Commission, July 29, 2020, No M.9796

EUROPEAN COMMISSION

Judgment

UNIQA / AXA (INSURANCE, ASSET MANAGEMENT AND PENSIONS - CZECHIA, POLAND AND SLOVAKIA)

Subject: Case M.9796 –UNIQA / AXA (INSURANCE, ASSET MANAGEMENT AND PENSIONS - CZECHIA, POLAND AND SLOVAKIA)

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 23 June 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Uniqa Österreich Versicherungen AG, Austria (“Uniqa” or the “Notifying Party”) would acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of insurance (life and non-life), asset management and pension business operations of AXA S.A. ("AXA") in the Czech Republic, Poland and Slovakia (the “Target”) (“the Transaction”)3. Uniqa and the Target are together referred to as the “Parties”.

1. THE PARTIES

(2) Uniqa is an Austrian insurance company, part of a group which provides insurance products and services primarily in Austria, Central and Eastern Europe. Uniqa is jointly controlled by (i) Uniqa Versicherungsverein Privatstiftung (“Uniqa PS”), a private foundation, whose exclusive beneficiaries are policyholders of Uniqa, and (ii) Raiffeisen Bank International (“RBI”), an Austrian banking group.

(3) The Target comprises the insurance (life and non-life), asset management and pension businesses in the Czech Republic, Slovakia and Poland of AXA, where the primary focus of its activities is on insurance.

2. THE OPERATION

(4) The Transaction is structured as a share purchase. Pursuant to the share purchase agreement, entered into on 7 February 2020, all shares in the Target and each right attached to these shares shall be acquired by Uniqa.

(5) As such, following completion of the Transaction, the entire share capital in the Target will be held by Uniqa and Uniqa will acquire sole control of the Target. The Transaction is therefore a concentration within the meaning of Article 3(1)(b) of the EU Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (Uniqa EUR 5 300 million; Target: […]).4 Each of them has an EU-wide turnover in excess of EUR 250 million (Uniqa: […]; Target: […]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. COMPETITIVE ASSESSMENT

4.1. Market Definition

4.1.1. Insurance products

(7) In previous decisions relating to the insurance sector, the Commission distinguished three categories of insurance products (life insurance, non-life insurance, and reinsurance), as well as a downstream market for insurance distribution.5 In the present case, only life and non-life insurance products are relevant for the competitive assessment of the Transaction.

4.1.1.1. Previous decisional practice

(8) As regards the product market definition for life insurance products, the Commission distinguished between: (i) pure risk protection products; (ii) pension products; and (iii) savings/investment products (sometimes grouping the two latter).6 In certain decisions, the Commission also distinguished between life insurance for individuals and group/corporate customers, or between products based on the type of risk covered. The Commission ultimately left open the precise product market definition for life insurance products for all plausible segmentations mentioned above.7

(9) As regards product market definition for non-life insurance products, the Commission’s consistent approach is to consider that relevant product markets can be divided into the types of risks to insure. Precedents typically distinguish the following non-life insurance segments: (i) accident and sickness, (ii) motor vehicle, (iii) property, (iv) liability, (v) marine, aviation and transport (“MAT”), (vi) credit and suretyship and (vii) travel insurance.8 In certain decisions, the Commission also distinguished fire insurance, and legal assistance. The Commission also considered several additional segmentations of the non-life insurance market, including based on national insurance classification9 or between individual and group (i.e. corporate/institutional) customers. The Commission ultimately left open the precise product market definition for non-life insurance products for all plausible segmentations mentioned above.

(10) As regards geographic market definition, in previous decisions, the Commission typically considered that the markets for life and non-life insurance products and their respective sub-segments are likely to be national in scope, and potentially wider than national for certain risk classes of non-life insurance.10

4.1.1.2. Notifying Party’s view

(11) Regarding non-life insurance, the Notifying Party indicates that there is supply side substitutability between the different segments of non-life insurance and, thus, different types of non-life insurance could form part of the same product market. The Notifying Party further indicates that, in the relevant Member States (including Poland and Slovakia where plausible affected markets arise), the classification of insurance into group or individual insurance often stems from reporting technicalities under the national regulatory framework, rather than reflecting different competitive dynamics that would justify identifying separate markets.11

(12) Regarding life insurance, the Notifying Party indicates in particular that the classification under the regulatory framework of Slovakia (where a plausible affected market arises) does not strictly distinguish between pure risk protection, pension insurance and saving/investment insurance products.12

(13) The Notifying Party provided information at national level, but indicates that the geographic scope of insurance markets can be left open as the Transaction does not raise potential competitive concerns under any plausible market definition.13

4.1.1.3. Commission’s assessment

(14) With respect to Poland, a potential product market segmentation of the non-life insurance market by risk classes provided by the Polish Insurance Act would lead to a number of plausible affected markets, including separated markets of non-life insurance for (i) sickness and (ii) accident as well as CASCO insurance of rail vehicles.14

(15) With respect to Slovakia, a potential segmentation of the life insurance market by risk classes could be made based on Directive 2009/138/EC of the European Parliament and of the Council of 25 November 2009 on the taking-up and pursuit of the business of Insurance and Reinsurance (“Solvency II”), which would lead to a plausible affected market for index-linked and unit-linked life insurance.15

(16) For the purpose of the present decision, the exact product and geographic market definition for the provision of life and non-life insurance can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition identified in paragraphs (8) to (10).

4.1.2. Voluntary retirement saving products

(17) Pension systems in the EU typically distinguish between three different pillars of support for retirees. Similarly, the Slovak pension system distinguishes between three different pillars, the first pillar ("p1") which is the publicly managed pension system with mandatory participation, the second pillar ("p2") which is the privately managed mandatory savings system operated by pension fund management companies (Dôchodková správcovská spoločnosť, "DSS"), and the third pillar (“p3”) which is a voluntary retirement saving product.16

(18) Pension fund products offered under p3 in Slovakia are offered by companies known as Doplnková dôchodková spoločnosť (“DDS”), funded by individuals to enhance retirement income. These DDS pension fund products have in particular the following features: they are typically purely market-based, are voluntary and private, with defined contributions, additional contributions from an employer and tax benefits, but provide no certainty of benefits.17

4.1.2.1. Previous decisional practice

(19) In its previous decisional practice, the Commission has not discussed the product market definition for voluntary retirement saving products in Slovakia, and in particular not whether DDS pension fund products belong to a wider market encompassing other voluntary retirement saving products. However, concerning Poland, the Commission found in case COMP/M.4950 Aviva/Bank Zachodni that p1 and p2 products fall within a different product market than p3 products, since, among other differences, the first two pillars (in the Polish pension system) were based upon mandatory contributions from wages whereas the p3 system was voluntary.18 Furthermore, regarding saving for retirement in case M.8257 NN Group/Delta Lloyd concerning insurance based saving / investment products and banking saving products, the market investigation indicated that there can be a certain degree of substitutability between insurance based saving / investment products and banking saving products which are designed to serve the same purpose as the saving / investment insurance products (life), depending on the national legislative framework.19 However, the Commission also pointed to differences in the products.20

(20) Regarding the geographic scope, the Commission considered previously that the market for pension products for Poland is national in scope, citing a specific national regulation, but left the final market definition open.21

4.1.2.2. Notifying Party’s view

(21) The Notifying Party is of the opinion that the relevant product market is a wider voluntary retirement saving market that includes not only DDS pension fund products but also other voluntary retirement saving products aimed at allowing individuals to accumulate savings to supplement their income in retirement, such as mutual funds, pension insurance (life), etc.22 This is because the main factor that matters to the individual when making a choice on how to save for retirement is that the selected product pays out the needed additional funds in the future. Thus, relevant parameters for an individual wishing to save for retirement are contributions in the pre-retirement phase, pay-outs during retirement and flexibility with respect to contributions and pay-outs.

