Commission, July 20, 2010, No M.5904

EUROPEAN COMMISSION

Judgment

SAP/ Sybase

Dear Sir/Madam,

Subject: Case No COMP/M.5904 – SAP/ Sybase Notification of 16 June 2010 pursuant to Article 4 of Council Regulation No 139/2004[1]

1.On 16 June 2010, the Commission received a notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which SAP AG ('SAP', Germany), through its wholly-owned subsidiary, SAP America, will acquire sole control over Sybase, Inc. ('Sybase', United States).

2.After examination of the notification, the Commission has concluded that the notified operation falls within the scope of the Merger Regulation and does not raise serious doubts as to its compatibility with the internal market and the EEA Agreement.

I. THE PARTIES

3.SAP, a German company active worldwide, develops, produces and markets enterprise application software ('EAS') solutions. It also provides support, consulting, maintenance and training services. SAP has a limited presence in the databases and middleware markets.

4.Sybase is a US-based software vendor, focusing on databases, data management, middleware and mobile architectures.

II. THE OPERATION

5.The proposed concentration concerns the acquisition of sole control by SAP AG of Sybase, through a public tender made by Sheffield Acquisition Corp, a wholly owned subsidiary of SAP America Inc, which in turn is a wholly owned subsidiary of SAP AG. The notified operation therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

III. EU DIMENSION

6.The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 billion[2] (SAP: EUR […]; Sybase: […]). Each of them has an EU-wide turnover in excess of EUR 250 million (SAP […]; Sybase […]), and does not achieve more than two-thirds of its aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has EU dimension.

IV. ASSESSMENT

7. Both SAP and Sybase are active in the databases, middleware and the EAS sectors. As will become apparent from the below the scope of the competitive overlap within those sectors is however marginal since the products of the parties are largely complementary.

8.Moreover, SAP is not at all active in a number of other markets where Sybase has a strong focus, such as wholesale international carrier services and mobile messaging services. Those markets will not be assessed further.

A. Market definition

1. Databases

9.Databases are software programmes designed to store, organise, analyse and retrieve information held in an electronic format as opposed to traditional paper-based filing methods. A complete data storage system consists of data storage (for example hard disks) in which the data is physically kept and a software system (the 'database management system' or 'DBMS') to manage the organisation, storage, access, security and integrity of data.

10.The most common system for organising databases today are relational database management systems (often abbreviated to 'RDBMS') which store data in separate tables and define relationships between these tables instead of placing all data in one large table. This makes it possible to combine the data from several tables for querying and reporting. Relational database technology allows databases to be larger, faster and more efficient.

11. In the Oracle/Sun Microsystems case, the Commission considered a number of possible narrower market definitions of RDBMS, such as distinguishing between general purpose databases and specialized databases for instance those for data warehousing[3], but ultimately concluded that the market was the one “comprising all RDBMS”.[4]

Possible submarkets in the data warehousing space

12.Both SAP and Sybase are active in the field of data warehousing. The notifying party considers that data warehousing tools should properly be classified as database software, rather than as a sub-segment of business analytics software (a possible segment of EAS), as indicated by industry analysts and considered by a Commission precedent (SAP/Business Objects5).

13.Industry analyst IDC defines the data warehousing platform software space as being composed of two market segments, data warehouse generation and data warehouse management. Data warehouse generation tools include software used in the design, cleansing, transformation, loading, administration of the data warehouse.[5] Data management tools include database management systems software used to manage and process data in the data warehouse.[6]

14.The market investigation did not allow the Commission to reach a clear conclusion as to whether data warehousing tools are properly classified as part of the business analytics software space rather than the database space. Indeed, some respondents indicated that since data warehouse platforms combine both business analytics software and a database, they may be classified as both database software and business analytics software.[7] Irrespective of whether this segment should be classified as part of the RDBMS market or the Business Analytics market, the proposed transaction would not raise any competition concern. Similarly, the market investigation did not allow the Commission to reach a clear conclusion as to whether for the purposes of market definition a distinction should be made between data warehouse generation tools and data management tools.[8] This issue may be left open since, even on the basis of a further segmentation between data warehousing generation tools and data warehousing management tools, the operation would not raise any competition concerns.

Possible submarket for embedded databases

15.In the Oracle/Sun Microsystems case, the Commission also analyzed the possibility of a sub-market for embedded databases but concluded that it was not appropriate to conclude as to existence of such separate market. In the case at hand, given that only Sybase is active in the embedded database segment with a small market share, the assessment of the case will not change in relation to any possible market definition.

16. For the purposes of this decision, the exact definition of the relevant product market in relation to databases can be left open, as the proposed transaction does not raise any competition concerns under any alternative market definition.

17. Given the purchase and utilisation patterns of databases software, the Commission considers the geographic scope of possible database markets as worldwide. This is inline with its conclusion in the Oracle/Sun Microsystems case.[9]

2. Enterprise Application Software (EAS)

18.EAS supports major business functions needed to manage a business effectively at a corporate or branch level (such as managing corporate finances, automating the sales and marketing functions of a company, or managing the resources involved in corporate projects).[10]

19.The notifying party submits that the relevant market for the purposes of the assessment of the proposed transaction is the supply of EAS. The notifying party also submits that a narrower delineation of the market such as on the basis of industry sector of application or on the basis of high-end, mid-range and low-end software would be inappropriate.

