Commission, June 9, 2016, No M.7986

EUROPEAN COMMISSION

Judgment

SYSCO / BRAKES

Dear Sir/Madam,

Subject: Case M.7986 - Sysco / Brakes

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

(1) On 29 April 2016, the European Commission ('the Commission') received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the undertaking Sysco Corporation, a Delaware corporation ('Sysco'), proposes to acquire sole control within the meaning of Article 3(1) of the EU Merger Regulation over Cucina Lux Investments Limited, the holding company for the Brakes Group ('Brakes')3, by way of a purchase of shares ('the transaction'). Sysco is designated hereinafter as the 'Notifying Party'. Sysco and Brakes are collectively referred to as the 'Parties' while the undertaking resulting from the transaction is referred to as the 'merged entity.'

1. THE PARTIES AND THE CONCENTRATION

(2) Sysco is active in the sale, marketing and distribution of food and related products, such as catering equipment and supplies, to the foodservice industry. Sysco is primarily active in the United States and Canada. Within the EEA, Sysco is mainly active in the Republic of Ireland and Northern Ireland (UK) through its wholly owned subsidiary Pallas Foods Ltd ('Pallas'), with minor sales elsewhere.

(3) Brakes is active in the distribution of food and related products to the foodservice industry and also holds separate divisions specialising in catering supplies and equipment. Brakes is a supplier to the foodservice sector primarily in the United Kingdom, France, Sweden and the Republic of Ireland, with some minor activities also in Belgium, Germany, Italy, Luxembourg and Spain.

(4) Pursuant to a sale and purchase agreement ('SPA') dated 19 February 2016, Sysco will acquire sole control over Brakes through an acquisition of 100% of Brakes' shares. The SPA also provides for Brakes to acquire the remaining minority interests in a number of its subsidiaries, which will be transferred to Sysco post- transaction. Brakes already exercises sole control over these subsidiaries.

(5) The transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

2. UNION DIMENSION

(6) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million4 (Sysco: EUR 40 648 million; Brakes: EUR 5 109 million). Each of them has an Union-wide turnover in excess of EUR 250 million (Sysco: […]; Brakes: EUR […]), but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has an Union dimension.

3. RELEVANT MARKETS

3.1. Overview of the industry

(7) The transaction concerns the distribution of food and non-food products to the foodservice industry. Food products include both food and beverages and non-food products include catering equipment and catering supplies.

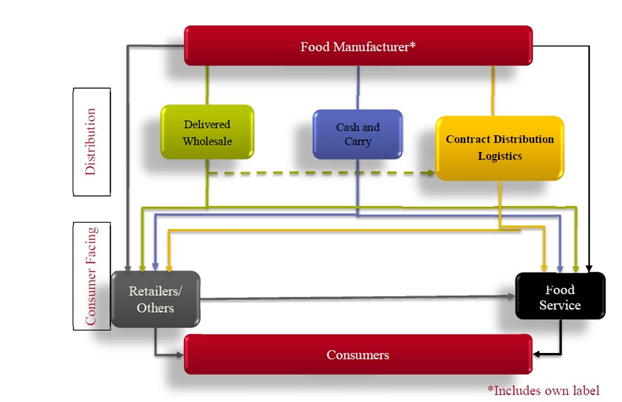

(8) There are four primary modes of supply in foodservice distribution, namely

(i) delivered wholesale, where the distributor purchases the products and handles the physical delivery to the customer's premises, (ii) contract distribution, where the customer negotiates supplies directly with manufacturers and the distributor provides a logistics solution for deliveries, (iii) cash and carry outlets, which offer a self-service model in which customers make purchases at the store and transport the purchased goods themselves, and (iv) retailers and others. These different modes of supply are illustrated in Figure 1 below.

Figure 1 The supply chain of food products, page 32 of the Form CO

(9) Both Parties are full range ("broadline") distributors, delivering a broad range of chilled, frozen and ambient food across all product categories and across all sectors of the foodservice industry and have delivered wholesale and contract distribution activities.

