Commission, March 22, 2017, No M.8361

EUROPEAN COMMISSION

Judgment

QATAR AIRWAYS / ALISARDA / MERIDIANA

Subject: Case M.8361 – QATAR AIRWAYS/ALISARDA/MERIDIANA

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 21 February 2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (3) by which Qatar Airways Q.C.S.C. ("Qatar", Qatar) and Alisarda S.p.A. ("Alisarda", Italy) (together the "Parties") will acquire within the meaning of Article 3(1)(b) of the Merger Regulation joint control over a newly formed holding company ("HoldCo") to which Alisarda will contribute the entire outstanding share capital of Meridiana fly S.p.A. ("Meridiana", Italy), by way of purchase of shares (the "Transaction").

1. THE PARTIES

(2) Qatar is a full service airline and operates international scheduled passenger air services and cargo services from its hub at Hamad International Airport in Doha, Qatar. Qatar is a member of the oneworld alliances and also provides certain ancillary services, including aircraft maintenance services, and ground handling, mostly in Doha.

(3) Alisarda is a holding company owning 100% of the shares in Meridiana. Alisarda is controlled by AKFED Aga Khan Fund for Economic Development, ultimately controlled by the Aga Khan family. Alisarda provides scheduled and chartered air passenger transport, tour organization, aircraft maintenance and airport administration services through its subsidiaries including Meridiana.

(4) Meridiana is an Italian airline and operates scheduled and charter passenger services and cargo services to destinations mostly in Europe and Northern Africa and some destinations in the Americas and Asia. Meridiana has the following subsidiaries: (i) Air Italy Holding S.r.l. and Air Italy S.p.A., which do not operate any flights (scheduled or chartered), but wet lease aircraft to Meridiana; (ii) Meridiana Maintenance S.p.A., a provider of aircraft maintenance services to Meridiana and third parties at Olbia airport in Sardinia; and (iii) Wokita S.r.l., a tour operator based in Olbia and offering holiday packages for Sardinia and other destinations in Italy and operating as a travel agent for the sale of airline tickets.

2. THE OPERATION

(5) According to the Contribution and Shareholder's Agreement ("CSA") of 14 July 2016, Alisarda will contribute the entire outstanding share capital of Meridiana including its subsidiaries to a newly formed holding company ("HoldCo"), which will be set up and initially wholly-owned by Alisarda.

(6) At closing, Qatar will acquire a shareholding of 49% in HoldCo and pay share capital in the amount of [confidential], whereas Alisarda will retain a majority shareholding of 51%. Qatar will also [description of certain financial links between Qatar and Alisarda.].

(7) According to the CSA, HoldCo's board of directors will have an odd number of between [confidential] directors. While Alisarda will have the right to appoint a majority of the board of directors, QR will have the right to appoint the other directors. The chairman of HoldCo's board of directors will be chosen among the directors appointed by Alisarda. HoldCo's board of directors will decide at simple majority, with the exception of "reserved matters", which are subject to a veto right by Qatar at board level (notably requiring an absolute majority including at least one favourable vote by a director appointed by Qatar) or at shareholders level (where reserved matters are subject to an [confidential] majority requirement).

(8) Reserved matters include amongst others: (i) [certain transactions exceeding a certain value] (4); (ii) the appointment, compensation, and dismissal of key managers [confidential] at Meridiana or the Meridiana subsidiaries.

(9) Key managers appointed and dismissed would hold ultimate responsibility for corporate and management functions such as [confidential]. Hence, they will play a decisive role in managing HoldCo.

(10) In view of its veto rights regarding reserved matters, Qatar will exercise de jure joint control over HoldCo within the meaning of paragraphs 65 to 74 of the Consolidate Jurisdictional Notice ("CJN"). This conclusion is supported by the absence of a deadlock mechanism between Meridiana and Qatar.

(11) In addition, according to the information submitted by the Parties, Qatar will represent a key financial and commercial partner of Meridiana and its subsidiaries, leading to a certain degree of dependency.[Assessment and description of financial links between Qatar and Alisarda.]. Such elements, while pointing out to financial ties between Meridiana and Qatar - taken together with the above veto rights in relation to the reserved matters - reinforce the conclusion that Qatar would exercise joint control over HoldCo.

(12) Finally, the Parties have also agreed on an initial five-year business plan for HoldCo to be implemented after closing.

