Commission, October 28, 2010, No M.5939

EUROPEAN COMMISSION

Judgment

VEOLIA WATER UK AND VEOLIA VODA / SUBSIDIARIES OF UNITED UTILITIES GROUP

Dear Sir/Madam,

Subject: COMP/M.5934 – VEOLIA WATER UK AND VEOLIA VODA / SUBSIDIARIES OF UNITED UTILITIES GROUP Notification of 23 September 2010 pursuant to Article 4 of Council Regulation No 139/2004[1]

1. On 23.09.2010, the European Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004[2] by which Veolia Water UK Plc ("VWUK", UK) and Veolia Voda SA ("VV", Czech Republic) both ultimately controlled by Veolia Environment SA ("VE", France) acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of certain businesses of United Utilities Group PLC ("the Target Business", UK) in UK by way of purchase of shares. In addition, VE Group will acquire shareholdings of the Target Business in water operating concessions in Bulgaria, Estonia and Poland.

I. THE PARTIES

2. VE Group is a global provider of environmental management services, divided into four operating segments as follows: a waste services division, an energy services division, a transportation division and a water division.

3. VWUK is the VE Group entity which provides water and wastewater infrastructure and services in the UK and Ireland, including services outsourced to it by other infrastructure providers and similar services to industrial and commercial customers, as well as utility connection services.

4. VV is the part of the VE Group which, through a number of subsidiary companies, is active in providing water and wastewater managementin Central and Eastern Europe.

5. The Target Business is active in the provision of outsourced water and wastewater management services to regulated water and wastewater companies and industrial customers in UK and utility connections in UK. In Bulgaria, Poland and Estonia it has interests in companies operating concessions for the municipal supply of water and wastewater services.

II. THE OPERATION AND THE CONCENTRATION

6. As a result of the proposed transaction VWUK will acquire sole control of certain businesses of the Target Business engaged in supplying outsourced contracting services and utility connections in the UK. Pursuant to a back to back agreement between VWUK and VV, the latter will acquire all the issued share capital in United Utilities (Poland) BV, 50% of the issued share capital of United Utilities Europe Holdings BV and 50% of the issued share capital of United Utilities (Sofia) BV.

7. Based on the above, the operation constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

III. EU DIMENSION

8. The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5,000 million (VE Group: EUR 34,551 million, Target Business: EUR 355.5 million, in 2009). Moreover, the aggregate EU-wide of both undertakings is more than EUR 250 million (VE Group: EUR […], Target business: EUR […]). […]. Target Business achieves more than two-thirds of its aggregate EU-wide turnover in the United Kingdom. Thus, the proposed transaction has an EU dimension in the meaning of article 1(2) of the Merger Regulation, and falls into its scope.

IV. RELEVANT MARKETS

9. The proposed transaction involves the following markets where both parties to the concentration operate: (i) operation and maintenance ("O&M") of water and wastewater treatment facilities and (ii) design, construction and management of water and wastewater facilities for UK regulated water companies.

10. The proposed transaction also gives rise to two vertical relationships. The first one occurs between (i) the upstream market for design and construction of technological solutions and equipments for water and wastewater treatment systems for municipal customers and (ii) the downstream market for the provision of outsourced O&M services for water and wastewater facilities to regulated water companies (if considered as a separate product market). The second one occurs between (iii) the upstream market for the provision of outsourced O&M services for water and wastewater facilities to regulated water companies and (iv) the downstream market for the provision of water and sewerage services to businesses and individuals in the UK by regulated water companies.

Relevant product markets

A Provision of outsourced O&M services and design, construction and management services of water and wastewater facilities to regulated water companies and to industrial customers

11. The provision of outsourced O&M services and design, construction and management services of water and wastewater facilities can either be done by the holder of the facility (regulated water company or industrial/commercial undertaking) or outsourced to third parties. In respect of the proposed transaction, only the outsourcing market will be considered since competition issues can only arise in this area.

12. In a recent decision the Commission has considered a market for design, engineering and construction of water and wastewater treatment systems, analysing the possibility of including therein the market for O&M without however concluding on this point[3].

