Commission, October 28, 2010, No M.5936

EUROPEAN COMMISSION

Judgment

EADS DS/ ATLAS/ JV

Dear Sir/Madam,

Subject: Case No COMP/M.5936 – EADS DS/ ATLAS/ JV Notification of 24.09.2010 pursuant to Article 4 of Council Regulation No 139/2004[1]

1. On 24.09.2010, the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 ("the Merger Regulation") by which EADS Defence & Security SAS ("EADS DS", France) and Atlas Elektronik GmbH ("Atlas", Germany) will create, within the meaning of Articles 3(1) and 3(4) of the Merger Regulation a new full-function joint venture ("NewCo", Germany).

I. THE PARTIES

2. EADS DS is a French-based system solutions provider for armed forces and civil security worldwide that belongs to the EADS group of companies controlled by the European Aeronautic Defence and Space Company EADS N.V. ("EADS", the Netherlands).

Through its subsidiary Sofrelog SAS ("Sofrelog", France), EADS DS is active in maritime safety and security systems ("MSS").

3. Atlas is a German-based supplier of electronics and other equipment in the naval systems sector, in particular offering combat management system solutions for submarines, surface combatants, mine counter vessels, as well as naval weapons. In addition, Atlas produces systems for civilian applications (maritime safety and hydrograph systems). Atlas is jointly controlled by ThyssenKrupp Technologies AG ("TKT", Germany) and EADS Deutschland GmbH, belonging to EADS[2]. Through its subsidiary Atlas Maritime Security GmbH ("AMS", Germany), Atlas is active in maritime safety and security systems.

4. NewCo will result from the merger between EADS DS' wholly owned subsidiary Sofrelog and Atlas' wholly owned subsidiary AMS. It will be located in Germany and will be active in MSS. NewCo will develop, sell and operate land based vessel traffic and security systems for coastal waters, waterways and harbours (coastal surveillance systems "CSS" and vessel traffic systems "VTS").

II. THE OPERATION

5. Pursuant to a Shareholders' Agreement signed on 16 June 2010, EADS DS and Atlas intend to create a joint venture performing on a lasting basis all the functions of an autonomous economic entity and will acquire joint control over this joint venture.

III. CONCENTRATION

Joint control over NewCo

6. NewCo will be jointly controlled by EADS DS and Atlas. EADS DS and Atlas will hold respectively 60 % and 40% of the shares in NewCo. Atlas will have additional rights which will allow Atlas to veto decisions on the strategic commercial behaviour of NewCo.

7. Firstly, both EADS DS and Atlas will have the right to appoint senior management of NewCo.

8. Secondly, a catalogue of decisions, among which approvals of the annual budget and the business plan, has to be unanimously approved by EADS DS and Atlas in the shareholders' meeting.

9. The above mentioned rights conferred upon EADS DS and Atlas are sufficient to enable both EADS DS and Atlas to exercise decisive influence on the strategic business behaviour of NewCo, thus granting them joint-control over NewCo[3].

Full-functionality of NewCo

10. NewCo will perform on a lasting basis all the functions of an autonomous economic entity and will operate actively on MSS (maritime safety and security systems) including CSS (coastal surveillance systems) and VTS (vessel traffic systems).

11. Firstly, EADS DS and Atlas will transfer all their activities related to MSS, including the necessary intellectual property rights and know-how to NewCo. NewCo will be equipped

with all necessary assets and resources, i.e. its own personnel, sufficient funding and a management dedicated to its day-to-day operations.

12. Secondly, NewCo will not depend on its parents. All contracts, offers and obligations in MSS will be transferred to NewCo. None of the parent companies will retain any market activities in the market where NewCo is active. Moreover, NewCo will not source any MSS inputs from its parent companies. Regarding the sale relationships between NewCo and its parents, in some cases, NewCo could be subcontractor of EADS with respect to large border security systems. These contracts will be executed at arm's length and will represent a minor share of NewCo sales.

13. In light of the above, NewCo will be a full-function joint venture within the meaning of Article 3(4) of the Merger Regulation.

