregs for Formula One applications, where the combined worldwide and EEA market shares of the parties are high,49 does not give rise to serious doubts, both on an EEA-wide and worldwide basis.

73. First, there are a number of competing suppliers which currently supply Formula One and/or other segments and that could enter and/or expand into the Formula One sub- segment within a reasonably50 short period of time.51

74. Second, Formula One customers indicated that in the event of a non-transitory 5-10% increase in the price of prepregs, they could find other sources of supply.52

75. Third, several prepreg suppliers showed an interest in entering this sub-segment and regarded themselves as potential entrants.53

76. Fourth, Formula One customers enjoy a certain degree of buyer power vis-à-vis prepreg suppliers for Formula One applications and this will not change post-transaction.54

77. Finally, several respondents to the market investigation characterised the Formula One sub-segment as a "bridge" between aerospace and industrial applications and a driver for innovation. Being a Formula One prepreg supplier is also regarded as a matter of prestige.55

4.4.2. Moulding tools

78. The vertical relationship between the supply of composite moulding tools by Umeco and the supply of prepregs by Cytec does not give rise to serious doubts on either a worldwide or EEA-wide basis.

79. First, composite moulding tools constitute only around 20-30% of the moulding tools market,56 and Umeco’s share of that market at both worldwide and EEA level is less than [5-10]%.57

80. Second, respondents to the market investigation indicated that several existing and credible competitive alternatives exist to composite moulding tools.58 In addition, respondents stated that most competitors of the merged entity can supply prepregs which can be used to manufacture moulding tools.59

4.4.3. Film adhesives used in association with prepregs tools and any of its possible sub-segments

81. The overlap between the activities of the parties on the market for film adhesives used in association with prepregs tools and any of its possible sub-segments does not give rise to serious doubts, both on an EEA-wide and worldwide basis.

82. First, the increment on the overall film adhesive market is low due to Umeco's limited presence in this segment (worldwide [0-5]%, EEA: [0-5]%).60

83. Second, the market for film adhesives is characterised by the presence of a number of competing suppliers, both at worldwide (3M ([20-30]%), Henkel ([10-20]%), Gurit ([5-10]%), MRC ([5-10]%)) and EEA-level (3M ([30-40]%), Henkel ([10-20]%), Gurit ([10-20]%) and Hexcel ([5-10]%)).

84. Third, film adhesive customers generally follow a multi-sourcing strategy in order to mitigate risks in terms of availability and to obtain the best terms from suppliers.61

85. Finally, an overwhelming majority of respondents to the market investigation considered that Cytec's closest competitor on the market for prepreg aerospace applications is not Umeco but Henkel, Hexcel and 3M.62

5. CONCLUSION

86. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 There are several different types of moulding including autoclave moulding, vacuum bag moulding (vacuum bagging), press moulding, pressure bag moulding and thermal expansion moulding.

3 Source: Form CO.

4 Cytec uses captively the majority of its carbon fibre production, with only about [30-40]% of its total fibre production being sold on the merchant market. As Cytec’s market share at worldwide level is [0-5]% and below [0-5]% in the EEA, with total sales amounting to less than […], the possible vertical relationship between Cytec’s supply of carbon fibres and Umeco’s purchase of such fibres will not be further discussed in this Decision. The market investigation, in any case, indicated that the transaction will not give rise to any vertical foreclosure concerns either in the EEA or worldwide.

5 The Commission has previously found that, within the man-made fibres industry, distinct product markets can be distinguished according to application (textile, carpet and industrial) as well as on a fibre-by-fibre basis. See cases IV/M.214 DuPont/ICI, decision of 6 June 1992, recitals 10 and 11; COMP/M.1182 Akzo Nobel/Courtaulds, decision of 22 August 1998, recital 38; COMP/M.2187 CVC/Lenzing, decision of 17 October 2001, recital 18; and COMP/M.3341 Koch/Invista, decision of 21 January 2004, recitals 9 to 14.

6 Umeco sells limited quantities of composite moulding tools which generate revenues in the EEA of less than […]. Umeco’s share of this market at both worldwide and EEA level is limited and not more than [5-10]%.

