Commission, September 3, 2012, No M.6581

EUROPEAN COMMISSION

Judgment

GKN / VOLVO AERO

Dear Sir/Madam,

Subject: Case No COMP/M.6581-GKN / Volvo Aero

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041

1. On 27 July 2012 the European Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which GKN Holdings plc (the United Kingdom), controlled by GKN plc ("GKN", the United Kingdom) acquires, within the meaning of Article 3(1)(b) of the Merger Regulation, control of the whole of Volvo Aero AB (Sweden) and Volvo Aero Connecticut LLC (the United States) by way of purchase of shares. In the following, Volvo Aero AB and Volvo Aero Connecticut LLC are jointly referred to as "Volvo Aero", while GKN and Volvo Aero are jointly referred to as "the Parties".

I. THE PARTIES

2. GKN is a global engineering company whose technologies and products are incorporated into vehicles and aircraft. GKN's aerospace division supplies engine components and composite aircraft structures such as wings and fuselages. It also provides a complete range of aftermarket services.

3. Volvo Aero is an independent producer of aerospace engine components for commercial and military aircraft engines. It also produces gas turbine components for power generation, as well as components for the space industry. In addition, Volvo Aero provides maintenance, repair and overhaul ("MRO") services for aircraft and gas turbine engines. Finally, Volvo Aero manufactured the RM12 engine for the Gripen fighter jet. Although the production of the RM12 engine has now ceased, Volvo Aero continues to provide a full range of related MRO services for this engine.2

II. THE OPERATION AND CONCENTRATION

4. The proposed transaction concerns the acquisition by GKN of sole control over Volvo Aero. GKN will purchase all the issued shares and outstanding membership interests in the capital of Volvo Aero.

5. Therefore, the transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

III. EU DIMENSION

6. The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million3 (GKN: EUR 6 620 million, Volvo Aero: EUR […] ). Each of them has an EU-wide turnover in excess of EUR 250 million (GKN: EUR […], Volvo Aero: EUR […]), and they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

IV. MARKET DEFINITION

IV.1 Introduction

7. The Parties are active in the production of engine components for commercial and military aircraft for customers worldwide.

8. A distinction can be drawn between the following groups of market players: OEMs, Tier 1 Suppliers and Tier 2 Suppliers:

· OEMs are companies with the capability to both design and manufacture engines. They notably include GE Aviation (a subsidiary of General Electric), Pratt & Whitney ("P&W", a subsidiary of United Technologies Corporation), Rolls-Royce ("RR") and Snecma (a subsidiary of Safran). A number of OEMs have formed alliances to develop particular engine programs or supply specific components. CFM International ("CFMI") and Fabrications Mécaniques de l'Atlantique ("FAMAT") are joint ventures between GE Aviation and Snecma; International Aero Engines ("IAE") is a joint venture between P&W, MTU Aero Engines GmbH ("MTU") and the Japanese Aero Engines Corporation ("JAEC"); and Engine Alliance is a joint venture between GE and P&W for designing, assembling and servicing the GP7000 engine.

· Tier 1 suppliers are companies with the capability to manufacture complete sections of an engine. Notable Tier 1 companies include Volvo Aero, MTU, Spain's Industria de Turbo Propulsores, S.A. ("ITP"),4 Italy's Avio S.p.A. ("Avio"), Japan's Mitsubishi Heavy Industries Ltd ("MHI"), IHI Corporation ("IHI") and Kawasaki Heavy Industries Ltd ("KHI").

· Tier 2 Suppliers are companies which supply OEMs and Tier 1 suppliers with engine parts. These companies can roughly be grouped by the processes they use to produce parts. Machining companies create components using machine tools. They notably include Goodrich Corporation and GKN. Forgers and casting companies forge metal into different shapes or cast metal components from liquid metal. As jet engines typically involve circular or cylindrical parts, forgers' products are often referred to as "ring forgings". Suppliers of such parts notably include the PCC Group and Forgital.

9. It should, however, be noted that both OEMs and Tier 1 suppliers including Volvo Aero retain in-house capability to manufacture individual parts and therefore may compete with Tier 2 suppliers.