IV. EU DIMENSION

14. The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million[4] [EADS DS: EUR […] million; Atlas: EUR […] million]. Each of them has an EU-wide turnover in excess of EUR 250 million [EADS DS: EUR […] million; Atlas: EUR […] million], without achieving more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

15. The notified operation therefore has an EU dimension within the meaning of Article 1(2) of the Merger Regulation.

V. ASSESSMENT A. Market definition (a) Relevant product market

16. The proposed transaction concerns the sector for MSS with its potential sub-segments CSS and VTS.

MSS

17. MSS are land based systems composed of a complex combination of industrial, software and hardware components, in particular radar and sensor packages.

18. MSS allow the surveillance of the sea, harbour and land surface. In particular, these systems are used to control, survey and secure vessel traffic. They also ensure the safety and security of harbours, vessel traffic routes and coastal sections. MSS are primarily civil products used for civil applications and purposes[5].

19. Generally, customers are national governments or their agencies such as ministries of transport or water management offices, but also search and rescue organisations, port authorities or private companies (such as oil companies).

CSS and VTS

20. CSS relate to the activity of control and security of borders against certain security threats, such as smuggling and illegal immigration (security segment of MSS), whereas VTS monitor vessels to ensure that they do not depart from pre-defined circulation lanes, helping these vessels to navigate properly, and to ensure the safety of harbours (safety segment of MSS).

21. CSS are usually larger and more sophisticated than VTS: CSS require a higher quantity of components as VTS do not cover complete coastlines. Therefore, complete CSS are usually overall more expensive than VTS. According to the estimates provided by the notifying parties, the value of VTS contracts is usually from EUR 1 to EUR 5 million[6] and the value of CSS contracts is usually from EUR 10 to EUR 30 million.

22. In line with a previous Commission's decision, the notifying parties consider the overall market for MSS, comprising both CSS and VTS, as the relevant product market[7] for the purpose of the present transaction. They notably argue that both types of systems (VTS and CSS) involve the same technical equipment and systems (e.g. hardware, software, radars, sonar systems, and communication networks).

23. According to the parties, both VTS and CSS are operated in the same way, therefore constituting integral sub-segments of MSS. They also require identical training for their operation and are purchased by the same type of customers (see paragraph 19).

24. Furthermore, the notifying parties submit that the general purposes of the VTS and CSS only differ to a very limited extent and mainly with respect to the user intention.

25. The arguments put forward by the notifying parties were not clearly supported by the market investigation. The vast majority of respondents indicated that CSS and VTS are not substitutable products in particular due the different purposes they serve and the price difference. While confirming that to a large extent the same technology and technical equipment are involved in the CSS and VTS segments, the majority of respondents to the market investigation do not support the definition of an overall market for MSS.

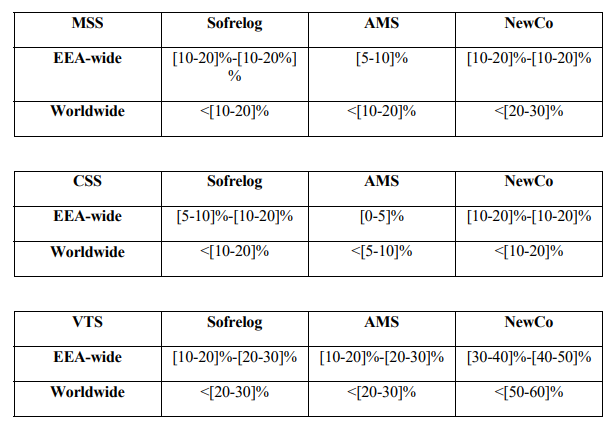

Conclusion on the relevant product market

26. For the purpose of the present transaction the exact product market definition as regards the possible distinction between VTS and CSS can be left open since under any alternative product market definition the proposed transaction would not raise serious doubts.

(b) Relevant geographic market

27. The notifying parties submit that the relevant geographic market for MSS is at least EEAwide and probably even worldwide, on the ground that customers usually source these systems on a worldwide basis.

28. Moreover, according to the notifying parties, there are no significant barriers to trade: MSS equipments are shipped around the world by air transport with costs that account for approximately 1% of the total system costs.

