Commission, October 7, 2011, No M.6281

EUROPEAN COMMISSION

Judgment

MICROSOFT/ SKYPE

Dear Sir/Madam,

Subject: Case No COMP/M.6281 - Microsoft/ Skype

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041

1. On 02.09.2011, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the undertaking Microsoft Corporation, USA (hereinafter "Microsoft"), acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of the undertaking Skype Global S.a.r.l, Luxembourg (hereinafter "Skype"), by way of purchase of shares2. Microsoft and Skype are designated hereinafter as "parties to the notified operation" or "the parties".

I. THE PARTIES

2. Microsoft is active in the design, development and supply of computer software and the supply of related services. The transaction concerns Microsoft's communication services, in particular the services offered under the brands "Windows Live Messenger" (hereinafter "WLM") for consumers and "Lync" for enterprises.

3. Skype offers software for communications over the Internet. Skype's software enables text (or "instant messaging" (hereinafter "IM")), voice and video communications.

II. OPERATION AND CONCENTRATION

4. Pursuant to a Purchase and Share Agreement signed on 09.05.2011, Microsoft will acquire 100% of the outstanding shares and therefore sole control over Skype. The notified operation thus constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

III. EU DIMENSION

5. The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 2 500 million3. Furthermore, in each of Germany, Italy and the UK the combined aggregate turnover of the two undertakings concerned is more than EUR 100 million and the aggregate turnover of each of the undertakings concerned is more than EUR 25 million in each of these three Member States. Finally, each of Microsoft and Skype has an EU-wide turnover in excess of EUR 100 million and they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

6. The notified operation therefore has an EU dimension within the meaning of Article 1(3) of the Merger Regulation.

IV. ASSESSMENT

7. The notified operation takes place in the Internet consumer and enterprise communications ("consumer and enterprise communications") markets4.

8. The parties provide software which allows users to communicate using various means of communication such as for instance presence/IM, voice call, video call, and collaboration tools in enterprises (video conference, edit/share of documents and others) over various platforms (mainly Personal Computers (hereinafter "PCs")5, smartphones and tablets). Therefore the notified operation requires an assessment of horizontal overlaps (see paragraphs 96 and following and paragraphs 177 and following).

9. Microsoft is also active with products, such as operating systems (hereinafter "OS"; with for instance "Microsoft Windows") or commercial office suites (with "Microsoft Office") which work together with communications software. The notified operation therefore requires an assessment of its potential conglomerate effects (see paragraphs 133 and following, paragraphs 203 and following.

A. Relevant markets Product markets

10. The notified operation concerns the consumer and enterprise communications markets. Both consumers and enterprises rely on services which integrate a number of communications functionalities (mainly IM, voice and video calls), but according to the parties, their needs differ. Whereas consumers approach communications from a social perspective, enterprises use communications from a task-oriented perspective.

11. Although a trend exists towards “consumerization” of enterprise communications products6, the parties consider that communication services remain different between these two categories of users in particular in terms of prices or features.

12. The Commission agrees with the parties for the following reasons:

13. First, with regard to the difference in terms of prices, enterprises (in particular large companies) buy communication services sometimes at very high price, whereas consumers are less willing to pay for a communication service offered on the Internet. According to an internal Skype document, only 6% of Skype’s connected users (most of them are consumers and not enterprises) are "paying users"7 and [> 75]% of its users would cease using its free service if it started charging for it.

14. Second, with regard to the difference in terms of features, enterprise communications services are more sophisticated and reliable than consumer communications services. Enterprises do not have the same service requirements and do not tolerate lower service quality as consumers do. Redundancy and robustness, security, reliability, ancillary functionality, management and support requirements are higher for enterprise communications services. For example, enterprise communications services offer additional features in terms of collaborating tools, such as the possibility to share and edit a document in real-time from different places. As regards voice calls, enterprise-grade communications services require features and functionality which are not available in consumer-grade communications services, such as park/hold, mute, simultaneous ringing or integrated voicemail.

15. Finally, there are only a limited number of providers of communications applications designed for both consumers and enterprises (for instance by Microsoft and to some extent Google). Others, including Skype, offer a communication application which is mainly targeted at consumers, even though it may also be used by some small businesses.

16. It appears therefore, that enterprise communications services and consumer communications services form two distinct markets. This conclusion is supported by the parties and a large proportion of the respondents to the market investigation conducted for the purpose of this case (hereinafter "the market investigation"), in particular the original equipment manufacturers8 (hereinafter "OEMs") which have knowledge of both the consumer and enterprise communications services markets. Three out of the four OEMs which replied to the market investigation consider that there is not one overall market for online communications services including consumer and enterprise communications9. As explained by one OEM, consumer communications services and enterprise communications services have two different business models: "for enterprise unified communications services, the providers are paid from users by customizing their services, while for consumer communications services, the providers offer their services for free and get revenue through advertising or other indirect channel".

17. Considering the above, the Commission takes the view that consumer communications services and enterprise communications services form two distinct product markets that have to be assessed separately.

1. Consumer communications services

18. The parties submit that consumer communications services form a single product market because consumers demand a user experience which integrates a range of functionalities (IM, voice and video calls) across all platforms (PCs, smartphones, tablets) and OSs. This user experience is illustrated by the growth of social networking sites such as Facebook, in terms of number of users but also in terms of time spent on them. Google has recently integrated its traditional communication services ("Google Talk" for voice, "Gmail" video chat for video, "Google chat" for IM/presence and Gmail for email) into a broader user experience called "Google +". Google + attracted around 20 million users in the first three weeks after its launch10.

19. The parties therefore argue that a further segmentation according to functionality, platform and/or OS does not reflect the current and foreseeable market reality. They explain that consumer communications services are undergoing rapid development and that the competitive landscape is poised to change very significantly in the next three to five years. According to the parties it would be artificial to distinguish between each individual communications' functionality or according to platform and/or OS.

20. The Commission, which is required by the present decision to assess Internet consumer communications services for the first time, considers that from a demand-side substitutability point of view, a further segmentation of the consumer communications market may be appropriate as today a majority of European consumers do not generally have access to all functionalities across all existing devices and OSs.

a) Segmentation of consumer communications services by functionality

21. The main functionalities of consumer communications services are IM, voice calls and video calls.

22. IM is a form of real-time short text messaging. IM generally includes presence which is the ability to detect other users’ availability (i.e. whether they are online, absent, or busy).

23. Voice calls refer in the present case to voice over Internet protocol (hereinafter "VoIP") calls and mean the delivery of voice services over networks based wholly or partly on Internet protocol (hereinafter "IP"). VoIP calls differ technically from public switched telephone network (hereinafter "PSTN") calls. PSTN is the network of the world's public circuit-switched telephone networks. It consists of telephone lines, fiber optic cables, microwave transmission links, cellular networks, communications satellites, and undersea telephone cables, all inter-connected by switching centres, thus allowing any telephone in the world to communicate with any other.

24. Video calls enable users from at least two or more locations to interact using two-way synchronized video and voice transmissions. To allow video calls, a device requires a webcam11 and microphone functionality, which is often already embedded in numerous devices or can be added at a low cost.

25. The parties consider that IM, voice and video calls are not viewed and used as stand- alone services, but are increasingly used as an adjunct to other activities, such as social networking. Indeed as indicated in a number of studies12, the Commission notes that consumers increasingly demand a user experience which integrates a range of communication functionalities. In this respect, the success of social networking websites and similar online social environments such as Facebook and Google+ are illustrative of such a trend for broad services for consumer communications services.

