Commission, December 16, 2015, No M.7839

EUROPEAN COMMISSION

Judgment

OUTOKUMPU / HERNANDEZ EDELSTAHL

Dear Sirs,

Subject: Case M.7839 - Outokumpu / Hernandez Edelstahl

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

(1) On 16 December 2015, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the undertakings Outokumpu Nirosta GmbH, part of the Outokumpu Group (‘Outokumpu’, Finland), and Hernandez Beteiligungs GmbH (‘Hernandez Beteiligungs’, Germany) acquire within the meaning of Article 3(1)(b) of the Merger Regulation joint control of the undertaking Hernandez Edelstahl GmbH (‘Hernandez Edelstahl’, Germany), by way of acquisition of shares. Outokumpu, Hernandez Beteiligungs and Hernandez Edelstahl are hereinafter collectively referred to as the ‘Parties’. (3)

1. THE PARTIES

(2) Outokumpu is active in the production, sale and distribution of a wide range of stainless steel products.

(3) Hernandez Beteiligungs is a holding and share management company.

(4) Hernandez Edelstahl distributes cold and hot rolled flat stainless steel products and stocks quarto plates.

2. THE OPERATION

2.1. Legal framework: types of control

(6) Control is defined by Article 3(2) of the Merger Regulation as the possibility of exercising decisive influence on an undertaking. Article 3(2) further provides that the possibility of exercising decisive influence on an undertaking can exist on the basis of rights, contracts or any other means, either separately or in combination, and having regard to the considerations of fact and law involved. The clearest form of joint control exists where there are two parent companies which share equally the voting rights in the joint venture, or where, in the event of unequal shares, the minority shareholder is able to exercise veto rights over strategic decisions of the joint venture. However, the Jurisdictional Notice explains, at paragraphs 20 and 78, that ‘[p]urely economic relationships may play a decisive role for the acquisition of control. In exceptional circumstances, a situation of economic dependence may lead to control on a de facto basis where, for example, very important long-term supply agreements or credits provided by suppliers or customers, coupled with structural links, confer decisive influence’. In particular, this might give rise to de facto joint control ‘where there is high degree of dependency of a majority shareholder on a minority shareholder’.

2.2. Structure of the transaction – no de jure control

(5) The proposed transaction is borne out of […]. Outokumpu is one of Hernandez Edelstahl’s primary suppliers satisfying over […]% of its demands. Outokumpu is also Hernandez Edelstahl’s main creditor representing close to […]% of Hernandez Edelstahl’s total debts. The remaining creditors are […].

(6) In light of […] agreed between the creditors and Hernandez Edelstahl’s owners, […] (a) transferral of 33.3 % of shares in Hernandez Edelstahl to Outokumpu (4), (b) obligatory purchasing quantities […], (c) agreed repayment […] to Outokumpu by […], (d) grant of a limited purchase option to Outokumpu to acquire the remaining shares (‘Option Shares’) in Hernandez Edelstahl on six months' notice, subject to a specific price mechanism (the ‘Option’).

(7) The Option is granted to Outokumpu by Hernandez Beteiligungs. In this regard, as part of the arrangement, shares held in Hernandez Edelstahl not transferred to Outokumpu and not currently held by Hernandez Beteiligungs will be transferred to Hernandez Beteiligungs. Outokumpu and Hernandez Beteiligungs will thus become the sole shareholders in Hernandez Edelstahl following the transaction.

(8) To guarantee the exercise of the Option, the Option Shares are assigned to Outokumpu. Outokumpu, however, will contractually be barred from exercising the voting rights associated with the Option Shares. Those voting rights will instead be exercised by Hernandez Beteiligungs acting as a representative who is not bound by instructions. If by 1 January 2023 Outokumpu will not have exercised the Option, the Option Shares will revert to Hernandez Beteiligungs.