20.In the Oracle/Peoplesoft decision, the Commission has considered the market for EAS as a sub-category of business application software (as opposed to consumer software) which comprises applications and services related to the implementation and use of such software.[11] In that decision, the Commission also found that the EAS market could be sub-divided into various categories having functionality with broadly similar purposes.[12]

21.In the SAP/Business Objects decision,[13] the Commission considered a possible subdivision of EAS (proposed by the notifying party) into: (i) Enterprise Resource Planning ('ERP'); (ii) Customer Relationship Management ('CRM'); (iii) Supply Chain Management ('SCM'); (iv) supplier relationship management ('SRM'); (v) product lifecycle management ('PLM') and (vi) business analytics[14] ('BA').

22.From the information submitted by the notifying party, it appears that the parties' activities would overlap in the field of EAS only if data warehousing tools were to be considered as part of the BA segment.

23.In the SAP/Business Objects case[15], the Commission considered further delineations of the BA segment into: (i) performance management tools and applications ('PMT');[16]and (ii) data warehouse platforms. Whilst the market investigation in this case pointed towards the existence of a market for BA, the exact product market definition was ultimately left open.[17]

24.Industry analyst, IDC, considers that the business analytics software market is segmented into four primary segments[18], namely: (i) analytics applications[19]; (ii) business intelligence ('BI') tools[20]; (iii) data warehousing platform software; (iv) spatial information analytics tools.

25.As explained in paragraph 12 above, the notifying party considers that data warehousing software is infrastructure software and should properly be classified as database software, rather than as business analytics software. As indicated in paragraph 14 above, the market investigation was inconclusive on this point.

26.In any event, the assessment of the case will not change regardless of whether the data warehousing tools are considered to be part of the database or EAS space. Similarly,

the assessment of the case would not change if a distinction were to be made between data warehouse generation tools and data management tools.

27.The market investigation also assessed whether it would be appropriate to segment EAS on the basis of industry sector of application or on the basis of high-end, midrange and low-end software, as has been considered in the recent Dassault Systemes /IBM DS decision.[21]

28.The market investigation was inconclusive regarding the segmentation of EAS on the basis of industry sector of application.[22] Yet, the market investigation indicated that it would be possible to segment EAS on the basis of high-end, mid-range and low-end software.[23] However, for the purposes of this decision, the exact product market definition may be left open in relation to EAS since the competitive assessment will not change regardless of the market definition.

29.In previous decisions[24], the Commission considered that the geographic market for EAS was at least EEA-wide, but ultimately left the market definition open. The notifying party submits that the geographic scope of the EAS market is worldwide.

30. For the purposes of this decision, the exact geographic market definition may be left open since the proposed transaction will not give rise to any serious competition concerns even on the narrowest possible geographic market (EEA).

3. Middleware and mobile middleware

31. Middleware refers to a wide category of software products that provide the infrastructure for applications to run on a server, be accessed from a variety of clients over a network and be able to connect a variety of information sources.[25]

32. In Oracle/BEA[26] a segmentation of the overall middleware space according to the enduse of the product, although widely acknowledged by the investigation, was ultimately left open.

33. The notifying party submits that a relevant product/service market is the overall middleware market and that, for the purpose of the transaction, it is not necessary to decide whether narrower markets exist.

34. The notifying party has identified a number of potential sub-segments on the middleware market where the parties are present. In particular, the notifying party has identified mobile middleware as a potential segment where the parties are present.

35. Mobile middleware consists of a software platform that includes server and/or client software that aims at enabling the mobile use of enterprises applications leveraging a variety of mobile devices as detailed below:

36. Most respondents to the market investigation consider mobile middleware as a separate sub-segment of the overall middleware market, due to distinct functions and technical characteristics on the demand side, and limited supply-side substitutability. A number of respondents indeed indicate that the entry of companies not active in mobile middleware but in other middleware products categories would require significant investment and time.

37. A number of respondents indicate on the contrary that the distinction between mobile middleware and other middleware is bound to blur as the distinction between mobile and non-mobile devices and applications become less clear. Moreover, it is also expected that barriers to entry might diminish: as outlined by one respondent "with the advent of more capable devices (smart phones) with active development communities and downloadable applications as well as more efficient mobile IP connectivity (HSPA, and later LTE) the barriers for new players in this field are becoming drastically lower."[27]

38. The Commission has also investigated the possible existence of a separate market for mobile corporate e-mail (i.e. solutions to access corporate emails through mobile devices). The outcome is however not conclusive, with respondents considering mobile corporate e-mail either as a separate market, either as part of the overall mobile middleware market or as a mobile application.

39. The notifying party does not consider it appropriate to further segment the mobile middleware market on the basis of the type of application or the type of mobile/wireless device.