3.2. Product market definition

3.2.1. The Notifying Party's arguments

(10) The Notifying Party submits that the relevant market for the competitive assessment of the transaction should be the broad market for the supply of food and related non-food products to the foodservice industry. It also submits that all modes of supply exert a competitive constraint on each other and should be considered as part of the same market. Moreover, according to the Notifying Party, foodservice customers purchase a variety of product categories from a single distributor at different temperatures, delivered in a single load, so that no segmentation by product type is necessary. Furthermore, according to the Notifying Party, the requirements of the different customer groups are so similar that no segmentation by customer type is warranted; negotiations with all customers will focus on price, quality and delivery requirements.

3.2.2. Past decisional practice

(11) In previous decisions, the Commission,5 the French Autorité de la Concurrence,6 the UK Competition and Markets Authority ('CMA')7 and the Irish Competition and Consumer Protection Commission ('CCPC')8 considered the following possible segmentations for the market while leaving open the exact product market definitions:

a. segmentation into food and related non-food products;

b. segmentation by mode of supply (delivered wholesale, contract distribution, cash and carry, retail/other);

c. segmentation by temperature range (frozen, chilled/fresh and ambient);

d. segmentation by geographic scope of the customer (national or independent);

e. segmentation by end-customer type (quick service, full service, pubs/coffee shops, hotels/accommodation, business & industry, other commercial, health, education, other institutional); and

f. segmentation by product category (fruit & vegetables, poultry, savoury bakery, sweet bakery, dairy, fish, grocery, confectionary, desserts, meat, all other).

3.2.3. The Commission's assessment

(12) The Parties are primarily active in the distribution of food products and this is the area in which the Commission focussed its investigation.9 The Commission in particular examined whether a distinction should be made according to (i) mode of supply; (ii) national and independent customers; and (iii) product category.

(13) As regards a distinction by temperature range or by end-customer type, the replies to the market investigation showed that all suppliers are able to offer multi- temperature deliveries to a full range of end-customers.10 As such, there appears to be full supply-side substitutability and the Commission does not consider these distinctions as relevant in this particular case.

3.2.3.1. Mode of supply

(14) Replies to the market investigation indicated that the majority of customers obtained all of their supplies through delivered wholesale, whereas a minority of customers multi-sourced their supplies through both delivered wholesale distribution and a number of additional modes of supply (cash and carry, contract distribution and direct supply by manufacturers).11 The majority of competitors considered that delivered wholesale distribution exerted the strongest competitive constraint on their business with the remaining modes of supply exerting a lesser constraint.12

(15) In any event, although the replies to the market investigation indicated that wholesale distribution could constitute a separate product market from other modes of supply, the Commission considers that, for the purpose of this decision, the question of whether foodservice distribution should be segmented according to mode of supply, can be left open since the transaction does not give rise to serious doubts about its compatibility with the internal market under any plausible market definition.

3.2.3.2. National and independent customers

(16) The results of the market investigation to some extent support the view of separate markets for national customers (with a number of outlets) and independent customers (with a smaller number of outlets). In particular, respondents indicated that national customers often require bespoke product lines. National customers also tend to purchase under long-term contracts, whereas independent customers rather make ad-hoc purchases.

(17) Finally, respondents to the market investigation indicated that national customers often centralise their procurement functions, placing orders with one supplier, for all outlets. Only the largest distributors, capable of delivery throughout the Island of Ireland, would be able to fulfil such orders. However, replies to the market investigation also indicated that although national customers may source food products from suppliers capable of servicing all outlets, these customers often also purchased additional product lines from specialist suppliers.

(18) In any event, although the replies to the market investigation indicated that the market could be segmented between national and independent customers, the Commission considers that, for the purpose of this decision, this question can be left open since the transaction does not give rise to serious doubts about its compatibility with the internal market under any plausible market definition.

