Commission, December 19, 2012, No M.6765

EUROPEAN COMMISSION

Judgment

PRECISION CASTPARTS / TITANIUM METALS

Dear Sir/Madam,

Subject: Case No COMP/M.6765 – PRECISION CASTPARTS / TITANIUM METALS

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041

1. On 14 November 2012, the European Commission received a notification pursuant to Article 4 of the Merger Regulation of a proposed concentration by which the undertaking Precision Castparts Corp. (“PCC” or the "Notifying Party", USA) will acquire, within the meaning of Article 3(1)(b) of the Merger Regulation, sole control of Titanium Metals Corporation (“Timet”, USA), by way of public bid announced on 9 November 20122. (PCC and Timet are designated hereinafter as the "Parties".)

I. THE PARTIES

2. PCC is a manufacturer of complex metal components and products, including investment castings, forgings and fasteners/fastener systems, for various applications mainly in the aerospace industry but also industrial gas turbine applications, aerostructures, industrial, armament, medical and other applications. PCC's activities in manufacturing titanium-based products are largely concentrated in the aerospace industry. PCC operates 134 manufacturing facilities worldwide and employs 22,400 people in total.

3. Timet is a worldwide producer of a range of titanium-based melted and mill products which are used in various industries. It is also active in the recycling of titanium scrap, primarily for its own internal use. Timet's activities in the field of titanium-based products are largely concentrated in the aerospace sector. Timet has titanium production facilities in both the European Union and the United States.

II. THE OPERATION AND THE CONCENTRATION

4. The proposed transaction is carried out by way of a public tender offer by which PCC will acquire 100% of the outstanding share capital of Timet. As a result, PCC will acquire sole control over Timet, which will in turn become a wholly owned subsidiary within the PCC group. The aggregate total value of the transaction amounts to approximately USD 2.9 billion.

5. The proposed transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of Merger Regulation.

III. EU DIMENSION

6. The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 2 500 million3 (PCC: EUR 6 977 million; Timet: EUR 751 million). In each of at least three Member States, the combined aggregate turnover of the undertakings concerned is more than EUR 100 million.4 In each of these Member States, the aggregate turnover of each of the undertakings concerned is more than EUR 25 million. The aggregate Union- wide turnover of each of the undertakings concerned is more than EUR 100 million. The notified concentration therefore has an EU dimension.

IV. MARKET DEFINITION

IV.1. Introduction

7. Timet is a supplier of titanium producing titanium sponge, titanium melted products (ingots, slab, electrode and scrap, as a by-product of its melting activities) and titanium mill products (long, flat and pipe, rotating and non-rotating products).5 Sponge and scraps are used by Timet internally for the production of melted and mill products and are not sold on the market.6

8. PCC, on the other hand, purchases a number of titanium melted and mill products for its manufacturing activities, in particular for use in the aerospace industry. The proposed transaction therefore relates to the upstream market(s) for the production and supply of titanium inputs and the downstream markets for the production of titanium based products.7 The Commission has not previously considered any of these titanium upstream and downstream product markets.

9. Whilst the main relationship between PCC and Timet is vertical in nature, it should be noted that PCC also produces ingots and electrodes for its own internal use in melted products.8 However, no horizontal overlap arises in this respect since PCC is not active in the market, rather, all of its production is for internal use only.9

10. Ultimately, although the relationship between Timet and PCC is vertical, the key customers at both levels of the supply chain are the aerospace Original Equipment Manufacturers ("OEM"s). A more detailed description of the titanium industry and its main features and dynamics is provided below in sectionV.1.

IV.2. Upstream markets

IV.2.1. Views of the Notifying Party

IV.2.1.1. Product Market Definition

11. The Notifying Party submits that the relevant upstream market is the overall market for the production and sale of titanium products. This overall product market includes all the titanium products which are used in the three different processing stages of titanium products, including (i) titanium raw material products, (ii) titanium melted products, and (iii) titanium mill products.

12. Titanium raw material products include titanium sponge and scrap and are used to produce melted and mill products. Sponges are the commercially pure form of titanium metal, whereas scraps are the by-product of milling and melting operations. Scraps can be split into recyclable and non-recyclable. Recyclable scarps consist of any by-product which can be re-melted and re-used in production activities. Non-recyclable titanium scraps are the low-graded scrap which cannot be used to produce titanium melted products. The Notifying Party considers that the market definition with respect to raw material products can in any event be left open since, irrespective of the exact market definition, the notified concentration does not give rise to any competition concerns.

13. Titanium melted products are produced in three forms: titanium ingots, titanium electrodes and titanium slabs. The Notifying Party submits that there is no basis for a segmentation of the hypothetical market for titanium melted products into these three sub-segments: indeed, from a supply-side perspective, inputs and processes for the production of ingots, electrodes and slabs are similar, whilst customers typically source the complete range of titanium melted products.

14. Titanium mill products are also produced in three forms: titanium long,10 flat11 and pipe products. The Notifying Party considers that the proposed concentration should be analysed on the basis of a single market for all mill products, but acknowledges that mill products can be segmented according to the form and the grade: indeed, inputs and production processes differ between mill products of different forms and different grades and also from a demand-side there is little (if any) substitutability between mill products of different forms and different grades. For example, a clear distinction can be made between standard and rotating grades within mill long products since these are used for different end-use applications.

IV.2.1.2. Geographic Market Definition

15. As regards the geographic scope of the markets concerned, the Notifying Party submits that the market(s) is worldwide, or at the very last EEA-wide.12 Titanium inputs are sourced on a global basis, the same competitors are active globally and the customer base is global. Moreover, the conditions of supply and demand are homogeneous worldwide and transportation costs and trade barriers are minimal.

16. The Notifying Party has provided market share data for all forms and grade of products worldwide and at EEA level.

IV.2.2. The Commission's assessment

IV.2.2.1. Product Market Definition

17. The market investigation has not confirmed the Notifying Party's views. To the contrary, the results of the market investigation clearly indicate that demand-side and supply-side substitutability for titanium inputs is limited. According to market participants, one could even consider each alloy as constituting a separate product market.

18. First, as regards demand-side substitutability, the overwhelming majority of the purchasers of melted and milled products (which includes PCC's casting and forging competitors as well as OEMs) has indicated that there is no substitutability between melted products and milled products. Milled products are used for forging whereas melted products are mainly used for casting. The only melted product that can be used for some casting and some forging products is ingots. However, no milled products can be used for casting.

19. Second, the vast majority of customers who replied to the market investigation has clearly indicated that demand-side substitutability is limited even between different forms of melted13 and different forms of milled products and the choice of product will heavily depend on the specific end-use.

20. Finally, the majority of the customers also indicated that the relevant product market could, in some cases, be defined not only by the form of the product (e.g. bars and billets) but also by the grade (rotating versus non-rotating), going all the way to a specific alloy which is not substitutable by any other product. Some customers have indicated that in certain circumstances rotating grades can be used instead of non-rotating grades, but if any substitutability exists this would be only one-way, i.e. non-rotating grades cannot be used for producing rotating components.

21. Customers further explain that the reason for this lack of substitutability is that generally, once the initial design of an OEM's product and its related components is established, there is no viable way to redesign them to allow for substitution between different inputs. An additional factor making demand-side substitutability difficult in the aerospace industry has been identified in the certification process that OEMs require to be run on both the titanium inputs and the downstream component products to ensure that a certain quality standard is attained.14

22. As regards supply-side substitutability, the overwhelming majority of suppliers has indicated that there is limited possibility for switching the production from melted to mill products. The ability to switch will depend on the facilities each player has and if no facilities exist, the investments would be too significant.

23. Likewise, the majority of suppliers explained that additional investments are required in order to switch the production from one to another melted product, i.e. between ingots, slabs or electrodes.

24. Finally, as regards different milled products, the majority of the suppliers has also indicated that supply-side substitutability requires additional investments, but also that it may depend on the products concerned. For example, suppliers indicated that it would not be possible to simply switch to producing rotating grades from producing non-rotating grades given the investments and certifications needed. On the contrary, suppliers could be able to adapt their production from rotating grades to standard grades, given that low investments and no certifications are required. Likewise, whilst minor additional investments may be required to produce e.g. plates for a supplier already active in sheets, switching is more costly from plates to sheets, given that, among others, thinner dimensions require different rolling mills. Hence, when it exists, substitutability also on the supply-side is at best only one-way.

25. Therefore, on balance, on the basis of the results of the market investigation, the Commission considers that the product markets may need to be defined by at least form and grade, and potentially, even by alloy. However, given that the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition, the exact scope of the relevant product markets can be left open.

