Commission, May 17, 2016, No M.7941

EUROPEAN COMMISSION

Judgment

SAINT-GOBAIN GLASS FRANCE / CORNING / JV

Dear Sir/Madam,

Subject: Case M.7941 - SAINT-GOBAIN GLASS FRANCE / CORNING / JV. Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

(1) On 6 April 2016, the European Commission received a notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Compagnie de Saint-Gobain S.A. ("Saint-Gobain", France) and Corning Incorporated ("Corning", USA) acquire, within the meaning of Article 3(4) of the Merger Regulation, joint control of a newly created company constituting a joint venture (the "JV") (3). Saint- Gobain and Corning are designated hereinafter as the 'Notifying parties' to the proposed transaction.

1. THE PARTIES

(2) Saint-Gobain is active in three business sectors, namely (i) innovative materials (including flat glass), (ii) construction products, and (iii) building materials distribution.

(3) Corning is a U.S.-based materials company active in speciality glass, ceramics and optical physics for use in a wide range of industries. Corning's main areas of activity are flat glass for display and cover applications for use in consumer electronics; optical fiber, cable, hardware and related equipment for communication networks; vessels for drug research and discover applications in the life sciences industry; pharmaceutical tubing; ceramic filters and substrates to reduce emissions from combustible engines; and advanced glass technologies for new applications.

2. THE OPERATION

(4) The operation consists of the incorporation of a JV between Saint-Gobain and Corning which will focus on the development, manufacture and commercialisation of laminated lightweight automotive glazing solutions, which will incorporate soda-lime glass (traditional glass used in the automotive industry) and at least one layer of thin aluminosilicate glass ("TAG") (the product to be developed by the JV is hereunder referred to as “TAG-based automotive glazing solutions”) (the "Proposed Transaction"). The JV’s products are expected to have unique characteristics and to meet car manufacturers' (“OEM”) specifications in terms of thickness, impact resistance and optical qualities.

3. THE CONCENTRATION

(5) The Proposed Transaction consists in the creation of a jointly controlled and fully functional JV by Corning and Saint-Gobain. Therefore, the Proposed Transaction constitutes a concentration within the meaning of article 3(4) of the Merger Regulation..

3.1. Full Functionality

(6) The JV will have sufficient resources to operate independently on the market, both in terms of financial resources, staff and assets (paragraph 94 of the Jurisdictional Notice).

(7) First, as to the financial resources to operate independently on the market, the Parties will make an initial investment of […]. This initial capital contribution is expected to suffice for the purposes of covering the expenditures of the JV during the development and starting of production of the TAG-based automotive glazing solutions. After this start-up period, the JV should finance itself both by retaining part of the profits generated and by accessing the capital markets.

(8) Second, the JV will also have sufficient staff to operate independently. At the beginning of operations, [details on staffing of the JV].

(9) During the initial development phase, [details on staffing of the JV].

(10) Once the development phase is over, [details on staffing of the JV].

(11) The JV is expected to have its [details on staffing of the JV].

(12) Third, the JV’s activities will be beyond those of the Parents (paragraphs 95-96 of the Jurisdictional Notice). The JV will develop a new product offering (the TAG-based automotive glazing solutions) adding significant value to the Parties’ input products with its activity. The development of a TAG-based automotive glazing solution will in fact require research and development efforts and the activities of the JV will go beyond one specific function for the parents and the JV will offer to the market a product significantly different to those of the Parties.

(13) Fourth, albeit the JV will receive the input products from the Parents, the JV will sell its products exclusively to third parties. The JV will be selling TAG-based automotive glazing solutions directly to the OEM and no sales to the Parties are expected.

(14) As to purchases from the Parents, the development process which will be carried out by the JV will add significant value to the Parties input products. Therefore the fully functional nature of the JV will not be impaired.

(15) Finally, the JV is expected to operate on a lasting basis as it is not incorporated for a specific period of time.