(22) Therefore, according to the Notifying Party p3 products form a separate market from p2 and p1 products with their respective roles in the Slovak pension system. p3 encompasses all voluntary retirement saving products, regardless whether they are state designed or not. This includes notably, pension insurance (life), (retail) mutual funds and DDS pension fund products.

(23) Regarding the geographic scope, the Notifying Party does not contradict the Commission, that considered in its previous decisional practice that the market for pension products for Poland is national in scope.

4.1.2.3. The Commission’s assessment

(24) According to the Commission’s market investigation, DDS pension fund products should be considered a separate and standalone market, distinctly from other voluntary retirement savings products.

(25) According to the Notifying Party`s competitors in the retirement saving market, consumers do not view DDS pension fund products as interchangeable with other voluntary retirement saving products such as mutual funds and pension (life) insurance products, mainly because the key criterion for consumers when choosing a financial product for retirement is the employer’s contribution, which is specific to DDS pension fund products and a specific regulatory framework applicable to DDS pension fund products.23 In direct comparison of DDS pension fund products with mutual funds and pension (life) insurance products it was also pointed out that DDS pension fund products profit from favourable tax treatment.24 Competitors also were of the opinion, that there are no specific categories of consumers that would particularly consider DDS pension fund products as suitable alternative to other voluntary retirement saving products such as mutual funds and pension (life) insurance products. The market investigation furthermore revealed, that competitors believe that Slovak consumers would not move their savings from DDS pension fund products to mutual funds (or pension life insurance products) if fees for these two products were to decrease permanently by e.g. 5-10%.25 One competitor explicitly stated that “only DDS out of these three product is real pension saving product, remaining two are more investment and risk insurance products”.26 Another competitor stated that Slovak consumers do not use mutual funds for long- term pension savings purposes in large extent. A third competitor stated that no switch of products would take place “because the original purpose of the investment was different”. If consumers decided to save money for retirement purposes, they will not change products, even if more attractive from the fees perspective. The result is similar when asking for fund flows in the other direction. Competitors are also of the opinion, that Slovak consumers would not move their savings from mutual funds or pension life insurance products to DDS pension fund products if management fees for DDS pension fund products were to decrease from 1.2% to 1%.27

(26) According to brokers of voluntary retirement financial products in Slovakia, consumers would not clearly rule out interchangeability between DDS pension fund products and other voluntary retirement saving products such as mutual funds and pension (life) insurance products. However, brokers also state that there will be no flow of savings from DDS pension fund products on the one hand to mutual funds or pension life insurance products on the other hand if fees for the latter two product groups were to decrease permanently by e.g. 5-10%.28 Neither do brokers expect a flow of savings into the other direction to DDS pension fund products, if fees for DDS pension fund products were to decrease from 1.2% to 1%.29

(27) Also in the opinion of the National Bank of Slovakia, “insurance products or other mutual funds offered by asset managers are not substantive competitor for DDS products”. The reason is that, in majority, these products “are not primarily created with the intention to save for retirement and the payment to clients is not conditioned by this purpose.” Moreover, “insurance products and funds offered by asset managers don´t provide any tax benefits neither for the employer nor for employees and the client generally takes the investment risk (if there in one).”30

(28) Additionally, the market investigation confirmed the differing characteristics of the three pillars of the Slovak pension system. According to the National Bank of Slovakia, the first pillar is a mandatory pension insurance defined by benefits and funded on an ongoing basis and administered by the Social Insurance Agency. The second pillar is also mandatory and defined by contributions and capital funded insurance administered by pension fund management companies. The third pillar is a privately managed voluntary personal pension plan administered by specialized DDS.31 Moreover, it was confirmed that DDS pension fund products are governed by separate legislation.32 Therefore, as in case COMP/M.4950 Aviva/Bank Zachodni the Commission considers that a distinction can be made between the mandatory p1 and p2 products and the voluntary DDS pension fund products.

(29) The market investigation revealed no indication that the market is wider than national in scope and it was repeatedly pointed out, that DDS pension fund products are subject to national legislation.33

(30) For the purpose of this decision, the exact product and geographic market definition for the provision of DDS pension fund products and the question of whether they are part of a wider market for voluntary retirement saving products such as mutual funds and pension (life) insurance products can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition identified in paragraphs (24) to (29).

4.1.3. Distribution of voluntary retirement saving products

(31) Voluntary retirement saving products are distributed either indirectly via retail banks, insurance companies and brokerage houses, or directly by the providers of these products.34

4.1.3.1. Previous decisional practice

(32) In past decisions, the Commission has considered the existence of a distinct product market for the distribution of pension products in the Netherlands, without concluding on the exact product or geographic market definition.35 In other cases, the Commission has suggested the existence of a market for the distribution of pension or related products, without discussing the precise definition of such a market but ultimately left open the precise product market definition.36

4.1.3.2. The Notifying Party’s view

(33) The Notifying Party does not dispute the potential existence of a separate market for the distribution of voluntary retirement saving products, but did not provide further arguments regarding its product or geographic definition.37

4.1.3.3. The Commission’s assessment

(34) The Commission notes that a variety of products would generally be suitable to accumulate savings for the retirement age. This would include, for example, mutual funds, for which a separate distribution market exists in the context of asset management. The existence of a further distinct product market for the distribution of specific voluntary saving products may therefore depend on the availability of such products in the Member State in question. In the present case, a potential distinct product market for DDS pension fund products may exist in Slovakia38, as discussed in paragraphs (17) to (30). Consequently, a distinct product market for the distribution of such products may also exist. The Commission notes that, for the purpose of this decision, the exact definition of such a market can be left open, as no competition concerns are raised under any plausible market definition. The Commission further notes that a potential separate product market for the distribution for voluntary retirement saving products, and specifically DDS pension fund products, would likely be national in scope, due to the high relevance of national regulation.

4.1.4. Asset management

(35) Asset management concerns the creation, establishment and marketing of funds mainly to retail clients on an “off-the-shelf” basis and the provision of portfolio management services for institutional investors.39

4.1.4.1. Previous decisional practice

(36) In previous cases, the Commission has considered a relevant product market for asset management overall. Furthermore, the Commission has considered, but ultimately left open, a further segmentation between retail and institutional clients (such as pension funds, banks or insurance companies).40

(37) Within the potential segment of institutional clients, the Commission has considered in previous cases a further segmentation between active and passive asset management. In active asset management, an asset manager aims at outperforming a benchmark such as an index, whereas in passive asset management, the asset manager aims at replicating the performance of an index.41 Regarding retail clients, the Commission has previously considered a segmentation between open retail funds, with no restriction on the number of investors, and closed retail funds, which are tailor-made for a small group of investors.42 For all these plausible segmentations, the Commission ultimately left open the precise product market definition.

(38) Apart from that, the Commission has in previous cases considered, but left open, a separate segment for mutual funds, and within mutual funds a further sub-segment of money market funds. Money market funds are short-term investments used by investors to optimise working capital.43

(39) As regards the geographic market definition, the Commission has previously considered the market for asset management to be national or wider than national in scope. With respect to asset management for institutional clients, the Commission has previously considered a geographic market wider than national, whereas the market for open retail mutual funds and money market funds was considered to be national in scope.44

4.1.4.2. The Notifying Party’s view

(40) The Notifying Party does not submit that the Commission should depart from its decisional practice for the assessment of the present case.