(13) Based on the above, Alisarda and Qatar will acquire joint control over HoldCo and thus over Meridiana within the meaning of article 3(1)(b) of the Merger Regulation.

(14) Finally, the Commission recalls that, regarding the EU air transport licensing provisions, pursuant to paragraph 23 of the Jurisdictional Notice, "the concept of control under the Merger Regulation may be different from that applied in specific areas of Community and national legislation concerning, for example, prudential rules, taxation, air transport or the media. The interpretation of ‘control' in other areas is therefore not necessarily decisive for the concept of control under the Merger Regulation." [emphasis added].

3. EU DIMENSION

(15) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (5). Each of them has an EU-wide turnover in excess of EUR 250 million, but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.(6) The notified operation therefore has an EU dimension according to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

(16) The activities of Qatar and Meridiana overlap mainly in scheduled passenger air transport services, and, to very limited extent, in cargo services. (7)

4.1. Scheduled air transport services

4.1.1.1. O&D approach

(17) The Commission has traditionally defined the relevant market for scheduled passenger air transport services on the basis of the "point of origin/point of destination" (O&D) city-pair approach. Such market definition reflects the demand-side perspective whereby customers consider all possible alternatives of travelling from a city of origin to a city of destination which they do not consider substitutable to a different city-pair. As a result, every combination of a point of origin and a point of destination is considered a separate market (e.g. Milan-Rome). This approach allows assessing the horizontal effects of the merger on O&D passengers travelling between particular city-pairs which are served by both QR and Meridiana.(8)

(18) The Parties agree with the Commission's approach.

(19) In light of the above, the effects of the Transaction will be assessed on the basis of the city-pair O&D approach.

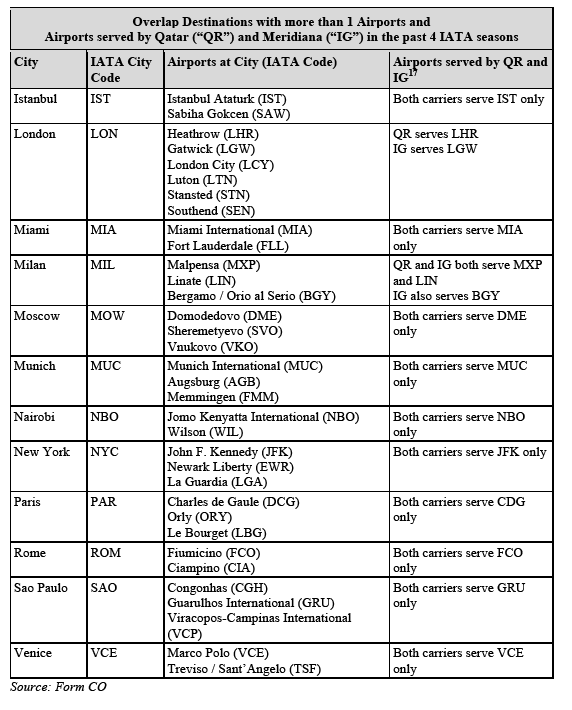

4.1.1.2. Time sensitive vs. non-time sensitive

(20) The Commission has traditionally found that a distinction may be drawn between time sensitive/premium and non-time sensitive/non-premium passengers.(9)

(21) Time sensitive/premium passengers usually travel for business purposes and value flexibility (such as cost-free cancellation and modification of the time of departure, etc.) and high level of comfort and tend to pay higher prices for such flexibility. Non-time sensitive/non-premium passengers, on the other hand, travel predominantly for leisure purposes or to visit friends and relatives book long time in advance, do not require flexibility with their booking and are generally more price sensitive.

(22) The Parties do not consider it meaningful to segment markets between types of passengers. Nonetheless the Parties have provided and assessed route-by-route market data not only for all passengers, but also separately for premium/non- premium passengers.

(23) For the purpose of the present Transaction, however, the question on whether premium and non-premium passengers belong to the same product market can be left open as the Transaction will not give rise to any serious doubts under any plausible market definition.