3.2. Joint Control

(16) Corning and Saint-Gobain will each own 50% of the shares in the JV and both Parties will have the possibility to exercise decisive influence over it for the reasons explained below.

(17) First, shareholders’ resolutions (which include the appointment of the Managing Directors and the members of the JV’s Management Committee) will be taken by an affirmative vote of more than 50% of the voting shares or by unanimous written consent, with a quorum requiring the presence of Shareholders representing more than 50% of the shares.

(18) Second, each Party will have the right to appoint one managing director.

(19) Third, strategic decisions – including the adoption of the JV's annual budget and business plan – will be made by the Managing Committee which will be composed of an even number of members (half designated by each Party). The Management Committee will adopt resolutions by unanimous written consent with a quorum requiring the presence of at least two representatives of each Party. Therefore, both Parties will be able to veto decisions at the level of the Management Committee.

(20) In light of the above, Corning and Saint-Gobain will jointly control the JV

4. EU DIMENSION

(21) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (4). Each of them has an EU-wide turnover in excess of EUR 250 million, but they do not achieve more than two-thirds of their aggregate EU- wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

5. COMPETITIVE ASSESSMENT

(22) The Parties are not active in the same product market, hence the Proposed Transaction does not give rise to horizontally reportable markets. Depending on the market definition retained, the Proposed Transaction might generate a (future) horizontal overlap between the activity of Saint-Gobain and those of the JV in the sale of automotive glass.

(23) As to possible vertical relationships, the JV will be active in a market which will possibly be downstream to the markets where the Parties are currently active. In particular, the JV will use the products manufactured by the Parties as input for the products it will manufacture.

5.1. The business activity of the JV

(24) The business activity of the JV will be the development and subsequent production of an innovative laminated lightweight glazing solutions for the automotive sector that incorporates soda-lime glass and thin aluminosilicate glass.

(25) Soda-lime glass is the basic flat glass product category. It is the most common flat glass type and accounts for the vast majority of flat glass being produced. Soda-lime glass is produced through an uninterrupted process where a continuous stream of molten glass is poured from a furnace on to a large shallow bath of molten tin. The molten glass floats on the tin, as oil floats on a pool of water, and forms a level surface. Thickness is controlled by the speed at which solidifying glass ribbon is drawn off from the bath. After annealing (controlled cooling), the glass emerges as a polished product with virtually parallel surfaces.

(26) The resulting float glass can be processed in a number of different ways, e.g. by laminating or toughening the glass to produce a safety glass which will be shatter-safe on impact, or by coating the glass such as to enhance the energy efficiency qualities of the glass. Once processed, the glass may be further transformed and used for different end-applications, in particular for the automotive industry (i.e. car windows and sunroofs) and for architecture/construction (i.e. internal and external glass used in buildings).

(27) Aluminosilicate glass is a specialised glass that has aluminium oxide in its composition, a very small amount of soda and no lime. This composition results in a highly resistant glass capable of supporting very high temperatures, sudden temperature changes and other conditions which can damage the surface of other types of glass having a different composition. The aluminosilicate composition also enables this type of glass to undergo further heat or chemical processing, and it is therefore used for industrial applications such as combustion tubes or gauge glasses for high pressure steam boilers which require a type of glass resistant to very high temperatures.

(28) Corning uses a proprietary fusion draw process to produce its thin aluminosilicate glass ("TAG"). This proprietary production process includes a chemical processing through an ion-exchange process. This process creates a compression which strengthens the glass and prevents it from breaking on flaws. The combination of the aluminosilicate glass composition and the ion-exchange process results in a glass product that is resistant to surface damage and better able to resist breakage when flaws are introduced to the surface of the glass.

(29) The focus of the JV will be the manufacture of TAG-based automotive glazing solutions combining at least one sheet of TAG with a soda-lime layer. The JV’s products are expected to have unique characteristics and to meet OEM specifications in terms of thickness, impact resistance and optical qualities. The initial market opportunity is small. In the long term, TAG-based automotive glazing solutions may become more widely adopted as automobile makers seek to meet lower emissions standards and improve energy consumption without sacrificing automobile performance by lowering the overall weight of the vehicle.

