Commission, July 27, 2020, No M.9736

EUROPEAN COMMISSION

Judgment

LONE STAR / BASF CONSTRUCTION CHEMICALS (EB) BUSINESS

Subject: Case M.9736 – Lone Star/BASF Construction Chemicals (EB) business Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 22 June 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which LSF11 Skyscraper Investments S.à r.l. (Luxembourg), an indirect subsidiary of Lone Star Fund XI, L.P. (“LSF XI”, Bermuda), and belonging to the global private equity group Lone Star Funds (“Lone Star”, USA) acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of BASF’s construction chemicals business (“BASF’s EB business”, Germany).3 Lone Star is referred to as “the Notifying Party” and, together with BASF’s EB business, as “the Parties”.

1. THE PARTIES

(2) Lone Star is a private equity firm that invests globally in real estate, equity, credit and other financial assets. Two of the companies controlled by Lone Star are of interest in the case at hand, namely Xella International S.A. (“Xella”, Germany) and Stark Group A/S (“Stark”, Denmark). Xella is a producer of autoclaved aerated concrete (“AAC”) products in the EEA. Stark is a building materials distributor in the Nordic countries and Germany.

(3) BASF’s EB4 business produces and distributes admixture systems and construction systems for new constructions, maintenance, repair and renovation of residential and commercial buildings, as well as infrastructure. BASF’s EB business has two main lines of business, namely (i) EBA5, which is specialised in the manufacture of additives for concrete and other cementitious materials and (ii) EBC6, which produces concrete repair and protection systems, performance grouts, waterproofing systems, sealants, performance flooring systems, wall systems and coatings for mulch and wood fibres.

2. THE OPERATION AND THE CONCENTRATION

(4) On 21 December 2019, the Parties entered into a sales and purchase agreement pursuant to which BASF’s EB business will be transferred to the Notifying Party. The Transaction will be accomplished by way of purchase of shares.

(5) Following completion of the Transaction, the Notifying Party will thus acquire sole control of BASF’s EB business. The Transaction is therefore a concentration within the meaning of Article 3(1)(b) of the EU Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (Lone Star: EUR […] million; BASF’s EB business: EUR […] million)7. Each of them has an EU-wide turnover in excess of EUR 250 million (Lone Star: EUR […] million; BASF’s EB business: EUR […] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension.

4. MARKET DEFINITIONS

4.1. Introduction

(7) BASF’s EB business is active in the manufacture of polymer-based concrete admixtures (through EBA), as well as mortars and several other specialty construction products (through EBC).

(8) Xella, one of the companies currently under the control of Lone Star, is active in the production of construction materials, and in particular the following products:

(a) autoclaved aerated concrete (“AAC”) blocks; which are a lightweight, precast, foam concrete building material made of autoclaved aerated concrete which can be lifted by hand and do not require equipment for handling;

(b) AAC large format prefabricated compound units; which are made of the same material as AAC blocks, but require equipment such as cranes for handling;

(c) Aerated concrete roofing panels, fire walls and outer walls; which are a sub- category of AAC large format prefabricated compound units that are specifically used for roofing, walls, as well as fire walls applications;

(d) Mineral insulation boards; which are niche insulation products suitable for special types of applications;

(e) calcium silicate units (“CSU”); which are masonry product units made from a mixture of lime and natural siliceous materials (sand, siliceous gravel or rock or mixtures thereof);8

(f) Mortars.9

(9) In this Decision, AAC large format prefabricated compound units will be referred to as “AAC large format units” for concision’s sake, and, together with AAC blocks as “AAC products”.

(10) Xella’s activities were examined closely in three recent Commission decisions all related to Lone Star.10

(11) Stark is active in the distribution of building products at retail level, to both professional and non-professional customers.

(12) The Transaction gives thus rise to different horizontal and vertical overlaps between the activities of BASF’s EB business, Xella and Stark.

4.2. Concrete admixtures

(13) Concrete admixtures are used to modify the properties of concrete and to provide it with some specific qualities. Concrete admixtures include air entrainers, water reducers, accelerators, retardants as well as plasticisers.

4.2.1. Product market definition

4.2.1.1. Commission precedents

(14) In the past,11 the Commission found that chemical-based and mineral-based admixtures constitute separate product markets.

(15) The Commission excluded any further segmentation of chemical-based and mineral- based admixtures. In particular, the Commission excluded the relevance of a potential distinction between different uses of admixtures (such as concrete admixtures, cement admixtures or mortar admixtures) because of a high degree of supply side substitutability between the different chemical admixtures for those uses.12

4.2.1.2. The Notifying Party’s view

(16) The Notifying Party points out that BASF’s EB business is only active in chemical- based (and in particular polymer-based) concrete admixtures, thus belonging to the wider market of chemical admixtures.13 None of the companies controlled by Lone Star is active in the manufacture of concrete admixtures.

(17) The Notifying Party agrees with the Commission’s precedents, and provided BASF’s EB business’ market shares in the market of chemical-based admixtures.14

4.2.1.3. Results of the market investigation and conclusion

(18) Admixture customers15 and competitors16 confirmed that chemical-based admixtures are not substitutable with other products and therefore constitute a distinct product market. Both admixture customers17 and competitors18 also confirmed that no further segmentation of chemical-based admixtures by use or sub-category is necessary. In light of the above and for the purposes of the assessment of the Transaction, the Commission considers that chemical-based admixtures constitute a separate product market, distinct from the market for mineral-based admixtures, and that no further segmentation is necessary.

4.2.2. Geographic market definition

4.2.2.1. Commission precedents

(19) In the past,19 the Commission has left open whether the relevant geographic market for concrete admixtures was EEA-wide or narrower, and has analysed competition on the basis of national markets as the narrowest plausible market definition.

4.2.2.2. The Notifying Party’s view

(20) The Notifying Party does not express a view on the relevant geographic market for chemical-based admixtures, but provided BASF’s EB business’ market shares in chemical-based admixtures at national level.

4.2.2.3. Results of the market investigation and conclusion

(21) Replies of admixture customers and competitors indicate that the market may be wider than national. Responding customers are somewhat split between a regional market (a cluster of neighbouring countries), an EEA-wide market, or even a worldwide market.20 The majority of responding competitors see the market as worldwide.21 Ultimately, the question of whether the appropriate geographic market definition is national, or wider (regional, EEA-wide or worldwide) can be left open, as the Commission considers that the Transaction does not raise serious doubts for either geographic market definition. In this decision, the Commission will carry out its assessment on a national market basis as the narrowest plausible geographic market definition, this being the most conservative approach, since BASF EB business’ market shares would be lower under any broader geographic market definitions for chemical-based admixtures.

4.3. Mortars

4.3.1. Product market definition

4.3.1.1. Commission precedents

(22) In the past, the Commission has made a distinction between premix mortars, which are mixed at the factory and on-site mortars, which are mixed on the construction site.22 Within premix mortars, the Commission has distinguished between dry mortars (supplied in a dry powder form), wet mortars (ready-mixed with water at the factory), and ready-to-use paste mortars (supplied as paste, including organic compounds as binders.23 Moreover, the Commission has also distinguished between mortars based on the application, namely: (i) construction mortars, used for various building construction purposes, such as casting and setting, masonry, plastering, floor levelling and concrete repair; (ii) façade mortars, used as an outer layer of buildings for protective or aesthetic purposes, or as part of insulation systems and

(iii) tile-fixing mortars used for fixing tiles, both on substrate (adhesive mortars) and as sealants between tiles (grouts).24

4.3.1.2. The Notifying Party’s view

(23) The Notifying Party does not express a view on the relevant product market for mortars.

4.3.1.3. Results of the market investigation and conclusion

(24) Replies in the market investigation of competitors25 active in mortars confirmed the relevance of the Commission’ precedents in this respect, as well as the absence of a need to further sub-segment the market.

(25) The questions of whether the appropriate product market definition is mortars as a whole or whether separate product markets exist for any of the segmentations listed in paragraph (22), which were considered in previous decisions, can be left open, as the Commission finds that no serious doubts arise for any of the possible product market definitions.