3.2.3.3. Broadline/product category

(19) The vast majority of customers responding to the market investigation indicated that the breadth of product choice was important to them and that there were considerable advantages in purchasing from one supplier. These included better value, more efficient invoicing/ordering processes, and consistency of supply. The majority of customers responding to the market investigation however also considered that specialist suppliers for certain product categories, such as meat or dairy suppliers, were an equally good alternative to broadline suppliers. A minority of responding customers also considered that specialists were good alternatives for certain product categories or for high-end products which broadline suppliers do not always offer.13

(20) The majority of competitors responding to the market investigation considered that it was very important for their company to offer a broad product range to customers. However, those specialist suppliers who responded to the market investigation and who only offer certain product categories were of the view that they were still able to compete against broadline suppliers in the product categories that they offered.14

(21) In any event, although the replies to the market investigation indicated that the market could potentially be segmented between broadline and specialist suppliers, the Commission considers that, for the purpose of this decision, this question can be left open since the transaction does not give rise to serious doubts about its compatibility with the internal market under any plausible market definition.

3.3. Geographic market definition

3.3.1. The Notifying Party's arguments

(22) The Notifying Party submits that the market for foodservice distribution is at least national, with the exception of Northern Ireland, which exhibits more competitive interaction with the Republic of Ireland than the rest of the United Kingdom and that the relevant geographic scope should therefore be the Island of Ireland. In addition, the Notifying Party argues that the Island of Ireland is a small geographic area that can be readily covered by service vehicles and that it is possible to service the entire island from one depot.15

3.3.2. Past decisional practice

(23) The Commission has previously considered the geographic market to be national, although ultimately left this open.16 The CCPC, when reviewing Pallas’ acquisition of Crossgar in 2012, found that the geographic market definition could be considered to be the Island of Ireland (i.e. encompassing both the Republic of Ireland and Northern Ireland), on the basis that both parties delivered to both the Republic of Ireland and Northern Ireland.17

3.3.3. The Commission's assessment

(24) Replies to the market investigation provided a mixed picture. While the majority of customers require their distributors to be able to have a territory-wide presence on the Island of Ireland, all but one of these customers also purchase from distributors that are only able to supply one of either the Republic of Ireland or Northern Ireland. As regards competitors, although each competitor is stronger in either the Republic of Ireland, or Northern Ireland, the majority are able to supply the entire Island of Ireland and to maintain the same quality of distribution services throughout the whole territory. However, the location of multiple depots, or cross- docks are considered necessary when supplying the Island of Ireland. Finally, while there are no border restrictions between the Republic of Ireland/Northern Ireland, currency fluctuations were cited as having an impact on cross-border business.

(25) In the light of the above and taking into account the outcome of the market investigation, the Commission considers that, for the purpose of this decision, the exact scope of the geographic market can be left open since the transaction does not give rise to serious doubts about its compatibility with the internal market under any plausible geographic market definition.

3.4. Conclusion on market definition

(26) The Commission considers that the question of whether the distribution of food products to foodservice customers should be segmented by (i) mode of supply; (ii) national and independent customers; (iii) product category, as well as the geographic scope of any such possible relevant market, can be left open, as the transaction does not raise serious doubts as to its compatibility with the internal market.

4. COMPETITIVE ASSESSMENT

4.1. Overview

(27) The transaction gives rise to horizontal overlaps between Sysco's and Brakes’ activities in food distribution to the foodservice sector in the Island of Ireland.

(28) As regards the segmentation by mode of supply, the Parties are mainly active in delivered wholesale,18 although they have some more limited activities in contract distribution.19

(29) More particularly, in respect of delivered wholesale, affected markets arise in respect of broadline supply to national customers, broadline supply to independent customers as well as in relation to the supply of specific product categories. In respect of various product categories, the highest combined market share arises in the distribution of dairy products in the Republic of Ireland (combined share of [30-40]% with an increment of [0-5]%). The combined share in all other product categories remains below 30%. As the highest combined market shares arise in respect of broadline delivered wholesale to national and independent customers, the Commission focused its investigation on these potential markets.

4.2. Delivered wholesale distribution: broadline supply to national customers

4.2.1. The Notifying Party’s arguments

(30) The Notifying Party submits that no competition concerns arise as a result of the Transaction for the following reasons:

(31) First, some of the Parties' customers place ad hoc orders without any obligation to buy products on an ongoing basis. For these sales, the Parties and their larger distributor competitors are competing against a wide array of medium and smaller sized foodservice distributors. Larger customers award contracts through competitive tendering and tend to move towards a predominantly contract distribution model. Therefore, logistics companies such as DHL, Wincanton, Gist and Kühne+Nagel also pose a competitive threat to the Parties.