5.2. Market Definition

(30) The Proposed Transaction, depending on the market definition retained, will give rise possibly to three affected markets: two upstream vertically affected markets where Saint-Gobain and Corning are active and one downstream affected market where the JV will be active.

5.2.1. Production of automotive glass

(31) Saint-Gobain is active in the production of automotive glass which will be an input for the TAG-based automotive glazing solution that will be developed and produced by the JV.

(32) In previous decisions, the Commission found that automotive glass constitutes a separate product market. It distinguished between (i) automotive glass supplied to original equipment manufacturers (“OEMs”) and (ii) automotive glass supplied to the independent aftermarket (“IAM”) (5).

(33) The Parties also agree with the above market definition.

(34) As to the geographic scope of the market, the Commission has in the past decision regarded this market as EEA-wide in scope, however it did not reach a final conclusion.

(35) The information provided by the Parties over the course of the investigation indicated that the vast majority of the automotive glass is sold within the Member States where it is produced. This might point to a narrower geographic scope of the product market.

(36) The market investigation however indicated that it is more appropriate to regard this market as EEA-wide in scope. This is because, first, the majority of manufacturers of automotive glass indicated that they compete on an EEA wide level and, second, no customers gave any indication that the geographic scope of this market should be regarded as narrower than EEA.

(37) Ultimately however, the definition of the relevant product and geographic markets can be left open, as regardless of the precise market definition, the transaction will not give rise to competition concerns.

5.2.2. Cover material for consumer electronic devices

(38) Screens of consumer electronic devices need to be protected and for this purpose different materials are available, such as TAG, extra thin soda-lime glass (with a thickness of up to 1.1mm), sapphire glass and non-glass covers.

(39) The Commission has not analysed this market in previous cases. The Parties claim that the appropriate market definition should encompass all types of cover material as from a demand-side perspective these would be fully substitutable for the reasons explained below.

(40) First, the various types of cover material, albeit having slightly different physical characteristics, can be employed on all consumer electronic devices and do guarantee comparable levels of performance.

(41) Second, consumer electronic device manufacturers can and do switch from one material to the other. When developing a new product, all types of cover material are considered and the Parties provided examples of switching from one product to another.

(42) The Parties' claims were supported by the findings of the market investigation. Competitors responding to the market investigation indicated that, from a demand side perspective, all types of cover material can be used interchangeably. The market investigation also indicated that customers have in the past switched between various types of cover material. Hence, it is plausible to consider that substitution exists between different types of cover material for consumer electronic devices.

(43) As to the geographic scope of this market, the Parties claim that it should be regarded as worldwide as TAG and other cover materials are delivered worldwide from the production sites, which are located mainly in Asia.

(44) The market investigation broadly confirmed the Parties' claims and gave indications that this market could be considered worldwide in scope.

(45) Ultimately however, the definition of the relevant product and geographic markets can be left open, as regardless of the precise market definition, the transaction will not give rise to competition concerns.

5.2.3. TAG-based automotive glazing solutions

(46) TAG-based automotive glazing solutions will be the result of the development effort carried out by the JV and, according to the Parties, should be regarded as a distinct product market from the production of automotive glass for the reasons explained below.

(47) First, so far, laminated solutions incorporating TAG have been used for a limited number of applications in high-end vehicles with minimal market shares in the automotive sector. These are generally “concept-type” cars where new technologies are introduced at premium prices.

(48) Second, it is expected that TAG-based glazing solutions will be used in high performance premium cars. When OEMs incorporate new technological breakthroughs for the production of their cars, they often market them as an important part of the enhanced technological features of their vehicles and as distinguishing factor(s) vis-à- vis other cars. Hence, OEMs developing and manufacturing high-end cars cannot easily switch from TAG-based glazing to non-TAG-based automotive glazing solutions. Therefore according to the Parties there will be no demand side substitutability between TAG-based glazing solutions and traditional glazing solutions.