4.3.2. Geographic market definition

4.3.2.1. Commission precedents

(26) In the past, the Commission left the geographic market definition open and conducted the competitive assessment both at national and at local/regional levels, assuming a 120 km radius around the production plant.26 In its most recent decisional practice, the Commission has carried out its competitive assessment on the basis of national markets but, with regard to large volume/low value heavy mortars, it has also considered narrower hypothetical regional/local markets, assuming a 120 km radius around production plants.27

4.3.2.2. The Notifying Party’s view

(27) The Notifying Party does not express a view on the relevant geographic market for mortars, but explains that the types of mortars sold by BASF’s EB business, as well as Xella, do not fall under the category of large volume/low value heavy mortars, for which the competitive assessment should be carried out on the basis of a 120 km radius around production plants, and consequently provide the Parties’ market shares for mortars at national level only.28

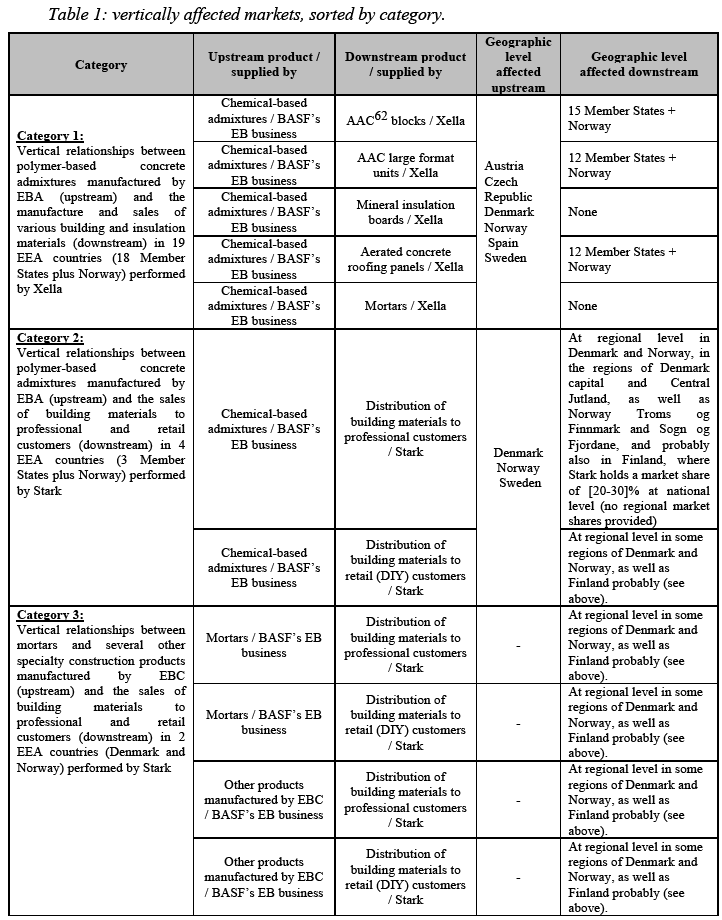

4.3.2.3. Results of the market investigation and conclusion

(28) The majority of the replies in the market investigation of competitors29 active in mortars showed that the geographic scope for these products would be national. In light of the above and for the purposes of the assessment of the Transaction, the Commission considers that the market for mortars other than large volume/low value heavy mortars (which are of no relevance in the case at hand) could be national in scope. In any event, the precise geographic market definition can be left open, as the Transaction does not raise serious doubts under any plausible market definition (see paragraphs (22) and (26) above).

4.4. AAC blocks

4.4.1.Product market definition

4.4.1.1. Commission precedents

(29) In the past, the Commission found that AAC blocks form a single relevant product market, which is not likely to comprise other products.30 No further sub- segmentation was considered.31

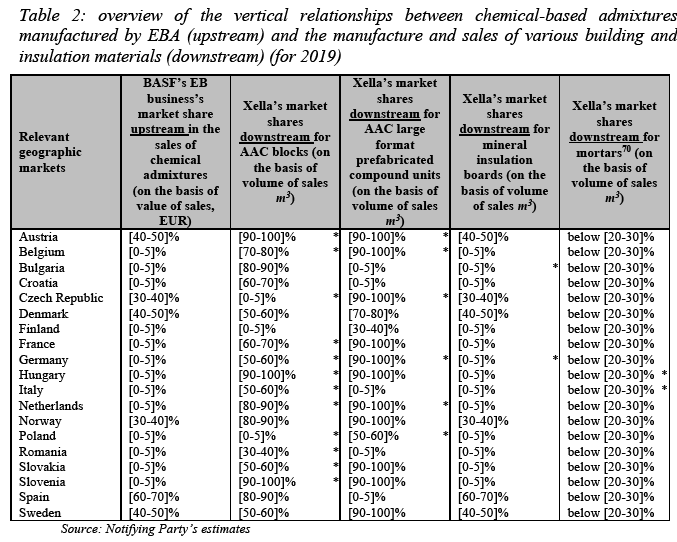

4.4.1.2. The Notifying Party’s view

(30) The Notifying Party considers that the product market definition for AAC blocks should encompass other products, such as aggregate blocks and potentially also other wall-building materials, in particular bricks, sand-lime bricks/calcium silicate units and pumice blocks.32 The Notifying Party, however, considers that the exact product market can be left open.33

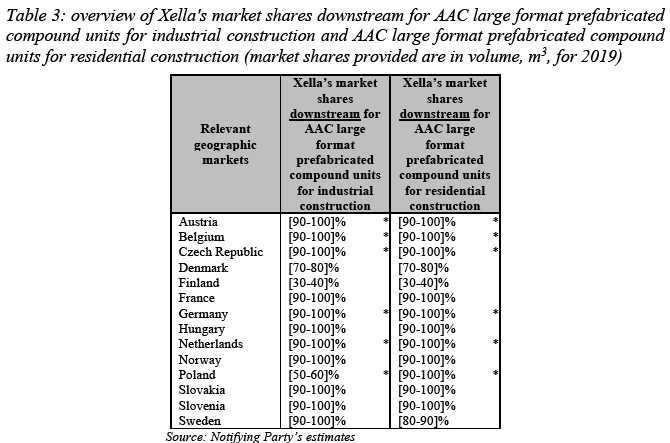

4.4.1.3. Results of the market investigation and conclusion

(31) Responses of AAC competitors suggest that AAC blocks may be substitutable with some other products34 and could thus be part of a broader product market including those other products as well.35 AAC competitors also took the view that no further sub-segmentation of AAC blocks by type or category was necessary.36

(32) In light of the above and for the purposes of the assessment of the Transaction, the Commission considers that the question of whether AAC blocks constitute a separate product market or are part of a wider market also encompassing products such as clay bricks, clay blocks, aggregate blocks, dense concrete blocks, CSU and other building products can be left open, as the Commission considers that the Transaction does not raise competitive concerns under either product market definition. The Commission also considers that no further segmentation of AAC blocks is necessary. For the purposes of this decision, the Commission will carry out its assessment on the basis of a market restricted to AAC blocks only as the narrowest plausible product market definition, this being the most conservative approach, since Xella’s market shares would be lower under any broader product market definitions for AAC blocks

4.4.2. Geographic market definition

4.4.2.1. Commission precedents

(33) In the past, the Commission found that the relevant geographic market for AAC blocks was local in scope and examined the market for AAC blocks in Germany under four separate regions (North Germany, West Germany, South Germany and East Germany).37

4.4.2.2. The Notifying Party’s view

(34) The Notifying Party submits that the geographic market for AAC blocks is at least national in scope.38

4.4.2.3. Results of the market investigation and conclusion

(35) Responses of AAC competitors took the view that the geographic scope of the AAC blocks market is narrower than national.39

(36) Ultimately, the question whether the appropriate geographic market definition is national or local (smaller than national) can be left open, as the Commission considers that the Transaction does not raise serious doubts for either geographic market definition.

4.5. AAC large format units and aerated concrete roofing panels, fire walls and outer walls

4.5.1. Product market definition

4.5.1.1. Commission precedents

(37) AAC large format units and aerated concrete roofing panels, fire walls and outer walls were examined by the Commission in Case M.9406 – Lone Star – Stark group / Saint-Gobain BDD. In this case, the Commission found that aerated concrete roofing panels, fire walls and outer walls were part of the same market as AAC large format units. The Commission also found indications that AAC large format units for industrial construction are not substitutable with those for residential construction. However, the Commission ultimately left the exact product definition for AAC large format prefabricated compound units open.