(9) Following the transaction, Outokumpu will vote with 33.3% of the shares while Hernandez Beteiligungs will vote with 66.7% of the shares. Outokumpu will not be granted any formal veto rights in Hernandez Edelstahl. The casting vote in Hernandez Edelstahl’s advisory board, which enjoys powers in matters related to the nomination of senior management and the adoption of business plan, will be held by the chairman who is nominated by Hernandez Beteiligungs.

(10) Therefore, Outokumpu does not exercise de jure control of Hernandez Edelstahl.

2.3. Outokumpu will have de facto joint control over Hernandez Edelstahl

(11) Hernandez Edelstahl is economically dependent on Outokumpu […]. Outokumpu currently satisfies more than […] of Hernandez Edelstahl’s demand for steel products, and […] imposes an obligation on Hernandez Edelstahl to purchase a minimum share ranging from […] to […] of its total requirements from Outokumpu. Outokumpu also is – and will remain – Hernandez Edelstahl’s primary creditor following the transaction.

(12) Moreover, Hernandez Beteiligungs’ ability to exercise its casting vote in Hernandez Edelstahl’s advisory board will be compromised by the proposed transaction: If Hernandez Edelstahl exercises its casting vote to force through a matter of strategic importance against Outokumpu's wishes, Outokumpu could exercise the Option, which would result in Hernandez Beteiligungs losing control of Hernandez Edelstahl. The risk of losing control over Hernandez Edelstahl is likely to limit Hernandez Beteiligungs’ ability to make use of its casting vote. Even if the Option is subject to a six-month notice period, such a period would not render it unfeasible for Outokumpu to exercise the Option given that strategic decisions, such as a budget and business plan, govern normally the longer-term strategy of a company.

(13) Furthermore, the pricing mechanism under which Outokumpu could acquire the shares under the Option means that there will not be significant financial barriers to dissuade Outokumpu from exercising the Option. In light of the evidence available to the Commission, the purchase price for exercising the Option is likely to be low compared to the overall credit exposure of Outokumpu vis-à-vis Hernandez Edelstahl, possibly significantly less than Hernandez Edelstahl’s actual value at the moment that the Option is exercised. In addition, given Outokumpu’s financial resources, the purchase price is not likely to constitute a significant impediment to the exercise of the Option by Outokumpu. As a consequence, even if the exercise of the Option could not be immediate, it would be a reasonable step for Outokumpu and could cause significant economic losses for Hernandez Beteiligungs, as it might lose all control over Hernandez Edelstahl without getting a price corresponding to its full value at the moment when the Option is exercised.

(14) In light of the above and based on the evidence available to the Commission, Outokumpu exercises de facto joint control over Hernandez Edelstahl with Hernandez Beteiligungs.

3. UNION DIMENSION

(15) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (5). Each of them has a Union-wide turnover in excess of EUR 250 million, but they do not achieve more than two-thirds of their aggregate Union- wide turnover within one and the same Member State. The notified operation therefore has a Union dimension.

4. ASSESSMENT

4.1. Introduction

(16) Outokumpu and Hernandez Edelstahl are both active in the distribution of stainless steel flat products through steel service centres (‘SSCs’). Outokumpu is also active in the production and supply of stainless steel flat products, an activity that is upstream of the distribution of those products.

(17) The proposed transaction gives rise to horizontally affected markets in the distribution of stainless steel flat products (excluding quarto plates) through SSCs in Austria and Hungary (6). In addition, the proposed transaction also gives rise to a vertically affected market between Outokumpu’s production and supply of stainless steel flat products in the EEA and the Parties’ downstream distribution of such products.

4.2. Relevant market definitions

4.2.1. Product markets

Production level

(18) The Commission has in its case precedents constantly distinguished steel products based on the one hand on the chemical composition of the steel (metallurgical characteristics) and on the other hand on the physical shape of the products.