(49) The market investigation indicated that TAG-based automotive glazing solutions are expected to have different characteristics compared to traditional automotive glazing solutions, in particular, they are expected to be significantly lighter and thinner. Also, the market investigation indicated that both competitors and customers expect that TAG-based automotive glazing solutions will likely be more expensive compared to traditional automotive glazing; the premium being estimated above 40%. Finally, the OEMs responding to the market investigation indicated that in the future they are likely to be able to use the two different glazing solutions on all their vehicles.

(50) Notwithstanding the above, TAG-based automotive glazing solutions and traditional glazing solutions will most likely not be substitutable in practice because of the expected technical and price differences between the two. TAG-based automotive glazing solutions will likely be installed on premium/more expensive vehicles and will likely not be attractive for other types of vehicles, mainly due to price considerations.

(51) This conclusion is also supported by the replies of OEMs to the market investigation where the majority of respondents indicated that they expect TAG-based automotive glazing solutions to be used mainly on more expensive vehicle segments.

(52) As to the geographic scope of the market, the Parties claim that it – in line with the market for automotive glass – this market will be EEA wide in scope. The market investigation gave indication that this definition might be appropriate.

(53) Ultimately however, the definition of the relevant product and geographic markets can be left open, as regardless of the precise market definition, the transaction will not give rise to competition concerns.

5.2.4. TAG as an input for TAG-based automotive glazing solutions

(54) Notwithstanding the fact that consumer electronic TAG can likely be substituted with other materials, these cannot be employed for the development of TAG-based automotive glazing solutions. The TAG-based automotive glazing solutions which the JV intends to develop will incorporate one layer of TAG and no other materials, Also, the Parties claim that added value of this solution will be brought about by TAG's physical characteristics.

(55) Hence, with respect to the development of TAG-based automotive glazing solutions, the Commission considers it plausible that there will not be demand side substitutability between TAG and other materials as inputs.

(56) In light of the above, and notwithstanding the conclusions reached in section 5.1.2. above, the Commission considers that – for the purposes of the present case – TAG could potentially be regarded as a separate input product market.

(57) As to the geographic scope of this plausible market, the analysis and conclusion reached in section 5.1.2 above is plausibly applicable to this product market as well.

(58) Ultimately however, the definition of the relevant product and geographic markets can be left open, as regardless of the precise market definition, the transaction will not give rise to competition concerns.

5.3. Competitive Assessment

5.3.1. Non-horizontal effects

(59) If the market for TAG-based automotive glazing solutions was to be considered as a separate product market, the Parties to the Proposed Transaction will be active on two markets (the production of TAG for Corning and the production of glass for automotive applications for Saint-Gobain) which are directly upstream to the market where the JV will be active.

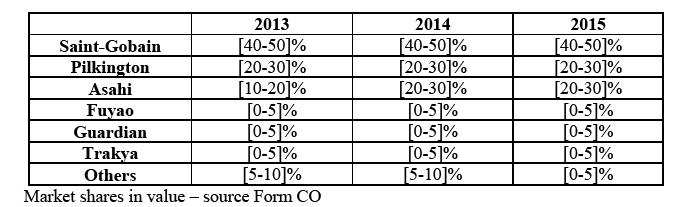

(60) As already explained above, the business activity of the JV will be the development of a glazing solution for the automotive industry combining at least one sheet of TAG with a soda-lime layer. Hence, the inputs for the development and later manufacture of this new glazing solution are products manufactured by the Parties (soda-lime glass for Saint-Gobain and TAG for Corning).

(61) Hence, the Transaction could lead to input (TAG or soda-lime glass) foreclosure. The Commission however takes the view that, post transaction, the Parties will not have the ability to foreclose access to either of the inputs to the JV's competitors.

