Commission, August 4, 2010, No M.5908

EUROPEAN COMMISSION

Judgment

Honeywell/ Sperian

Dear Sir/Madam,

Subject:Case No COMP/M.5908 – Honeywell/ Sperian Notification of 30.06.20 pursuant to Article 4 of Council Regulation No 139/2004[1]

I. INTRODUCTION

1. On 30.06.2010, the European Commission received a notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Honeywell International Inc. ("Honeywell", USA) acquires within the meaning of Article 3(1)(b) thereof control of Sperian Protection SA ("Sperian", France) by way of purchase of shares.

2. After examination of the notification, the Commission has concluded that the notified operation falls within the scope of the Merger Regulation and does not raise serious doubts as to its compatibility with the internal market and the EEA Agreement.

II. THE PARTIES AND THE OPERATION

3. Honeywell is a global technology supplier for aerospace and automotive products, electronic materials, specialty materials, transportation and power systems and home and building controls. Honeywell's Safety Products division manufactures personal protection equipment (hereinafter "PPE"), supplying integrated protective equipment solutions in a number of areas, including protective footwear, protective headgear and gloves. In addition, Honeywell manufactures and sells gas detection devices and gas detection sensors.

4. Sperian is active worldwide in the manufacturing of PPE held or worn in hazardous environments, focusing on head protection (eye and face, hearing, respiratory), and body protection (clothing, safety footwear, protective gloves and fall protection). Further to this, Sperian has limited activities in the field of portable gas detection devices.

5. The proposed transaction will be accomplished by way of a share purchase agreement between Honeywell and Sperian's largest shareholders, and by way of public cash tender offer to acquire the entire issued share capital of and thus control over Sperian. Consequently, the proposed transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

III. EU DIMENSION

6. The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 billion[2] (Honeywell: EUR 22 billion, Sperian: EUR 660 million). Each of them has a Union-wide turnover in excess of EUR 250 million (Honeywell: EUR […], Sperian: EUR […]), and they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State.

7. The proposed transaction therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

IV. COMPETITIVE ASSESSMENT

8. The activities of the Parties overlap with respect to PPE and portable gas detection devices in the EEA.

9. Honeywell is also active on the upstream market for gas detection sensors, which is an input for the manufacturing of portable gas detection devices.

A. PERSONAL PROTECTION EQUIPMENT

10. This transaction primarily concerns the PPE industry. PPE is designed to protect users from injuries or illnesses resulting from contact with radiological, chemical, physical, mechanical, electrical or other hazards[3].

11. PPE includes a variety of products, such as traditional work wear, protective clothing, footwear protection, fall protection, hand protection, respiratory protection, head, eye and face protection and hearing protection equipments. The activities of the Parties overlap in the EEA with respect to the supply of all the abovementioned categories of PPE, with the exception of traditional work wear, since Honeywell is not present in this segment in the EEA.

Relevant product markets

12. The Parties submit that the relevant product market for the purposes of the assessment of the proposed transaction could encompass all PPE products. However, they indicate that, from a demand side perspective, there will normally be little or no substitutability between the main categories of PPE products, and that, from a supply side perspective, these categories are generally produced using different materials and production methods (although there may be some overlaps concerning the production equipment). Therefore, the Parties acknowledge that it may be possible to divide the PPE market into product segments, according, notably, to the part of the body the equipment is intended to protect.

13. The Parties have thus identified the following segments as relevant: (i) protective clothing; (ii) footwear protection; (iii) fall protection; (iv) hand protection; (v) respiratory protection; (vi) head, eye and face protection; and (vii) hearing protection equipment.

14. The Commission, in a previous decision, considered that the different categories of PPE products do not constitute a single product market.[4] The Commission furthermore indicated that some of the aforementioned categories may be further subdivided, notably according to the functionalities of the different products and the use made by the final customers.[5] In the following sections the relevant categories of products will be examined in detail.

Footwear protection equipment

15. Foot and leg protection devices include all equipment and/or accessories (whether or not detachable), designed and fabricated specifically to guard the foot and/or the legs, and to facilitate anti-slip protection.