(19) Based on the chemical composition, the Commission has distinguished four broad categories of steel products: (i) carbon steel, (ii) stainless steel, (iii) specialty steels and (iv) electrical steel. (7) The present case only concerns stainless steel.

(20) Stainless steel is a steel alloy with a minimum content of 10.5% chromium and a maximum of 1.2% carbon. It is an intermediate product between carbon steel (carbon- based steel not containing nickel or other alloys) and high performance alloys. Its main properties include the resistance to corrosion. (8)

(21) As to the physical shape of products, the Commission has distinguished between long products and flat products in previous cases. That distinction also applies to stainless steel. Within flat stainless steel products, the Commission has further distinguished between (i) hot-rolled and (ii) cold-rolled steels, each of which is the result of a specific production process. (9)

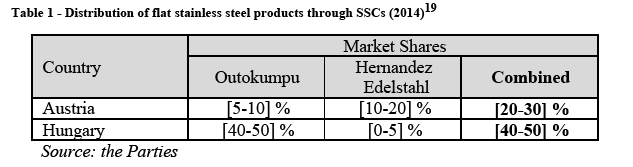

(22) The Parties do not contest those outlined market definitions applied by the Commission in previous cases.

(23) As regards hot-rolled products, a potential segmentation between hot black band (‘HBB’) and hot white band (‘HWB’) was considered in the Outokumpu/Inoxum case, but the precise market definition was ultimately left open. (10) As regards cold-rolled products, the Commission concluded in Outokumpu/Inoxum that the relevant product market was the overall market for the production and supply of cold-rolled flat products, excluding precision strip, though it also considered the potential distinction between bright annealed and not bright annealed products. (11)

(24) It is not necessary to conclude on the exact product market definition as the proposed transaction does not give rise to serious doubts about its compatibility with the internal market and the functioning of the EEA agreement under any alternative market definition.

Distribution level

(25) The Commission has considered in previous cases that the distribution of stainless steel products forms a separate market from the production and direct (ex-works) sales of those products. (12) The Parties agree with this distinction.

(26) As to the distribution sales, the Commission has in recent cases considered possible delineation of the market according to the categories of products sold and the service level offered into (i) stainless steel service centres (‘SSC’), (ii) stockholding centres/stockists and (iii) oxy-cutting centres (which only distribute quarto plates). However, the Commission has ultimately left the exact market definition open. (13)

(27) Outokumpu submits that there is an overall market for the distribution of stainless steel products, with exception of the distribution of quarto plates, which it considers to be a separate market. However, the Parties have provided market information on the basis of the narrowest feasible market definition, including the distribution of flat stainless steel products through SSCs (excluding quarto plates). The proposed transaction only gives rise to affected markets under this narrowest market definition.

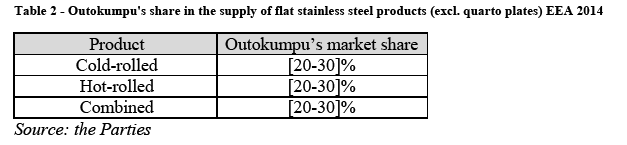

(28) The results of the market investigation generally indicate that that there is some though limited substitutability between SSCs and other distribution channels. (14)

(29) It is not necessary to conclude on the exact product market definition as the proposed transaction does not give rise to serious doubts about its compatibility with the internal market and the functioning of the EEA agreement under any alternative market definition.