5.3.1.1. Ability to foreclose access to TAG

5.3.1.1.1. The Parties Claims

(62) The Parties claim that the Proposed Transaction will not affect customers’ ability to source TAG on a global level and, in particular, in the EEA for the purpose of using it as an input to produce automotive glazing applications for the reasons explained below.

(63) First, Corning’s existing supply relationships in the EMEA region (6) (namely with [details on customers]) will not be discontinued as a result of the JVA and Corning will be entitled to continue offering such companies the required technical support.

(64) Second, in addition to allowing for the continuity of existing supply relationships with automotive glass manufacturers in the EEA, the JVA, notwithstanding the fact that it is incorporated for an indefinite period of time, only limits Corning’s ability to supply TAG to third parties for the purpose of developing or selling TAG-based automotive glazing solutions until […].

5.3.1.1.2. Commission's assessment regarding Access to TAG

(65) On the upstream market encompassing all cover material for consumer electronic devices, the market share of Corning is estimated at circa [30-40]% in volume.

(66) If the possible market for the sales of TAG as input for TAG-based automotive glazing solutions is considered as the relevant input market – the narrowest possible market definition in this case – Corning estimates that its market share in 2015 was [80- 90]% and the closest competitors would be Asahi ([10-20]%) and NEG ([5-10]%). The latter two competitors' market shares increased significantly compared to 2014 (Asahi [0-5]%, NEG [0-5]%).

(67) The market investigation as well gave indications that Corning holds a significant market share, however not as significant. According to the respondents to the market investigation, Corning share is [60-70]%, Asahi [10-20]% (2014) and NEG of circa [10- 20]%. The market investigation also indicated that both Asahi and NEG have been steadily increasing their market share in the last 3 years. Specifically, Asahi market share increased from [10-20]% in 2013 to the current share and NEG from [0-5]% in 2013 to the current [10-20]%. Apart from the two competitors above, the market investigation also indicated that Schott manufactures TAG albeit having a more limited market share.

(68) As to the (future) market structure on the downstream market (that is the plausible market for TAG-based automotive glazing solutions), the market investigation indicated that for the development of automotive glazing solutions (irrespective of the type of glass used), it is very important to have the technical capability to curve glass and automotive glass manufacturers have this capability. In light of this requirement, the Commission considers as plausible that downstream competitors of the JV will most likely be automotive glass manufacturers (alone or in partnership with TAG manufacturers).

(69) Hence, downstream, it is plausible – albeit not certain – that the possible future competitors of the JV will be automotive glass manufacturers such as Asahi, Pilkington, Guardian, Trakya, Isoclima, Salgglas and Hirschler. In light of the fact that the development of this product is at a very early stage, the Commission at this moment is not in the position to determine which companies will actually be active on such a market. However, the above list includes the major automotive car manufacturers and those smaller automotive car manufacturers for which it is known that a development of TAG-based glazing solutions is ongoing.

(70) Under this assumption, Corning, notwithstanding the high share of supply of TAG, will have limited possibility to foreclose access to inputs for the reasons explained below.

(71) First, alternative credible suppliers exist. Asahi, for example, is active on both the upstream and downstream market and therefore can self-supply TAG to its downstream business for the development of a competing solution to that of the JV. NEG on the upstream market has a share of supply estimated at circa [10-20]% and could also serve as a supplier of TAG for downstream competitors of the JV. Finally, prospective competitors to the JV responding to the market investigation indicated that also Schott can be regarded as a viable supplier of TAG for the development of a TAG-based automotive glazing solution. A respondent to the market investigation indicated that Schott has a limited footprint in North America but confirmed that in the EEA, it is an established manufacturer and therefore is a viable supplier in this region.

