Commission, March 17, 2020, No M.9623

EUROPEAN COMMISSION

Judgment

AMG / SHELL / JV

Subject: Case M.9623 - AMG / Shell / JV

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 12 February 2020, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which AMG Advanced Metallurgical Group N.V. (“AMG”) and Shell Overseas Investments B.V. (“SOI”), a wholly owned subsidiary of Royal Dutch Shell plc (“Shell”), acquire within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation joint control of a newly created joint venture Shell & AMG Recycling B.V. (“S&AR”, or the “JV”, the Netherlands)3. Shell and AMG are designated hereinafter as the “Notifying Parties”.

1. THE PARTIES

(2) AMG is a global specialty metals and engineering group supplying products and solutions to the aviation, infrastructure, energy and chemical industries. AMG Critical Materials, one of AMG’s operating segments, provides recycling services for oil refineries in relation to the spent residue upgrading catalysts (“resid catalysts”) generated from crude oil processing.4 AMG is currently active in catalyst recycling only in North America and sells the metals extracted through the recycling process on worldwide trading markets.

(3) Shell is the parent company of a global group of energy and petrochemical companies with businesses including: (i) oil and gas exploration, production and marketing; (ii) manufacturing, marketing and shipping of oil products and chemicals; and (iii) renewable energy products. Via its wholly owned subsidiary Shell Catalyst & Technologies, Shell supplies fresh resid catalyst (“FRC”) to oil refineries as well as associated technology, technical advisory services and research and development expertise.

(4) The JV will be a greenfield entity with no pre-existing market presence that will offer recycling services to oil refiners that use resid catalysts. Pursuant to the joint venture agreement (“JVA”) of 7 October 2019, the JV will be active in:

(a) the sourcing, recycling and reclamation of SRCs outside North America. The JV will do this [details on the JV's business strategy] once the proposed concentration has completed. [Details on the JV's business strategy], it expects to construct a recycling plant using AMG’s technology and know- how in the Middle East, which will have the ability to serve [details on the JV's business strategy]; and

(b) the worldwide sale of extracted by-products from the catalysts recycling process.

2. THE OPERATION AND CONCENTRATION

(5) AMG and Shell, via SOI, agreed to the creation of the full-function JV by signing a JVA on 7 October 2019.5 Under the JVA, the JV will be supervised and managed by the Board of Directors. AMG and Shell will each be entitled to appoint [an equal number of] board directors. [Information relating to the JV's governance structure] . Therefore, the proposed concentration consists of an acquisition of joint control of the JV by Shell and AMG.

(6) The JV will have sufficient own staff6 and dedicated management, as well as financial resources for its operation and for the management of its portfolio and business interests. The JV will have an independent market presence. It will engage in advertising its recycling services to potential customers and developing commercial opportunities with such customers. [Details on the JV's business strategy] once the regulatory approval for construction has been obtained, the JV will start construction of the first of its future recycling facilities […]. The JV will negotiate and enter into contracts with both oil refiners for the recycling of SRCs and buyers of the extracted industrial metals and other by-products from the recycling process.7 […]. Finally, the JV is intended to operate on a lasting basis. Therefore, the JV is a full-function entity.

(7) Therefore, it can be concluded that the creation of a JV by Shell and AMG constitutes a concentration within the meaning of articles 3(1)(b) and 3(4) of Council Regulation (EC) No 139/2004 (“EUMR”).

3. EU DIMENSION

(8) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million [AMG […], Shell […]].8 Each of them has an EU- wide turnover in excess of EUR 250 million [AMG […], Shell […]], but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. RELEVANT MARKETS [MARKET DEFINITION]

(9) The concentration does not give rise to horizontally or vertically affected markets. There are no horizontal overlaps or vertical links between the activities of the JV and Shell. As regards the activities of AMG and the JV, there is no horizontal overlap between the activities of the JV (which will be active outside of North America) and AMG ([…]) in respect of recycling of SRCs as the market is narrower than worldwide (see paragraphs 50 to 54). Although both AMG and the JV will be active in the sale of by-products retrieved from their respective recycling processes, AMG’s and the JV’s combined market share will remain below 20% on any plausible market.9 The sale of extracted by-products will therefore not be further discussed in this Decision.

(10) However, Shell’s activities in the sale of FRCs can be considered as neighbouring activities to those of the JV (recycling of SRCs). Given Shell’s relatively strong position in the sale of FRCs, the Commission investigated whether conglomerate concerns could arise.

4.1. Market for the supply of FRCs

(11) FRCs are used to treat refinery residue, i.e. the “bottom of the barrel” heavy oil remaining after distillates have been removed from crude oil feedstock. By treating refinery residues with resid catalysts, refiners can “upgrade” the residue and convert it into lighter fuels, such as gasoline, diesel, or kerosene.10 In contrast to other types of catalysts, FRCs refers to a group of catalysts which (i) have “active sites” composed of nickel and molybdenum that promote the reactions; and (ii) are supported on a shaped “carrier” with a high surface area upon which the active sites are distributed. They are used specifically in a process called “hydroprocessing” (including fixed bed resid reactors and ebullated bed resid reactors).11

4.1.1. Product market definition

4.1.1.1. The Commission's decisional practice

(12) The Commission has not previously analysed the market for FRCs.

(13) In previous cases concerning other types of catalysts, the Commission has found that catalysts can be distinguished based on their specific application.12

4.1.1.2. The Notifying Parties’ view

(14) The Notifying Parties agree with the Commission’s practice to distinguish catalyst markets based on the specific application of the catalyst and submit that the relevant product market is the market for FRCs, with its specific application being hydroprocessing.13

(15) FRCs are bespoke products, their composition differing to suit the nature of the residue feedstock they are seeking to upgrade (light, heavy etc.) and the desired output (specific by-products). However, all FRCs suppliers would be able to adapt the FRCs they produce to customer needs, according to the Notifying Parties.14

(16) The Notifying Parties therefore argue that it is not necessary to look at potential sub-segments of FRCs as (i) the resid catalysts used in the two main types of refinery residue upgrading process reactors (“fixed bed” and “ebullated bed” reactors) are broadly similar15 and (ii) the recycling of SRCs does not differ depending on the manufacturer of the catalysts, refinery specifications, type of reactor etc..16

(17) Therefore, the Notifying Parties submit that the relevant product market is that of FRCs and that no further segmentation is justified.

4.1.1.3. The Commission’s assessment

(18) There are different catalytic and non-catalytic options to upgrade heavy crude oil residue. However, the results of the market investigation confirmed that these options should not be part of the same product market as the supply of FRCs. A large majority of respondents replied that at the point in time when refineries decide on the technology to upgrade heavy crude oil residue, catalytic and non- catalytic solutions are not considered interchangeable/substitutable,17 as “process, product slate and equipment are very different” and it “depends on how well it fits within the existing refinery and synergies in the industrial complex.”18 Further, there are different catalytic solutions which customers do not consider substitutable either.19 Once customers have adopted a certain technology to upgrade heavy crude oil residue, they cannot easily switch, neither between different catalytic solutions nor between catalytic and non-catalytic solutions.20

(19) Based on the replies to its market investigation, the Commission considers that the product market definition should not be broader than FRCs.