4.5.1.2. The Notifying Party’s view

(38) The Notifying Party agrees that AAC large format units for industrial construction are not substitutable with those for residential construction, but considers that each of them form part of a broader product market. More specifically, the Notifying Party submits that AAC large format units for industrial construction form part of a market that also encompasses concrete panels and steel elements (but not elements made of in situ poured concrete which is not a usual method of producing panels for industrial buildings) and that AAC large format units for residential construction form part of a market that also encompasses concrete floor elements and full assembly floors out of reinforced concrete.40

4.5.1.3. Results of the market investigation and conclusion

(39) Responses of AAC competitors indicate that AAC large format units are substitutable with some other products41 and could thus be part of a broader product market including those other products42 as well. They also replied that no further sub-segmentation of AAC large format units by type or category was necessary.43

(40) Concerning aerated concrete roofing panels, firewalls and outer walls, AAC competitors confirmed that they are part of the market for AAC large format prefabricated compound units,44 and that no further-sub-segmentation would be necessary.45

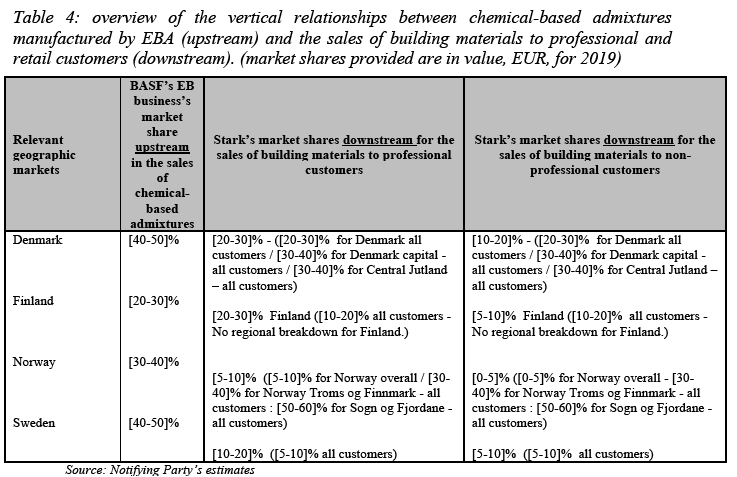

(41) In light of the above and for the purposes of the assessment of the Transaction, the Commission considers that the question of whether AAC large format units constitute a separate product market comprising aerated concrete roofing panels, fire walls and outer walls or are part of a wider market also encompassing products such as AAC blocks, prefabricated concrete panels or steel panels can be left open, as the Commission considers that the Transaction does not raise serious doubts under either product market definition. The Commission also considers that the question of whether a further sub-segmentation between AAC large format units for industrial construction and AAC large format units for residential construction is appropriate can be left open, as the Commission finds that the Transaction does not raise serious doubts under any product market definition set out above, this being the most conservative approach, since any wider product market definition for AAC large format units would lower Xella’s market shares.

4.5.2. Geographic market definition

4.5.2.1. Commission precedents

(42) In Case M.9406 – Lone Star – Stark group / Saint-Gobain BDD, the Commission left open whether the relevant geographic market for AAC large format units should be considered as local or national in scope.

4.5.2.2. The Notifying Party’s view

(43) The Notifying Party submits that the relevant geographic market is national.46

4.5.2.3. Results of the market investigation and conclusion

(44) Responses of AAC competitors in the market investigation confirmed that the geographic scope of the AAC large format prefabricated compound units, as well as for aerated concrete roofing panels, firewalls and outer walls markets are narrower than national. 47

(45) Ultimately, the question whether the appropriate geographic market definition is national or local (smaller than national) can be left open, as the Commission considers that the Transaction does not raise serious doubts for either geographic market definition.

4.6. Mineral insulation boards

4.6.1. Product market definition

4.6.1.1. Commission precedents

(46) The product market definition for mineral insulation boards has not been examined in any Commission precedent so far.

4.6.1.2. The Notifying Party’s view

(47) The Notifying Party considers that mineral insulation boards are part of a broader market encompassing other solution for interior and exterior insulation of buildings. The Notifying Party nonetheless explains that the exact product market definition for mineral insulation boards can be left open since Xella’s market shares would not exceed 20% under any plausible product or geographic market definition.48

4.6.1.3. Results of the market investigation and conclusion

(48) Mineral insulation boards manufacturers indicated that mineral insulation boards are substitutable with some other insulation products49 and could thus be part of a broader product market including those other products50 as well. They also replied that no further sub-segmentation of mineral insulation boards by type or category was necessary.51

(49) In light of the above and for the purposes of the assessment of the Transaction, the Commission considers that the question of whether mineral insulation boards constitute a separate product market or are part of a wider market also encompassing other insulation products can be left open, as the Commission considers that the Transaction does not raise serious doubts under either product market definition. The Commission also considers that no further segmentation of mineral insulation boards is necessary. In this decision, the Commission will carry out its assessment on the basis of a market restricted to mineral insulation boards only as the narrowest plausible product market definition, this being the most conservative approach (as indicated by the market investigation), since any wider product market definition for mineral insulation boards would lower Xella’s market shares.

4.6.2. Geographic market definition

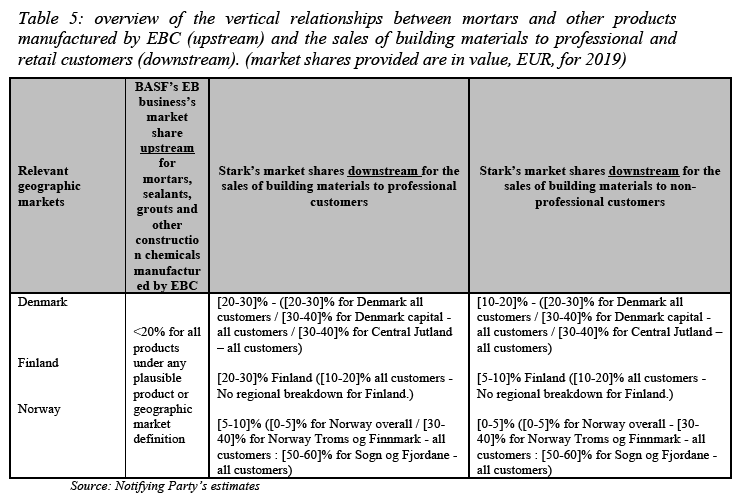

4.6.2.1. Commission precedents

(50) The geographic market definition for mineral insulation boards has not been examined in any Commission precedent so far.

4.6.2.2. The Notifying Party’s view

(51) The Notifying Party believes that the relevant geographic market for mineral insulation boards is national in scope.52

4.6.2.3. Results of the market investigation and conclusion

(52) Replies of mineral insulation boards manufacturers indicate that the geographic scope for mineral insulation boards is national, or even wider.53

(53) In light of the above and for the purposes of the assessment of the Transaction, the Commission considers that the question whether the appropriate geographic market definition is national, or wider (regional or EEA-wide) can be left open, as the Commission considers that the Transaction does not raise serious doubts for either geographic market definition. In this decision, the Commission will carry out its assessment on a national market base as the narrowest plausible geographic market definition, this being the most conservative approach (as confirmed by the market investigation), since any wider geographic market definition, mineral insulation boards would lower Xella’s market shares.

4.7. Distribution of building products

4.7.1. Product market definition

4.7.1.1. Commission precedents

(54) In its previous decisions, the Commission considered that the markets for the distribution of building materials in general can be divided into: (i) wholesale sales to retailers; (ii) retail sales to professional customers (B2B); and (iii) retail sales to non-professional customers (primarily through DIY stores), but left the precise product market definition ultimately open.54

4.7.1.2. The Notifying Party’s view

(55) The Notifying Party considers the above-mentioned product market segmentation to be conceivable, but nonetheless considers that it improperly reflects the real condition of the market. The Notifying Party considers in particular that distributors of construction materials do not keep track of their sales based on such a segmentation.55

4.7.1.3. Results of the market investigation and conclusion

(56) Replies of distributors of building materials fully confirmed the Commission’s precedents regarding the product market definitions for the distribution of building products.56

(57) Ultimately, the question of whether further sub-segmentation of the distribution of building material, between (i) wholesale sales to retailers; (ii) retail sales to professional customers (B2B); and (iii) retail sales to non-professional customers (primarily through DIY stores) is appropriate or not can be left open, as the Commission finds that the Transaction does not raise serious doubts under any product market definition set out above.

4.7.2. Geographic market definition

4.7.2.1. Commission precedents

(58) The Commission has previously considered that the scope of the market for the distribution of building products as well as its potential sub-segments (retail sales to professional customers and retail sales to non-professional customers) is either national or potentially smaller than national.57

4.7.2.2. The Notifying Party’s view

(59) The Notifying Party submits that while the geographic market might exhibit both some national and some regional features, the vertical nature of this case would make it appropriate to consider these markets on a national basis only.58

4.7.2.3. Results of the market investigation and conclusion

(60) Replies of distributors of building materials showed clearly that the market for the distribution of building products is narrower than national, both for professional and for retail customers.59

(61) Ultimately, the question whether the appropriate geographic market definition is national or local (smaller than national) can be left open, as the Commission considers that the Transaction does not raise serious doubts for either geographic market definition.