(72) Second, the Commission considers that TAG production capacity is not a constraint at this stage of the development as there is no particular need for very significant volumes of TAG. In fact, currently TAG-based automotive solutions are still under development and in the next two years, only samples and prototypes of TAG- based automotive glazing solutions are expected to be manufactured in order to engage in marketing activities and procurement negotiations with OEMs.

(73) During this development phase, and subject to the positive outcome of the development of the product itself, it is possible TAG manufacturers will be able to scale up their production facility. Hence, in the next 5 years, total production capacity of TAG will most likely be significantly different compared to that of today. This is also supported by the fact that both Asahi and NEG increased significantly their respective market share in just two years (7).

(74) The Commission therefore takes the view that alternative credible suppliers of TAG already exist and that, in any event, it is possible that total TAG production capacity will increase in the near future, lowering Corning's share of supply on the upstream market. This eliminates, or at the very least significantly reduces, Corning's ability to restrict access to TAG for the JV's competitors.

5.3.1.2. Ability to foreclose access to soda-lime glass.

(75) The Parties claim that as a result of the Proposed Transaction Saint-Gobain will not have the ability to foreclose access to soda-lime glass to the JV's competitors for the reasons explained below.

(76) First, customers will remain free to source float glass from several leading global suppliers which, aside from Saint-Gobain, are active in the EEA. Moreover, Saint- Gobain’s ability to supply float glass to other automotive glass suppliers and OEMs will not materially change.

(77) Second, most automotive glass manufacturers have in house capabilities to manufacture soda-lime glass and the majority of manufactured float glass is used for own use by the glass manufacturers. Third-party sales are exceptional and the marginal traded volumes will not be affected by the Proposed Transaction.

(78) Third, pursuant to the JV agreement, Saint-Gobain remains free to continue the supply of float glass to third parties for the production of laminated automotive glazing of traditional thicknesses (above 3.2mm). With regard to the supply of float glass for the production of laminated automotive glazing below 3.2mm, [details on contractual arrangements].

(79) The Commission takes the view that Saint-Gobain will not have the ability to foreclose access to soda-lime glass to the JV's competitors.

(80) In the event a TAG manufacturer wanted to start developing a TAG-based automotive solution and needed to source soda-lime glass as an input, then it could approach a number of alternative suppliers. Notwithstanding the relatively high market share of Saint-Gobain in number of operating floats (8) ([20-30]% in 2015) and in terms of sales of automotive glass ([40-50]% in 2015 and [40-50]% in both 2014 and 2103) (9), there are a number of other competitors with significant market shares.

(81) In light of the above the Commission considers that Saint-Gobain will not have the ability to restrict access to soda-lime glass to the JV's competitors.

5.3.1.3. Likely impact on effective competition

(82) The Commission takes the view that, even in the event that the Proposed Transaction would allow the Parties to foreclose access to TAG to the JV's downstream competitors, the Proposed Transaction will not have an impact on effective competition for the reasons explained below.

(83) The Commission considers that other technical solutions, alternative to TAG-based automotive glazing solutions, currently being developed by automotive glass manufactures, will pose a significant competitive constraint on the JV and will not require TAG for their development.

(84) The business rationale underlying the decision of the Parties to start the joint development of a TAG-based automotive glazing solution is to address the need of car manufacturers for weight saving in the vehicle architecture. Car manufacturers, in fact, will need to achieve higher fuel efficiencies for the vehicles they produce, and weight savings are one of the paths followed to achieve such targets. In order to achieve the required overall weight savings on each vehicle, car manufacturers are pushing for weight savings on the components including on windshield and glazing. Therefore, the development of the TAG-based glazing solution is one way among others of trying to obtain weight-saving in the automotive industry.

(85) Since weight-saving is the main goal to be reached, automotive glass manufacturers and OEMs are currently looking at several technical solutions to achieve them. [Details on development project].

(86) The market investigation indicated that alternative solutions to TAG-based solutions exist or are under development and indicated not only thin soda-lime laminates as a viable option but also Soda Lime single ply outer laminated with PVB to a PET film with scratch-resistant hard coating as another solution.