(32) Second, a sufficient number of strong competitors remain on the market(s). the Parties face strong competition from a range of delivered wholesale distributors. These include not just the other full-range (broadline) distributors whose product offering most closely matches those of the Parties, but also a large number of specialist distributors against whom the Parties must compete in order to grow their business with any given customer.

(33) Third, the Parties are not close competitors when considering the Parties’ offerings across a broad range of parameters such as Stock Keeping Units (SKU) offered, availability of own-label products, next day delivery, multi-temperature storage and distribution, and distribution capability across the Island of Ireland. Instead, many competitors have similar offerings across all of these competitive parameters.

(34) Fourth, customers are able to regularly switch between different sources of supply and distribution due to low switching costs. According to the Notifying Party, tenders and multi-year contracts are generally common among large customers, and to a lesser extent among smaller customers. Therefore, switching occurs because multi-year contracts typically allow for early termination and price reviews.

(35) Fifth, barriers to entry and expansion are low in the foodservice industry. The market essentially consists of trucks delivering food from a warehouse. The costs of multi-temperature trucks are insignificant such that all suppliers are capable of renting or buying these trucks. According to the estimations provided by the Parties, a large scale entry (sales of approximately […]) would entail a cost of […] per year for renting depots, […] per year to rent trucks, plus the fit out cost which would be […].

4.2.2. The market investigation and the Commission’s assessment

4.2.2.1. Competitive landscape and market shares

(36) According to the information provided by the Parties, the market size for broadline delivered wholesale to national customers in the Island of Ireland amounted to […] in 2015. Sysco achieved sales of […] and approximately [90-100]% of its sales was generated from its activities in the Republic of Ireland. In 2015, Brakes achieved sales of […], with its turnover evenly divided between the Republic of Ireland and Northern Ireland. The value of sales and market shares of the Parties and their competitors in 2015 are shown in Table 1 below.

Table 1: Market shares in broadline delivered wholesale distribution to national customers

| Island of Ireland | Republic of Ireland | Northern Ireland | |||

Sales (EUR million) | Share (%) | Sales (EUR million) | Share (%) | Sales (EUR million) | Share (%) | |

Sysco (Pallas) | […] | [20-30]% | […] | [20-30]% | […] | [5-10]% |

Brakes Ireland | […] | [10-20]% | […] | [5-10]% | […] | [20-30]% |

Combined | […] | [30-40]% | […] | [30-40]% | […] | [30-40]% |

Musgrave | […] | [20-30]% | […] | [20-30]% | […] | [10-20]% |

BWG | […] | [10-20]% | […] | [10-20]% | […] | [0-5]% |

Henderson | […] | [5-10]% | […] | [0-5]% | […] | [20-30]% |

Lynas | […] | [5-10]% | […] | [0-5]% | […] | [10-20]% |

La Rousse / Aryzta | […] | [0-5]% | […] | [0-5]% | […] | [5-10]% |

Other | […] | [10-20]% | […] | [10-20]% | […] | [5-10]% |

Total | […] | 100.0% | […] | 100.0% | […] | 100.0% |

Source: Form CO

(37) In the Island of Ireland, the transaction reduces the number of larger players from four to three. Based on the Parties’ estimates, the merged entity would have a market share of [30-40]%. Post-merger, the merged entity would continue to face competition from a number of players including Musgrave ([20-30]%) and BWG ([10-20]%). The rest of the market is relatively fragmented with several other smaller players present, such as Henderson ([5-10]%), Lynas ([5-10]%), and La Rousse/Aryzta ([0-5]%).

(38) In the Republic of Ireland, the merged entity’s combined market share would be [30-40]% with an increment of [5-10]%. The merged entity would continue to face strong competition from Musgrave and BWG (with Musgrave being nearly the same size as the merged entity). In Northern Ireland, the merged entity would have a combined market share of [30-40]% with an increment of [5-10]%. The merged entity would continue to face strong competition from two Northern Ireland-based distributors (Lynas and Henderson) as well as from Musgrave.