IV.2.2.2. Geographic Market Definition

26. As regards the geographic scope of the markets, the market investigation has confirmed the Notifying Party's views. Indeed, the overwhelming majority of both customers and suppliers has indicated that generally titanium producers are active worldwide and that their facilities can be located everywhere in the world to supply their customers.15 Whilst some customers have indicated that prices may vary between different regions, this does not lead to defining regional markets given that there is a relatively limited number of titanium producers active worldwide for aerospace applications, whereby each may have certain specific alloys that no one else produces. In addition, the buyers-side is concentrated and organised on a worldwide level.

27. The global nature of the market is further demonstrated by the procurement practices of customers. Customers purchase their titanium inputs for their EEA-based or US-based manufacturing activities from many locations around the world, including, for example, VSMPO (Russian supplier). Chinese companies may also be an alternative if the design of the relevant OEM's products and of the related components allows to do so and/or the certification requirement does not prevent customers (both OEMs and component producers) from using inputs sourced from such suppliers.

28. Therefore, on the basis of the results of the market investigation, the Commission considers that the geographic scope of the upstream titanium product markets is worldwide.16

IV.3. Downstream markets

IV.3.1. Views of the Notifying Party

IV.3.1.1. Product Market Definition

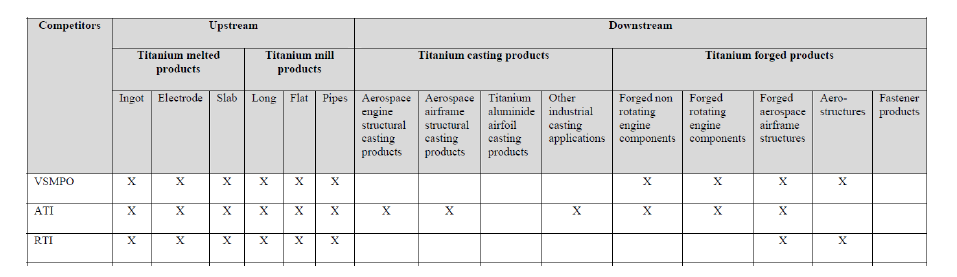

29. PCC manufacturers various titanium-based investment casting and forged products which use titanium melted and mill products as inputs.

30. The Notifying Party submits that the relevant markets are those for (i) all titanium based investment casting products; and (ii) all titanium based forged products.

31. As regards titanium based investment casting products, the Notifying Party submits that the market could be segmented into (i) aerospace airfoil casting, (ii) aerospace engine structural casting and (iii) aerospace airframe structural casting.17 From a demand-side perspective each of these products is designed and manufactured based on the OEMs' specifications:accordingly, each product has different characteristics and is intended for a different use from the other titanium-based investment casting products for aerospace applications. Moreover, on the supply-side each product is produced using different inputs and production methods.

32. PCC also has a minimal production of titanium based casting products for industrial markets other than commercial aerospace, namely medical and military end-use applications.

33. As regards titanium based forged products, the Notifying Party acknowledges that a possible segmentation could be made according to the end-use application. Production machinery and methods differ depending on the end-use application and industry and demand-side substitutability is very limited at best. According to the Notifying Party, were such a further segmentation to be made in the present case, the relevant market would be the one for titanium based forged products for aerospace applications.

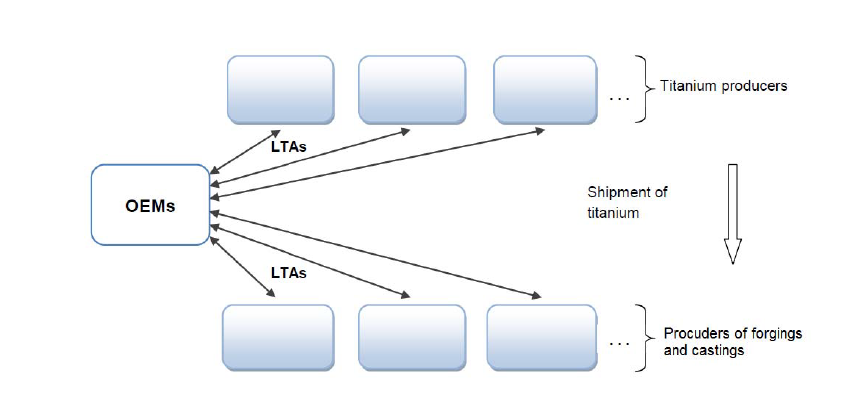

34. The Notifying Party further acknowledges that titanium based forged products for aerospace applications could be further split between engine components,18 airframe structures, aerostructures and fasteners.19 From a demand-side perspective each of these products is designed and manufactured based on the OEMs' specification: accordingly, each product has different characteristics and is intended for a different use from the other titanium-based forged products for aerospace applications.

IV.3.1.2. Geographic Market Definition

35. As regards the geographic scope of the markets concerned, the Notifying Party submits this to be worldwide, or at the very least EEA-wide.20 As in relation to the upstream titanium markets, the competitive dynamics are global and neither transportation costs nor trade barriers play a significant role.

36. Market share data has been provided by the Notifying Party for all possible segments worldwide as well as at EEA level.

IV.3.2. Commission's assessment

IV.3.2.1. Product Market Definition

37. The market investigation has not confirmed the Notifying Party's view of broadly defined markets. On the contrary, the market investigation suggests that the relevant product markets should be defined at a narrower level.

38. The vast majority of the OEMs and the majority of the casters and forgers (herein after, "component manufacturers") have indicated that casted and forged products are not substitutable. Indeed, castings and forgings have different material properties; e.g. casted components tend to be weaker and accordingly cannot be replaced by forged components. Furthermore, the reason for such limited, if any, supply and demand-side substitutability lies in the necessary re-engineering and re-qualification processes that switching requires.

39. The vast majority of the OEMs and the majority of component manufacturers have also indicated that further segmentations can be identified within both forged and casted products on the basis of the end-use application and customer's specifications. In particular, and in line with the Commission's precedents,21 casting products for aerospace applications can be distinguished at least in aerospace airfoil casting, aerospace engine structural casting and aerospace airframe structural casting. Likewise, within forged products for aerospace applications further segments can be identified, such as rotating and non-rotating engine components, airframe structures and aerostructures.

40. In this regard, component manufacturers explained that specific equipment and know-how is needed to produce the different titanium casting and forged products. In particular, specific technical capabilities are required to produce engine components, both castings and forgings, and this is especially the case for rotating grade forged products.

41. Likewise, on the demand-side, the OEMs explained that the specifications and the manufacturing processes differ for the individual products. In particular, rotating grade forged products require the use of high quality titanium inputs and the use of tightly controlled forging processes to deliver the specified properties for a given rotating application.

42. As is the case for the upstream products, the certification requirement plays a significant role. 22

43. Therefore, on balance, on the basis of the results of the market investigation, the Commission considers that separate product markets in this case could be defined along the following lines: (i) aerospace airfoil casting; (ii) aerospace engine structural casting; (iii) aerospace airframe structural casting; (iv) castings for medical and military end-use applications; (v) rotating engine components; (vi) non-rotating engine components; (vii) airframe structures; (viii) aerostructures; and (ix) fasteners.

44. However, given that the proposed transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition, the exact scope of the relevant product markets can be left open.