40. Most respondents to the market investigation share this view.

41. Whereas the results of the market investigation do not allow concluding on a concrete segmentation of the Mobile middleware market, several respondents have indicated that mobile device management, mobile security and mobile business applications can be considered as potential segments of the Mobile middleware market. Several respondents further indicated that for a company already active in other segment of the mobile middleware market, significant investments and time (up to 5 years according to one respondent) are necessary to enter one of the mobile middleware segments, suggesting the possible existence of sub-markets.

42. In the present case, although the market investigation points towards the existence of a market for mobile middleware and possibly towards the existence of separate submarkets, the exact delineation of the market can be left open as, even under the narrowest possible definition, the transaction does not raise serious competition concerns.

43. The Commission assessed middleware markets in the Oracle/BEA and the Oracle/Sun transactions as worldwide markets. In the present case, the worldwide scope of the market is also widely acknowledged by the investigation. The Commission will therefore assess the transaction under a worldwide scope.

B. COMPETITIVE ASSESSMENT

1. Databases

(a) The parties' products

44. Sybase's main database offering comprises two lines of enterprise class RDBMS, namely, (i) Adaptive Server Enterprise (ASE) which is Sybase’s basic RDBMS for mission critical transactions, with capabilities similar to that of Oracle's database or the databases of Microsoft and IBM; and (ii) Sybase IQ which is a data management software for data warehousing applications. IQ is a column-based high performance analytics platform for business intelligence and reporting needs and is optimized for high-speed query performance over large quantities of data.

45. Sybase also offers the Sybase RAP (Risk Analytics Platform), a data warehouse platform which is a specialized analytics platform operating on IQ mainly used in financial markets.

46. In addition Sybase has two main lines of embedded RDBMS: SQL Anywhere and Advantage Database Server (ADS). SQL Anywhere is the company’s embedded mobile database platform providing data management and synchronization capabilities between the data centre and frontline mobile devices.

47. SAP's main business focus is the sale of EAS solutions, where it is a clear market leader in the EEA and holds a leading market share, closely followed by Oracle, at worldwide level.[28] Together with its EAS solutions, SAP resells third-party databases which are SAP-certified such as Oracle database 11 G, IBM’s DB2 and Microsoft SQL Server. SAP also has its own database solution (MaxDB) included as part of the SAP suite (and not sold on an independent basis).

(b) Assessment

48. The activities of SAP and Sybase overlap only to a very limited extent in the relational database market.

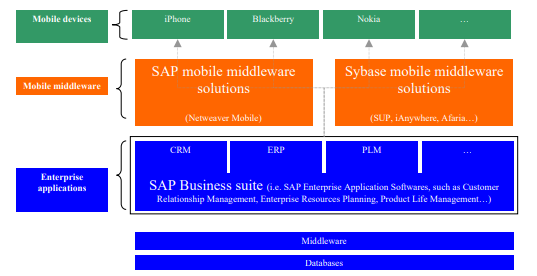

49. When considering the overall RDBMS, Sybase's market share based on revenue was below [5-10]% in 2009[29] and SAP's MaxDB sales amounted to less than [0-5]% on the basis of the market volume in 2009.[30] Therefore, the proposed transaction does not give rise to an affected market in this regard.

50. Moreover, the vast majority of respondents have indicated that Sybase's database offering, in particular its ASE database, and SAP's database offering (that is, MaxDB as embedded in SAP's enterprise application software) are not substitutes from a customer's perspective and not in direct competition on the market.[31]

51. The parties are also active in the possible sub-segment of data warehousing tools. Irrespective of whether this segment should be classified as part of the RDBMS market or the Business Analytics market, the proposed transaction would not raise any competition concern as regards the horizontal overlap. Indeed, the proposed transaction would result in a combined worldwide market share of approximately [05]%.[32] Moreover, the vast majority of respondents have indicated that they do not consider that SAP and Sybase are close competitors in the data warehouse platforms area.[33]

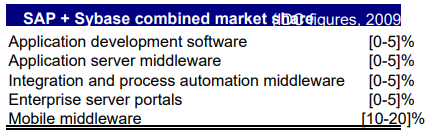

52. Even on the basis of possible further segmentation between data warehousing generation tools and data warehousing management tools, the operation does not raise any competition concerns. Given that SAP is not active in the field of data warehouse management, the proposed transaction would not give rise to a horizontal overlap. As regards data warehouse generation, the proposed transaction would only result in a worldwide combined market share below [5-10]%[34].

53. As regards the hypothetical segment for embedded databases, since only Sybase is active in this space, the proposed transaction would not give rise to a horizontal overlap in this regard.

54. In light of the above, it may be concluded that the proposed transaction would not give rise to any horizontal competition concerns as regards databases.

2. Enterprise Application Software

(a) Horizontal Overlaps

55. According to the notifying party, the parties' activities in the field of EAS would overlap only in so far as data warehousing products are considered to form part of the BA segment.[35]

56. Only the overall EAS market and the potential BI sub-segment would constitute affected markets. As regards the overall EAS market in Western Europe[36], the combined market share for the parties post transaction would be approximately [1020]% (SAP [10-20]%; Sybase: <[0-5]%).[37] As regards the BI sub-segment in Western Europe, the combined market share for the parties post transaction would be below [20-30]% (SAP [20-30]%; Sybase: [0-5]%).[38] Yet, in both cases the increment brought about by the proposed transaction would be insignificant. In addition, a number of other market players, including major competitors such as Oracle, Microsoft and Siemens, are present on the market and can be expected to continue to exercise significant competitive constraints on the merged entity post-merger[39].

