Commission, August 20, 2010, No M.5935

EUROPEAN COMMISSION

Judgment

Vion/ WEYL

Dear Sir/Madam,

Subject: Case No COMP/M.5935 - Vion/ WEYL Notification of 15 July 2010 pursuant to Article 4 of Council Regulation No 139/20041

1. On 15/07/2010 the European Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004[1] by which Vion Enschede B.V., Premium Fleischspezialitäten GmbH and Vion Buchloe GmbH, belonging to the Vion Food Group (collectively "Vion", The Netherlands) acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of all assets of Weyl Beef Products B.V. ("Weyl", The Netherlands) and certain of its group companies by way of purchase of assets.

I. THE PARTIES

2. Vion is active in the purchase and slaughtering of livestock, the processing, production and sale of meat products as well as derived convenience food products and ingredients. Vion is established in Best, the Netherlands.

3. Weyl is a beef and calf processing company, established in Enschede, the Netherlands. Weyl is subject to bankruptcy proceedings. The bankruptcy trustee of Weyl has stopped all activities of Weyl as from the end of May. Currently no animals are slaughtered in either of its locations. All personnel have been or are expected to be made redundant by the bankruptcy trustee shortly.

III. THE CONCENTRATION

4. Vion intends to acquire substantially all assets of Weyl. As a result, after completion of the proposed transaction, Vion will acquire sole control over Weyl within the meaning of Article 3(1)(b) of the Merger Regulation.

IV. EU DIMENSION

5. The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5,000 million3 (Vion: EUR 8,900 million and Weyl: EUR 290 million). Each of them has an EU-wide turnover in excess of EUR 250 million (Vion: EUR 8,133 million and Weyl: EUR 285 million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

6. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the EC Merger Regulation.

V. COMPETITIVE ASSESSMENT

7. The transaction horizontally relates to the markets of (i) purchase of live cattle and calves for slaughtering, (ii) sale of fresh beef and (iii) sale of fresh veal. In addition, there are a number of vertically affected markets in abattoir-by-products.

(i) Purchase of live cattle and calves for slaughtering

A. Relevant Product Market

8. According to Regulation 1165/2008 on livestock and meat statistics, bovine animals aged 8 months or under are considered to be calves; bovine animals aged over 8 months are to be considered cattle.4 The parties accepted this separation.

Purchase of live calves for slaughtering

9. In a previous case5 the Commission considered the market for the purchase of live calves for slaughtering to constitute a separate product market. The parties have agreed with this definition.

Purchase of live cattle for slaughtering

10. In previous cases[2], the Commission held that the market for the purchase of live cattle for slaughter constituted a separate product market. The parties agreed with this definition.

11. As the market investigation also largely confirmed this product market definition, it will be applied for the present case.

B. Relevant Geographic Market

Purchase of live calves for slaughtering

12. In its previous decision, the Commission considered the geographic market for the purchase of calves for slaughtering to be at least national in scope.[3] The parties agreed with this definition.

13. The geographic market is defined as national for the purchase of calves for slaughtering in the present case.

Purchase of live cattle for slaughtering

14. Previous Commission decisions have indicated that cattle can be economically transported at distances of up to 600 km, while in Germany the average distances travelled were between 300 and 450 km. On this basis the Commission concluded that Germany could be divided into two relevant geographic markets; i.e. Northern Germany and Southern Germany (comprising Baden-Württemberg and Bavaria).[4] In an earlier case[5], the Commission's market investigation suggested that the market for the purchase of slaughter cattle may be national in scope in both Germany and in the Netherlands.

15. The parties have stated that in view of the location of Weyl’s two slaughterhouses (Enschede and Nordhorn), both located around the Dutch/German border, and in view of the transportation range of 450 km, the geographical scope of the market in the case at hand would comprise at least the Benelux region and Northern Germany (i.e. Germany excluding Baden-Württemberg and Bavaria). However, according to the data the parties submitted there does not appear to be any substantial import of live cattle into Germany and the Netherlands[6].

16. The responses to the Commission's market investigation indicated that in Germany live cattle travelled no further than 450 km and that the bulk travelled no further than 300 km. This would indicate that the relevant geographic market could be considered as national or regional. The reasons given for this include preferences of customers for national products, the additional cost and administration involved in acquiring the necessary veterinary certificates. By contrast, the competitors indicated that transport costs do not account for an important part of the final price (1-5%).

17. In the Netherlands, respondents to the Commission's market enquiry indicated that they sell 100% of their live cattle to slaughter houses within a radius of 300 km. In majority, they considered the market as national or smaller. One supplier indicated that it did not regard export as an option given the additional costs for acquiring veterinary certificates. Consumer preferences, the availability of sufficient capacity in the Netherlands and the lack of sufficient capacity in neighbouring countries were given as the reasons for selling only in the home country according this supplier. As in Germany, respondents considered transport costs to account for a maximum of 5% of the final price.