(39) During the investigation, the Commission undertook a market reconstruction exercise of delivered wholesale for broadline supply to national customers and independent customers in the Island of Ireland overall, as well as separately in the Republic of Ireland and Northern Ireland. The market reconstruction confirmed that, on the one hand, the Parties have overestimated some of their competitors' market shares and underestimated others, giving the merged entity a market share of [40-50]% in the Island of Ireland. However, even if the Parties' market shares are higher than estimated, the Commission considers that, post-merger, the merged entity would continue to face sufficient competitive constraints in the Island of Ireland.

(40) Furthermore, as explained in section 3.2.3.3 above, the market investigation indicated that specialist suppliers exert competitive constraint on broadline distributors at least for certain categories of food products. For instance, bidding data from the Parties shows that specialist supplier Heaney Meats won contracts with customers for […]% of the tenders with one supplier where Sysco participated and for […]% of tenders split between multiple suppliers where both Parties participated.

(41) However, contrary to the Parties' arguments, the Commission does not consider that logistics operators provide a particularly strong competitive constraint on wholesale distributors. While respondents in the market investigation confirmed that logistics operators were expected to grow their food distribution business on the Island of Ireland, logistics companies were not expected to become a significant competitive force in the market, in particular due to the fact that logistics operators are not able to handle fresh produce to the same standard as other distributors, the Island of Ireland is too small for these operators to achieve the necessary scale, and it is not practical to order multiple product lines from logistics operators.

4.2.2.2. Closeness of competition

(42) In light of the results of the market investigation and the information available to it, the Commission concludes that Brakes is not a particularly close competitor to Sysco for the following reasons.

(43) First, the large majority of the national customers who responded to the market investigation identified Musgrave as Sysco’s closest competitor, followed by BWG. These competitors were identified as being close to Sysco in terms of product range, distribution network, delivery and price.20

(44) Although the majority of the competitors who responded to the market investigation identified both Musgrave and Brakes as equally close competitors to Sysco, Sysco and Musgrave are focused mainly on the Republic of Ireland, while Brakes is more focused on Northern Ireland.21 BWG, Lynas, Henderson and LaRousse were also mentioned as close competitors to both Parties.

(45) Second, according to the tender data submitted by the Parties for the years 2013-2016, Sysco and Brakes are not particularly close competitors in tenders, particularly in those tenders with a high aggregated value. Sysco also faces competitive pressure from other competitors such as BWG, Lynas, Henderson, Musgrave and Heaney Meats.

(46) Out of […] tenders where Brakes tendered against Sysco, Brakes achieved a win rate of […] and for an aggregated value of EUR […] million which is far below the aggregate value of tenders lost by Sysco to other competitors such as BWG (EUR [...] million) and Musgrave (EUR […] million). All other competitors bidding against Sysco achieved a win rate higher than that of Brakes, with the exception of Henderson ([…]%) and Musgrave ([…]%). Musgrave, however, won […] times more value than Brakes. In fact, Brakes won the lowest aggregate value of tenders against Sysco.

(47) Out of […] tenders where Sysco tendered against Brakes, Sysco achieved a win rate of […], but for an aggregate value of EUR […] million which is far below the aggregated value of tenders won by, for example, BWG (EUR […] million). BWG also has a higher win rate than Sysco ([…]%). Musgrave and Henderson are also above Sysco in terms of value, although their win rate is […]% and […]% respectively. Musgrave and Henderson also participated relatively often in tenders where both Parties participate.

(48) Third, Sysco has significantly higher numbers of sales staff than Brakes in the Island of Ireland: Sysco has […] while Brakes has […]. According to data provided by the Parties, the remaining competitors (Musgrave, BWG, Lynas and Henderson) have similar levels of sales staff to Brakes. However, the Commission's market investigation indicated that the Parties have underestimated the number of staff of some of their competitors. Furthermore, Sysco has a far greater product range than Brakes: in terms of stock keeping units (SKUs), […]. The only competitor comparable to Sysco in terms of SKUs is BWG, which was also confirmed by the market investigation.