29. According to the notifying parties, the existence of a worldwide market is also shown by the fact that most companies active in this market are active worldwide: for instance, Sofrelog has provided systems in North America (Vancouver) and Norcontrol, a Norwegian competitor, in two ports in California (USA) and in Canada. The parties, as well as their competitors Holland Institute of Traffic Technology B.V. ("HITT", the Netherlands), as well Raytheon Company ("Raytheon", USA) and Lockheed Martin Corp. ("Lockheed Martin", USA) are also active in Asia.

30. Lastly, the notifying parties underline the common international standards for MSS, as set by the International Maritime Organization (IMO) and the International Association of Marine Aids to Navigation and Lighthouse Authorities (IALA).

31. According to the notifying parties the above arguments apply to both VTS and CSS.

32. Respondents to the market investigation largely confirmed the arguments put forward by the notifying parties.

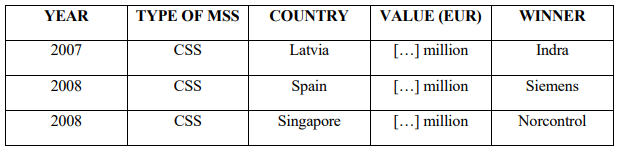

33. Some respondents however also emphasized that the presence of non-European competitors is limited in the EEA, especially in VTS. Indeed in the recent past Lockheed Martin and Raytheon have provided systems only in Bulgaria and Latvia. On the other hand, the market investigation did not reveal any specific barrier for non-European competitors to successfully compete in the EEA.

34. The existence of European regulation, which requires Member States to monitor the compliance of ships with VTS rules and defines the infrastructure for ship reporting systems, ships’ routing systems and VTS[8], could perhaps also suggest that there exists a narrower EEA-wide market for VTS. On the other hand, European VTS regulation is based on the international standards adopted by the IMO.

Conclusion on the relevant geographic market

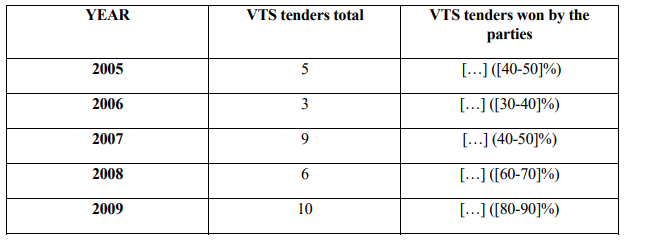

35. While the market investigation suggests that the market is probably worldwide, for the purpose of the present decision, the exact geographic market definition can be left open since under any alternative geographic market definition, the proposed transaction would not raise serious doubts in the EEA.

B. Competitive assessment

36. NewCo will only be active in MSS and its potential sub-segments VTS and CSS. Neither EADS nor TKT will continue to be active in this sector.

37. Contracts in the MSS sector and its subsegments are almost always awarded through tenders. According to figures provided by the notifying parties, the overall annual market for MSS solutions in the EEA ranged from EUR 27 million to EUR 104 million over the 2005-2009 period. This turnover relates however to a very limited number of contracts in the EEA, rarely more than ten per year for each category. MSS contract amounts are usually between EUR 5 and EUR 20 million, although smaller and larger contract can also be observed. CSS contracts are usually larger than VTS ones[9].

38. The competitors of the parties active in the EEA include: Holland Institute of Traffic Technology B.V. ("HITT", The Netherlands), Selex Communications S.p.A ("Selex", Italia), Indra Systemas S.A. ("Indra", Spain), Kongsberg Norcontrol IT As ("Norcontrol", Norway), Transas Russia & CIS ("Transas", Russia), Thales Group ("Thales", France), Elbit Systems Ltd ("Elbit", Israel), Saab AB ("Saab", Sweden), Lockheed Martin Corp ("Lockheed Martin", USA), Raytheon Company ("Raytheon", USA) and Siemens AG ("Siemens", Germany). Most of these competitors are subsidiaries of large industrial groups for which the MSS business represents only a limited share of costs and revenues.

1. Market shares

39. The parties submit that given the limited number of tenders launched and contracts awarded each year, the duration of contracts which is usually of several years (around ten years) and the absence of customer brand loyalty, annual market shares are extremely volatile and would not properly reflect the relative position of the various suppliers. They submit therefore that the relevant market share data to analyse the market positions of the parties and their competitors should be based on a reference period of five years.