(20) As for a potential sub-segmentation, the majority of respondents to the market investigation consider that no distinction is required between FRCs for fixed bed and ebullated bed technologies. Both of these technologies are used in the EEA (about half of the refineries that participated in the market investigation use one or the other, some use both).21 Whilst from a demand-side perspective, each refinery customer requires a FRCs that fits the technology and type of oil it uses (and as such, requires a bespoke solution), supply side substitutability is high: a majority of both competitors and customers confirmed that most competitors of FRCs are able to supply FRCs for refineries using any type of residue upgrading process reactor, i.e. “fixed bed”, “ebullated bed” or any other technology.22

(21) Based on its market investigation, the Commission therefore considers that the relevant product market for the purposes of this case is that of the supply of FRCs. No further sub-segmentation is necessary for the purposes of this case.

4.1.2. Geographic market definition

(22) As explained in recital (12), the Commission has not previously analysed a market for FRCs.

4.1.2.1. The Notifying Parties’ view

(23) According to the Notifying Parties, the geographic market is worldwide, as suppliers of FRCs operate globally. Plant proximity to the customer location is a relevant consideration but not the determining factor. Rather, the decision will be based on […].23 All suppliers of FRCs (Axens, Sinopec, Nippon Ketjen and Albemarle) are active in the EEA, in the sense that they are often invited to participate in tenders.24

(24) Transport costs only make up 2-3% of the total supply price, so FRCs suppliers can profitably supply customers around the world.25 Prices do not differ between regions, but are negotiated individually with customers (notably, as FRCs are bespoke products).26

4.1.2.2. The Commission’s assessment

(25) The results of the market investigation pointed towards a worldwide market for FRCs.

(26) All suppliers of FRCs and a clear majority of customers consider that the market for the supply of FRCs is global, as all operators are active at a global level, “trade flows are worldwide” and there are “no specific barriers at this moment”.27

(27) Suppliers of FRCs explained that customers are still supplied from the closest facility where the FRC is produced as long as that facility has sufficient capacity.28

(28) The Commission notes that in […] Shell itself supplied FRCs to the EEA [details in respect of supply]29 .

(29) That being said, the overview of all refineries worldwide purchasing FRCs shows that different suppliers are more present in certain parts of the world than others, suggesting that if there is a choice at closer proximity, this supplier may have an advantage. For instance, some suppliers of FRCs are only supplying refineries in Asia Pacific, in North America, Europe or the Middle East.30

(30) In any case, the exact geographic market definition can be left open between the EEA and worldwide, as the proposed concentration will not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement on either of the two plausible geographic market definitions.

4.2. Market for the recycling of SRCs

(31) After FRCs are used to upgrade oil residue, they become “spent” and cannot be used a second time. This waste product can be either landfilled or recycled by first roasting it and then melting the roasted catalyst in a primary and a secondary furnace. In these different steps, by-products can be recovered and resold on the market, namely: ferronickel molybdenum, calcium sulphate, calcium aluminate and vanadium.31

4.2.1. Product market definition

4.2.1.1. The Commission's decisional practice

(32) The Commission has not previously analysed the market for recycling of SRCs.

4.2.1.2. The Notifying Parties’ view

(33) The Notifying Parties argue that the service of SRCs recycling should not be further segmented between (i) different stages of the refining process, (ii) on the basis of recovered materials and the technology of the recycling process or (iii) between different types of SRCs.32

(34) The different stages of the recycling process are the collection of SRCs, the roasting and melting in a primary and a secondary furnace and the extraction of various by-products during this process. The Notifying Parties argue that a segmentation is not necessary as, from the perspective of customers, the individual procedural steps are not relevant for the selection of a recycling service provider.33

(35) While the type and amount of materials that can be reclaimed through SRCs recycling can vary, a further segmentation on the basis of recovered materials is not necessary. What and how much can be reclaimed impacts the commercial conditions under which the recycling service is provided, but the recycling process will remain the same.34

(36) The Notifying Parties also consider that there are no differences between the recycling of different types of SRCs. Considering other recycling providers already active in the market ([…]), these do not differentiate their price for recycling services on the basis of catalyst type.35 So, there is no reason for a split on the basis of the fresh resid manufacturer, the refinery specifications or the type of reactor from which the SRC originated.36

(37) The Notifying Parties conclude that the relevant market should be the market for SRCs recycling including all stages of the recycling process. The Notifying Parties however submit that the precise product market definition can be left open.37

4.2.1.3. The Commission’s assessment

(38) Based on its market investigation, the Commission considers that for the purposes of this case, the relevant market is that of recycling of SRCs.

(39) As regards the different stages of recycling, replies to the Commission’s market investigation showed that recyclers are integrated to different extents. In respect of collection, according to the Notifying Parties, transportation of the SRCs is typically a responsibility of the refineries (although there can be specific instances where a recycler may agree with a refiner to take responsibility over the logistics). This seems to be supported by the market investigation.38 In any event, transportation is carried out by a (specialised) freight handler for the physical transportation of the SRC to the facilities of the SRC recycling services provider, since refineries (or recyclers) generally do not own specialised bins or rail cars for such transportation. As regards the stages of roasting, melting and by-product extraction, whilst the major competitors active in the recycling of SRCs are active across the value chain, there are some market participants who only offer roasting.39 AMG is […] active in the full value chain […]. The JV is intended [details concerning the JV’s services]. For the purposes of this Decision, the Commission therefore considers that it is not necessary to sub-segment the relevant market by different stages of recycling.

(40) As regards a sub-segmentation based on recovered materials and the technology used in the recycling process, this does not appear warranted. In order to recycle SRCs, there are different technologies that fulfil the function to dispose of non- hazardous waste and recover metals, in particular pyro-40 and hydrometallical41 processes are used. There were some indications in the market investigation that some technologies are better for extracting certain types of metals than others (e.g. where the vanadium content is high, a different technology is preferable than where the platinum content is high in order to recover as much of these metals as possible)42, but in general, the respondents to the market investigation considered that generally their customers would not focus on the technology used by the recycler.43 In general, respondents indicated other factors determining whether recyclers could serve their refinery (e.g. proximity).44

(41) The type and amount of materials that can be reclaimed through SRC recycling can also vary between customers as products are bespoke and will normally impact the commercial conditions under which the recycling services are offered ([…] is one of the elements that determines the overall pricing of the recycling service). In addition, fluctuating metal prices determine the relative importance of reclaiming specific by-products, so the commercial needs of customers vary in terms of the recycling process. All suppliers of recycling services seem to be able to recycle SRCs with differing metal contents (albeit some are better and/or more focused than others with specific resid catalysts/types of metals).45

(42) As regards the recycling of different types of SRCs, respondents to the market investigation were largely of the view that a segmentation based on the type of SRC to be recycled is not warranted. Recyclers offer recycling services for SRCs to a refinery using any type of residue upgrading process reactor i.e. “fixed bed” and “ebullated bed”46. So a distinction between different sources of the SRC is not required.