26. Furthermore, taking into account demand-side substitutability, a consumer can switch easily, immediately and without cost between the three main types of services (IM, voice and video calls). For instance, a consumer can start a conversation by IM, then turn to the voice or video call modality to continue the conservation; moreover, consumers who have a PC with a camera and voice functionality can switch from one modality to the other whenever (s)he likes and without any need for interrupting the conversation.

27. In addition, with regard to the supply-side substitutability most of the providers of consumer communications services offer the whole range of functionalities.

28. The Commission considers from assessing the evidence from the market investigation that consumer communications services should not be distinguished according to functionality. For instance IM is not perceived as a stand-alone communication service, but as part of a broader market. IM should not therefore constitute a separate product market13. A large majority of respondents also state that voice and video calls should not be regarded as constituting different product markets14. One OEM explains that "most consumer communications clients have grown in functionality to the point where they offer some capabilities across many of the multiple functional categories". This is supported by the fact that Microsoft, Skype, Google, Apple, Facebook, Yahoo!, and AOL all offer the three main functionalities of consumer communications. One competitor of the parties underlines also that "almost every competitive product offers the same spread of features - voice, video, text - in order to remain competitive. It would be difficult to split this market into smaller chunks without serious functionality overlap".

29. However, for the purpose of the assessment of the present transaction, it can be left open whether the market for consumer communications services needs to be segmented according to functionalities (IM, voice calls, video calls), as the proposed transaction does not give rise to any competition concerns even on the narrowest possible definition of the relevant product markets.

b) Segmentation of consumer communications services by platform

30. The parties submit that most consumer communications services can increasingly be used on all types of platforms: PCs, smartphones, tablets, but also gaming consoles and TVs15.

31. According to the parties the way platforms are purchased and used is changing. There is a significant growth in sales of smartphones and tablets whereas the sales of PCs are declining.

32. PCs have historically been the predominant platform for communication on the Internet. Smartphones and tablets are however increasingly used by consumers, in particular in order to communicate over the Internet. Forecasts16 show that sales of smartphones and tablets in Western Europe are expected to grow very rapidly while sales of laptop and desktop PCs are expected to stagnate. By 2010, sales of smartphones and tablets already exceeded those of PCs, and for 2011 it is estimated that sales of smartphones and tablets will exceed the sales of PCs by a factor of 2:1.

33. The parties submit that communications services have to be interoperable across platforms. They claim that Skype is "platform agnostic" and that consumers can multi- home17 because they increasingly expect to be able to move seamlessly between platforms. According to the parties, consumer communications are therefore used on a multi-platform basis and should be assessed as a single product market.

34. With regard to segmentation according to platforms, the market investigation is not conclusive. Only a small majority of respondents agrees with the parties' view that a segmentation of consumer communications services by platform is not appropriate18.

35. The Commission observes that, from a demand-side perspective, consumer communications services are different in terms of features and quality on the different types of platforms.

36. Furthermore, many European consumers are not equipped with all platforms. Today European consumers mainly use their PCs to communicate over the Internet. The parties indicate that there is limited public data available regarding the percentage of PC users who also use smartphones and/or tablets in the EEA. A recent survey however indicates that 35% of US adults own a smartphone, and 78% of these smartphone owners also have a laptop PC19. Assuming that the proportion in the EEA is not substantially different today, only approximately one third of EEA customers have the possibility to substitute a PC by a smartphone in order to communicate over the Internet.

37. In any event, for the purpose of the assessment of the present transaction, it can be left open whether the market for consumer communications services needs to be segmented according to platforms (PCs, smartphones, tablets etc.), as the proposed transaction does not give rise to any competition concerns even on the narrowest possible definition of the relevant product markets.

c) Segmentation of consumer communications services by operating system ("OS")

38. Within each platform, consumer communications services are used in connection with the OS which is installed on a device. An OS is a "system software" which controls the basic functions of an electronic device (mainly PCs, smartphones and tablets) and enables the user to make use of such an electronic device and run application software on it20. Major OSs are Windows (and its OS for mobile phone, Windows Phone 7), Linux, Apple's Mac and iOS, Android, Blackberry, Nokia N900, Symbian and Xbox21.

39. The parties stress the cross-platform availability of Skype. Skype enables IM, voice and video calls from, to and between, all the above-mentioned OS with the exception of Windows Phone 722, BlackBerry OS, and Xbox23.

40. The Commission considers, however, that a number of consumer communications services are still not available on all OS24. For instance Windows Live Messenger (hereinafter "WLM") has limited cross-platform availability. The complete range of WLM (mainly IM, voice and video calls) is mainly available on Windows and Mac OS PCs. The WLM functionality on other OSs (including other Microsoft OSs) is limited. For example, only the IM and presence functionalities of WLM are available on mobile platforms, including the mobile OS of Windows, Windows Phone 7.

41. Furthermore, a Windows user cannot switch to Apple's communications services (FaceTime, iMessage or iChat). Therefore it is impossible today for all consumers to switch between all existing consumer communications services as the choice is technically limited by the OS installed on the device.

42. For the purpose of the assessment of the present transaction, it can however be left open whether the market for consumer communications services shall be segmented according to OSs (Windows, Mac, Linux, Android etc.), as the proposed transaction does not give rise to any competition concerns even on the narrowest possible definition of the relevant product markets.

d) Conclusion

43. For the purpose of the assessment of the present transaction, the exact product market definition as regards consumer communications services can be left open since the proposed transaction does not give rise to any competition concerns even on the narrowest possible product markets considered.

2. Enterprise communications software services ("Entreprise communications services")

44. In a previous Commission decision enterprise communications (also called "unified communications" or "UC") services were defined as "products and services […] used by business customers of all sizes to improve workgroup and collaborative communications, and […] designed to provide a simple and consistent user experience across all types of communications (telephone, fax, email, voicemail, voice and videoconference, instant messaging, etc.)"25.

45. The Commission recognised a growing trend towards a UC market, but concluded that such an overall market did not yet exist.26 In Cisco/Tandberg27, the Commission considered instead that video communications solutions form a distinct market within the wider enterprise communications services sector. The Commission further distinguished between (i) dedicated-room solutions; (ii) multi-purpose room-based solutions; and (iii) executive office/desktop communications systems, which include PC-based solutions. Within the executive office/desktop communications systems, a narrower segmentation between software-based solutions and hardware-based solutions was also considered. However the Commission left open the question of the exact delineation of the product market28.

46. In the present case, the parties submit that the relevant product market for enterprise communications services includes not only video or videoconferencing calls, but a wider range of functionalities as for instance advanced telephony, unified messaging – email, fax, voice messaging combined, web, voice and videoconferencing, IM/presence, collaborating tools.

47. The parties take the view that a provider of enterprise communications services must provide all or most of these features. The majority of suppliers of enterprise communications services indeed provides a broad range of functionalities, including voice and video calls, video conferencing, IM, and collaborative tools. The parties also refer to studies that define the enterprise communications services market broadly29.