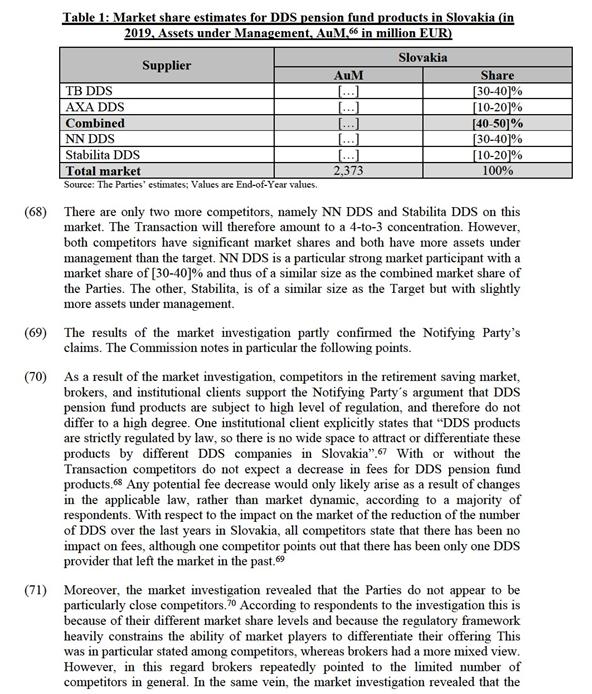

4.1.4.3. The Commission’s assessment

(41) For the purpose of this decision, the exact product and geographic market definition for the provision of asset management services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

4.1.5. Distribution of asset management products

(42) This market relates to the distribution of retail funds, either indirectly via the retail networks of banks, insurance companies and brokerage houses, or directly via online channels.45 The Transaction affects the market of distribution of asset management services due to the banking operations of Tatra Banka downstream to the asset management activities of the Parties, which include asset management for retail customers.

4.1.5.1. Previous decisional practice

(43) In the past, the Commission considered a relevant market comprising all retail banking products as well as the possibility of segmenting the retail banking market according to offered products (personal current accounts, savings accounts, consumer loans, mortgages and distribution of mutual funds). However, the exact product market definition was left open.46

(44) In previous decisions, the Commission concluded the market for retail banking, including the distribution of mutual funds, to be national in scope.47

4.1.5.2. The Notifying Party’s view

(45) The Notifying Party does not argue that the Commission should deviate from its previous decisional practice.48

4.1.5.3. Commission’s assessment

(46) The exact product market definition can be left open for the present case, as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible definition. Regarding the geographic scope, there is no element to deviate from the Commission’s previous decisional practice.

4.1.6. Custody and depositary services

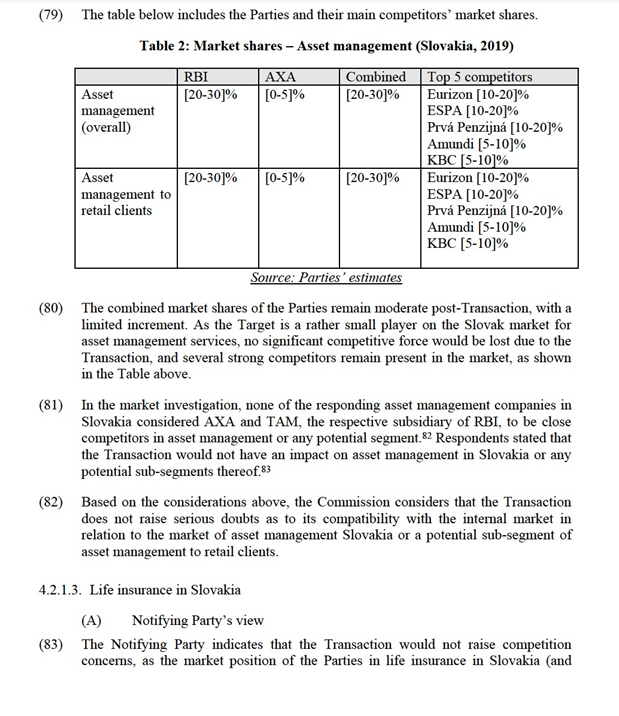

(47) The provision of custody and depositary services is significantly influenced by national regulation. Custody services alone typically comprise the safekeeping of the securities of the customer’s clients. A custodian therefore is the trustee of the securities of the client. Depositary services go beyond that, comprising also the monitoring and auditing of the fund and its transactions. In Slovakia, such services are provided to DDS companies, DSS companies, and asset management companies.49

4.1.6.1. Previous decisional practice

(48) In past decisions, the Commission has considered custody services as a potential narrower market within asset management services, but left this product market definition open.50 Furthermore, the Commission has considered depositary services as part of fund administration services, which was defined as one product market with no further segmentation.51 In later decisions, the exact product market definition of fund administration was left open.52 Depositary services for mutual and pension funds were also considered to be potentially a distinct product market in the area of custody services or asset management, and ultimately left the market definition open.53 The Commission thereby noted that depositary services would largely include custody services, but would further comprise certain control functions prescribed by national law.

(49) As for the geographic market with respect to custody services, the Commission considered that some services might be global in scope (provided to investment institutions regardless of their location), while others would be provided on domestic level.54 Regarding a potential market for depositary services, the Commission did not conclude on a geographic scope, but referred to the national regulatory framework of such services.55

4.1.6.2. The Notifying Party’s view

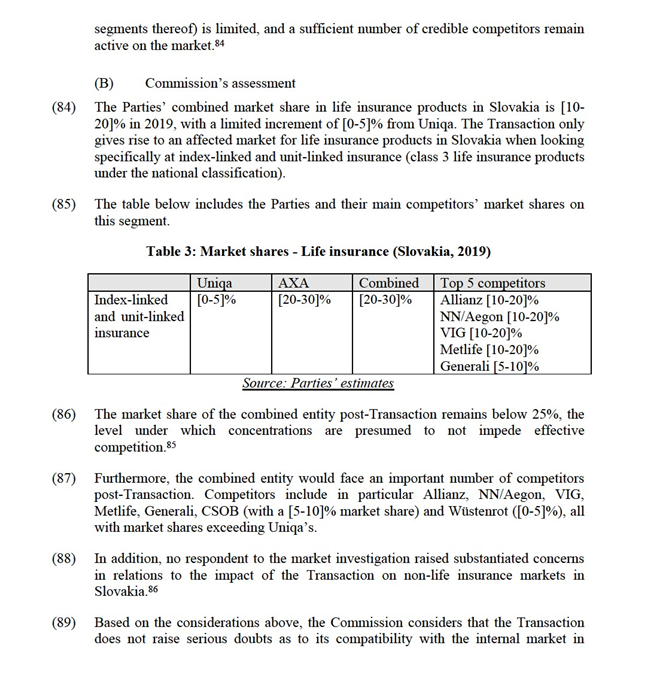

(50) The Notifying Party expresses doubts as to whether depositary services would indeed form a separated market from custody services, first because there are synergies between the provision of both services, and second because Slovak law would require the DSS and DDS pension fund companies to source both of these services from one supplier.56 Regarding the geographic scope of a custody and depositary service market, the Notifying Party points to the significant relevance of national regulations.