5. COMPETITIVE ASSESSMENT

5.1. Overview of affected markets

(62) The Transaction does not give rise to any horizontally affected markets.

(63) The Transaction however gives rise to several affected vertical links, that can be classified under three main categories, namely

(i) the vertical relationships between polymer-based concrete admixtures manufactured by EBA (upstream) and the manufacture and sales of various building and insulation materials (downstream) in 19 EEA countries (18 Member States60 plus Norway) performed by Xella;

(ii) the vertical relationships between polymer-based concrete admixtures manufactured by EBA (upstream) and the sales of building materials to professional and retail customers (downstream) in 4 EEA countries (three Member States61 plus Norway) performed by Stark; and

(iii) the vertical relationships between mortars and several other specialty construction products manufactured by EBC (upstream) and the sale of building materials to professional and retail customers (downstream) in two EEA countries (Denmark and Norway) performed by Stark. Table 1 below summarises all these vertical links by category.

5.2. Framework of the competitive assessment of vertical links

(64) The Commission’s Guidelines on the assessment of non-horizontal mergers under the Merger Regulation (the "Non-Horizontal Merger Guidelines") distinguish between two main ways in which vertical mergers may significantly impede effective competition, namely input foreclosure and customer foreclosure.63

(65) For a merger to raise input foreclosure competition concerns, the merged entity must have a significant degree of market power upstream.64 In assessing the likelihood of an anticompetitive input foreclosure strategy, the Commission has to examine whether (i) the merged entity would have the ability to substantially foreclose access to inputs; (ii) whether it would have the incentive to do so; and (iii) whether a foreclosure strategy would have a significant detrimental effect on competition downstream.65

(66) For a merger to raise customer foreclosure competition concerns, the merged entity must be an important customer with a significant degree of market power in the downstream market.66 In assessing the likelihood of an anticompetitive customer foreclosure strategy, the Commission has to examine whether (i) the merged entity would have the ability to foreclose access to downstream markets by reducing its purchases from its upstream rivals; (ii) whether it would have the incentive to do so; and (iii) whether a foreclosure strategy would have a significant detrimental effect on consumers in the downstream market.67

5.3. Vertical relationships between polymer-based concrete admixtures (upstream) and the manufacture and sales of various building and insulation materials (downstream)

(67) BASF’s EB business, through its EBA business, manufactures chemical-based admixtures. Some of these products (as well as the ones manufactured by BASF’s EB business upstream competitors) are used in the manufacture of several building and insulation materials manufactured by Xella.

(68) This vertical link gives rise to markets that are affected upstream at national level in six EEA countries (Austria, Czech Republic, Denmark, Norway, Spain and Sweden) because BASF’s EB business’ market shares in the sale of chemical-based admixtures is above 30% in these countries, as well as markets that are affected downstream in 19 EEA countries68 for most products sold by Xella (AAC blocks, AAC large format units and mineral insulation boards, but not for mortars), because Xella’s market shares are above 30% for these products.69

(69) Table 2 below provides an overview of these vertical relationships. Countries where Xella has manufacturing plants for the manufacture of a given product are marked by an asterisk “*” at the end of the corresponding line. Market shares below the 30% threshold are marked with a “-“.

(70) In addition, as regards a potential sub-segmentation of AAC large format prefabricated compound units between AAC large format prefabricated compound units for industrial construction and AAC large format prefabricated compound units for residential construction, the Notifying Party has provided the following separate market shares estimates for these potential downstream markets.

5.3.1. Potential input foreclosure

5.3.1.1. The Notifying Party’s view

(71) First, as regards ability, the Notifying Party argues that chemical-based admixtures are not an important input for the manufacture of AAC products, mineral insulation boards and mortars, and also, that admixtures represent a negligible cost factor in the production of all these products. The Notifying Party explains (i) that the share of chemical-based admixtures in Xella’s total per plant production costs where it produces the above-listed downstream products ranges between [0-5]% and [0-5]% only, depending on the factory, (ii) that as a share of Xella’s total production costs per country, it is only about [0-5]% in Germany and around [0-5]% in France, and sinks further to below [0-5]% in terms of Xella’s overall production costs in Europe, (iii) that since Xella’s competitors use similar production processes and technologies, it can be inferred that similar proportions would also apply to Xella’s competitors and (iv) that even considering producers of mortars that are not Xella’s direct competitors,71 chemical-based admixtures only account for well below [0-5]% of the production costs of the respective down-stream products (namely AAC blocks, AAC large format units, mineral insulation boards and mortars).72

(72) The Notifying Party also claims that the cost of switching between different chemical-based admixtures suppliers is low, that there is a wide range of admixture producers besides BASF’s EB business across the EEA and that EBA products do not represent a significant source of product differentiation for the downstream market of Xella’s products and their competing products since Xella’s and its competitors’ customers have no knowledge of, or interest in, the particular supplier that Xella relies on for chemical-based admixtures used in its AAC blocks or other products.73

(73) Finally, the Notifying Party explains that overall the risk of potential input foreclosure strategies would be low, given that BASF’s EB business is only an important supplier of chemical-based admixtures to be used in AAC products for Xella. It explains that [70-80]% of BASF’s EB business’s sales of chemical-based admixtures to customers active in the manufacture of AAC products in the EEA today are already made to Xella. Apart from Xella, BASF’s EB business only supplies chemical-based concrete admixtures to only […] other purchasers in the AAC industry, with minimal purchases: [less than EUR 100,000 worth in each case]. Thus, potential input foreclosure would be limited to those […] customers, which with the exception of the […] customer are not located in countries, where the merged entity would hold a strong market position upstream.74

(74) Second, as regards incentive, the Notifying Party submits that any attempt to foreclose competitors of Xella would ultimately prove unprofitable, as Xella’s competitors can easily procure the chemical-based admixtures they need from alternative sources, without an appreciable (if any) effect on the production costs. As such, the combined entity would incur a decrease of its sales upstream without reaping any benefit from this strategy downstream.75(75) Third, as regards effects, the Notifying Party considers that given the lack of ability and incentive, any effects of such a potential input foreclosure would be purely hypothetical, in particular because of the existence of other chemical-based admixtures manufacturers across the EEA and Xella’s competitors’ ability to switch their procurements easily.76

5.3.1.2. The Commission’s assessment

(76) First, as regards ability, the Commission notes that in several of the vertically affected markets for chemical-based admixtures, input foreclosure appears rather unlikely based on the merged entity’s relatively modest market shares at the upstream level, namely in Czech Republic: [30-40]%; Norway [30-40]%, and Sweden [40-50]% (market shares by volume, 2019). In other national markets, the merged entity would hold a more important position on the upstream market, namely in Austria ([40-50]%), Denmark ([40-50]%) and Spain ([60-70]%) (market shares by volume, 2019).

(77) However, replies to the market investigation by chemical-based admixtures customers confirmed that post-transaction, there would remain a sufficient number of suppliers selling chemical-based admixtures including in the latter categories of countries (Austria, Denmark, and Spain), if BASF’s EB business stopped selling chemical-based admixtures to their company.77 This suggests that in none of the relevant national markets (Austria, Czechia, Denmark, Norway, Spain and Sweden), the combined entity would not have the ability to put in place an effective input foreclosure strategy, simply because foreclosed customers would be in a position to find readily available alternatives for their chemical-based admixtures procurement on the market.

(78) Second, as regards incentive, customers including those located in the six relevant countries listed in Austria, Czechia, Denmark, Norway, Spain and Sweden also confirmed that they did not expect that the combined entity would have an incentive to have BASF’s EB business stop selling chemical-based admixtures to their company.78

(79) Third, as regards effects, based on the elements provided by the Notifying Party, the Commission considers that chemical-based admixtures do not appear to represent an important cost factor in the manufacture of any of the relevant downstream products (namely AAC products, mineral insulation boards and mortars). Replies to the market investigation by customers for chemical-based admixtures overwhelmingly showed that chemical-based admixtures represent less than 1% of their total production costs for the manufacture of AAC blocks, AAC large format prefabricated compound units, mineral insulation boards, CSU, aerated concrete roofing panels, fire walls and outer walls and less than 5% of the production costs of mortars.79 As a result, the Commission considers that a potential input foreclosure of chemical-based admixtures in Austria, Czechia, Denmark, Norway, Spain and Sweden will likely not have any material impact, given that those admixtures only account for below 1% of the production costs of the respective down-stream products (namely AAC blocks, AAC large format units, mineral insulation boards and mortars),80 and any deterioration of the terms or prices offered by BASF’s EB business would therefore have a minimal impact on the overall price of the final products. This was also confirmed by the fact that the majority of respondents to the market investigation expected no impact as a result of the Transaction.81

5.3.2. Potential customer foreclosure

5.3.2.1. The Notifying Party’s view

(80) First, as regards ability, the Notifying Party argues that Xella is not an important customer for chemical-based admixtures in the EEA, since Xella (overall) represents [0-5]% of all purchases of chemical-based concrete admixture (from BASF’s EB business and its competitors) in Germany, [0-5]% in France, and well below [0-5]% in all other countries where it is active. As such, if the combined entity were to put in place a customer foreclosure strategy, BASF EB business’ competitors in the manufacture of chemical-based admixtures would still have a sufficiently large pool of customers to sell to.82

(81) Second, as regards incentive, the Notifying Party argues83 that since competitors of BASF’s EB business also have very low sales to Xella, a decision by Xella post- Transaction to divert its relevant chemical-based admixtures orders to the Target would not reduce the ability and incentive of the Target’s competitors to compete and therefore that Xella could not affect the Target’s upstream competitors by increasing their cost to access downstream customers or by restricting their access to a significant customer base.