16. In absence of any Commission precedent for this type of products, the Parties submit that safety footwear includes non-metal toe, steel toe, slip-resistant shoes, metatarsal-guard, conductive, dielectric and heat-resistant shoes, shoes resistant to cold environments, chemicals and blood borne pathogens, and fatigue protection shoes. Other safety footwear components include heavy-duty work shoes and boots, hiker-style and casual athletic protective footwear.

17. As the planned operation does not give rise to any affected market in the area of footwear protection equipment whatever the market definition applied, the question of whether the relevant product market is the market for footwear protection equipment or should be further segmented can be left open.

Protective clothing

18. In absence of any Commission precedent for this type of products, the Parties submit that protective clothing includes those garments which protect people against dangerous materials, elements, events or processes encountered during their leisure activities or during the course of their work. Protective clothing also includes highvisibility-clothing, garments intended to safeguard people in the workplace, from certain products or the environment, for example welding clothing or gas-tight suits.

19. As the planned operation does not give rise to any affected market in the area of protective clothing whatever the market definition applied, the question of whether the relevant product market is the market for protective clothing or should be further segmented can be left open.

Fall protection

20. Fall protection equipment includes equipment designed and produced to provide protection against falls from a height. Major product categories include belts, harnesses, kinetic energy absorbers, anchors, connectors, straps, ropes, lanyards, railings, lifelines, and lifting devices.

21. In absence of any Commission precedent for this type of products, the Parties consider that it may be relevant to distinguish within fall protection between individual and collective fall protection equipment. Individual fall protection equipment is aimed at securing an individual whereas collective fall protection is aimed at securing certain sites, for example through the installation of safety nets. The market investigation in the present case largely confirmed the proposed delineation of the Parties, especially in view of the different end users' needs and of the significant price differences between collective and individual fall protection equipment.

22. Ultimately, the question of whether the relevant product market is the market for fall protection or should be differentiated by type of protection device (collective or individual) can however be left open, since the planned operation does not give rise to competition concerns whatever the market definition applied. Honeywell not being active in collective fall protection equipment, the proposed transaction will be assessed on the basis of a potential market for individual fall protection equipment.

Hand protection

23. Hand protection equipment is composed of the equipment and/or accessories (whether detachable or otherwise), designed and fabricated specifically to safeguard the hand and/or the arm. Hand protection encompasses mainly gloves.

24. In absence of any Commission precedent for this type of products, the Parties distinguish between two types of gloves: traditional working gloves and protective or safety gloves. Protective or safety gloves, which are the most relevant products for the assessment of the proposed transaction, are developed for specific work places and vary from the heavy-duty gauntlet to the lightest latex gloves. Protective gloves could be further classified into the following list depending on the usage of the glove:

─ cut resistant gloves (typically knitted or mesh gloves that contain a fibre or metal mesh which prevents cuts from reaching the hand/fingers),

─ cold/heat-resistant gloves (typically knitted gloves that include some type of fibre that will isolate the hand either from extreme heat or cold),

─ liquid and chemical-resistant gloves (dipped gloves that are liquid proof and designed so that they can withstand contact to water, other liquids and potentially one or a range of different chemicals),

─ disposable gloves (these can be dipped or synthetic rubber gloves that are used to provide a thin layer of protection and disposed of after use),

─ specialty protective gloves (this category covers a variety of niche gloves that are designed to meet a specific requirement such as a very strong chemical, or high voltage electricity),

─ consumer gloves (entry-level gloves that are used for cleaning or similar tasks and which offer only a limited level of protection).

25. The market investigation in the present case confirmed the relevance of the proposed delineations of the Parties due notably to different end users needs and to the sometimes significant price differences between different types of protective gloves.

26. Ultimately, the question of whether the relevant product market is the market for hand protection or should be differentiated by type of protection device can however be left open, since the planned operation does not give rise to competition concerns whatever the market definition applied.

Respiratory protection

27. Respiratory protective devices include all respiratory equipment designed and fabricated to provide protection (i) from the atmosphere, (ii) against solid and liquid aerosols or gases and (iii) from viral and microbial infections. The respiratory protection products range from very simple disposable masks to the more sophisticated powered air purifying respiratory masks and self-contained breathing apparatus.

28. In absence of any Commission precedent for this type of products, the Parties submit that, among respiratory products, two main categories could be distinguished: disposable and reusable respiratory protection products.

