Commission, January 9, 2014, No M.7023

EUROPEAN COMMISSION

Judgment

PUBLICIS / OMNICOM

Dear Sir/Madam,

Subject: Case No COMP/M.7023 – PUBLICIS / OMNICOM

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041

1. On 25 November 2013, the European Commission received a notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Publicis Groupe

S.A. ("Publicis", France) and Omnicom Group, Inc. ("Omnicom", the United States of America) enter into a full merger within the meaning of Article 3(1)(a) of the Merger Regulation by way of a stock-for-stock exchange (the "Transaction").

2. Publicis and Omnicom are together designated hereinafter as the "Parties".

I. THE PARTIES

3. Publicis is a French international communications and advertising group. Publicis' agencies are organised in separate networks of offices present throughout the world and collectively provide a broad range of advertising services, including digital advertising, creative services, public affairs, corporate communications and events, media strategy, planning and buying, and specialty communications.2

4. Omnicom is a U.S.-based global advertising, marketing and corporate communications company. Omnicom's agencies are also organised in separate networks of offices present throughout the world and collectively offer a range of advertising, marketing, media and other related services.3

II. THE TRANSACTION

5. By way of a Business Combination Agreement dated 27 July 2013 between Omnicom and Publicis, HoldCo, a newly-formed Dutch holding company, will successively acquire Publicis and Omnicom. First, Publicis will merge directly with HoldCo, with HoldCo continuing as the surviving legal entity. Then, Omnicom will merge with a newly formed wholly owned subsidiary of HoldCo, Merger Sub, with Omnicom continuing as the surviving legal entity and a wholly owned subsidiary of HoldCo. The Transaction has been structured so that the shareholders of Publicis and Omnicom will each hold approximately 50% of the fully diluted equity of the merged group.

6. The Transaction therefore constitutes a concentration within the meaning of Article 3(1)(a) of the Merger Regulation.

III. EU DIMENSION

7. The undertakings concerned had a combined aggregate worldwide turnover of more than EUR 5 000 million4 in 2012 (Publicis: EUR 6 610 million; Omnicom: EUR 11 067 million). They both had a combined aggregate EU-wide turnover of more than EUR 250 million in 2012 (Publicis: EUR […]; Omnicom: […]) and each did not achieve more than two-thirds of its aggregate EU-wide turnover in 2012 within one and the same Member State.

8. The Transaction therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

IV. COMPETITIVE ASSESSMENT

9. Publicis and Omnicom are both active, through their various subsidiaries, in the advertising, marketing, communications ("AMC") services sector, including marketing communications services ("MCS") and media buying services ("MBS") in several Contracting Parties to the EEA Agreement (referred to hereinafter as "EEA countries").

10. Publicis is active in the sale of advertising space in France and in the Netherlands. These markets are vertically related to the MBS markets, and some of their possible segments. Publicis’ activity is downstream from the activity of both Parties’ media agencies on the procurement side of MBS, in the sense that Publicis sells on behalf of cinema owners advertising space to advertisers either directly or through media agencies.5 The effects of this vertical relationship will be assessed in section IV.6 of the Decision.

11. Regarding data analytics services, Publicis and Omnicom have marketing data analytics capabilities but they are essentially used in-house as a mean of targeting and optimising MCS campaigns or MBS in support of the provision of core MCS or MBS services.6 However, Publicis has one subsidiary that provides data analytics services to third parties on a stand-alone basis, named Ninah. Within the EEA, Ninah is active in the United Kingdom only, with revenues of around EUR […].7 Omnicom has a subsidiary called Analect, with world-wide turnover of around EUR […], of which only less than EUR […] is achieved in the United Kingdom.8 On a hypothetical data analytics market, or any of its segments, in the United Kingdom, the Parties' 2012 combined market shares would therefore have been small, and no material increment will occur as a consequence of the Transaction. Therefore, data analytics services are not assessed any further in this Decision.

IV.1. RELEVANT MARKETS

IV.1.1 MEDIA BUYING SERVICES

IV.1.1.1. PRODUCT MARKET

12. MBS include purchasing of advertising time and/or space in various types of media, such as broadcast and cable TV, newspapers and magazines, radio, billboards and the Internet, for clients running advertising campaigns.9 According to the Parties, media buying agencies will also usually provide media planning and strategic advice, including research into target audiences, which media to use, and the monitoring/tracking of the success of a campaign.

13. In previous decisions in the advertising sector,10 the Commission has identified separate product markets for MBS and MCS. The Parties support this segmentation and their submissions are based on the distinction between MBS and MCS.

14. A majority of respondents to the market investigation indicated that there is a distinction between MBS and MCS.11 The strategies, necessary skills, tools and overall activities are different between MBS and MCS. Advertisers use MCS to create a message and MBS to deliver that message to the target group. While a key competitive parameter in MCS is creativity, MBS depend on negotiation power and skills as well as know-how about media planning and monitoring, characteristics which are of rather technical nature. Likewise, the market investigation suggested that a majority of advertisers use different agencies for MCS and for MBS.12

15. In WPP/Grey, the Commission considered a further segmentation of the market for MBS between: (i) the sales market, in which media buying agencies act as suppliers of MBS to final customers (advertisers); and (ii) the procurement market, in which media buying agencies buy (usually on behalf of their clients) advertising time or space in the media from media owners (for example TV broadcasters, publishing houses, radio stations, etc.).13 The Parties do not dispute this additional segmentation. Equally, none of the respondents to the market investigation opposed such a further distinction.

16. The competitive assessment for the present Transaction will therefore be based on separate markets for MBS and MCS, on the one hand, and within the MBS market, the Commission will further distinguish between the sales and procurement of MBS, on the other hand.

IV.1.1.1.1. Sale of media buying services Segmentation by type of service

17. The Commission has investigated whether on the sales-side of the MBS market, an additional segmentation should be made, in particular based on the type of MBS provided by media buying agencies, such as the development of media placement plans, strategic advice surrounding media placement plans, media buying, etc. The Parties do not consider as relevant any further segmentation on the sales-side of the MBS market.

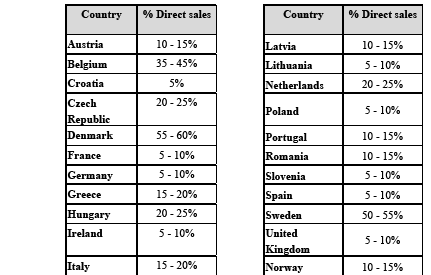

18. In previous Commission decisions,14 no such segmentation by type of MBS was considered. Respondents to the market investigation did not provide any evidence that would justify a further distinction on the sales-side market of MBS. Even though some competitors mentioned that certain advertisers may want to keep separate the strategic planning from the buying and split them between different agencies, the majority of competitors indicated that the most common offered service includes all MBS.15 Likewise, the majority of customers confirmed that they generally purchase these services together as the combined scope of services is more efficient and allows for a more coherent media strategy as well as for optimised costs.16

19. In light of the above, the Commission considers that no additional segmentation by type of service within the sales-side of the MBS market should be made for the purpose of assessing the present Transaction.

Segmentation by type of media

20. The Commission considered in previous decisions that the market for the sale of MBS should not be further segmented according to the media in question, because media buying agencies are not specialised in one media segment, but normally carry out MBS for all media channels. Additionally, most advertisers buy multiple types of media and want central coordination and oversight of their media planning.17

21. The Parties submit that this conclusion is still valid and that the sales-side of the MBS market should not be further segmented by type of media, in particular for the following reasons. First, from a demand-side perspective, most advertisers buy multiple media types as they need to interact on a cross-channel basis with consumers whose media consumption is increasingly diverse and fragmented. This feature of MBS is also evidenced by the fact that an overwhelming majority of MBS pitches require media agencies to buy on all types of media channels. Second, from a supply-side perspective, with the exception of the agencies that only buy digital advertising space, media buying agencies are not compartmentalised across media channels. Third, the Parties consider that the growth of the Internet has neither changed the nature of demand for MBS, nor the manner in which these services are supplied and, thus, does not warrant segmentation by type of media in the sales-side of MBS or for digital services in particular.