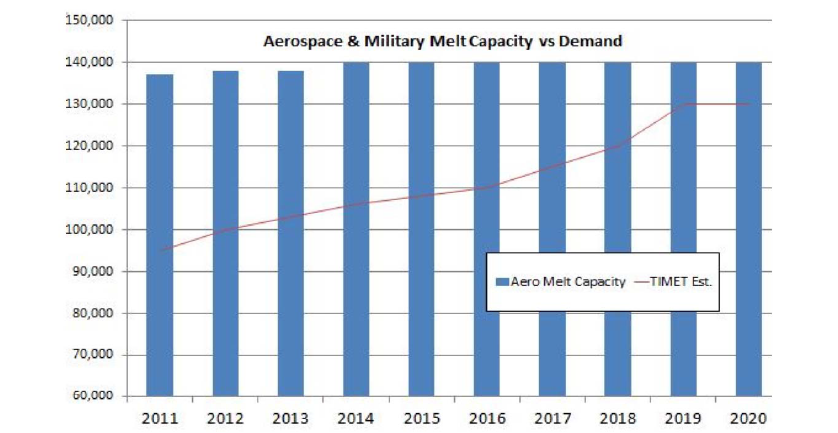

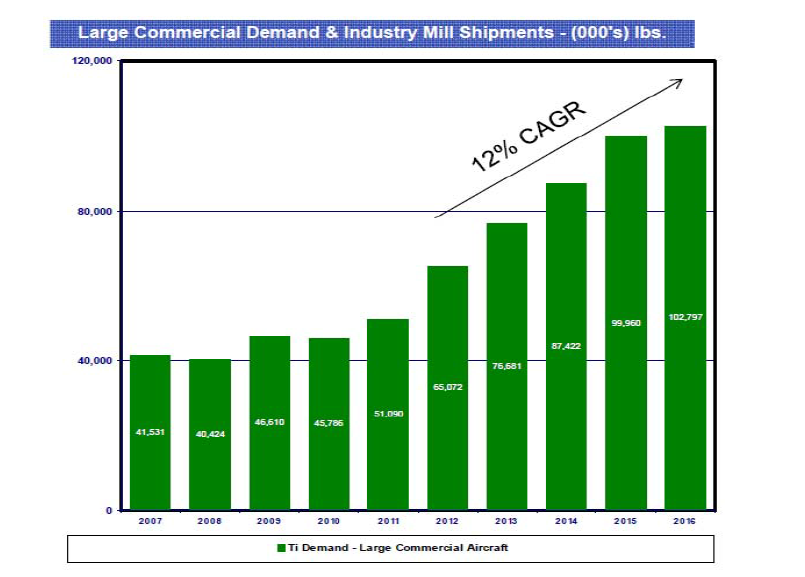

IV.3.2.2. Geographic Market Definition

45. As regards the geographic scope of the titanium-based component markets, the market investigation has not fully confirmed the Notifying Party's view.

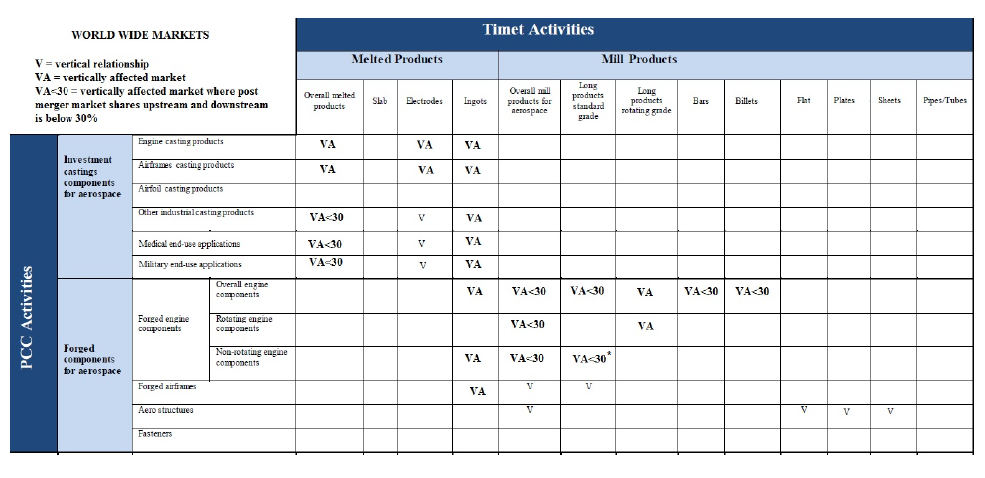

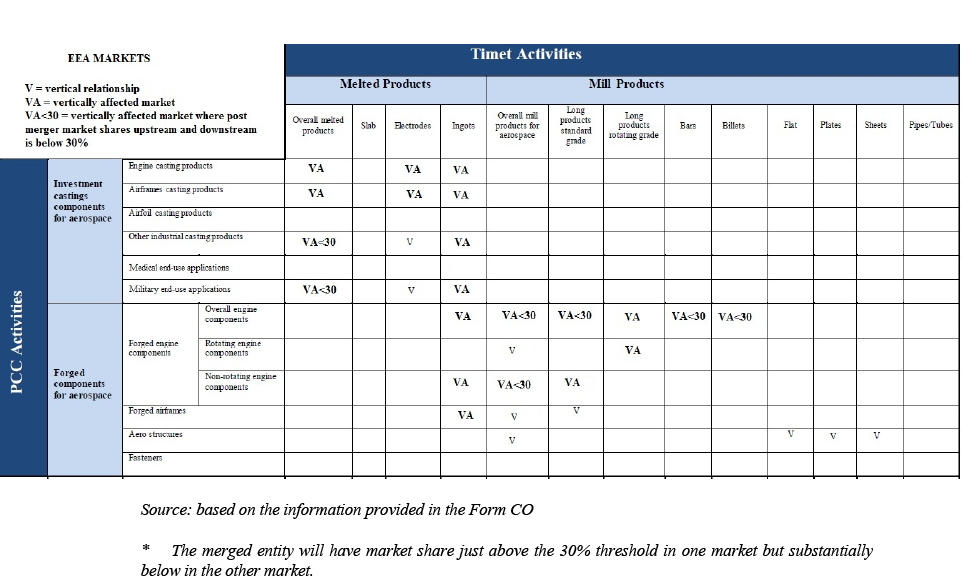

46. Indeed, whilst all OEMs indicated that component manufacturers supply customers all over the world, they all indicated that there are price differences among different regions, mainly due to different tax regimes, energy costs, labour costs, etc. Moreover, the vast majority of the component manufacturers are not active in all regions of the world to a similar extent.23 Given that the aerospace OEMs are mainly based in the United States and the EEA, most component manufacturers supplying the aerospace industry are active in these two regions.

47. However, it is not necessary for the Commission to take a definite view on the geographic scope of the downstream markets as the proposed transaction does not raise serious doubts as to its compatibility with the internal market whether the downstream markets are considered worldwide or EEA-wide in scope.

V. COMPETITIVE ASSESSMENT

V.1. Introduction: the titanium industry for aerospace applications

48. The proposed transaction concerns the vertical integration of an undertaking active in forging and casting of titanium based components, PCC, with an upstream supplier of titanium inputs, Timet. The Parties' activities within the titanium industry are in particular focused on the supply of titanium inputs and titanium based components for aerospace applications.

49. The aerospace titanium industry presents very distinctive features that affect its competitive dynamics and therefore must be taken into account in the assessment of the effects of the proposed transaction. These distinctive features concern in particular (i) the structure of supply and demand of titanium; (ii) the presence of long term supply agreements ("LTAs"); and (iii) the certification requirements for the suitability of titanium inputs and titanium based components for specific end-use applications.

V.1.1. Structure of the upstream and downstream markets: vertical integration

50. The upstream markets for the supply of titanium inputs for aerospace applications are fairly concentrated. However, there has been some new entry in the last five years, namely UKAD, a joint venture between the French Aubert & Duval and Kazakh-based UKTPMP, as well as of certain Chinese suppliers. Apart from these new entrants and Timet, other relevant melting and milling companies are Alcoa/Howmet, ThyssenKrupp, Kobe Steel Ltd., ATI, RTI and the Russian VSMPO.24

51. However, not all upstream players are (yet) able to produce all relevant products. This is in particular true for mill products. Due to the need to certify all input products for aerospace applications (as will be explained below, section V.1.4), players that enter the market must gradually progress certifying from the less complicated input products (such as non-rotating grades) to the more complicated products (such as rotating grades). Hence the key competitors of Timet upstream, who generally have already capability to produce the whole range of input products, consist of ATI, RTI and VSMPO.

52. ATI, RTI and VSMPO are already vertically integrated, at least to some extent, into component manufacturing. The table below sets out all the upstream and downstream market segments where the most relevant market participants are active.25

Table 1 - Overview of the vertical integration of Timet's competitors

Source: paragraph 274 of the Form CO.

53. The merged entity would, however, be the most fully vertically integrated company active in the titanium industry for aerospace applications given that its breadth of product areas covered is not matched by any other company.

54. Compared to the upstream markets, the downstream markets for component manufacturing are more fragmented. There are many forgers and casters active in manufacturing titanium components for the aerospace industry (see section V.3.2 below for a description of the key players).

V.1.2. The role of the OEMs in the market

55. Originally, the aerospace titanium industry was characterized by a normal vertical supply chain model, where melting and milling companies were selling inputs to component manufacturers, and the latter were supplying OEMs with the components they needed for their aerospace products. However, the great importance of raw material in determining the costs of the components purchased by the OEMs has led to an evolution of this originally conventional structure of the supply chain.

56. In order to control their costs, OEMs have increasingly sought greater transparency and leverage as regards the costs of the component inputs. Therefore, OEMs eventually started negotiating directly with titanium input producers for the supply of inputs not only for their own manufacturing activities, but also for the components they purchased from component manufacturers. This effectively means that instead of being at the end of the supply chain, OEMs such as Rolls-Royce, Safran (Snecma), General Electric and UTC (Pratt & Whitney), as well as the large airframe manufacturers, like Boeing and Airbus, have gradually acquired a role in the middle of the supply chain. In practice, this development has resulted in the conclusion of LTAs between the OEMs and the upstream titanium input providers on the one hand and between the OEMs and the component manufacturers on the other hand. The functioning of LTAs will be described in the following section.