(51) The Notifying Party argues that identifying a separate product market for fund administration (including establishing and pursuing an investment strategy, keeping records and analysing performance), would not be appropriate as Tatra Banka would only provide these services [description of sales channels] and has no market offering. However, Tatra Banka does offer custody and depositary services to third parties in Slovakia.57

4.1.6.3. The Commission’s assessment

(52) The Commission notes that there is a high relevance of national regulation for the provision of custody and depositary services in Slovakia.58 Feedback from the market suggests some degree of substitutability between the provision of custody and depositary services from a supply side point of view in Slovakia.59 One respondent described depositary services to be typically an “add-on service” to custody service. This would be an argument that custody and depositary services in Slovakia belong to the same or a closely related product market. On the other hand, both types of services differ in the sense that depositary services in Slovakia comprise the supervision, examination, inspection and compliance checks with respect to the applicable national laws for each transaction.60 This would suggest to treat custody and depositary services in Slovakia as separate product markets. The Commission further notes that the strong impact of national regulation of the provision for depositary services in Slovakia suggests the geographic market is national in scope.

(53) For the present case, the exact product and geographic market definition of custody and depositary services can be left open, as no competition concerns would arise under any plausible market definition.

4.2. Competitive assessment

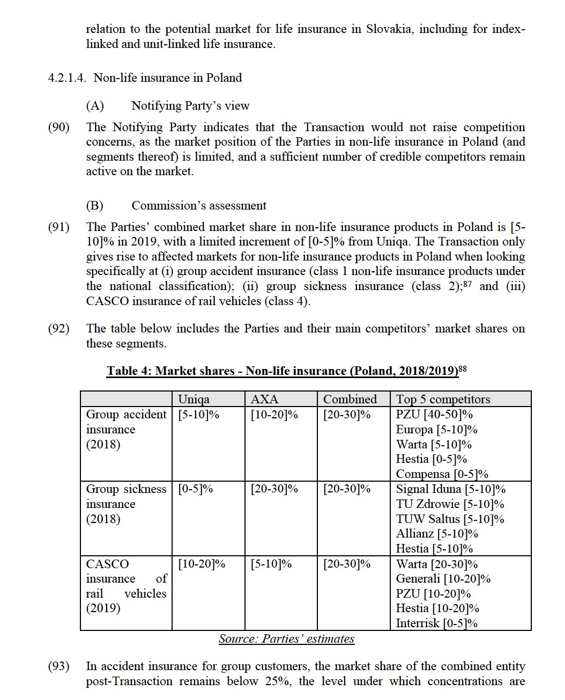

(54) The Transaction gives rise to horizontally-affected markets in:

(a) Asset management in Slovakia, including in retail asset management in Slovakia;

(b) Voluntary retirement saving products in Slovakia, including in DDS pension fund products in Slovakia;

(c) Life-insurance products in Slovakia, specifically in index-linked and unit- linked life;

(d) Non-life insurance products in Poland, specifically in (i) group accident insurance; (ii) group sickness insurance; and (iii) CASCO insurance of rail vehicles.

(55) The Transaction gives rise to vertically-affected markets in:

(a) DDS pension fund products (upstream) and the distribution of voluntary retirement saving products (downstream) in Slovakia;

(b) Custody and depositary services (upstream) and DDS pension fund products (downstream) in Slovakia;

(c) Asset management (upstream) and the distribution of asset management products (downstream) in Slovakia; and

(d) Asset management (upstream) and DDS pension fund products (downstream) in Slovakia.

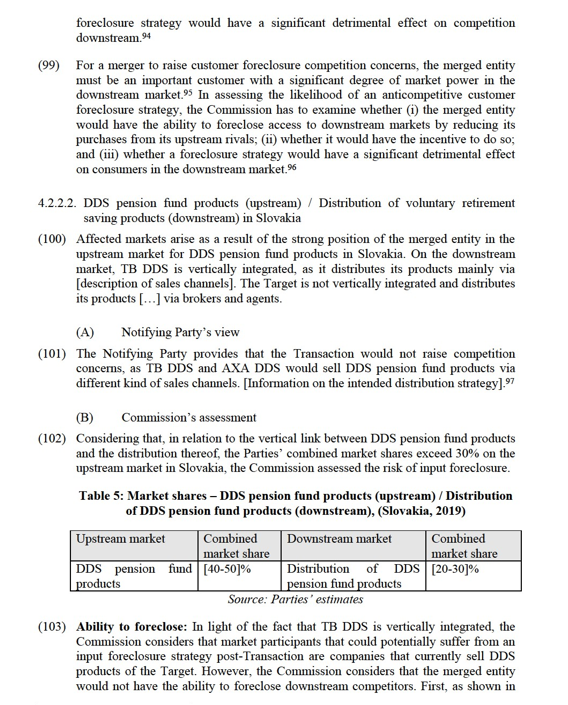

4.2.1. Horizontal effects

(56) Article 2 of the Merger Regulation requires the Commission to examine whether notified concentrations are compatible with the internal market, by assessing whether they would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(57) The Commission Guidelines on the assessment of horizontal mergers under the Merger Regulation (the "Horizontal Merger Guidelines") distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non- coordinated effects and coordinated effects.

(58) Non-coordinated effects may significantly impede effective competition by eliminating the competitive constraint imposed by each merging party on the other, as a result of which the merged entity would have increased market power without resorting to coordinated behaviour. The Horizontal Merger Guidelines list a number of factors61 which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. Not all of these factors need to be present for significant non-coordinated effects to be likely. The list of factors, any one of which is not necessarily decisive, is also not an exhaustive list.

4.2.1.1. Voluntary retirement saving products in Slovakia

(A) Notifying Party’s view

(59) The Notifying Party is of the opinion that the Transaction will not lead to a significant impediment to effective competition.62 It states that the relevant market is the market for voluntary retirement saving products, with a combined market share of the Parties of below 30 % and a multitude of alternative suppliers. Furthermore, the Parties claim that market share estimates do not consider cross-border sales, and therefore overstate the market shares. The market share level of the Parties and increment resulting from the Transaction would therefore be limited for such a market.

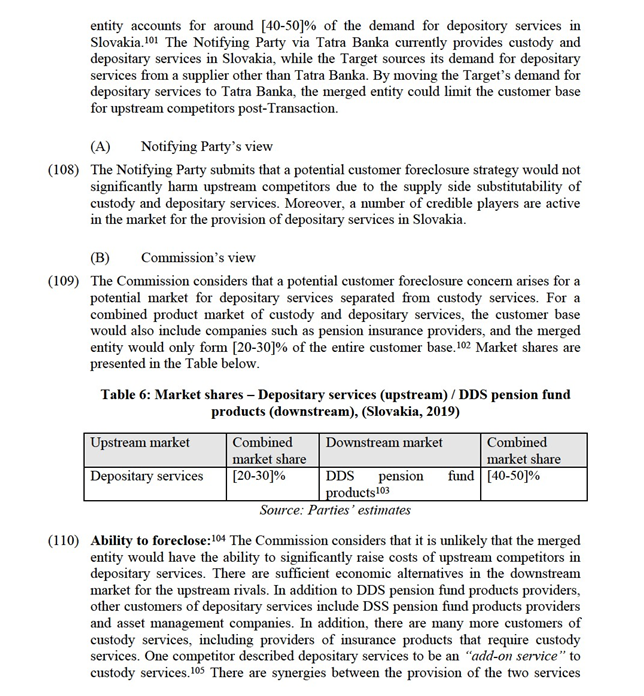

(60) But even on a narrower market for pension funds in the third pillar in Slovakia the Transaction will not lead to a significant impediment to effective competition according to the Notifying Party. DDS pension fund products are and will remain competitively restrained not only by the other voluntary retirement saving products, but by any product which allows an individual to save money and to earn a return for later use at retirement.