22. Respondents to the market investigation indicated that it would be appropriate not to segment by type of media within the sales-side of the MBS market. While some MBS may focus on a specific media channel such as the Internet, the majority of media buying agencies do not usually specialise in selling MBS to advertisers for specific types of media.18 A majority of customers also suggested that they usually purchase a range of MBS covering more than one media channel,19 which allow them to reach their final consumer target, and that they usually look for MBS suppliers that are able to provide services with respect to all types of media.20 This is a separate question to whether for an advertiser the placement of an online advertisement is substitutable with the placement of an advertisement on other offline media channels. This question does not need to be answered in the present Decision since advertisers will typically seek to buy from an MBS agency a full package of complementary services covering several (online and offline) media channels and including advice on how best to distribute advertisement space over these different media channels. MBS agencies offer such packaged solutions.

23. In light of the above, the Commission considers that no additional segmentation by type of media within the sales-side of the MBS market should be made for the purpose of assessing the present Transaction.

Segmentation by type of sector

24. In previous Commission decisions, no further segmentation by type of sector within the sales-side of the MBS market was considered. The Parties do not consider relevant any further segmentation on the sales-side of the MBS market.

25. Respondents to the market investigation suggested that no such segmentation by type of sector should be made. Even though certain sectors are governed by rules that may require specific knowledge by the MBS supplier, such as healthcare or alcoholic beverages, the majority of respondents to the market investigation did not consider that such sectors have specific requirements that only certain media buying agencies can address.21

26. In light of the above, the Commission considers that no additional segmentation by type of sector within the sales-side of the MBS market should be made for the purpose of assessing the present Transaction.

Segmentation by size of account

27. The Commission has previously considered whether the sales-side of the MBS market, MBS should be further segmented into: (i) large-scale MBS for large advertisers, that is to say advertisers that pursue mostly extensive and costly nation-wide advertising campaigns ("large-scale media buying") and (ii) small-scale MBS for small advertisers pursuing predominantly local/regional advertising campaigns ("small-scale media buying").22 However, the Commission did not retain this possible segmentation except in Germany, where only large agencies belonging to one of the international networks were viewed as being capable of providing MBS to large-scale advertisers.23

28. The Parties contest any possible segmentation, including in Germany, on the basis that the same group of media buying agencies compete for "large-scale" and "small-scale" accounts. The Parties explain that, on the one hand, independent agencies compete with international groups for large accounts and, on the other hand, international groups do not only compete for large accounts, but also for smaller ones.

29. Responses to the market investigation differed with regard to a possible segmentation by size of account within the sales-side of the MBS market. On the one hand, a majority of competitors considered that not every media buying agency active in MBS can be selected by large-scale advertisers, as larger MBS agencies may be able to offer larger scale services that smaller agencies may not.24 On the other hand, competitors indicated, in the majority of cases, that their respective media buying agencies can be selected by any advertiser, no matter its size.25 Furthermore, a majority of customers pointed to the fact that large-scale advertisers require MBS agencies that have large-scale capabilities, a broad geographic presence, and are able to build up the skills and knowledge, and manage the complexities of the required services.26

30. In any event, for the purposes of the present Decision, it is not necessary to conclude on whether the market for the sales of MBS should be further segmented between small- scale and large-scale media buying as the Transaction does not raise serious doubts even considering that large-scale advertisers may have specific requirements.

Segmentation depending on the inclusion/exclusion of direct sales

31. The Commission also investigated whether direct sales are part of the same market as MBS and whether an additional segmentation should be considered. The direct sales represent the media purchased directly by advertisers from media owners rather than through a media buying agency

32. The Parties see no basis to exclude direct sales from the market size and disagree with any such exclusion because direct purchasing is a competitive constraint on media buying agencies. The higher the level of direct buying in a given country, the more media agencies are constrained by the threat of advertisers bypassing their services and dealing directly with media owners, and, in all events, major advertisers especially have as good an opportunity as media buying agencies to acquire the human talent necessary to satisfy their MBS needs

33. Responses to the market investigation differed regarding such an additional segmentation. In particular, the replies of customers were mixed regarding whether they would switch to buying directly from media owners if prices of MBS agencies were to increase by 5-10% post-Transaction.28 However, a majority of media owners explained that they sell advertising time and/or space directly to advertisers.29

34. Moreover, the Commission considers that in two EEA countries where the Parties' activities overlap (Sweden and Denmark), direct sales represent a high percentage of total media buying sales of media owners (on average 50-55% and 55-60% respectively), and would likely exercise a significant competition constraint on advertisers. In the other countries where the Parties' activities overlap, the ratio of direct sales against total media buying sales is significantly lower.

35. In any event, for the purposes of the present Decision, it is not necessary to conclude on whether direct sales belong to the same market for MBS in some or all EEA countries where the Parties' activities overlap, except in Sweden and Denmark, as the Transaction does not raise serious doubts under any alternative product market definition. The extent to which the threat of actual or prospective advertisers opting to bypass the services of a media buying agency may act as a competitive constraint on the media buying agencies will be assessed in the competitive analysis. For Sweden and Denmark however, direct sales, given their magnitude, have to be included in the MBS markets.

Conclusion

36. In light of the above, the Commission’s competitive assessment will be based on a broader market for the sale of MBS encompassing all types of MBS services, all media channels, all types of sectors, and will also take into consideration the specific requirements of small-scale versus large-scale media buying, as well as including and excluding direct sales depending on the countries.

IV.1.1.1.2. Procurement of media buying services Segmentation by type of media

37. In past decisions, the Commission has considered30 a segmentation of MBS on the procurement-side of the MBS market based on different types of media and concluded that different procurement markets for TV and print should be defined, due to the general lack of demand substitutability between different types of media and the fact that media owners could not switch from one type of media to the other without substantial investment and know-how. Additionally, the Commission left open the question whether a further segmentation is necessary within the procurement market for a specific type of media.31

38. While the Parties generally concur with the Commission's previous findings, they consider, however, with respect to the Internet channel which has considerably developed since WPP/Grey, that from the point of view of advertisers, there is a certain degree of substitutability between the procurement of advertising space online and in other media (in particular print). Moreover, the Parties argue that as newspaper and magazine publishers can easily launch digital editions of their publications, there is also a certain degree of supply-side substitution between the two. In any event, the Parties submit that for the purpose of assessing the present Transaction it can be left open whether the procurement of online advertising space constitutes a separate market. Finally, the Parties reject any further segmentation within the procurement markets between TV, print and online/mobile.

39. Responses to the market investigation differed with regard to a possible segmentation by type of media within the procurement-side of the MBS market. On the one hand, a majority of media owners considered that the traditional delineation between various types of media is becoming increasingly blurred, because media owners compete with other media owners in order to provide the best product for the advertisers' campaigns and because media channels are to some extent substitutable.32

40. On the other hand, a majority of customers indicated that the different media segments are in general not substitutable with respect to the type of advertising they offer.33 The degree of flexibility across media channels depends to a large extent on the individual advertiser and the specific target groups to be reached. All types of media have specific characteristics in relation to the effects of advertisement. In that regard, a majority of customers and competitors that responded to the market investigation indicated that depending on the needs and media strategy of advertisers, there may be one or several "must-have" media channels to promote advertisers' products or services, which are not substitutable with other media channels.34

41. In any event, for the purposes of the present Decision, it is not necessary to conclude on whether the procurement side of the MBS market should be further segmented by type of media as the Transaction does not raise serious doubts under any alternative product market definition.

Segmentation by size of account

42. The Commission has previously considered a further segmentation of the different MBS procurement media segments into small-scale and large-scale clients, but concluded that such distinction would be artificial.35 The Parties agree with the Commission’s past approach and support the lack of segmentation by size of client.

43. In the present case, respondents to the market investigation did not bring forward any conclusive evidence indicating that such segmentation should be made.

44. In light of the above, the Commission considers that no additional segmentation by size of account within the procurement-side of the MBS market should be made in order to assess the present Transaction.

Segmentation depending on the inclusion/exclusion of direct sales

45. The Commission has also investigated whether direct sales should be included on the procurement side of the MBS market and whether an additional segmentation should be considered.36

46. The Parties disagree to any exclusion of direct sales. They consider that direct purchasing by advertisers represents a competitive constraint on media buying agencies.