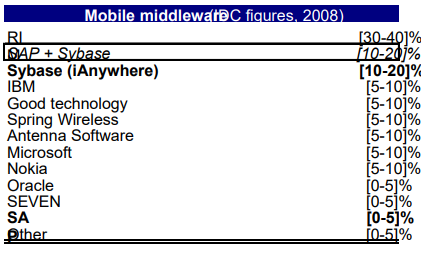

57. The parties' activities overlap with a small combined market share in the possible subsegment of data warehousing tools. As indicated in paragraph 51 above, irrespective of whether this segment should be classified under the RDBMS market or under the

Business Analytics market, the proposed transaction would not raise any competition concern as regards the horizontal overlap. Indeed, the proposed transaction would result in a combined worldwide market share of approximately [0-5]%.[40] Therefore, the proposed transaction does not give rise to affected markets in this regard.

58. With regard to a potential segmentation on the basis of industry sector of application, neither Gartner nor IDC report on EEA market shares on industry-specific markets. Sybase's presence in Business Analytics, which is limited to data warehouse management, has a strong focus on financial services sector. On the other hand, SAP's estimated share, based on IDC’s 2009 Business Analytics Top 10 Vendors revenue by industry, is at [5-10]% in banking, [0-5]% in insurance and [0-5]% in securities and investment services.[41] Therefore, given the complementarity of Sybase and SAP's products, SAP’s minor presence as regards financial services and the small presence of Sybase in Business Analytics, even in a hypothetical market for BA used in the financial sector, the transaction would not raise any horizontal concerns.

59. In light of the above, it may be concluded that the proposed transaction would not give rise to any horizontal competition concerns as regards EAS.

(b) Non-Horizontal issues – SAP EAS and Sybase databases

60. Post-merger, the merged entity will have the possibility to offer to its customers a stack of databases, middleware and enterprise application software. SAP and Sybase are active in neighbouring markets. SAP is amongst the market leaders in EAS, whereas Sybase is present in RDBMS, where SAP held a worldwide market share of less than [0-5]% in 2008. Furthermore, SAP is amongst the market leaders in BA[42], whereas Sybase is present in data warehousing with a market share of [0-5]% worldwide 2008.

61. The notifying party submits that SAP has not sufficient market power on the market for EAS to be able to foreclose database competitors. Moreover, the notifying party submits, if SAP were to force customers of its EAS to use Sybase databases, it would risk losing significant customers given the presence of vertically integrated competitors such as Oracle or Microsoft and other EAS vendors which allow heterogeneous environments.[43]

62. EAS applications need to run on the enterprise's databases: therefore purchasing decisions of these two elements of the stack are interconnected and often happen simultaneously. SAP holds market shares above [30-40]% on the following potential EAS segments in Europe: (i) ERP segment ([30-40]% market share in terms of revenue) and (ii) SCM segment ([30-40]% market share).[44] SAP faces competition on these segments from a number of vertically integrated firms, including Oracle and Microsoft.[45]

63. Given SAP's substantial presence on these EAS segments, the market investigation examined whether the merged entity would have the ability and incentive to engage in bundling/tying practices and, in particular, to restrict customers' ability to use other vendors' database products by for example no longer supporting other vendors' databases or restricting the interoperability of its EAS with other vendors' database products[46]. Although SAP's market shares in relation to BA are well below [30-40]% and therefore do not indicate, prima facie, market power[47], the market investigation also assessed the ability and incentives of the merged entity to engage in tying and bundling of SAP BA and Sybase data warehousing products (in so far as these products may be considered as distinct from the EAS space).

64. All but one of the respondents to the market investigation indicated that the merged entity would not control a 'must have' product and that there would be one or several viable alternatives.[48]

65. Furthermore, the vast majority of respondents to the market investigation indicated that the merged entity would not, as a result of the proposed transaction, have the ability and the incentive to restrict, in the short term, the ability of customers to use other vendors' database products.[49]

66. Moreover, the vast majority of customers do not consider that SAP, as a result of the proposed transaction, would have an interest in terminating its partnerships with any of its current database partners in order to sell its enterprise solutions only with ASE or other Sybase products.[50]

67. Even though, post merger, the merged entity would have the possibility to offer its customers a stack of databases, middleware and EAS, the vast majority of respondents to the market investigation do not consider that the merged entity would be in a position to foreclose its competitors in the different layers of the stack.[51]

68. Given the level of the combined market shares and the presence of strong competitors on all the layers of the stack, together with the elements above, the Commission considers that the proposed transaction does not give rise to any non-horizontal competition concerns.

3. Middleware and mobile middleware

(a) The parties' products

69. With regard to middleware, SAP has home-grown solutions for application infrastructure suites (NetWeaver and SAP Platform Infrastructure), application servers (SAP Web Application Server), and portal products (SAP Enterprise Portal). SAP also developed mobile middleware by enabling its NetWeaver Mobile platform.