57. Another typical feature of the industry, which is again linked to the high importance of titanium inputs for aerospace manufacturing, is the practice of multi-sourcing titanium inputs. Indeed, to the extent that this is possible,26 OEMs (as well as component manufacturers) try to secure the inputs they need from several suppliers to ensure timely delivery of determined quantities of inputs and obtain competitive prices from suppliers.

V.1.3. LTAs

58. The LTAs generally set multi-annual (up to 10 years) supply conditions (a) upstream – between titanium input producers and OEMs and (b) downstream – between titanium based component manufacturers and OEMs.

59. The LTAs are designed to grant OEMs price stability and security of supply as well as to guarantee the suppliers at both upstream and downstream levels an assured base of sales to spread upfront fixed cost investments as well as plan the utilisation of the capital intensive manufacturing equipment. Typically, the LTAs provide for (i) share of total supply commitments or firm annual volumes; (ii) set prices; and (iii) price adjustments based on industry wide indices to account for fluctuations in the price of certain raw material, labour and energy.

60. The upstream LTAs therefore set the base price of the titanium inputs for both direct deliveries to OEMs as well for deliveries, under the direction of the OEMs, to component manufacturers. The LTAs also allow the OEMs to determine the specific volumes delivered to component manufacturers within the overall volume/supply commitments agreed in the LTA. The LTAs generally also contain specific penalties in the event that the supplier does not respect its contractual obligations.27

61. The downstream LTAs, on the other hand, determine the prices at which the OEMs purchase the components and provide the ability for the OEM to specify the source from which the component manufacturers must obtain their inputs under the pricing terms of the upstream LTAs.

62. The table below shows the commercial relationships under the LTAs.

Figure 1 - Commercial relationship between OEMs, input titanium suppliers and downstream producers

Source: based on the information provided by the Notifying Party

63. In conclusion, the prevalence of the LTAs in the titanium industry for aerospace applications provides price protection and security of supplies to the OEMs on the one hand (and are designed for these purposes), and the ability for both the upstream and downstream manufacturers (in particular the upstream manufacturers) to spread the upfront fixed cost investments over a guaranteed base of sales as well as plan the utilisation of the capital intensive manufacturing equipment.

V.1.4. Certification process

64. OEMs require their suppliers, both upstream and downstream, to go through a certification process of their products. This is done to guarantee that certain levels of quality and performance and ultimately security are met by the titanium based components included in aerospace manufacturing. Therefore, only certified titanium inputs and forging and castings are accepted and purchased by OEMs.

65. The extent and complexity of the certification processes will depend on (i) whether the supplier already produces the particular product; (ii) what type of product is certified and its end use; (iii) whether the titanium supplier has a pre-existing supply relationship with the OEM for other similar products; and (iv) the willingness/incentive of the OEM to move quickly to certify another supplier.

66. According to the Notifying Party, certification of titanium inputs upstream will cost between USD 2,000 and USD 10,000 and take between six to nine months for a simple certification. In these cases the producer manufactures and evaluates between one and five heats worth of metal which may be converted into a component, involving additional testing and evaluation.28 In certain cases, OEMs may consider it sufficient if producers provide production data for a certain number of past years without submitting product samples. This certification does not involve costs and is at times deemed sufficient for suppliers with whom they have already a pre-existing supply relationship.

67. In contrast, in certain specific cases, in particular with respect to inputs for the manufacture of fatigue sensitive rotating engine components, the certification process can cost between USD 500,000 and USD 1 million and take up to two years per product. In these cases engine testing is required to simulate and prove the performance of the product (the “rig- spin” test). In particular, this test is normally required for the certification of titanium rotating grade alloys.

68. With regard to the downstream products, it has to be distinguished between (i) the certification of a new component for a new programme developed by an OEM and (ii) the certification of an existing component on an existing programme of an OEM wishing to switch supplier.29 The latter process is simpler and can be done more quickly. The most stringent and time-consuming requirements relate to rotating engine components which require engine testing as described above.

V.1.5. Future developments

69. Finally, as regards the future developments of the aerospace titanium industry, market projections foresee an increase in the demand of titanium melted and milled products in the years to come. Nonetheless, the upstream market is estimated to have enough capacity to meet, and even exceed, this demand. The figures below show the Parties' projection for melted and mill products.30

Figure 2 – Projections of capacity and demand for melted products

Source: Form CO Note: Timet's estimates.

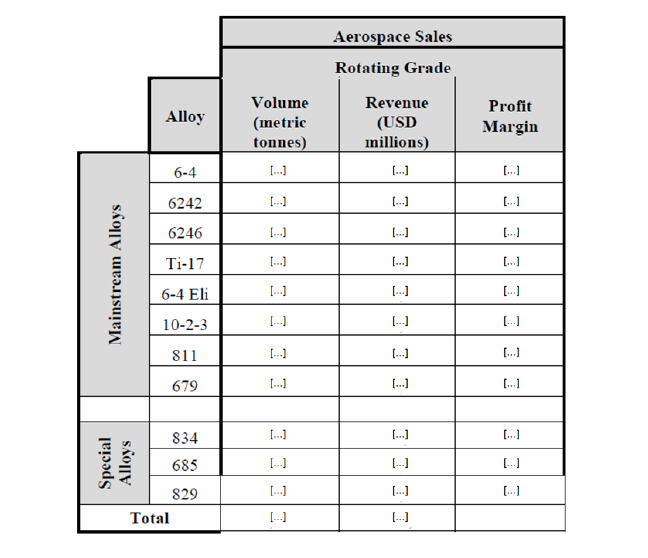

Figure 2 – Projections of the demand for mill products

Source: Project Tile presentation of 1 October 2012, Appendix, Annex 5.4a to the Form CO.

V.1.6. Conclusions

70. Due to the distinctive characteristics of the aerospace titanium industry described above, and the fact that the reasoning is similar in relation to all products, the competitive assessment of the proposed transaction is not carried out product market by product market. Rather, an overall view is taken whilst taking into account any specificities arising from the dynamics relating to specific narrower product markets.

V.2. Market shares

71. The tables below illustrate the vertical relationships between the Parties at both the global and EEA levels of the downstream markets, by showing which Timet titanium inputs are used for the manufacture of each of PCC's products: the vertical relationship is highlighted by the symbol "V". The symbol "VA" identifies the markets where the vertical relationship results in an affected market.

Table 2 - Overview of the vertical relationships

72. Those affected markets which are unlikely to raise concerns are marked with the symbol "VA<30". These are markets where the Parties' shares at each level remain below 30% (or just above the 30% threshold in one market but substantially below (<10%) in the other market).31

73. The table below indicates the Parties' market shares in the vertically affected markets which do not fall under the presumption of paragraph 25 of the Guidelines on non-horizontal mergers.

Table 3 – Market shares in the vertically affected markets (2011)

Upstream market | Worldwide Market share* |

Downstream markets | Worldwide Market share* | EEA Market share* |

Melted products | [20-30]% | Aerospace engines casting | [50-60]% | [40-50]% |

Aerospace airframe casting | [50-60]% | [40-50]% | ||

Ingots |

30- 40% | Aerospace engines casting | [50-60]% | [40-50]% |

Aerospace airframe casting | [50-60]% | [40-50]% | ||

Other industrial casting | [10-20]% | [5-10]% | ||

Military end use application | [5-10]% | [0-5]% | ||

Forged engine components | [20-30]% | [20-30]% | ||

Forged engine non-rotating components | [30-40]% | [30-40]% | ||

Forged airframes | [10-20]% | [0-5]% | ||

Electrodes | [10-20]% | Aerospace engines casting | [50-60]% | [40-50]% |

Aerospace airframe casting | [50-60]% | [40-50]% | ||

Long standard grade products |

[5-10]% |

Forged engine non-rotating components |

-- |

[30-40]% |

Long rotating grade products |

[40-50]% | Forged engine components | [20-30]% | [20-30]% |

Forged engine rotating components |

[20-30]% |

[10-20]% |

Source: based on the information provided in the Form CO; (*) value based market shares.32

74. PCC is the market leader downstream in all markets with the exception of forged non- rotating engine components and forged airframe structures on a worldwide level, with the competitors following having 12 to 44 percentage point lower market shares. At EEA level, PCC is again the market leader in all markets with the exception of forged rotating engine components and forged airframe structures with competitors having significantly lower market shares in relation to most other products.