(82) Third, as regards effects, the Notifying Party explains that given the very limited importance of Xella’s purchases, the volume of lost sales for the Target’s competitors in case of a potential customer foreclosure attempt would be de minimis and would not give rise to price increases in the upstream market.84

5.3.2.2. The Commission’s assessment

(83) First, as regards ability, the Commission notes that Xella has very high market shares (above 40%) at national level downstream in some countries, in particular, with respect to (i) AAC blocks in Austria, Belgium, Bulgaria, Croatia, Denmark, France, Germany, Hungary, Italy, the Netherlands, Norway, Slovakia, Slovenia, Spain and Sweden; (ii) AAC large prefabricated compound units in Austria, Belgium, Czech Republic, Denmark, France, Germany, Hungary, Netherlands, Norway, Poland, Slovakia, Slovenia and Sweden; and (iii) mineral insulation boards in Austria, Czech Republic, Denmark, Norway, Spain and Sweden (see Table 2 above). Despite these high market shares, it would appear unlikely that the merged entity would have the ability to engage in customer foreclosure to the detriment of other suppliers of chemical-based admixtures.

(84) Preliminarily, it should be noted that Xella only has manufacturing facilities in a subset of the countries where it sells construction material, namely in Austria, Belgium, Bulgaria, Czechia, France, Germany, Hungary, Italy, the Netherlands, Poland, Romania, Slovakia and Slovenia.85 In light of this and taking into account the national scope of the market for chemical-based admixtures, a potential customer foreclosure scenario resulting from Xella’s high market shares downstream at national level would be more likely to take place in countries with manufacturing facilities, rather than in those countries where it has no manufacturing facilities (in other words, if the potential customer foreclosure issue is considered at national level, thus in any country where Xella has no plant, there is as such no customer to foreclose). In particular, for mineral insulation boards, if the potential customer foreclosure issue is considered at national level, no customer foreclosure scenario would be possible with respect to chemical-based admixtures, since Xella does not purchase chemical-based admixtures in any of the 6 countries where it has a high market share (>30%) downstream86.

(85) In addition, the market investigation confirmed that chemical-based admixtures are used in a multitude of applications, such as the production of regular concrete above everything else,87 and that the types of products manufactured by Xella only represent a small share in those applications. As such, Xella therefore does not appear to be an important purchaser of chemical-based admixtures. The market investigation also revealed that BASF EB Business’ competitors in the manufacture of chemical-based admixtures would still have a sufficiently large pool of customers to sell to if Xella stopped purchasing polymer-based concrete admixtures from their company, where Xella has a high market share (>30%) downstream, that is for (i) AAC blocks in Austria, Belgium, Bulgaria, Croatia, Denmark, France, Germany, Hungary, Italy, the Netherlands, Norway, Romania, Slovakia, Slovenia, Spain and Sweden; (ii) AAC large format units in Austria, Belgium, Czechia, Denmark, Finland, France Germany, Hungary, the Netherlands, Norway, Poland, Slovakia, Slovenia and Sweden and (iii) for mineral insulation boards in Austria, Czechia, Denmark, Norway, Spain and Sweden. 88

(86) Second, as regards incentive, chemical-based admixtures manufacturers responding to the market investigation consider that post-Transaction, Xella would not have any incentive to stop purchasing polymer-based concrete admixtures from their company, where Xella has a high market share (>30%) downstream, that is for

(i) AAC blocks in Austria, Belgium, Bulgaria, Croatia, Denmark, France, Germany, Hungary, Italy, the Netherlands, Norway, Romania, Slovakia, Slovenia, Spain and Sweden; (ii) AAC large format units in Austria, Belgium, Czechia, Denmark, Finland, France Germany, Hungary, the Netherlands, Norway, Poland, Slovakia, Slovenia and Sweden and (iii) for mineral insulation boards in Austria, Czechia, Denmark, Norway, Spain and Sweden.89

(87) Third, as regards effects, the market investigation showed that chemical-based admixtures manufacturers consider that the Transaction would have no impact on the market for polymer-based concrete admixtures, where Xella has a high market share (>30%) downstream, that is for (i) AAC blocks in Austria, Belgium, Bulgaria, Croatia, Denmark, France, Germany, Hungary, Italy, the Netherlands, Norway, Romania, Slovakia, Slovenia, Spain and Sweden; (ii) AAC large format units in Austria, Belgium, Czechia, Denmark, Finland, France Germany, Hungary, the Netherlands, Norway, Poland, Slovakia, Slovenia and Sweden and (iii) for mineral insulation boards in.90

(88) In light of the above, the Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to the vertical link arising between chemical-based admixtures, in Austria, Czechia, Denmark, Norway, Spain and Sweden (upstream) and the manufacture and sales of various building and insulation materials, that is for (i) AAC blocks in Austria, Belgium, Bulgaria, Croatia, Denmark, France, Germany, Hungary, Italy, the Netherlands, Norway, Romania, Slovakia, Slovenia, Spain and Sweden; (ii) AAC large format units in Austria, Belgium, Czechia, Denmark, Finland, France Germany, Hungary, the Netherlands, Norway, Poland, Slovakia, Slovenia and Sweden and (iii) for mineral insulation boards in Austria, Czechia, Denmark, Norway, Spain and Sweden (downstream).

5.4. Vertical relationships between chemical-based admixtures (upstream) and the retail sales of building materials to professional and non-professional customers (downstream)

(89) BASF’s EB business, through its EBA business, manufactures chemical-based admixtures. Some of these products (as well as the ones manufactured by BASF’s EB business’ upstream competitors) are purchased and then resold by Stark to professional and retail customers.

(90) This vertical link gives rise to markets that are affected upstream at national level in three EEA countries (Denmark, Norway and Sweden) because BASF’s EB business’ market share in the sale of chemical-based admixtures is above 30% in these countries. It also gives rise to markets that are affected downstream at regional level in Denmark in the regions of Denmark capital and Central Jutland (where Stark has a [30-40]% market share in volume), in Norway in the regions Troms og Finnmark ([30-40]%) and Sogn og Fjordane ([50-60]%), and probably also in some regions of Finland (where Stark holds a [20-30]% market share at national level for the sales to professional customers, but was not able to provide a regional breakdown of its market share at sub-national level). The Notifying Party did not submit separate market share data for professional customers and non-professional customers at regional level.91 Table 4 below provides an overview of these vertical relationships.

5.4.1. Potential input foreclosure

5.4.1.1. The Notifying Party’s view

(91) First, as regards ability, the Notifying Party submits that Stark does not actively engage in the sale of chemical-based admixtures, and that these products are not generally sold through distributors of building materials. The Notifying Party further claims that Stark is not aware of sales of chemical-based admixtures by its competitors.92 As such, it would therefore appear that admixtures are not an important input for the distribution of building materials.

(92) Second, as regards incentive, the Notifying Party, again93 argues94 that since competitors of BASF’s EB business also have very low sales to Xella, a decision by Xella post-Transaction to divert its relevant chemical-based admixtures orders to the Target would not reduce the ability and incentive of the Target’s competitors to compete and therefore that Xella could not affect the Target’s upstream competitors by increasing their cost to access downstream customers or by restricting their access to a significant customer base.