(43) For the purpose of this Decision, the Commission considers the relevant market to be that of recycling of SRCs without any further sub-segmentation.

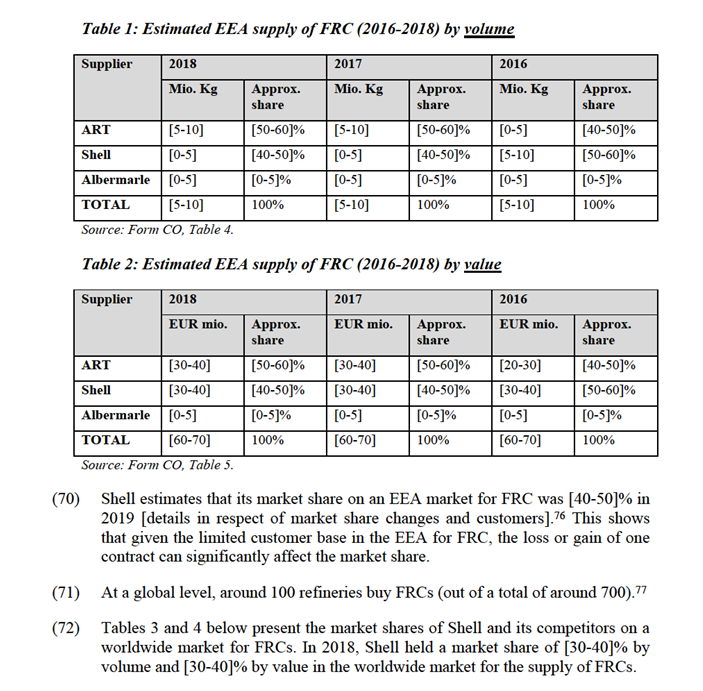

4.2.2. Geographic market definition

4.2.2.1. The Commission’s decisional practice

(44) As explained in paragraph (32), the Commission has not previously analysed a market for the recycling of SRCs.

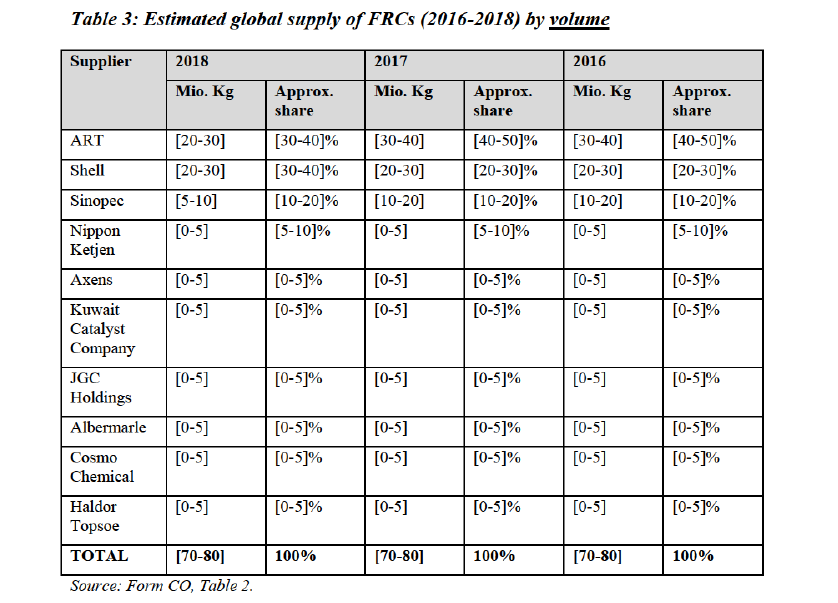

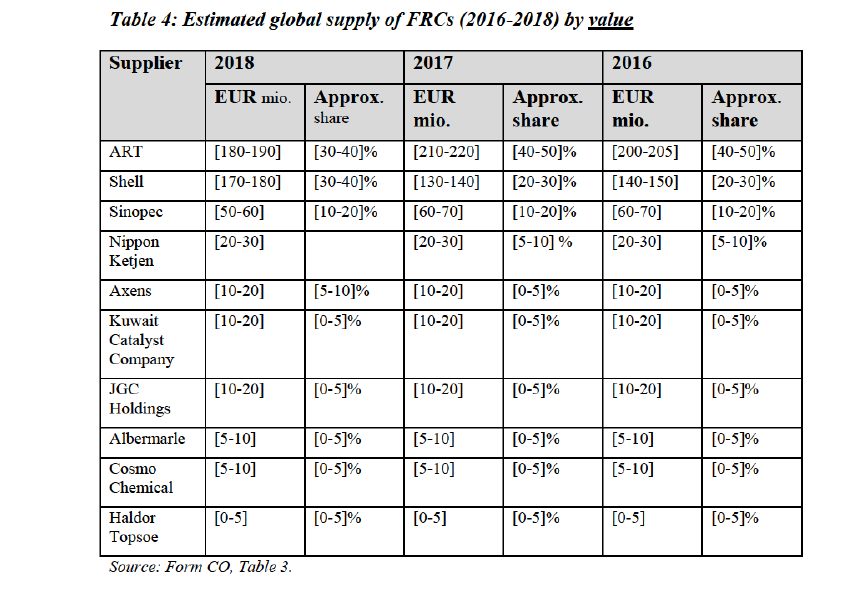

4.2.2.2. The Notifying Parties’ view

(45) According to the Notifying Parties, the geographic market for SRCs is EEA-wide, potentially including the Middle East and Asia as (i) transport costs for SRCs are significant, limiting the profitability of transporting the waste product from a refinery to a recycling facility, and (ii) as spent catalysts are toxic/hazardous, the related regulatory costs mean that recyclers in a different region are at a competitive disadvantage.47

(46) Given its hazardous nature and the relevant regulatory restrictions (as further discussed in paragraph (51)), SRC cannot be easily transported due to the cost involved.48 While regulatory hurdles can be overcome, in most circumstances spent catalysts are processed at regional level only, often in the vicinity of “clusters” of refineries, based on prevailing commercial conditions.49

(47) In addition, based on AMG’s experience [details on AMG's business strategy], transportation can account for up [details on AMG's business strategy].50

(48) The Notifying Parties therefore consider that, from the supply perspective, companies active in the SRC recycling business broadly operate on a regional, rather than a global, basis.51

(49) Therefore, the Notifying Parties submit that the geographic market is likely EEA- wide, potentially including the Middle East and Asia, but that the exact market definition can be left open between EEA-wide and worldwide.52

4.2.2.3. The Commission’s assessment

(50) The replies to the market investigation indicate that the relevant geographic market is likely to be EEA-wide or possibly EMEA (Europe, Middle East and Asia).53

(51) A majority of respondents confirmed that the distance between recyclers and refineries played an important role for the choice of recycler: “It is a benefit if the service provider is close by and long distance shipments can be avoided”, because of transport costs and regulatory constraints, namely:

· “European regulations on hazardous wastes;

· National regulations on hazardous wastes that can be even more constraining than EU regulations, such as the one implemented […];54

· Where these regulations do not apply (e.g. in Switzerland, even if that country is unrelated to [the refinery]’s activities in […]), the Basel Convention is relevant;

· Transportation costs and logistics (transportation by trucks); and CO2 emissions.”55

(52) Consideration about greenhouse gas emissions are an additional reason for refineries to prefer recyclers located at shorter distance.56

(53) All competitors for recycling services considered the closeness of their customers’ plants and the facility where the spent resid catalyst is recycled somewhat or very important.57 Some refineries replied to the market investigation that they have procured recycling services from recycling plants that are located on average at a distance of around 1000-1500km and not more than 2500km from the refinery. Also this points to an EEA-wide market rather than one including the Middle East and Asia or a worldwide market.58 While shipments of SRCs do sometimes take place over longer distances depending on the amount of metals involved and the metal price, this appears rather exceptional.59

(54) Based on its market investigation, the Commission therefore considers that for the purpose of this Decision the relevant geographic market can be EEA-wide or EMEA-wide. The exact geographic market definition can be left open, as the proposed concentration will not give rise to serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement on either of the two plausible geographic market definitions.

5. COMPETITIVE ASSESSMENT

(55) The proposed concentration does not give rise to horizontally affected markets, neither actually nor potentially.

(56) Nor does the proposed concentration give rise to actual or potential vertically affected markets. Shell currently has [details in respect of Shell’s group activities] and that is [details in respect of the JV’s operations].

(57) However, as the customers who purchase FRCs (a market where Shell has a market share of [40-50]% in the EEA) increasingly also purchase recycling services for the SRCs, this Decision analyses the effects of the proposed concentration on these potentially neighbouring markets.

5.1. Conglomerate non-coordinated effects

5.1.1. Legal framework

(58) According to the Non-Horizontal Merger Guidelines, conglomerate mergers do not lead to any competition problems under most circumstances.60 However, foreclosure effects may arise where the merged entity offers a combination of products in related markets and has the ability and incentive to leverage a strong market position from one market to another closely related market through tying, bundling or other exclusionary practices.61

(59) Tying refers to situations where customers that purchase one good (the tying good) are required also to purchase another good from the producer (the tied good). Tying can take place on a technical or contractual basis.62

(60) Bundling can take the form of pure bundling, which is similar to contractual tying, or mixed bundling. Mixed bundling refers to situations where the products are also available separately, but the sum of the stand-alone prices is higher than the bundled prices.63 Tying and bundling as such are common practices that often have no anticompetitive consequences. Nevertheless, in certain circumstances, these practices may lead to a reduction in actual or potential rivals’ ability or incentive to compete. Foreclosure may also take more subtle forms, such as the degradation of the quality of the standalone product.64 It may reduce the competitive pressure on the merged entity allowing it to increase prices.65

(61) Foreclosure can be a potential concern, if (i) there is a large common pool of customers, which is more likely when products are complementary;66 (ii) at least one of the merging parties’ products is viewed by many customers as particularly important and there are few relevant alternatives for that product;67 and (iii) the merged entity must have a significant degree of market power, but not necessarily dominance, in one of the markets concerned.68

(62) The incentive to foreclose rivals through bundling or tying depends on the degree to which this strategy is profitable.69 For instance, it is unlikely that the merged entity would be willing to forego sales on one highly profitable market in order to gain market shares on another market where turnover is relatively small and profits are modest.70 The Commission will also take into account the ownership structure of the merged entity, type of strategies adopted on the market in the past or the content of internal strategic documents such as business plans.71

(63) Finally, it is only when a sufficiently large fraction of market output is affected by foreclosure resulting from the concentration that the concentration may significantly impede effective competition. If there remain effective single- product players in either market, competition is unlikely to deteriorate following a conglomerate concentration.72 The effect on competition needs to be assessed in light of countervailing factors such as the presence of countervailing buyer power, the likelihood that entry would maintain effective competition in the closely related markets concerned, or indeed the ability of single-product competitors to combine their offers.73

5.1.2. Leveraging Shell’s position in FRC into the recycling of SRC

5.1.2.1. Potential concern

(64) Shell is active in the market for the supply of FRCs, whereas the JV will be active in the market for the recycling of spent catalysts. These two products/services are in principle purchased by the same customers, namely by refineries.

(65) Two competitors active in the recycling of SRCs in the EEA expressed some concerns that refineries would opt for a bundled offer and lose the flexibility to select the most appropriate FRC supplier and/or the most appropriate recycler, and that the large companies AMG and Shell will crowd out smaller family owned recycling businesses.74

(66) The Commission has assessed a potential competition concern whereby Shell would leverage its relatively strong position in the market for the supply of FRCs into the market for the recycling of SRC where the JV will be active and thereby foreclose recycling competitors, causing harm to consumers.

(67) The Commission has assessed in particular the ability and the incentive of Shell engaging in the following tying/bundling practices, together with the JV:

· Technical tying: differentiating the degree of technical compatibility between FRC and recycling of SRC;

· Contractual tying/pure bundling: imposing the purchase of recycling services for SRC by the JV on Shell’s customers of FRC; and/or

· Mixed bundling: incentivising the joint purchase of FRC by Shell and recycling services of SRC by the JV by offering higher prices for mix-and- match solutions involving only one of the products as compared to the bundle.

5.1.2.2. Shell’s position in the sale of FRCs

(68) At the outset, the Commission notes that in the EEA, only seven refineries out of around 90 currently use FRCs (and as such, are potential customers for SRC recycling services). Shell is currently the […] supplier of FRCs to […] refineries. In addition, […]. However, […] as of 2020.75

(69) Tables 1 and 2 below present the market shares of Shell and its competitors on an EEA-wide market for FRC. In 2018, Shell held a market share of [40-50]% both by volume and by value in the market for the supply of FRC.

(73) Shell estimates that its market share on the global market for FRCs was at [30- 40]% in 2019 and will [details in respect of market share changes] in 2020 (volume) based on Shell’s actual sales for 2019, forecast sales for 2020, and Shell’s internal best estimates for total demand.78

5.1.2.3. Notifying Parties’ view

(74) The Notifying Parties argue that Shell will not have the ability and incentive to leverage its potentially strong position in the market for FRC into the market for recycling of SRC where the JV will be active. In any event, the Notifying Parties submit that any putative leverage could not lead to anticompetitive foreclosure of Shell’s or the JV’s competitors. The reasons are the following.

(A) As regards ability

(75) The Notifying Parties argue that Shell will not have the ability to leverage its market position in the market for FRC, because it lacks market power.