70. Sybase’s middleware offering includes mostly application development software (PowerDesigner, PowerBuilder, Workspace), application servers (EAServer) and mobile middleware. With regard to the latter, its main products is Sybase Unwired Platform (“SUP”), a platform for the design, development and deployment of mobile solutions that integrate enterprise applications interfacing with databases or Web services.

71. As part of its mobile offering, Sybase offers in particular: (i) Afaria (mobile security and management solution); (ii) iAnywhere Mobile Office (corporate emails); and (iii) RemoteWare (retail polling, file transfer and content distribution).

(b) Horizontal overlap

72. Both SAP and Sybase have a very limited presence in the overall middleware market defined globally. On the basis of IDC 2008 figures, their combined market share is estimated at [0-5]%. On the basis of Gartner 2009 figures, their combined market share is [0-5]%.

73. With regard to the possible sub-segments of the middleware market, defined according to IDC classification, their combined market share is estimated in 2009 as follows:

74. In all these sub-segments, the parties face strong competitors such as IBM, Oracle, Microsoft, Hitachi and NEC. Given the relatively higher market share in mobile middleware, the market investigation focussed essentially on this segment.

75. "Mobilizing" SAP's EAS solutions was presented by the notifying party as one of the key rationales of the transaction.

76. SAP NetWeaver Mobile platform is not offered on a stand-alone basis53. Currently, SAP relies extensively on partnerships for the mobilization of its applications: (i) cobranded ventures such as with RIM, Syclo and Sybase (ii) solution extensions54 to SAP (iii) partner offerings certified on SAP NetWeaver and (iv) other alternatives such as SAP BusinessObjects Mobile and Nokia’s support for the SAP portal on Symbian Series 60 devices.

77. Sybase has a strong focus on the development of mobile middleware solutions with a neutral architecture, since its Sybase Unwired Platform supports heterogeneous operating systems and device environments and enables interoperability with a variety of enterprise applications, databases and web services. According to the parties, SAP’s partnership with Sybase for Mobiles Sales and Mobile Workflow products is an indication of the complementary nature of their services.

78. A rough estimate, based on Gartner Mobile enterprise application platforms market size figures55 and SAP's and Sybase's entire "Mobility" revenues, indicates a combined share ranging from [20-30]% to [20-30]% in 2009 with a small increment. According to Gartner, Sybase is as a leader in mobile enterprise application platforms alongside Antenna software and Syclo. Furthermore, Gartner considers RIM and Microsoft as challengers on that market. In addition, Gartner forecasts a 15 to 20% annual growth of this market through 2013.

79.As regards potential sub-markets, the only overlap between SAP and Sybase relate to mobile business applications. According to IDC 2008 data, SAP's and Sybase's combined market share is estimated at [10-20]%.

80. However, the IDC figures encompass revenues from mobile corporate e-mail services. If this component is excluded, then the parties' combined market share is estimated at [3040]% (Sybase: [20-30]%, SAP: [5-10]%) in 2008 (notably because RIM has a more limited share in such a market). However, IBM ([10-20]%), Spring Wireless ([1020]%), Antenna Software ([10-20]%) and Oracle ([5-10]%) remain present with significant market shares.

81. The market investigation confirmed the limited competitive constraint exerted by SAP on the middleware market.

82. First, most respondents amongst the customers do not consider SAP as an actual or potential significant competitive force in the mobile middleware market. The responses from competitors, albeit more nuanced, point in the same direction. A competitor also indicates that "It seems that SAP currently lacks the capabilities and products to compete strongly in this area. (…) The Sybase acquisition will make them more competitive and fill some obvious holes in their portfolio, but it will in our opinion still not make them a contender in the mobile middleware market".[52]

83. Second, SAP is not perceived as a close competitor of Sybase. A majority of respondents to the market investigation indeed confirm the largely complementary nature of SAP and Sybase mobile offerings. According to one respondent, "The SAP offering comprises only middleware solutions for its own applications, whereas Sybase's products enables mobilisation of a wide range of business applications. Due to limited product scope of SAP, its competitive relevance on the middleware market appears to be limited as well."[53]

84. Third, as regards potential competition and barriers to entry into the mobile middleware market, several respondents refer to a number of new entrants (e.g. Syclo, Google, Huawei…). While the investigation also reveals the existence of certain barriers to entry, notably the number of backend systems and devices to integrate, one respondent makes a distinction between device specific APIs (e.g. Blackberry) and open or standard APIs (e.g. Microsoft ActiveSync), for which the barriers to entry are lower. Moreover, according to one customer, "the mobile middleware market is nascent with significant growth potential. Many new vendors have entered this market and many vendors offer niche products. […] believes these vendors have the potential to expand the functionality of their products as they continue to grow."[54]

85. Lastly, while most respondents amongst the customers do not see open source as a credible alternative in the mobile middleware market, the responses from the competitors are more nuanced. Most respondents on the competitors' side consider that open source products affect the positioning of traditional players, but it is also outlined that this depends on the specific segment considered.