13. The parties claim that the manner of contracting in the UK does not reflect a clear distinction between design and construction projects on one hand and operation and maintenance projects on the other hand. Both water regulated companies[4] and industrial/commercial customers would contract either design and construction services separately with respect to O&M services or both services, depending on the object of each individual contract for outsourced infrastructure services. The parties, therefore, claim that there is a continuum of services, from construction and maintenance through O&M services in the UK. Conversely, there are a large number of suppliers who are able to provide some or all of the services, from planning, design and consulting, through to engineering, construction and programme management and operation and maintenance. Although each company may specialise in providing particular services, they compete with each other to varying degrees across the whole spectrum of infrastructure services. Thus, it would not be accurate to draw a line along this spectrum from the supply side perspective.

14. The majority of the respondents to the market investigation expressed the view that design and construction management should be separated from operation and maintenance services. O&M has a cyclical nature while design and construction, which is capital funded, is performed on a project by project basis. In addition, the skills required in the two types of services are different; O&M is labour intensive and demands local presence while design and construction requires high professional skills which can be supplied centrally and remotely. Procurement practices also are different.

The procurement of the O&M usually results in a smaller number of respondents who

are not the same as for the design and construction although there may be some companies that compete for both.

15. Moreover, according to the parties, regulated water companies outsource approximately [80-90]% of their design and construction services and only [10-20]% of their O&M needs, which is in line with to the findings of the market investigation.

16. Therefore, taking into consideration past decisions and the results of the current market investigation, it appears that the most plausible alternative would be to analyse separately the market for the design and construction management on one hand and operation and maintenance services on the other hand.

17. A further segmentation of the O&M and design and construction markets can be made according to the recipients of the service, namely regulated companies and commercial/industrial customers. Additionally, a sub-segmentation of these markets can be done in water and wastewater services.

18. However, the precise definition of the product market can be left open, as under any delineation, effective competition would not be significantly impeded

A.1. Provision of outsourced O&M services to regulated water companies and to industrial customers

19. The Commission has already considered a market for O&M of water and wastewater treatment facilities[5].

A.1.1 A possible separation of the market according to the recipients of the service

20. In the same decision[6] the Commission has analysed a possible distinction between the recipients of the services provided, namely municipal companies and industrial customers without concluding on this point. The parties claim that the services provided to the two categories of customers should belong to different product markets. They argue that: (i) regulated water companies treat larger volumes of water than commercial customers and (ii) services are contracted by regulated water companies in a tendering market subject to EU public procurement rules while the services contracted by industrial customers follow different procedures. In addition, the tendering process by regulated water companies in the UK follows a five year price control period[7].

21. The majority of competitors replying to the market investigation considered that O&M services should be divided according to the recipients of the service. Some of them were of the opinion that industrial wastewater has a larger range of water quality and requires more complex operation and treatment processes. Moreover, while industrial customers may request higher quality for water treatment, for regulated water companies pathogen removal is critical which requires different treatment processes and operation.

22. However, customers had a different view, the majority of them considering that there is one market for O&M irrespective of the service recipient. Customers claimed that, while the requirements of industrial and commercial customers are likely to be smaller in scale, O&M skills required and the services provided are the same for regulated water and sewerage companies as for industrial/commercial customers.

23. In any case, there is no need to conclude on this point, since under any alternative market definition there will be no competition concerns.

A1.1.1. A possible division of the market in water and wastewater treatment

24. In COMP/M.5724 – Suez Environnement/AGBAR[8] the Commission has analysed this possibility in connection with the market for O&M, without concluding thereon. The parties claim that the product market should not be further segmented giving that water and sewerage companies outsource the largest projects on a combined water and wastewater programme basis.

25. The vast majority of respondents indicated that water and wastewater treatment facilities include both plants used to treat water and wastewater. However, the overwhelming majority of respondents replied that contracts for O&M services are not always awarded for both water and wastewater facilities.

26. In addition, the vast majority of respondents replied that water and wastewater treatment facilities are located at different sites. Industrial customers usually have water and wastewater infrastructures located on the same site. For regulated companies, water and wastewater facilities are separate and are usually located large distances away from each other as they are usually designed in the way that the water treatment facility is at the beginning, while the wastewater facility is at the end, of the network system.

27. However, there is no need to conclude on the product market definition, since under any plausible market definition there will be no competition concerns.

