Commission, March 24, 2017, No M.8359

EUROPEAN COMMISSION

Judgment

AMUNDI / CREDIT AGRICOLE / PIONEER INVESTMENTS

Subject: M.8359 - Amundi / Credit Agricole / Pioneer Investments Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir/Madam,

(1) On 20 February 2017 the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Amundi S.A. (Amundi), subsidiary of Crédit Agricole S.A. (France) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of Pioneer Global Asset Management S.p.A. ("Pioneer"), the asset management business of UniCredit S.p.A (Italy) by way of purchase of shares ("the Transaction").3 Amundi and Pioneer are collectively referred to as "the Parties".

I. THE PARTIES AND THE OPERATION

(2) Crédit Agricole is a publicly-traded French banking group active globally in retail banking, insurance, real estate and financial services.

(3) Amundi is a subsidiary of Crédit Agricole specialising in asset management for both institutional and retail clients, covering all asset classes. It is active worldwide.

(4) Pioneer is a subsidiary of Italian banking group UniCredit specialised in asset management, active worldwide.

(5) On 11 December 2016, the Parties concluded a stock purchase agreement pursuant to which Amundi acquires sole control over Pioneer's subsidiaries in a number of countries, i.e. Austria, the Czech Republic, Germany, Ireland, Italy, Luxembourg and the United States. The Pioneer subsidiaries in Australia, Hungary, India, Romania, Switzerland and Taiwan will also be part of the Transaction provided that the Parties receive the relevant regulatory approval in time for closing. Pioneer's subsidiaries in Bermudas, Ireland, Israel and the US Alternative Pioneer Investments (New York) Ltd are not included in the perimeter of the Transaction.

(6) On 8 december 2016 UniCredit signed a separate share purchase agreement with Powszechny Zakład Ubezpieczeń SA ("PZU Group") and the Polish Development Fund S.A. ("PFR") for the sale of Pioneer's Polish subsidiaries; this transaction is being reviewed by the Polish authorities. Should PZU Group and PFR fail to receive the necessary regulatory approvals in Poland, the Polish subsidiaries of Pioneer would also be included in the Transaction. The assessment of the impact of the Transaction below presumes the largest possible scope of the Transaction, so that the conditionality on the exact perimeter of the Transaction would not impact the merger review.

(7) In the light of the above, the Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

The distribution agreements

(8) In Italy, Austria and Germany Amundi has entered into distribution agreements with UniCredit for the distribution of Pioneer’s retail funds in these three Member States. In addition, Amundi and UniCredit have agreed to maintain the existing distribution agreements entered into between UniCredit Bank Czech Republic and Slovakia, a.s. and Pioneer, dated 22 August 2016, for the distribution of Pioneer funds in the Czech Republic and Slovakia (all together, the “Distribution Agreements”).

(9) Based on the Distribution Agreements post-Transaction UniCredit will continue to distribute Pioneer funds through its banking networks. Pursuant to the Distribution Agreements, Pioneer funds shall represent at least (i) […]% of the asset management funds distributed by UniCredit in Italy, (ii) […]% of the asset management funds distributed by UniCredit in Austria, (iii) […]% of the asset management funds distributed by UniCredit in Germany and (iv) […]% of the retail funds distributed by UniCredit in the Czech Republic and Slovakia, provided that Pioneer meets qualitative and performance criteria. The Distribution Agreements have been concluded for ten years.

(10) The Notifying Party does not seek the benefit of the Commission Notice on restrictions directly related and necessary to concentrations (the "Notice").4 In this context, the Commission notes that in any event the Distribution Agreements clearly fall outside the scope of the principles set out in the Notice and they cannot be considered part of the main object of the concentration, which is the acquisition of sole control by Amundi over Pioneer. As provided for in paragraph 7 of the Notice, the Distribution Agreements cannot be considered directly related and necessary to the implementation of the concentration and are therefore not covered by this Decision. Consequently, such Agreements remain subject to the assessment under Articles 101 and 102 TFEU without prejudice to their compatibility or otherwise with the said Articles.

(11) Notwithstanding that the scope of the present Decision does not cover the Distribution Agreements these arrangements nonetheless are taken into consideration when assessing the competitive effects of the Transaction, in particular in the context of vertical links between asset management and the distribution of asset management products.