48. Furthermore, the parties submit that a segmentation of the enterprise communications services market according to the type of platform or OS is not appropriate as all services are accessible through common user interfaces on desktop and mobile devices using voice or tactile controls.

a) Segmentation of enterprise communications services by functionality

49. With regard to a possible segmentation according to the type of functionality, a small majority of respondents to the market investigation tends to consider that such segmentation is warranted30. These respondents claim for instance that video calls and voice calls should not be assessed as a single product market. Furthermore, a significant number of customers of the parties which replied to the market investigation purchase communications services from several providers. This could indicate a specialization in the functionalities provided, in particular for voice calls where telecom operators provide their own solutions.

50. Other respondents describe a trend where computer and telephony technologies create new products, for instance for services using internet protocol (IP) technology. As a consequence of this ongoing convergence, the traditional distinctions between data and voice, between hardware and software, and between the various distinct products and services that are offered by enterprise communications companies are blurring.

51. For the purpose of the assessment of the present transaction, it can be left open whether the market for enterprise communications services needs to be segmented according to functionalities (advanced telephony, unified messaging – email, fax, voice messaging combined, web, voice and videoconferencing, IM/presence, collaborating tools etc.), as the proposed transaction does not give rise to any competition concerns even on the narrowest possible product markets considered.

b) Segmentation of enterprise communications services by platform

52. With regard to a possible segmentation according to the type of platform, a large majority of respondents to the market investigation tends to consider that such segmentation is appropriate. The respondents note in particular that a full range of enterprise communications services is not available on all platforms (PCs, smartphones, tablets)31.

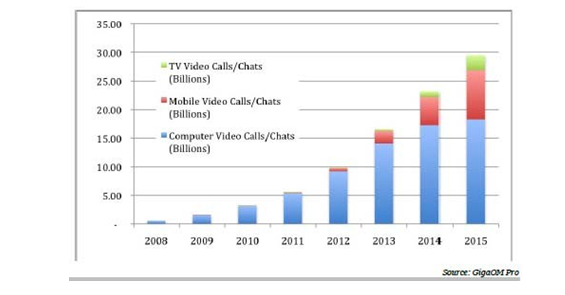

53. From a supply-side perspective substantial investment is required in order to provide full enterprise communications solutions on every electronic device and the proportion of people using at least two devices is not very high (about 20%).

54. The Commission takes the view that the absence of availability of all enterprise communications services on all existing platforms is an important argument to take into account when considering the existence of a further segmentation of the product market. On the other hand, the use of tablets and smartphones is increasing within the enterprise sector and the existence of a broader product market including PCs, smartphones and tablets cannot be excluded in a foreseeable future.

55. For the purpose of the assessment of the present transaction, it can be left open whether the market for enterprise communications services needs to be segmented according to platforms (PCs, smartphones, tablets), as the proposed transaction does not give rise to any competition concerns even on the narrowest possible product markets considered.

c) Segmentation of enterprise communications services by OS

56. The Commission considers that it is not as easy for enterprises as it is for consumers to change an existing OS installed on their platforms. Furthermore, the Commission takes the view, confirmed by the replies of many competitors of the parties, that switching between OSs is difficult. Indeed, building cross-OS enterprise communications services is costly and there is a lack of interoperability, contrary to the parties' claim (see paragraph 48 above)32.

57. However, for the purpose of the assessment of the present transaction, it can be left open whether the market for enterprise communications services needs to be segmented according to OSs, as the proposed transaction does not give rise to any competition concerns even on the narrowest possible product markets considered.

d) Segmentation of enterprise communications services by size of customers

58. An additional segmentation of the enterprise communications services according to the size of the enterprise has also been considered in the market investigation.

59. Although the parties submit that such a segmentation is not relevant, the Commission considered that prima facie a distinction between small (less than 50 employees), medium (50 to 250 employees), and large (more than 250 employees) companies could be relevant due to their different needs and expectations in terms of reliability and security for enterprise communications services33.

60. A large majority of the respondents to the market investigation consider that a possible segmentation according to the size of customers should be considered34. One OEM summarizes their view by saying that "some communication capabilities are common to all, email, telephony, fax, etc. Others, such as video, are more applicable for medium to large enterprises. Telepresence is probably only applicable to very large enterprises".

61. The Commission takes the view that this segmentation mainly coincides with the segmentation by type of functionality. SMEs have other and more limited needs for communications services than large companies. The Commission also notes that there are products and services mostly suited for large companies while other products are particularly suited for SMEs. The market investigation confirms for instance that the light version of Lync, Lync Online is perceived as a product for SMEs.

62. However, for the purpose of the assessment of the present transaction, it can be left open whether the market for enterprise communications services needs to be segmented according to the size of the company, as the proposed transaction does not give rise to any competition concerns even on the narrowest possible product markets considered.

e) Conclusion

63. For the purpose of the assessment of the present transaction, the exact product market definition as regards enterprise communications services can be left open since the proposed transaction does not give rise to any competition concerns even on the narrowest possible product markets considered.

Geographic markets

64. The parties submit that consumer and enterprise communications markets are at least EEA-wide if not worldwide. The software-based nature of the services does not require local support and sales networks. The communications services are provided and sourced globally by a majority of market players, and there seem to be no legal or technical standards that limit the offer or the use of these services.

65. The market investigation indicates that the geographic markets for consumer and enterprise communications are at least EEA-wide and most of the respondents state that they consider the geographic market as worldwide for the reasons put forward by the parties35. A majority of respondents considers in particular that there are no legal and technical barriers that restrict the use or trade of communications services worldwide. Moreover communications services are generally perceived as not different in terms of quality, price, and features worldwide, with the exception of some geographic area. Many respondents to the market investigation consider also that users' habits in communications services are identical within the EEA and worldwide.

66. For the above reasons, the Commission considers that the geographic markets for consumer communications services are at least EEA wide. In addition it should be mentioned that suppliers of consumer communications provide their services on a global level with limited differentiation in the quality and the features in the EEA – and to a lesser extent worldwide36. Regarding prices, most of the services provided are free – irrespective of the location of the consumer.

67. For the above reasons, the Commission considers that the geographic markets for enterprise communications services are at least EEA-wide. This is consistent with the Commission's precedents in its decisions Avaya/Nortel Enterprise Solutions (2009)37 and Cisco/Tandberg (2010)38. The Commission has received no evidence during its market investigation which would require changing the assessment in this regard.

68. Nevertheless, for the purpose of the assessment of the present transaction, the exact geographic scope of consumer and enterprise communications markets (and any potential submarkets) can be left open as the notified operation does not give rise to any competition concerns even on the narrowest possible geographic market (i.e. EEA).

B. Competitive assessment

Consumer communications services

1. Market characteristics

a) Overview on consumer communications services

69. Consumer communications services are characterised by two general trends: they constitute nascent and growing sectors and their use on platforms is changing.

- nascent and growing sector

70. With regard to IM, the use of IM as a stand-alone product on PCs is in decline, but mobile IM use and IM use as an adjunct to other products and functionalities (such as social networking) has grown and continues to grow significantly. For example, it is expected39 that the number of mobile IM users will exceed 1.3 billion by 2016 (triple the number of users in 2010). Further, the use of sites such as Facebook, Google+, LinkedIn and Twitter has more than doubled since January 2009. It is also expected that the number of global IM accounts (both consumer and business) will continue to grow, with an increase from 2.4 billion active accounts in 2010 to over 3.5 billion by 201440.