40. According to the information submitted by the notifying parties, the proposed transaction will give rise to affected markets both worldwide and in the EEA.

41. According to paragraph 15 of the Guidelines on the assessment of horizontal mergers the Commission may use historic data where as in the present case, market shares are volatile because the MSS sector and its sub-segments (CSS and VTS) are characterised by large and lumpy orders. In line with previous practice[10] the Commission considers therefore that a five-year period may be a relevant timeframe to assess the position on bidding markets such as the ones in the MSS sector.

42. Based on the reference period from 2005 to 2009, the parties' combined market shares in value are the following[11]:

2. Effects on competition

a. MSS as a whole and CSS

43. The new entity's market shares for MSS as a whole as well as for the sub-segment of CSS remain below [20-30]% both worldwide and in the EEA.

44. The market investigation carried out by the Commission confirmed that the proposed transaction will not raise competition concerns on an overall market for MSS or for the sub-segment of CSS.

45. None of the customers expressed any competition concerns. On the contrary, some respondents indicated that they see this transaction as a positive event in a market that will remain highly competitive in the EEA post-merger and which is characterized by rapid innovation.

46. In MSS as a whole and in the sub-segment of CSS the new entity will continue to face numerous competitors, such as Lockheed Martin, Raytheon, HITT, Selex, Indra, Norcontrol, Transas, Thales, Elbit, Saab and Siemens. Almost all these competitors are active both worldwide and in the EEA.

47. Many of these competitors are active since years and have an established reputation illustrated by a number of installed MSS in the EEA.

48. As mentioned above, most of these competitors are part of larger groups and consequently do not face the danger of rapid exit for financial reasons if they do not win a tender during a short to medium period of time.

49. The notifying parties were not able to estimate the market share of each of their main competitors. To their best knowledge, there are no independent market studies available for the market for MSS and its potential sub-segments.

50. The notifying parties have however provided sufficient information demonstrating that these competitors won against them several and important tender offers in the last five years. This argument was confirmed by the investigation.

51. The table below provides examples of some recent important CSS contracts won by the parties' competitors at the EEA-level and worldwide.

52. On an overall MSS market or CSS submarket, NewCo's limited market share and the presence of other significant competitors ensure that the proposed transaction will not lead to a significant impediment of competition.

b. VTS

53. NewCo's market shares in VTS in the EEA and worldwide are estimated between [3040]% and [50-60]% (see table paragraph 42).

54. On a yearly basis, the figures provided for the VTS bids in the last five years in the EEA confirm that there are indeed only a few VTS tenders per year and that market shares percentage points are greatly affected by a single win or loss of contract.

53. The parties indicate that their knowledge of the market is strongly affected by their own sales activities. Accordingly the figures provided may not contain tenders in which they did not participate and of which they never had any knowledge. According to the notifying parties, it is likely that there are some additional contracts of which they are not aware and that taking them into account would have the effect of diluting their market position.

54. The market investigation confirms that usually a MSS player is not aware of all VTS and CSS tenders. The market shares data submitted by the parties should thus be considered with caution.

55. Nonetheless as the parties seem to have won a particularly large part of the contracts in the EEA in the VTS sector in the last two years, the market investigation has looked in details whether this recent pattern reflected a high degree of market power or was only the result of statistical fluctuations or of specific elements unlikely to persist in the medium to long term.

Relevance of market shares to measure market power in VTS

58. The notifying parties submit first of all that market shares fluctuate significantly from one year to another. This fluctuation is also reinforced by the limited number of VTS tenders (about ten a year in the EEA) as a result of the limited number of ports requiring new systems.

59. Secondly, and more importantly, the VTS is a classic bidding market (like CSS). Buyers are sophisticated and oblige suppliers to engage in competitive bidding. In such a setting as long as there are effective competitors a high share of won contracts may not as such indicate market power of the successful bidders. It follows from the Commission's constant practice[12], that a high combined market share of the parties in such bidding markets is not alone an indicator of the market power that the merged entity will obtain post-merger.

60. Thirdly, the notifying parties indicate that at least in 2009 there is a statistic bias overestimating their market power. Out of the ten contracts awarded in 2009, five have been awarded in France and one in Germany: the French contracts have mostly been won by Sofrelog ([…] out of five) and the German contract has been won by AMS, which might stem from the fact that they had as national companies a slight competitive advantage over their competitors in the countries where the offers were made.