A.2. Provision of outsourced O&M services and design, construction and management services of water and wastewater facilities to regulated water companies and to industrial customers

28. As mentioned in paragraph 10, in COMP/M.5724 – Suez Environnement/AGBAR[9], the Commission has considered a market for design, engineering and construction of water and wastewater treatment systems.

A.2.1. A possible separation of the market according to the recipients of the service

29. In the same decision[10] the Commission has analysed a possible distinction between the recipients of the services provided, namely municipal companies and industrial customers, without concluding on this point. As mentioned in paragraph 18, the parties submit that the services provided to the two categories of customers should belong to different product markets. The requirements of industrial/commercial customers are likely to be smaller in scale. In addition, a regulated company usually is subject to long term fixed assets returns while industrial/commercial customers face higher earnings volatility; therefore the contracting characteristics of the two sectors are likely to be different.

30. Notwithstanding the above, there is no need to conclude on this point, since under any alternative market definition there will be no competition concerns.

A2.1.1. A possible division of the market in water and wastewater treatment

31. The parties claim that the product market should not be further segmented given that water and sewerage companies outsource the largest projects on a combined water and wastewater programme basis.

32. The vast majority of the respondents to the market investigation indicated that outsourced services for design and construction management should be separated between water and wastewater treatment services. One of the reasons mentioned was that UK regulated water and wastewater companies have separate design and construction framework contracts for water and wastewater. In addition, the majority of respondents replied that water and wastewater treatment facilities are located at different sites; water treatment facilities are situated at the upper end of watersheds and wastewater treatment services are at the lower end of watersheds. Moreover, water treatment is performed separately from wastewater in order to avoid contamination.

33. In any event, there is no need to conclude on the product market definition, since under any plausible market definition there will be no competition concerns.

Conclusion

34. For the purpose of this decision there is no need to decide whether O&M and design and construction management services should be segmented further according to the recipient of the service or if there should a further segmentation of these markets in water and wastewater services. Under any alternative delineation there will be no competition concerns.

Relevant geographic markets

B.1. Provision of outsourced O&M services of water and wastewater facilities to regulated water companies and to industrial customers

35. In COMP/M.5724 – Suez Environnement/AGBAR the Commission indicated that the O&M market should be at least national in scope[11].

36. The notifying party submits that the relevant geographic markets for both O&M and design and construction services should be EEA-wide for both water regulated companies and commercial and industrial customers. Regarding the first group of customers, VE submits that (i) all contracts within the EU are let following tendering and there is no significant difference in the types of services provided by the suppliers of water and wastewater services throughout the EEA and (ii) there are several companies operating in the EEA that have the same resources and expertise as the parties.

37. Concerning the commercial and industrial market, the notifying party argues that (i) there is no significant difference in the types of services required by industrial and commercial customers throughout the EEA and (ii) it would be relatively inexpensive and easy for a foreign company with expertise in the water sector to win contracts in the UK.

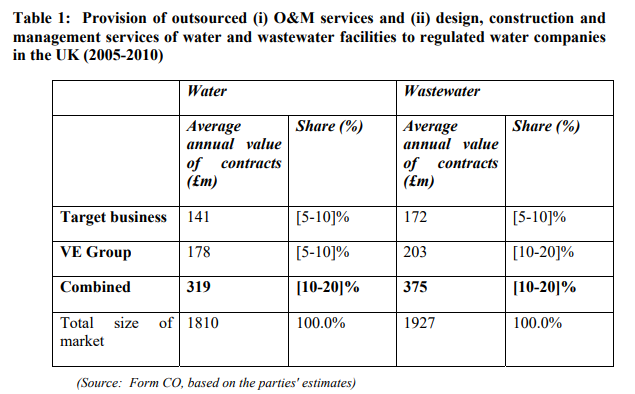

38. The majority of respondents replying to the market investigation considered that the geographic scope of the O&M market should be national. Some respondents indicated that, although there are European players active in this market, a local presence and knowledge of the UK industry is essential. In addition, some mentioned the existence of different national standards and regulatory requirements. Also, the municipal O&M market varies largely across EEA with respect to the extent of which companies outsource services. Finally, the majority of the respondents mentioned that companies generally bid for O&M contracts on a national basis.