4.1.1.3. Non-stop (direct) vs. one-stop (indirect) flights (10)

(24) On a given O&D pair, passengers can travel either by way of a direct flight between the point of origin and the point of destination or by way of an "indirect" flight on the same O&D pair but via an intermediate destination. (11)

(25) In previous cases, the Commission considered that the substitutability between non-stop and one-stop flights on a route-by-route depends on various factors, including notably the flight duration but also on the type of passengers, the inconvenience associated with the stop-over or price considerations. In particular, when defining the relevant O&D markets for air transport services, the Commission has considered in prior decisions (12) that with respect to short-haul routes (generally below 6 hours flight duration) indirect flights do not generally provide a competitive constraint to direct flights absent exceptional circumstances (for example, the direct connection does not allow for a one-day return trip or the share of indirect flights in the overall market is significant).

(26) The Commission has in its practice (13) also considered that, with respect to long-haul routes (more than 6 hours flight duration), indirect flights constitute a competitive alternative to direct services under certain conditions (for example if they are marketed as connecting flights on the O&D pair in the computer reservation system).

(27) The Parties concur with the Commission's approach. In particular, the Parties claim that Qatar’s services will always be routed through Doha, which means that any Qatar connection would involve flying first East-bound (to Doha) and then West- bound (from Doha) to the final destination. Since all of Meridiana's destinations are located to the West of Doha, Qatar’s indirect services would not materially constrain Meridiana’s direct services on any of the (long-haul) overlap routes, as flight times on Qatar (indirect) connections would be significantly longer than Meridiana's direct flights.

(28) For the purpose of the present Transaction, the question on whether non-stop/direct and one-stop/indirect flights belong to the same product market can be left open as the proposed Transaction will not give rise to any serious doubts under any plausible market definition.

4.1.1.4. Airport substitutability

(29) In prior decisions, when defining a relevant O&D pair, the Commission has considered flights to or from airports with sufficiently overlapping catchment areas (particularly if the airports serve the same main city) to be substitutable with each other. Airport substitution will typically be considered when services are provided from more than one airport at one end of the route. In order to correctly capture the competitive constraint that flights from and to two (or more) different airports exerts on each other, a detailed analysis is necessary by taking into consideration the specific characteristics of the case at hand.(14)

(30) To assess airport substitutability, the Commission has taken into account various elements, such as an airport’s distance to the city in question, travel times to the airport, the existence of connecting traffic, the characteristics of the passengers travelling on a specific route, the Parties' practice in terms of monitoring and whether the routes in question are short-haul or long-haul.(15)

(31) The Parties consider that, in the present case, a separate assessment of airport substitutability is relevant only at those destinations where Qatar and Meridiana serve different airports, that is routes to/from Milan and London. For all other destinations which are served by more than one airport,(16) the question of airport substitutability can be left open as the outcome of the assessment would not change.

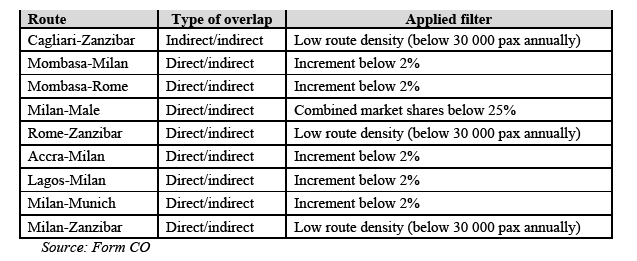

(32) The table below illustrates the overlap origins/destinations in the past 4 IATA seasons that are served by more than one airport:

(33) As the table shows, case airport substitutability is particularly relevant for the routes to and from (i) Milan and (ii) London, given that as regards the other origin/destinations airports the Parties serve the same airport. For the remaining overlap origin/destination the question of airport substitutability is less relevant to establish the overlap, as an overlap exists irrespective of whether or not other airports are included in the relevant catchment areas. Besides, the Parties combined market shares would be highest on the narrowest markets.

Airport-by-airport assessment for Milan and London

(34) Milan is served by three main airports, i.e., Malpensa (MXP), Linate (LIN) and Bergamo Orio Al Serio (BGY).

i. LIN is 11 km (25 minutes by car and 20 minutes by bus), MXP is 45 km (50 minutes by car and 40 minutes by train) and BGY is 54 km (52 minutes by car) from the city centre.(18)

ii. In prior cases, the Commission found these airports “prima facie to be substitutable from the demand side for point-to-point scheduled passenger” on the basis of the 1-hour/100 km catchment area benchmark.(19) In Alitalia/Etihad, the Commission’s market investigation indicated that MXP and LIN were substitutable.(20) The Commission also referred to the decision of the Italian competition authority stating that these airports were substitutable for international flights.(21)

iii. The Parties agree with the Commission’s previous assessment.