(93) Third, as regards effects, the Notifying Party argues that such foreclosure strategy would likely lack of impact, given that chemical-based admixtures typically represent [0-5]% of the sales made by Stark as a distributor and [0-5]% of its procurements, and the Notifying Party submits that it can be inferred that the same ratio would apply to Stark’s competitors in the distribution of construction materials.95 Therefore, any attempt by the combined entity to cease supplying chemical-based admixtures to Stark’s downstream competitor, or degrade the terms or conditions of supply is not likely to have any meaningful impact on Stark’s competitors’ profitability on the downstream market.96

5.4.1.2. The Commission’s assessment

(94) First, as regards ability, the Commission observes that BASF EB business’ market shares upstream suggests that in all three countries (Denmark, Sweden and Norway), there are alternative suppliers of chemical-based admixtures, which jointly make up for a large share in the supply in all three countries ([50-60]% in Denmark; [60-70]% in Sweden and [60-70]% in Norway).

(95) Moreover, replies to the market investigation by chemical-based admixtures customers confirmed that post-transaction, admixture customers present in all three countries (Denmark, Sweden and Norway) and active in both the retail distribution of building materials to DIY customers and to professional customers consider that there would remain a sufficient number of suppliers selling chemical-based admixtures, if BASF’s EB business stopped selling chemical-based admixtures to their company.97 This would suggest that the combined entity would not have the ability to put in place an effective input foreclosure strategy, simply because foreclosed customers would be in a position to find readily available alternatives for their chemical-based admixtures procurement on the market.

(96) Second, as regards incentive, the Commission notes that it is questionable whether the merged entity’s downstream market position would allow it to recover customers for chemical-based admixtures through the Stark distribution outlets, given that the market position at the downstream level is only strong in very limited regions. Therefore, it is questionable that the merged entity would have an incentive in engaging in input foreclosure.

(97) The Commission’s market investigation confirmed that chemical-based admixtures customers present in all three countries (Denmark, Sweden and Norway) and active in both the retail distribution of building materials to DIY customers and to professional customers did not expect the combined entity to have an incentive to have BASF’s EB business stop selling chemical-based admixtures to their company.98

(98) Third, as regards effects, based on information provided by the Notifying Party, the Commission observes that such foreclosure strategy would likely lack of impact, given that chemical-based admixtures typically represent [0-5]% of the sales made by Stark as a distributor, and the Notifying Party submits that it can be inferred that the same ratio would apply to Stark’s competitors in the distribution of construction materials. Therefore, any attempt by the combined entity to cease supplying chemical-based admixtures to Stark’s downstream competitor, or degrade the terms or conditions of supply is not likely to have any meaningful impact on Stark’s competitors’ profitability on the downstream market.

(99) This was confirmed in the course of the Commission’s market investigation, which unambiguously showed that chemical-based admixtures represent less than 1% of distributors of building materials’ sales, both to professional customers and to DIY customers.99 As a result, the Commission considers that a potential input foreclosure of chemical-based admixtures will likely not have any material impact, since any deterioration of the terms or prices offered by BASF’s EB business would have a minimal impact on the amount of sales made by distributors of building materials. The market investigation also revealed that the majority of customers expected no impact as a result of the Transaction.100

5.4.2. Potential customer foreclosure

5.4.2.1. The Notifying Party’s view

(100) First, as regards ability, the Notifying Party submits that Stark’s purchases represents well below 30% of the total sales of chemical-based admixtures in the countries where it is active, and that Stark can therefore not be considered as an important customer for admixture manufacturers.101

(101) Second, as regards incentive, the Notifying Party claims that excluding the chemical-based admixtures products of the Target’s competitors from Stark’s outlets would generate hardly any additional EBA sales through Stark, as the distribution of EBA products does not generally take place through such outlets.102

(102) Third, as regards effects, the Notifying Party explains that given the very small amount of chemical-based admixtures purchased by Stark, foreclosing access to Stark as a purchaser of chemical-based admixtures would not have any effects on the upstream competitors of BASF’s EB business, nor would it have any meaningful impact on the competitive dynamics of the market in general.

5.4.2.2. The Commission’s assessment

(103) First, as regards ability, the Commission observes that given the national nature of the market for chemical-based admixtures, any upstream competitor of BASF’s EB business in the market for admixtures would be likely to be rather indifferent to whether Stark is stronger in the distribution of building products to professional or retail customers at sub-national level in some regions than others, because their main interest would be whether Stark is an important buyer of admixtures at national level overall. Consequently, Stark’s market share in the distribution of building products to professional or retail customers at national level, is a sufficient proxy in order to carry out the assessment of these vertical relationships. These market shares at national level are below the 30% threshold for a market to be considered as vertically affected for every country where Stark is present, it would appear that any customer foreclosure scenario is very unlikely, for lack of ability.

(104) Moreover, the Commission’s market investigation confirmed that that BASF EB Business’ competitors in the manufacture of chemical-based admixtures would still have a sufficiently large pool of customers to sell to if Stark stopped purchasing polymer-based concrete admixtures from their company, where Stark has a high market share (>30%) downstream, that is in Denmark, Norway and Sweden.103

(105) Second, as regards incentive, the Commission’s market investigation revealed that chemical-based admixtures manufacturers consider that post-Transaction, Stark would not have any incentive to stop purchasing polymer-based concrete admixtures from their company.104

(106) Third, as regards effects, based on information submitted by the Notifying Party, the Commission observes that such foreclosure strategy would likely lack of impact, given that Stark’s purchases of chemical-based admixtures are below 30% of the total sales of admixtures in the countries where it is active. Moreover, the market investigation confirmed that chemical-based admixtures’ manufacturers consider that the Transaction would have no impact on the market for polymer-based concrete admixtures.105

(107) In light of the above, the Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to the vertical link arising between chemical-based admixtures (upstream) and the distribution of building materials (downstream) to i) wholesale sales to retailers; (ii) retail sales to professional customers (B2B); and (iii) retail sales to non-professional customers (primarily through DIY stores) in Denmark, Norway and Sweden.

5.5. Vertical relationships between mortars and several other specialty construction products (upstream) and the retail sales of building materials to professional and non-professional customers (downstream)

(108) BASF’s EB business, through its EBC business, manufactures a variety of products such as mortars, concrete repair and protection systems, performance grouts, waterproofing systems, sealants, performance flooring systems, wall systems and coatings for mulch and wood fibres. It is however noted that mortars are the most important amongst them. Some of these products (as well as the ones manufactures by BASF’s EB business upstream competitors) are purchased and resold by Stark to professional and retail customers.

(109) BASF’s EB business’ market share do not give rise to affected markets upstream106. Given the Parties’ (through BASF’s EB business) small market shares in the upstream markets, and consequently the combined entity’s inability to foreclose access to the relevant products post-Transaction, input foreclosure will not be assessed in this decision.

(110) This vertical link gives rise to markets that are affected downstream at regional level in Denmark in the regions of Denmark capital and Central Jutland (where Stark holds a [30-40]% market share), in Norway in the regions Troms og Finnmark ([30- 40]%) and Sogn og Fjordane ([50-60]%), and probably also in some regions of Finland (where Stark holds a [20-30]% market share at national level for the sales to professional customers, but was not able to provide a regional breakdown of its market share). The Notifying Party did not submit separate market share data for professional customers and non-professional customers at regional level (see Footnote 91 above). Table 5 below provides an overview of these vertical relationships.

5.5.1. Potential customer foreclosure

5.5.1.1. The Notifying Party’s view

(111) First, as regards ability, the Notifying Party claims that in light of the national nature of the upstream markets for mortars, sealants, grouts and other products manufactured by EBC (“EBC products”), it would be not be appropriate to consider Stark’s market shares at a sub-national level. Given that Stark’s market share in every country where it is active remains below 30%, the Notifying Party submits that the combined entity would lack the ability to foreclose access to an important customer downstream.107 In addition, the Notifying Party explains that Stark is not an important customer for products manufactured by EBC, which is evidenced by the fact that (i) Stark’s purchase shares for all EBC products in all countries where it is active is below 30%,108 and (ii) [80-90]% of the total sales made by EBC in Denmark and [60-70]% in Norway were direct sales to customers (without the intermediary of a distributor).109 The Notifying Party further submits that BASF’s EB business’ competitors for EBC products follow similar commercial policies to those of BASF’s EB business and are comparably reliant on direct sales as opposed to sales to distributors.110 Therefore, Stark would not appear to be an important customer for EBC products.