39. Therefore the geographic scope of the O&M market is most likely to be national. However, the exact definition can be left open, since under any alternative market definition there will be no competition concerns.

B.2. Provision of outsourced design, construction management services of water and wastewater facilities to regulated water companies and to industrial customers

40. In COMP/M.5724 – Suez Environnement/AGBAR the Commission did not conclude on the geographic scope of the market for design, engineering and construction of water and wastewater treatment systems[12].

41. As mentioned in paragraph 36, the notifying party submits that the relevant geographic markets should be EEA-wide for both regulated water companies and industrial/commercial customers.

42. The majority of respondents to the market investigation expressed the view that the market should be national, for both regulated companies and industrial/commercial customers. In this regards, the respondents mentioned the existence of specific national standards, the need of having a good reputation and knowledge of local practices.

43. Moreover, even those respondents which were in favour of an EEA wide market stated that, in order to provide construction services in UK companies need local staff and a good knowledge of country specific standards and regulations.

44. Therefore, also in this case the geographic scope of the market is likely to be national, the exact definition will be, however, left open since at a level as narrow as national there are no competition concerns.

C. Provision of water and sewerage services to businesses and individuals in the UK by regulated water companies

Relevant product market

45. Commission precedents divided the management of potable water into (i) municipal supply and treatment of potable water; and (ii) municipal wastewater collection and treatment[13]. The notifying party submits that such a sub-division is not appropriate in the UK, given that many regulated companies (i.e. 10) are licensed to provide both water and wastewater services and it is not possible to be licensed to provide wastewater services alone.

46. In any event, it is not necessary to conclude on this issue as the proposed transaction would not raise competition concerns under any alternative market delineation.

Relevant geographic market

47. Previous decisions of the Commission generally take the view that the relevant market(s) are national in scope[14]. In COMP/ M.567-Lyonnaise des Eaux/Northumbrian Water[15], the Commission considered that the geographic market may be England and Wales, but did not conclude on this point. The notifying party submits that the market should be considered national in scope. It claims that it would not be appropriate to subdivide England and Wales, Scotland and Northern Ireland into separate geographic markets.

48. However, the exact scope of the market can be left open since under any alternative definition, the proposed transaction would not raise competition concerns.

D. Design and construction of technological solutions and equipment for water and wastewater treatment for municipal customers

Relevant product market

49. The technological solutions and equipment for water and wastewater treatment for use by municipal customers include the production of “engineered solutions”. These are large pieces of water and wastewater treatment equipments which are designed and built off-site and subsequently incorporated into the water treatment plant.

50. In M.1514 Vivendi / US Filters the Commission has analysed if this market should be divided into systems for industrial purposes and systems for municipalities but left the market definition open.

51. The notifying party considers the product market should be divided into design and construction of technological solutions and equipment for water and wastewater treatment for municipal customers on one hand, and the provision of the said services to industrial customers on the other hand.

52. In the same decision[16], the Commission considered that further distinctions could be made between water treatment systems and waste water treatment systems or between the various types of water and waste water treatment systems (e.g. membrane treatments, biological treatments etc.). However, it left the exact definition of the product market(s) for water and waste water treatment systems open.

53. In this case also the precise product market definition can be left open since under any alternative market definition(s), the operation does not raise competitive concerns.

Relevant geographic market

54. The notifying party, in line with the Commission findings in Vivendi/US Filters[17], considers that the market for design and construction of technological solutions and equipment for water and wastewater treatment for municipal customers is at least EEAwide. In support of its claim, it submits that many of its UK-based competitors active in this market provide services outside the UK and there are non-UK companies providing these services within the UK (some with UK bases or interests, some without).

55. However, there is no need to conclude on the geographic market definition, since under any alternative market definition there will be no competition concerns.

V. COMPETITIVE ASSESSMENT

56. The parties combined market share would be above 15% on a wider market for (i) O&M of water and wastewater treatment facilities and (ii) design, construction and management of water and wastewater facilities for UK regulated water companies within the price control period 2005-2010. The same holds true considering the two types of services as constituting two separate product markets. To the opposite, the above markets are not considered as affected within the current price control period 2010-2015 as the parties' combined market share would be below 15% under any envisageable market definition.