10. The proposed transaction will bring together the Parties' following complementary activities:

· Volvo Aero's machined forged metal products and fabrications5 and GKN's expertise in composite technologies;

· The Parties' ancillary strengths (e.g. composite aircraft structures such as wings and fuselages for GKN; rocket engine components for Volvo Aero); and

· Volvo Aero participations in risk and revenue sharing partnerships ("RRSPs") earning a pro rata share of engine sales with GKN's focus on long term agreements ("LTAs") to supply specific components.

11. Consequently, as a result of the transaction, GKN will become an integrated supplier present at Tier 1 and Tier 2 levels.

IV.2 Product market definition

IV.2.1 Aircraft engine components

12. The Commission has previously identified distinct markets for machined parts, fabrications and ring forgings used in aircraft engines.6 However, the question whether each part should constitute a distinct product market was left open.

13. The Commission has also considered segmenting the market for aircraft engine components according to the relevant aircraft mission profile (large commercial aircraft compared to regional aircraft or corporate jets) and the engine use (commercial or military).7 However, that question was also left open.

14. According to GKN, industrial gas turbine ("IGT") components and jet engine components for aircraft are part of a single product market for gas turbines as the companies which machine or produce components for either type of engine are largely the same. GKN considers that the process capability to turn pieces of metal (or carbon fibre) into high- specification components is more important than the question of which specific components a company produces at a given time.

15. Moreover, GKN submits that it is not necessary to distinguish further segments within the market for aero-engine components and IGTs. Whilst GKN recognises that there is often a lack of demand-side substitutability at component level, as specialist components are often developed for a specific engine platform, it points to supply-side substitutability since aero- engine component producers are engaged in the production of a variety of such components. In GKN's view, OEMs tend to approach a component supplier based on that supplier’s ability to supply a number of different engine components to each OEM's specification rather than a supplier's expertise in producing a particular aero-engine component.

16. The market investigation did not confirm that IGT components and aircraft engine components are fully substitutable from the supply side.8 While some respondents recognised that manufacturing processes and technologies are similar, others insisted that aircraft engine components require a specific qualification and certification process by airworthiness authorities which implies significant investments in aero engineering, design systems, material property and characterisation capabilities, capital equipment, and aero quality systems.

17. Similarly, the market investigation did not confirm that various aircraft engine components are substitutable from a supply-side perspective.9 In particular, respondents to the market investigation (both competitors and customers) pointed out that different aircraft engine components require a wide variety of differing engineering expertise, equipment, materials and manufacturing processes. This is because of the different requirements (in terms, for instance, of size, strength, stiffness, durability, fracture toughness, temperature, pressure, environmental factors) that govern the design and manufacture of each aero component.

18. However, the precise market definition in this case can be left open, since even under the narrowest market definition, the concentration does not raise serious doubts.

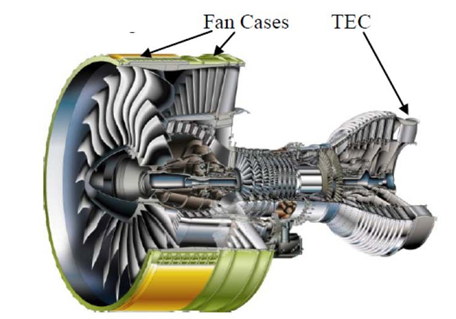

IV.2.2 Fan cases

19. Fan cases (see Figure 1 for an illustration) generally consist of two or three separate components that make up the outer casing structure of a commercial jet engine.

Figure 1: Fan cases and TECs

20. Fan cases are frequently split into "forward" and "rear" fan cases. The primary purpose of forward and rear cases differs slightly. The forward fan case serves as the primary containment vessel in case of a fan blade failure. It also provides both the internal "bypass" air flow surface for the front section of the engine and noise abatement. The rear fan case provides a continuing primary "bypass" air flow, the mounting platform for the exit guide vanes, noise abatement, further primary structure and the mounting surface for the engine controls systems.