4.2.2.3. National Customers are able to switch suppliers

(49) In light of the outcome of the market investigation and the information available to it, the Commission considers that it is relatively easy for national customers to change suppliers for the following reasons.

(50) First, the majority of national customers responding to the market investigation considered that is relatively easy to change suppliers once a tender has been launched. Contracts typically run for two to five years and, changing suppliers may take place at the end of the contract when new tenders are launched.

(51) Second, tenders are the predominant method of procurement by national customers. Switching food suppliers is relatively easy since in every new tender, most or all of the sales could be lost to another competitor.

(52) In view of the above, the Commission considers that, although contracts for national customers are for three years on average and switching therefore takes longer than for independent customers, once the next tender has been launched, an existing supplier could be replaced with a new one on the merits of the bids.

4.2.2.4. Barriers to entry and expansion

(53) In light of the outcome of the market investigation and the information available to it, the Commission considers that barriers to expansion for foodservice suppliers in the Island of Ireland are not high for the following reasons.

(54) First, the majority of competitors responding to the market investigation confirmed that they have plans to expand in the Island of Ireland in the next three years through increasing the number of depots, warehousing, fleet, route capacity and staff.22

(55) Second, with respect to the Parties' arguments on multi-temperature vehicles, the large majority of competitors responding to the market investigation confirmed that all their major competitors have similar capabilities in offering multi-temperature deliveries on the Island of Ireland.23 The Commission therefore considers that the large majority of existing suppliers wishing to expand would be capable of offering multi-temperature deliveries.

(56) Third, previous expansions by existing competitors indicate that barriers to expansion are low. For instance, Lynas successfully entered the Republic of Ireland in 2008 and now has [500-2000] customers in delivered wholesale and [2-20]% of the contracts with customers in the Republic of Ireland.24

4.2.2.5. Exclusive supply arrangements

(57) One competitor and one customer in the market investigation raised concerns regarding possible exclusive supply arrangements that the merged entity could conclude post-transaction. In particular, these respondents raised concerns that some food suppliers might be forced to enter into exclusive agreements with the merged entity, such as the one between Sysco and […].25 The same competitor indicated that, given the increased financial power, the combined entity would be in a better position to negotiate better deals with food manufacturers and therefore force existing competitors out of the market.26

(58) In light of the outcome of the market investigation and the information available to it, the Commission considers that it is unlikely that post-transaction, the merged entity could foreclose its competitors through forcing some of the food suppliers to enter into exclusive arrangements with the merged entity for the following reasons.

(59) First, Sysco is already […] larger than Brakes in terms of spend on purchasing food in the Island of Ireland and […] has […] exclusive supply agreements. [Confidential information regarding the value of the agreements]. Adding Brakes to the overall spend on purchasing food post-transaction will not significantly increase Sysco's purchasing power to the extent that the merger would change Sysco’s ability or incentive to foreclose other competitors.

(60) The Parties' largest competitors also purchase considerable volumes of food in Ireland, in particular since two of them, BWG and Musgrave, purchase food not only for their delivered wholesale but also for their distribution through other channels, such as cash and carry. These competitors can act as a significant competitive restraint on the merged entity post-merger.

(61) Third, Sysco indicated that the choice of having exclusive supply agreements is based on efficiencies, in the sense that Sysco can ensure consistency, quality and provenance with a brand that is recognised by the customers. Furthermore, suppliers can benefit from the security of supply and simpler distribution.

(62) Fourth, Sysco currently has […] exclusive supply agreements in place. [Confidential information regarding description of exclusive agreements]. This only points to a balance of power between the foodservice distributors and their suppliers of raw materials, rather than suppliers being forced to accept exclusive supply agreements with the foodservice distributors.

(63) Fifth, with respect to the alleged exclusive agreement with […], Sysco confirmed that although it has publicly indicated on occasion that […] is available exclusively to Sysco customers, in reality […] products are supplied on the Island of Ireland through other distributors as well, such as Cunningham Foods and previously also by Lynas.27 Sysco does not, in fact, have an exclusive supply agreement with […].