18. In the case of Germany, the market definition can be left open as the proposed operation would not raise competition concerns irrespective of whether the relevant geographic market is defined as national or North and South Germany.

19. The relevant geographic market in the Netherlands is also left open as the radius of 450 km around the parties' slaughterhouses would include at least the Benelux region and Northern Germany (i.e. Germany excluding Baden-Württemberg and Bavaria). The market will be analysed at regional and national level.

20. C. Competitive Assessment

Purchase of live calves for slaughtering

21. The parties are relatively small players in the purchase of live calves. In the Netherlands, Vion did not purchase live calves in 2009[7], while Weyl's market share amounted to [05]%.

22. In Germany, the combined market share of the parties, in 2009, amounted to [5-10]% (Vion: [0-5]%, Weyl: [0-5]%).

23. Based on the above, it can be concluded that the proposed transaction will not give rise to competition concerns.

Purchase of live cattle for slaughtering

Germany

24. At the national level, Vion operates several slaughterhouses at various locations in Germany, while Weyl has only one slaughterhouse at the Dutch border (Nordhorn). In 2009, the combined market share of Vion and Weyl was [30-40]% in Germany (Vion: [20-30]%, Weyl: [0-5]%). […], in 2008 and in 2009, Weyl exceeded the maximum permitted slaughtering capacity of its Nordhorn slaughterhouse[8]. In 2009, it exceeded the capacity permit by […]. This means that if Weyl had respected the capacity limit in 2009, its market share would have been […] and the share of the combined entity would be […]. An important number of competitors is active on the market, with the two largest having market shares of [5-10] % each.

25. The parties also submitted that the Nordhorn slaughterhouse has not been operational since Weyl was declared bankrupt in May 2010, and that Vion would be unable to operate it in a commercially viable manner immediately because: i) the slaughterhouse does not meet Vion's standards, and Vion would need to build a new slaughterhouse and invest EUR […]. It would thus take at least 12 months until the new slaughterhouse will be operational. ii) key management have joined competing undertakings. As a result, until the recommissioning of the Nordhorn slaughterhouse, there will be no increase in Vion's market share. In the interim the parties' competitors will continue to purchase the cattle that would have been bought by Weyl.

26. In any case, the parties' combined market shares are comparatively modest (maximum [30-40]%) and the increment is not substantial (maximum [0-5]%). There is a large number of alternative purchasers of live cattle in either Germany or Northern Germany to which suppliers could turn. These slaughterhouses have significant unused capacity available to restrain the combined entity ([35-55]% according to the parties and [1040]% according to competitors).

27. As cattle are usually sold on weekly orders rather than on the basis of long term contracts, suppliers would be able to switch between slaughterhouses easily in either Germany or neighbouring countries. This is facilitated by the EU uniform quality criteria (SEUROP system) which allows slaughterhouses to purchase cattle of comparable quality based on established quality standards in any EU Member State and which enables cattle suppliers to easily compare prices offered to them by slaughterhouses throughout the EU. Consequently, suppliers have a good idea of the prices obtainable in neighbouring countries and make their decisions accordingly. Also, there is a very high degree of price transparency, since in Germany – as in most Member States - prices are published on a weekly basis. In their replies to the market investigation, the majority of the German competitors agreed with the statement that suppliers could switch if the merged entity tried to decrease the prices.

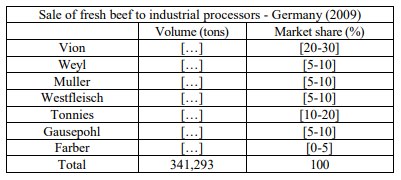

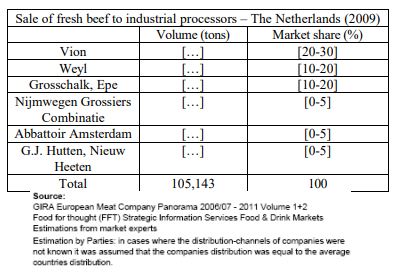

28. In Northern Germany, Vion operates several slaughterhouses and Weyl's only German slaughterhouse is also located in this area. The combined market share would be lower than at the national level: [20-30]% (Vion: [10-20]%, Weyl: [5-10]%) in 2009. If Weyl had respected the capacity permit, its market share would have been […]% and the combined entity's market share would have been […]%.The five main competitors had a combined market share of 45.7%, with two of them having comparable market shares to Vion.[9]

29. Southern Germany, as Weyl does not purchase live cattle in Southern Germany, the proposed operation would not lead to horizontal overlaps.

Conclusion for the German market

30. Based on the above, for Germany as a whole and on the narrower markets for Northern and Southern Germany, it can be concluded that the proposed transaction will not give rise to competition concerns.