29. The market investigation in the present case confirmed the relevance of the proposed delineation of the Parties due to different end users needs and to the significant price differences between disposable and reusable respiratory protection equipment.

30. Ultimately, the question of whether the relevant product market is the market for respiratory protection or should be differentiated by type of protection device can however be left open, since the planned operation does not give rise to competition concerns whatever the market definition applied.

Head, eye and face protection

31. Head, eye and face protection is used to protect the user against overhead hazards or from potentially toxic, corrosive, or infectious material. Head protection usually covers safety helmets, while face protection includes products such as medical visors, face shields, or metal mesh visors. Eye protection includes a variety of lens types, in particular safety spectacles and goggles. All these products are used in a variety of industries, such as construction, engineering and manufacturing, oil, gas as well as emergency services.

32. Head, eye and face protection equipments are, according to the notifying Parties, to some extent substitutable and serve a common purpose. The market investigation in the present case showed however that this substitutability is limited. The respondents largely underlined that head protection, on one side, and eye and face protection, on the other side, constitute different segments, arguing notably that these products are subject to different standards and correspond to different end users needs and that there exist significant prices differences between these products.

33. As in the past decisional practice, the question of whether the relevant product market is the market for head, eye and face protection or should be differentiated by type of protection device can however be ultimately left open[6], since the planned operation does not give rise to competition concerns whatever the market definition applied.

Hearing protection

34. Hearing protection devices consist of all equipment (whether worn outside or inside the ear) which protect hearing. Hearing protection devices mainly consist of muffs and plugs and may be disposable or reusable. The Parties consider that since ear plugs and ear muffs serve the same purpose of protection from high noise levels, there is no basis for a distinction between the two. Within the area of ear plugs, the Parties submit that there is also reason to distinct between disposable and reusable ear plugs as those products are fully substitutable and have comparable prices.

35. Within hearing protection, the Commission, in a previous decision[7], distinguished between products which are solely designed to protect the wearer from outside noise ("passive hearing protection products") and those which protect, but in addition are equipped with an electronic unit for communication or entertainment ("active hearing protection") and concluded that they constitute separate product markets.

The Commission based its conclusion, in particular, in that there is no or only

limited demand- or supply-side substitutability between passive and active hearing protective products, that they are used in different working environments and that active hearing protection products are much more expensive.

36. The market investigation in the present case confirmed the relevance of this delineation due to different end users needs and to the significant price differences between active and passive hearing protection equipment.

37. Honeywell not being active in active hearing protection, the proposed transaction will be assessed on the basis of the market for passive hearing protection equipment.

Relevant geographic markets

38. The Parties submit that the relevant geographical scope of the market(s) for PPE devices is EEA-wide. The Parties base their reasoning on the fact that PPE products are subject to an EEA-wide regulatory standard established by the EC Directives on PPE and workplace safety[8] and are therefore identical in all Member States. Furthermore, the Parties consider that these products, for which the suppliers normally have an EEA-wide price list, are typically manufactured from a central site and then distributed throughout the EEA from a central logistics centre without a significant presence in the ground in individual countries. Moreover, these products would be sold to distributors which have both a national and trans-national footprint and which are more and more integrated within European distribution groups.

39. As regards hearing protection and head, eye and face protection devices, the Commission left open in 3M/Aearo whether the relevant geographic market should be defined as EEA-wide or national[9]. The Commission pointed out that the most important suppliers were present across several Member States and that some distributors had multi-framework agreements with suppliers covering several countries based on a European price list. The Commission also observed, however, that prices differed across Member States and suppliers often applied national or regional price lists and that local sales forces and marketing played an important role in this sector.

40. The market investigation conducted by the Commission in the present case has not brought to light any indication that would contradict these earlier findings, with regards to the different categories of PPE products. On the one hand, a significant number of customers explained that prices differ across Member States and that some suppliers are still organized locally and often apply national price lists. Moreover, a significant number of respondents also stressed the importance of a local sales force and marketing as well as of technical and educational assistance which are all adapted by country to the countries, or to the small group of countries, where the products are sold. Most competitors of the Parties have emphasized the existence of different commercial contexts due to historical reasons, in particular as regards branding, packaging, quantities sold on retail and eventually end users preferences.