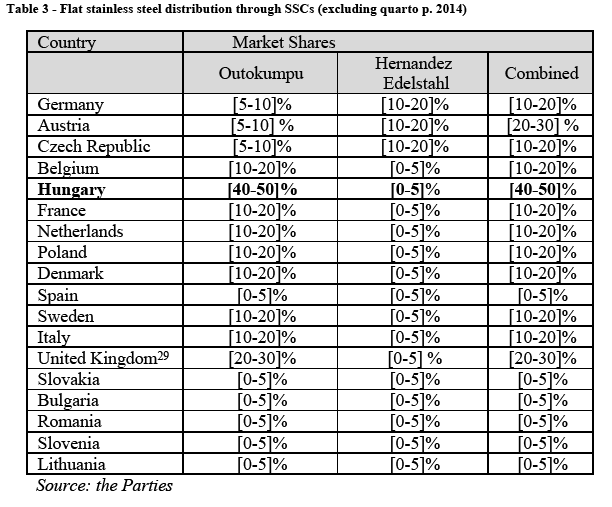

4.2.2. Geographic markets

Production level

(30) The Commission found in Outokumpu/Inoxum that the market for the production and supply of flat stainless steel products is EEA-wide. (15)

(31) The Parties submit that the production markets are at least EU/EEA-wide.

(32) The results of the market investigation support the view that distributors can source flat stainless steel products from suppliers located anywhere in the EEA. (16) For the purposes of the present case, the Commission did not investigate whether the markets could be wider than the EEA.

(33) It is not necessary to conclude on the exact geographic market definition as the proposed transaction does not give rise to serious doubts about its compatibility with the internal market and the functioning of the EEA agreement under any alternative market definition.

Distribution level

(34) The Commission has in previous cases considered the distribution markets to be at least national if not cross-border regional. (17)

(35) The Parties are of the view that the distribution markets are at least national.

(36) The results of the market investigation indicate that there are some distribution flows across national borders. Nonetheless, some market participants considered, for instance transport costs to be prohibitive for sourcing from neighbouring countries. (18) The proposed transaction only gives rise to affected markets if the distribution markets are considered national.

(37) It is not necessary to conclude on the exact geographic market definition as the proposed transaction does not give rise to serious doubts about its compatibility with the internal market or the functioning of the EEA Agreement under any alternative geographic market definition.

4.3. Competitive assessment

4.3.1. Horizontal effects: distribution of flat stainless steel products

(38) According to the Parties, Hernandez Edelstahl operates a steel service centre in Germany (Hockenheim) through which it only sells flat stainless steel products. The activities of Hernandez Edelstahl overlap with Outokumpu’s distribution activities in Germany as well as in a number of other EEA-countries to which Hernandez Edelstahl exports products from Germany.

(39) The Parties submit that the proposed transaction does not give rise to competition concerns as the Parties’ combined market shares and market share increments remain low. Moreover, they submit that the Parties primarily target different customer groups: while Outokumpu sells a significant share of its distribution sales to end-users of flat stainless steel products, Hernandez Edelstahl mostly sells to other distributors.

(40) The Parties’ activities give rise to horizontally affected markets with respect to the distribution of flat stainless steel products (excluding quarto plates) through SSCs in the potential national markets of Austria and Hungary. The Parties’ market shares in those countries are given in Table 1 below.

(41) In Austria, the combined market share and market share increment will remain modest. A number of other competitors will also remain active in Austria, including Aperam ([10-20]%), Acerinox ([10-20]%) and Kreuer ([5-10]%). (20)

(42) In Hungary, the Parties will reach a combined market share of [40-50]% but the market share increment will be limited at only [0-5] percentage points. It is thus unlikely that the proposed transaction would significantly change the market structure in Hungary. (21) A number of competitors will also remain active in Hungary, including Aperam ([10-20]%), ThyssenKrupp ([5-10]%) and Italinox ([5-10]%). (22)

(43) The Commission has earlier found that barriers to entry and expansion in the distribution markets are moderate at most. (23) Besides, in the present case market participants have stated that SSCs competing with the Parties have excess capacity and could increase their sales, (24)

(44) The results of the market investigation show that market participants do not consider Outokumpu and Hernandez Edelstahl to be each other’s closest competitors. (25) The replies do not point towards any significant competition concerns related to horizontal effects. (26) Particularly with respect to Hungary, market participants have indicated that Hernandez Edelstahl only has a very limited presence there. (27)

(45) Therefore, the Commission concludes that the proposed transaction does not give rise to serious doubts about its compatibility with the internal market and the functioning of the EEA Agreement.