(76) First, the market shares of Shell are not indicative of sustained market power as they are prone to rapid change when refineries re-tender supply which occurs every 1-3 years. Moreover, currently only seven refineries in the EEA purchase FRC.79

(77) Second, Shell faces strong competition both at global and EEA level, notably from market leader ART (with [30-40]% at global level and [50-60]% in the EEA), as well as Sinopec, Nippon Ketjen and Axens. Although at present Axens, Sinopec and Nippon Ketjen do not have contracts in the EEA, they are often invited to participate in tenders. Generally, all suppliers of FRC operate globally, and could potentially become active in the EEA.80

(78) Third, the Notifying Parties argue that the rising demand for FRC will attract new entrants while existing suppliers are likely and able to increase capacity.81 For customers, there are no barriers to switching as contracts are relatively short (e.g. annual basis).82

(79) Fourth, technical tying is not a possibility as there are no specific characteristics that could create a technical dependence or otherwise require compatibility between Shell’s supply of fresh resid and the JV recycling business (or vice versa)83.84

(80) Fifth, contractual tying will not take place, as Shell will continue to have refinery customers who are free to use other recycling providers (e.g. better geographically located), Shell and the JV will operate at arm’s length, and as Shell and the JV will be accountable to their own shareholders they will not sacrifice potential margin or opportunity to support the other (unless collectively the most attractive competitive proposition).85

(81) Sixth, refinery customers enjoy a wide choice of other recycling services suppliers – with at least five providers active in the EEA. Moreover, as ten providers of recycling services are active globally, refinery customers could also seek interest from alternative suppliers. AMG (and the JV) have no current EEA presence. Refineries also have an interest in maintaining a choice of suppliers and may multi-source SRC recycling services.86

(82) Seventh, refineries are large and sophisticated customers who carry out procurement processes to secure optimal supply options, both in respect of fresh resid supply and spent resid recycling services. 87

(83) Eight, the competitive dynamics in FRC supply and SRC recycling differ, with a local presence far more significant in the choice of recycling provider given the transportation challenges involved.88

(B) As regards incentives

(84) According to the Notifying Parties, Shell does not have the incentive to engage in a bundling strategy of the two products it offers to refineries.

(85) First, the value of fresh catalyst contracts is significantly larger than that for recycling services. In 2018, the value of the overall fresh resid supply sales worldwide represented an estimated [550 – 600] million EUR compared to the market for recycling of SRC worth approximately [150 – 200] million EUR.89

(86) The Notifying Parties further argue that [information about the Parties' profit margins] stable margins are found in the business of supplying FRC to refineries, as compared with the supply of spent catalyst recycling services ([information about the Parties' profit margins]).

(87) Shell’s net sales of FRC in 2018 were EUR […] (2019 EUR […]) with a gross profit of EUR […] (2019 EUR […]). The gross margin amounted to […]% (2019 […]%). For 2020 Shell expects the net sales to go [details in respect of Shell’s sales, customers and margins]. Based on AMG’s SRC recycling activities […], in 2018 revenues were EUR […], with gross profits of EUR […] and a gross profit margin of […]. The Parties emphasize that the result was driven by […] and submitted that for 2019 […]. If taken over a two-year period (2018 – 2019), AMG's gross profit margin of below […].

(88) Therefore, according to the Notifying Parties, the JV's future business model ([details of the JV’s business model]) means Shell will have no incentive to put at risk a business yielding consistent gross profits and margins to pursue a bundling strategy outside of North America through the JV.90

(89) Second, in many cases, the JV would not be an attractive solution for Shell’s FRC customers, either because they do not recycle or because the transport to the location of the recycling facilities of the JV makes recycling too expensive. Thus Shell will be careful not to lose customers who are not interested in recycling services, or who do not consider the JV an attractive solution given its geographic location.91

(90) Third, refineries often purchase recycling services from more than one company, in particular if they generate large amounts of SRC, to manage any supply side risks.92

(91) Fourth, as explained in paragraph (78), switching costs for fresh catalyst are low, so Shell would risk losing contracts if it tried to leverage its market position and force refinery customers to acquire recycling services from the JV. Barriers to switching are also low for recycling services of SRC,93 so refineries could react timely to any attempts to bundle.

(92) Fifth, Shell’s competitors have the ability to increase production of FRC to react to changes in demand, by reallocating existing production capacity from other catalyst types to resid catalyst, as well as by adding additional capacity.94

(93) Sixth, as for the JV’s competitors in the EEA market for recycling of SRC, the Parties estimate that Treibacher is the market leader in the EEA with 50-70% market share, followed by Moxba (20-30%) and Eramet, Nickelhuette and Aura Technologie. Transport costs mean that recyclers located close to refineries have a stronger position.95

(94) Therefore, refinery customers will remain free to choose to use other FRC providers as well as recycling providers, while Shell and the JV will each operate to maximise their own financial performance and will therefore not sacrifice potential margin or opportunity to support the other.

(C) As regards effects

(95) According to the Notifying Parties, it should also be noted that not all refineries that purchase FRC also choose to recycle the spent catalyst after use. An estimated [20-30]% of SRC is disposed of in landfills, particularly in the Middle East.96 This is due to the current recycling capacity constraints in the industry.

(96) The Notifying Parties argue that the JV’s entry into the market for recycling services will enhance competition because it will add capacity to the market of recycling services for SRC and provide an alternative to landfill. The JV will also provide an alternative choice and increase availability of metal by-products which would otherwise be lost if they were landfilled.97

5.1.2.4. The Commission’s assessment

(A) Ability

(97) The Commission considers that Shell and the JV will not have the ability to engage in tying or bundling for the following reasons.

(98) First, despite Shell’s relatively strong market position in 2018 ([40-50]% in the EEA and [30-40]% worldwide), Shell does not have a significant degree of market power.

(99) In the EEA in particular, its market shares […]. There are currently only seven refineries in the EEA using hydroprocessing and Shell’s market share can decrease rapidly. In 2019, Shell […].98

(100) The lack of market power is also supported by the replies to the market investigation where respondents indicated that (i) it is easy to switch suppliers; (ii) a choice of suppliers exists; and (iii) competitors are expected to expand and increase capacity.

(101) Buyers of FRC are able to switch and do so regularly. A majority of customers that responded to the market investigation procure FRC by tender.99 Tenders for procuring FRC are concluded for different durations, ranging from one to five years.100 Around half of the buyers of FRC have switched supplier in the last five years.101 One other respondent to the market investigation observed that switching of FRC provider had not taken place, as they never faced problems.102 In consequence, there are no obstacles for customers to choose and change their supplier of FRC on a regular basis.