71. Voice calls grew rapidly over the last 20 years, driven in part by market liberalization and the emergence of VoIP as an alternative to time division multiplex (“TDM”) services. The parties refer to an increasing number of market participants offering VoIP calling services, including Viber, Google, Facebook, Mail.Ru, AOL, Fring, Trillian, Nimbuzz and Miranda (in addition to Skype and WLM)41.

72. Video calls are the most dynamic functionality within the consumer communications services. It is expected that the number of video calls will increase from 3.2 billion in 2011 to 29.6 billion in 201542.

- shift away from PCs to other devices

73. Consumer communications services are shifting away from PCs to smartphones, tablets, and other Internet connected devices such as IP telephones and videotelephones. It is expected that already in 2011 smartphone and tablet sales will overtake those of PCs.

74. This general trend has been estimated in particular for video calls. It is expected that the contribution of non-PC-based video calling to overall growth in the short- to medium-term is substantial: a 14-fold increase, to almost 40% of overall consumer video traffic by 201543.

b) Prices

75. Consumer communications services are mostly offered for free. Only few voice calls services are charged, such as calls from and to PSTN for instance, but IM, voice and video calls are delivered free of charge by the market players.

76. The parties have provided an internal document of Skype revealing that [>75] % of the users of its Skype Manager product44, which are mainly private customers, would cease to use the product if Skype started charging for its use.

77. The Commission takes the view that this demonstrates high price sensitivity. Success of providers of consumer communications services depends very much on whether they are free of charge. If a provider starts charging for a service which was used for a long time free of charge and there exist alternative services offered for free, it can be expected that consumers would immediately switch to these competing services.

c) Market shares

78. Market shares only provide a limited indication of competitive strength in the consumer communications services markets. As explained above in paragraphs 70 to 72, consumer communications services are a nascent and dynamic sector and market shares can change quickly within a short period of time. Furthermore, almost all communications services are offered free of charge.

79. For the purposes of the present decision, the parties have provided their best estimates of market shares based on volume (i.e. unique users). A unique user is, for a specified period of time (i.e. a month in the present decision), an individual that has actively used a given service.

80. In the present case, the Commission considers that market shares in volume constitute better indicators than market shares in value as most of the consumer communications services are provided free of charge.

d) Innovation

81. Since consumer communications services are mainly provided for free, consumers pay more attention to other features. Quality is therefore a significant parameter of competition.

82. The parties submit that there has been a significant research and development trend over the last five to ten years towards digitization of traditionally analogue communications (such as voice and video). This results in a significant expansion in the number and types of platforms supporting consumer communications services. The parties also state that the markets are characterised by innovation in video codecs45 that are able to accommodate differing amounts of available bandwidth.

83. The innovation cycles in these markets are short. As a result, software and platforms are constantly being redeveloped. Innovators generally enjoy a short lead in the market.

84. The Commission considers that competition in the consumer communications services markets is driven by innovation. The high degree of innovation in these markets is proven by the pace at which new innovation has been introduced in the past, such as group video, mobile video and HD video, or PC-to-PSTN, PSTN-PC calls.

e) Barriers to entry and expansion

85. The parties submit that some barriers to entry in the markets for consumer communications services can be observed.

86. The absence of a strong consumer brand may represent an impediment to entry. This is demonstrated by the fact that one economic rationale of the notified operation is […]. Furthermore, new entrants have to accommodate growing consumer demand for cross-platform applications. New entrants have to produce versions of their communications applications for several platforms. The aspect of revenue generation could also constitutes a barrier to entry to these markets where most services are delivered free of charge. As Skype's experience illustrates, it is difficult to monetize consumer communications products in an environment where competitors provide them for free (and cover their costs using revenues generated in other markets).

87. However, these possible barriers to entry were not considered as significant by respondents to the market investigation. On the contrary, it should be mentioned that a majority of respondents to the market investigation consider that barriers to entry to the markets for consumer communications services are low46. This can be explained inter alia by the fact that consumers can download the software of an alternative provider easily and for free.

88. With regard to the cost of setting up a new service, the parties have provided a case study with data for three consumer communications companies (Fring, Tango and Tinychat)47. The results of this study are summed up in the following table:

Capital investment | EUR 750 000 – EUR 9,7 million |

Estimated time to bring product to market | 8 – 24 months |

Size of user base one year after launch | 2.4 million – 17 million |

89. The Commission notes that these data indicate that setting up a new service in consumer communications services does not entail high costs.

90. The Commission observes also several recent entries48 into the consumer communications services markets. The example of Viber Media ("Viber") shows that it is possible even for a small company to enter the market and attract a significant number of users within a short period of time. Viber was created in February 2010 and launched its free voice calls application for iPhone in December 2010. Like Skype, Viber for iPhone enables users to make free calls to other Viber users over 3G and wi- fi networks, but it does not require any registration. After launching on 2 December 2010, Viber reported that its application had been downloaded over 1 million times in its first three days. Within two months 10 million people had downloaded the application. In May 2011 Viber had more than 15 million users worldwide and Viber is continuing to improve its application49.

91. Respondents to the market investigation also stress the existence of network effects in the consumer communications markets as a barrier to expansion. They consider that the more users a provider of communications has, the better its chances are to expand its user base50.

92. However, the network effects are mitigated by the fact that most consumers of communications services make the majority of their voice and video calls to the small number of family and friends that make up their so called "inner circle". According to Facebook data, users engage in regular two-way interaction with four to six people51. Therefore, it is not difficult for these groups to move between communications services. Moreover the Commission observes that consumers multi-home to a certain degree among various providers of consumer communications services52.

93. The existence of low barriers to expansion is illustrated by the fast growth in terms of active users of recent new entrants in the consumer communications services markets, in particular Facebook. Facebook's monthly unique users have grown from 62.2 million in January 2009 to 157.4 million in April 2011.53 Other new entrants met immediate success, such as Viber (see paragraph 90 above), but also Fring and Tango54.

94. Moreover, as described in paragraphs 70 to 72, the consumer communications services are a nascent and rapidly growing sector which should facilitate entry and expansion into the consumer communications services markets.

95. As a result of the above, the Commission takes the view that the barriers to entry and expansion to the markets for consumer communications services are not high.

2. Horizontal assessment

96. Both Microsoft's WLM and Skype offer consumer communications services (IM, voice calls and video calls). However, the parties' activities mainly overlap on Windows-based PCs and to a lesser extent on Mac-based PCs, Linux-based PCs and the mobile platforms iOS and Android.

97. WLM provides mainly IM, voice and video calls55. WLM does not support video communications among more than two users and does not enable users to make calls to the PSTN or public mobile networks. Moreover, the mobile version of WLM does not enable users to make voice and video calls.

98. Skype provides mainly IM, voice and video calls56. The parties submit that Skype's brand is closely associated with voice and video communications and to a lesser extent with IM communications. Skype enables users to make voice calls which terminate on the PSTN through its paid application SkypeOut57.

a) Market shares

99. As explained in paragraph 78, market shares are not the best proxy to evaluate the market power of providers of consumer communications services and they only give a preliminary indication of the competitive situation in these dynamic markets.

100. The parties have provided their best estimates of their market shares and their main competitors' on each segment of the consumer communications services market, for the EEA and worldwide.