57. The same consideration applies in relation to the market for (i) O&M of water and wastewater treatment facilities and (ii) design, construction and management of water and wastewater facilities for industrial customers in UK as the parties' market shares would not approach 15% under any alternative product market definition.

58. Finally, the transaction gives raise to two minor vertical relationships. The first occurs, between (i) the upstream market for design and construction of technological solutions and equipments for water and wastewater treatment systems for municipal customers, where VE group operates and (ii) the downstream market for the provision of outsourced O&M services for water and wastewater facilities to regulated water companies, should this market be considered as a separate product market. The second occurs between (iii) the upstream market for the provision of outsourced O&M services for water and wastewater facilities to regulated water companies and (iv) the downstream market for the provision of water and sewerage services to businesses and individuals in the UK by regulated water companies.

Horizontal overlaps

Provision of outsourced (i) O&M services and (ii) design, construction and management services of water and wastewater facilities to regulated water companies

59. On a wider market encompassing both the provision of outsourced (i) O&M services and (ii) design, construction and management services of water and wastewater facilities to regulated water companies in the UK, the parties' combined market share would not approach 15% in the current price control period 2010-2015. The same applies considering O&M services as belonging to a separate market, as opposed to design, construction and management, as confirmed by most of the respondents to the market investigation. Therefore, the transaction would not give rise to affected markets.

60. To the opposite, taking into account the past price control period (2005-2010), the parties' combined market shares would exceed 15%, as displayed below[18].

61. The notifying party argues that the above market shares are only historical and in any event of limited relevance due to the bidding nature of the market. Between the periods of bidding (as explained in recital 20 generally every five years) the market can change considerably, with new undertakings entering the market and others exiting the market. Additionally, there is no guarantee that contractors that won projects in the previous price control period will be chosen again when competing in a new tender. An example in this regards, the fact that […] had limited contracts with […] within the past price control period 2005 – 2010 but won a substantive tranche of work from […] for the 2010 – 2015 price control period. Analogous event regards […], a major framework partner to […] in 2005 – 2010 which lost all of its framework agreements with […] for the period 2010 - 2015.

62. By analogy, the contracts available for tender from the UK regulated water companies change in scope from one price control period to another. Thus, regulated water companies may choose to bring some activities in-house or to outsource additional contracts. In this respect the parties submit that […].

63. Based on the foregoing, the parties believe their estimated market shares for the past price control period (2005-2010) cannot be considered as faithful indicators of long term market power.

64. In any event, the parties stress that there are numerous players competing with them for the provision of different types of services (either separately for O&M and design and construction of water and wastewater treatment facilities or for both services), as proved by the fact that out of the 42 capital expenditure contracts awarded during the round of tenders associated with the current price control period only […] have been won by VE and the Target Business.

65. In particular, they submit that the following suppliers, inter alia, will exert competitive pressure on them post-transaction, namely, Ondeo, Weir, Balfour Beatty, Morgan Sindall, Galliford Try, Kelda Water Service, Black&Veatch, Regulated Water Companies, May Gurney, Costain, Biwater.

66. The parties submit that, although some companies specialise in providing a particular service, they compete with each other to varying degrees across the whole spectrum of design, construction and O&M services. Indeed, several competitors who replied to the market investigation confirmed that they would be able to provide both O&M and design and construction services (depending on the customer's needs) either with their own resources or subcontracting some services to specialised third parties. This practice appears to be common to this sector.

67. Furthermore, the parties maintain that an aspect of the UK regulatory framework that enhance competition in the market is the obligation on the regulated water companies to procure services competitively and efficiently through bidding processes governed by EU public procurement rules. As a consequence, any outsourced work which is carried out by an unregulated associate company is subject to market test before being realised as provided by the regulatory accounting guidelines on transfer pricing, RAG 5.

68. Additionally, the parties submit that there is no incumbent advantage when companies bid for contracts in this market and that generally contracts are not renegotiated after having been awarded. Although there are occasions where the same or similar groups of suppliers may win a further contract with the same customer, the supplier would have to submit the most competitive bid in order to be successful. In fact, as fully confirmed by most of the respondents to the market investigation, the overall market for outsourced services to regulated water companies is essentially price driven and highly cost conscious.