(61) Furthermore, the Notifying Party argues that, post-Transaction, the Parties will be unable to increase prices to the detriment of consumers for third pillar products. This is due to the regulatory environment in Slovakia. DDS are highly regulated, in particular regarding their fees, which leads to the absence of price competition. Fees are capped and have steadily been reduced in the past, to now 1.2% of assets under management (“AuM”) annually. All DDS providers factually charge management fees at this cap. Furthermore, regulation imposes significant restrictions on the distribution of contributions among asset classes to ensure diversification.

(62) The Notifying Party argues that it is also not plausible that competition will be reduced on any other parameter of competition. The Transaction will not reduce the incentive for the DDS providers to seek optimising the performance of their pension fund products. Moreover, concerning DDS pension fund products, the Parties are not competitors. Uniqa does not directly offer DDS pension fund products. It is only a subsidiary of Uniqa`s jointly controlling parent company, RBI, which provides DDS pension fund products in Slovakia via its subsidiary TB DDS. But the Uniqa`s jointly controlling parent company has only a 10.9% stake in Uniqa. Therefore, there is no incentive for harmful conduct post-Transaction.

(63) Furthermore, according to the Notifying Party, DDS providers use different distribution channels that prevent customers from switching between providers. For TB DDS, DDS pension fund products are primarily sold to [description of customers]. Stabilita DDS relies predominantly on its relationships with employers, whose employees are eligible for DDS pension fund products. The Target and NN, make use of [description of sales channels] to acquire customers.

(64) Additionally, the Notifying Party argues that pan-European Personal Pension Products (“PEPP”) will soon be introduced. The Parties expect this to allow cross- border business and the opening of the local pension markets for other players.63

(65) For these reasons, the Notifying Party argues that the high combined market shares [40-50]% do not adequately reflect competition in the market post-Transaction.

(B) Commission`s assessment

(66) The Transaction would give rise to an affected market for voluntary retirement saving products in Slovakia, encompassing pension insurance (life), (retail) mutual funds, and DDS pension fund products. The Parties have a combined market share of [20-30]% in 2019 based on AuM. The increment provided by the Target is [5- 10]%.64

(67) The Transaction would also give rise to an affected market for the narrower potential market of DDS pension fund products in Slovakia. As shown in the following table, in a potential market for DDS pension fund products in Slovakia, the Parties’ combined market share would be [40-50]% post-Transaction with an increment of [10-20]% from the Target (“AXA DDS”) and a [30-40]% market share by a subsidiary of one of Uniqa’s controlling parents, namely RBI which controls Tatra Banka, a banking group which operates its own DDS in Slovakia (“TB DDS”).65

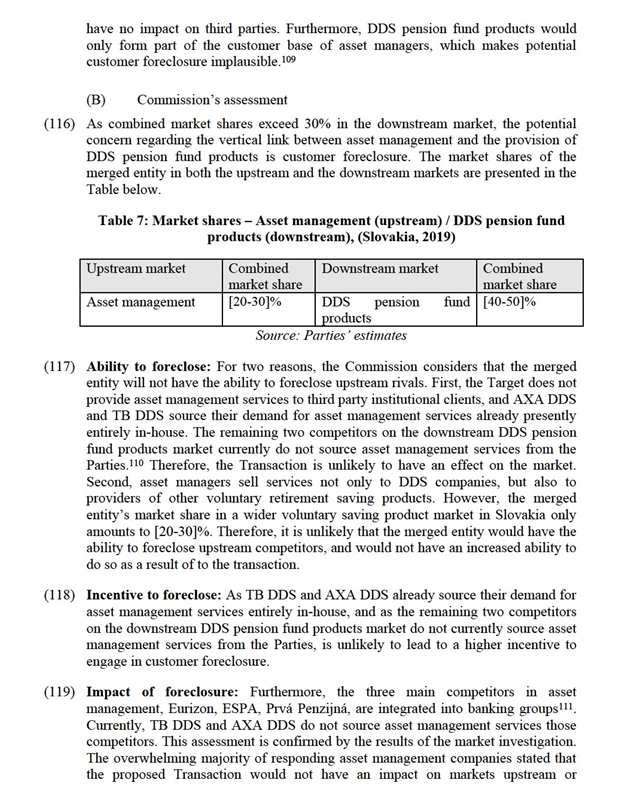

Parties are not considered particularly aggressive either in the provision of DDS pension fund products, nor in enrolling intermediaries to offer their products. This is supported by the investigation`s outcome, that one of the two most important key criteria for individuals to choose one specific DDS rather than another one is an existing customer relationship with the DDS (or the group of companies it belongs to).71 The other one is the provider`s representation (local offices etc.). This points to an importance of the distribution channel for DDS pension fund products. However, the results as to whether and how, the distribution channels (e.g. brokers, bank agencies etc.) influence the choice of consumers to select one specific DDS rather than another is inconclusive. Respondents to the market investigation pointed out that consumers might be influenced by their employers that make a "prechoice" of specific DDS for their employees. Furthermore, it was stated that easy access to a provider`s representation could play a role as well as the payed commission to a distributor or the distributor`s affiliation to the DDS provider.72

(72) The lack of closeness of competition among the Parties is supported by the market investigation also, insofar as the majority of competitors is of the opinion that customers of DDS pension fund products do not regularly switch between DDS.73 However, none of the competitors pointed to barriers of switching, such as fees. Brokers supported that view, also with a majority stating that customers of DDS pension fund products only rarely switch between DDS.74

(73) Asked about the Transaction`s impact on the market, an overwhelming majority of competitors, brokers, and institutional clients do not expect any impact from the Transaction on the DDS pension fund product market in Slovakia.75 Most of responding competitors in the overall voluntary retirement saving market expect the Transaction to have no impact on DDS pension fund products, including on fees and quality or choice. The two other providers of DDS pension fund products expect no impact on fees.76 Neither do competitors expect any impact on fees, quality or choice of voluntary retirement saving products (including DDS, mutual funds and pension life insurance products). All responding brokers supported this view and state that the Transaction will likely not have an impact on fees or quality or choice regarding both DDS pension fund products in particular or voluntary retirement saving products in general, although one broker acknowledged, that there will be one competitor less to choose from.77 Employers also do not expect the transaction to have any negative effect neither on the DDS market nor for employers that offer DDS pension fund products for their employees to save for retirement age.

(74) The two competing DDS pension fund providers expressed concerns during pre- notification contacts and in the market investigation.78 These concerns raised in relation to the Transaction include the ability of the Parties to improve the quality of products or better adapt to lower fee requirements and thus to gain market share post-Transaction.79 They also expressed concerns in relation to the Parties increased ability to distribute their DDS pension fund products post-Transaction. While the Commission notes that these effects may actually be pro-competitive, it also notes that these concerns were not confirmed in the market investigation, which revealed that the Transaction will likely have no impact, in particular on fees.