86. The overall outcome of the market investigation appears positive with regard to the impact of the transaction on a hypothetical mobile middleware market. Notably, most respondents consider that the impact of the transaction on prices will be limited, given the characteristics of the mobile middleware market as detailed above. Some respondents point out that the transaction may lead to more innovation. According to one customer, "these markets are nascent and ever changing. New entrants exert competitive pressure on established companies and all players must continue to create State of the Art products to remain competitive. Furthermore as device capabilities expanded, companies will have to continue to develop new applications to enable a mobilized workforce."[55] Most respondent suggest that a strategy to raise prices would be counter-productive in the presence of a several alternative solutions from a number of competitors. A competitor comments that "if they raise prices too much or fail to continue to innovate, they will, over time fall behind the market and have less ability to control pricing and access within their customer base. Similarly, if they raise prices or fail to continue to innovate, they could lose customers/market share with non-SAP customers."[56] Finally, most respondents consider that, post-transaction, consumers will continue to have sufficient choice.

87. The Commission therefore considers that the merged entity will continue to face significant and strong competition and that customers will still have access to a sufficient number of alternative solutions.

(c) Non - horizontal issues

88. The acquisition of Sybase by SAP will enable SAP to be present on every layer of the Mobile IT stack and thus to provide enterprises with a combined software stack optimized to create a seamless flow of information between the data centre on the enterprise premises to any mobile or fixed end-point. The merged entity will be present on all markets or segments, with a significant market share on mobile middleware ([1020]%), mobile device management ([10-20]%) and mobile security ([20-30]%), and to a lesser extent on embedded databases[57] ([5-10]%).

89. Most respondents to the market investigation confirm however that none of Sybase's products in mobile middleware represent a "must-have" product, for which alternatives would be limited. Moreover, a large majority of respondents consider that market presence for every layer of the Mobile IT stack, while being a possible advantage, is not indispensible to compete effectively in the mobile space. Most respondents do therefore not anticipate that, given Sybase's significant presence on the mobile middleware market, post transaction the merged entity could have incentives to impose the acquisition of SAP EAS products to its customers, since such a strategy could put at risk the existing customer base of Sybase.

90. Moreover, the Commission considers that a foreclosure strategy on the EAS market would significantly undermine Sybase’s current customer base which is largely reliant on competing EAS solutions and would be in contradiction with Sybase’s current successful strategy to develop an open architecture. In light of these elements, together with the existence of alternative solutions for Sybase's products, the Commission can conclude that it is unlikely that the merged entity will engage in a foreclosure strategy on the EAS market.

91. Another issue raised in the market investigation was whether, given SAP's significant presence on the EAS market, post transaction the merged entity could have incentives to impose the acquisition of Sybase's products, for instance through bundled offers.

92. According to one competitor, given SAP's large customer base, and its strong product portfolio, SAP might have incentives to offer rebates on Sybase products (or even offer them for free) in exchange of the acquisition of a significant number of SAP products.

93. It appears however that a foreclosure scenario on the mobile middleware market is also unlikely.

94. First, according to the notifying party, the merged entity does not have the ability to engage in a foreclosure strategy on the Mobile middleware market.

95. EAS and mobile middleware are generally purchased separately and a number of system integrators seek to purchase mobile middleware separately from their applications in order to develop tailored solutions for specific devices such as Motorola and Intermec.

96. This is confirmed by the market investigation which shows that mobile middleware products are either sold on a stand alone basis or as part of a suite. In addition, one competitor indicates that the trend is clearly towards unbundled products.

97. Moreover, although SAP enjoys a relatively strong competitive position on the EAS market, it is facing significant competition in that space from major players such as Oracle, IBM and Microsoft. The notifying party indicates that, should the merged entity attempt to engage in a foreclosure strategy in the mobile middleware market, Sybase's competitors would retain access to a significant share stemming from SAP's competitors on EAS. This is evidenced by offerings already developed by Sybase's competitors with other EAS vendors, such as SMART (Syclo's solution to mobilize Oracle CRM) and AMP (Antenna's solution to mobilize Oracle CRM). In addition, the notifying party estimates the common customers' base of SAP and Sybase at around [20-30]% of the mobile middleware market, which leaves a significant share of the market to be exploited by other mobile middleware vendors.

98. Lastly, a foreclosure strategy would be clearly limited, at least in the short term, by Sybase's competitors' offerings certified by SAP (such as Syclo's SMART, Antenna's Mobility platform, Concert and Dexterra Concert) or co-branded offerings developed by SAP together with RIM, Spring Wireless, Abaco Mobile and Sky Technologies. It must be noted that none of the responding Sybase's competitors that are in partnerships with SAP anticipate that the transaction will have any effect on the offering they have developed jointly with SAP.

99. Therefore, the Commission concludes that the merged entity will not have the ability to adopt a successful foreclosure strategy on the Mobile middleware market.

100. Secondly, according to the notifying party, the merged entity does not have the incentive to engage in a foreclosure strategy on the Mobile middleware market. Since mobile workers require access to a variety of applications, if SAP were to narrow its applications to Sybase mobile middleware only, it would risk to undermine the attractiveness of its applications. Given the differences in proportions of the revenues generated on both markets, it appears unlikely that SAP puts at risk its EAS revenues to foreclose the mobile middleware market. In 2009, licence revenues stemming from Sybase Unwired Platform represented less than […]% of SAP Business suite licence revenues. The entire mobile middleware market represents only […] of SAP Business suite revenues.