(102) In terms of choice of suppliers of FRC, respondents to the market investigation indicated that several alternative suppliers compete in the supply of FRC both at EEA-wide and worldwide level.103 Whereas customers identified ART and Shell as those most active in the EEA, one competitor also named the following companies as competitors: Albemarle, Axens, JGC Holdings and Haldor Topsoe on a worldwide basis.104 Other players active on a worldwide market are for instance Sinopec, Nippon Ketjen, Kuwait Catalyst Company (KCC), Cosmo Chemical.105

(103) Finally, a clear majority of refineries expects the market for FRC to grow, with increasing demand from new hydroprocessing units all over the world. Competitors do not see capacity constraints in the market for FRC. In particular, several respondents noted that “there is plant capacity available in the Middle East.” In addition to existing production capacity that is not yet fully used, one respondent noted that “New resid capacity is coming online in 2020 that will address additional demand.”106 One customer also expects the entry of “one or two new players in the market in 10 years” for both economic and regulatory reasons107

(104) Second, technical tying is very unlikely. None of the respondents to the market investigation mentioned technical tying as a possibility. One respondent to the market investigation noted with regard to the supply of fresh catalysts and recycling services for SRCs that “from a technical perspective, the two activities have nothing in common: they follow two different processing steps and there would be no possibility for the JV to technically link the two activities”.108

(105) Third, contractual tying/bundling or mixed bundling is unlikely because in the first place, refineries’ choice of the supplier of FRC is not subject to offering recycling services but largely based on the performance of the catalyst. None of the respondents to the market investigation would refuse to consider a supplier for FRCs that does not offer recycling services.109 As one potential customer stated “FRCs, as any other catalysts, are a specialty materials that are selected based on performance/price ratio. Other factors are not so determining.”110 The offering of recycling service may be a nice add on, but will not determine the outcome of selecting the FRC provider.111

(106) Where the offers for FRC differed, it would be easy to switch to a different supplier.112 When assessing a bundled offer including recycling, customers would carefully consider “[t]he whole picture […] the amount of discount reasonable and favourable, where is the recycling facility located, the amount of paperwork (different regulations) needed, etc.”113

(107) The refineries that responded to the market investigation overall underlined that the supply of FRC is relatively more important than recycling services for the choice of a FRC supplier.114 Even if some respondents considered that offering a recycling service may give an advantage, act as a differentiator for refiners who need a “cradle to grave” catalyst solution, or indeed provide efficiencies for customers,115 the majority of customers buying FRCs clearly considered that they would procure FRCs from suppliers who do not offer recycling services. Only in a case where all FRC suppliers participating in a tender could provide the same quality and margins, could an offer for recycling services potentially make a difference.116

(108) In the second place, refineries are sophisticated buyers that typically use tenders, both for the procurement of FRC and for the procurement of recycling services for SRC.117 These buyers have in the past been selecting and changing suppliers of FRC in tender procedures. They have also experience in selecting suppliers of recycling services. They will choose those suppliers for each service that provide the best performance and margins for the refinery.

(109) In the third place, even if refineries procure both the supply of FRC and recycling services of SRC, all buyers of FRC that responded to the market investigation stated that they procure recycling services for SRC separately from the procurement of FRC.118 The duration of the contracts for respectively the supply of FRC and the recycling of FRC can differ (see paragraph (101) and footnote 117). This difference in timing negatively impacts on the possibility of tying/bundling.

(110) Finally, as explained in paragraph 103 of the non-horizontal merger guidelines, ability to foreclose is unlikely to exist if counterstrategies by rivals exist. One example cited is when single-product companies combine their offers so as to make them more attractive to customers. In this context, the Commission notes that, while the driver of FRC demand remains technical performance, there is demand for bundling on the market. Respondents to the market investigation confirmed that refineries have been asking their suppliers of fresh catalyst to also supply recycling services for the spent catalyst. As a competitor stated, “[t]here is a high demand in the industry to offer closed loop services and to keep the valuable metals involved in a circle. This is protecting the environment and reduces the mining activities for metals.”119

(111) In consequence, some of Shell’s competitors offer to put their customers in contact with providers of recycling services, where requested by customers. Market leader ART stated: “We primarily sell FRCs. However, we have business arrangements with metals reclaiming companies.”120As such, counterstrategies between competing FRC suppliers and SRC recyclers already exist.

(112) Therefore, the Commission considers that the JV will not have the ability to engage in foreclosure through tying or bundling.

(B) Incentives

(113) The Commission considers that even if there were to exist an ability to foreclose through tying or bundling, Shell and the JV have no incentives to do so for the following reasons.

(114) First, the margins […] on the sale of FRC are [details concerning Shell’s and AMG's margins], based on AMG’s experience […] (see paragraph (87).

(115) Second, Shell’s likely incentives to foreclose recycling rivals is further reduced by the fact that Shell is only a 50% shareholder in the JV. It is therefore unlikely that Shell would sacrifice […] margins on its sale of FRC for […] offered by the JV.

(116) Third, there is no evidence of past tying and bundling in the industry.121

(117) Therefore, the Commission considers that Shell is unlikely to have the incentive to engage in foreclosure through a tying or bundling strategy.

(C) Effects

(118) Any foreclosure strategy would be very unlikely to result in significant anticompetitive effects.

(119) First, the envisaged activities of the JV would likely only affect competitors to a limited extent. Both the market for FRC and the market for the recycling of SRCs is expected to grow in the future. Refineries generally expect “demand for recycling servicing will increase tremendously in the next 10 years as more and more resid hydroprocessing units are coming up all over the world”. Overall, “[r]ecycling services for SRCs should increase for three reasons:

a) it should shadow the market for FRCs, which is expected to increase over the next 10 years […]

b) regulatory requirements will enforce reuse of waste materials;

c) economic incentive to reclaim base metals from SRCs helps offsetting the cost of recycling.”122

(120) About half of the refineries that responded to the market investigation consider that there are not enough suppliers/capacity for recycling of SRCs.123 “There are more and more resid hydroprocessing units coming up all over world. Though many spent catalyst recycling facilities are planning for revamp, there could be shortage of spent catalyst recycling capacity in the near future.”124

(121) Furthermore, the respondents to the market investigation indicated that refineries no longer landfill their SRC in the EEA.125 A customer also noted that landfill will likely be banned worldwide in the future.126

(122) Second, the market investigation further confirmed that several alternative suppliers of recycling services are present in the EEA and EMEA Customers or potential customers in the EEA listed the following companies as potential suppliers: Treibacher, Moxba, Sadaci,, whereas, for an EMEA-wide market, a Middle East located refinery also mentioned GS Ecometals, Rubamin and Gladiuex Metal Recycling.127 These companies will continue to offer alternative solutions to refineries and form a competitive constraint to the JV. Recyclers of SRCs list as their competitors also Eurecat and SPT Czech, in addition to those mentioned by refineries.128

(123) Third, the JV will in fact increase competition and choice in the market. As one of the respondents to the market investigation considered “I hope this transaction brings good competition to the market”.129

(124) This is despite the fact that replies to the market investigation indicated plans exist to increase recycling capacity in the future even if increasing capacity for recycling of SRCs is (very) difficult.130 The fact that recyclers have nevertheless plans to increase capacity shows that demand for hydroprocessing is expected to increase significantly.