(75) Concerning the likely impact of the introduction of PEPP, the results of the market investigation were inconclusive80. However, in light of the overall results of the market investigation it can be left open, whether PEPP will have a significant impact on the market for voluntary retirement saving products or DDS in Slovakia, since even without new PEPP products there are no competition concerns. The same holds true for the Notifying Party`s argument that incentives for harmful conduct post- Transaction are not aligned between the Uniqa and the Target, because of the fact that the acquirer’s jointly controlling parent company holds only a 10.9 % stake in the acquirer. Even if this argument is disregarded, no competition concerns arise.

(76) Based on the considerations above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the market of DDS pension fund products or voluntary retirement saving products in Slovakia, due to horizontal non-coordinated effects.

4.2.1.2. Asset management in Slovakia

(A) Notifying Party’s view

(77) The Notifying Party submits that the Transaction would not raise competition concerns, as the Target is only a minor player in the Slovak market for asset management, and provides most of its services captively. Furthermore, a number of competitors in the market would continue to exercise competitive pressure on the merged entity. 81

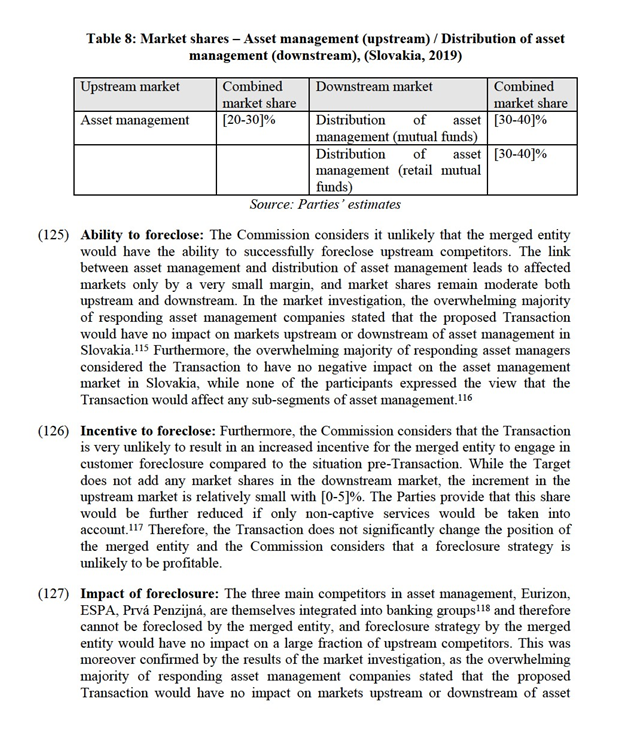

(B) Commission’s assessment

(78) The Transaction would give rise to an affected market for overall asset management in Slovakia, as well as for as a potential sub-segment of asset management for retail clients. Both Uniqa’s parent company RBI, through its subsidiaries, as well as the Target offer asset management services.

presumed to not impede effective competition.89 In sickness insurance for group customers, the market share of the combined entity post-Transaction remains moderate (below 30%) and the increment brought about by Uniqa is inconsequential (around [0-5]%).90 In CASCO insurance of rail vehicles the market share of the combined entity post-Transaction also remains moderate (below 30%).

(94) The combined entity would also face an important number of competitors post- Transaction on all markets, including at least three competitors with market shares around or exceeding the increment brought about by the Transaction. Therefore, post-Transaction a sufficient number of suppliers would remain present in the market.

(95) In addition, no respondent to the market investigation raised substantiated concerns in relation to the impact of the Transaction on non-life insurance markets in Poland, highlighting instead the complementarity of the Parties’ portfolio and the fact that with respect to non-life insurance overall, they will remain significantly smaller than current Polish insurance market leaders (PZU, ERGO Hestia and Warta/Talanx) post-Transaction.91

(96) Based on the considerations above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the potential market for non-life insurance in Poland, including for (i) group accident insurance; (ii) group sickness insurance; and (iii) CASCO insurance of rail vehicles.

4.2.2. Non-horizontal effects

4.2.2.1. Introduction

(97) The Commission’s Guidelines on the assessment of non-horizontal mergers under the Merger Regulation (the "Non-Horizontal Merger Guidelines") distinguish between two main ways in which vertical mergers may significantly impede effective competition, namely input foreclosure and customer foreclosure.92

(98) For a merger to raise input foreclosure competition concerns, the merged entity must have a significant degree of market power upstream.93 In assessing the likelihood of an anticompetitive input foreclosure strategy, the Commission has to examine whether (i) the merged entity would have the ability to substantially foreclose access to inputs; (ii) whether it would have the incentive to do so; and (iii) whether a

Table 1, two alternative providers of DDS pension fund products remain in the market, that offer a largely similar product as the merged entity. Second, downstream competitors supply customers with a portfolio of products, which may include other pension products, mutual funds or insurance products, Therefore, DDS pension fund products of the merged entity are not a crucial product for companies active in the downstream market. The Commission therefore considers that the merged entity would lack the ability to engage in any input foreclosure strategy.

(104) Incentive to foreclose: Additionally, the Commission considers that the merged entity would not have the incentive to foreclose downstream competitors post- Transaction. The Parties’ distribution channels are rather complementary, as TB DDS distributes more than [70-80]% of its products [through group entities], while AXA DDS uses […] a network of agents and brokers. The Commission therefore considers that the merged entity has no clear incentive to switch the distribution of the Target’s DDS pension fund products mainly to Tatra Banka, because Tatra Banka already offers a comparable product of TB DDS. Moving the Target’s DDS operation to the distribution network of Tatra Banka would come at the cost of limiting the merged entity’s ability to reach customers via brokers and agents with DDS pension fund products, and is therefore unlikely to be profitable. Consequently, the merged entity lacks an incentive to foreclose.

(105) Impact of foreclosure: The Commission considers that the Transaction is unlikely to have an impact on competition in the market for distribution of DDS pension fund products or distribution of voluntary retirement saving products in general. Downstream competitors do not rely on the input of the merged entity, which would therefore not be in a position to raise downstream prices. This is confirmed by results of he market investigation, as the overwhelming majority of responding brokers stated that the Transaction would have no impact on the distribution of DDS pension fund products in Slovakia.98

(106) Based on the considerations above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the vertical link between the market of DDS pension fund products and the market of distribution of DDS pension fund products in Slovakia.

4.2.2.3. Custody and depositary service (upstream) / DDS pension fund products (downstream) in Slovakia

(107) In Slovakia, there is a limited customer base for depositary services alone. National regulation requires suppliers of DSS pension fund products, DDS pension fund products and asset managers to source such services.99 Custody services, in turn, have a significantly broader customer base, as they can also be sourced for instance by insurance companies.100 Markets become affected as the combined market shares of the merged entity in the downstream market for DDS pension fund products exceed 30%, a product that requires depositary services. In addition, the merged

for companies, even if depositary services were ultimately considered to be a product market separate from custody services. This also limits the effect that a potential foreclosure to depositary customers by the merged entity has on the ability of upstream competitors to operate efficiently since rival’s costs would not be driven up for custody services, which rely on the same assets and personnel.

(111) Incentive to foreclose: Moreover, the Commission considers that the merged entity lacks a clear incentive to foreclose upstream competitors by moving the Target’s demand for depositary services to Tatra Banka. First, the Commission notes that the Target has been relying on the same provider of such depositary services since 2004. The Notifying Party currently does not source all demand for depositary services in- house, as TB DDS sources depositary services from a competitor, and there is no clear argument why this would change post-transaction.106 Second, the merged entity would be unable to enjoy higher price levels downstream as a result of the regulatory framework applicable to DDS products, for the reasons laid out in Section 4.2.1.1.