61. Indeed, although the markets are probably worldwide or at least EEA-wide, national companies have local expertise, local contacts and a thorough understanding of the local culture, which could partly contribute to explain the success of Sofrelog and AMS in 2009 in their respective home countries.

62. Fourthly, in 2010 the notifying parties are aware of six VTS contracts put out for tender in the EEA. Out of these six contracts, the parties have already lost […] and only won […]. Their 2010 market share as measured in contract wins will therefore be at most as high as in 2008.

63. It follows that, as discussed in paragraphs 39 to 41, the percentage of contract wins per year as such is not a reliable proxy to measure the market power of the parties.

Competitive constraint exercised by competitors

64. The market investigation showed that post-merger NewCo will continue to face several effective competitors in the VTS market.

65. At the EEA level, according to the data provided by the notifying parties, HITT, Norcontrol, Transas, Indra and Selex are currently active in VTS in the EEA and participate in tender procedures.

66. HITT is a global provider of solutions for marine and aviation applications. HITT encompasses the two business units Traffic and Hydrography & Navigation. HITT provides a wide range of solutions for marine and aviation applications, including hydrographics, precision navigation, port management, vessel traffic services, ground movement control and airside operations management. HITT’s products are applied and serviced in the Netherlands, Germany, Spain, India, Turkey, Ireland, Sweden, Denmark, Norway, Finland, the UK, Russia, Egypt, Singapore, Taiwan, China and South Korea. In 2009 HITT generated a total worldwide turnover of EUR 32.3 million.

67. Selex belongs to the Finmeccanica group of companies, an Italian group active in engineering, aerospace and defence. Selex focuses on the development and supply of advanced mission- critical communication, navigation and identification solutions to protect communities. Moreover, Selex provides critical national infrastructure solutions for government, civil and military applications. Selex encompasses the business units Avionics, Military & Space, Professional Communications and Telecommunications Operators. The company’s products include surveillance systems and traffic control systems. Selex generated orders valued at EUR 1 015.5 million in 2009. The Finmeccanica group generated a total worldwide turnover of EUR 18.2 billion in 2009.

68. Indra is a technology company and IT multinational headquartered in Spain. Indra is organized around six vertical markets: Security and Defence; Transport and Traffic; Energy and Industry; Telecom and Media; Finance and Insurance and Public Administration and Healthcare. In the segment Security and Defence, Indra provides global solutions based on in-house solutions to defence departments all over the world. Indra belongs to leading consortiums and participates in multinational programs of the sector. Indra’s solutions in this sector include protection, control and defence of sovereign air and land space and coastal and border surveillance. More than 2 500 km of land and see border are being surveyed by Indra systems. In 2009 Indra generated a worldwide turnover of EUR 2 513 million, thereof approximately EUR 682 million in the segment Security and Defence.

69. Norcontrol is a company predominantly active in Maritime Surveillance Systems. Norcontrol belongs to the Kongsberg group since 2005 and provides cutting edge technology for Vessel Traffic Service Systems (also known as Vessel Traffic Management and Information Systems), Automatic Identification System (“AIS”) networks and domain awareness solutions. Moreover, Norcontrol provides Coastal Surveillance Systems, River Information Systems and Offshore Collision Avoidance, Safety and Security Systems. The Kongsberg Maritime Division generated a total turnover of approximately EUR 763 million in the financial year 2009, its Naval Systems & Surveillance Division has won contracts in 2008 valued at approximately EUR 125 million.

70. Transas develops and supplies a wide range of software, integrated solutions and hardware technologies for the marine and aviation industry, including both onboard and shorebased applications. Transas distributes its products via offices in 110 countries. Transas’ annual turnover exceeded EUR 136 million in 2008.

71. Moreover, in spite of less contract wins as compared to the parties, the market investigation has confirmed that both the competitors themselves and customers regard those competitors as strong and credible alternatives to the parties.

72. All competitors that replied to the market investigation, with one exception[12], consider that they (i) are as competitive as Sofrelog and AMS and will remain as such post-merger, (ii) are able to win in the EEA bids against them, (iii) are in the position to react if NewCo would increase prices post-merger, and (iv) will not exit the market.