21. GKN considers that fan cases are part of a wider market encompassing both IGT and aircraft engine components. A fortiori, it submits that a further distinction between rear and front cases, between metal and composite fan cases or according to the type of aircraft would not be relevant.

22. The market investigation did not confirm that the rear and front cases are fully substitutable from the supply side. Several respondents to the market investigation pointed out that the manufacturing processes required to produce front and rear fan cases can differ significantly, depending on a particular design.10 Front fan cases are thick metal machined forgings, whereas rear fan cases can be made using a range of processes, from sheet metal fabrication to carbon fibre lay-up. Thus the engineering expertise, know-how and equipment required for the different processes may be substantially different.

23. Likewise, the market investigation provided indications that fan cases for large commercial aircrafts and air fan cases for other types of aircraft are not fully substitutable from the supply side.11 Certain respondents to the market investigation indicated that the production of fan cases for large commercial aircraft requires different technical capabilities in terms of engineering expertise and equipment and that design requirements for fan cases are dependent upon engine configuration, physical size and construction, fan speed, engine thrust, and attachment means to the pylon/wing. These requirements may lead to important differences in the fan case design, materials, manufacturing process, quality requirements, and acceptance testing.

24. The market investigation also did not confirm that composite and metal fan cases are substitutable both on the demand and the supply-side.12 On the demand side, an engine must be optimised around the differing stiffness, weight, containment capability and cost of the chosen material. On the supply side, the equipment and know-how required to manufacture fan cases in the different materials are not the same. Metal fan cases are produced and processed using traditional metal machining methods (i.e. milling, turning etc.) while composite fan cases are produced with composite build up (i.e. fabric winding/laying etc.).

25. However, the precise market definition with regards to fan cases can be left open in this case, since the concentration does not raise serious doubts under any possible approach.

IV.2.3 Turbine exhaust cases

26. TECs (see Figure 1 above), also known as Turbine Rear Frames, are the rear structure in a jet engine. The structure serves as the rear primary mount of the engine to the pylon and is manufactured only out of metal due to high temperature requirements. The TEC serves three primary functions in the engine system. First, it provides the rear main structural mount for the rear of the engine. Second, it directs the hot gasses that exhaust from the rear turbine through the vanes to optimise the exit flow in such a way as to optimise the engine's efficiency. Third, it provides the structure support for the rear bearing and the necessary plumbing to provide the bearing section with lubricating oil and cooling air, if so designed.

27. GKN considers that TECs are part of a wider market encompassing both IGT and aircraft engine components. A fortiori, it submits that a further distinction according to the type of aircraft would not be relevant.

28.The market investigation provided indications that TECs for large commercial aircraft and TECs for other types of aircraft are not fully substitutable from a supply-side perspective.13 Similar to the difference in equipment required for large and small fan cases, the scale of components differs between TECs for small and large engines, and therefore the scale of equipment required also differs. Switching from one product to another thus requires specific investments in tooling equipment and the development of stable manufacturing processes, which cannot be executed at short notice.

29. However, the precise market definition with regards to TECs can be left open in this case, since the concentration does not raise serious doubts under any possible approach.

IV. 3 Geographic market definition

30. The Commission has previously considered the relevant geographic market for aero- engine components to be worldwide in scope.14 GKN does not question this approach since transport and delivery costs for engine parts are negligible and customers of such products are active on a worldwide basis. This was also confirmed by the market investigation.15

31. However, the precise geographic definition can be left open in this case, since the concentration does not raise serious doubts under any possible approach.

V. Competitive assessment

V.1 Introduction

32. The proposed transaction leads to horizontally affected markets on the markets for fan cases and TECs. The competitive assessment focuses on the narrowest product market definitions, i.e. fan cases and TECs for large commercial aircraft, since Volvo Aero is not active in the manufacture of aero-engine components for regional aircraft, corporate aircraft and military aircraft.16

33. In addition, the transaction does not result in any vertically affected markets.17

V.2 Fan cases – unilateral effects

34. GKN estimate that, in 2011, producers of fan cases for large commercial aircraft supplied fan cases for […] engines, in a market amounting to EUR […]. The combined 2011 market share of the Parties was [10-20]% if captive sales are included (GKN: [5-10]%, Volvo Aero: [0-5]%) and [30-40]% if captive sales are excluded (GKN: [20-30]%, Volvo Aero: [10-20]%).