(87) Competitors of Saint-Gobain contacted in the course of the market investigation indicated that they are developing other solutions, not necessarily based on TAG, to respond to the push from OEMs for lighter glazing solutions and some others indicated that development will soon start.

(88) At this stage, the TAG-based automotive glazing solution is still under development and whether this solution will be successful and widely adopted by the OEMs is uncertain at this stage. The same applies for the alternative solutions currently being developed, or which will soon be developed, by the JV's competitors.

(89) Not only it is not certain whether TAG-based glazing solutions will be the only viable, or economically more attractive, light weight solution or whether other solutions developed by competitors will prove more attractive to OEMs but competitors will also all deploy significant efforts to develop and promote their own solution. This will put them in direct competition with the JV during this development phase.

(90) Also, it is not certain that only one technical solution will finally be marketed. Therefore, it is possible that once the development phase is over, different technical solutions will be competing with that of the JV for the future business opportunities.

(91) The Commission therefore takes the view that the JV will face significant competition from the development of alternative automotive glazing solutions not requiring TAG as an input product.

(92) In light of the existence of the above mentioned alternative solutions, the Commission takes the view that is likely that, in the future, neither of the Parties will be a necessary or unavoidable upstream supplier for the JV's competitors. Therefore, the Parties will not have a significant role on the competitive dynamics of the downstream market. Hence, the Proposed Transaction will not allow the Parties to increase the cost of downstream rivals and therefore will not lead to an upward pressure on the (future) sales price.

(93) The Commission also takes the view that the alternative technical solutions under development indicate that access to and IPR related to TAG can be avoided in the development of a lightweight glazing solution. Therefore, the strong position of the Parties on the input market and their IPR portfolio will likely not represent an impediment to the JV's competitor to develop and market their product offering as they can rely on different technological solutions requiring different IPRs. Hence, the Commission concludes that the cooperation between the Parties will not increase barriers to entry on the (future) downstream market where the JV will be active.

5.3.1.4. Conclusion

(94) In light of all the above, the Commission considers that input foreclosure can be excluded with regard to the vertical relationship between the upstream manufacture of TAG and automotive flat glass and the downstream manufacture of TAG-based automotive glazing solutions.

(95) Also, in the event that an input foreclosure was to happen, the Commission takes the view that it will not have an impact on effective competition.

5.3.2. Horizontal non-coordinated effects

(96) If TAG-based automotive glazing solutions, and all lightweight automotive glazing solutions to be developed, were to be considered as part of a broader product market encompassing all automotive glass, then the Proposed Transaction could in the future give rise to a horizontally affected market.

(97) Under this framework of analysis, in fact, the JV will be competing on the same market as Saint-Gobain, albeit with a different value proposition compared to that currently offered by the latter.

(98) On this market, Saint-Gobain has a significant market share but the combined entity will face competition from a number of other credible competitors (Asahi, Pilkington, Fuyao, Trakya). (10)

(99) If limiting the analysis to only traditional glazing solutions, OEMs can easily switch supplier when new vehicle models are developed. If upcoming lightweight automotive glazing solutions are taken into account, it is likely that at least some of Saint-Gobain's competitor will develop a solution which will eventually reach the market. Hence, OEMs will likely also have the opportunity to switch suppliers of lightweight automotive glass.

(100) In light of the above, the Commission considers that the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market with regard to the markets for automotive glass in the EEA.

6. CONCLUSION

(101) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No 130, 13/04/2016, p. 10.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 COMP/M.4173 - NIPPON SHEET GLAS / PILKINGTON.

6 Europe, Middle East and Africa.

7 See para 59 above.

8 According to the Parties, market share in number of floats is a good proxy for market share in volume.

9 All market share reported are calculated at EEA level

10 For market share figures, please refer to the table in pare 73 above. At this stage it in not possible to estimate which will be the JV's market share in the future.