(112) Impact of foreclosure: The Transaction is unlikely to have an impact on prices in the upstream market of depositary services. Apart from Tatra Banka, five other suppliers of depositary services are active in Slovakia, three of which the Parties currently does not source from, and that therefore cannot be foreclosed.107 Raising prices for the provision of depositary services is indeed not a concern for downstream companies. During the market investigation, the overwhelming majority of responding voluntary retirement saving competitors (who typically also procure depositary and/or custody services) considered the Transaction would not have an impact on the market for the provision of these services.108

(113) Based on the considerations above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the vertical link between the market of custody and depositary services and the market of the provision of DDS pension fund products in Slovakia, even if a separate product market for depositary services was defined.

4.2.2.4. Asset management (upstream) / DDS pension fund products (downstream) in Slovakia

(114) The link between asset management and the provision of DDS pension fund products leads to affected markets due to the considerable market share of the merged entity in the downstream market. Both the Notifying Party and the Target are present in asset management and the provision of DDS pension fund products in Slovakia.

(A) Notifying Party’s view

(115) The Notifying Party argues that the Target offers only captive institutional asset management services. The Target’s downstream operations would source its demand for asset management services entirely in-house. Therefore, the Transaction would

downstream of asset management in Slovakia.112 The overwhelming majority of responding asset managers also considered the Transaction to have no negative impact on the asset management market in Slovakia, while none of the participants expressed the view that the Transaction would affect any sub-segments of asset management.113 One of the two competitors in DDS pension fund products stated that the Transaction would have an impact on asset management in Slovakia, while none of the responding suppliers of other voluntary saving products such as pension insurance or mutual funds considered the Transaction to have such an impact.114

(120) Consequently, the Commission considers customer foreclosure by the merged entity unlikely to have in impact on effective competition on the upstream market.

(121) Based on the considerations above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the vertical link between the market of asset management and the market of the provision of DDS pension fund products in Slovakia.

4.2.2.5. Asset management (upstream) / Distribution of asset management (downstream) in Slovakia

(122) This affected market stems from the fact that Tatra Banka’s market share in asset management distribution exceeds 30% for the distribution of mutual funds, as well as in the potential sub-segment of distribution of retail mutual funds in Slovakia. The Target is active in asset management services in Slovakia, but does not have an integrated downstream business.

(A) Notifying Party’s view

(123) The Notifying Party provides that the main asset managers in Slovakia are integrated into banking groups and therefore would not be affected by foreclosure by the merged entity. Moreover, Tatra Banka predominantly distributes products of its own upstream entity TAM, which further reduces the potential for customer foreclosure, as competitors currently do not rely on Tatra Banka as distribution channel.

(B) Commission’s assessment

(124) The merged entity’s market shares barely exceed 30% in the downstream market. The relevant potential concern with respect to the vertical link between asset management and the distribution of asset management via the banking activities of the Notifying Party is therefore customer foreclosure. Market shares of the merged entity are presented in the Table below:

management in Slovakia.119. Therefore, the Commission considers customer foreclosure by the merged entity unlikely to have in impact on effective competition on the upstream market.

(128) Based on the considerations above, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the vertical link between the market of asset management and the market of distribution of asset management in Slovakia.

5. CONCLUSION

(129) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C 216, 30.6.2020, p. 21.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 See M.9432 - Allianz Holdings / Legal and General Insurance, para 7 and cases cited.

6 See M.8837 Blackstone/Thomson Reuters F&R Business, para 29; M.8257 NN Group/Delta Lloyd, para 12; M.7478 Aviva/Friends Life/Telenet, para 13; M.6743 Talanx International/Meiji Yasuda Life Insurance Company/HDI Poland, para 19.

7 See M.8837 - Blackstone / Thomson Reuters F&R Business, para 29; M.8257 - NN Group / Delta Lloyd, para 12; M.7478 Aviva / Friends Life / Telenet, para 13, and cases cited.

8 See M.9432 Allianz Holdings/Legal and General Insurance, para 8; COMP/M.9056 Generali CEE/AS, para 12; COMP/M.8257 NN Group/Delta Lloyd, para 73; COMP/M.4844 Fortis/ABN Amro Assets, para 72.

9 Specifically regarding Poland for instance, the Commission considered a potential segmentation according to risk classes defined by the Polish Insurance Act. See M.6743 Talanx International / Meiji Yasuda Life Insurance Company / Hdi Poland, paras 22 et seq. Such classes include group accident insurance (class 1) sickness insurance (class 2) and (iii) CASCO insurance of rail vehicles (class 4), which are potentially affected markets in the present case.

10 See M.8257 - NN Group / Delta Lloyd, para. 16 and cases cited (for life insurance); M.9531 - Assicurazioni Generali / Seguradoras Unidas / AdvanceCare, para. 13 and cases cited (for non-life insurance). For certain non-life insurance products, including MAT insurance and generally large risk insurance, the Commission have considered the market to be potentially wider than national in scope. See M.9056 - Generali CEE/AS, para. 16 and cases cited.

11 See Form CO, para 100.

12 See Form CO, para 109.

13 See Form CO, para 112.

14 See Form CO, Annex 12.

15 See Form CO, paras 269 and 346.

16 For voluntary retirement savings products an affected market only arises in Slovakia.

17 See Form CO, para 142 and 618.

18 See M..4950 Aviva/Bank Zachodni, para 21.

19 See M.8257 NN Group/Delta Lloyd, paras 48 et seq.

20 See M.8257 NN Group/Delta Lloyd, para 53.

21 See M.4950 Aviva/Bank Zachodni, para 24.

22 See Form CO, para 198 et seq. and 209.

23 See response to question 5 of Questionnaire Q1.

24 See response to question 5.1 and 8 of Questionnaire Q1.

25 See response to question 10 of Questionnaire Q1.

26 See response to question 9 of Questionnaire Q1.

27 See response to question 11 of Questionnaire Q1.

28 See response to question 12 of Questionnaire Q2.

29 See response to question 13 of Questionnaire Q2.

30 See reply to an email questionnaire received on 24. April 2020.

31 See reply to an email questionnaire to the National Bank of Slovakia, received on 24. April 2020.

32 See reply to an email questionnaire to the National Bank of Slovakia, received on 24. April 2020 and

response to question 5.1 and 9 of Questionnaire Q1.

33 See response to question 9 of Questionnaire Q1 and reply to an email questionnaire to the National Bank of Slovakia received on 24. April 2020

34 See Form CO, para 218.

35 See M.8257 NN Group / Delta Lloyd, paras 98, 102.

36 See M.4950 Acica / Bank Zachodni, para 31.

37 See Form CO, para 220, 221.

38 Affected distribution of voluntary retirement saving product markets only arise in Slovakia.

39 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 16.

40 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 17; M.6812 SFPI / Dexia, para 31.

41 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 18; M.5728 Credit Agricole / Societe

Generale Asset Management, para 35, COMP/M.5580 Blackrock / Barclays Global Investors UK Holdings, para 10.

42 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 19; M.5728 Credit Agricole / Societe Generale Asset Management, paras 68, 69.

43 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 20; M.3894 Unicredito / HVB, para 35.

44 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 28; M.8257 NN Group / Delta Lloyd,para 112; M.6812 SFPI / Dexia, para 32.

45 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 32.