(35) London is served by six main airports, i.e., Heathrow (LHR), Gatwick (LGW), London City (LCY), Luton (LTN), Stansted (STN), and Southend (SEN):

i. In IAG/Aer Lingus, the Commission found indications that, at least for short- haul flights, the six London airports could be considered to belong to the same relevant market.(22) For long-haul flights, the Commission however has taken the position that the relevant market, at London, includes more likely just Heathrow, Gatwick, and, potentially at least, London City.(23)

ii. The Parties agree with the Commission’s previous assessment.

(36) For the purpose of the present Transaction, the Commission does not have to reach a conclusion as to whether flights between alternative airports and the same destination are substitutable to each other as the outcome of the Commission's competitive assessment would not change under any plausible market definition.

4.2. Cargo air services

(37) In prior decisions, the Commission considered a market for air transport of cargo including all kinds of transported goods provided by all types of air cargo carriers.(24)

(38) In addition, based on the Commission’s prior decisions, the O&D approach to market definition is not appropriate for air cargo transport services because cargo is

(i) in principle less time-sensitive than passengers, and (ii) usually transported behind and beyond the points of origin and destination by trans-modal transport methods and thus can be routed via a higher number of stops than passengers.(25)

(39) Based on the Commission's precedents, the geographic market definition for cargo transport services is usually broader than O&D pairs.(26) Accordingly, the Commission defined the market in intra-European routes of air cargo transport as European-wide. As regards intercontinental routes, the Commission established that catchment areas at each end of the route broadly correspond to continents where local infrastructure is adequate to allow for onward connections (for example, by road, train, or inland waterways), such as Europe and North America.(27) As regards continents where local infrastructure is less developed, the relevant catchment area has been considered the country of destination.(28) In addition, according to the Commission's precedents, cargo transport markets should be assessed on a unidirectional basis.(29)

(40) The Parties agree with the Commission's decision-making practice.

(41) For the purpose of the Transaction, the precise scope of the definition of cargo transport services can be left open as the Transaction would not likely give rise to any competition concerns under any plausible market definition.

5. COMPETITIVE ASSESSMENT

5.1. Scheduled air transport services

5.1.1.1. Conceptual framework

(42) In accordance with the Commission's previous practice,(30) all possible overlaps have been identified on the basis of the overlaps between Qatar and Meridiana as well as between each of Qatar and its joint business or codeshare partners on the one hand, and Meridiana and its joint business or codeshare partners on the other hand.

(43) In this respect, Qatar entered into joint business with British Airways and Royal Air Maroc. No overlap arises in connection with the joint business with Royal Air Maroc, which covers services between Qatar and Maroc only, where Meridiana does not operate. With its shareholding of 20.1% in IAG, Qatar is also the largest individual shareholder of IAG, the holding company of British Airways, Iberia, Vueling and Aer Lingus. However, in the absence of control by Qatar over IAG or of specific rights attached to this shareholding,(31) overlap routes between IAG and Meridiana are not relevant for the purposes of assessing the Transaction (unless they are subject to the existing joint business between Qatar and British Airways).(32)

5.1.1.2. Filters

(44) Consistent with its practice,(33) the Commission has applied the following filters to exclude likely unproblematic routes from the scope of its investigation.(34) For a route to be excluded, at least one of the filters must have been met in all the 4 last completed IATA seasons (35) and for all passenger segmentations:

a) For direct/indirect overlaps:

i. the Parties' combined market share was below 25%; or

ii. one of the Parties had a market share below 2%; or

iii. short-haul routes where the total share of indirect operations in the relevant market was below 10%; or

iv. at least one end of the city pair is outside the EU and the total annual traffic was below 30 000 passengers; or

v. the route was below the HHI thresholds of paragraph 20 of the Horizontal Merger Guidelines. )

b) For indirect/indirect overlaps:

i. the Parties' combined market share was below 25%; or

ii. one of the Parties had a market share below 2%; or

iii. as regards short-haul routes where the total annual traffic was below 15 000 passengers or as regards long-haul routes where the total annual traffic was below 30 000 passengers; or

iv. the route was below the HHI thresholds of paragraph 20 of the Horizontal Merger Guidelines.