47. Responses to the market investigation differed regarding such an additional segmentation. In particular, the replies of customers were mixed regarding whether they would switch to buying directly from media owners if prices of MBS agencies were to increase by 5-10% post-Transaction.37 However, a majority of media owners explained that they sell advertising time and/or space directly to advertisers.38

48. For the purposes of the present Decision, it is not necessary to conclude on whether direct sales belong to the same market for MBS on all EEA countries where the Parties' activities overlap (except for Sweden and Denmark, given their important size of direct sales in these two countries), as the Transaction does not raise serious doubts under any alternative product market definition. The extent to which the threat of actual or prospective advertisers opting to bypass the services of a MBS agency may act as a competitive constraint on the media buying agencies will be assessed in the competitive analysis.

49. For Sweden and Denmark, direct sales, given their magnitude, have to be included in the MBS markets for all media channels, except for TV and outdoor in Sweden, and TV in Denmark. This is because, different from the average percentage at country level, the level of direct sales is low for TV (6%) and outdoor (16%) in Sweden, and for TV (1%) in Denmark.39

Conclusion

50. In light of the above, the Commission’s assessment of the Transaction will be based on the market for procurement of MBS segmented along different types of media, as well as including and excluding direct sales depending on the countries and media channels.

IV.1.1.2. GEOGRAPHIC MARKET

IV.1.1.2.1. Sale of media buying services

51. The Commission considered in previous cases40 that the market for the sale of MBS were national in scope. This conclusion was based inter alia on the fact that media buying agencies need to gather locally the necessary knowledge of customer patterns with regard to different media channels and of the differing national regulatory frameworks. In addition, the Commission also noted the tendency of the national markets for the sale of MBS to become wider in scope, at least with regard to multinational firms advertising in different countries. However, it was concluded at that time that the tendency was not developed enough to justify wider markets, in particular due to the limited number of multinational advertisers having a global strategy for media buying as well as acknowledgement by those multinational advertisers of the necessity for local presence.41

52. The Parties concur with the Commission's previous conclusions and submit that the necessity of a local presence remains a key element for the sale of MBS. First, it is essential to master the national language when negotiating with media buyers, who are mostly organised on a national basis. Second, local knowledge is needed to adapt an advertiser’s media strategy to differing media consumption trends and habits. Third, even though only high-level strategies and ideas may be defined on an international basis, the most important part of the services offered by MBS agencies is still performed on a national basis.

53. In addition, the Parties reject any additional segmentation of MBS into markets that would be narrower than national, as most campaigns are national in scope, and most media channels cover the whole territory of a country

54. Responses to the market investigation differed with regard to the geographic scope of the sales-side of the market for MBS. On the one hand, a majority of customers indicated that, in many cases, their contracts with MBS suppliers have in a large proportion a national dimension.42 On the other hand, a majority of competitors considered that many advertisers have a global media strategy and customise the experience for geographic and national considerations. Moreover, a number of competitors noted the rise of digital media and the appearance of large global digital groups, which allows global or regional negotiations and buying.43

55. In any event, for the purposes of the present Decision, it is not necessary to conclude on whether the sales side of the market for MBS should be national or wider than national (EEA-wide) because the Transaction does not raise serious doubts under any alternative geographic market definition.

IV.1.1.2.2. Procurement of media buying services

56. In WPP/Grey, the Commission considered that the procurement market for MBS was national in scope, notably due to the fact that as most advertisers and media buying agencies need to advertise in the national media, they require their media buying agencies to purchase time or space with national TV broadcasters or publishers.44 Furthermore, the Commission considered in Google/DoubleClick that the market for online advertising space could be EEA-wide in scope from a technical point of view, but concluded that this market is to be considered as segmented alongside national or linguistic borders within the EEA.45

57. The Parties do not contest such an approach and submit that advertising is directed to the area where media owners have their main audience. As media advertising is intrinsically linked to media broadcasting, and media broadcasting is national, negotiations for media owners’ advertising inventory take place at national level.

58. The view of the Parties was supported by the market investigation, as the majority of respondents indicated that the market for procurement of advertising time and/or space is national in scope.46

59. In light of the above, for the purposes of the present Decision, the Commission considers that the procurement side of the MBS market, segmented along different types of media, in each of the EEA countries where the Parties operate, is national.

IV.1.2 MARKETING AND COMMUNICATION SERVICES

IV.1.2.1. PRODUCT MARKET

60. In WPP/Grey, the Commission considered that the relevant product market for the provision of MCS encompasses an array of disciplines including advertising, insight and consultancy, public relations, consumer relationship management/direct marketing/event management, brand identity and design and other areas of specialist communications.47

Segmentation by type of service

61. The Commission considered in past decisions that all MCS belonged to the same relevant market and that a further segmentation would not have reflected the way in which these disciplines were demanded and offered.48 The Commission also considered that the types of MCS represented different methods for a business to communicate with a group of people, be they consumers/customers, the press, industry, other companies, government and other regulatory bodies and that all these disciplines were substitutable to a sufficient extent and that most agencies were able to offer all type of disciplines.

62. The Parties submit that the Commission's previous conclusions should be upheld.49 First, both large international network and country-specific independent agencies tend to offer the full range of disciplines to clients to create and deliver a coherent and consistent brand message across different media channels. Few agencies choose to specialise in one particular MCS discipline and even those that do are likely in practice to provide more than one MCS discipline.

63. Second, although customers may purchase single disciplines from different providers for specific projects, they expect and demand that agencies provide services across all or most types of MCS disciplines.

64. Third, segmentation by type of MCS discipline is meaningless in light of the significant blurring of the lines between different disciplines brought about in recent years by the increased use of digital resources.50

65. In general, respondents to the market investigation indicated that the different MCS disciplines are substitutable both from the supply and demand side perspective.51

66. Although small independent agencies may specialise in a given MCS discipline, a majority of respondents to the market investigation pointed out that a majority of agencies aim to provide an integrated offer to customers. Likewise, a majority of customers indicated that they purchase a variety of MCS disciplines to achieve the same goal of communicating with a group of people.

67. The Commission is of the view that MCS disciplines may be purchased on a stand-alone basis for a given project or as part of a wider strategy or campaign. Furthermore, customers may instruct either individual agencies or a number of agencies. This indicates that different MCS discipline and types of agencies could be used to design a creative message for a campaign and that fully-fledged and more specialised agencies compete with each other for the provision of these disciplines.

68. Even if one competitor that replied to the market investigation referred to a possible separation of public relation ("PR") from other MCS disciplines, no one else raised the issue regarding the need to consider a segmentation for PR, as such disciplines are not usually provided on a stand-alone basis, but rather are offered by large agencies alongside a wide range of other MCS disciplines.52

69. In light of the above, the Commission concludes that all MCS disciplines are part of the same market, since the different types of MCS are substitutable to a sufficient extent, and most agencies offer all or most MCS disciplines to their customers.

Segmentation by type of media

70. The Commission has previously left open whether it would be appropriate to segment MCS by media channel.53

71. The Parties consider that a further segmentation by media channel (including the Internet) would be artificial. First, from a demand-side perspective, advertisers purchase MCS irrespective of the media channel where the message or the advertising campaign will be placed, as they are interested in targeting a broad audience and in conveying a coherent and consistent message across all media.

72. Second, from a supply-side point of view, agencies create messages and insights with a multi-channel approach, without focusing on a specific type of media.

73. Third, traditional advertising can easily be adapted for on-line publication. In that respect, there are no barriers to entry for a traditional agency to create advertising for online distribution. Pure digital MCS agencies compete thus with traditional players.

74. A majority of respondents to the market investigation indicated that MCS are provided through all types of media, including the Internet. In particular, several respondents indicated that agencies are expected to deliver consistency and recognise interconnectivity between different channels and thus are not requested to provide aservice tailored according to media type. In addition, media channels are seen as different ways to convey a message and to reach different targeted audiences.54 This question of whether MCS should be segmented by media channel is a different one to whether for an advertiser the placement of an online advertisement is substitutable with the placement of an advertisement on an offline media channel. This latter question does not need to be answered in the present Decision.