101. WLM and Skype have their strongest position in Windows-based PCs. In June 2011, around [90-100]% of WLM users logged in via a Windows-based PC ([0-5]% via Mac OS and [0-5]% via Windows mobile). In May 2011, around [70-80]% of Skype users logged in via a Windows-based PC ([10-20]% via iOS, [5-10]% via Mac OS and [0- 5]% via Android).

102. Therefore the following market shares for the markets where the parties' activities overlap correspond to a 'worst-case scenario' since they have been provided on the narrowest product market considered, which is the market for consumer communications services (segmented by type of functionality) delivered on Windows- based PCs. On the other markets where the parties' activities overlap, that is the markets for consumer communications services on Mac-based PCs and the mobile platform iOS, it can be excluded that the parties market position is stronger as Apple offers its services iChat (IM) and Facetime (video calls) which are pre-installed on its platforms. On the corresponding markets for Linux-based PCs and Android the usage of WLM is close to [0-5]%.

- IM:

Provider of IM | Market shares June 2011 EEA-wide58 | Market shares June 2011 worldwide |

[50-60]% | [40-50]% | |

WLM | [30-40]% | [20-30]% |

ICQ | [5-10]% | [0-5]% |

Skype | [0-5]% | [0-5]% |

Yahoo! Messenger | [0-5]% | [5-10]% |

Ebuddy.com | [0-5]% | [0-5]% |

Google Talk | [0-5]% | [0-5]% |

103. In addition, there are many other providers of IM in the EEA, with low market shares, such as AOL IM, ooVoo.com, PalTalk and Meebo Messenger. They had between 350 000 and 689 000 unique users in June 2011. In comparison, Facebook alone had around 94 million and WLM 63 million unique users in June 2011.

104. With regard to the low market share of Google Talk, the parties stress that the study they used for calculating market shares59 only includes data for the Google Talk (voice and video) application of Google, but not the web chat version of Google Talk. This means that Google's market share for IM should be rather understated.

105. Post-transaction, Microsoft will hold a [30-40]% market share in the EEA behind the market leader Facebook ([50-60]%). Worldwide, these market positions do not change significantly (Microsoft: [30-40]% and Facebook: [40-50]%). Other competitors on these markets are ICQ in the EEA or Yahoo! Messenger worldwide, with market shares of respectively [5-10]% and [5-10]%.

- Voice calls:

106. The parties submit that the total volume of Skype-to-Skype traffic (including video traffic) is approximately 20% of international TDM and VoIP traffic (excluding PC- to-PC traffic). The parties are unaware of any source that estimates shares of (voice only) VoIP traffic but they calculated an upper bound for their combined PC-to-PC (voice only) VoIP shares60.

107. Skype’s market share of international VoIP carrier traffic and PC-to-PC VoIP traffic in 2010 is less than [40-50]%. Further, since WLM-generated PC-to-PC voice minute volumes amount to approximately [0-5]% of Skype’s Skype-to-Skype minute volumes, the parties believe that the combined share of the parties is less than [40- 50]%61.

108. With regard to voice calls, competitors of the parties are Google, Facebook, AOL, Fring, ICQ, Trillian, Nimbuzz and Miranda, all available on Windows. Viber is currently available only for mobile OSs and Fring is only available for iPhone, Android and Nokia OVI62.

- Video calls:

Provider of video calls | Market shares 2011 EEA-wide63 |

Skype | [40-50]% |

WLM | [30-40]% |

[5-10]% | |

ICQ | [5-10]% |

Yahoo! | [0-5]% |

ooVoo.com | [0-5]% |

[0-5]% | |

AOL | [0-5]% |

109. Post-transaction, Microsoft will have a combined market share of [80-90]% in the EEA followed by Facebook ([5-10]%) and a number of competitors with smaller market shares (ICQ [5-10]%, Yahoo!, ooVoo.com, Google, AOL)64. According to the parties, worldwide these market positions do not change significantly65.

b) Commission's assessment

- IM

110. With regard to IM, Skype is not a significant player and adds an increment of less than [0-5]% to WLM ([30-40]%) which is not the leader in this market.

111. Furthermore, the parties have provided evidence showing that WLM is loosing active users. Between January 2009 and January 2011, the number of WLM IM users in the EEA decreased by approximately [10-20]%. This trend reinforces WLM's limited competitive strength in a fast growing market.

112. Moreover, the Commission notes that IM is a dynamic market, as illustrated by the fast growth of Facebook that has become the leader for IM in less than three years with a market share of approximately 50%. The Commission also takes into account the competitive pressure exerted by alternative forms of communications, such as voice and video calls which are expanding faster than IM.

113. The Commission also considers that the growing use of smartphones and tablets for sending IM, where WLM is almost absent, in combination with the preference of consumers for integrated communications experience (illustrated by the success of social networking websites) including IM, are a disincentive for Microsoft to charge for this service or to stop innovating66.

114. In light of the analysis above, the Commission considers that the notified operation does not raise serious doubts as to the compatibility with the internal market with regard to the provision of IM services.

- Voice calls

115. With regard to voice calls, WLM is almost absent, and adds an increment of less than [0-5]% to Skype which has a market share of [40-50]%.

116. Moreover, the parties have provided evidence showing that WLM is loosing active users67. Between March 2011 and May 2011, the number of WLM voice users in the EEA decreased by approximately [10-20]% ([10-20]% worldwide). This trend proves that WLM is loosing market strength in a fast growing market.

117. The parties add that WLM voice and Skype voice communications services are not close substitutes from a demand-side. According to them, there are significant functional differences between the two services. WLM users can only call other WLM users and they cannot call (or receive calls from) the PSTN. By contrast, Skype users can call not only other Skype users but they can also call any PSTN number68 and receive PSTN-originated calls69.

118. Furthermore, the Commission notes that voice calls services are a highly competitive sector, in which many VoIP providers compete for customers' call minutes, not only against each other, but also to a certain point against providers of PSTN services70. Google has recently started offering cross-subsidized PSTN calls for free in the United States and at very competitive prices in the EEA, undercutting those of Skype. The Commission notes also that Google is a relatively new entrant in voice calls in the EEA since it has entered the market in June 2010.

119. In light of the above, the Commission considers that the notified operation does not raise serious doubts as to the compatibility with the internal market with regard to the provision of voice calls.

- Video calls

120. With regard to video calls, the notified operation leads to the creation of a market leader. Nevertheless, for the reasons outlined in the following paragraphs, the Commission considers that the notified operation does not raise serious doubts as to its compatibility with the internal market.

121. First, as mentioned in paragraph 78 above, market shares may not be the best proxy to determine competitive strength in markets for consumer communications services. These markets, and this is also true for video calls, are currently free of charge. If a company were to charge for its service, competitors would switch to alternative providers offering their service free of charge. This is confirmed by internal documents of Skype showing that [> 75]% of its users would switch to an alternative provider if Skype started charging for its free service (in particular for video calls).

122. A similar switching behaviour would likely be observed if innovation was stopped or slowed down. Consumers are very sensitive to innovative services or products in consumer communications services. Providers of consumer communications services lose traction quickly if they are unable to offer users new and innovative functionality. For example, Skype’s innovations over the last eight years highlight the critical role innovation players in its success, as illustrated in the table below.

| (up to 5 participants) and file transfer |

2004 | Skype Out |

2005 | Skype Online Numbering and voicemail |

2006 | video calling and SMS |

2009 | screen sharing |

2010 | group video calling71 |

123. Moreover, smaller players have succeeded in rapidly entering, and gaining traction in the consumer communications sector with innovative products. For example, ooVoo launched its first video chat product in February 2007, and was one of the first providers of group video calling in May 2009. Today, ooVoo has more than 25 million users.