(45) The Commission applied the filters consistently with respect to direct/indirect overlaps and indirect/indirect overlaps.(36)

(46) The Parties identified the affected direct/indirect and indirect/indirect routes.(37) The section below illustrates how filters have been applied to those markets and the outcome of the market investigation relating to the impact of the Transaction on air transport of passenger services.

5.1.1.3. Direct/indirect and indirect/indirect overlap routes

(47) The Parties' activities in relation to their direct/indirect and indirect/indirect services lead to 9 affected routes.

(48) However, none of these routes meets the conditions for closer scrutiny based on the application of filters used by the Commission in prior cases to exclude from its assessment routes that do not pose any likely competition problem. The affected routes and the reasons why they are not likely to raise any competition concerns are listed in the table below:

(49) A majority of respondents to the market investigation did not raise any material and/or substantiated concern as regards the Parties' activities on the 9 affected routes as well as more generally on any of the overlap routes.(38)

(50) In light of the above and of all other available evidence, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market on scheduled air transport services under any plausible market definition.

5.2. Cargo air transport services

(51) Qatar provides cargo-only air transport services while Meridiana currently does not operate cargo-only aircraft and transports limited volumes of cargo in the belly space of its passenger aircraft.(39)

(52) In a market for the provision of cargo air transport services encompassing all types of air cargo carriers and all kind of transported goods on a unidirectional basis the Parties' activities give rise to an affected market only on a continent-to-country basis on the route Maldives - Europe, where the Parties' combined market shares for 2016 would amount to [30-40]%.(40)

(53) The Parties however note that the available market data likely underestimate total cargo market volumes, as not all cargo carriers report their cargo volumes to the World Air Cargo Data (WACD) database. Accordingly, the Parties claim that the cargo market shares are likely overestimated based on the available third-party data.

(54) The Commission considers that the Transaction will not give rise to any significant merger-specific effect on the Maldives-Europe cargo market since Meridiana is a marginal competitor on this market, as its negligible presence (below [0-5]%) of the total air cargo volumes transport on this route illustrates.

(55) In addition, on the Maldives-Europe route the merged entity would face competition from sizeable competitors such as e.g. Emirates, Etihad, SriLanka Airlines, Singapore Airlines, Turkish Airlines.(41)

(56) Respondents to the market investigation did not raise any concern in connection with the Parties' activities in the provision of markets other than that of passenger air transport services, including the provision of cargo services.(42)

(57) In light of the above and of all other available evidence, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market on the provision of cargo air transport services under any plausible market definition.

6. CONCLUSION

(58) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 OJ L 24, 29.1.2004, p. 1 (the "Merger Regulation").

4 [examples of certain transactions exceeding a certain value].

5 Turnover calculated in accordance with Article 5 of the Merger Regulation.

6 Qatar calculated its turnover on the basis of the three methodologies used in airlines cases, namely the "50/50", the "point of origin", and the "point of sale" methodologies. Alisarda calculated its turnover on the basis of the "50/50" and the "point of sale" methodologies, but could not provide an estimate on the basis of the "point of origin" methodology, in particular because Meridiana accounts sales for return tickets (i.e. origin-destination-origin) based on the entire return journey and not separately for each leg of the return journey. The Parties' turnover meets the thresholds set in Article 1(2) of the Merger Regulation under each of the methodology they have used respectively to calculate their turnover.

7 There are no other overlaps between Qatar and Meridiana in charter services, ground handling services, catering services and lounge management. Qatar and Meridiana provide both aircraft maintenance services, but they are present at different airports. The Transaction would not lead to any vertically affected markets as regards the activities of Meridiana in the passenger air transport sector and Qatar's activities in (i) airport management services; (ii) catering; (iii) ground handling and (iv) lounge management services, as Qatar carries out these activities at any airport that is currently served by Meridiana or that is expected to be served by Meridiana in the foreseeable future. Likelwise, the Transaction would not lead to any vertical relationship between the activities of Meridiana as a provider of charter flights as well as as tour operator (through its subsidiary Wokita) and Qatar's activities in the passenger air transport services, as Qatar is not a customer of charter services (i.e. it does not own any tour operator) and it does not supply charter seats on a wholesale basis.