75. In light of the above, the Commission concludes that no additional segmentation of the MCS market by type of media is necessary when assessing the present Transaction.

Segmentation by type of sector

76. In past decisions55, the Commission has investigated whether a separate market for the provision of specialist communications advice, such as to the healthcare sector, exists.

77. The Parties acknowledge that while certain sectors present specificities, these are insufficient to justify a further segmentation of the market. The Parties refer in support of their submission to the healthcare sector. On the one hand, the communication of messages about drugs and medical products is strictly limited as regards the content and the audience that can be targeted, with the result that agencies prefer to organise their MCS activities in the healthcare sector separately. On the other hand, the MCS skills and tools in this sector are the same as those necessary to carry out MCS in non- regulated sectors.

78. While a minority of respondents to the market investigation pointed out that certain sectors, such as healthcare, requires specialised MCS agencies, a majority of respondents considered that their sectors of activity do not require specific knowledge, expertise, skills and tools that only certain MCS agencies can address.56

79. In light of the above, the Commission concludes that no additional segmentation of the MCS market by type of sector is necessary when assessing the present Transaction.

Segmentation by size of account

80. In past decisions57, the Commission left open whether large-scale customers that develop international budget and campaigns constitute a distinct market. On the one hand, the Commission noted that the supply of international MCS may require specific implementation needs that are not necessary for the provision of MCS at national level and that can be successfully offered only by large-scale MCS agencies. On the other hand, the evidence the Commission gathered was insufficient to support the definition of a distinct market for the provision of international MCS.

81. The issue was not meaningfully addressed by the Parties in their submissions.

82. Even though certain respondents pointed out that only large-scale agencies may be appointed by multi-national customers to deliver global campaigns, as they are the only ones able to offer the required scale of resources and network to ensure implementation of the campaign across different countries, a majority of respondents to the market investigation indicated that the supply of international MCS should not be considered as a distinct market. In particular, these respondents indicated that any agency can be selected by large-scale customers as advertising services mostly depend on creativity which can also be provided by a small agency.58

83. In light of the above, the Commission concludes that no additional segmentation of the MCS market by size of account is necessary when assessing the present Transaction. The specific needs of large, multinational, customers will, however, be taken into account in the assessment of the Transaction.

IV.1.2.2. GEOGRAPHIC MARKET

84. In WPP/ Grey, the Commission considered that the market for MCS was national in scope, even with regard to large, multinational, customers, because of language differences, different media conditions, pricing differences between countries and the need to inform the public, government or other institutions and therefore plan a campaign on a national basis.59

85. The Parties submit that the Commission's conclusions in WPP/Grey are still valid, even with reference to multinational customers, as campaigns continue to be designed mostly on a national basis.

86. Even if a majority of the respondents to the market investigation did not express a view on whether the conclusions drawn in WPP/Grey are still valid today, a majority of the customers that expressed their opinion replied affirmatively, whereas answers were more nuanced among competitors. In particular, competitors acknowledged that MCS contracts are mostly national in scope, while referring to a tendency towards globalisation, especially in relation to customers with an international footprint. However, a majority of the respondents to the market investigation stated that MCS contracts have mostly national coverage.60

87. Given the still high percentage of national coverage of MCS contracts, the Commission takes the view that the conclusion drawn in WPP/Grey are still valid, and the MCS markets are national in scope.

Conclusion

88. In light of the above, the competitive assessment of the Transaction will be based on the provision of MCS in each EEA country where the Parties are present.

IV.1.3 SALE OF ADVERTISING SPACE IN CINEMAS

IV.1.3.1. PRODUCT MARKET

89. The Commission has so far never considered whether the sale of cinema advertising constitutes a separate market or should be considered as part of the global market for the sale of advertising space in all media.

90. However, in past decisions relating to other media channels, the Commission has considered that the supply of advertising space and time in certain media channels, such as TV, outdoor and radio, could be considered as a separate product market. In particular, the Commission has considered as a separate market the market of advertising space on TV, while it has left open the exact market definition in relation to the provision of advertising space for outdoor and radio.61

91. The Parties consider that the exact scope of the relevant product market can be left open in this case, as the Transaction does not raise any serious doubts under any possible market definition.

92. For the purpose of the present Decision, the Commission agrees that the exact scope of the relevant product market can be left open because the Transaction does not raise serious doubts under any possible market definition.

IV.1.3.2. GEOGRAPHIC MARKET

93. The Commission has considered in previous decisions62 that the procurement side of the MBS market, which is a downstream market of the market for the sale of advertising space or time, is national in scope, as most advertisers and media buying agencies need to advertise in the national media.

94. The Parties have not expressed any specific view on the possible geographic scope of the relevant market beyond the statements it has made regarding the national dimension of procurement markets, where negotiations for the advertising inventory of media owners take place at national level (see Section IV.1.1.2.2).

95. In light of the above, the Commission concludes that the markets for the sale of advertising space in cinema are also national in scope.

IV.2. METHODOLOGIES FOR ESTIMATING MARKET SHARES FOR MEDIA BUYING SERVICES

96. The Commission will first present the methodologies proposed by the Parties on of the sales and procurement sides for estimating the total MBS market size and the Parties' and their competitor's market shares (Section IV.2.1). The Commission will then conduct its own assessment of the Parties' proposed methodologies (Section IV.2.2).

IV.2.1 METHODOLOGIES PROPOSED BY THE PARTIES

IV.2.1.1. SALES SIDE

IV.2.1.1.1. Estimates of market size and market shares of the Parties

97. The Parties have provided estimated market sizes for the MBS markets in the EEA countries where the activities of the Parties overlap from industry reports that cover these countries, such as the ZenithOptimedia Advertising Expenditure Forecasts for 2012 released in June (the "ZenithOptimedia report")63, the World Advertising Research Center 2012 Reports released on 9 September 2013 (the "WARC report")64, the Group M report "This Year, Next Year"65 (the "Group M report") and other national reports.

98. As to the calculation of their own market shares, the Parties have primarily used their own revenues and the market size estimated in the ZenithOptimedia and the WARC reports. According to the Parties, these two reports are reliable benchmarks for total market size estimates, and the market shares estimated using either source are broadly consistent – see sub-section (a) below. In addition, the other sources which the Parties have used will be described in sub-section (b) below.

(a) The ZenithOptimedia report and the WARC report

99. The ZenithOptimedia report includes annual reports estimating advertising expenditure by country and is produced by ZenithOptimedia, which belongs to the Publicis Group. The ZenithOptimedia report excludes agency commissions and seeks to estimate the net cost of media purchasing.66 It relies both on surveys of advertisers, agencies and media owners, and on data containing advertising volumes and advertising rate cards.

100. The Parties have used the WARC report as an alternative source for estimating the total market size. WARC collects data on advertising expenditure in the same way as ZenithOptimedia, primarily through an annual survey.

101. The main difference between the two methodologies used for producing the two reports is that the WARC report seeks to incorporate agency commissions and fees whereas the ZenithOptimedia report seeks to exclude them.

102. For the purpose of estimating their own market shares, the Parties have used their own revenues in two different manners for consistency with the methodologies used by the ZenithOptimedia report and the WARC report respectively: (i) when using the ZenithOptimedia market size, they divided their media purchase costs by the ZenithOptimedia report market size (that is to say they excluded their own fees and commissions from their total revenues); and (ii) when using the WARC report market size, they divided their total revenues by the WARC report market size (that is to say they included their agency fees and commissions).67 The Parties did so in order to allow the Commission to verify whether the inclusion of agency commissions and fees would materially change the Parties’ market share estimates.