75. Likewise, Timet is the market leader in all worldwide markets referred to in the table above (with the exception of electrodes and long standard grade products), with the second line competitors having 9 to 15 percentage points lower market shares.

76. As indicated above in section IV.2.2, the upstream markets could also be segmented on the basis of each alloy. However, due to the way the industry works (see section V.1above), calculating market shares by specific alloys does not appear to add significantly to the competitive assessment. The fact that for certain alloys very few alternative suppliers exists or that for certain alloys (namely Ti 685, Ti 829 and Ti 834) Timet is the only certified supplier and current producer will nevertheless be taken into account in the competitive assessment.

V.3. The competitive landscape

V.3.1. Upstream markets

77. As indicated above in section V.1.1, upstream markets for the supply of titanium melted and mill products for aerospace applications are fairly concentrated and characterized by a high degree of vertical integration downstream. In particular, the market investigation has revealed that ATI, RTI, Timet and VMSPO are the only certified producers of mill products, in particular rotating grade products: additional producers are instead certified to supply melted products, in particular ingots, but these are less critical inputs. Therefore, the following paragraphs will describe ATI, RTI and VMSPO.

V.3.1.1.ATI

78. ATI (Allegheny Technologies, Inc.) is a US based producer of titanium ingot, bars, billets, rotating grade products, standard grade products, sheets, plates, coil, rectangles, shapes seamless tubing.33 According to the information provided by the Parties in the Form CO, it has a relatively significant market share in all the relevant markets (identified by form and grade) affected by the present transaction, ranging from [10-20] up to [30-40]%. It is vertically integrated downstream in forged and casting products via its subsidiary Ladish, but also in the production of raw material, such as sponge.

79. ATI considers having similar capabilities to those of Timet, as far as the upstream markets are concerned, including internal production of titanium sponge. Nonetheless ATI acknowledges that it does not produce certain alloys that Timet does.34

V.3.1.2.RTI

80. RTI (RTI International Metals, Inc.) is a US based producer of melted (ingot, slab, electrodes) as well as mill products (bars, billets, rotating grade, standard grade, sheets, plates and pipe).35 According to the information provided by the Parties in the Form CO, it has market share in the relevant markets ranging from [5-10] to [20-30]%, with the exception of long rotating grade, where it has a market share of [0-5]%. It is vertically integrated downstream, but it does not have sponge production.

81. RTI considers that it has the ability to produce anything that Timet can produce, although it acknowledges that there may be some know-how that Timet possess which enables it to produce certain special products, in particular mill input. Moreover, RTI has spare mill product capacity.36

V.3.1.3.VSMPO

82. VSMPO (Verkhnesaldinskoye metallurgicheskoye proizvodstvennoye ob'yedineniye) is a Russian based supplier of titanium melted and mill products. According to the information provided by the Parties in the Form CO, it has market share in the relevant markets of around [10-20]%. Like ATI, it is vertically integrated downstream, but also in the production of raw material, such as sponge, and the market investigation has revealed that, because of the capabilities of its internal production of raw material, VSMPO is able to provide very competitive prices for mill and melted products.

83. Nonetheless the market investigation has also indicated that, due to certain export licence requirements, as Russian based company, VSMPO may not be a suitable supplier of inputs for military applications procured by certain Governments.

V.3.2. Downstream markets

84. The downstream markets for forging and casted products for aerospace applications are more fragmented than the upstream markets. The major players which are not significantly vertically integrated upstream, and have not described in the section above, are the following:

85. Alcoa is active in forging products as well as in casted products through Howmet. As Alcoa/Howmet also operates titanium melting facilities, it is vertically integrated from titanium melted products to titanium based casted products.

86. Aubert & Duval is a producer of, in particular, forging components for rotating engine components, airframe structures, aerostructures.37 Via its joint venture UKAD it is also active in the upstream market for the production of melted product.

87. Cammel Forge, a subsidiary of OEM UTC, manufactures titanium-based forged rotating and non-rotating engine components.38

88. Firth Rixson, Ltd., is a forger with significant market shares in forged engines components, in particular for non-rotating engines components at a worldwide level where it is the market leader with [30-40]% market share (EEA wide it is the second player after PCC with a market share of [20-30]%.) Firth Rixson, Ltd., also produces rotating engines components

89. Kobe Steel, Ltd., is a vertically integrated Japanese player active on both levels of the market, i.e. it manufactures melted and milled titanium products and it forges titanium products for the aerospace industry via its joint venture Japan Aeroforge (it does not produce castings). Kobe is not active in titanium sponge production but purchases sponge on the market.39

90. Selmet manufactures titanium-based structural castings for aerospace engines, airframes and aerostructures.

91. Snecma is a subsidiary of the OEM Safran and it manufactures titanium based forged rotating and non-rotating engine components as well as aerostructures.41

92. , Tital GmbH is a manufacturer of titanium based casting products42.

V.4. Input foreclosure

93. According to the Commission’s Non-Horizontal Merger Guidelines,43 a merger may result in foreclosure where actual or potential rivals’ access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing these companies’ ability and incentive to compete. Such foreclosure is regarded as anticompetitive where, as a result of the merger, the merging companies, and possibly also some of its competitors, are able to profitably increase the price charged to consumers.

94. When assessing the likelihood of such an anticompetitive input foreclosure scenario, the Commission examines whether the merged entity would have the ability post-merger to foreclose access to inputs, whether it would have the incentive to do so, and moreover, whether a foreclosure strategy would have a significant detrimental effect in the downstream market.

V.4.1. Concerns raised in the market investigation

95. A number of PCC’s downstream forging and casting competitors as well as OEMs have raised input foreclosure concerns during the market investigation. According to these market participants, there is a risk that the merged entity would discriminate between supplies to downstream competitors and in-house supplies. However, such concerns were not raised or supported by either Timet’s upstream titanium competitors or by the main airframe customers, i.e. Airbus and Boeing.

96. According to the concerned market participants, the merged entity would be able to and have the incentive to (i) delay or withhold titanium supplies or (ii) raise prices for titanium input for PCC’s casting and forging competitors and favour deliveries to its own casting and forging production units. This would result in higher input prices and more generally less favourable supply conditions for the forging and casting products of PCC’s competitors downstream. As a consequence, the competitive pressure imposed by PCC’s competitors would be reduced and the merged entity would have the possibility to gain market shares and increase prices downstream.

97. Most of these input foreclosure concerns were raised, in particular, with respect to the supply of milled rotating grade titanium where Timet’s market shares are higher than in the other potential titanium sub-markets. In contrast, several market participants stated that no competition concerns will arise with respect to titanium products used in casting processes or with respect to non-rotating products. 44

V.4.2. The Parties’ arguments

98. In contrast, the Notifying Party claims that the transaction does not give rise to input foreclosure concerns. It argues that the merged entity would have neither the ability nor the incentive to substantially foreclose access to inputs or raise prices.

V.4.2.1. Ability to foreclose access to inputs

a) Timet’s market power upstream

99. The Notifying Party claims that Timet does not have the necessary market power on the upstream markets to allow the merged entity to successfully pursue an input foreclosure strategy. It submits that there is considerable competition from Timet’s rivals, such as ATI, VSMPO and RTI, all of which are already vertically integrated.

b) LTAs

100. Moreover, in the Notifying Party's view, the merged entity would not be able to foreclose access to inputs due to the existence of LTAs. The LTAs set multi-annual supply conditions with the OEMs, including minimum market share provisions and formula- determined prices, as described in section V.1.3 above. Under these binding LTAs, the merged entity would not be able to legally modify the conditions of supply for all those titanium volumes covered under LTAs until the expiry of each contract.

101. The Notifying Party submits that - with the exception of titanium ingots - significant volumes of Timet’s sales are currently covered by LTAs expiring at various times through to 2030. In particular, the LTAs currently cover (i) […]% of Timet’s global sales of melted products, and (ii) […]% of Timet’s global sales of titanium mill products used in the aerospace industry. These percentages are higher if only Timet’s sales in the EEA are considered.45

102. Considering only rotating grade titanium, which is the area where most concerns have been raised, according to the Notifying Party, […]% of Timet’s global revenues of titanium long rotating grade products are covered by LTAs.46 Considering those alloys that are currently only produced by Timet, i.e. Timetal-685, Timetal-829 and Timetal-834, the Notifying Party further submits that between […]% and […]% of their supply is covered under LTAs.47 The majority of these LTAs run through to […] and […].48

103. The Notifying Party thus argues that the LTAs provide significant price protection to the OEMs because Timet (or indeed the combined entity post-merger) is unable to unilaterally modify its conditions of supply during the course of the LTAs, neither as regards the quantity, nor the quality, nor the price. Accordingly, the merged entity would not be able to pursue an input foreclosure strategy at least in respect of all the products covered by existing LTAs.

c) The OEMs' bargaining power

104. In the Notifying Party’s view, the OEMs have significant buyer power to counteract any potential input foreclosure strategy pursued by the merged entity.