124. Second, Microsoft will remain under a strong competitive pressure from numerous current players. Despite their low market shares, some competitors such as Google and Facebook hold a strong consumer brand with a robust monetization model derived from online advertising72. Both Google and Facebook have recently entered these markets with growing success as described below. The parties have provided a long, non-exhaustive list of recent entries on the market for video calls, such as Bistri, IMO Instant messaging, Friendcaller, Paltalk, or VZOchat. All these players provide alternative competing services.

125. Google has a strong brand and a broad product range including video call services. Google offers this service through its web-based and advertising-supported email service Gmail. Gmail users can make video calls part of the chat functionality.

126. Facebook is a leading global social networking site with more than 750 million active users worldwide. The number of its users has grown rapidly over the past several years. Facebook is offering video calls enabling Facebook users to make calls to other Facebook users. For this purpose, Facebook relies on Skype's technology pursuant to a […] agreement renewable, concluded in June 2011. Under the terms of the agreement, Skype cannot invoke its termination rights before […]. If after this date Skype were to exercise its rights to terminate the agreement early, Facebook would continue to benefit from the use of Skype on Facebook for a […] "wind-down period". In addition, Facebook controls the user ID and the user experience73. Hence, Facebook can be seen as a competitor to the parties.

127. Google and Facebook also have a competitive advantage vis-à-vis Microsoft because they offer video calls services as part of a broader user experience through Facebook social network and Google+. As social networks are becoming a favourite means of communications, consumers tend to use increasingly the functionalities they offer.

128. Third, the use of WLM is declining despite the overall increase in the demand for video calls. During the period November 2010 to May 2011, the number of video calls made on WLM declined by [20-30%]. The same trend can be observed for WLM unique users during the period March 2011 to June 2011. The table below illustrates the decline of WLM for video calls.

| EEA-wide | Worldwide | ||

WLM unique users in million | Video calls in million | WLM unique users in million | Video calls in million | |

November 2010 | N/A | N/A | N/A | […] |

March 2011 | […] | […] | […] | […] |

June 2011 | […] | […] | […] | […] |

129. Fourth, WLM's weakness is reinforced by the fact that it has currently no presence or only a limited presence on tablets and smartphones, which are the fastest-growing platforms. These platforms are characterized by the significant presence of Google and Apple

130. Fifth, consumers use video calls services to communicate with a small circle of family and friends and multi-home. Therefore it is easy to switch small groups of users to other competing services. The Commission considers that this significantly mitigates any possible network effects related to the proposed transaction (see paragraph 91).

131. In light of the analysis above, the Commission considers that the notified operation does not raise serious doubts as to the compatibility with the internal market with regard to the provision of video calls.

c) Conclusion on horizontal effects

132. In light of the analysis above, the Commission considers that on the markets for consumer communications services the notified operation does not raise serious doubts as to the compatibility with the internal market.

3. Conglomerate assessment

133. As Microsoft and Skype's products are complementary or at least closely related products, the notified operation may give rise to conglomerate effects. Microsoft holds a leading/dominant position in a number of products, such as OS (Windows), Internet browser (Internet Explorer) or personal productivity application software (Office).

134. A number of conglomerate concerns were expressed during the market investigation:

135. First, Microsoft could, post-transaction, differentiate Skype's user experience according to the platforms or the OS by degrading the interoperability of Skype with competing OS and platforms in order to favour user experience on its own OS or platform and consequently increase its market power in these markets.

136. Microsoft could also differentiate its Windows' user experience vis-à-vis Skype's and WLM's competitors by degrading the interoperability of Windows with competing providers of consumer communications services in order to favour Skype and WLM and consequently increase their market powers in these markets.

137. Second, Microsoft could decide to integrate Skype and Windows or Skype and Office in order to increase Skype's footprint in the consumer communications market and make it a "must-have" product, creating or reinforcing its dominant position (i.e. tying).

138. Third, Microsoft could also decide for the same reasons explained in the above paragraph to commercially bundle Skype with Windows or Office (i.e. commercial bundling).

139. Several respondents to the market investigation submit that such strategies (taken in isolation or together) would aim at leveraging Microsoft's or Skype's strong position in their respective markets, leading to the exit or at least significant weakening of their competitors within the next two to five years74.

140. Since the theories of harm identified following the market investigation are similar as regards the three products of Microsoft (Windows, Internet Explorer, Office), the Commission assesses the possible conglomerate effects of the transaction on the basis of the link between Windows and Skype only.

141. It should be noted that in most cases, conglomerate mergers do not give rise to competition problems. Only in cases where the merged entity enjoys strong market power in one of the markets concerned, a conglomerate merger may create possibilities for exclusionary bundling or tying practices that could disadvantage or foreclose competitors and ultimately lead to them exiting the market, or otherwise significantly impede competition in the markets concerned75.

142. According to the Commission's Guidelines on the assessment of non-horizontal mergers ("Non-horizontal Merger Guidelines"), conglomerate effects require (a) the ability to foreclose, (b) the incentives to foreclose, and (c) the overall likely impact on competition and consumers. In order to be taken into account, any conglomerate effect must be merger specific. In other words, the conglomerate effect must result from Microsoft's acquisition of Skype.

a) Ability to foreclose

143. The Commission's investigation reveals that Microsoft has the ability to enter into each of these three practices (degradation of interoperability, tying and commercial bundling). This view has been confirmed by a majority of respondents to the market investigation76. Generally the respondents consider that it would be easy for Microsoft to degrade the interoperability of Skype (or of its products) with other platforms if it decides to enter into such a strategy, or to tie or commercially bundle their respective products.

b) Absence of incentives

144. The parties claim, however, that Microsoft has no incentives to enter into each of the three practices mentioned above (degradation of interoperability, tying and commercial bundling).

145. With regard to a possible degradation of interoperability vis-à-vis competitors, the parties underline that the acquisition of Skype is an important part of Microsoft’s strategy to […]. Microsoft has therefore no incentive to degrade the interoperability of Skype's product vis-à-vis the competing OSs since Skype's value is mainly based on its large active user base. Degrading current interoperability with non-Windows or non-PC platforms would lead to a loss of customers for Skype's communications services77.

146. Hence, in order to maintain and enhance the value of the Skype brand, which Microsoft bought for USD 8.5 billion, the Commission considers that it is essential that Skype branded products are available on as many platforms as possible and at least on the platform with which Skype currently interoperates.

147. If Microsoft were to degrade Skype's user experience on competing (and growing) OS, such as Android, iOS, Mac OS and other platforms it would give its main competitors an advantage with the risk that over time the consumer appeal of Skype’s brand would be lost. In this case, Microsoft would have lost a significant part of its initial investment for the acquisition of Skype. This is particularly true with regard to mobile OS platforms where Microsoft’s market position is much weaker than it is in PC OSs.

148. Neither Skype nor WLM are “must-have” products in the consumer communications services markets. There are many alternatives to Skype, and consumers increasingly use non-Windows platforms for online communications (see paragraphs 73 and 74 above). Hence, any attempt to withhold Skype from, or degrade the Skype's user experience on non-Windows platforms would hurt Skype, and therefore Microsoft. It would not harm the competing OS platforms. For instance, Google is pre-installing Google Talk on Android and Apple is pre-installing Facetime on iOS.