103. The Parties submit that their own market shares using media purchase costs and the total market size from the ZenithOptimedia report are close to their shares using total revenues and the total market size from the WARC report. The market size estimates in the WARC report are similar to the market size estimates in the ZenithOptimedia report, although typically slightly higher, which is likely because of the inclusion of agency commissions and fees. The Parties further submit that no adjustment to the WARC report estimated market size is necessary as was done at the time of the WPP/Grey decision68 which mentioned that the WARC report’s estimates of the total size of the market were based on rate cards, and did not take into account discounts granted by media vendors. This implied that, at that time, the WARC report data over-estimated the total size of the market and thus needed to be scaled down to account for discounts granted by media vendors. The Parties explain that today, the WARC report as used by the Parties indicates that, for all EEA countries, data taking into account the discounts. Therefore, the WARC report is sufficiently reliable as such and there is no need to“scale down” WARC-produced data.69

(b) Other sources for estimating the market size and the Parties' market shares

104. The Parties have also provided other sources for estimating the MBS market size in the overlap EEA countries

105. In particular, the Parties have provided the Group M report which estimates media expenditures per country. Group M is WPP's media buying organisation. In addition, the Parties have provided advertising expenditure estimations by Nielsen in all EEA countries where, to the Parties’ best knowledge, such estimations, exist, albeit even partially.70 In certain EEA countries, the Parties have provided the total market size as estimated by national local sources such as IREP Communication and Kantar in France or Infoadex in Spain.

106. The Parties have provided the market size as estimated in the reports of the Research Company Evaluating the Media Agency Industry (RECMA), namely the Overall Activity Ranking reports (the "RECMA reports").71

107. As regards the calculation of their own market shares, the Parties have provided three additional methodologies: (i) the Parties have divided their media purchase costs by the total market size calculated in the Group M report72; (ii) they have calculated their own market shares by using their actual revenues and the total market size as estimated in the RECMA reports; and (iii) they have provided the market shares as estimated in the RECMA reports (that is to say without calculating their shares on the basis of their real revenues).

108. However, according to the Parties, the RECMA reports suffer from several important shortcomings. First, the RECMA reports focus only on larger agencies and do not take into account direct sales, thus excluding part of demand, which introduces a downwards bias in the RECMA reports' total demand. Second, as of its 2013 reports, RECMA no longer reports buying billings; instead, it reports a measure it refers to as "Overall Activity". This measure includes several categories of services in addition to media buying and planning, including digital services, diversified services and international account coordination. This introduces an upwards bias into the Overall Activity when considered as a measure of MBS demand size. Third, the Parties know from their actual data that the RECMA reports considerably overstate the Parties’ own activity in many EEA countries. Fourth, in Bulgaria, Estonia, Finland, Ireland and Slovakia, RECMA allocates billings to the Parties from entities that are not controlled by them. Such overestimation is likely to affect all agencies covered by the RECMA reports but the Parties do not know the degree of the overestimation of their competitors’ activity. Fifth, the RECMA reports are only used by the industry to assess relative rankings of agencies rather than demand size or market shares.

109. The Parties believe that all these shortcomings prevent the RECMA reports from being a reliable estimate of total market size and of their own market shares.

IV.2.1.1.2. Competitors' market share estimates

110. The Parties submit that neither the ZenithOptimedia report, nor the WARC report provide data broken down by competitor, so these sources cannot be used to estimate market shares of their competitors

111. The Parties submit that the RECMA reports are the only data source that provide billings estimates for large international groups, and provide the Parties with at least some means to estimate the shares of competitors. While some information on competitor rankings can be deduced from the RECMA reports73, the Parties explain that there are several important shortcomings with the RECMA reports. First, the RECMA reports focus on large global groups and ignore most independent media buyers. Second, RECMA limits research to large accounts (above a certain threshold which varies by country, typically EUR 1 000 000). Third, the RECMA reports do not include direct media purchasing performed in-house by advertisers. Fourth, RECMA relies on data and assumptions which, according to the Parties, are not robust – for example, it assumes that purchasers pay full advertising rate card rates to build up gross billings activity and does not adequately adjust for the discounts which are achieved in reality. As a result, RECMA grossly overestimates the billings and shares of the major global networks.74 Such overestimation of global network activity comes at the expense of the many independent media buying agencies that are not accounted for in the RECMA reports and which compete vigorously with the Parties for major MBS accounts.

112. To adjust for the fact that the RECMA reports overstate the gross billing activities of international groups, the Parties attempted to estimate the size of media buying activity that was not accounted for in the RECMA reports, which includes independent media buyers and direct media purchases. The remainder of the ZenithOptimedia-estimated market size was allocated among the competitors tracked by the RECMA reports in the same proportion to one another as in the RECMA reports.

IV.2.1.2. PROCUREMENT SIDE

113. The Parties have provided estimated shares of media purchases by media channel following the same methodology as for MBS sales, using their own media purchases by channel and the market size estimated in the ZenithOptimedia report, which is also available by media channel. In addition, the Parties have also provided estimates of the share of the Internet channel within the 2012 total advertising expenditures at the EEA- level as provided by the ZenithOptimedia report.

114. The Parties have not estimated their combined market shares on each media channel excluding direct sales, except for Denmark and Sweden, due to the specifics of these countries (see Section IV.2.2.2.).

115. The Parties have been unable to provide market shares of competitors on each media channel. They explained that the only relevant data source that provides billing estimates for competitors is the RECMA reports which however, do not provide any information by media channel. The Parties have further explained that they do not know the actual MBS revenues, media purchase costs and billings of their competitors and that therefore they have no data to split these by media channel.

IV.2.2 COMMISSION'S ASSESSMENT

IV.2.2.1. SALES SIDE: MARKET SIZE AND MARKET SHARES (FOR THE

PARTIES AND THEIR COMPETITORS)

116. The Commission has conducted an in-depth assessment of the methodologies used by the Parties to assess their own market shares and to the extent possible the market shares of their competitors. The Commission engaged with the main MBS competitors of the Parties in order to test the methodologies relied on by the Parties. In addition, the Commission has sought to obtain MBS revenue information from the Parties' competitors.

(a) Market size and market shares of the Parties

117. The main competitors of the Parties were first asked whether the methodologies used by the Parties to calculate the Parties' combined market shares (using the ZenithOptimedia report and the WARC report) was appropriate and, if not, whether they could suggest alternative methodologies to the ones proposed by the Parties.

118. The main competitors of the Parties considered that the Parties' proposed methodologies for estimating the total market size were generally reasonable. Competitors also cited other sources for estimating the total market size, which the Parties provided to the Commission (see Section IV.2.1 above).

119. The Commission notes that when comparing the total market sizes estimated in the various sources provided by the Parties75, in most countries, the smallest market size is estimated in the ZenithOptimedia report, the WARC report or the Group M report. For the EEA countries in which this is not the case, the difference in the estimated market size does not lead to any material differences in the combined market shares of the Parties.76

120. As a result, the Commission considers that a comparison of the Parties' combined market shares on the basis of these three sources appears reasonable. Table 1 below provides the overview of the Parties' combined market shares on the MBS sales market based on the market size as estimated in each of the ZenithOptimedia, WARC, and Group M reports

Table 1: Overview of Parties’ combined share on the MBS market

Country | Zenith Optimedia | WARC | Group M |

Austria | [5-10]% | [5-10]% | [5-10]% |

Belgium | [5-10]% | [10-20]% | [10-20]% |

Croatia | [0-5]% | [10-20]% | [10-20]% |

Czech Rep | [20-30]% | N/A78 | [20-30]% |

Denmark | [10-20]% | [10-20]% | [10-20]% |

France | [20-30]% | [10-20]% | [10-20]% |

Germany | [10-20]% | [10-20]% | [10-20]% |

Greece | [5-10]% | [10-20]% | [5-10]% |

Hungary | [10-20]% | [10-20]% | [20-30]% |

Ireland | [10-20]% | [5-10]% | [10-20]% |

Italy | [20-30]% | [10-20]% | [10-20]% |

Latvia | [20-30]% | [20-30]% | [20-30]% |

Lithuania | [10-20]% | [20-30]% | [10-20]% |

Netherlands | [5-10]% | [10-20]% | [5-10]% |

Poland | [30-40]% | [30-40]% | [20-30]% |

Portugal | [20-30]% | [5-10]% | [20-30]% |

Romania | [30-40]% | [30-40]% | [30-40]% |

Slovenia | [0-5]% | [5-10]% | [10-20]% |

Spain | [20-30]% | [20-30]% | [10-20]% |

Sweden | [10-20]% | [10-20]% | [10-20]% |

United Kingdom79 | [20-30]% | [10-20]% | [20-30]% |

Norway | [10-20]% | [10-20]% | [10-20]% |

EEA | [10-20]% | [10-20]% | [10-20]% |

Source: Form CO, Annex 38 (updated for the United Kingdom). All MBS share are based on the latest reports available (ZenithOptimedia, WARC and Group M). The Parties are not aware of any events that would materially alter their estimates after the publication of these reports.