II. EU DIMENSION

(12) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million5 (Crédit Agricole: EUR 90 495 million, Pioneer: EUR 2 313 million). Each of them has an EU-wide turnover in excess of EUR 250 million (Crédit Agricole: EUR […], Pioneer: […]). Not all undertakings concerned achieve more than two-thirds of its aggregate EU-wide turnover within one and the same Member State.

(13) The notified operation therefore has an EU dimension under Article 1(2) of the Merger Regulation.

III. COMPETITIVE ASSESSMENT

(14) The Transaction brings together the activities of Amundi and Pioneer, which are to a certain extent complementary in terms of geographic presence and product offering. Consequently, the Transaction results in horizontal overlaps between Amundi and Pioneer on the market for asset management and its segments in a number of countries, but leading to affected markets for asset management only in France and in the Czech Republic and for the distribution of asset management products in France. The Transaction also leads to an affected market for distribution of asset management products in France since Crédit Agricole is a provider of retail banking services and distributor of asset management products to retail clients.

(15) In addition, the Transaction leads to vertical links leading to affected markets in France (i) between asset management for retail clients (upstream) and the distribution of asset management products for retail clients (downstream), (ii) between asset management (downstream) and custody services (upstream) and (iii) between asset management (downstream) and fund administration services (upstream).

A. Market definition

Asset management

(16) Asset management concerns the creation, establishment and marketing of funds mainly to retail clients on an “off-the-shelf” basis and the provision of portfolio management services for institutional investors. A variety of assets are used as the basis of an investment, such as equity, fixed income, real estate, or money market instruments.

(17) In previous cases the Commission has considered a relevant product market for overall asset management. Further segmentation was also considered. In particular, the Commission examined the possible distinction between a relevant product market for the creation and managing of mutual funds for retail clients on the one hand, and the tailor-made funds for corporate and institutional customers, on the other hand.6 Institutional clients are entities such as pension funds, banks or insurance companies that purchase asset management product and services directly from asset management companies rather than via a non-specialised intermediary such as a retail bank7. Conversely, retail clients are provided with asset management products and services through general corporate banking networks acting as distributors.8

(18) Within the asset management for institutional clients the Commission considered existence of separate market for active asset management and passive market management.9 Active asset management consists of strategies applied by the investment manager with the goal of outperforming a benchmark, for instance an index, while passive strategies merely seek to replicate the performance of an index.

(19) As regards retail customers, the Commission considered a segmentation between open and closed retail funds.10 Closed funds are funds which are tailor-made for a small group of investors and not distributed through retail channels. Such funds are not open to the subscription of new capital by persons unknown to the nominative shareholders. On the other hand, open funds do not have any restrictions on the number of investors.

(20) In previous cases the Commission considered also the existence of a separate segment for mutual funds and, within the mutual funds, a separate market for money market funds. Money market funds were considered to constitute relatively short-term investment vehicles used by investors for optimizing working capital.11

(21) To conclude, in its previous decisions the Commission has left open the question whether the asset management market should be treated as one relevant market or should be segmented according to the above distinctions.

(22) The Notifying Party submits that there should be no segmentation of the overall market for asset management.

(23) The market investigation in the present case has largely confirmed the possibility of segmenting the market for asset management according to the above delineations.

(24) Some market participants suggested additional delineations. For example, one competitor suggested a distinction per type of asset under management: equities, bonds, alternative assets.12 Another competitor active in France explained that one could consider distinguishing so called Alternative investment funds (AIF) regulated by the AIF Directive13, and the so called Undertakings for Collective Investments in Transferable Securities (UCITS)14, which are regulated by the UCITS Directive.15 These were however isolated voices.16

(25) In general, the responses by the market participants confirm that it is possible to consider various segments within the asset management market, but it is also justified to look at the asset management as a whole. For example, one of the competitors explained that : "We consider that it make sense for institutional business to split between passive and active management. However (…) more and more UCITS funds are addressed to both institutional and retail clients. In addition most of the money market funds are mainly sold to institutional clients for treasury needs but retail clients are also able to invest.17

(26) Furthermore, as regards the supply side, although according to the Notifying Party's asset management providers tend to provide a full range of asset management products and services, the market investigation results provide for a more nuanced view. While large asset managers tend to cover all main asset classes, there is a number of so called "boutique" suppliers, who tend to specialise in certain categories of products. 18

(27) In any event, for the purpose of the present case it can be left open whether the market for asset management constitutes one product market or whether each segment within the asset management category should be considered a distinct product market, since the transaction does not raise competition concerns under any plausible product market definition.