41. However, on the other hand, a significant number of customers that are active in several Member States indicate that they increasingly source centrally at the EEA level, on the basis of a European price list. The market investigation also showed that transport costs account for less than 5% of the sales price of the respective products, which facilitates their trading. Several customers also pointed out at the existence of EU standards that apply to PPE devices to justify that the markets are EEA-wide. In addition, the most important suppliers at the EEA level are present across various Member States and the competitive advantage, according to the respondents to the market investigation, granted by the ability to provide a wide range of products seem to favour pan European, or at least multi countries players.

42. In any event, the question whether the relevant geographic market for fall protection, hand protection, respiratory protection, head, eye and face protection and hearing protection equipments are EEA-wide or national can be left open in the current case as the planned operation does not give rise to competition concerns whatever the market definition applied.

Competitive assessment

43. Taking into consideration a potential overall market for PPE, the Parties' combined market shares in the EEA in 2009 would be of only [5-10]%, with an increment of [0-5]% brought about by Honeywell. The market for PPE in the EEA is actually quite fragmented, the main competitors of the Parties being 3M (with a market share of [5-10]%), Dragerwerk ([0-5]%), Uvex ([0-5]%), Ansell ([0-5]%), MSA ([0-5]%), Delta Plus ([0-5]%) and Tyco/Scott ([0-5]%), according to the estimates of the Parties. When considering national markets for the overall PPE sector, the combined market shares of the Parties remain below 15% in any country, with normally small increments.

44. However, in line with its 3M/Aearo[10] decision and the results of the market investigation in the present case, the Commission will assess separately the markets for the different families of PPE products (and, eventually, possible alternative further segmentations). In that case, Honeywell's and Sperian's activities will overlap in the following segments: (i) protective clothing (ii) footwear protection (iii) fall protection (iv) hand protection (v) respiratory protection (vi) head, eye and face protection and (vii) hearing protection.

45. The activities of the Parties with regards to PPE are, in any event, generally complementary, both from a product and geographic perspective. Sperian largest sales in the EEA are in the areas of respiratory protection and fall protection equipment, while Honeywell, whose sales in the EEA are more limited, generates most of its EEA-wide turnover from the sales of hand protection equipment.

46. As it will be further explained in more detail in the sub-sections below, the merged entity will, after the transaction, hold market shares of between [10-20]% and [10-20]% on three affected markets in the EEA (individual fall protection, respiratory protection and passive hearing protection; in a potential sub-segmented market for disposable respiratory protection equipment, the Parties would hold a combined market share of [30-40]% and in a potential sub-segmented market for specialty gloves, the Parties would hold a combined market share of [20-30]%), with only very modest increments (between [0-5]% and [0-5]%). At the national level, the transaction would result in affected markets in 13 EU Member States and in Norway, when considering possible sub segmentations of the overall PPE market. In that case, the combined market shares of the Parties would be relatively significant in several markets, but below [40-50]% in any event, with generally small increments.

(i) Individual fall protection

47. Considering an EEA-wide market, the Parties will have a combined market share of [20-30]% in the market for individual fall protection equipment in 2009 (Honeywell: [0-5]%; Sperian: [10-20]%). Other significant market participants are Capital Safety ([10-20]%), as well as an important number of market players with market shares ranging from [0-5]% of the EEA market (such as Tractel, Spanset, Petzl, Bornack, Lachtways and Delta Plus).

48. At the national level, the combined market shares of the Parties would exceed [2030]% and lead to an increment of more than [5-10]% only in Finland in the market for individual fall protection (namely a combined market share of [20-30]% with an increment of [5-10]% brought by Honeywell). The Parties will however continue to face competition of a number of market players including Sujainlaitie, Skylotec and Skydda, which all have a market share of [10-20]% as well as Petzl which has a share estimated at [5-10]% in 2009. Furthermore, the private label suppliers account for over [40-50]% of the market.