The Netherlands

31. In the geographic market comprising Benelux region and Northern Germany (i.e. Germany excluding Baden-Württemberg and Bavaria), based on 2009 data, the parties would have a combined market share of [10-20]% (Vion: [10-20]%, Weyl: [5-10]%)14. However, if Weyl had respected its capacity permit in Germany, the parties' combined market would have been […]% (Weyl: […]%). In addition, there are two strong competitors having similar market shares to the parties (Westfleish: [5-10]%, Gausepohl: [5-10]%).

32. In the Netherlands, there are nine slaughterhouses, of which those of Weyl and Vion are the largest. Following the transaction, and on the basis of 2009 data, they would have a combined market share of [40-50]% (Vion: [10-20]%, Weyl: [20-30]%)15. The five largest competitors had a combined market share of 36.5% in 2009, with one strong competitor having a [20-30]% market share.16 The market shares have not changed significantly in the last three years and the parties import only a small proportion (Weyl:[10-20]%, Vion: [0-5]%) of their purchases).

33. On the basis, of 2009 data, the parties' combined market share is comparatively modest (maximum [10-20]%) and the increment is not substantial (maximum [5-10]%) in the wider, regional geographic market. Concerning the Netherlands, the planned acquisition transaction would bring about relatively high market shares regarding purchase of live cattle for slaughtering in the Netherlands ([40-50]%). However, there is a strong competitor and significant free capacity on the market (according to the parties about 30% and possibly higher according to one competitor). If suppliers needed to switch to other slaughterhouses, according to their replies to the market investigation, they would be able to do so easily due to the established SEUROP standard. In addition, prices are transparent, as they are published weekly. These prices are also similar to a high degree, as half of the suppliers indicated that the difference of weekly prices is maximum 5%. Also, the majority of suppliers did not perceive the merger as having a negative effect, but some of them even evaluated it positively, because the merger would ensure that the Weyl business would not be permanently closed. None of the competitors expressed concerns about the merger.

34. Although the planned acquisition could strengthen the buying position of Vion for cattle in the Netherlands, the buying power in itself does not raise competition concerns. This is because in case a purchaser faces strong competition on the downstream selling market (which is the case at hand; on the markets of "sale of fresh beef" and "sale of fresh veal", both analysed below) it is very likely that he will be obliged to pass on the benefits gained (lower input costs) to consumers. However, given the dependency of both Weyl and Vion on the suppliers of live cattle, the parties cannot lower the purchase price of live cattle drastically as suppliers would switch supply to alternative slaughterhouses in the Netherlands or potentially to neighbouring countries.

Conclusion for the Dutch market

35. Considering the arguments above, it can be concluded that the proposed transaction will not give rise to competition concerns in the geographic market including Benelux region and Northern Germany (i.e. Germany excluding Baden-Württemberg and Bavaria) and in the Netherlands.

(ii) Sale of fresh beef

A. Relevant Product Market

36. In an earlier decision the Commission concluded that fresh meat includes both fresh and frozen meat (including minced meat) which is not further processed17. The Commission has, in previous decisions, defined separate product markets for the sale of various types (pork, veal, lamb, etc.) of fresh meat, including fresh beef18.

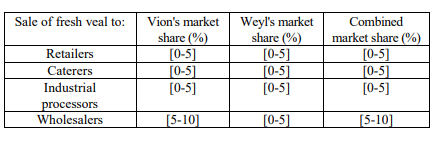

37. The sale of fresh beef was further segmented19 into: (i) sale to retailers, which was further divided into (a) sales to supermarkets and (b) sales to butchers; (ii) sale to caterers, such as restaurants, canteens, government institutions, ship and airport handlers and (iii) sale to industrial processors. Caterers prepare the meat to serve it to the final customer as part of a ready-cooked meal and do not sell the fresh meat as such. Industrial processors buy meat from slaughterhouses and turn it into different types of processed meat products, which are then sold to the retail market or the catering market as processed meat. Industrial processors of fresh meat include producers of sausages, ham, hamburgers, canned food and convenience products20.

38. The parties agreed with these product definitions21 which have been largely confirmed by the market investigation.

39. Therefore, the above market definition will be maintained in the present decision.

B. Relevant Geographic Market

40. With regard to the sale of fresh beef to retailers, as Vion does not sell to butchers, only the market for the sale to supermarkets will be addressed. In the past, with regard to the sale of fresh beef to supermarkets, the Commission conducted its investigation on the basis of three possible alternative geographic market definitions: national, regional (including the Benelux, Denmark, France and Germany) and EEA-wide22.

41. The parties submit that the geographic market for this segment is EEA-wide in scope, on the basis of limited transport costs (only 2.6% of the average beef sales price of EUR 3.40/kg is attributed to transport costs), pre-packaging techniques that prolong the shelflife of meat products in supermarkets, significant intra-Union trade, international sourcing by supermarkets, identical veterinary regulations and uniform European quality standards.