(28) As regards the geographic market definition, the Commission has previously considered the market for asset management products to be national or wider than national in scope.19 As regards the asset management for institutional clients, the Commission considered that the market may be wider than national in scope.20 In contrast, in relation to the asset management for retail clients, the Commission held that the geographic scope of the markets for open retail mutual funds as well as for money market funds should be considered national, due to the importance of distribution.21

(29) The market investigation results have to a large extent confirmed the past findings of the Commission. As explained by one of the competitors active in France "For main of the European countries, competition takes place more and more at a national level. However, part of this competition comes from cross-border players, sometimes coming from the US."22 Furthermore, in line with the past assessment of the Commission, another competitor active in France explained that the approach depends on whether the institutional or retail clients are concerned, which determines two different levels of competition.23 In general, the majority of competitors consider the asset management market for institutional clients to be EEA-wide or even global in scope, although some respondents consider that even for the institutional clients the asset management market is national.24 Consequently, definite conclusions cannot be drawn but the overall review of the responses has provided support for the view that for retail clients the market is national due to the need for national distribution channel, while for the institutional clients the market may be wider.

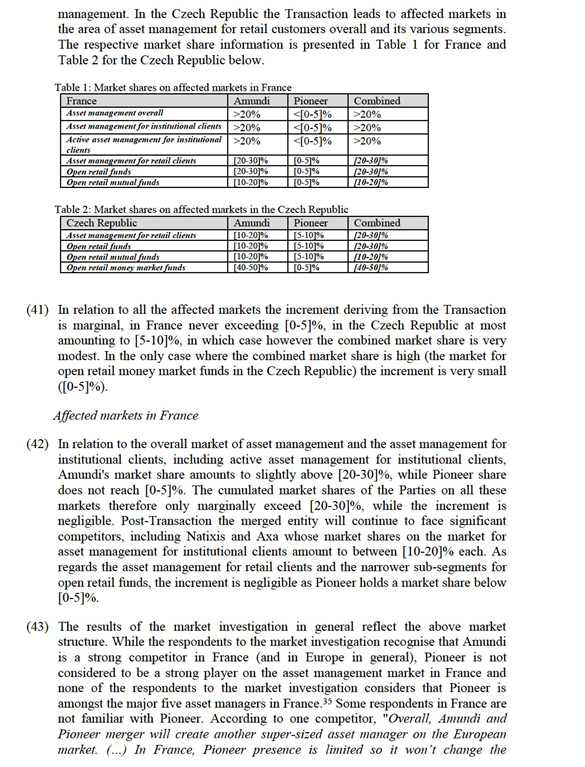

(30) Furthermore, while the results of the marker investigation show that the general regulatory framework for asset management has been harmonised across the EU through the UCITS and AIF Directives, competitors indicated that in conformity with the EU legislation some rules remain national in particular the marketing rules for selling UCITS funds in host Member States. The rules and requirements relating to advertising and marketing documentation are not harmonised across the EU.25

(31) In any event, for the purpose of the present case it can be left open whether the market for asset management is national or supra-national in scope, since the Transaction does not raise competition concerns under any plausible geographic market definition.

Distribution of asset management products

(32) The Notifying Party submits that retail funds are distributed either indirectly via the retail networks of banks, insurance companies, and brokerage houses, or directly via online channels. Like most of their main competitors in Europe, Amundi and Pioneer are vertically integrated and currently distribute a significant part of their funds via the retail networks of their respective banking groups: Amundi via Crédit Agricole and Pioneer via UniCredit. Therefore the Parties' activities overlap in the area of distribution of asset management products specifically via the retail networks of banks.

(33) In previous decisions26 the Commission considered a relevant market comprising all retail banking products as well as the possibility of segmenting retail banking market according to offered products (personal current accounts, savings accounts, consumer loans, mortgages and distribution of mutual funds).. In any event, the product market definition regarding the market for the distribution of the asset management products, and specifically regarding the retail banking can be left open since the Transaction does not raise any competitive concerns under any plausible market definition.