101. In addition, Sybase will continue as a standalone business unit within SAP. The notifying party refers to its practice following a recent large acquisition - Business Objects. BusinessObjects was acquired in 2007 and SAP has continued to maintain BusinessObjects’ analytics business and in particular, to maintain open standards based interoperability.

102. Therefore, the Commission concludes that the merged entity will in any event also have no incentive to adopt a foreclosure strategy on the Mobile middleware market.

103.Thirdly, the EAS market is characterised by strong competition given the presence of large vertically integrated vendors (such as Oracle, Microsoft and IBM), of wellestablished application vendors with business suites (such as Sage, Lawson and SAS) and highly specialised point solution vendors.

104. Therefore, the Commission concludes that the overall impact on prices and choice of a foreclosure strategy on the mobile middleware market would in any event be limited.

105. In light of these elements, the Commission can conclude that it is unlikely that the merged entity will engage in a foreclosure strategy on the Mobile middleware market.

VI. CONCLUSION

106. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 Turnover calculated in accordance with Article 5(1) of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C95, 16.04.2008, p1).

3 As stated in Case No. COMP/M.5529, Oracle/Sun Microsystems, 21 January 2010, recital 37, data warehouses contain (often massive amounts of) historical data that normally does not change much. Therefore, databases optimised for data warehousing need to be able to read large amounts of data very quickly. They are frequently needed for "data mining", where data are used for business intelligence, analytics and other decision support requirements.

4 Case No. COMP/M.5529, Oracle/Sun Microsystems, 21 January 2010, recital 109. Case M. 3216 - SAP/BusinessObjects, 22 October 2007.

5 According to IDC, master data management applications as well as the majority of data quality tools are not included in the data warehouse generation segment.

6 IDC, "Worldwide Data Warehouse Platform Software 2008 Vendor Shares", July 2009, page 1.

7 See reply to question 23 and 15 of the EAS and Database questionnaires to customers and competitors respectively.

8 See reply to question 22 and 17 of the EAS and Database questionnaires to customers and competitors respectively.

9 Case No. COMP/M.5529, Oracle/Sun Microsystems, 21 January 2010, paragraph 114

10 Case M. 3216 - Oracle/Peoplesoft, 26 October 2004, paragraph 17 and Case No. COMP/M.5529, Oracle/Sun Microsystems, 21 January 2010, paragraph 24.

11 Case M. 3216 - Oracle/Peoplesoft 26 October 2004, paragraph 15.

12 Case M. 3216 - Oracle/Peoplesoft 26 October 2004, paragraph 18.

13 Case M. 3216 - SAP/BusinessObjects, 22 October 2007.

14Business analytics applications are tools and applications for tracking analysing and managing data in support of corporate decision processes (Case M. 3216 - SAP/BusinessObjects, 22 October 2007, paragraph 8).

15 Case M. 3216 - SAP/BusinessObjects, 22 October 2007.

16 Itself sub-divided into (a) business intelligence ('BI'), (b) financial performance strategy management applications, (c) customer relationship management analytics, (d) supply chain management analytics, service operations management applications and (e) workforce analytics.

17 The market investigation in that case did not allow reaching a clear conclusion as to whether BA could be further divided into sub-markets such as BI.

18 IDC, "Worldwide Business Analytics Software 2009 – 2013 Forecast and 2008 Vendor Shares", August 2009, page 1.

19 Financial performance and strategy management applications ; customer relationship, workforce, supply chain, and services operations analytic applications ; and production planning applications.

20 Query, reporting, analysis (dashboards, production reporting, OLAP and ad hoc query) and advanced analytics tools (data mining and statistics).

21 Case M.5763 – Dassault Systemes/IBM DS, 29 March 2010.

22 See reply to question 9 and 8 of the EAS and Database questionnaires to customers and competitors respectively.

23 See reply to question 10 and 7 of the EAS and Database questionnaires to customers and competitors respectively.

24 See for example Case M. 3216 - SAP/BusinessObjects, 22 October 2007 and Case M. 5229 - Oracle/Sun Microsystems, 21 January 2010.

25 See Commission decisions in Case M. 5080 Oracle/BEA, 29 April 2008 and Case M. 5229 - Oracle/Sun Microsystems, 21 January 2010.

26 See Commission decision in Case M.5080 – Oracle/BEA, 29/04/2004.

27 See reply to question 8 of the Mobile middleware questionnaire to competitors

28 Oracle and SAP hold worldwide market shares of [5-10] % and [10-20] % respectively (IDC 2009 Worldwide Enterprise Applications 2009 – 2011 Forecast Update and 2008 Vendor Shares, December 2009). At a Western European level, SAP and Oracle hold market shares of [10-20] % and [5-10] % respectively (IDC 2009 Western European Software Market Forecaster – Customised).