42. For the purpose of this decision, however, the geographic market definition can be left open as the proposed operation will not give rise to competition concerns under any of the alternative geographic market definitions.

43. With regard to sale of fresh beef to caterers and industrial processors, in previous decisions, the Commission considered the relevant geographic markets to be wider than national[10]. The parties agree with this market delineation, further submitting that the market for sale of fresh beef to industrial processors would be EU-wide.

44. The majority of the respondents to the market investigation considered that the market has at least a regional scope, almost half of them being of the opinion that the market is EEA wide. For the purpose of this decision, however, the geographic market definition can be left open as the proposed operation will not give rise to competition concerns under any of the alternative geographic market definitions.

C. Competitive Assessment

1) Sale of fresh beef to retailers

45. As concerns the sale of fresh beef to supermarkets, the only potentially affected market is Germany, where the parties, on the basis of 2009 data, would have a combined market share of [20-30]% but with Weyl adding only [0-5]%. Such a small increment is unlikely to lead to any competition concerns.

2) Sale of fresh beef to caterers

46. With regard to the sale of fresh beef to caterers the combined market share of the parties is [05]% (Vion: [0-5]%, Weyl: [0-5]%) in the European-wide market and on the basis of 2009 data. In no individual country would the parties’ combined market share exceed 15%.

3) Sale of fresh beef to industrial processors

47. With regard to the sale of fresh beef to industrial processors the combined market share of the parties is [10-20]% (Vion: [5-10]%, Weyl: [0-5]%) in the EU market and on the basis of 2009 data. If the geographic market is defined as national in scope, the affected markets would be Germany [30-40]% (Vion: [20-30]%, Weyl: [5-10]%) and the Netherlands [3040]% (Vion: [20-30]%, Weyl: [10-20]%).

48. The parties' exports to industrial processors in the EU were particularly high. Vion's exports (from its slaughterhouses in the Netherlands, Germany and the UK) accounted in 2009 for [40-50]% and Weyl's exports (from its slaughterhouses in the Netherlands and Germany) accounted for [30-40]% of total sales to industrial processors. The parties contend that, in view of the international purchasing behaviour of industrial processors, those located in Germany and the Netherlands could easily obtain supplies of fresh beef from other EU countries, for example Belgium and France.

49. The market investigation has largely confirmed the parties' claim. The overwhelming majority of the competitors are of the opinion that industrial processors and/or wholesalers purchase fresh beef from slaughterhouses irrespectively of their location within the EEA. Moreover, the market investigation revealed that industrial processors in the Netherlands and Germany do source from abroad. Therefore, even if the geographic market was to be considered national, customers in Germany and the Netherlands would be able to restrain any attempts by the parties to raise prices by sourcing their beef from third countries.

50. On a wider regional market (including Belgium, the Netherlands, Denmark, France and Germany) the parties' market shares would be considerably lower (Vion: around [1020]% and Weyl: [5-10]%) and would not raise competition concerns.

51. Moreover, the industry is characterised by overcapacity. According to the parties, in the Netherlands, the utilization ratio of the slaughterhouses was approximately 72% in 2009 while in Germany24 the utilization ratio was 57%. Therefore, it is unlikely that the proposed transaction will create or strengthen a dominant position or otherwise significantly impede effective competition25.

52. As illustrated in the tables below, a large number of competitors in the market for sale of fresh beef to industrial processors would remain in both Germany and the Netherlands after the proposed transaction.

53. On a market for sale of fresh beef to industrial processors and wholesalers in Germany and in the Netherlands, the parties’ market share (based on 2009 data) would not change significantly from their market shares on the market for sale of fresh beef to industrial processors. In Germany it would amount to approx. [30-40]% ([30-40]% for Vion and approx. [5-10]% for Weyl). On a market for sale of fresh beef to industrial processors and wholesalers in the Netherlands, the parties’ market share would amount to approx. [30-40]% ([20-30]% for Vion and approx. [10-20]% for Weyl).

54. The majority of respondents to the Commission's market investigation considered that it would have no negative effect on the markets for fresh beef, while several considered it would even reinforce competition. The market investigation also revealed that industrial processors and wholesalers would be able to replace the combined entity Vion-Weyl for the supply of fresh beef in the event of an increase in price by 5-10 % after the merger.

55. In Germany and the Netherlands, although the market shares are comparatively high, competition concerns are unlikely to arise for the following reasons. In both Germany and the Netherlands competitors account for over 60% of the supply. Furthermore, capacity utilisation rates in both countries are comparatively low so that competitors could easily increase their supply to counteract any attempt by the combined entity to raise prices.

56. For these reasons the Commission considers that the proposed transaction does not raise serious doubts as to its compatibility with the internal market regarding the market for the sale of fresh beef under any of the alternative geographic market definitions.