(34) In relation to the relevant geographic market, in previous decisions the Commission considered the market for retail banking to be national in scope, including for the distribution of mutual funds.27

Custody services

(35) Custody services comprise the settlement, safekeeping and reporting of customers’ (asset manager) marketable securities. More specifically, custody services include the following types of activity: safekeeping of the assets; presentation of securities for, and reception of securities from, clearing and settlement platforms; income and dividend processing; etc. The Commission has in the past considered whether a distinction should be made between global services (provided to investment institutions wherever they are localised) and domestic services (provided at a domestic level)28. Furthermore, within the market for domestic custody services the Commission considered distinguishing separate markets for (domestic) institutional custody services, sub-custody services and retail custody services.29

(36) The Notifying Party submits that segmenting the market for custody services is not necessary.

(37) As for the geographic definition, in its previous decisions, the Commission left open the exact definition of the geographic market.30 Nevertheless, the Commission noted that the market for global custody services could be considered worldwide or at least EEA-wide31, while domestic markets have been assessed at the national level.32

(38) In any event, for the purpose of this case the precise product and geographic market definition for custody services can be left open as the Transaction does not to raise competitive concerns irrespective of the precise product or geographic market definition.

Fund administration

(39) Fund administration services include various services such as acting as trustee, depositary or depot bank of mutual funds, accounting services etc. In previous cases the Commission considered this activity to constitute one distinct product market.33 As regards the geographic scope, in its previous decisions, the Commission left open whether the geographic market should be considered national or wider in scope.34 The Notifying Party submits that the market is worldwide in scope. In any event, the precise product and geographic scope of the market for fund administration can be left open for the purpose of this case, as the Transaction does not raise competition concerns under any plausible product or geographic definition of the market for fund administration services.

B. Competitive assessment

1. Horizontal overlaps

(40) The Transaction leads to affected markets only in the area of asset management. Should the market for asset management was considered EEA-wide in geographic scope, the Transaction would not lead to any affected markets. Assuming that the competition takes place at the national level, the Transaction leads to a number of horizontally affected markets in France and in the Czech Republic. In France the Transaction leads to affected markets for overall asset management, asset management products for retail clients and its sub-segments and asset management products for institutional clients and in particular the market for active asset

competitive landscape. (…). As both actors are mainly operating on the European market, this would create a major player competing with BlackRock and JP Morgan on size."36

(44) The respondents to the Commission’s market investigation do not consider Amundi and Pioneer to be close competitors and they seem to specialise in different areas of asset management. Most respondents recognise that Amundi is a global player with a comprehensive offer and strong results, conversely, as regards Pioneer some respondents were not even in position to assess the performance and the positioning of Pioneer on the French market.37 As explained by one of competitors [Pionner has] "to the best of our knowledge, not a strong footprint in France".38 Consequently a number of competitors was considered closer to Amundi than Pioneer in France, namely Natixis, BNP Paribas and Axa.39

(45) All the respondents to the market investigation consider the market for asset management in France to be competitive.40 As explained by one of the institutional customers in reply to the market investigation: "There is a large number of global asset managers offering services in France (over 150 of them are of a reasonable size). As an example, [a customer] works with more than 57 of them. During each request for proposal we conduct, [the customer] always have a sizeable number of candidates willing to offer their services (usually between 10 and 30 according to the asset class and the size of the mandate) and [the customer] also considers the prices offered to be fairly attractive." Or as explained by another respondent "With around 600 French Asset Managers, we can consider that French market is competitive".41 Consequently it is not expected that the Transaction could have any significant impact on the market for asset management or any of its segments in France.42

Affected markets in the Czech Republic

(46) As regards the Czech Republic, Amundi has a market share of approximately [10- 20]% in the market of asset management for retail clients and the sub-segment for open retail funds, while the market share of Pioneer amounts to [5-10]%. The cumulated market shares of the Parties therefore just reach [20-30]%, and the Parties will continue to face significant competitors, including the two market leaders Ceska sporitelna (CS) and the CSOB Group. As regards the narrower subsegment for money market, the increment is negligible as Pioneer holds a [0-5]% market share, with AuM of less than €[0.5 million], with the resulting delta HHI will below 10. In any event, money market funds are almost non-existent in Czech Republic and Amundi itself has very limited assets under management in this regard (less than €[50-100] million, compared to over [>1 billion] in the market for open retail mutual funds), so that its market share of [40-50]% cannot be considered as raising competition concerns.