73. All these competitors are also active to a significant extent outside Europe. Consequently, even if they do not win bids during a limited period of time at the EEA level, it is unlikely that they will exit the market. They will thus continue to exert a competitive pressure on NewCo by continuing to submit alternative offers.

74. Finally, the existence of strong competitors has been also validated by all customers that replied to the market investigation. These customers (mainly public authorities) indicated that post-merger they will still have credible alternatives other than NewCo.

75. The finding that the competitors in question are strong players and credible alternatives to the parties is also confirmed by an analysis of the contracts awarded at the worldwide level where the parties have lost a significant number of VTS contracts to their competitors in the last years.

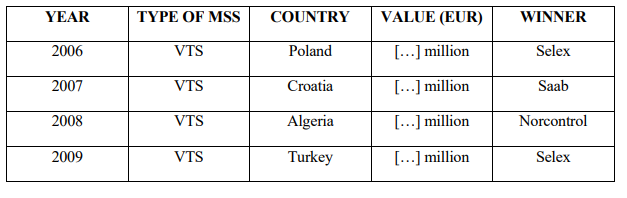

76. In particular, the parties recently lost important contracts, such as Angola in 2007 (EUR […] million), Algeria in 2008 (EUR […] million), Croatia in 2008 (EUR […] million), and Turkey in 2009 (EUR […] million)[13].

In particular during the last three years (2007-2010), the values of the VTS contracts which the parties have won are limited compared to the values of some VTS contracts they have lost to their competitors. In this respect, the parties did not win any contracts worth more than EUR 5 million, while, for instance, the VTS contract won by Norcontrol in Algeria in 2008 has been estimated at EUR […] million. This ability of NewCo's competitors to win important VTS contracts against the parties outside the EEA suggests that they are also credible competitors that are able to effectively compete with the parties within the EEA.

64. It follows that post merger the competitive constraint from competitors on the parties will continue to be strong.

65. The market investigation has indicated that most companies active in the MSS market offer comparable solutions. Hardware (radars, sensors…) is outsourced and companies focus on software and services. Respondents have generally indicated that they consider their solutions competitive compared to those of the parties.

3. Barriers to entry

a. Barriers to enter the MSS

80. The notifying parties consider that entering the MSS market is possible for certain type of players, such as defence industry players who have experience in the field of electronic components such as radars, sensors or sonar systems. In particular, this applies to subsystem suppliers that have already worked in a consortium with suppliers of integrated systems. For such actors, the notifying parties claim that it would be possible to successfully enter the market within 1-2 years. However they also admit that there might be some entry barriers for potential entrants who have no prior relevant experience in the technology used in MSS.

81. The market investigation has confirmed that strong competitors of the parties such as Saab, Selex, Thales and Indra are valid examples of companies that have relatively recently entered MSS market first by winning local contracts and then becoming successful within a few years.

82. In the notifying parties' view, the US competitors such as Lockheed Martin or Raytheon are also likely to compete more forcefully in the EEA market within the next few years. Both companies are strong competitors in the US and according to the notifying parties mention that they strive to enlarge their presence also outside the US.

83. It follows from the foregoing that entry in the relatively small MSS sector in particular for players active in much larger neighbouring defence markets as well as entry from third country players is possible and could defeat any attempt by NewCo to exercise market power.

b. Barriers to enter the VTS market

84. According to the notifying parties, once a new player enters the MSS market, it can benefit of its position on one of its segment (CSS for instance) to enter in the other one (VTS).

85. They explain that players often enter the segment of one type system before also supplying the other type of system. CSS manufacturers can use the same components and their existing software which only needs to be slightly modified with respect to the parameters in order to fit the VTS requirements.

86. Most of the respondents pointed out the need of extensive knowledge and experience in VTS in order to participate in tender procedures and compete with the existing players. Some competitors also indicated that references in previous VTS contracts, possibly in the same country, are often required by customers. In the absence of reference in one country, successful entry in this country was considered as more difficult, although not impossible, and subject to more aggressive bidding.