8 M. 7541 – IAG/Aer Lingus, paragraphs 14-19, M. 7333 – Alitalia/Etihad, paragraphs 63-69, M. 6607– US Airways/American Airlines, paragraphs 8-12, M. 6663 – Ryanair/Aer Lingus, recitals 49-61.

9 Cases M. 7541 – IAG/Aer Lingus, paragraphs 20-29, M. 7333 –Alitalia/Etihad, paragraphs 70-74, M. 6607 – US Airways/American Airlines, paragraphs 13-18, M. 6663 – Ryanair/Aer Lingus, recitals 382-387.

10 "Non-stop" flights are flights that take off at airport A and land at airport B where they load off passengers without any stops in between. By contrast, "direct" flights may entail a refuelling stop and/or a disembarking/re-embarking stop, but are marketed under a single flight code and are flown with a single aircraft. "One-stop" flights include direct flights that do not qualify as "non-stop", as well as indirect flights which are journeys that require a change of aircraft or a change of flight code.

11 Case M.6663 – Ryanair/Aer Lingus III, recital 373.

12 Cases M.7333 – Alitalia/Etihad, paragraphs 75 and following; M.6663 – Ryanair/Aer Lingus III, recitals 374- 375; M.5440 – Lufthansa/Austrian Airlines, paragraph 25 and following; M.5403 – Lufthansa/bmi, paragraph 17; M.5335 – Lufthansa/SN Airholding, paragraph 37 and following.

13 Cases M.6607 – US Airways/American Airlines, paragraph 19; M.5440 – Lufthansa/Austrian Airlines, paragraph 27.

14 M.7333 – Alitalia/Etihad, paragraphs 82 and following; M.6663 – Ryanair/Aer Lingus III, recital 65 and following; M.4439 – Ryanair/Aer Lingus, recital 73 and following.

15 M. 7541 – IAG/Aer Lingus, paragraphs 37 and following; M. 7333 – Alitalia/Etihad, paragraphs 82 and following; M. 6607 – US Airways/American Airlines, paragraphs 23 and following; M. 6663 – Ryanair/Aer Lingus, recitals 62 and following; M.5747 – Iberia/British Airways, paragraphs 19 and following; M.5440 – Lufthansa/Austrian Airlines, recitals 15 and following; M.5335 – Lufthansa/SN Airholding, recitals 51 24and following ; M.3280 – Air France/KLM, paragraphs and following. See also judgment of the General Court of 6 July 2010 in case T-342/07 Ryanair v Commission, paras. 99 and following.

16 These are: Istanbul, Miami,Moscow, Munich, Nairobi, New York, Paris, Rome, Sao Paulo and Venice.

17 Including through codeshare, SPA, and interline services.

18 Case M.7333 – Alitalia/Etihad, paragraph 100.

19 Cases M.7333 – Alitalia/Etihad, paragraph 101; M.6663 – Ryanair/Aer Lingus III, paragraph 246.

20 Cases M.7333 – Alitalia/Etihad, paragraphs 102-105. The Commission ultimately left the assessment open as the effect of the transaction would not materially change regardless of whether these three airports were considered in the same market. In the Ryanair/Aer Lingus I & III cases, the Commission found substitution between three airports in Milan for Rynair and Aer Lingus passengers from Dublin; M.4439 – Ryanair/Aer Lingus, paragraphs 263-267; Case M.6663 – Ryanair/Aer Lingus III, paragraphs 245-252

21 Case M.7333 – Alitalia/Etihad, footnote 91.

22 The Commission concluded that “scheduled point-to-point passenger air transport services between Dublin and Belfast, and the six London airports belong to the same market”; see, e.g., Case M.7541 – IAG/Aer Lingus, paragraph 74. The Commission also concluded that the degree of substitutability between the London airports would depend on various factors such as passengers’ preference, the degree of differentiation in the services offered by the carriers and characteristics of each route (see at paragraph 74).