(47) According to the replies to the market investigation Amundi and Pioneer are not considered close competitors in the Czech Republic. None of them is actually considered to be among the top five asset managers in the Czech Republic.43 Among the most important market players, pointed out by the competitors44 and distributors45 in the Czech Republic are Generali, CS/Erste, CSOB/KBC and KB/Societe.

(48) In general, all market respondents say that the asset management market in all segments in the Czech Republic is competitive and they do not expect that the Transaction could have major impact on the market for asset management in the Czech Republic. 46

(49) In view of the above assessment, the Commission considers that the Transaction does not raise any competition concerns in the market for asset management or any of its segments.

2.Vertical links

(50) The Transaction will lead to vertical links

a. between asset management activity (by Amundi and Pioneer, upstream) and asset management distribution by Crédit Agricole (downstream),

b. between asset management activity by Amundi and Pioneer (downstream) and custody and fund administration services provided by a subsidiary of Crédit Agricole, CACEIS, (upstream activity).

(51) The market shares of the Parties will remain below 30% both upstream and downstream in all Member States and in potential market segments, except in France.

a. Relationship between asset management activity (by Amundi and Pioneer, upstream) and mutual funds distribution by Crédit Agricole (downstream)

(52) On the downstream market for mutual funds distribution Crédit Agricole has a market share of approximately [10-20]%, while the combined market share on the upstream market, as indicated in Table 1 above, at maximum amounts to [20-30]% with virtually no change brought by the Transaction. The market investigation confirmed that the Transaction will not lead to any input or customer foreclosure, as there are numerous alternative suppliers both on the upstream and the downstream market. Most importantly the Transaction does not bring any significant change to the current situation since increments deriving from the Transaction are negligible.

b. Relationship between asset management activity by Amundi and Pioneer (downstream) and custody and fund administration services provided by a subsidiary of Crédit Agricole, CACEIS, (upstream activity)

(53) CACEIS holds respectively a [30-40]% market share in custody services and [40- 50]% market share in fund administration services. As regards input foreclosure, the parties submit that CACEIS is already vertically integrated and has never refused to provide custody services to customers other than Amundi. As explained in recitals (42) to (45) the Transaction brings hardly any difference in France on the asset management market, so it seems unlikely that CACEIS behaviour would change because of the Transaction. Also, significant market shares are held several strong competitors on the market for custody services and for fund administration in France and consequently, asset managers competing with Amundi/Pioneer will remain able to reply on a significant number of options for custody services and fund administration. In this regard, the incentives to adopt input foreclosure strategies seem low since there is possibility of migration of customers to other providers.

(54) The market investigation responses did not reveal any concerns that the Transaction could change the current behaviour of the merged entity and Crédit Agricole in particular. CACEIS is identified by the competitors as one of the main providers of custody and fund administration services in France together with BAN Paribas, Société Générale and Crédit Mutuel.47 Nevertheless, none of the respondents to the market investigation considers that the Transaction could incentivise the merged entity to pursue the foreclosure strategy and limit the access of asset managers in France to custody and fund administration services.48

(55) In addition, as regards customer foreclosure, given the minimal market share brought by Pioneer in France, even if Pioneer were to stop using providers of custody service or fund administration other than CACEIS, this could be hardly noticed by these suppliers.

(56) Therefore, the Commission considers that the Transaction does not lead to any competition concerns in the markets for the distribution of asset management products, custody services or fund administration services.

IV. CONCLUSION

(57) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 62, 25.2.2017, p. 10.

4 OJ C 56, 5.3.2005 p. 24.

5 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C95, 16.4.2008, p. 1).

6 M.6812, SFPI / Dexia, Commission decision of February 2, 2013, para. 31; M.3894, UniCredito / HVB, paras. 35-36; M.4844, Fortis / ABN Amro Assets, paras. 67-70; M.5580, Blackrock / Barclays GIH, paras. 8-13.