(112) Second, as regards incentive, the Notifying Party submits that given the modest volumes of EBC products sold by Stark, any attempt by the combined entity to exclude sales by BASF EB business’ competitors would not generate an increase of sales in EBC products manufactured by BASF’s EB business that would be sufficient to outweigh the loss of sales of similar products manufactured by BASF’s EB business’ competitors. On the contrary, it would deteriorate Stark’s relationships with BASF’s EB business’ competitors, from whom Stark purchases a variety of products besides EBC products, which would in turn negatively affect the terms and conditions (e.g., discounts) offered by such suppliers to Stark for their whole range of products.111

(113) Third, as regards effects, the Notifying Party explains that given the modest volumes of EBC products sold by Stark and Stark’s modest purchase shares of EBC products in all countries where it is active, it cannot be considered that a sufficiently large fraction of upstream output is affected by the revenue decreases resulting from the Transaction, so that any attempt by the combined entity to put in place a customer foreclosure strategy would have no impact on the upstream market.112

5.5.1.2. The Commission’s assessment

(114) First, as regards ability, the Commission agrees that given the national nature of the upstream markets for mortars, sealants, grouts and other products manufactured by EBC, any upstream competitor of BASF’s EB business in the market for admixtures would be likely to be rather indifferent to whether Stark is stronger in the distribution of building products to professional or retail customers at sub-national level in some regions than others, because their main interest would be whether Stark is an important buyer of admixtures at national level overall. As a proxy for this in the first place, Stark’s market share in the distribution of building products to professional or retail customers at national level, appear to be sufficient for the purposes of the assessment of these vertical relationships. These market shares at national level being below the 30% threshold for a market to be considered as vertically affected for every country where Stark is present; it would appear that any customer foreclosure scenario is very unlikely, for lack of ability.

(115) Moreover, the Commission’s market investigation confirmed that BASF EB Business’ competitors in the manufacture of mortars, sealants and other EBC products would still have a sufficiently large pool of customers to sell all of their products to if Stark stopped purchasing mortars, sealants and other EBC products from their company.113

(116) Second, as regards incentive, the Commission’s market investigation confirmed that BASF EB Business’ competitors in the manufacture of mortars, sealants and other EBC products consider that post-Transaction, Stark would not have any incentive to stop purchasing mortars, sealants and other EBC products from their company.114

(117) Third, as regards effects, the Commission’s market investigation confirmed that BASF EB Business’ competitors in the manufacture of mortars, sealants and other EBC products consider that the Transaction would have no impact on the market for mortars, sealants and other EBC products.115

(118) In light of the above, the Commission considers that the Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to the vertical link arising between mortars and several other specialty construction products (upstream) and the distribution of building materials (downstream) toi) wholesale sales to retailers; (ii) retail sales to professional customers (B2B); and (iii) retail sales to non-professional customers (primarily through DIY stores) , Denmark, Norway and Sweden.

6. CONCLUSION

(119) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C 217, 1.7.2020, p. 18.

4 “E” is a BASF organisational code. “B” stands for “Bauchemie”.

5 “A” stands for “Admixtures”.

6 “C” stands for “Construction Systems”.

7 Turnover calculated in accordance with Article 5 of the Merger Regulation.

8 Since concrete admixtures are not used in the manufacture of CSUs, CSUs are not vertically linked to any products manufactured by BASF’s EB business. As a result, CSUs will not be discussed further in this Decision.

9 Xella does not produce and market mortar as a stand-alone product, but only as part of complete solutions involving its aerated concrete products. Moreover, these mortars are specially adapted to the needs of Xella’s AAC blocks, CSUs and mineral insulation boards, and sold at a higher price than the commoditised types of mortars, which account for the majority of mortars sales. See Form CO, paragraph 74.

10 M.9406 – Lone Star – Stark group / Saint-Gobain BDD; M.8733 – Lone Star/Stark; and M.8341 – Lone Star Fund/Xella International.

11 See Cases M.7498 – Compagnie de Saint Gobain/Sika and M.4177 - BASF/Degussa Construction Chemicals.

12 See Cases M.7498 – Compagnie de Saint Gobain/Sika, recital 104

13 Form CO, paragraph 125

14 Form CO, paragraph 127

15 See replies to question 8 of Q1 – Questionnaire to admixtures customers.

16 See replies to question 6 of Q2 – Questionnaire to admixtures competitors and to question 7, Q4 - Questionnaire to admixtures customers active in mortars and sealants.

17 See replies to question 9 of Q1 – Questionnaire to admixtures customers.

18 See replies to question 7 of Q2 – Questionnaire to admixtures competitors and to question 8 of Q4 - Questionnaire to admixtures customers active in mortars and sealants.

19 See Cases M.7498 – Compagnie de Saint Gobain/Sika and M.4177 - BASF/Degussa Construction Chemicals.

20 See replies to question 21a of Q1 – Questionnaire to admixtures customers.

21 See replies to question 8 of Q2 – Questionnaire to admixtures competitors.

22 See Cases M.9276 - Sika/Financière Dry Mix Solutions, M.7498 – Compagnie de Saint-Gobain/Sika, M.4898 – Compagnie de Saint-Gobain/Maxit and M.3572 – Cemex/RMC.

23 See Cases M.9276 - Sika/Financière Dry Mix Solutions, M.7498 – Compagnie de Saint-Gobain/Sika and M.4898 – Compagnie de Saint-Gobain/Maxit.

24 See Cases M.9276 - Sika/Financière Dry Mix Solutions, M.7498 – Compagnie de Saint-Gobain/Sika, M.7249 – CVC/Parexgroup and M.4898 – Compagnie de Saint-Gobain/Maxit.

25 See replies to questions 5-8 of Q3 – Questionnaire to mortars and sealants competitors and questions 9- 12 of Q4 - Questionnaire to admixtures customers active in mortars and sealants.

26 See Cases M.7249 – CVC/Parexgroup, M.4898 – Compagnie de Saint-Gobain/Maxit, M.4719 – Heidelberg Cement/Hanson and M.1779 – Anglo American/Tarmac.

27 See Cases M.9276 - Sika/Financière Dry Mix Solutions and M.7498 – Compagnie de Saint-Gobain/Sika.

28 Form CO, paragraph 73

29 See to replies to question 9 of Q3 - Questionnaire to admixtures competitors active in mortars and sealants and question 14 of Q4 - Questionnaire to admixtures customers active in mortars and sealants.

30 See Cases M.8341 – Lone Star Fund/Xella International; M.8733 – Lone Star/Stark and M.9406 – Lone Star – Stark group / Saint-Gobain BDD

31 See Cases M.8341 – Lone Star Fund/Xella International; M.8733 – Lone Star/Stark and M.9406 – Lone Star – Stark group / Saint-Gobain BDD

32 Form CO, paragraph 37

33 Form CO, paragraph 38

34 See replies to question 10 of Q1 – Questionnaire to admixtures customers.

35 See replies to question 10.1 of Q1 – Questionnaire to admixtures customers. Potential substitutes mentioned by respondents include “[…] Dense Concrete blocks, CSU, clay blocks and timber framed structures […]”; “[...] brick, sand-lime brick […]”; “[…] calcium silicate or clay bricks [...]”; “[…] clay bricks – ceramic, precast concrete elements, wood panels, etc […].”.

36 See replies to question 11 of Q1 – Questionnaire to admixtures customers.

37 See Cases M.8341 – Lone Star Fund/Xella International; M.8733 – Lone Star/Stark and M.9406 – Lone Star – Stark group / Saint-Gobain BDD

38 Form CO, paragraph 39

39 See replies to question 21 of Q1 – Questionnaire to admixtures customers.

40 Form CO, paragraphs 47 - 53

41 See replies to question 12 of Q1 – Questionnaire to admixtures customers.

42 See replies to question 12.1 of Q1 – Questionnaire to admixtures customers. Potential substitutes mentioned by respondents include AAC blocks, as well as prefabricated concrete or steel panels.

43 See replies to question 14 of Q1 – Questionnaire to admixtures customers.

44 See replies to question 13 of Q1 – Questionnaire to admixtures customers.

45 See replies to question 14 of Q1 – Questionnaire to admixtures customers.

46 Form CO, paragraphs 54 – 55

47 See replies to question 21 of Q1 – Questionnaire to admixtures customers.

48 Form CO, paragraph 59

49 See replies to question 12 of Q1 – Questionnaire to admixtures customers.

50 See replies to question 15.1 of Q1 – Questionnaire to admixtures customers. “Mineral wool insulation board can readily be replaced in many applications with various types of plastic foam insulation boards just as there are a number of other insulation products, like aerogel, cellulose, vacuum panels, natural products like straw etc that in some applications can replace mineral wool insulation boards”; “Maybe other materials are possible, if the architect or the costomer prefer other insulation products.” ; “There are mineral insulation boards that can be substitutable with”.

51 See replies to question 16 of Q1 – Questionnaire to admixtures customers.

52 Form CO, paragraph 60.

53 See replies to question 21 of Q1 – Questionnaire to admixtures customers.

54 See Cases M.9406 – Lone Star – Stark group / Saint-Gobain BDD; M.7910 – Kesko/Onninen; M.7703 – PontMeyer/DBS; M.3407 – Saint Gobain/Dahl and M.3142 – CVC/Danske Traelast.