35. Table 1 shows the 2011 market share of the Parties and of competitors (including and excluding captive sales18).

Table 1 – Large commercial aircraft fan cases Worldwide market shares by volume – 2011 | ||

Supplier | Market share (incl. captive sales) | Market share (excl. captive sales) |

GKN | [5-10]% | [20-30]% |

Volvo Aero | [0-5]% | [10-20]% |

Combined | [10-20]% | [30-40]% |

FAMAT | [60-70]% | [5-10]% |

KHI | [10-20]% | [40-50]% |

P&W | [0-5]% | [5-10]% |

Goodrich | [0-5]% | [0-5]% |

Source: ACAS data and Parties' estimates | ||

36. If the market for large commercial aircraft fan cases is sub-divided into front and rear cases, the Parties had a combined 2011 market share (including captive sales) of [10-20]% (GKN: [5-10]%, Volvo Aero: [5-10]%) in front cases and [10-20]% (GKN: [5-10]%, Volvo Aero: [0-5]%) in rear cases. If captive sales are excluded, the Parties had a combined 2011 market share of [40-50]% (GKN: [20-30]%, Volvo Aero: [10-20]%) in front cases and [20-30]% (GKN: [20-30]%, Volvo Aero: [0-5]%) in rear cases.

37. Tables 2 and 3 list the 2011 market shares of the Parties and of competitors in front cases and rear cases respectively.

Table 2 – Large commercial aircraft fan cases – front segment Worldwide market shares by volume – 2011 | ||

Supplier | Market share (incl. captive sales) | Market share (excl. captive sales) |

GKN | [5-10]% | [20-30]% |

Volvo Aero | [5-10]% | [10-20]% |

Combined | [10-20]% | [40-50]% |

FAMAT | [50-60]% | [0-5]% |

KHI | [10-20]% | [40-50]% |

Goodrich | [0-5]% | [5-10]% |

P&W | [0-5]% | [5-10]% |

Source: ACAS data and Parties' estimates | ||

Table 3 – Large commercial aircraft fan cases – rear segment Worldwide market shares by volume – 2011 | ||

Supplier | Market share (incl. captive sales) | Market share (excl. captive sales) |

GKN | [5-10]% | [20-30]% |

Volvo Aero | [0-5]% | [0-5]% |

Combined | [10-20]% | [20-30]% |

FAMAT | [60-70]% | [0-5]% |

KHI | [10-20]% | [40-50]% |

Goodrich | [0-5]% | [5-10]% |

P&W | [0-5]% | [0-5]% |

Source: ACAS data and Parties' estimates | ||

38. GKN submits that the fan case market continues to diversify with new market entrants, such as ATK and Forgital. ATK had never competed or supplied before winning the contract to supply fan cases for the GEnx-2B engine that powers Boeing's 747-8 aircraft in 2009/10. ATK was also selected by RR to supply the rear fan case for the Trent XWB engine which will power Airbus's new wide body A350. Forgital succeeded in the tender for RR's Trent XWB forward fan case (where GKN, Volvo Aero, AVIC, Singapore Technologies Aerospace competed).

39. […]. According to GKN, both P&W and RR have in-house capability, while GE and Snecma are also present upstream through their joint venture FAMAT.

40. In general, none of the respondents to the market investigation raised any concerns relating to the impact of the proposed transaction in the market for fan cases or in possible sub- segments for front and rear fan cases. Competing suppliers were unanimous in stating that they did not expect any anti-competitive effect to arise as a result of the proposed transaction. Most customers shared the same view.

41. Furthermore, a majority of customers indicated that neither GKN nor Volvo Aero are able to supply specific types of fan cases for which there is no credible alternative supplier. Indeed, further to the competitors identified by the Parties, the market investigation pointed to the existence of other alternatives, notably a company active in front and rear fan cases, as well as Senior plc, which is active in rear fan cases and has the capability to produce front fan cases. In addition to these, customers listed as alternative suppliers ATK (for composite rear fan cases), FAST, Samsung, SAM and Mecachrome. Moreover, most customers and competitors confirmed that customers have in-house capability. This is in line with the information provided by the Parties, and also appears to be an important element explaining why customers have not shown concerns.