121. As can be seen in Table 1, Austria, Croatia, Denmark, Germany, Greece, Ireland, the Netherlands and Sweden are not affected markets under any of the three sources on the sales side of the MBS market.

122. Table 1 further shows that if estimated by using the market size in the ZenithOptimedia report in all EEA countries where the activities of the Parties overlap except for Slovenia, the estimated combined market shares of the Parties are either at their highest or not significantly different from the other sources. While the difference in the total market size estimations is also rather high in Croatia, the Transaction does not lead to an affected market under any of the three sources. The Commission therefore considers that it is appropriate to conduct its competitive assessment using market shares of the Parties calculated on the basis of the ZenithOptimedia report in all EEA countries except for Slovenia.

123. In Slovenia, the ZenithOptimedia report estimates of the market size are significantly higher than the other two reports, WARC and Group M, leading to an affected market under one methodology. As the Group M report excludes certain types of media and therefore underestimates the total market size, the Commission will consider the WARC report for the purpose of assessing the competitive effects on the sales side market for media buying services in Slovenia.

124. The Parties also provided information regarding their combined market shares if direct sales were excluded from the total market size (that is to say media sold directly by media vendors to advertisers, rather than through a media buying agency). Table 2a below shows the Parties' estimates of the level of direct buying in each EEA country. ;Using these estimated shares of direct sales, Table 2b shows the Parties market shares excluding direct sales from the total market size80:

Table 2a: Parties’ estimates of level of direct sales per EEA country

Source: Paragraph 346 of the Form CO.

Table 2b: Parties’ MBS share estimates excluding direct sales

Country | Omnicom | Publicis | Combined |

Austria | [0-5]% | [0-5]% | [5-10]% |

Belgium | [5-10]-[5-10]% | [5-10]-[5-10]% | [10-20]-[10-20]% |

Croatia (WARC) | [5-10]% | [5-10]% | [10-20]% |

Czech Rep | [10-20]-[10-20]% | [10-20]-[10-20]% | [20-30]-[20-30]% |

Denmark | [10-20]-[20-30]% | [5-10]-[5-10]% | [20-30]-[20-30]% |

France | [5-10]-[5-10]% | [10-20]-[10-20]% | [20-30]-[20-30]% |

Germany | [5-10]-[5-10]% | [0-5]% | [10-20]-[10-20]% |

Greece | [5-10]% | [0-5]% | [10-20]% |

Hungary | [10-20]% | [10-20]-[10-20]% | [20-30]-[20-30]% |

Ireland | [5-10]-[5-10]% | [0-5]% | [10-20]-[10-20]% |

Italy | [10-20]-[10-20]% | [10-20]-[10-20]% | [20-30]-[30-40]% |

Latvia | [10-20]-[10-20]% | [5-10]% | [20-30]-[20-30]% |

Lithuania | [10-20]% | [5-10]% | [10-20]-[10-20]% |

Netherlands | [5-10]-[5-10]% | [5-10]-[5-10]% | [10-20]% |

Poland | [10-20]-[10-20]% | [20-30]-[20-30]% | [30-40]-[30-40]% |

Portugal | [10-20]-[10-20]% | [10-20]-[10-20]% | [20-30]-[20-30]% |

Romania | [5-10]% | [20-30]-[20-30]% | [30-40]-[30-40]% |

Slovenia (WARC) | [5-10]% | [0-5]% | [5-10]% |

Spain | [5-10]-[5-10]% | [10-20]-[10-20]% | [20-30]-[20-30]% |

Sweden | [10-20]-[10-20]% | [10-20]-[10-20]% | [20-30]-[20-30]% |

United Kingdom | [10-20]% | [10-20]% | [20-30]-[20-30]% |

Norway | [10-20]% | [5-10]% | [10-20]-[10-20]% |

EEA | [5-10]-[5-10]% | [5-10]% | [10-20]-[10-20]% |

Source: ZenithOptimedia market size - Annex 14/R30 for all EEA countries except for Croatia and Slovenia for which WARC market size- Annex R25.

125. As can be seen from Table 2b, Austria, Croatia, Germany, Greece, Ireland, the Netherlands and Slovenia are not affected markets even if direct sales are excluded from the MBS market.

126. According to the Parties, excluding direct sales would artificially increase the Parties’ market shares. However, as explained in paragraphs 48 and 49 above, it is not necessary to decide whether direct sales belong to the same market for MBS in all EEA countries where the activities of the Parties overlap (except for Sweden and Denmark, where they have to be included for reasons specific to these two countries), as the Transaction does not raise any serious doubts under any alternative product market definition.

127. Therefore, the Commission will conduct its competitive assessment on a market including and excluding direct sales and will consider the competitive constraint exercised by direct sales in each country.

(b) Market shares of competitors

128. The Parties' main competitors were also asked whether the Parties' methodology for estimating the market shares of their competitors (using the relative rankings in the RECMA reports) was appropriate, and, if not whether they could suggest an alternative methodology to the one proposed by the Parties.

129. The Parties' main competitors consulted on the methodology issue responded that they considered the approach proposed by the Parties to be a suitable starting point for an analysis of market shares on the sale side for the MBS market. Certain of these competitors also stated that they use the market shares estimated in the RECMA reports in the course of their business to gain a better understanding of the rankings of the various agencies on the markets. However, certain of these competitors also raised certain shortcomings in the RECMA reports as described by the Parties

130. Table 3 below provides an overview of the Parties' estimates of the market shares of competitors:

Table 3: MBS shares of Parties and competitors, 2012 (%)81

Country | Omnico m |

Publicis | Combi ned | Dentsu- Aegis |

WPP |

Havas |

IPG | Indepen- dents |

Others |

|

|

|

|

| [30- |

| [10- |

|

|

Austria | [0-5] | [0-5] | [5-10] | [5-10]- [5-10] | 40]- [30- | [0-5]- [0-5] | 20]- [10- | [10-20]- [20-30] | [10-20]- [20-30] |

|

|

|

|

| 40] |

| 20] |

|

|

Belgium |

[0-5] |

[5-10] |

[5-10] | [10- 20]- [10- 20] | [10- 20]- [10- 20] | [5-10] - [5-10] | [10- 20]- [10- 20] |

[0-5]- [0-5] |

[40-50]- [50-60] |

Country | Omnico m |

Publicis | Combi ned | Dentsu- Aegis |

WPP |

Havas |

IPG | Indepen- dents |

Others |

|

|

|

|

|

|

| [10- |

|

|

Croatia (WARC) | [5-10] | [5-10] | [10-20] | [0-5]- [0-5] | [10- 20] | [0-5] | 20]- [20- | [40-50]- [50-60] | [10-20]- [10-20] |

|

|

|

|

|

|

| 30] |

|

|

|

|

|

|

| [10- |

|

|

|

|

Czech Republic | [10-20] | [5-10] | [20-30] | [0-5]- [5-10] | 20]- [20- | [0-5]- [0-5] | [0-5]- [5-10] | [10-20]- [10-20] | [30-40]- [40-50] |

|

|

|

|

| 30] |

|

|

|

|

Denmark |

[5-10] |

[0-5] |

[10-20] | [5-10]- [10- 20] | [10- 20]- [10- 20] |

[0-5] |

[0-5]- [5-10] |

[0-5] |

[50-60]- [60-70] |

|

|

|

| [10- | [10- | [10- |

|

|

|

France | [5-10] | [10-20] | [20-30] | 20]- [10- | 20]- [10- | 20]- [10- | [0-5]- [0-5] | [0-5] | [20-30]- [30-40] |

|

|

|

| 20] | 20] | 20] |

|

|

|

|

|

|

| [10- | [30- |

|

|

|

|

Germany | [5-10] | [0-5] | [10-20] | 20]- [10- | 40]- [40- | [0-5]- [0-5] | [5-10] | [10-20]- [10-20] | [10-20]- [20-30] |

|

|

|

| 20] | 50] |

|

|

|

|

|

|

|

|

| [30- |

| [10- |

|

|

Greece | [5-10] | [0-5] | [5-10] | [5-10]- [5-10] | 40]- [40- | [0-5] | 20]- [10- | [5-10]- [5-10] | [10-20]- [20-30] |

|

|

|

|

| 50] |

| 20] |

|

|

Hungary |

[5-10] |

[5-10] |

[10-20] | [10- 20]- [10- 20] | [20- 30]- [20- 30] | [5-10] - [5-10] | [10- 20]- [10- 20] |