49. The transaction will also give rise to the following national affected markets for individual fall protection equipment, with the increment brought by Honeywell being generally very small (below [0-5]% in all markets except for the Netherlands and Belgium): Austria (combined market share of [20-30]%, increment of less than [0-5]%), Belgium ([20-30]%, increment of [0-5]%), Denmark ([20-30]%, increment of [0-5]%), France ([30-40]%, increment of less than [0-5]%), Germany ([20-30]%, increment of [0-5]%), Ireland ([20-30]%, increment of [0-5]%), The Netherlands ([20-30]%, increment of [5-10]%), Portugal ([10-20]%, increment of [0-5]%), Slovakia ([20-30]%, increment of [0-5]%), Slovenia ([30-40]%, increment of [05]%), Sweden ([20-30]%, increment of [0-5]%) and Norway ([30-40]%, increment of [0-5]%). In all these countries, further to the Parties, other established market players are present.

(ii) Hand protection

50. Considering an EEA wide market, the only affected market within hand protection equipment will be a potential market for specialty gloves where the Parties will hold a combined market share of [20-30]% in 2009 (Honeywell: [0-5]%; Sperian: [1020]%). The Parties' competitors in the field of specialty gloves in the EEA are in particular Ansell, Mapa and Marigold with market shares estimated at [20-30]%, [510]% and [5-10]% respectively. Private label suppliers account for over [40-50]% of the EEA market.

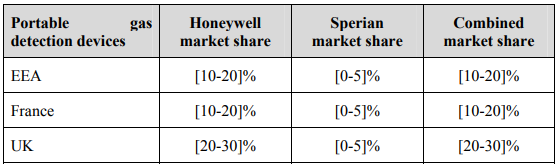

51. At the national level, the combined market shares of the Parties would exceed [2030]% and lead to an increment of more than [5-10]% only in France in a potential market for specialty gloves (combined market share of [30-40]%, increment of [510]% brought by Honeywell). The Parties would continue however to face competition of the following main competitors: Ansell, Marigold, Mapa and Piercan with market shares estimated at [10-20]%, [10-20]%, [10-20]% and [5-10]% respectively. It should also be noted that private label suppliers account for over [2030]% of the French market.

52. The transaction will also give rise to affected markets as regards disposable gloves in Germany (combined market share of [10-20]%, increment of [0-5]% brought by Sperian) as well as regards specialty gloves in Denmark (combined market share of [20-30]%, increment of [5-10]% brought by Sperian) and in Belgium ([10-20]%, increment of [5-10]% brought by Honeywell). In all these countries and segments, further to the Parties, other established market players are present.

(iii) Respiratory protection

53. Considering an EEA wide market, the Parties will have a combined market share of [10-20]% in 2009 in the market for respiratory protection equipment with an increment of [0-5]% brought by Honeywell. The merged entity will face competition of a large number of competitors such as 3M (with a market share of [20-30]%), Dragerwerk AG ([20-30]%), MSA ([10-20]%) and Tyco/Scott ([10-20]%).

54. Under a further segmented product market delineation, the Parties will have a combined market share of [30-40]% at the EEA level in the market for disposable respiratory protection equipment with an increment of [0-5]% brought by Honeywell. 3M will however remain the market leader in the field of disposable respiratory protection equipment with a significantly higher market share estimated at approximately [40-50]%. The Parties’ other main competitors in the field of disposable respiratory equipment are Kimberly Clark, Dragerwerk, Moldex and JSP.

55. At the national level, there would be no market where the combined market shares of the Parties would exceed [20-30]% and lead to an increment of more than [510]% as Honeywell only has very limited activities in that field.

56. In effect, the transaction will only give rise to affected markets as regards overall respiratory protection equipment in France (combined market share of [20-30]%, increment of [0-5]% by Honeywell). Alternatively, it will give rise to affected markets as regards disposable respiratory protection equipment in France (combined market share of [10-20]%, increment of [0-5]% by Honeywell) and United Kingdom ([20-30]%, increment of [0-5]% by Honeywell) and as regards reusable respiratory protection equipment in France (combined market share of [10-20]%, increment of [0-5]% by Honeywell) and Denmark ([10-20]%, increment of [0-5]% by Sperian). In all these countries and segments, further to the Parties, other established market players are present.

(iv) Head, eye and face protection

57. Considering an EEA-wide market, the transaction will not give rise to any affected market in the field of head, eye and face protection whatever the product market definition retained.