42. It can therefore be concluded that the transaction does not raise serious doubts as to its compatibility with the internal market as regards fan cases.

V.3 TECs – unilateral effects

43. GKN estimates that, in 2011, producers of TECs for large commercial aircraft supplied TECs for […] engines, in a market amounting to EUR […]. The combined 2011 market shares of the Parties was [20-30]% if captive sales are included (GKN: [5-10]%, Volvo Aero: [20-30]%) and [60-70]% if captive sales are excluded (GKN: [10-20]%, Volvo Aero: [50-60]%).

44. Table 3 shows the 2011 market shares of the Parties and of competitors (including and excluding captive sales).

Table 3 – Large commercial aircraft TECs Worldwide market shares by volume – 2011 | ||

Supplier | Market share (incl. captive sales) | Market share (excl. captive sales) |

Volvo Aero | [20-30]% | [50-60]% |

GKN | [5-10]% | [10-20]% |

Combined | [20-30]% | [60-70]% |

Snecma | [50-60]% | [0-5]% |

FAMAT | [5-10]% | [10-20]% |

ITP | [0-5]% | [10-20]% |

Avio | [0-5]% | [5-10]% |

Source: ACAS data and Parties' estimates | ||

45. GKN submits that there is room for entry in the TEC sector, as illustrated by Boeing's recent award of the CFM Leap 1 for its 737 MAX programme to Avio.

46. […]. According to GKN Snecma has internal manufacturing capability and is also present upstream with GE through FAMAT. RR's preferred supplier is ITP, where the company is one of the two shareholders.

47. The vast majority of respondents (competitors and most customers) to the market investigation did not raise any concerns regarding the impact of the proposed transaction.

48. As regards alternative suppliers, a majority of customers indicated that neither GKN nor Volvo Aero are able to supply specific types of TECs for which there is no credible alternative supplier. The investigation confirmed that customers and competitors perceive a number of alternative suppliers, such as Avio, ITP, MTU and MHI. Moreover, as with regard to fan cases, most customers and competitors confirmed that customers have in- house capability.

49. It can therefore be concluded that the transaction does not raise serious doubts as to its compatibility with the internal market as regards TECs.

V. 4 Fan cases and TECs – coordinated effects

50. GKN submits that there is no potential for coordinated effects to arise from the proposed transaction. With a combined share of [0-5]% of an overall market for aero-engine components characterised by numerous competing suppliers, the Parties do not possess market power, have only modest combined shares at the individual component level and deal with large customers who possess considerable buyer power in relation to the Parties with whom they choose to do business. According to GKN, even at the narrow component level, the terms of business and prices are set through competitive tender by OEM customers that have the option of self-supply.

51. None of the customers or competitors that responded to the market investigation raised any issues relating to potential coordination behaviour as a result of the proposed transaction.

52. Therefore, it is unlikely that the transaction would increase the likelihood of any coordinated effects.

V. 5 Conglomerate effects

53. GKN submits that there is no potential for any conglomerate effects. First, the combined product line of the Parties will not be unmatchable, as other large Tier 1 suppliers including Avio and MTU will continue to be able to offer competitive product lines and OEMs will retain the capacity to manufacture their own components. Second, customers of the Parties (engine OEMs) possess buyer power, tend not to contract with one supplier for all of their aero-engine component needs and have the ability to manufacture their own components if they are unsatisfied with a supplier's product offer. Third, barriers to entry are low and the Parties do not possess market power ([0-5]% of the overall market for aero-engine components). Fourth even with regards to TECs, where the combined market share of the Parties is higher, there is no risk that the Parties would be able to leverage this to commercially bundle or tie TECs with their other product offerings since Snecma, FAMAT and ITP will remain strong competitors within the TEC segment.

54. The market investigation confirmed the existence of buyer power and of the procurement behaviour and capabilities of engine OEMs. Furthermore, customers did not express any concern relating to potential conglomerate effects.