7 Umeco’s Process Materials segment focuses on the development, manufacture and supply of a range of materials and systems (including custom-made bags and kits and input materials such as films, tapes and valves) used in the vacuum bagging process for curing composite parts, including those manufactured using prepregs, resin infusion and wet lay-up. Umeco’s vacuum bagging film products are also used in applications requiring vacuum compaction including glass lamination and vapour barriers such as food preservation and corrosion inhibition.

8 Cases COMP/M.5484 SGL Carbon/Brembo/BCBS/JV, decision of 27 May 2009, recitals 29 to 31 and 52 to 56; and COMP/M.5712 Mitsubishi Chemical Holdings/Mitsubishi Rayon Co., decision of 25 July 2010, recitals 9 to 16 and 20 to 22.

9 Cases COMP/M.3593 Apollo/Bakelite, decision of 11 April 2005, recitals 8 to 17 and 19 to 25; and COMP/M.4835 Hexion/Huntsman, decision of 30 June 2008, recitals 24 to 35.

10 Case COMP/M.4835 Hexion/Huntsman, decision of 30 June 2008, recitals 34 to 39.

11 Replies to question 11 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector; replies to question 11 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Automotive sector.

12 Replies to question 13 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector; replies to question 13 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Automotive sector.

13 Replies to question 5 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

14 Replies to question 23 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

15 Replies to question 12 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector.

16 Replies to question 12 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Automotive sector.

17 Replies to question 7 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

18 Replies to question 24 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs; replies to question 20 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector; replies to question 19 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Automotive sector.

19 Replies to question 19 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs; replies to question 16 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector; replies to question 16 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Automotive sector.

20 Replies to question 20 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs; replies to question 17 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector.

21 Replies to question 22 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs; replies to question 17 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Automotive sector.

22 Replies to question 27 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

23 Replies to questions 29 and 30 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs; replies to question 22 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector.

24 Replies to question 33 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

25 Replies to question 28 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

26 Replies to question 31 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

27 Replies to question 35 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

28 Replies to question 34 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

29 Replies to question 38 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs; replies to question 26 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector; replies to question 26 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Automotive sector.

30 Replies to question 37 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

31 Structural adhesives are adhesives that are designed to join surfaces forming part of a load-bearing structure. They usually have a higher durability and can withstand heavier loads.

32 Replies to questions 7 and 8 of the Commission’s questionnaire of 14 June 2012 to competitors in adhesives used in association with prepregs; replies to questions 51 to 53 of the Commission’s questionnaire of 14 June 2012 to customers in prepregs and adhesives used in association with prepregs.

33 Replies to questions 9 and 10 of the Commission’s questionnaire of 13 June 2012 to competitors in adhesives used in association with prepregs; replies to questions 54 and 55 of the Commission’s questionnaire of 14 June 2012 to customers in prepregs and adhesives used in association with prepregs.

34 Cases COMP/M.5484 SGL Carbon/Brembo/BCBS/JV, decision of 27 May 2009, recitals 29 to 31 and 52 to 56; and COMP/M.5712 Mitsubishi Chemical Holdings/Mitsubishi Rayon Co., decision of 25 July 2010, recitals 9 to 16 and 34 to 39.

35 Cases COMP/M.3593 Apollo/Bakelite, decision of 11 April 2005, recitals 8 to 17 and 19 to 25; and COMP/M.4835 Hexion/Huntsman, decision of 30 June 2008, recitals 24 to 35.

36 Case COMP/M.4835 Hexion/Huntsman, decision of 30 June 2008, recitals 34 to 39.

37 Replies to questions 42 and 43 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

38 Replies to question 44 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs; replies to questions 31 and 33 of the Commission’s customers of prepregs and adhesives used in association with prepregs – Aerospace sector.

39 Replies to question 43 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs; replies to question 30 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs – Aerospace sector; replies to question 42 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

40 Replies to questions 13, 14, 15 and 18 of the Commission’s questionnaire of 14 June 2012 to competitors in adhesives used in association with prepregs; replies to questions 58, 59, 60 and 63 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs.