58. At the national level, the combined market shares of the Parties would exceed [2030]% and lead to an increment of more than [0-5]% only in Belgium in a potential market for eye and face protection equipment (combined market share of [20-30]%, increment of [10-20]% by Honeywell in 2009). The Parties will continue to face competition of a number of players, such as Uvex, Bollé, Delta Plus and VDP with market shares estimated at [10-20]%, [10-20]%, [5-10]% and [5-10]% respectively. It should also be noted that private label suppliers account for over [20-30]% of the Belgian market.

59. The transaction will also give rise to an affected market on the overall market for head, eye and face protection equipment in the Netherlands (combined market share of [10-20]%, increment of [0-5]% by Sperian). Alternatively, it will give rise to affected markets in the eye and face protection equipment market in the Netherlands ([30-40]%, increment of [0-5]% by Sperian) and in Finland ([10-20]%, increment of [5-10]% by Sperian). In all these countries and segments, further to the Parties, other established market players are present.

(v) Passive hearing protection

60. Considering an EEA wide market, the Parties will have a combined market share of [10-20]% in 2009 in the market for passive hearing protection equipment, with a minimal increment of [0-5]% brought by Honeywell. The market leader will remain 3 M with a market share above [20-30]%.

61. At the national level, there would be no market where the combined market shares of the Parties would exceed [20-30]% and lead to an increment of more than [510]% as Honeywell only has very limited activities in that field.

62. In effect, the transaction will give rise to affected markets in the overall market for hearing protection equipment in Denmark (combined market share of [20-30]%, increment of [0-5]%), Finland ([10-20]%, increment of [0-5]%), Sweden ([10-20]%, increment of [0-5]%), United Kingdom ([20-30]%, increment of [0-5]%) and Norway ([20-30]%, increment of [0-5]%). Alternatively, it will give rise to affected markets in the market for passive hearing protection equipment in Belgium (combined market share of [20-30]%, increment of [0-5]%), Finland ([10-20]%, increment of [0-5]%), The Netherlands ([10-20]%, increment of [5-10]%), Sweden ([10-20]%, increment of [0-5]%) and United Kingdom ([30-40]%, increment of [05]%). In all these countries and segments, further to the Parties, other established market players are present.

Overall assessment

63. Further to the market structure presented in the above sections, the transaction is unlikely to raise any concerns on the markets for fall protection, hand protection, respiratory protection, head, eye and face protection and hearing protection equipments (or any alternative further sub-segmentation thereof) for a number of reasons that apply to all these markets.

64. First of all, as there are strong differences between the two companies Honeywell and Sperian in terms of geographic and product focus, the areas of overlap between the Parties’ activities are limited, so that the proposed Transaction generally gives rise to only small increments at the EEA level or at the national level.

65. Secondly, the merged entity will continue to face competition from a large number of suppliers both at the EEA and at the national levels. Some of the suppliers, such as 3M, Dragerwerk AG, Uvex, Ansell, MSA or Delta Plus, are international companies of a similar size to the Parties and operate in several segments across an important number of countries.

66. Furthermore, the market investigation carried out by the Commission indicated that Honeywell and Sperian are not perceived to be the closest competitors. A significant number of respondents argued when considering all the PPE products together, 3M is the closest competitor to Sperian. This also corresponds to Sperian's market position, being currently the second largest player on a EEA-wide basis for an overall market for PPE products with a [5-10]% market share (3M being currently the leader of the market with a [5-10]% market share).

67. Furthermore, the market investigation showed that PPE products are predominantly distributed via distributors who mostly multisource products from various suppliers, which can facilitate the expansion of the Parties’ competitors. A broad majority of respondents have indicated that barriers to entry and expansion are low and several customers have underlined that they can rely across the EEA on the compliance of all marketed PPE devices with European standards. The market investigation also underlined that transport costs are low and that there are no particular logistic challenges for distribution of PPE devices.

68. Though imports from Asia are still generally low, the market investigation also confirmed the Parties' submission that these imports exert an increasing competitive pressure on the existing suppliers on the market, in particular for the low entry products.

69. Finally, the vast majority of respondents to the market investigation, both competitors and customers, have not expressed any substantiated concerns as regards as regards the competitive effects of the proposed transaction.