105. As described in section V.1.3 above, OEMs typically enter into LTAs both at the upstream and downstream level to control pricing levels and the overall organisation of their supply chains. Under these LTAs the OEMs either purchase titanium input directly for their own use or indirectly for the benefit of the downstream component manufacturers (the LTAs giving the OEM the right to direct the titanium inputs to component manufacturers of their choosing). The OEMs therefore typically determine which downstream manufacturer should be supplied with a specific titanium input, at the price set under the LTA with the upstream producer.

106. The Notifying Party argues that the fact that OEMs are in a position to set the price of titanium to be paid by the downstream producers of titanium-based products as well as the OEMs' ability to direct specific volumes to specific component manufacturers is evidence of the OEMs' bargaining power.

107. Moreover, according to the Notifying Party, demand in the aerospace industry is highly concentrated. In 2011, Timet’s ten largest customers accounted for […]% of its sales revenue. Considering the potential rotating grade sub-market in particular, four major OEMs represent in aggregate […]% of Timet’s sales of long rotating grade products, either through direct purchases or through indirect purchases.

108. In addition, the Notifying Party notes that Timet’s profit margin in percentage of revenue for the special alloys that only Timet produces is not larger than its margin for other alloys for which OEMs can switch to other suppliers (for example the alloy 6242). On this basis the Notifying Party submits that Timet has not been in a position to increase the prices of the special alloys. According to the Notifying Party, this shows that OEMs have significant bargaining power and can prevent price increases.

Table4: Volume, revenues and profit margin information for rotating grade alloys

Source: Discussion Paper submitted by the Parties on 7 December 2012, p.9

109. According to the Notifying Party, the proposed transaction will not have any effect on the OEM’s existing buyer power as the number of suppliers in the upstream and downstream titanium markets will remain the same. Thus, the OEMs will have the same choice of suppliers and will be able to pursue the same purchasing strategies as prior to the proposed transaction.

d) Alternative titanium suppliers and switching costs

110. Furthermore, according to the Notifying Party, PCC’s competitors and the final OEM customers can rely on a sufficient choice between alternative titanium suppliers and do not face significant switching costs.

111. The Notifying Party submits that there are alternative certified titanium suppliers for the vast majority of the alloys Timet produces. This includes in particular those alloys that require certification of the supplier, as described in section V.1.4 above. The table below lists all of the titanium alloys Timet is currently certified to produce for aerospace applications and also shows which of Timet’s competitors are equally certified to produce such alloys for aerospace applications:

Table 5: List of alloys produced by Timet as a certified supplier and alternative suppliers

Titanium alloys which Timet is certified to produce |

ATI (US) |

RTI (US) |

VSMPO (Russia) |

Kobe (Japan) |

Bao-Ti (China) |

10-2-3 | X | X | X | X | X |

15-3 | X |

| X | X | X |

21S | X |

|

|

|

|

230 |

|

|

|

| X |

3-2.5 | X | X | X | X |

|

550 | X | X | X |

|

|

5553 |

|

| X |

|

|

6242 | X | X | X | X | X |

6246 | X | X | X | X | X |

6-4 | X | X | X | X | X |

6-4 Eli | X | X | X | X | X |

662 | X | X | X | X | X |

679 | X | X | X |

| X |

685 |

|

|

|

|

|

811 | X | X | X | X | X |

829 |

|

|

|

|

|

834 |

|

|

|

|

|

CP | X | X | X | X | X |

Ti-17 | X | X |

| X |

|

Source: Parties' Response to the Commission’s Request for Information of 4 December 2012, question 4

112. Accordingly, there are three alloys, Timetal-685, Timetal-829 and Timetal-834, that Timet supplies as the only certified supplier to aerospace customers. However, according to Timet, these alloys are not patent protected. Moreover, the Notifying Party argues that the revenues derived from the sale of these three alloys amounts to less than […] MT of titanium and are, as such, minor compared to Timet’s overall business, representing [0-5]% of Timet’s 2011 sales to the aerospace industry and [5-10]% of Timet’s 2011 sales of rotating grade inputs (see Table .

113. The Notifying Party further submits that switching costs are not significant at the upstream level. As described in section V.1.4 above, it estimates that certification of titanium inputs upstream will cost between USD 2,000 and USD 10,000 for a simple certification and take between six to nine months. In certain specific cases, in particular with respect to inputs for the manufacture of fatigue sensitive rotating engine components, the certification process can cost between USD 500,000 and USD 1 million and take up to two years per product.

e) Sponsoring new entry

114. Finally, the Notifying Party also argues that the OEMs are in a position to sponsor entry of new certified titanium suppliers in reaction to any potential increase in price. Since the vast majority of LTAs will only expire in several years’ time, the OEMs will have sufficient time to take the necessary measures to sponsor entry of alternative suppliers for any of the potential titanium sub-markets. According to the Notifying Party, the required investments to certify alternative suppliers are not significant in relation to the overall financial and organisational power of OEMs.

V.4.2.2. Incentive to foreclose access to inputs

a) Profitability of complete foreclosure - PCC's capacity to absorb Timet's production

115. The Notifying Party submits that PCC does not have the capacity to absorb all of Timet’s titanium production after the proposed transaction.

116. In forging applications, sales to customers other than PCC currently represent approximately […]% of Timet’s sales.49 If PCC were to internalize all of its titanium sourcing for forging applications, Timet would still have approximately […]% of its capacity available for sales to third parties.50

117. In casting applications, sales to customers other than PCC currently represent approximately […]% of Timet’s sales. If PCC were to internalize all of its titanium sourcing for casting applications, it could in theory absorb all of Timet’s production. However, the Notifying Party argues that in this case the Notifying Party’s competitors would still have the ability to source their needs from Timet’s competitors as there is sufficient available capacity in the market.

118. In addition, the Notifying Party submits that it currently has no plans to increase its production capacity in the field of titanium-based casting or forging products.

119. Therefore, the Notifying Party submits that a decision to stop supplying titanium to third parties would result in the loss of the majority of Timet’s revenues which would not be economically rational for the merged entity.

b) Profitability of partial foreclosure - Ability to increase sales downstream

120. The Notifying Party submits that a partial input foreclosure strategy, for example through increasing prices to downstream competitors, would be equally unprofitable for the merged entity.

121. The Notifying Party argues that although the upstream margins are smaller than the downstream margins, the difference in margins between Timet’s and PCC’s businesses is not large, especially in the rotating grade products where most concerns were raised by market participants.

122. Timet’s average profit margin in the affected upstream markets is estimated to be approximately […]% for titanium ingots, […]% for titanium electrodes, […]% for titanium long rotating grade products and […]% for titanium long standard grade products.

123. PCC's average profit margin in the downstream markets is estimated to be approximately […]% for titanium-based engine castings, […]% for titanium-based airframe castings, […]% for forged engine rotating components, […]% for titanium forged airframe components and […]% for titanium forged engine non-rotating components.

124. Moreover, according to the Notifying Party, the base of sales of the merged entity downstream is not very large with a global market share of [20-30]% in forged rotating grade components ([10-20]% at EEA level). Accordingly, any profit gain due to a reduction in competition downstream and higher downstream margins may remain limited (especially in relation to the potential losses upstream).

c) Behaviour of existing vertically integrated players in the industry

125. The Notifying Party submits that the vertically integrated business model, whereby a producer of titanium melted and mill products is also active downstream in the manufacture of titanium based products, constitutes a common feature of the industry. It argues that all of Timet's competitors, with the exception of Sumitomo, are, at least to some extent, vertically integrated. Nevertheless, all have continued to supply titanium melted and mill products to their competitors downstream, including to PCC.

d) PCC’s strategy as a vertically integrated player in the nickel and cobalt alloy markets

126. The Notifying Party argues that the absence of competition effects further to its strategy and experience in the nickel and cobalt alloy market can be considered as an additional element in assessing the effects of the proposed transaction. PCC is already a vertically integrated player in the market of nickel and cobalt alloy products for the aerospace industry since its acquisition of Specialty Metals Corporation in 2006. The Notifying Party submits that it has not engaged in any type of input foreclosure behaviour in this industry which is similar to the titanium industry in many respects, such as the extensive involvement of OEMs in the titanium inputs supply chains through the use of LTAs.

127. The Notifying Party submits that it has continued to operate separate LTAs upstream and downstream and has not engaged in price discrimination between in-house supplies and supplies to competitors.