29 […] May 2010 indicates a worldwide market share (in terms of revenue) of [0-5] % for Sybase and market shares of [40-50] %, [20-30] % and [20-30] % for Oracle, IBM and Microsoft respectively. Similarly, Gartner ("Gartner Market Share : RDBMS Software by Operating System, Worldwide, 2009, 30 April 2010") indicates a [0-5] % market share (in terms of revenue) for Sybase and market shares of [40-50] %, [20-30] % and [10-20] % for Oracle, IBM and Microsoft respectively.

30 The notifying party estimates that it holds a market share of [0-5] % in terms of revenue.

31 See reply to question 14 and 12 of the EAS and Database questionnaires to customers and competitors respectively.

32 IDC ("Worldwide Data Warehouse Platform Software 2008", July 2009) indicates 2008 market shares (in terms of revenue) of [0-5] % and [0-5] % for Sybase and SAP respectively and market shares of [30-40] %, [20-30] % and [10-20] % for Oracle, IBM and Microsoft respectively. The notifying party estimates 2009 market shares (in terms of revenue) of [0-5] % and [0-5] % for Sybase and SAP respectively and market shares of [30-40] %, [20-30] % and [10-20] % for Oracle, IBM and Microsoft respectively.

33 See reply to question 21 of the EAS and Database questionnaires to customers and competitors.

34 IDC ("Worldwide Data Warehouse Platform Software 2008", July 2009) indicates 2008 market shares (in terms of revenue) of [0-5] % and [0-5] % for SAP and Sybase respectively and market shares of [10-20] %, [10-20] % and [10-20] % for IBM, SAS and Informatica respectively

35 According to the information submitted by the notifying party, although Sybase is active in mobile content, mobile banking and mobile messaging applications, SAP has no such activities.

36 IDC aggregates data for Western Europe, which may not include some Eastern European countries.

37 IDC 2009 Western European Software Market Forecaster – Customised. Gartner data ("Gartner Dataquest Market Statistics – Market Share: All Software Markets, Worldwide, 2008") for EAS in Europe (defined as the sum of Western and Eastern Europe and including Russia Ukraine and Belarus) do not differ significantly. Indeed, Gartner indicates a [20-30]% market share in terms of revenue for SAP and market shares of [5-10]% and [5-10]% for Oracle and Microsoft respectively. Sybase's share of the market is not included in this Gartner data.

38 IDC 2009 Western European Software Market Forecaster – Customised.

39 IDC indicates market shares of [5-10]% and [0-5]% for Oracle and Siemens respectively (IDC 2009 Western European Software Market Forecaster - Customised).

40 IDC ("Worldwide Data Warehouse Platform Software 2008", July 2009) indicates 2008 market shares (in terms of revenue) of [0-5]% and [0-5]% for Sybase and SAP respectively and market shares of [30-40]%, [20-30]% and [10-20]% for Oracle, IBM and Microsoft respectively. The notifying party estimates 2009 market shares (in terms of revenue) of [0-5]% and [0-5]% for Sybase and SAP respectively and market shares of [30-40]%, [20-30]% and [10-20]% for Oracle, IBM and Microsoft respectively..

41 Sybase’s share is too small to be referenced in this data.

42 IDC indicates market share of [10-20]% and [10-20]% for SAP in Western Europe and worldwide respectively and market shares of [5-10]% and [10-20]% for Oracle in Western Europe and worldwide respectively (Western European Software Market Forecaster – Customised and IDC 2009 Worldwide Enterprise Applications 2009 – 2011 Forecast Update and 2008 Vendor Shares, December 2009).

43The notifying party also pointed out that following its acquisition of BusinessObjects in 2007, the merged entity continued to maintain BusinessObjects' analytics business and in particular, maintained open standards based on interoperability.

44Gartner Dataquest Market Statistics – Market Share: All Software Markets, Worldwide 2008.

45Gartner indicates that Oracle and Microsoft hold market shares of [5-10]% and [0-5]% in Europe respectively

46 As regards the impact of the vertical integration brought about by the proposed transaction on the financial services sector, industry analyst IDC considers that such impact would be minimal: "… No acquisition will see the company tightly couple the database and application as the sole offering, so we will not see a reduced product offering of database support going forward. SAP has already said it will continue to support a range of databases from key partners such as Microsoft and IBM." ("Financial Services Impact of SAP Acquisition of Sybase for $5.8B", IDC, 14 May 2010.

47SAP also faces competition from vertically integrated competitors such as Oracle. Please refer to footnote 33 above.

48See reply to question 26 and 25 of the EAS and Database questionnaires to customers and competitors respectively.

49See reply to question 28 of the EAS and Database questionnaires to customers and competitors respectively.

50 See reply to question 27 and 29 of the EAS and Database questionnaires to customers and competitors respectively.

51See reply to question 25 and 26 of the EAS and Database questionnaires to customers and competitors respectively.

52See reply to question 20 of the Mobile Middleware questionnaire to competitors.

53 See reply to question 21.1 of the Mobile Middleware questionnaire to customers.

54 See reply to question 24 of the Mobile Middleware questionnaire to customers.

55 See reply to question 36 of the Mobile Middleware questionnaire to customers.

56See reply to question 34 of the Mobile Middleware questionnaire to competitors.

57 Embedded databases may be incorporated in mobile devices.