70. Based on the above, the Commission has concluded that the proposed transaction does not raise competition concerns on any market for fall protection, hand protection, respiratory protection, head, eye and face protection and hearing protection equipments or any alternative sub-segmentation thereof.

B. PORTABLE GAS DETECTION DEVICES

Relevant product markets

71. Gas detection devices are used to monitor the concentration of toxic or flammable gases in order to warn about possible hazards of intoxication, suffocation or explosion in a variety of situations. The purpose is either to protect people or to protect property.

72. The Parties consider that it is appropriate to distinguish between fixed gas detection devices and portable gas detection devices, Sperian being in any event only active in the field of portable gas detection devices. According to the Parties, there is no need for a further sub-segmentation depending on the technology used in the detectors.

73. Portable gas detectors are self-contained units which sense gases and show on the unit itself the result of the monitoring. The portable gas detection units are designed to be easily moved around, usually worn on a person outside their breathing zone. Portable gas detectors are often designed to detect multiple gases such as CO, Oxygen, Hydrogen Sulphide and flammable gases at the same time.

74. The market investigation widely confirmed that both competitors as well as customers consider that a segmentation should be made between portable and fixed gas detection devices, primarily because of different sizes and weight and their respective applications, since portable gas detection devices have to be – contrary to fixed devices - worn on-person. Customers do not switch between these devices. Some respondents suggested a further sub-segmentation, either according to different technologies, or distinguishing measuring and alarm devices or single- versus multi-gas detection devices, but the results of the market investigation were not conclusive in that regard. Furthermore, some devices combine several technologies or functionalities. Finally, no specific concerns were raised with regard to a particular sub-segment or sub-segments.

75. In any event, since the transaction does not raise competition concerns under any alternative market definition in this sector, the precise product market delineation may ultimately be left open.

Relevant geographical market

76. The Parties submit that the market for gas detection devices is EEA-wide, because the products supplied throughout the EEA are identical from a technology point and there are no regional differences or preferences[11]. Suppliers are also able to serve customers throughout the EEA from one or a few locations.

77. The market investigation largely confirmed that competitors and customers consider the market for portable gas detection devices as at least EEA-wide. Some respondents considered however a narrower than EEA-wide market, based on purchases from local distributors and the existence of price or regulatory differences between countries, although this does not seem to deter them from cross-border selling or sourcing.

78. In any event, since the transaction does not raise competition concerns under any alternative geographical market definition, the precise delineation may ultimately be left open.

Competitive assessment

79. Since Honeywell's and Sperian's activities overlap only in the field of portable gas detection devices, the assessment of the proposed transaction will be limited to this category of products.

80. The Parties submit that given Sperian's minimal activities in the field of portable gas detection devices, the competitive landscape would remain unchanged further to the proposed transaction. Customers could, according to the Parties, easily switch from one supplier to the other, and the large number of suppliers makes the market very competitive.

81. Honeywell manufactures a broad range of portable gas detectors. According to the Parties, its sales accounted for a share of approximately [10-20]% of the EEA market. Sperian is a small player with limited activities in this field. In 2009, Sperian’s sales accounted for a share of approximately [0-5]% of the EEA market.

82. If a narrower (i.e. nationwide) geographic market definition was taken into account, this would lead to only two affected national markets, namely France ([10-20]% combined market share) and UK ([20-30]% combined market share). In these countries, the increments in market share brought about by the transaction ([0-5]% in France and [0-5]% in the UK, respectively) will also be small.

83. The strongest competitors of the Parties in the EEA are Drägerwerk, with an estimated [30-40]% market share, MSA with [10-20]%, GFG with [5-10]% and Crowcon with [5-10]%. Thus, even post-transaction Drägerwerk would still be the market leader and MSA would still hold a similar market position to that of the Parties. These competitors are generally active as well in France and the UK.

84. The market investigation largely confirmed the competitive structure of the market. Nearly all respondents see alternative suppliers in the EEA-wide market as well as in France and the UK, such as Drägerwerk, MSA and ISC/Oldham, with estimated market shares similar to that of the merged entity in the EEA as well as in France and the UK. Several respondents also mentioned new entries from Far East as well as from Brazil, the US and Canada.