149. The Commission also notes that the CEO of Microsoft, Steve Balmer, claimed publicly that "[Microsoft] will continue to support [Skype on] non-Microsoft platforms because it's fundamental to the value proposition of communications"78.

150. In the course of its investigation, the Commission has not received any substantiated replies demonstrating that Microsoft has incentives to degrade the interoperability of Skype or its products with competitors' products or services.

151. With regard to a possible tying between Skype and Microsoft's products, the Commission considers that most of the arguments mentioned above in order to demonstrate the absence of incentives for a strategy of degradation of interoperability (in particular the necessity for Microsoft to maintain and enhance the value of the Skype brand) are also relevant to the assessment of the strategy of tying.

152. In addition, the parties claim that consumers do not simply use whatever communications product is provided with Windows. The consumers use multiple communications services on multiple platforms, such as Apple iOS and Android, which include their own built-in communications services (Facetime and Google Talk). The parties further submit that some online communications applications such as Facetime and Viber are not even made available for the Windows platform, and yet they are very successful.

153. Moreover, consumers increasingly prefer services that offer online communications as part of a broader user experience such as Facebook, the recent Google+ and Gmail, which all run on Windows.

154. Competitors would therefore have many possibilities to market and many different means available to attract consumers.

155. In the course of its investigation, the Commission has not received any substantiated replies demonstrating that Microsoft has incentives to tie Skype and Microsoft's products.

156. With regard to a possible commercial bundling between Skype and Microsoft's products, the Commission considers that such a strategy is not likely in the present case.

157. Skype is currently offered for free to customers and if prices were charged for this service, the large majority of consumers would switch to alternative providers (see paragraph 76 above) as for instance Google, Facebook, Viber, ooVoo or Fring. Commercial bundling is therefore unlikely in this free market.

158. For the above reasons, the Commission concludes that Microsoft has no incentives to engage in any of the three foreclosure strategies (degradation of interoperability, tying, commercial bundling).

c. Overall likely impact on competition and consumers

159. With regard to the effects of a foreclosure strategy based on degradation of interoperability, tying or commercial bundling, the Commission considers that effects will be non-existent or at most limited.

160. First, Skype is currently operated as a closed system. It is not possible for consumers to communicate between Skype and competing communications service such as for instance Viber. The notified operation has therefore no effect on Skype's inter-operability.

161. Second, the effect of degradation of interoperability could be in any event only very limited as Skype is already pre-installed on a significant share of OEM PCs sold to consumers. Skype has distribution and/or pre-installation arrangements with OEMs accounting for at least [>60]% of Windows PC vendor shipments worldwide79. The parties estimate that Skype is already pre-installed on approximately [>50]% of Windows-PCs sold to consumers.

162. OEM pre-installation results only in a small share of Skype registered and connected users. Only [few] purchasers of PCs on which the Skype client has been pre-installed register as new Skype users. Further, only [few] of all Skype registered users use versions of the software which was pre-installed by OEMs. This means that even if Skype was pre-installed on 100% of Windows-PCs, the expected increase of new users would be limited.

163. Third, there is an increasing trend of consumers using smartphones and tablets instead of PCs (see paragraphs 73 and 74). This development limits the effects of any foreclosure strategy by the parties which provide services predominantly based on Windows PCs.

164. Fourth, the Commission received a number of submissions with regard to a possible degradation of the interoperability of Windows Phone OS and related devices vis-à-vis competing consumer communications services.

165. The Commission considers that these particular concerns are not convincing as the Windows Phone OS does not have a strong position in the market for mobile OS. The Commission notes indeed that Windows is not a dominant player in mobile OS and has a market share of less than [5-10]% (for smartphones and for tablets)80. The market leader is Android followed by Apple, Blackberry and Symbian. Furthermore, paragraph 113 of Non-horizontal Mergers Guidelines state: "if there remain effective single-product players in either market, competition is unlikely to deteriorate following a conglomerate merger. The same holds when few single-product rivals remain, but these have the ability and incentive to expand output".

166. In the present case, consumer communications services markets are characterized by the existence of numerous players, including rivals that hold the ability and incentive to expand, such as most notably Google and Apple.

167. Fifth, the Commission notes that there are competitors, such as Google, that provide their services directly on the Internet, avoiding the necessity to download any application on platforms.

168. Finally, as explained above (see paragraph 76) if the parties start charging for this currently free service or stop innovating, consumers are likely to switch to competing services.

169. For the reasons above, the Commission concludes that foreseeable effects of the three foreclosure strategies referred to above would be non-existent or at most limited.

d. Conclusion on conglomerate effects

170. In light of the analysis above, the Commission considers that on the markets for consumer communications services the notified operation does not raise serious doubts as to the compatibility with the common market.

Enterprise communications services

1. Market characteristics

171. The parties submit that enterprise communications services are characterized by two general trends: (i) in the same manner as consumer communications services, they are a fast-growing sector, (ii) and they are characterized by a "consumerization" of their products.

- fast-growing sector

172. There is a growing demand for enterprise communications services by large companies, illustrated by the significant number of enterprises intending to use UC in the short and medium term. It is expected that [80-90]% of enterprises in the US employing over 50 employees indicate that they intend to use UC in the next coming years81.

- consumerization of the enterprise products

173. According to the parties, employees increasingly expect to have access at the workplace to communications services which they use as consumers. The parties consider that iPhone and iPad which are used by enterprises and consumers are examples of this trend. Both products were initially developed for consumers, and are now being increasingly used within enterprises.

174. Given the growth of smartphones and tablets, IT departments have been forced to change their previous evaluation on how to support this growing array of devices in the enterprise. Consumerization of IT is therefore changing the markets for enterprise communications services.

175. While there is a trend towards "consumerization" of enterprise communications services, which is also confirmed by the market investigation82, this trend does not imply that enterprise and consumer communications services markets are converging.

176. The impact of "consumerization" of IT appears to be limited to two specific areas: First, devices designed primarily for consumer use are increasingly adopted in the enterprise environment driving demand for enterprise services to run on those devices. Second, enterprises also increasingly expect consumer functionalities to be available within enterprise products or use social networks services such as Facebook. However, once these functionalities are adopted in the enterprise, IT managers modify and adapt the service to meet the more robust and secure requirements of the enterprise environment.

2. Horizontal assessment

177. Microsoft offers enterprise communications services through Lync, which is made of Lync Client and Server, and of Lync Online.

178. Lync Client and Server is the successor product to Office Communications Server and was released in November 2010. Lync Online is the remotely hosted and managed version of Lync (i.e. the product is not installed on the customer's servers but on servers within Microsoft's data centers) and was released in June 2011.

179. Lync incorporates IM and presence, unified (audio, video and web) conferencing with up to 250 participants, voice communications (end-to-end VoIP) within a corporate network, VoIP calls to corporate networks federated with the user's own corporate network, video and IM communications with WLM users, as well as PSTN break-in/- out, video calls, group calls, file transfer, white boarding, desktop and application sharing, and co-authoring of documents, presentations and spread sheets.

180. Lync's voice functionality also provides a range of advanced features that enterprises require, including consultative transfer, call park/retrieve, call recording, call filters, personalized ringing, response groups and hunt groups83 team calls.