69. The market investigation corroborated the above arguments. In particular, the majority of respondents submitted that regulated water companies have bargaining power vis-àvis their service providers both in relation to the provision of O&M services as well as design and construction services.

70. With respect to the provision of O&M services, it results from the market investigation that regulated water companies mainly carry out internally O&M activities. Therefore, they have always the option to internalise again an outsourced activity if they consider that this would result in costs savings. In this regards, the majority of the customers interviewed confirmed that although there might be some difficulties to bring back in house outsourced O&M activities (such as the transfer of systems, data and maintenance records), those are not considered as significant barriers and in any case may all be mitigated by transition arrangements to be negotiated with the former supplier. A recent example in this respect, broadly highlighted by the market investigation, involves […].

71. In relation to the submarket for design and construction services, the majority of respondents confirmed that there are numerous players and that competition is high. Moreover, one of the suppliers underlined that regulated water companies are among the largest clients of providers of design and construction services which fiercely compete to be awarded with the large multi-year capital expenditure programmes, generally tendered every 5 years. As a consequence, water companies have a certain degree of buyer power when choosing among the different services offered by the suppliers.

72. To conclude, the market investigation showed that the UK market for the provision of O&M and design and construction services to regulated water companies is sufficiently competitive. This is also due to the presence of consortia among market players which allow smaller providers as well as foreign companies to compete against the best established competitors. Finally, although some of the respondents stated that suppliers of O&M services are comparatively fewer than those providing design and construction services, most of the respondents equally confirmed that post-transaction there will remain enough players in the UK and that the transaction will have no or limited impact on their businesses. Additionally, some respondents underlined that the increased need to save costs and comply with technical regulations might create opportunities for growth of the outsourced market in the future.

73. In light of the above arguments, it can be concluded that the transaction does not raise serious doubts with respect to both the provision of outsourced (i) O&M services and (ii) design, construction and management services of water and wastewater facilities to regulated water companies in the UK. The same conclusion applies if the market were to be considered as EEA wide, since the increment due to the transaction would be negligible under any alternative market delineation.

Provision of outsourced (i) O&M services and (ii) design, construction and management services of water and wastewater facilities to industrial customers

74. On the market for the provision of (i) O&M and (ii) design, construction and management services of water and wastewater facilities to industrial customers in the UK, the parties combined market shares would not reach 15% under any envisageable product market definition for the years 2009-2010. The parties submit that their main competitors are Ondeo, Alpheus (Anglian Water), Severn Trent, Kelda, which are considered to have analogous market position as the parties, as well as many other players.

75. In this respect, the parties stressed that there are no authoritative public sources from which their market shares figures can be exactly calculated as contrary to the regulated water companies, industrial customers are not obliged to offer contracts through regular tender procedures and even in that case, the market is not transparent. Also the market investigation confirmed the parties' arguments as to the difficulty in reconstructing the outsourced market for industrial customers since the customers' base is very fragmented and the types of contracts used by clients vary to a large extent depending on their needs.

76. However, as it will be explained below, it resulted from the replies to the market investigation that no competition concerns would arise from the proposed transaction.

77. First, it emerged from the replies of the respondents that the outsourced market has a potential to grow and that the customer's base is potentially wide. This is in particular the case as industrial customers call for solutions which allow them to reduce the costs of connecting to the public water and wastewater facilities and to charge the provider of outsourced services with the risk on non-compliance with the strict rules of the environment agency. As a consequence, suppliers tend to compete along the whole spectrum of infrastructures services with a view to offer targeted solutions to their customers specific needs.

78. The majority of respondents confirmed that industrial customers have a certain degree of bargaining power vis-à-vis their providers (of either O&M or design and construction services) as they generally have procurement professionals which ensure that only the most cost beneficial propositions are accepted.

79. In any event, as pointed out by the parties and confirmed by the market investigation, industrial customers have always the alternative option to use the water and wastewater network belonging to the local regulated water companies if they consider this solution to be more beneficial. As a result, the incumbent regulated water company acts as a direct competitive constraint with respect to the providers of outsourced services.