(iii) Sale of fresh veal

A. Relevant Product Market

57. The Commission has pointed toward separate product markets for the sale of fresh veal26, into: (i) sale to retailers, (ii) sale to caterers, (iii) sale to industrial processors, and

(iv) sale to wholesalers. In its assessment in the Van Drie/Alpuro27 case, the Dutch Competition authority left open a segmentation of the veal market into the very same segments. The parties agreed with this market definition.

58. The market investigation has largely confirmed these product market delineations which will be maintained in the present decision.

B. Relevant Geographic Market

59. In Van Drie/Schils28, the Commission observed that the markets for sale of fresh veal (to wholesalers) may be EU-wide in scope. In the decision Van Drie/Alpuro29, the Dutch competition authority NMa further analysed the geographic scope of the market and concluded that the markets for sale of fresh veal are EU-wide in scope.

60. For the purpose of this decision, the geographic market definition will be left open as the proposed transaction would not lead to competition concerns even if the markets were defined as national in scope.

C. Competitive Assessment

61. The following table shows the parties' market shares in 2009 on the EU-market for the sale of fresh veal:

62. Only in Germany, on a hypothetical market for the supply to wholesalers, would the parties’ combined market share exceed 15% on any of the four segments in any Member State.

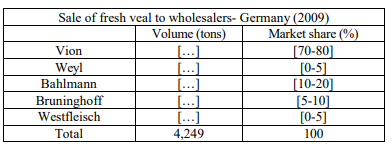

63. Any competition concerns relating to the sale of fresh veal are therefore confined to Germany. Under any alternative market definition there are no affected markets with respect to the sale of fresh veal. On the potential market for sale of fresh veal to wholesalers in Germany, the parties' combined market share would amount to [70-80]%, with an increment of [0-5]%.

64.The increment of [0-5]% is very small and would not change the market structure in Germany to any significant extent. In addition, as illustrated in the table below there would be several competitors remaining in Germany.

65. In light of the above, the Commission considers that the proposed transaction does not raise serious doubts as to its compatibility with the internal market with regard to the market for the sale of fresh veal.

(iv) Abattoir by-products

66. During the slaughtering process, slaughterhouses produce different abattoir by-products (“ABPs”) which can either be further processed to become suitable for human consumption ("food grade") or which have to be disposed or fed to animals ("non-food grade"). Like all slaughterhouses, both Vion and Weyl produce ABPs. Only Vion purchases and processes ABPs from third parties. As Weyl only slaughters calves and cattle, it can only deliver ABPs of such origin.

Collection and disposal of non-food grade materials

A. Relevant Product Market

67. Non-food grade products may not be used for further processing into products for human consumption. They are for example processed into pet food, used for other nonfood grade applications or have to be disposed of. On the basis of EC Regulation 1774/2002 of 3 October 2002, ABPs not intended for human consumption are classified into three different categories. (i) Category 1 materials are mainly body parts of animals suspected of being infected by certain diseases (e.g. BSE); (ii) Category 2 materials cover dead animals not infected by dangerous diseases as well as animals which are not admitted for slaughtering; (iii) Category 3 materials include all other ABPs which are not used in the food/gelatine-grade sector. These are parts of slaughtered animals (e.g. blood) which could be fit for human consumption but are not used for that purpose for commercial reasons.

68. In previous cases30 the Commission identified a product market for the collection and disposal of category 1 and 2 material. Both under EU and national law, the two groups are strictly regulated. As regards the category 3 material the previous Commission's precedents considered that they might be part of the relevant product markets (i.e. bones, fat, etc.) but ultimately left the definition open.

69. In previous cases31 the Commission identified a geographic market that is at most national as the category 1 and 2 materials may not be exported and need to be processed in the area where they originate from. National regulations require slaughterhouses to supply category 1 and 2 material for disposal to a specific rendering plant that holds an exclusive license. In the Netherlands, and certain regions of Germany, Vion companies hold exclusive licenses (subsidiaries Rendac and SNP). The activities of and prices paid to Rendac and SNP are subject to governmental control.

C. Competitive Assessment

70. In the Netherlands, Vion's subsidiary Rendac holds an exclusive license for the processing of category 1 and 2 material and therefore has a statutory monopoly and holds a market share of 100% on the market for the collection and disposal of category 1 and 2 materials. Rendac’s tariffs are subject to strict governmental control. For these reasons, the transaction will not bring about any change in the market structure and therefore will not give rise to competition concerns.

71. In Germany, Vion operates rendering plants in Icker, Rotenburg en Jagel, through its subsidiaries Rendac and SNP while Weyl has no such plants. Vion’s catchment areas do not cover the area in which Weyl is located in Germany (Nordhorn). Therefore in Germany no vertical relationship arises for disposal of Category of 1 and 2 materials and the transaction will not give rise to competition concerns.