181. In addition, Lync also includes key management communications features, such as automatic call distribution, call type detection, call authorization codes, advanced call controls, centralized administration and monitoring, centralized management and maintenance.

182. The parties argue that the activities of Lync and Skype do not overlap horizontally. They submit that Skype is not active in enterprise communications services because Skype offers services that are primarily for and used by consumers. Although the services are also used by enterprises, in particular SMEs, they submit that Skype should not be considered as a competitor for enterprises communications services according to the parties.

183. Skype's user interface is identical for all users (consumer or enterprise) and Skype offers only very limited service management tools. Skype's limited screen sharing functionality enables users to share content such as photos by allowing one user to let others see what is on her/his desktop. It essentially allows one user to passively see another user's desktop, as opposed to desktop sharing. It does not enable a user to take over another user's screen, nor does it enable multiple users to collaboratively edit or work on a document or other content or provide whiteboarding84 or similar collaborative functionality.

184. The Skype client lacks key management features, such as automatic call distribution, detailed call records, advanced call controls, centralized monitoring and management, call type detection, centralized administration and monitoring and call authorization codes. Enterprises require such management features in communications services.

185. According to one internal document of Skype, only [5-10]% of Skype client users use Skype's services exclusively or mainly for business purposes and tend to be SMEs.

a. Market shares

186. Microsoft's market share is below [10-20]% on any alternative product market in the EEA.

187. The parties have provided market shares on the basis of a worst case scenario, which is a market for enterprise communications services confined to the functionalities which are offered by Skype that is IM/presence, voice calls and video calls. On such a market which includes only software-application based communications for enterprise85 Microsoft has a market share of [10-20]%, far behind the market leader Cisco ([30-40]%). Other competitors are Citrix ([5-10]%) and IBM ([5-10]%). Skype's market share on such a market would be close to [0-5]%.

188. If the market was further segmented according to the functionalities (IM/presence, voice calls and video calls), Microsoft’s share would not increase compared to its share in enterprise communications applications. The parties claim that the identification of distinct markets for stand-alone IM/presence, voice and video would reduce Microsoft’s share for the following reasons. First, Microsoft only offers Lync which is not a product that is adapted to meeting demand for stand-alone products. Second, there are far more suppliers of stand-alone enterprise voice, video and IM/presence solutions than there are for enterprise UC products. Lync is therefore a less attractive solution for customers seeking stand-alone products, and Microsoft faces significantly more competitors in attempting to supply such customers. As a result, Microsoft’s share in any one of these segments would be lower than its share in enterprise communications applications.

189. If the market were further segmented according to platform or OS, Microsoft's market share would not be significantly different since today the great majority of enterprises run Windows in the EEA.

190. If the market were further segmented according to the size of the company and a market for enterprise communications services for small enterprises (up to 50 employees) or SMEs was defined the combined market share of the parties would not be more than [30-40]%. On such a market Skype's market share would be about 1/2 to 1/3 of Google's market share.86 The increment would be minimal as Microsoft would have a de minimis market share with its product Office 365 Plan P1 (hereinafter "Plan P1") targeted at companies with up to 25 employees. It includes functionalities of Lync Online, the hosted managed version of Lync. By 27 August 2011, there were […] customers worldwide for this product. Therefore, Microsoft's market share on such a market would be minimal.

b. Commission's assessment

191. Contrary to Microsoft's claims, Lync is perceived by the overall majority of respondents to the market investigation as a significant competitor in the enterprise communications services markets by respondents to the market investigation87. In this regard, the market share of [10-20]% estimated by Microsoft does not seem to reflect its real competitive strength in these markets. The Commission also notes that Microsoft entered this market recently (November 2010) and numerous market participants state that Lync has already expanded rapidly in that short time-span.

192. However, in the markets for enterprises communications services, Skype is not considered as a market player. While Skype supplies a communication application, its products lack key enterprise-grade functionality and UC features, as explained in paragraphs 182 and 183 above. Further, Skype does not provide any form of business collaboration platform. Its software client offers basic functions such as IM/presence, voice and video calls. Skype does not offer calendar, email, web conferencing, document editing, whiteboarding or other collaboration tools enabling the joint creation of content or sharing of workspaces. Skype does not offer broad management and administration tools.

193. The parties have provided an analysis of Microsoft's ad hoc win/loss data that covers […] new business opportunities for which Microsoft competed over the last two years. This analysis shows that out of these […] opportunities, Skype competed only […] with Microsoft, and was never successful.

194. The market investigation also largely confirms that Skype is not perceived as a provider of enterprise communications services and as a competitor of Microsoft with regard to enterprise communications services. Cisco, Siemens, IBM, Aastra and Avaya are mostly quoted by the respondents to the market investigation as the closest competitors of Microsoft88.

195. Last but not least IDC has confirmed that it does not consider Skype to be a supplier of enterprise communications services. As such, IDC has not included Skype as a supplier of either enterprise communications applications or business collaboration platforms.

196. The Commission notes that Skype recently revised its approach towards business customers, adjusting its strategy to focus on SMEs and seeking limited solutions in enterprise communications. On its website, Skype shows how its consumer products can be used by enterprises. This targets mainly SMEs whose needs are to a certain extent similar to consumers.

197. On possible markets for enterprise communications services for small enterprises or SMEs, the Commission takes the view that Skype's products and Microsoft's products are however not close competitors. Microsoft's product Plan P1 offers collaborative and conferencing functionality that Skype does not provide. On the other hand, Skype offers PSTN voice functionality that Plan P1 does not. Moreover Microsoft's Plan P1 is a paid solution whereas Skype is mainly bought because it is free or for its low prices for calls to PSTN that Plan P1 does not offer.

198. On markets for enterprise communications services for small enterprises or SMEs the Commission takes the view that Google with its free Google applications rather appears to be the closest competitor of Skype.

199. Moreover, Microsoft's market positions would be de minimis (below [0-5]%) on markets for enterprise communications services for small enterprises or SMEs.

200. Finally, the Commission notes that the markets of enterprise communications services are characterized by numerous other players such as Citrix, Adobe, Intercall, Alcatel- Lucent, Avaya as well as Google if a narrower market according to the size of the company were defined. Considering the expected growth of these markets (see paragraph 172 above), the Commission considers that the acquisition of Skype does not raise any horizontal competition concerns in the enterprise communications services markets.

201. Post-merger, Microsoft will not be a market leader in enterprise communications services and it will remain under the competitive pressure of its current competitors for the foreseeable future.

c. Conclusion on horizontal effects

202. In light of the analysis above, the Commission considers that on the markets for enterprise communications services the notified operation does not raise serious doubts as to the compatibility with the internal market.

3. Conglomerate assessment

203. The Commission considers that with regard to enterprise communications services a conglomerate assessment is not relevant since Skype is not active in these markets. Hence, any bundling or tying between Microsoft's products within the enterprise world (such as Windows OS, Office or Outlook) and Skype as enterprise communications services provider will not have any significant effects in the markets concerned.

204. Nevertheless, in the course of its investigation, the Commission received submissions from competitors of Microsoft in the markets for enterprise communications services. These mainly originated from the following two categories of competitors (i) telecom operators and (ii) other providers of enterprise communications services. Both categories are competitors of Microsoft in the enterprise communications services, but telecom operators provide mainly traditional voice call services and are therefore competitors only for the functionality of voice calls.