[0-5] |

[20-30]- [30-40] |

Ireland |

[5-10] |

[0-5] |

[10-20] | [10- 20]- [20- 30] | [20- 30]- [20- 30] |

[0-5] | [5-10] - [5-10] |

[20-30]- [20-30] |

[10-20]- [20-30] |

|

|

|

| [10- | [20- |

|

|

|

|

Italy | [10-20] | [10-20] | [20-30] | 20]- [10- | 30]- [30- | [0-5]- [0-5] | [0-5]- [0-5] | [0-5]- [0-5] | [20-30]- [30-40] |

|

|

|

| 20] | 40] |

|

|

|

|

Latvia |

[10-20] |

[5-10] |

[20-30] | [5-10]- [10- 20] | [10- 20]- [10- 20] | [5-10] -[10- 20] | [10- 20]- [10- 20] |

[5-10]- [5-10] |

[20-30]- [30-40] |

Lithuania |

[5-10] |

[5-10] |

[10-20] | [10- 20]- [10- 20] | [10- 20]- [10- 20] | [5-10] - [5-10] | [10- 20]- [10- 20] |

[0-5] |

[30-40]- [40-50] |

Country | Omnico m |

Publicis | Combi ned | Dentsu- Aegis |

WPP |

Havas |

IPG | Indepen- dents |

Others |

Netherlands |

[5-10] |

[0-5] |

[5-10] | [5-10]- [10- 20] | [20- 30]- [30- 40] |

[0-5] | [10- 20]- [10- 20] |

[0-5] |

[30-40]- [40-50] |

Poland |

[10-20] |

[20-30] |

[30-40] |

[5-10] | [30- 40]- [30- 40] |

[0-5]- [5-10] | [5-10] - [5-10] |

[0-5] |

[10-20]- [20-30] |

|

|

|

|

| [20- | [10- | [10- |

|

|

Portugal | [10-20] | [5-10] | [20-30] | [5-10]- [5-10] | 30]- [20- | 20]- [10- | 20]- [10- | [0-5] | [10-20]- [20-30] |

|

|

|

|

| 30] | 20] | 20] |

|

|

|

|

|

|

| [10- |

| [10- |

|

|

Romania | [5-10] | [20-30] | [30-40] | [0-5]- [0-5] | 20]- [10- | [0-5] | 20]- [10- | [10-20]- [10-20] | [20-30]- [30-40] |

|

|

|

|

| 20] |

| 20] |

|

|

Slovenia (WARC) |

[0-5] |

[0-5] |

[5-10] | [10- 20]- [10- 20] | [10- 20]- [10- 20] |

[0-5] | [5-10] -[10- 20] |

[50-60]- [50-60] |

[5-10]- [10-20] |

|

|

|

| [10- | [10- | [20- |

|

|

|

Spain | [5-10] | [10-20] | [20-30] | 20]- [10- | 20]- [10- | 30]- [20- | [0-5] | [5-10]- [5-10] | [10-20]- [20-30] |

|

|

|

| 20] | 20] | 30] |

|

|

|

|

|

|

|

| [5- |

|

|

|

|

Sweden | [5-10] | [5-10] | [10-20] | [0-5]- [5-10] | 10]- [10- | [0-5] | [0-5]- [0-5] | [0-5]- [0-5] | [60-70]- [70-80] |

|

|

|

|

| 20] |

|

|

|

|

United Kingdom |

[10-20] |

[10-20] |

[20-30] | [5-10]- [10- 20] | [20- 30]- [20- 30] |

[0-5]- [0-5] |

[0-5]- [0-5] |

[0-5] |

[30-40]- [40-50] |

|

|

|

| [10- |

|

|

|

|

|

Norway | [10-20] | [0-5] | [10-20] | 20]- [20- | [30-40]- [30-40] | [0-5] | [5-10] | [0-5] | [10-20]- [20-30] |

|

|

|

| 30] |

|

|

|

|

|

EEA |

[5-10] |

[5-10] |

[10-20] | [10- 20]- [10- 20] | [20- 30]- [20- 30] | [5-10] - [5-10] | [5-10] - [5-10] |

[5-10]- [5-10] |

[20-30]- [30-40] |

Source: Table 43 of the Form CO, as amended for the United Kingdom in Annex R30. For Croatia and Slovenia, the Parties' combined market shares are calculated on the basis of the WARC report

131. The Commission obtained revenue information during the market investigation from certain of the Parties’ competitors (including from certain independent agencies). The Commission compared the actual revenues of the Parties and of these competitors on the overlap EEA countries with the revenues estimated in the RECMA reports. The Commission found that the RECMA reports may heavily over- or underestimate the revenues of both the Parties and their competitors. Therefore, the Commission does not consider that the market size or the market shares as estimated in the RECMA reports are a sufficiently reliable source for the purpose of the present Decision in all EEA countries where the activities of the Parties overlap.

132. Furthermore, the Commission compared the market shares of the competitors as estimated by the Parties with the market shares these competitors would have if considering the market size estimated in the ZenithOptimedia report. The Commission found that for some EEA countries, the relative rankings of the Parties versus their competitors is different from the Parties' estimates in Table 3 above in that the Parties' underestimate their own shares compared to their competitors or overestimate their competitors' shares. This can be explained by the fact that the Parties used the relative rankings in the RECMA reports for estimating their competitors' relative positions, which, as explained above, is not sufficiently reliable. However, despite the existence of such differences in the relative rankings, this does not change the Commission's conclusions with regard to the competitive assessment that it has conducted on all relevant markets (see Section IV.4.1).

133. Considering all the above, and the other available evidence, after having analysed the revenue data of certain of the Parties' competitors insofar as such information was available and of the Parties independently, the Commission considers that the methodology used by the Parties, relying on the ZenithOptimedia report and using actual media cost for calculating their own individual and combined market shares, is sufficiently reliable82 as a starting point for the purpose of assessing the Transaction.

134. As to the market shares of the Parties’ competitors, the Commission notes that there are some discrepancies in the relative rankings; however despite these discrepancies, the Commission's conclusions as set out in Section IV.4.1 remain materially the same.

IV.2.2.2. PROCUREMENT SIDE

135. The Commission considers that the methodology provided by the Parties for estimating their combined market shares on the procurement side on each media channel is sufficiently reliable. The Parties relied on the ZenithOptimedia report for providing the split by media channel and calculated their own market shares by using their actual media purchase cost data. As explained in Section IV.2.2, the Commission considers that the ZenithOptimedia report is sufficiently reliable for the purpose of the present Decision.