Purchase and processing of blood

A. Relevant Product Market

72. Food-grade blood is supplied to producers of plasma and haemoglobin, to butchers or to meat processors. Category 3 blood is supplied to producers of (feed-grade) plasma and haemoglobin and to pet food manufacturers. According to past Commission decisions, food grade blood and category 3 blood constitute separate product markets, and food grade blood and category 3 blood could be further split according to species from which the blood has been collected, e.g. cattle and pigs32. However, the exact product market definition was left open. The market definition can be left open in this case as the transaction does not give rise to competition concerns under any alternative market definition.

B. Relevant Geographic Market

73. The previous Commission decisions33 indicate that blood purchasers source most of their blood within a radius of 200 – 300 km from the processing plants. In any event, the precise geographic market definition can be left open for the purpose of this case, as no competition concerns arise from the transaction.

C. Competitive Assessment

74. Regardless of the product and geographic market definition, Weyl already supplies 100% of its food grade cattle blood to Vion's subsidiary Sonac for processing. Weyl has not supplied any category 3 blood in 2009. Moreover, Sonac already collects and processes approx. 100% of food grade cattle blood in the Netherlands. Therefore, the transaction does not bring any market change with respect to blood market and will not give rise to competition concerns.

Purchase and processing of bones

A. Relevant Product Market

75. Bones can be used in the production of gelatine, foodstuff, meat and bone meal, fat and technical glues, colloidal products and bone ash. In principle, cattle bones and bones from other bone types (pig) can be used for all applications even though cattle bones are better suited for certain applications.

76. In past decisions the Commission indicated (but left open the precise market definition) that there is one single product market for all bones34 (category 3 bones, food/gelatine grade bones). Category 1 and 2 bones are included in the collection and disposal of category 1 and 2 ABPs (e.g. bones from cows which were infected by BSE) and are not used for the production of gelatine.

B. Relevant Geographic Market

77. According to previous Commission decisions, the relevant geographic market comprises at least the Netherlands, Belgium and Germany, with the possible inclusion of France35.

C. Competitive Assessment

78. Vion's subsidiary Sonac purchased approx. […] tons of all bones (non category 1 and 2) in the Netherlands and Germany, which amounts to a market share of approx. [2030]%. Weyl purchased […] tons of bones (non category 1 and 2) in 2009. This amounts to approx. [0-5]% of the bones (non category 1 and 2) supplied in the Netherlands, Belgium and Germany. The upstream market share of [20-30]% is not indicative of competition concerns.

Purchase and processing of fat

A. Relevant Product Market

79. In previous Commission decisions, the exact market definition for the purchase/processing of fat was left open. However, as for other ABPs, separate product markets exist for category 3 fat and food grade fat36. The market definition can be left open in this case as the transaction does not give rise to competition concerns under any alternative market definition.

80. The geographic market for fat has not been defined in previous Commission decisions. The impact of the transaction will be analysed on a national basis, as this is considered by the market investigation to be the most likely scope of this market. In this case, the exact scope of the market can be left open as the transaction will not give rise to competition concerns under any alternative definition.

C. Competitive Assessment

81. Weyl currently only supplies food grade fat to a processor in Germany. In Germany, Vion operates, through its subsidiary Sonac, three food grade fat-melting plants in Versmold, Erolzheim and Elsholz. Vion purchased/processed approx. […] tons of food grade fat in 2009. This amounts to a market share of approx. [30-40]% in Germany. However, it must be noted that approx. [20-30]% of food grade fat purchased by Sonac was purchased internally from Vion slaughterhouses. Weyl produced […] tons of food grade fat in 2009. This amounts to approx. [0-5]% of food grade fat supplied in Germany. Weyl has not supplied any category 3 fat in 2009.Vion’s competitors in the area of purchasing and processing food grade fats in Germany include Ten Kate (approx. market share of [10-20]%), Fischermanns (approx. market share of [5-10]%) and KFU (approx. market share of [5-10]%). Given that the upstream market share does not exceed 40%, that there are credible competitors of Vion and that Weyl's downstream market share is small, the transaction will not result in input or customer foreclosure. Therefore, the transaction will not give rise to competition concerns in this respect.

Purchase and processing of bovine hides

A. Relevant Product Market

82. Bovine hides are mainly purchased by tanneries, which further process the hides by separating the bovine hide into three layers: the flesh-containing subcutaneous layer, which is removed; the outside skin, which is processed to leather and the mid layer, which is sold to the collagen casing industry (in which Vion is not active) and to gelatine producers.

83. The Commission has previously addressed but not defined the product market for the purchasing of bovine hides[11]. For bovine hides the category 3 material reference does not apply. On the market for purchasing bovine hides, Vion is also active as a purchaser/trader. Vion purchases bovine hides from slaughterhouses and supplies sorted hides to tanneries.