23 Cases M.6828 – Delta Airlines/Virgin Atlantic, paragraph 43; M.6663 – Ryanair/Aer Lingus III, paragraph 67 (“the degree of substitutability may also depend on the length of the sector covered, as catchment areas increase with sector length”). As regards London City, there are at present only few long-haul flights departing from London City (essentially to New York); however, London City has recently received planning permission for expansion, which will open up opportunities for airlines for longer-haul destinations including the Gulf and Middle East and Turkey; see London City Airport press release of July 27, 2016, available at: https://www.londoncityairport.com/news/readpressrelease/major-boost-for-uk-and-london-economy- as-london-city-airport-receives-planning-permission-for-expansion-

24 Cases M.5747 – Iberia/British Airways, paragraph 40; COMP/M.6447 – IAG/bmi, paragraphs 91-92, M. 6828 – Delta Airlines/ Virgin Group / Virgin Atlantic Limited, paragraphs 72-81.

25 Cases M.5747 – Iberia/British Airways paragraphs 36-43 and M.5440 – Lufthansa/Austrian Airlines, paragraphs 28-32.

26 The O&D approach to market definition is not appropriate for air cargo transport services because cargo is in principle less-time sensitive than passengers and usually transported behind and beyond the points of orgin and destination by trans-modal transport methods and can thus be routed via a higher number of stops than passengers.

27 See, among others, M. 5747 – Iberia/British Airways, paragraphs 36-43, case M. 5440 – Lufthansa/Austrian Airlines, paragraphs 28-32.

28 Cases M.5440 – Lufthansa/Austrian Airlines, paragraph 30, M.5747 – Iberia/British Airways, paragraph 42, M.6447 – IAG/bmi, recital 94, and M. 6828 – Delta Airlines/ Virgin Group / Virgin Atlantic Limited, paragraphs 72-81.

29 Cases M.5747 – Iberia/British Airways, paragraph 39, M. 5440 – Lufthansa/Austrian Airlines, paragraph 31.

30 Case M.7333 - Alitalia/Etihad, paragraphs 138 and following.

31 In particular, Qatar's minority shareholding does not confer on Qatar any influence that can put into question the fact that IAG acts independently from Qatar on the market and does not grant to Qatar access to confidential IAG information beyond information that is available to any IAG shareholders. See also the assessment carried out in M.7333 - Alitalia/Etihad, Section 5 “Etihad’s investmets in other carriers” paragraphs 30-55.

32 Besides, the economic and financial power of Qatar Airways and of its shareholders would not materially alter the competitive analysis of any of the overlap routes. The alleged fact that Qatar Airways would possess a strong financial capacity is not per se indicative of competition concerns and does not alter, as such, the conclusion reached by the Commission as regards the impact of the Transaction on the relevant markets.

33 Cases M. 7541 – IAG/Aer Lingus, paragraphs 151-153; M.7333 – Alitalia/Etihad, paragraphs 171 - 175; M.6828 – Delta/Virgin, footnote 77; M.6607 – US Airways/American Airlines, paragraph 32; M.5889 – United/Continental, footnote 25; M.5830 – Aegean/Olympic I, footnote 365; M.5747 – BA/Iberia, paragraph 117; and M.5335 – LH/SN Airholding, footnote 302.

34 Filters do not apply to direct/direct overlaps, for which the general rules apply (there is no affected market if the Parties combined market share is below 20%).

35 Winter Season 2014/15, Summer Season 2015, Winter Season 2015/16 and Summer Season 2016.

36 Form CO, paragraphs 143-153 and Annex QP25.

37 No direct/direct overlap leads to any affected market. Form CO, paragraphs 143-153 and Annex QP25.

38 Responses to questions 3-4-5-6-8 and 9 of Questionnaire to Competitors – Q1; responses to questions 3-4-5-6-8 and 9 of Questionnaire to Corporate Customers - Q2; responses to questions 3-4-5-6-8 and 9 of Questionnaire to Travel Agents – Q3.

39 These cargo services are marketed not by Meridiana but by an independent third party, ECS Group, which manages all aspects of Meridiana’s cargo capacity (e.g., sales of cargo capacity and contracts with handlers and forwarders). Meridiana only receives net revenues from these services.

40 Source: World Air Cargo Data (WACD) and IATA Cargo Accounts Settlement System (CASS); Parties.

41 Parties' response of 24 February 2017 to the Commission's request for information of 22 February 2017.

42 Responses to question 7-8 and 9 of Questionnaire to Competitors – Q1; responses to questions 7-8 and 9 of Questionnaire to Corporate Customers - Q2; responses to questions 7-8 and 9 of Questionnaire to Travel Agents – Q3.