128. Furthermore, the Notifying Party notes that, whilst it has lost the component business around one of its “monopoly nickel alloys” to a competitor, it is still obliged to sell this “monopoly nickel alloy” to its competitor under the directed purchase clauses of an existing LTA.

V.4.3. Commission’s assessment

V.4.3.1. Ability to foreclose access to input

129. The Commission’s Non-Horizontal Merger Guidelines point to three conditions which are necessary for the merged entity to have the ability to foreclose its downstream competitors, namely the existence of a significant degree of market power upstream, the importance of the input and the absence of timely and effective counter-strategies. With respect to the existence of market power and the availability of counter-strategies, the Commission will in particular discuss the protection offered to customers and competitors by the LTAs, the countervailing buyer power of OEMs, the ability for Timet’s customers to switch to alternative suppliers and the possibility of sponsored new entry.

a) Timet’s market power upstream and importance of the titanium inputs

130. For input foreclosure to be a concern, the merged entity must have a significant degree of market power in the upstream market.51

131. As discussed in section V.2 above, Timet’s market shares remain below 30% in many of the potential upstream titanium markets identified in section IV.2 above, exceeding this threshold only in the markets for ingots (30-40%) and long rotating grade products ([40- 50]%).52

132. However, Timet can be considered to be a monopoly supplier of three specific alloys, namely Timetal-685, Timetal-829 and Timetal-834, as no other titanium producer currently supplies these alloys to the market (hereinafter referred to as the “monopoly alloys”). Moreover, Timet may in certain instances be the only certified supplier of a specific alloy to a specific OEM customer (hereinafter referred to as the “sole-sourced alloys”).

133. Furthermore, input foreclosure may raise competition problems only if it concerns an important input for the downstream product, for example when the input represents a significant costs factor relative to the price of the downstream product.53

134. According to the results of the Commission’s investigation, the cost of the titanium inputs represent approximately 20% of the final price of casting products and 50% of the final price of forging products.54

135. On the basis of the above, the Commission finds that although Timet’s upstream market power appears relatively moderate when product groups are considered, there may be specific alloys where Timet achieves a monopoly or near-monopoly position on important input products. However, the Commission needs to assess whether Timet’s market power in these products is likely to translate into the ability for the merged entity to raise rivals’ costs in the downstream markets, as will be discussed in the following sections.

b) Protection offered by LTAs

136. The Commission considers the extensive involvement of OEMs in the organisation of their titanium supply chains to constitute a key and distinguishing feature of the titanium supply industry. Timet’s existing LTAs with OEMs will constrain the merged entity’s behaviour post-merger. The effects of the LTAs on the assessment of the proposed transaction are two-fold.

137. First, the upstream LTAs will constrain the ability of the merged entity to increase input prices to its downstream rivals for the duration of the LTAs. The LTAs cover significant proportions of Timet’s sales as outlined in paragraphs 101 and 102 above. Over […]% of Timet’s sales of rotating grade titanium products (the main area of concern) were covered by LTAs in 2011. Most of these volumes are under LTAs with OEMs (representing […]% of Timet’s sales of rotating grade products), whilst […]% of Timet’s sales of rotating grade products are under LTAs with non-OEMs (e.g. PCC itself, representing more than […]% of these sales).

138. The percentage of Timet's sales covered by LTAs with OEMs do not change significantly going forward due to the long term nature of the contracts. In particular, less than […]% of Timet's OEM contract revenues expire before or by the end of […]. By contrast, more than […] of Timet's OEM contract revenues are covered at least until the end of […], with several large LTAs expiring only at the end of […] (including the LTA with and two of the LTAs with).

Table6: Timet’s LTAs with OEMs with respect to the supply of titanium products for aerospace applications

Source: Annex 1 to the Parties’ response to the Commission’s Request for Information of 30 November 2012

139. Second, the LTAs with the OEMs directly limit the ability of the merged entity to discriminate between in-house supplies and supplies to downstream competitors. In the LTAs the prices for the inputs are agreed with a specific OEM. Under the terms of the LTA the OEM can subsequently direct the upstream input to any of the merged entity’s downstream competitors who have entered into an equivalent LTA with the OEM at the downstream level. LTAs tends to provide for uniform input prices across all downstream suppliers.55 In the case of PCC, close to […]% of its sales of rotating engine components are produced on the basis of directed input supplies.

140. The OEMs can therefore exercise their bargaining power via the LTAs to protect the merged entity’s downstream competitors from the effects of an input foreclosure strategy. OEMs face incentives to exercise their bargaining strength in this manner in order to prevent a reduction of competition downstream.

(i) Potential limits to the protection offered by LTAs

141. A number of the market participants raising input foreclosure concerns argue that their LTAs with Timet will not offer sufficient protection against price increases or withholding strategies.

142. In particular, some of the concerned market participants argue that there is a risk that the merged entity would try to review the existing LTAs before expiry or possibly breach the existing contracts.

143. Having assessed the most important LTAs of Timet with major OEMs, the Commission finds in accordance with the Notifying Party’s submissions that the merged entity are likely to continue to be legally bound by the terms of the LTAs.

144. First, the price review clauses contained in the LTAs do not allow for renegotiations of prices between the parties before the expiry of the contracts. The clauses only allow for price increases based on indexation formulae to reflect cost increases following changes in price indices. Second, the LTAs do not contain clauses allowing for the renegotiation of prices in the event of change of ownership. Where LTAs contain a change of control provision, generally only the customer has the option of terminating the LTA.56 Therefore, the Commission does not find sufficient indications to conclude that the merged entity has the ability to disregard its LTA obligations after the proposed transaction.

145. Some market participants argue that they would be exposed to the merged entity’s input foreclosure strategy when the existing LTAs with Timet expire.

146. However, the Commission has assessed the remaining length of the LTAs and finds on this basis that the majority of LTAs will remain in force for several years after the proposed transaction. The […] years remaining until the expiry of the most important LTAs as listed in paragraph 138 above should give the OEM customers sufficient time to switch considerable volumes of their purchases to alternative titanium suppliers if necessary. Further details on the possibility to switch will be discussed in section V.4.3.1 d) below.

147. Moreover, some market participants claim that the LTAs do not necessarily cover all of the titanium volumes they purchase in practice. Rather the LTAs define minimum and maximum purchasing volumes based on the OEM’s forecasted needs of specific titanium inputs. If a customer’s demand exceeds these pre-determined volumes, the customer will enter into negotiations with the titanium suppliers to obtain additional volumes. In this context, some of the concerned market participants argue that they will either not be able to obtain these additional titanium volumes from the merged entity in the future or that they will have to pay increased prices for these volumes. Finally, a limited number of market participants argue that the LTAs do not cover titanium inputs relating to newly developed aerospace projects and programmes.

148. However, the Commission's investigation pointed out that individual negotiations for additional volumes rarely occur in practice. For example, according to the Notifying Party, all of Timet’s sales of rotating grade products that occurred under LTAs (i.e. […]% of Timet‘s sales of rotating grade products) were made under the scope of the original LTAs and not under individually negotiated terms. Therefore, the Commission considers that the additional volumes outside of the scope of the LTAs’ protection are not significant enough to raise competition concerns. Furthermore, the Notifying Party submits that in the case of new aerospace programmes OEMs will require a new LTA with fixed titanium base prices covering any such new programme.

149. The assessment of these questions links closely to the power relationship between OEMs and their suppliers in the titanium industry which will be discussed in sectionV.4.3.1 c) below.

(ii) Commission’s conclusion on the potential limits to the protection offered by LTAs

150. On the basis of the above, the Commission finds that the potential limits to the protection offered by LTAs are not significant enough to raise significant doubts on the LTAs’ overall effectiveness in protecting OEM customers and downstream competitors from potential input foreclosure by the merged entity.

c) The OEMs' bargaining power

151. The demand-side of the market is highly concentrated, essentially comprising the major engine OEMs (such as UTC, Rolls-Royce, GE/Safran), Airbus and Boeing, in particular in the rotating grades. For example, four OEMs account for close to […]% of Timet’s sales of titanium rotating grade products and three OEMs account for […]% of PCC’s sales of engine rotating components.

152. Furthermore, the OEMs play a central role in the titanium industry. As described in section V.1.2 above, the OEMs are involved extensively in the organisation of the supply chain at different levels. Most importantly, the OEMs effectively control the relationship between the suppliers of titanium inputs and producers of titanium components through the use of LTAs. In most case, in particular in the rotating grade products, the OEMs indicate to the manufacturers which titanium supplier must be used.