B. Relevant Geographic Market

84. The geographic market has not been defined in previous Commission decisions. The parties consider that the market for the purchase and processing of bovine hides is wider than national, i.e. comprising Germany and the Netherlands as Weyl sold all bovine hides from its slaughterhouses in the Netherlands and Germany to purchasers in the Netherlands. In this case, it can be left open whether the scope of the market could be narrowed down to a national level as the transaction will not give rise to competition concerns under any of the alternatives considered.

C. Competitive Assessment

85. Only Vion (through its subsidiary Almox) is active as a purchaser/trader of bovine hides. Vion purchases bovine hides from slaughterhouses, including the Vion slaughterhouses and supplies sorted hides to tanneries.

86. Weyl's sells all of its hides in the Netherlands and has not sold any hides in Germany. The proposed operation will not therefore raise competition concerns in relation to Germany.

87. Weyl's sales of hides amounted to about […] pieces which represented about [60-70]% of all hides purchased in the Netherlands. The impact of the transaction is therefore limited to Weyl becoming a potential captive supplier of bovine hides to Vion in the Netherlands, where in 2009 Almox purchased about [10-20]% of the hides largely from its own operations. If Vion was able to deal with all of Weyl's bovine hides it would become the largest buyer in the Netherlands. However, it would be unable to use this power to reduce purchase prices from the slaughterhouses as there would be sufficient competitors (four in the Netherlands with the market share in 2009 of between [30-40]% and [5-10]%) to constrain such behaviour. Furthermore Dutch slaughterhouses could sell their bovine hides to companies operating in neighbouring countries. It should be noted that Weyl sold the hides produced from its German slaughterhouse in the Netherlands which indicates that such sales are not only possible but also beneficial.

88. The hides have to be sold, in competition with other operators to the competitive tanning industry. So that even if Almox succeeded in obtaining additional volumes by purchasing all of the Weyl production of bovine hides would be likely to be forced to pass on these savings to tanners

89. Finally, it should be noted that on a combined geographic market including both Germany and the Netherlands Almox's share of purchases including Weyl's would have been a modest [20-30]% of which about [10-20]% are captive purchases. Therefore, the transaction will not give rise to competition concerns in this respect.

Purchase and processing of bowel packages and cattle heads

90. Some respondents to market test also pointed out that the markets for bovine bowels and cattle heads should be considered as a distinct markets.

A. Relevant Product Market

91. Bowels or bowel packages are raw abattoir by-products including small and large intestines, stomach fat, spleen and pancreas. Parts of the bowel package are further processed into natural casings for sausages and parts of them are used for pharmaceutical applications or are disposed. In the previous decisions the product market definition for bowel packages was left open.

92. Cattle heads are sold to companies that remove the meat on the heads and process it into meat products. The product market for the purchase or sale of cattle heads has not been previously defined by the Commission.

93. In the previous decisions the geographic market definition for bowel packages was left open. Given that there are no restrictions on exports of bowel packages as abattoir byproducts, the market is possibly wider than national. In this case the market definition can be left open as the transaction will not give rise to competition concerns under any alternative market definition, i.e. a national scope.

94. The geographic market for purchase or sale of cattle heads has not been previously defined by the Commission. As the parties do not purchase cattle heads the purchase market will not be discussed further. As regards the market for the sale of cattle heads, the parties submit that the scope of this market is likely to correspond with the market for the purchase of live cattle. This would imply that in the case of Germany, the geographic market would be defined as national in scope or would consist of Northern and Southern Germany. The relevant geographic market in the Netherlands would be national in view of the size of the country and the distance over which cattle heads are transported. However, the market definition can be left open as the transaction will not give rise to competition concerns under any alternative market definition

C. Competitive Assessment

95. The total market volume for the sales of bowel packages corresponds with the total number of slaughtered cattle as the production of bowel packages is directly proportional to the number of animals slaughtered. Weyl does not purchase bowel packages. Vion mostly processes its bovine bowels internally. In the Netherlands Vion does not purchase bowel packages. In Germany Vion's merchant purchases of bovine bowels amounted to [0-5]%. Even if this market share is aggregated to Vion's market share in slaughtering of cattle in Germany, which amounts to [20-30]%, the total market share in the purchase of bowels will be below 40%. Purchase and sale of bowel packages is a low margin business and accounts for a small fraction of slaughterhouses revenue. For these reasons the parties are unlikely to have any incentives to engage in any strategies aimed at input or customer foreclosure. Therefore, the transaction will not give rise to impediment of competition.

96. Neither Vion nor Weyl purchase cattle heads from third parties. With respect to the sale of cattle heads, as the market shares of the parties correspond to slaughtering of cattle they would vary between [40-50]% in the Netherlands to [10-20]% in Benelux and Germany, depending on how the geographic market is defined. Even if the radius would be considered smaller than 450 km, there is a number of competing slaughterhouses in Northern Germany and the Netherlands that can supply cattle heads to industrial processors. Sale of cattle heads is a low margin business and accounts for a small fraction of slaughterhouses revenue. For these reasons the parties are unlikely to have any incentives to engage in any strategies aimed at customer foreclosure. Therefore, the transaction will not give rise to impediment of competition.