46 See M.9359 Amundi / Credit Agricole / Pioneer Investments, para 33, M.5384 BNP Paribas / Fortis, para 10.

47 M.5384 BNP Paribas / Fortis, para 86.

48 See Form CO, paras 135, 137.

49 See minutes call with a competitor, 1 July 2020, para 3.

50 See M.8257 NN Group / Delta Llyod, para 110.

51 See M.3781, Crédit Agricole / Caisse d' Epargne / JV, para 20.

52 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 39.

53 See M.3894 Unicredito / HVB, para 37.

54 See M.8359 Amundi / Credit Agricole / Pioneer Investments, para 35.

55 See M.3894 Unicredito / HVB, para 37.

56 See Form CO, paras 229, 230.

57 See Form CO, paras 534 and 541.

58 See Minutes of a phone call with a competitor, 1 July 2020, paragraph 7.

59 Affected custody and depositary markets arise only in Slovakia.

60 See Minutes of a phone call with a competitor, 1 July 2020, paras 3 and 8.

61 Horizontal Merger Guidelines, paras 24 et seqq.

62 See Form CO, para 20.

63 See Regulation (EU) 2019/1238 of the European Parliament and of the Council of 20 June 2019 on a pan- European Personal Pension Product.

64 Source: The Parties’ estimates.

65 RBI holds 78.8 % of the shares in Tatra Banka. TB DDS is a fully owned subsidiary of Tatra Banka.

66 These market shares do not differ substancially when measured by number of contacts

67 See response to question 12.1 of Questionnaire Q3

68 See response to question 24 of Questionnaire Q1

69 See response to question 15 of Questionnaire Q1

70 See response to question 13 of Questionnaire Q1 ; response to question 16 of Questionnaire Q2 ; response to question 14 of Questionnaire Q3

71 See response to question 16 of Questionnaire Q1. Respondents were asked to choose among the following

options Additional products offered by the DDS company (e.g. insurance or banking products), Brand recognition, Employer preference, Existing customer relationship with the DDS (or the group of companies it belongs to), Expected return on investment, Information provided by the provider, Level of fees, Marketing campaigns, Provider representation (local offices etc.), Safety profile of the investment, Other.

72 See response to question 18 of Questionnaire Q1.

73 See response to question 21 of Questionnaire Q1.

74 See response to question 21 of Questionnaire Q2.

75 See response to question 25 of Questionnaire Q1; response to question 25 of Questionnaire Q2; response to question 18 of Questionnaire Q3.

76 See response to questions 25 of Questionnaire Q1

77 See response to question 25.1 of Questionnaire Q2.

78 See response to question 25.5 of Questionnaire Q1

79 See Minutes of a phone call with a competitor, 8 April 2020, paragraph 20.

80 See response to question 22 of Questionnaire Q1; response to question 24 of Questionnaire Q2; response to question 17 of Questionnaire Q3.

81 Form CO, paras 388, 398, 399.

82 See responses of question 5 of Questionnaire Q4 ; one respondent refered to AXA as « a niche distributorin Slovakia », will another one described the company as a « smaller player ». Only one of seven competitors considered that the Transaction would have a negative effect on asset management in Slovakia ; the respondent explained that the Transaction would be « decreasing » […] competition », and and stated that « any company is good »

83 See responses of question 7 and 8 of Questionnaire Q4. Only one of seven competitors considered that the Transaction would have a negative effect on asset management in Slovakia, explaining that the Transaction would be « decreasing […] competition » and stated that « any competition is good ».

84 See Form CO para 262

85 See Guidelines on the assessment of horizontal mergers under the Council regulation of the control of concentrations between undertakings, OJ C 031, of 05/02/2004 (the Horizontal Merger Guidelines ») para 18.

86 See responses to question 29 of Q1 ; response to question 28 of Q3 ; and response to question 20 of Q4. One respondent indicated that the Transaction could have a negative impact on the insurance market as the Parties are « […] two significantly (sic) different companies with very low synergies in terms of organisation and services to the clients […] », impliying that the Parties are not close competitors on the Slovak market. Another one indicated in general terms that the Transaction could have an impact on the insurance market, as the « […] [r]isks of any merger are well documented. Lower choice on the market, bigger less flexible corporation. Economies of scales etc. »

87 The potential market for non-life group insurance is also technically affected. However, as such market combines both group accident insurance and group sickness insurance, the competitive assessment does not differ from those narrower segments put together and will thus not be addressed separately.

88 According to the Notifying Party, the total market volume split between group and individual customers for 2019 will only be made available by the relevant authority in September 2020.

89 See Horizontal Merger Guidelines, para. 18.

90 See Horizontal Merger Guidelines, para. 18.

91 See response to questions sent to Polish insurance competitors; see response to questions sent to Polish insurance brokers. One respondent indicates that the two companies compete closely in motors insurance, but based on available data, their combined market share on this segment does not exceed 10% in any plausible market (including when looking at individual insurance classes for third party liability or hull motor insurance).

92 OJ L 24, 29.1.2004, p. 1.

93 Non-horizontal Merger Guidelines, paragraph 35.

94 Non-horizontal Merger Guidelines, paragraph 32

95 Non-horizontal Merger Guidelines, paragraph 61

96 Non-horizontal Merger Guidelines, paragraph 59

97 Form CO, para 500.

98 Form CO, para 534.

99 Form CO, para 549.

100 The customer base for custody services by AuM would be around EUR 60,000 million, while the customer base of depositary services alone by AuM would be around EUR 20,000 million, see Form CO, para 536, and Form CO, footnote 212.

101 The Commission notes that DDS companies are not the only customers in Slovakia that source depositary services. Across all products that demand depositary services (DDS, DSS and asset management), the merged entity would form approx [40-50]% of the entire customer base.

102 See response to RFI 4, paragraph 6

103 The Commission notes that DDS companies are not the only customers in Slovakia that source depositary services

104 The Commission notes that changing the Target’s provider for depositary services would require the approval by the National Bank of Slovakia, and would be subject to the assessment whether Tatra Bank would be in a position to provide unbiased depositary services to AXA DDS, despite the structural links.

105 Minutes call with a competitor, 1 July 2020, para 3.

106 Form CO, Table 20.

107 Form CO, para Table 20.

108 See response to question 27 of Questionnaire Q1; the only respondent who does consider the Transaction to have an impact stated that it would lead to a “higher concentration in depository services providers” which is factually inacurrate as the Target does not offer such services.

109 Form CO, paras 480, 481.

110 Form CO, para 470.

111 Form CO, para 423.

112 See responses to question 9 of Questionnaire Q4; the company that considered the Transaction to have an impact on upstream or downstream markets did not specify its assessment, and explained only that the Transaction would lead to “lower competition”.

113 See responses to questions 7 and 9 of Questionnaire Q4.

114 See responses to question 26 of Questionnaire Q1; the one competitor that expects the Transaction to have an impact on asset management provides that “DDS Tatrabaka (sic) and Uniqua (sic) [would have the] majority in the DDS market”.

115 See responses to question 9 of Q4 ; the company that considered the Transaction to have an impact on upstream or downstream markets did not specify its assessment and explained only that the Transaction would lead to « lover competition »

116 See responses to questions 7 and 9 of Q4

117 The Notifying Party estimates that AXA’s market offering excluding captive services would only amount to a market shares of [0-5] % , see Form CO, para 418.

118 Form CO, para 423 .

119 See responses to question 9 of Questionnaire Q4; the company that considered the Transaction to have an impact on upstream or downstream markets did not specify its assessment, and explained only that the Transaction would lead to “lower competition”.