87. A majority of customers and competitors confirmed however also that for a player already active in the more complex and lucrative CSS segment it is relatively easy to enter the more standardised VTS segment. This is evidenced first by the fact that virtually all players active in CSS are also active in VTS. Secondly, both Indra and Selex provided CSS before they turned to VTS[14].

88. It follows that players currently active in the CSS segment are relatively easily able to enter the VTS market.

Buyer power

89. The constraint exerted on the parties by their actual competitors is reinforced by the buyer power of their customers, which are sophisticated players in a market characterized by bidding processes.

90. Public authorities, government agencies and similar bodies fulfilling public duties and responsibilities are the main source of demand for CSS and VTS.

91. According to the notifying parties, these customers are often sophisticated and educated, knowing the market and the standard they demand.

92. Moreover, the system of tender procedures allows them to exert buyer power. These tender procedures typically contain several competitive rounds. According to the parties, the tender procedures lead to fierce price competition as they are very transparent with intense negotiations with all bidders before choosing one provider. Each customer can directly compare all competitors and their respective offers. Tenders are generally conducted openly throughout the world and there is frequent exchange and communication among port operators and government agencies.

93. Due to the limited demand, customers are free to generate additional competition by asking and comparing the costs for on the one hand integrating a new system and on the other hand refurbishing an existing system or providing individual spare parts.

94. Moreover, buyer power seems also reinforced by the fact that there is only limited demand for MSS, due to the limited number of ports and coast lines requiring such systems.

95. Finally, none of the main customers of the notifying parties that have replied to the market investigation expresses any concern on the transaction.

4. Conclusion on the competitive assessment

96. It follows from the foregoing that in MSS and CSS, but also in the VTS sector, where the parties have relatively high market shares as expressed in contract wins, the creation of NewCo will not lead to a significant impediment of competition. This is essentially because (i) the markets concerned are bidding markets with sophisticated buyers (mainly public authorities), (ii) there is a large number of strong and credible competitors who compete with the parties not only in the EEA but also worldwide and (iii) in any event countervailing entry coming from the CSS segment or from outside the EEA would be able to defeat attempts to raise prices in VTS.

VI. CONCLUSION

96. For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation.

[1] OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2COMP/M.4160 - ThyssenKrupp/EADS/Atlas, 10 May 2006.

3 See paragraphs 62 to 73 of the Commission's Consolidated Jurisdictional Notice under Council Regulation (EC) n.139/2004 on the control of concentrations between undertakings.

4 Turnover calculated in accordance with Article 5(1) of the Merger Regulation.

5 MSS are usually not used for specifically military missions, but may be used by military authorities, such as Ministries of Defence. MSS that serve military purposes are rare. Neither Sofrelog nor AMS produce such products.

6 However some important VTS contracts exceed these estimates.

7 COMP/M.4160 - ThyssenKrupp/EADS/Atlas, 10 May 2006, paragraph 10.

8 Vessel Traffic Monitoring and Information System ("VTMIS") Directive 2002/59, OJ L 208/10.

9 See paragraph 21.

10 COMP/M. 3803 – EADS / Nokia of 28 July 2005.

11 The total market value is based on the best estimates of the notifying parties.

12 See for example COMP/M.1940 - Framatome/Siemens/Cogem/JV, 13 December 2000, COMP/M3653 - Siemens/Va Tech, 20 July 2005, and COMP/M.3148 - Siemens/Alstom Gas and Steam Turbines, 10 July 2003.

13 In particular, this competitor refers to the possibility of being prevented from purchasing its radars from Atlas as post-merger Sofrelog will also have access to Atlas' radars and become more price competitive. However, the competitor also emphasized that prior to the merger he had already tried to source its radars from Atlas, yet unsuccessfully and thus was sourcing them from another company at a higher price.

14 As the notifying parties do not have visibility over all contracts which have been awarded, the list of contracts provided by them covers only those contracts for which Sofrelog and AMS bid and not any contracts that have been won by competitors without participation of one of the parties. Thus the notifying parties claim that overall their competitors have won more contracts outside the EEA than the ones provided in their submission: for instance according to the notifying parties Transas won recently 9 contracts in which the parties were not able to participate.

15 According to the notifying parties, Indra and Selex are very strong in CSS, with market shares of 33% and 29% on an EEA-wide market, respectively, over the last five years.