VI.CONCLUSION

97. For the above reasons, the Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 OJ L 24, 29.1.2004, p. 1 (the "Merger Regulation").

3 Turnover calculated in accordance with Article 5(1) of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C95, 16.04.2008, p1).

4 Regulation No 1165/2008 of the European Parliament and of the Council of 19 November 2008 concerning livestock and meat statistics and repealing Council Directives 93/23/EEC, 93/24/EEC and 93/25/EEC, OJ L-321, 1 December 2008, p 1-13.

5 COMP/M.3535 Van Drie/Schils, para 14.

6 COMP/M.1313 Danish Crown/Vestjyske Slagterier, para. 20, COMP/M.3337 Best Agrifund/Nordfleisch, para. 17, COMP/M.3968 Sovion/Südfleisch, para. 12.

7 COMP/M.3535 Van Drie/Schils , para 22.

8 idem, para. 35.

9 COMP/M.3337 Best Agrifund/Nordfleisch, paragraphs 18-21.

10 In Germany, about 1.5% and in the Netherlands, about 3.7% of the live cattle slaughtered originated from third countries.

11 VION did purchase live calves in 2007 and 2008. Its market share in those years was estimated at approx. [0-5]% and [0-5]%.

12 In 2008, Weyl's production was […] heads, while its capacity permit was for […] heads. In 2009 its production was […] heads, while its capacity permit was equally limited to […] heads.

13 Westfleisch: [10-20]%, Gausepohl: [10-20]%.

14 These market shares are based on 2009 figures, however the slaughterhouse in Enschede has not operated since Weyl's bankruptcy. Vion intends to operate the plant so the 2009 market shares have been used although it will take time to reach this level of output.

15 These market shares are based on 2009 figures, however the slaughterhouse in Enschede has not operated since Weyl's bankruptcy. Vion intends to operate the plant so the 2009 market shares have been used although it will take time to reach this level of output.

16 Gosschalk being by far the largest competitor; the four others have a market share of below [5-10]%.

14 COMP/M.3337 Best Agrifund/Nordfleisch, para. 23.

15 COMP/M.3968 SoVion/Südfleisch, para. 61. COMP/M.3605 SoVion/HMG, para. 56. COMP/M.3337 Best Agrifund/Nordfleisch, para. 23. COMP IV/M.1313 Danish Crown/Vestjyske Slagterier, para. 33.

16 COMP/M.3337 Best Agrifund/Nordfleisch, para. 24.

17 Idem.

18 The parties further submit that the sale of fresh beef to wholesalers should be included in the market for sale to industrial processors, since the conditions under which the parties supply wholesalers are most comparable to those under which industrial processors are supplied; both categories of customers, after processing, resell the beef to caterers and/or retailers.

19 COMP/M.3968 SoVion/Südfleisch, para. 65.

20 For caterers: COMP/M.3968-SoVion/Südfleisch, para. 63 and IV/M.1313-Danish Crown/Vestjyske Slagterier, para. 94; For industrial processors: IV/M.1313-Danish Crown/Vestjyske Slagterier, para. 95, COMP/M.3968-SoVion/Südfleisch, para. 63 and COMP/M.3337-Best Agrifund/Nordfleisch, para. 38.

21 By way of example, Tönnies, the second player on the German market has around 40-60% utilisation rate and Westfleisch, the number four, has between 60-85% utilisation rate. In addition, all the competitors responding to the market investigation mentioned that they would be able to increase their current level of production capacity in response to an increase in demand or price increase although most of them said it could take them several months to do so.

22 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings, paragraph 33.

23 COMP/M.3535 Van Drie/Schils, para. 18, 19, 26 and 27.

24 NMa Case 6891 Van Drie/Alpuro (04.05.2010), para. 58.

25 COMP/M.3535 Van Drie/Schils, para. 26.

26 NMa Case 6891 Van Drie/Alpuro, para. 67.

27 COMP/M.3175 Best Agrifund / Dumeco and case COMP/M.3337 Best Agrifund / Nordfleisch (para. 75).

28 Idem para 77.

29 COMP/M. 3605 SOVion / HMG, para. 134. COMP/M. 2968 SOVion / Südfleisch, para. 89.

30 COMP/M.3337 Best Agrifund / Nordfleisch, para. 96.

31 COMP/M. 3175 Best Agrifund / Dumeco, para. 24. COMP/M.3337 Best Agrifund / Nordfleisch, para. 124 – 125. COMP/M. 3605 SOVion / HMG, para. 143 – 144.

32 Idem.

33 COMP/M.3337 Best Agrifund / Nordfleisch, para. 72, 144 – 145.

34 COMP/M.3337 Best Agrifund / Nordfleisch, para. 138 – 139.