85. Furthermore, the market investigation generally revealed no specific concerns with regard to the proposed transaction's effects on the market for portable gas detection devices.

86. In the light of this, the proposed transaction does not give rise to competition concerns in the field of portable gas detection devices.

C. GAS DETECTION SENSORS

Relevant product and geographic market

87. The manufacturing and supply of gas detection sensors constitutes an upstream market for the manufacture of gas detection devices.

88. A gas detection sensor is the core unit of a gas detection device. It detects gases mostly by using electrochemical sensing, combined with a catalytic bead. They generate an electrical signal when gases react on specially prepared surfaces. Gas detection sensors are produced by independent manufacturers that supply to producers of gas detection devices, or by vertically integrated manufacturers of gas detection devices, which use internally part of their production of sensors to manufacture their own gas detection devices and also sell these sensors to third party producers of gas detection devices.

89. The Parties submit that the market for gas detection sensors could be considered worldwide, since suppliers of these generally operate out of one or a few plants which are used to serve customers throughout the world. There are many suppliers located in the EEA, but also in the Far East. The market investigation confirmed that sensor producers supply worldwide and that the manufacturers of gas protection devices source gas sensors at least at the EEA level.

90. For the purposes of the assessment of the proposed transaction, in any event, the precise product and geographic market definition may ultimately be left open.

Competitive assessment

91. Honeywell is active in the production of gas sensors, some of which are supplied to other gas detection manufacturers. Sperian, in turn, does not produce or sell gas sensors. Therefore, the transaction does not give rise to horizontal overlaps with regards to gas sensors. The proposed transaction gives rise, however, to vertically affected markets in the EEA in relation to portable gas detection devices, where both Parties are active, and the upstream activity of the supply of gas detection sensors for use in gas detection equipment, given Honeywell activities in this segment.

92. Honeywell is active in the manufacture of gas sensors, with a share of [30-40]% of the market in the EEA in 2009 and of [40-50]% in the EEA merchant market (i.e. without captive sales). Other important suppliers are Alphasense, Figaro and Nemoto, with estimated market shares in the merchant market of between about [510] and [5-10]%.

93. The Parties submit however that this vertical link is unlikely to give rise to competition concerns in the light of the low value of Sperian's purchases of gas sensors and the low market share of Sperian's downstream business in the gas detection devices market.

94. In effect, Sperian has very limited activities in the supply of gas detection devices, since it is only present in the sector of portable gas detection devices, with a market share in this segment of [0-5]% in the EEA in 2009. Sperian's purchases of gas detection sensors are estimated to be below [0-5]% of the total purchases in the merchant market of these sensors both worldwide and in the EEA in 2009. Thus, the proposed transaction is not likely to lead to any risk of customer or input foreclosure, since only a very small share of the demand side for gas detection sensors gets vertically integrated by the proposed transaction.

95. Therefore, for the abovementioned reasons, the proposed transaction does not give rise to competition concerns in the field of gas detection sensors.

V. CONCLUSION

96. In light of the above, the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market and the functioning of the EEA Agreement.

97. The European Commission thus has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 Turnover calculated in accordance with Article 5(1) of the EU Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C95, 16.04.2008, p1).

3 Case COMP/M.5012 3M/Aearo of 28 March 2008

4 Case COMP/M.5012 3M/Aearo of 28 March 2008. The Commission distinguished, in particular, between hearing protection devices and head, eye and face protection.

5 In particular, the Commission considered in Case COMP/M.5012 3M/Aearo that, within the family of hearing protection devices, active hearing protection products and passive hearing protection products constitute separate product markets

6 Case COMP/M.5012 3M/Aearo of 28 March 2008.

7 Case COMP/M.5012

8 Directive 89/686/EEC of December 21, 1989, on the approximation of the laws of the Member Sates relating to personal protective equipment; Directive 2003/10/EC of February 6, 2003, on the minimum health and safety requirements regarding the exposure of workers to the risks arising from physical agents (noise).

9 Case COMP/M.5012 3M/Aearo of 28 March 2008.

10 Case COMP/M.5012 3M/Aearo of 28 March 2008.

11 The Parties submit that the only regulatory requirement in the EEA is based on an EU-wide EN standard.