80. Finally, some respondents to the market investigation pointed out that the companies offering O&M services to industrial customers are comparatively fewer than those offering design and construction services as these services are still predominately carried out by the local regulated suppliers. Despite this, the majority of respondents equally confirmed that there are sufficient providers competing for the provision of both types of services. Additionally, one competitor stressed that, should more opportunities arise in this market segment, there would be a number of companies willing to enter the market.

81. It follows from the foregoing that the proposed transaction does not impede effective competition into the internal market with respect to the provision of outsourced O&M services and design, construction and management services of water and wastewater facilities to industrial customers.

Vertical relationship

Design and construction of technological solutions and equipment for water and wastewater treatment for municipal customers/ Provision of outsourced O&M services for water and wastewater facilities to regulated water companies

82. Veolia Water Solution and Technologies ("VWS"), a wholly owned subsidiary of VE group, designs, builds and install technological solutions and equipments for water and wastewater treatment for use by water companies. VWS generally provides such services as subcontractor to suppliers of outsourced services to regulated water companies; as a consequence, it acts as a supplier of a vertically related input for the execution of the capital programme contracted by the providers of outsourced services (such as VWUK and the Target Business ) with the regulated water companies.

83. On the upstream market for design and construction of technological solutions and equipment for water and wastewater treatments for municipal customers, VE estimates its market share (in value) to be below [10-20]% in the EEA. Its main competitors would be Degremont Suez ([5-10]%), Stereau ([0-5]%) and Stulz ([0-5]%), among others.

84. On a national basis, VE estimates that its market share has not reached [0-5]% in the last three years. The main players in UK are Black & Veatch with approximately [5-10]%, Biwater with approximately [5-10]% and Enpure with approximately [0-5]% among many others.

85. On none of the narrowest possible product market definitions, namely, separate submarkets for (i) installations and (ii) components, (iii) water treatment systems and (iv) wastewater treatment systems or between (v) the various types of water and waste water treatment systems (e.g. membrane treatments, biological treatments etc.) VE market share would be above 15% both in the EEA and in the UK.

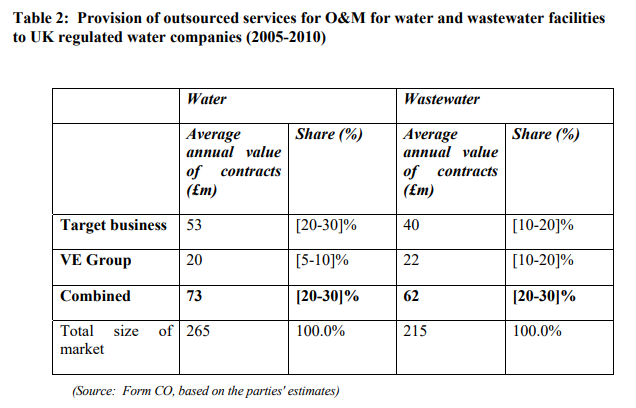

86. On the downstream market for the provision of outsourced O&M services for water and wastewater facilities to regulated water companies, the parties' combined market shares would not approach [30-40]% under any alternative segmentation, as displayed at table 2. Moreover, a number of companies and especially regulated water companies are present on this market as explained at recital 64.

87. If follows from the foregoing that due to the limited market presence of VE group on the upstream market for design and construction of technological solutions and equipments for water and wastewater treatments for municipal customers as well as of the merged entity on the downstream market for the provision of outsourced O&M services for water and wastewater facilities to regulated water companies, the parties would not have the ability to foreclose their competitors.

88. Based on the above it can be concluded that the proposed transaction does not impede effective competition into the internal market as regards the above vertically related markets.

Provision of outsourced O&M services for water and wastewater facilities to regulated water companies/Provision of water and sewerage services to businesses and individuals in the UK by regulated water companies

89. On the upstream market for the provision of outsourced O&M services for water and wastewater facilities to regulated water companies, the parties' combined market shares would be below [30-40]% under any alternative market definition, as displayed at table 2. Moreover, a number of companies and especially regulated water companies are present on this market as explained at recital 64.

90. VE group operates on the downstream market for the provision of water and sewerage services through its 3 regulated water companies out of a total of 11 regulated water only companies and 10 regulated water and sewerage companies in England and Wales.