(125) The activities of the JV could prevent a future capacity shortage. A majority of respondents in the market investigation see an increasing demand for recycling services in the coming years: “[t]he volume of spent catalyst generated from hydroprocessing units is increasing due to the trend in higher capacity refinery units. Also, the environmental regulations for the disposal of hazardous waste or dangerous goods – in Europe and elsewhere - are becoming more stringent. Refiners are looking for more economic solutions to dispose of this material, which in some cases are recycling.”131

(126) Fourth, the JV is likely to [details as to the JV’s strategy and plans] serve customers in the Middle East, as [details as to the JV’s strategy and plans] recycling facility of the JV is [details as to the JV’s strategy and plans] envisaged to be built in Saudi Arabia. The respondents to the market investigation indicated that there are not enough recycling facilities in this region, whereas demand is growing and whereas there are already a number of alternative recycling services suppliers for SRC in the EEA.

(127) Competitors for recycling services recognised that “In Europe the volume of spent resid units is more or less in line with the current recycling capacity. In the Middle-East there is not enough capacity.”132 “In the Middle-east the number of resid units is growing”, so in consequence, demand for the recycling of SRC is high, but few recycling service suppliers are based in the region. Therefore, “[a]vailable capacities for recycling metal containing wastes are limited while the generation of these wastes is constantly increasing.”133

(128) Therefore, the JV is likely to [details as to the JV’s strategy and plans] recycle SRCs from the Middle East, where demand is greatest and where the Notifying Parties are carrying out plants feasibility studies. In consequence, it would not closely compete with recyclers of SRC located in the EEA, on either an EEA or EMEA-wide market. It follows that the creation of the JV would have a limited impact on competition in the EEA if the market for recycling of SRC were to be defined as EEA-wide.

(129) If the market for recycling of SRC were to be defined as EMEA-wide, the JV would compete with providers of recycling services for SRC listed in paragraph (122).

(130) Therefore, even in case the JV would in the future establish recycling facilities in the EEA, this would have the positive effect of adding an alternative supplier to the market.

(131) The market results of the market investigation also pointed to the ability of the JV to increase the availability of metals extracted via the recycling process: “Europe has no primary metal deposits for vanadium, nickel or molybdenum - so recycling (secondary raw materials) becomes increasingly important.”134

(132) Finally, it is also unlikely the JV could leverage its future position in the market for the recycling of SRC to increase Shell’s sales of FRC. First, as set out above, refineries chose their supplier of FRC on the basis of the technical performance and consider the recycling service as an add-on. It is also unlikely that AMG would agree to leveraging the recycling service as only Shell would have the benefit of selling more FRC. In any event, it is unlikely that any offer for recycling services can determine the outcome of the selection process for the FRC supplier which is driven by the technical performance of the FRC.

5.1.3. Conclusion on conglomerate non-coordinated effects

(133) Based on the analysis set out above, the Commission concludes that it is unlikely that the JV or Shell could, through tying and bundling the supply of FRC with the recycling of SRC, foreclose competitors in the EEA-wide or worldwide market for the supply of FRC or in the EEA-wide or EMEA-wide market for recycling of SRC.

6. CONCLUSION

(134) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This Decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this Decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C 56, 19.02.2020, p. 9.

4 Oil refiners can use various technologies to upgrade “bottom of the barrel” heavier “residue” crude oil into lighter, higher-value refined products (e.g. gasoline, diesel, or kerosene). One such technology is hydroprocessing which uses resid catalysts. When supplied to oil refiners, the resid catalysts are “fresh” (“FRCs”). Once used in the hydroprocessing process to upgrade the residue, the resid catalysts become “spent” (“SRCs”, “SRCs”).

5 The JV’s implementation is subject to the prior receipt of necessary competition clearances, but is expected to complete shortly thereafter.

6 Once established, the JV will be free to recruit its own staff and appoint its own independent management team. The Parents will provide the JV with initial funding of […].

7 The JV will develop its own market presence as it will enter into contracts: (i) with refiners to procure SRC to be recycled; and (ii) with buyers of the extracted industrial metals and other by-products from the spent catalyst recycling process. These operations will be distinct from both Shell’s activities (as Shell is not active in recycling and reclamation services) and AMG’s activities (as it will be active outside of North America […]).

8 Turnover calculated in accordance with Article 5 of the Merger Regulation.

9 The Notifying Parties estimated AMG’s market shares as respectively (i) [0-5] % on the worldwide market for the supply of vanadium and [5-10]% excluding China, and in any event less than 20% on any plausible market (see case M.4494); (ii) less than [0-5] % on an EEA wide or worldwide market for the supply of ferronickel molybdenum (see case M.4000); (iii) AMG […] sells calcium aluminate […], and an overlap with the JV activities would occur […] on a global market for the supply of calcium aluminate where AMG’s market share is less than [0-5] % (see case M.4157); and AMG […] sells calcium sulphate […] and an overlap with the JV activities would occur […] on a global market for the supply of calcium sulphate where AMG’s market share is below [0-5] % (see case M.4898). The JV has no market activities yet, but the Notifying Parties confirm that no affected market is expected to arise in respect of any extracted by-product from the JV’s activities given AMG’s minor market shares.

10 Form CO, paragraph 87.

11 Form CO, paragraph 166.

12 Cases COMP/M.4102 – BASF / Engelhard, paragraph 9, and COMP/M.3125 Huntsman / Matlinpatterson

/ Vaticano, paragraphs 10-14.

13 Form CO, paragraph 168.

14 Form CO, paragraph 269.

15 There are two main reactor types, “fixed bed” and “ebullated bed”. Fixed bed resid reactors tend to be used for relatively lighter residue feedstock. Such feedstock is reacted through catalyst that is fixed or held in a bed in the reactor. Once the catalyst is deactivated the unit is shut down and the catalyst is replaced. Ebullated resid reactors tend to be used for processing heavier residue feedstock. The ebullated bed reactor allows catalyst to be added and withdrawn in small portions several times per day, so no down time is required to replace the FRC. (Form CO, paragraph 167, footnote 129).

16 Form CO, paragraph 89.

17 Replies to question 5 of questionnaire to customers. Replies to question 3 of questionnaire to competitors FRC.

18 Replies to question 5.1 of questionnaire to customers.

19 Replies to question 5.2 of questionnaire to customers. Replies to question 3.3 of questionnaire to competitors FRC.

20 Replies to question 5.3 of questionnaire to customers.

21 Replies to question 6 of questionnaire to customers.

22 Replies to question 4 of questionnaire to competitors FRC.

23 Form CO, paragraph 72.

24 Form CO, paragraph 177.

25 Form CO, paragraph 177.

26 Form CO, paragraph 167.

27 Replies to question 5 of questionnaire to competitors FRC. Replies to question 10 of questionnaire to customers.

28 Replies to question 7 of questionnaire to competitors FRC.

29 Form CO, paragraph 287.

30 Form CO, Annex 12.

31 Form CO, paragraph 92.

32 Form CO, paragraph 97 a.

33 Form CO, paragraph 97 a.

34 Form CO, paragraph 97 b.

35 Prices are based on other factors such as: the metals content in the SRC, the hazardous content of the SRC, the volume of the SRC as a whole, contract duration, condition of the spent catalyst, and value of the metals contained within the spent catalyst.