153. Accordingly input foreclosure is likely to be a risky and ultimately costly strategy for the merged entity.

154. First, OEMs have the ability to certify the merged entity’s upstream competitors for the supply of certain alloys, especially within the remaining lifetime of Timet’s LTAs (mainly expiring between […] and […]). This would prevent Timet from engaging in an input foreclosure strategy even after the expiry of the LTAs.

155. Second, OEMs can leverage one supplier against another by switching or threatening to switch suppliers in relation to those upstream and/or downstream purchases where they face sufficient choice of suppliers. This would reduce the incentives to engage in input foreclosure, as is discussed further below in the Commission’s overall assessment of incentives to foreclose.

156. Alternative choices are available to OEMs both in their upstream standard grade purchases and for the majority of their downstream casting and forging purchases. For example, Timet achieves […]% of its aerospace revenues from sales of standard Ti 6-4. As standard grade Ti 6-4 can also be produced by four other suppliers, OEMs face a number of supply options in the upstream purchases of standard grade titanium products. Accordingly, OEMs can threaten to switch parts of their purchases of Ti 6-4 to alternative suppliers in reaction to any potential input foreclosure strategy by the merged entity in respect of monopoly or sole-supplied products.

157. The Commission therefore considers that the OEMs’ bargaining power in the aerospace industry continues to constitute a significant constraint on the merged entity’s ability to foreclose access to titanium inputs.

d) Alternative titanium suppliers, switching costs and possibility of sponsored entry

158. The Commission has also assessed possible counter-strategies that could be adopted by downstream competitors and OEMs in relation to switching to alternative titanium suppliers and sponsoring entry of new qualified suppliers.57

159. The majority of the market participants raising input foreclosure concerns submit that switching supplies to alternative titanium suppliers would be difficult and would require significant investments. They refer to two main obstacles to switching.

160. First, the monopoly alloys are not produced by any of Timet’s upstream competitors. Second, for some products Timet is the only certified titanium producer for a specific OEM, again leaving the downstream customer without the choice of an alternative titanium supplier in the short term. As a consequence, switching to alternative suppliers would require customers to invest in certification procedures with OEMs (as described in section V.1.4 above) that are perceived to be too lengthy and costly to constitute a viable option for the switching of significant numbers and volumes of alloys.

161. However, the Commission notes that for the majority of titanium inputs, the OEMs have alternative certified suppliers. Considering milled rotating grade titanium (where the majority of concerns were raised), there are rotating grade alloys which OEMs already multisource from alternative suppliers. In addition, where an individual OEM may currently sole-source rotating grade alloys from Timet, other OEMs may source the same alloy from alternative certified suppliers.58 Furthermore, there are certain rotating grade alloys for which there is currently no alternative producer. However, the monopoly alloys represent a very small percentage of Timet’s total sales of titanium alloys to the aerospace industry, namely [0-5]%.

162. In addition, the OEMs have the option of certifying other suppliers. ATI, RTI and VSMPO are already certified suppliers of different types of non-rotating and rotating grade alloys and as such have the required experience to go through the certification process.59

163. As regards the cost and time investments, market participants contacted in the market investigation explained that the certification process differs according to a variety of factors. The most common estimates for the most complicated certification processes were of investments of at least USD 500,000 over a time of one to two years.60

164. On this basis, the Commission considers that in the short to medium term, OEMs would have the capacity to certify alternative suppliers for a certain amount of alloys. This could result in loss of business for the merged entity before the expiry of the existing LTAs within the limits of market share requirements under the LTAs.61 This would provide additional incentives for the merged entity to preserve its good relationships with the OEMs and possibly to enter into new LTAs with OEMs to prevent further loss of business.

165. In the long run, OEMs could qualify alternative suppliers for significant numbers and volumes of alloys. The OEMs would be protected whilst undertaking these investments until the expiry of their LTAs, i.e. until […] for a number of important Timet OEM customers.

166. In this context, the Commission has also considered that the certification process is ultimately influenced by the large airframe manufacturers, i.e. Airbus and Boeing. This influence results in leverage of the airframe manufacturers over suppliers active in the industry. If there are risks to the titanium supply chain or there are strategic benefits in certifying new suppliers, the airframe manufacturers could sponsor entry of alternative suppliers for the OEMs, including by carrying parts or all of the costs of the certification process.

167. The Commission therefore considers that there are effective and timely counter- strategies that downstream competitors, OEMs and airframe manufacturers would be likely to deploy in reaction to an input foreclosure strategy by the merged entity.

e) Conclusion on the ability to foreclose access to inputs

168. Based on the above, the Commission finds that on balance the protection offered by LTAs, the bargaining power of OEMs, the possibility of customers to switch to alternative titanium suppliers and the possibility of sponsored new entry is likely to constrain the merged entity’s market power after the proposed transaction. Therefore the Commission considers that the merged entity is unlikely to have the ability to foreclose access to titanium inputs.

V.4.3.2. Incentive to foreclose access to input

169. The Commission’s Non-Horizontal Merger Guidelines further require the assessment of the profitability of an input foreclosure strategy, in order to substantiate an input foreclosure concern. For the merged entity to have the incentive to foreclose its downstream competition, the profit gains downstream must outweigh the profits lost upstream.

170. The Commission's conclusion on the inability by the merged entity to engage in input foreclosure means that the question of whether the merged entity would face incentives to engage in this strategy can ultimately left open. However, for the reasons given below, the Commission also considers it unlikely that the merged entity would have incentives to engage in input foreclosure.

a) Profitability of complete foreclosure - PCC's capacity to absorb Timet's production

171. The Commission has analysed the Notifying Party’s argument that a complete foreclosure strategy would not be economically rational for the merged entity.

172. The Notifying Party has demonstrated that it will not be able to absorb all of Timet’s production of titanium for forging purposes (the area where the vast majority of concerns were raised). This position was also confirmed by statements made by different market participants contacted in the market investigation.62 Therefore complete foreclosure in forging products would result in the loss of substantial business for the merged entity upstream, making such strategy unprofitable.

173. With regard to casting products, the Notifying Party could in theory absorb all of Timet’s production of titanium for casting applications. However, the Notifying Party already purchases […]% of Timet’s output of titanium products for casting applications, while only […]% or […] MT of Timet’s output for casting applications are currently sold to third parties. Therefore, even if the Notifying Party were to absorb all of Timet’s titanium for casting applications, this would not result in a significant change in the market. The merged entity’s downstream competitors already have the necessary supply relationships in place with alternative titanium suppliers. Accordingly, any profits to be gained from such strategy would be limited.

174. The Commission therefore considers that the merged entity is unlikely to have the requisite incentives to pursue a complete foreclosure strategy.

b) Profitability of partial foreclosure - Ability to increase sales downstream

175. In addition the Commission has assessed whether a partial foreclosure strategy, i.e. through raising rivals costs, would make economic sense for the merged entity. The Commission finds that there are not sufficient incentives to pursue such a strategy for three reasons.

176. First, PCC would not be able to expand its sales significantly due to existing capacity constraints. According to data submitted during the Commission’s investigation, the Notifying Party has approximately […]% of spare additional capacity for titanium-based forged products and a similar level of spare additional capacity for titanium-based casting components on aggregate. These existing capacity constraints would limit the gains from input foreclosure.63

177. Second, the downstream LTAs limit the ability of the merged entity to increase its downstream margins and prices as a result of an input foreclosure strategy.64 Currently practically all of PCC's sales are covered by LTAs, with more than […]% of its sales covered by LTAs that expire in […] or beyond. Even if the merged entity raised prices for those sales of rotating grade components where LTAs expire within the next two years, the Notifying Party estimates additional downstream profits to be limited to approximately USD […]65. This short term gain appears minor against the potential loss of business through OEMs’ long-term switching of business of standard upstream products or downstream products to alternative suppliers. More generally, the base of sales over which the merged entity would benefit from an increase in prices downstream is relatively limited, given that PCC has a share of less than 30% of the markets for forged engine components.66

178. Third, the counter-strategies available to OEMs due to their bargaining power and their ability to switch volumes away from the merged entity, as described in sections V.4.3.1 c) and d) above, would limit the overall profitability of such foreclosure strategy.

179. The Commission therefore considers that the merged entity is unlikely to have the incentives to pursue a partial foreclosure strategy, even if it had the ability to engage in such a strategy.

c) Previous examples of vertical integration in the titanium and nickel industries

180. Finally, the Commission has also taken into account additional evidence related to previous strategies pursued by vertically integrated players in the titanium and nickel industries.67 Due to the role played by OEMs in directing sales from inputs suppliers to component manufacturers, there are continued sales between vertically integrated players and their competitors in the upstream and downstream markets. The market investigation has not revealed evidence about attempts at pursuing input foreclosure strategies by vertically integrated players in these markets.

d) Conclusion on the incentives to foreclose access to inputs