4.2.2.6. Impact of the transaction

(64) One national customer indicated that the transaction would reduce competition between suppliers that have a full range of products and can supply the entire island or that could do central distribution.28 The majority of national customers responding to the market investigation, however, indicated that the proposed transaction would not have an impact on their company or on the supply of foodservice products to foodservice customers on the Island of Ireland.

4.2.3. Conclusion

(65) In the light of the considerations in recitals (36) to (64) and the outcome of the market investigation, the Commission concludes that the proposed transaction does not raise serious doubts as to its compatibility with the internal market with regard to the broadline delivered wholesale distribution of foodservice products to national customers in the Island of Ireland.

4.3. Delivered wholesale distribution: broadline supply to independent customers

4.3.1. The Notifying Party's arguments

(66) For the reasons set out in recitals (30) to (35), the Notifying Party submits that no competition concerns arise as a result of the transaction with respect to broadline supply to independent customers.

4.3.2. The market investigation and the Commission's assessment.

(67) In light of the outcome of the market investigation and the information available to it, the Commission considers that the transaction does not raise serious doubts as to its compatibility with the internal market in the Island of Ireland in relation to broadline supply to independent customers for the following reasons.

Table 2: Market shares in broadline delivered wholesale distribution to independent customers

| Island of Ireland | Republic of Ireland | Northern Ireland | |||

Sales (EUR million) | Share (%) | Sales (EUR million) | Share (%) | Sales (EUR million) | Share (%) | |

Sysco (Pallas) | […] | [20-30]% | […] | [20-30]% | […] | [5-10]% |

Brakes Ireland | […] | [0-5]% | […] | [0-5]% | […] | [0-5]% |

Combined | […] | [20-30]% | […] | [30-40]% | […] | [10-20]% |

Lynas | […] | [10-20]% | […] | [0-5]% | […] | [30-40]% |

Musgrave | […] | [10-20]% | […] | [10-20]% | […] | [5-10]% |

Henderson | […] | [10-20]% | […] | [0-5]% | […] | [20-30]% |

BWG | […] | [5-10]% | […] | [10-20]% | […] | [0-5]% |

La Rousse / Aryzta | […] | [5-10]% | […] | [5-10]% | […] | [5-10]% |

Other | […] | [20-30]% | […] | [30-40]% | […] | [5-10]% |

Total | […] | 100.0% | […] | 100.0% | […] | 100.0% |

Source: Form CO

(68) First, the combined market share of the Parties remains below 30% ([20-30]%) and the increment brought about by the transaction is relatively small ([0-5]%). The market in the Island of Ireland is fragmented with a range of important players: Lynas ([10-20]%), Musgrave ([10-20]%), Henderson ([10-20]%), BWG ([5-10]%), LaRousse ([5-10]%) and other smaller players. In the Republic of Ireland, the combined market shares are slightly higher ([30-40]% with an increment of [0-5]%). Musgrave is the closest competitor ([10-20]%), followed by BWG ([10-20]%), LaRousse ([5-10]%), Corrib ([5-10]%) and Stonehouse ([5-10]%). There are no affected markets in Northern Ireland.

(69) The results of the Commission's market reconstruction yielded similar results to the data provided by the Parties in the Island of Ireland. In the Republic of Ireland, the combined market shares are similar to those estimated by the Parties, but two competitors have market shares above 30%. In addition, the majority of independent customers in the market investigation were of the view that the market for the supply of food products in the Island of Ireland is competitive with many options on all suppliers categories.29 The Commission therefore considers that the merged entity would face sufficient competitive constraint on the Island of Ireland in respect of broadline supply to independent customers.

(70) Second, the majority of independent customers responding to the market investigation confirmed that is relatively easy to change suppliers and the large majority of them indicated that they have switched suppliers in the past.30 Independent customers award contracts generally on a yearly basis which can be reviewed occasionally.31 The Commission therefore considers that it is relatively easy for independent customers to switch suppliers since these yearly contracts allow for early termination and price reviews.

(71) Third, as explained in section 4.2.2.4 above, barriers to expansion are low.