136. Table 4 presents the Parties’ combined market shares by media channel on the procurement side of the MBS markets:

Table 4: Parties’ combined MBS share estimates by media channel

| Country | TV | Radio | Outdoor | Online/M obile | Cinema | |

1. | Austria | [0-10]% | [0-10]% | [10-30]% | [0-10]% | [0-10]% | [0-10]% |

2. | Belgium | [10-30]% | [0-10]% | [0-10]% | [0-10]% | [10-30]% | [0-10]% |

3. | Croatia (WARC) | [10-30]% | [0-10]% | [0-10]% | [0-10]% | [10-30]% | N/A |

4. | Czech Republic | [30-50]% | [0-10]% | [10-30]% | [30-50]% | [10-30]% | [0-10]% |

5. | Denmark | [30-50]% | [0-10]% | [0-10]% | [10-30]% | [0-10]% | [10-30]% |

6. | France | [10-30]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% |

7. | Germany | [10-30]% | [0-10]% | [10-30]% | [10-30]% | [0-10]% | [0-10]% |

8. | Greece | [10-30]% | [0-10]% | [0-10]% | [10-30]% | [10-30]% | [0-10]% |

9. | Hungary | [10-30]% | [0-10]% | [10-30]% | [10-30]% | [0-10]% | [0-10]% |

10. | Ireland | [10-30]% | [0-10]% | [10-30]% | [10-30]% | [0-10]% | [0-10]% |

11. | Italy | [10-30]% | [10-30]% | [0-10]% | [50-70]% | [10-30]% | [30-50]% |

12. | Latvia | [10-30]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% |

13. | Lithuania | [10-30]% | [0-10]% | [0-10]% | [30-50]% | [10-30]% | [10-30]% |

14. | Netherlands | [0-10]% | [0-10]% | [10-30]% | [10-30]% | [0-10]% | [0-10]% |

15. | Poland | [30-50]% | [10-30]% | [10-30]% | [30-50]% | [10-30]% | [10-30]% |

16. | Portugal | [10-30]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% |

17. | Romania | [30-50]% | [30-50]% | [10-30]% | [10-30]% | [10-30]% | [0-10]% |

18. | Slovenia (WARC) | [0-10]% | [0-10]% | [0-10]% | [10-30]% | [10-30]% | [0-10]% |

19. | Spain | [10-30]% | [10-30]% | [10-30]% | [30-50]% | [10-30]% | [0-10]% |

20. | Sweden | [10-30]% | [0-10]% | [10-30]% | [10-30]% | [0-10]% | [10-30]% |

21. | United Kingdom | [30-50]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% |

22. | Norway | [30-50]% | [0-10]% | [0-10]% | [10-30]% | [0-10]% | [10-30]% |

| EEA | [10-30]% | [0-10]% | [10-30]% | [10-30]% | [10-30]% | [10-30]% |

Source: Table 46 to the Form CO as amended in Annex R27 for all EEA countries except the United Kingdom and Slovenia. Annex R30 for the United Kingdom and the WARC report for Croatia and Slovenia.

137. As mentioned above, for Slovenia, the Commission considers that the market size estimated by the ZenithOptimedia report is not sufficiently reliable. The Commission therefore uses the alternative WARC report to estimate the market shares split by type of media in Slovenia.83

138. As can be seen in Table 4 above, the Transaction will not lead to any affected markets on any type of media in Austria and Croatia. These two countries will therefore not be considered further for the purpose of the present Decision.

139. In the same way as for the sales side for MBS, the Commission has collected revenue information split by media type from the Parties' competitors during the market investigation. Having analysed the Parties' revenues and some of their main competitors' revenues, insofar as such information was available, the Commission is satisfied that the Parties' estimations are sufficiently reliable for the purpose of this Decision.

140. As regards the market shares on the media channels excluding direct sales, the Parties have not been able to provide the estimated share of direct sales by type of media in each country. Based on their experience, they estimate that the level of direct buying is generally lower in the TV channel than in the Internet and print channels.84 In particular in Denmark and Sweden, the two EEA countries where the activities of the Parties overlap and in which the direct sales represent on average a significant proportion of the total market, the Parties estimated that the share of direct sales would be 6% for TV and 16% for outdoor in Sweden, and 1% for TV in Denmark85.

141. In the light of the above and on the basis of all available evidence, the Commission considers that calculating the Parties' market shares on the basis of their actual media cost in each media type and the market size per media type as estimated in the Zenith Optimedia report is a reliable starting point for the purpose of assessing the Transaction.

IV.2.2.3. CONCLUSION

142. In light of all the above, the Commission considers that affected markets exist for the sales MBS markets when at least one of the three methodologies (ZenithOptimedia, WARC, Group M) or a country-relevant source, leads to combined market shares of the Parties of more than 15%, and regardless of whether direct sales are excluded. The following geographic markets, where both Parties are active in MBS, are therefore affected: Belgium, Czech Republic, Denmark, France, Hungary, Italy, Latvia, Lithuania, Poland, Portugal, Romania, Slovenia, Spain, Sweden, the United Kingdom, and Norway.

143. Furthermore, when considering market shares by media channel on the procurement side of the MBS markets, further geographic markets are affected (in addition to the EEA countries already mentioned above). These countries are: Germany, Greece, Ireland and the Netherlands.

IV.3. METHODOLOGIES FOR ESTIMATED MARKET SHARES FOR MARKETING AND COMMUNICATIONS SERVICES

IV.3.1 VIEWS OF THE PARTIES

144. The Parties state that due to the high fragmentation of the MCS market, there are few sources that estimate total market size by EEA country. To estimate their combined shares of supply for the MCS market, the Parties have used their own MCS revenues and the following sources: (i) Eurostat; (ii) Barnes 2013 Worldwide Advertising Agencies Industry report (the "Barnes Report"); (iii) and some local sources of information86

145. Eurostat compiles annual revenue data for advertising agencies and public relations and communications companies, by country. However, these revenues include media buying revenues that accrue within these companies. The most recently published data is for 2010. The Parties made a number of adjustments to this data in order to use it as a source of demand for their share of supply estimates

146. First, the Parties made an adjustment for growth to obtain an estimate of demand for 2011 and 2012. They assumed that the demand for MCS grew from 2010 to 2011 and 2012 at the same rate as the demand for MBS has grown. They therefore applied a growth rate based on the MBS growth in advertising expenditure (from ZenithOptimedia). Given that the purchase of media placements is closely linked to the supply of advertising itself (and the related MCS work that goes into producing that supply), MBS growth rate should be a relatively good proxy for MCS growth rate.

147. Second, the Parties subtracted MBS revenues from the Eurostat figures. To do this, they estimated the maximum amount of MBS revenues that could be included. ZenithOptimedia reports that MBS revenues are at most 15% of advertising expenditures. The Parties therefore reduced the Eurostat total revenues by that amount.

148. The Barnes Report calculates total revenues for advertising agencies by country, for 18 EEA countries.87 The demand estimates in the Barnes Report are slightly smaller, on average, than the adjusted Eurostat estimates (and about half of the size of the raw Eurostat data).

149. When available, the Parties also cross-checked the above estimates against the few country-specific sources of information with estimates of total agency advertising revenues.

150. According to the Parties, the combined entity estimated market shares from adjusted Eurostat figures and from Barnes do not materially differs and this conclusion is further supported by country-specific sources of information.

151. By discipline, the Parties have been able to calculate their share of supply only for PR as Eurostat provides only an estimation of the total revenues derived from PR services. This share is below [5-10]% in each EEA country. The Parties consider that as they are not relatively stronger in any particular MCS discipline, their shares in any one of these other disciplines would be of the same order of magnitude.

IV.3.2 COMMISSION'S ASSESSMENT

152. The Commission has assessed the methodologies used by the Parties to estimate their combined market shares. The Commission has also engaged with the Parties' four main MCS competitors in order to understand whether the methodology identified is appropriate to reflect the positioning of the Parties on the MCS market.

153. On the one hand, one of the four main competitors referred to a number of shortcomings regarding the methodologies used by the Parties. In particular, it mentioned that the sources proposed by the Parties are not recognised in the industry, that the data is out-of- date and that the adjustments and assumptions of the Parties are not sufficiently reliable.

154. On the other hand, another of the four main competitors indicated that examining revenues is an appropriate basis to estimate MCS market share but suggested to complement this data by revenue ranking from an industry publication such as Advertising Age. Another of the four main competitors acknowledged the evolution of the sector since the WPP/Grey decision and highlighted the importance of conducting an analysis of the current situation.

155. In WPP/Grey, the Commission estimated the MCS demand in EEA countries on the basis of the 2002 report issued by the U.S. organization Advertising Age. The Commission used this report with adjustments made to update data for MCS growth to 2002 and 2003.

156. However, the last Advertising Age report for individual European Member States ("Top Agencies in 146 Countries") dates back to 2002 and refers to estimates for 2001.

157. Therefore, the Commission considers that this report is not a good proxy to estimate MCS demand for 2012.