7 M. 5728, Credit Agricole/ Societe Generale Asset Management, para 33.

8 M.5728 Credit Agricole/ Societe Generale Asset Management, para 35.

9 M.5580, BlackRock/Barclays GIH, para. 10; M.5728, Crédit Agricole /Société Générale Asset Management, para. 35-39.

10 M.5728, Crédit Agricole / Société Générale Asset Management, paras. 68-69.

11 M. 3894 Unicredito/HVB paras. 35-36; M. 1453 –AXA/GRE; M. 4844 Fortis/ABN AMRO Assets, para. 67, paras. 7 and 8.

12 Replies to question 4 of Questionnaire Q4 – Customers, France.

13 Directive 2011/61/EU of the European Parliament and of the Council of 8 June 2011 on Alternative Investment Fund Managers and amending Directives 2003/41/EC and 2009/65/EC and Regulations (EC) No 1060/2009 and (EU) No 1095/2010, OJ L 174, 1.7.2011, p. 1–73.

14 Replies to question 6 of Questionnaire Q1 – Competitors, France.

15 Directive 2009/65/EC of the European Parliament and of the Council of 13 July 2009 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities (UCITS), OJ L 302, 17.11.2009, p. 32–96.

16 See replies to question 4, Questionnaire Q4 – Customers, France.

17 See replies to question 6 of Questionnaire Q1 – Competitors, France.

18 Replies to question 7 of Questionnaire Q1 – Competitors, France.

19 M.6812, SFPI / Dexia, Commission decision of February 2, 2013, para. 32.

20 M.5728, Crédit Agricole / Société Générale Asset Management, para 41.

21 M.5728, Crédit Agricole / Société Générale Asset Management, para. 84.

22 Replies to question 8 of Questionnaire Q1 – Competitors, France.

23 Replies to question 8 of Questionnaire Q1 – Competitors, France and to question 7, questionnaire Q4 – Customers, France and to question 8 of Questionnaire Q2 – Competitors, the Czech Republic.

24 Replies to question 8 of Questionnaire Q1 – Competitors, France and replies to question 8 of Questionnaire Q2 Competitors, the Czech Republic.

25 Replies to question 9 of Questionnaire Q1 – Competitors, France.

26 M.4844, Fortis / ABN Amro Assets, para. 41; M.5384, BNP Paribas / Fortis, paras. 9-10.

27 M.4844, Fortis / ABN Amro Assets, para. 85, 139-142, 155-158; M.3894, UniCredito / HVB, para. 41 and 54-57; M.6168 – RBI/EFG EUROBANK/JV, paras. 27-28.

28 M.1618, Bank of New York / Royal Bank of Scotland Trust Bank, para. 10.

29 M.5728, Crédit Agricole / Société Générale Asset Management, para. 114; M.4844, Fortis / ABN AMRO Assets, para. 69.

30 M.5728, Crédit Agricole / Société Générale Asset Management, para. 122

31 M.3781, Crédit Agricole / Caisse d' Epargne / JV, para. 17.

32 M.3781, Crédit Agricole / Caisse d' Epargne / JV, para. 20

33 M.3781, Crédit Agricole / Caisse d' Epargne / JV, para. 21.

34 M.5728, Crédit Agricole / Société Générale Asset Management, para. 124.

35 Replies to question 10, Questionnaire Q1 - Competitors, France and question 12, Questionnaire Q4 - Customers, France

36 Replies to question 19, Questionnaire Q1 – Competitors, France.

37 Replies to questions 12, 13 Questionnaire Q1 – Competitors, France.

38 Replies to question 15, Questionnaire Q1 – Competitors, France.

39 Replies to question 14, Questionnaire Q1- Competitors, France and to question 6, Questionnaire Q4

– Customers, France. At the European level it is considered that close competitors of Amundi are for example BlackRock, Allianz, Vanguard, JP Morgan etc.

40 Replies to question 16, Questionnaire Q1 – Competitors, France and to question 15, Questionnaire Q4 – Customers, France.

41 Replies to question 15, Questionnaire Q4 – Customers, France.

42 Replies to question 19, Questionnaire Q1 – Competitors, France and question 16 Questionnaire Q4, Customers, France.

43 Replies to questions 11, 12, 13 Questionnaire Q2 – Competitors, the Czech Republic.

44 Replies to question 10, Questionnaire Q2 – Competitors, the Czech Republic.

45 Replies to question 10, Questionnaire Q5 – Distributors, the Czech Republic.

46 Replies to question 16, Questionnaire Q6 – Customers, the Czech Republic.

47 Replies to question 17, Questionnaire Q1, France.

48 Replies to question 18, Questionnaire Q1 – Competitors, France.