55. Therefore, it is concluded that the transaction would not result in any conglomerate effects.

VI. CONCLUSION

56. For the above reasons, the European Commission considers that the notified operation does not raise serious doubts as to its compatibility with the internal market.

57. It has therefore decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 There are no overlaps between the MRO activities of the Parties since the Parties do not provide services for the same engine programmes. These activities are therefore not further addressed in this decision.

3 Turnover calculated in accordance with Article 5(1) of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C95, 16.04.2008, p1).

4 ITP is owned by Sener Aeronáutica (53.125%) and Rolls-Royce plc (46.875%).

5 Fabrications, as opposed to forged or cast metal products, are created by welding metal material forms such as extruded shapes or sheet or plate metal together.

6 Case No COMP/M.4561 - GE/Smiths Aerospace, decision of 23 April 2007, recitals 19–45.

7 Case No COMP/M.4561 - GE/Smiths Aerospace, decision of 23 April 2007, recitals 10 and 44.

8 Replies to questions 8-10 of the Commission’s questionnaire to customers in fan cases and turbine exhaust cases and replies to questions 5-8 of the Commission’s questionnaire to competitors in fan cases and turbine exhaust cases.

9 Replies to questions 11-13 of the Commission’s questionnaire to customers in fan cases and turbine exhaust cases and replies to questions 9-13 of the Commission’s questionnaire to competitors in fan cases and turbine exhaust cases.

10 Replies to questions 14-16 of the Commission’s questionnaire to customers in fan cases and turbine exhaust cases and replies to questions 14-17 of the Commission’s questionnaire to competitors in fan cases and turbine exhaust cases.

11 Replies to questions 17-19 of the Commission’s questionnaire to customers in fan cases and turbine exhaust cases and replies to questions 18-21 of the Commission’s questionnaire to competitors in fan cases and turbine exhaust cases.

12 Replies to questions 20-23 of the Commission’s questionnaire to customers in fan cases and turbine exhaust cases and replies to questions 22-26 of the Commission’s questionnaire to competitors in fan cases and turbine exhaust cases.

13 Replies to questions 24-26 of the Commission’s questionnaire to customers in fan cases and turbine exhaust cases and replies to questions 27-30 of the Commission’s questionnaire to competitors in fan cases and turbine exhaust cases.

14 Commission Decision of 23 April 2007 in Case No COMP/M.4561 - GE/Smiths Aerospace, recitals 23, 32 and 46.

15 Replies to questions 27-30 of the Commission’s questionnaire to customers in fan cases and turbine exhaust cases and replies to questions 31-37 of the Commission’s questionnaire to competitors in fan cases and turbine exhaust cases.

16 Furthermore, while both GKN and Target are active in the market for aero-engine components, GKN estimates that their combined market share in aero-engine components is below 15%, even if this market were to be segmented by engine size, aircraft mission profile or manufacturing method. In IGT components, the activities of the Parties do not overlap in any component.

17 Since the production of RM12 engines has now ceased, the vertical links between the jet engine market (and any segment thereof) and the aero-engine components market (and any segment thereof) will not be further addressed. Furthermore, GKN also manufactures aluminium rolled rings, which can be used for the manufacture of fan cases. Volvo Aero currently purchases rolled rings from […] and its total purchases of aluminium rings amounted to approximately $[…] in 2011, i.e. less than […]% of […] overall output according to Volvo Aero's estimates. GKN submits that even if Volvo Aero's ring-sourcing needs could be and were met by GKN post-transaction, this would have no material effect on the overall market for engine rings since the market for engine rings is highly fragmented, with GKN having [0-5]% market share overall and […] having a [10-20]% market share. In light of these elements, the vertical link relating to GKN's activities in aluminium rolled rings will not be further addressed.

18 Captive sales are those sales realized in "captive" engine programmes, i.e. those for which the component is entirely self-supplied by an OEM or an OEM joint venture. These programmes include the CFM56 (where FAMAT supplies fan cases and Snecma supplies TECs) and PW4000 (where P&W supplies fan cases) programmes.