91. On this market, VE group market share is below 15%[19] either considering together water and wastewater services in England and Wales (VE group is not active in Scotland and Northern Ireland) or singling out (i) water supply services and (ii) waste water services.

92. It follows from the foregoing that the transaction would not give rise to any input or costumer foreclosure strategy due to the limited market presence of the merged entity on both vertically related markets.

93. Based on the above, it can be concluded that the proposed transaction does not impede effective competition into the internal market regarding the above vertically related markets.

VI. CONCLUSION

94. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

[1] OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 OJ L 24, 29.1.2004, p. 1 (the "Merger Regulation").

3 COMP/M.5724 – Suez Environnement/AGBAR, Paragraph 29, decision of 27.04.2010

4 Regulated water companies are the equivalent to the municipal providers of some or all of such services in other countries in Europe.

5 COMP/M.5724 – Suez Environnement/AGBAR, Paragraph 12, decision of 27.04.2010

6 Paragraph 12-16

7 In England and Wales, Scotland and Northern Ireland each regulated water company is subject to a five year regulatory price control settlement or price control period. The duration of most of the contracts and the tendering process in the market for provision of outsourced O&M services and design, construction and management services of water and wastewater facilities to regulated water companies in the UK are significantly influenced by this price control period, which in England, Wales and Scotland has duration of five years. The current price control period runs from 2010 to 2015

8 Paragraph 11 and 16

9 Paragraphs 24-29

10 Paragraph 27

11 COMP/M.5724 – Suez Environnement/AGBAR, Paragraph 23, decision of 27.04.2010

12 COMP/M.5724 – Suez Environnement/AGBAR, Paragraph 23, decision of 27.04.2010

13 COMP/M.5461 – Lyonnaise des Eaux/Société de Distribution d’Eau et d’Assainissement, paragraph 16; COMP/M.5464 – Veolia Eau/Société des Eaux de Marseille/Société des Eaux d’Arles/Société Stéphanoise paragraph 16; COMP/M.5812 Société Lyonnaise des Eaux/Sociétés de Distribution d’Eau et d’ Assainissement (II) paragraph 19

14 COMP/M.5461 – Lyonnaise des Eaux/Société de Distribution d’Eau et d’Assainissement, paragraph 17; COMP/M.5464 – Veolia Eau/Société des Eaux de Marseille/Société des Eaux d’Arles/Société Stéphanoise paragraph 17; COMP/M.5812 Société Lyonnaise des Eaux/Sociétés de Distribution d’Eau et d’ Assainissement (II), paragraph 20

15 Paragraph 12

16 Paragraph 10

17 Paragraphs 15

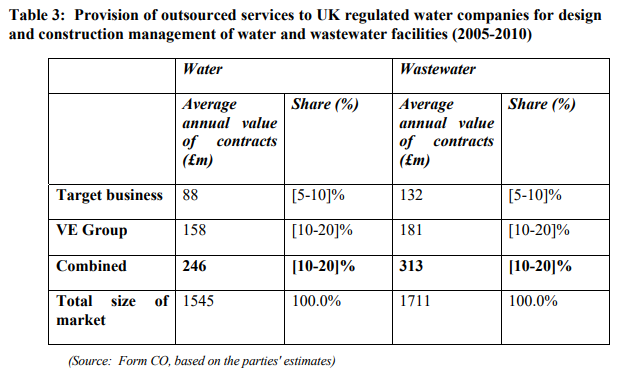

18 The market segmentation as showed at Tables 1,2 and 3 is the most conservative, under any wider product market definition the parties' combined market shares would be lower in UK.

19 VE Group estimates that in total it serves only [5-10]% of the population of England and Wales, it accounts for less than [5-10]% of all allowed capital and operating expenditure of regulated companies in England and Wales. Finally in terms of turnover, VE group approximate share of a wider market encompassing both water and wastewater services would be [0-5]%. Segmenting water services and wastewater services, VE group share of supply of water by reference to the number of its regulated companies and population served would be respectively [10-20]% and [5-10]%. Considering instead the value of its turnover, its market share would amount to [5-10]%. Finally, VE group would have a negligible market share in England and Wales with respect to the provision of wastewater services.