36 Form CO, paragraph 97 c.

37 Form CO, paragraph 98.

38 Minutes call with a competitor for recycling services, paragraph 2.

39 Replies to question 5 and 5.1 of questionnaire to competitors recycling services.

40 Pyro-metallurgical processes involve the use of heat (i.e. thermal treatment) to bring about physical and chemical transformations in the materials to enable recovery of valuable metals.

41 Hydrometallurgy involves the use of aqueous chemical reactions (solvent) chemistry for the recovery of the metals.

42 Reply to question 3.1 of questionnaire to competitors recycling services.

43 Replies to question 4 of questionnaire to competitors recycling services.

44 Reply to question 8.1 of questionnaire to customers.

45 Views of a purchaser of FRCs.

46 Replies to question 6 of questionnaire to competitors recycling services.

47 Form CO, paragraph 99.

48 The spent catalyst is caked in toxic compounds and metals from the “bottom of the barrel” feedstock and becomes up to twice as heavier in weight as compared to when it is fresh (Form CO, paragraph 99).

49 Form CO, paragraph 101.

50 Form CO, paragraph 102.

51 Form CO, paragraph 104.

52 Form CO, paragraph 104.

53 Replies to question 14 of questionnaire to customers. Replies to question 7 of questionnaire to competitors recycling.

54 Regulation (EC) No 1013/2006 of the European Parliament and of the Council of 14 June 2006 on shipments of waste.

55 Reply to question 14.1 of questionnaire to customers.

56 Reply to question 16.1 of questionnaire to customers.

57 Reply to question 8 of questionnaire to competitors recycling services.

58 Replies to question 15 of questionnaire to customers.

59 Views of a purchaser of FRCs.

60 Non-Horizontal Merger Guidelines, paragraph 92.

61 Non-horizontal Merger Guidelines, paragraph 93.

62 Non-horizontal Merger Guidelines, paragraph 97.

63 Non-horizontal Merger Guidelines, paragraph 96.

64 Non-horizontal Merger Guidelines, paragraph 33.

65 Non-horizontal Merger Guidelines, paragraph 93.

66 Non-horizontal Merger Guidelines, paragraph 100.

67 Non-horizontal Merger Guidelines, paragraph 99.

68 Non-horizontal Merger Guidelines, paragraph 99.

69 Non-horizontal Merger Guidelines, paragraph 105.

70 Non-horizontal Merger Guidelines, paragraph 107.

71 Non-horizontal Merger Guidelines, paragraph 109.

72 Non-horizontal Merger Guidelines, paragraph 113.

73 Non-horizontal Merger Guidelines, paragraphs 103 and 114.

74 Reply to question 26 of questionnaire to competitors recycling services.

75 As of 2020, Shell […] in the EEA, […]. […] (Form CO, paragraph 176). […] following tenders held annually (in 2017, 2018 and 2019).

76 Form CO, Table 12.

77 Form CO, Paragraph 196

78 Form CO, Table 13.

79 Form CO, paragraph 196.

80 Form CO, paragraph 177.

81 Form CO, paragraph 241.

82 Form CO, paragraph 253.

83 Although the JV’s business plans have not been finalised, its [details of the JV's strategy] strategy is to construct a recycling plant using AMG’s technology and know-how in the Middle East (Form CO, paragraph 12).

84 Form CO, paragraph 220(a)(i).

85 Form CO, paragraph 220 (a)(ii).

86 Form CO, paragraph 220 (a)(iii).

87 Form CO, paragraph 220 (a)(iii).

88 Form CO, paragraph 220 (a)(iii).

89 Form CO, paragraph 220 (b)(i).

90 Response of 24 February 2020 to RFI dated 20 February 2020.

91 Form CO, paragraph 220 (b)(ii).

92 Form CO, paragraph 236.

93 Form CO, paragraph 236.

94 Form CO, paragraph 249.

95 Form CO, paragraph 209.

96 Form CO, paragraph 17.

97 Form CO, paragraph 5.

98 Form CO, paragraph 264.

99 Replies to question 19 of questionnaire to customers.

100 Replies to question 20 of questionnaire to customers.

101 Replies to question 21 of questionnaire to customers.

102 Reply to question 21 of questionnaire to customers.

103 Replies to question 18 of questionnaire to customers and replies to question 9 of questionnaire to competitors FRC.

104 Replies to question 18 of questionnaire to customers, and replies to question 9 of questionnaire to competitors FRC.

105 Form CO, tables 2 and 3.

106 Replies to question 17 of questionnaire to competitors FRC.

107 Replies to question 22 of questionnaire to customers; “The non-catalytic route (e.g. solvent deasphalting, delayed coking) should not increase much because of difficulties in finding markets for asphalt and petroleum coke products. The catalytic upgrading of resid has also better economics at current oil prices and above. Besides the conversion economic incentive, there are also fiscal policies in some countries (e.g. Russia) stimulating resid upgrading by taxing black oil products exports. These are also supported by regulatory changes, such as the recent IMO shift from 3.5 to 0.5% sulfur fuel oil on international waters. This has led to a major change in crude oil selection for refiners not equipped with resid upgrading, with an economic impact.”

108 Minutes of a call with a competitor of recycling services, paragraph 11.

109 Replies to question 29 of questionnaire to customers.

110 Replies to question 29.1 of questionnaire to customers.

111 Views of a purchaser of FRCs.

112 Minutes of a call with a potential customer, paragraph 10.

113 Replies to question 30.1 of questionnaire to customers.

114 Replies to question 29 and 30 of questionnaire to customers.

115 Replies to question 29.1 of questionnaire to customers, replies to question 16 of questionnaire to competitors.

116 Views of a purchaser of FRCs.

117 The average duration of contracts is 2 to 5 years. Replies to question 25 of questionnaire to customers.

118 Replies to question 24 of questionnaire to customers.

119 Reply to question 19.1 of questionnaire to competitors recycling services.

120 Reply to question 14.1 of questionnaire to competitors FRC.

121 [Details about the future commercial strategy of the JV], nor did anyone in the market investigation suggest that such behaviour or attempts at such behaviour has taken place in the past.

122 Replies to question 28 of questionnaire to customers.

123 Replies to question 27 of questionnaire to customers.

124 Reply to question 27.1 of questionnaire to customers.

125 Replies to question 9 of questionnaire to customers. Non-confidential replies to question 24.1 of questionnaire to competitors recycling services.

126 Replies to question 28 of questionnaire to customers.

127 Replies to question 23 of questionnaire to customers. However, one refinery also noted that “[the refinery] currently […] and is not in a position to list other potential suppliers because it has opted for a particular technical choice for unloading catalysts limiting the number of potential suppliers - hydro-jetting”.

128 Replies to question 12 of questionnaire to competitors recycling services.

129 Reply to question 33 of questionnaire to customers.

130 Reply to question 21.2 of questionnaire to competitors recycling services.

131 Reply to question 16.2 of questionnaire to competitors FRC.

132 Replies to question 20 of questionnaire to competitors recycling services.

133 Reply to question 19.1 of questionnaire to competitors recycling services.

134 Reply to question 19.2 of questionnaire to competitors recycling services.