(72) Finally, the majority of independent customers responding to the market investigation indicated that the proposed transaction would not have an impact on their company or on the supply of foodservice products to independent customers on the Island of Ireland. A minority of independent customers raised concerns that the transaction would create a large company with large market shares that would push out of the market the other competitors.32 However, the Commission considers that the combined market shares of the merged entity is not significant and the increment brought about by the transaction is relatively small. A sufficient number of players will remain on the market, posing a competitive threat to the new entity. In addition, as explained in section 4.2.2.5 above, it is unlikely that post-transaction, the merged entity could foreclose its competitors through forcing some of the food suppliers to enter into exclusive arrangements with the Parties.

4.3.3. Conclusion

(73) In the light of the considerations in recitals (67) to (72) and the outcome of the market investigation, the Commission concludes that the transaction does not raise serious doubts as to its compatibility with the internal market with respect to the broadline supply of food products to independent customers in the Island of Ireland.

5. CONCLUSION

(74) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 167, 11.5.2016, p. 18.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 M.2891 CD&R Fund VI Limited/ Brake Bros plc, decision of 25 July 2002 and M.4293 Nordic Capital Fund VI/ ICA MENY, decision of 8 September 2006. The Commission’s most recent cases were reviewed under the simplified procedure: M.4820 Bain Capital/ Brake Bros, decision of 7 September 2007, M.5835 Cucina/ Brakes/ Menigo Group, decision of 13 April 2010, M.7651 Bain Capital / Davigel Group, decision of 21September 2015.

6 French Case Décision 5-DCC-141 Bain Capital/ Davigel, decision of 27 October 2015.

7 UK Case ME/6490/14 Cucina Acquisition (UK) Limited/certain assets of Fresh Holdings Limited, decision of 16 February 2015; UK Case ME/1222/04 Musgrave Investments plc/Londis (holdings) Limited, decision of 30 September 2004.

8 Irish Case M/12/010 Pallas Foods Ltd./Crossgar Foodservice Ltd, decision of 23 August 2012.

9 Only [5-10]% of Sysco's turnover and [5-10]% of Pallas' turnover on the Island of Ireland relates to non-food distribution, so this will not be considered further in this Decision.

10 Questionnaire to Competitors (Q2), question 22.

11 Questionnaire to Customers (Q1), question 11.

12 Questionnaire to Customers (Q1), question 9.

13 Questionnaire to Customers (Q1), question 19.

14 Questionnaire to Competitors (Q2), question 15.

15 The Parties argued that both Parties had serviced the entire Island of Ireland from one depot: Pallas operated form Limerick in the south west of the Republic of Ireland and Brakes from Lisburn in Northern Ireland. Both Parties have since opened second depots (in 2013 and 2015 respectively).

16 Case COMP/M.2891 CD&R Fund VI Limited/ Brake Bros plc, decision of 25 July 2002.

17 Irish Case M/12/010 Pallas Foods Ltd./Crossgar Foodservice Ltd, decision of 23 August 2012.

18 [90-100]% of Sysco's and [70-80]% of Brakes' turnover on the Island of Ireland was achieved through delivered wholesale in 2015.

19 [0-5]% of Sysco's and [20-30]% of Brakes' turnover on the Island of Ireland was achieved through contract distribution in 2015. No affected markets arise in respect of contract distribution.

20 Questionnaire to Customers (Q1), question 39.

21 Questionnaire to Competitors (Q2), question 40.

22 Questionnaire to Competitors (Q2), question 53.

23 Questionnaire to Competitors (Q2), question 22.

24 Questionnaire to Competitors (Q2), question 47. Ranges are provided to protect their confidential information.

25 Questionnaire to Competitors (Q2), question 57.

26 Questionnaire to Competitors (Q2), question 57.

27 Parties' reply to Commission's Request for Information of 20 May 2016.

28 Questionnaire to Competitors (Q2), question 53.

29 Questionnaire to Customers (Q1), question 36.

30 Questionnaire to Customers (Q1), question 37.

31 Questionnaire to Customers (Q1), question 44.

32 Questionnaire to Competitors (Q2), question 53.