41 The potential product market for aerospace interiors in the EEA would not be affected as the merged entity's market share would remain below 15% (Cytec [0-5]%, Umeco [0-5]%).

42 Hexcel (worldwide [20-30]%, EEA [20-30]%), Toray (worldwide [10-20]%, EEA [10-20]%), Gurit (worldwide [5-10]%, EEA [10-20]%) and TenCate (worldwide [5-10]%, EEA [10-20]%).

43 (i) Market for prepreg aerospace applications: Hexcel (worldwide [30-40]%, EEA [30-40]%), Toray (worldwide [10-20]%, EEA [5-10]%), Gurit (worldwide [0-5]%, EEA [5-10]%), TenCate (worldwide [5-10]%, EEA [10-20]%); (ii) market for prepregs for aerospace interiors: Hexcel (worldwide [0-5]%, EEA [0-5]%), Gurit (worldwide [20-30]%, EEA [40-50]%), TenCate (worldwide [10-20]%, EEA [20-30]%), MC Gill (worldwide [5-10]%, EEA [5-10]%); (iii) market for prepregs for aerospace primary structures; (iv) market for prepregs for aerospace secondary structures: Hexcel (worldwide [40-50]%, EEA [40-50]%), Toray (worldwide [0-5]%, EEA [5-10]%), Gurit (worldwide [0-5]%, EEA [0-5]%), TenCate (worldwide [5-10]%, EEA [0-5]%).

44 Replies to question 36 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs - Aerospace sector.

45 See customer non-confidential reply to question 44 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs in Aerospace sector.

46 Hexcel (worldwide [10-20]%, EEA [10-20]%), Toray (worldwide [20-30]%, EEA [0-5]%), Gurit (worldwide [5-10]%, EEA [5-10]%), DeltaPreg (worldwide [5-10]%, EEA [10-20]%).

47 See replies to question 36.2 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs.

48 Replies to questions 37 and 38 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs.

49 Umeco: EEA [70-80]%; Cytec: EEA [20-30]%; Amber Composites: EEA [0-5]%, DeltaPreg: EEA [0-5]%. See parties' submission of 3 July 2012. As only one Formula One customer is currently located outside the EEA, worldwide market shares are unlikely to significantly differ from those in the EEA. Hexcel used to be active in the Formula One segment but withdrew from this specific market niche in 2002.

50 The Formula One prepreg segment is characterised by supply contracts of […] in duration.

51 Within one year according to one respondent. By contrast, establishing a solid supplier relationship would take between two to three years. See also minutes of phone call of 2 July 2012 with Mr Roger Sloman, who is a well-known and early promoter of the use of advanced composite materials in Formula One racing cars, and founder of ACG, Umeco's predecessor. Another respondent claimed that the qualification process with the FIA could last between six to twelve months. See minutes of phone call of 29 June 2012 with Saati Composites.

52 See minutes of phone call of 26 June 2012 with […]; minutes of phone call of 28 June 2012 with […]; and minutes of phone call of 29 June 2012 with […].

53 See minutes of phone call of 29 June 2012 with […]; and minutes of phone call of 29 June 2012 with […].

54 Replies to question 37.2 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs.

55 Customer reply to question 37.3 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs: "Formula is the pinnacle of technology and hence is a technical showcase for supplier of this nature." See also the minutes of phone call of 29 June 2012 with Amber Composites.

56 While Composite tools are more expensive than metal tools and less durable, they are also lighter and can be easier to shape into large and complex structures.

57 Cytec is not active in this market as it does not manufacture or supply moulding tools (either composite-based or otherwise).

58 Replies to questions 9 and 64 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

59 Replies to question 10 of the Commission’s questionnaire of 13 June 2012 to competitors in prepregs.

60 Similarly, for all adhesives Umeco’s total sales reflect a market share of less than [0-5]% at both worldwide and EEA level.

61 Replies to question 68 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs.

62 Replies to question 22 of the Commission’s questionnaire of 14 June 2012 to competitors in adhesives used in association with prepregs; replies to question 65 of the Commission’s questionnaire of 14 June 2012 to customers of prepregs and adhesives used in association with prepregs.