55 Form CO, paragraph 101.

56 See replies to questions 19 and 20 of Q1 – Questionnaire to admixtures customers.

57 See Cases M.9406 – Lone Star – Stark group / Saint-Gobain BDD and M.7910 – Kesko/ Onninen.

58 Form CO, paragraph 103

59 See replies to question 21 of Q1 – Questionnaire to admixtures customers.

60 Austria, Belgium, Bulgaria, Croatia, Czech Republic, Denmark, Finland, France, Germany, Hungary, Italy, Netherlands, Poland, Romania, Slovakia, Slovenia, Spain and Sweden

61 Denmark, Finland and Sweden

62 Autoclaved aerated concrete.

63 OJ L 24, 29.1.2004, p. 1.

64 Non-horizontal Merger Guidelines, paragraph 35.

65 Non-horizontal Merger Guidelines, paragraph 32.

66 Non-horizontal Merger Guidelines, paragraph 61.

67 Non-horizontal Merger Guidelines, paragraph 59.

68 Austria, Belgium, Bulgaria, Croatia, Denmark, France, Germany, Hungary, Italy, Netherlands, Romania, Slovakia, Slovenia, Spain, Sweden and Norway for AAC blocks; Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Hungary, Netherlands, Poland, Slovakia, Slovenia, Sweden and Norway, for AAC large format units and Austria, Czech Republic, Denmark, Norway, Spain, Sweden and Norway for mineral insulation boards.

69 The Notifying Party did not provide market shares at sub-national level for AAC products. However, for the purposes of this case, when assessing the potential for customer foreclosure risks arising as a result of the vertical links between admixtures manufactured by EBA (upstream) and the manufacture and sales of AAC products (downstream), the Commission will analyse the downstream product market at national level. Even if the downstream products are considered at regional level and Xella constitutes the sole supplier in a particular region (which is already the case at national level in some countries, such as Slovenia for AAC large format prefabricated compound units), for the same reasons as at national level, the Transaction would not appear likely raise serious doubts as to its compatibility as a result of this vertical link (see assessment laid out in paragraphs (71) to (88)).

70 The Notifying Party confirmed that Xella’s market share downstream for mortars would remain below [20-30]% under any plausible product and geographic market definition.

71 Xella does not produce and market mortar as a stand-alone product, but only as part of complete solutions involving its aerated concrete products. Moreover, these mortars are specially adapted to the needs of Xella’s AAC blocks, CSUs and mineral insulation boards, and sold at a higher price than the commoditised types of mortars, which account for the majority of mortars sales. See form CO, paragraph 74.

72 Form CO, paragraphs 163 - 166

73 Additional submission by the Notifying Party dated 25.06.2020, paragraphs 9 and 10

74 Form CO, paragraphs 180 – 182

75 Additional submission by the Notifying Party dated 25.06.2020, paragraph 11

76 Additional submission by the Notifying Party dated 25.06.2020, paragraph 13

77 See replies to question 22 of Q1 – Questionnaire to admixtures customers as well as question 14 of Q4 – Questionnaire to admixture customers active in mortars and sealants. This was in particular the case from customers present in countries where BASF’s market shares in the sale of polymer-based concrete admixtures upstream is above 30%, namely Austria, Denmark and Spain, as well as Czech Republic, Norway and Sweden. Interestingly, with respect to AAC large format units, the Commission received responses from admixtures customers active in the production of AAC large formats units in Austria, Belgium, Czech Republic, Hungary, Slovakia, Slovenia and Sweden, suggesting that Xella’s market shares for AAC large format units in these countries might not be as high as [90-100]%. The Commission however did not receive any responses from AAC large format units manufacturers active in France, suggesting indeed that it might be possible that Xella holds a [90-100]% market shares for AAC large format units in this country.

78 See replies to question 23 of Q1 – Questionnaire to admixtures customers as well as question 15 of Q4 – Questionnaire to admixture customers active in mortars and sealants. This was in particular the case from customers present in countries where BASF’s market shares in the sale of polymer-based concrete admixtures upstream is above 30%, namely Austria, Denmark and Spain, as well as Czech Republic, Norway and Sweden.

79 See replies to question 3 of Q1 – Questionnaire to admixtures customers as well as question 3 of Q4 – Questionnaire to admixture customers active in mortars and sealants.

80 See also paragraph (71) above

81 See replies to question 24 of Q1 – Questionnaire to admixtures customers as well as question 16 of Q4 – Questionnaire to admixture customers active in mortars and sealants.

82 Form CO, paragraph 185

83 Additional submission by the Notifying Party dated 25.06.2020, paragraph 16

84 Additional submission by the Notifying Party dated 25.06.2020, paragraph 17

85 More precisely, for (i) AAC blocks in Austria, Belgium, Czechia (not affected downstream), France, Germany, Hungary, Italy, Netherlands, Poland (not affected downstream), Romania, Slovakia and Slovenia; (ii) AAC large format units in Austria, Belgium, Czechia, Germany, Netherlands and Poland;

(iii) for mineral insulation boards in Bulgaria and Germany (both countries not affected downstream); and

(iv) for mortars in Italy and the Netherlands (both countries not affected downstream).

86 Austria, Czechia, Denmark, Norway, Spain and Sweden.

87 See replies to question 2.1 of Q2 – Questionnaire to admixtures competitors. Admixtures manufacturers in particular that confirm that the vast majority of admixtures sales are made to ready mix concrete plants as well as final customers producing plain concrete and plain concrete elements.

88 See replies to question 9 of Q2 – Questionnaire to admixtures competitors “There is a sufficient number of potential customers in precast and ready mix industries in the market for all producers of admixtures”, “Xella and Stark produce very special types of materials, which have limited use/application in the building industry”, “There will be sufficient customers” .

89 See replies to question 10 of Q2 – Questionnaire to admixtures competitors “No customer has long term interest in keeping itself out of this highly evolving and technical market of the admixtures. Concentrating its purchases on one supplier for othe reasons than the best cost/efficiency ration would jeopardize any commercial effort to stay competitive in its final market”

90 See replies to question 11 of Q2 – Questionnaire to admixtures competitors.

91 The Notifying Party provided separate data for professional and non-professional customers for Stark at national level, as well as some rough estimates of Stark’s market shares in the sale of EBA and EBC products to professional, as well as non-professional customer, at regional level, in these five countries. However, these appear less informative than the ones provided in Table 4 since they are provided in the form of ranges (e.g. <30%) with upper bounds that are very similar to Stark’s overall market shares at regional level. Moreover, for the same reasons as mentioned above in Footnote 69, given the national nature of the market for admixtures, it appears relevant to the purposes of this case that the Commission carries its assessment of the downstream product market at national level when considering the potential for customer foreclosure risks arising as a result of the vertical links between admixtures manufactured by EBA (upstream) and the distribution of building materials (downstream).

92 Form CO, paragraph 110

93 See paragraph (81)

94 Additional submission by the Notifying Party dated 25.06.2020, paragraph 16

95 Form CO, paragraphs 196 – 197

96 Form CO, paragraphs 196 – 198

97 See replies to question 22 of Q1 – Questionnaire to admixtures customers.

98 See replies to question 23 of Q1 – Questionnaire to admixtures customers.

99 See replies to question 4 of Q1 – Questionnaire to admixtures customers.

100 See replies to question 24 of Q1 – Questionnaire to admixtures customers.

101 Form CO, Annex 12

102 Additional submission by the Notifying Party dated 25.06.2020, paragraph 26

103 See replies to question 9 of Q2 – Questionnaire to admixtures competitors

104 See replies to question 10 of Q2 – Questionnaire to admixtures competitors

105 See replies to question 11 of Q2 – Questionnaire to admixtures competitors.

106 On the basis of data provided by the Notifying Party.

107 Additional submission by the Notifying Party dated 25.06.2020, paragraph 30

108 See Annex 12 of Form CO

109 Additional submission by the Notifying Party dated 25.06.2020, paragraph 33. See also Annex 10 of the Form CO

110 Additional submission by the Notifying Party dated 25.06.2020, paragraph 34

111 Additional submission by the Notifying Party dated 25.06.2020, paragraphs 38 – 39

112 Additional submission by the Notifying Party dated 25.06.2020, paragraph 40

113 See replies to question 11 of Q3 – Questionnaire to mortars and sealants competitors

114 See replies to question 12 of Q3 – Questionnaire to mortars and sealants competitors

115 See replies to question 13 of Q3 – Questionnaire to mortars and sealants competitors