4.3.2. Non-horizontal effects

(46) The proposed transaction gives rise to a vertically affected market between (i) Outokumpu’s supply of flat stainless steel products and (ii) the Parties’ activities in the distribution of such products.

(47) Upstream, Outokumpu’s market share on the supply of stainless steel flat products in the EEA remains below 30% as illustrated in Table 2 below. (28)

(48) Competitors active in the supply of flat stainless steel products in the EEA include undertakings such as Aperam, ThyssenKrupp/AST and Acerinox.

(49) Downstream, only at a potential national market the Parties reach a combined market share above 30%, namely in Hungary. The Parties achieved a combined market share of [40-50]% in Hungary in 2014. The Parties’ combined market shares in Member States where Hernandez Edelstahl made sales in 2014 are presented in Table 3 below.

(50) A vertical link can give rise to two types of foreclosure issues: input foreclosure and customer foreclosure. The former is where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input. The latter is where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base. (30)

(51) In assessing a foreclosure scenario, the Commission takes into account fist the ability of the merged entity to substantially foreclose its rivals, second, whether it would have the incentive to do so, and third, whether a foreclosure strategy would have a significant detrimental effect on competition and consumers downstream. (31)

(52) The Parties submit that the merged entity would not have the ability or incentive to engage into input or customer foreclosure. They further argue that, even if they tried to engage in such behaviour post-transaction, adequate competition would remain and downstream competition would not be substantially jeopardised.

Input foreclosure

(53) As to the ability of the merged entity to foreclose its downstream rivals in Hungary (or elsewhere in the EEA), the Commission notes that Outokumpu’s market shares in the upstream market remain below 30%. They are as such not an indication of particularly significant market power on those markets. The proposed transaction also does not strenghten Outokumpu’s position upstream and, therefore, does not enable it to foreclose its downstream rivals in a way it could not already do prior to the transaction.

(54) During the market investigation, a limited number of distributors referred to Outokumpu being strong in some high-end grades of cold-rolled stainless steel products and suggested that the transaction could therefore give rise to negative effects. However, a clear majority of distributors, including SSCs, sourcing from Outokumpu and/or Hernandez Edelstahl indicated that they could find alternative suppliers such as Aperam, ThyssenKrupp, Acerinox or Marcegaglia. (32) Moreover, even some of those market participants that did refer to Outokumpu’s particular strengths, mentioned that other suppliers were innovative as well and that the market was dynamic. (33) The Commission has also previously explicitly ruled out the need to segment the market according to grades or between commodities and specialities. (34)

(55) Concerning the incentive to foreclose, foreclosing third-party distributors from access to Outokumpu’s steel would likely result in Outokumpu suffering some lost sales at the upstream level as the number of and geographic coverage of SSCs selling its products would be limited. For a foreclosure strategy to be profitable for Outokumpu, it would need to be able to recoup those losses through increased sales through its own distribution network, including Hernandez Edelstahl.

(56) It appears unlikely that Outokumpu could recoup the losses it would make on the upstream market as a result of foreclosure strategy as a number of competitors will remain both up- and downstream. Outokumpu would also need to bear the losses generated on the upstream market alone while it would need to share the potentially increased profits made at Hernandez Edelstahl with Hernandez Beteiligungs.

(57) It therefore appears unlikely that the acquisition of an SSC whose market share in the downstream market is modest at best would significantly change Outokumpu’s incentives of selling its flat stainless steel products to other SSCs.

(58) Lastly, it appears unlikely that an attempted foreclosure by Outokumpu would significantly harm competition as a number of credible competitors will remain both up- and downstream and customers would continue to have access to flat stainless steel products at the distribution level through various sources.

Customer foreclosure

(59) When analysing the likelihood of customer foreclosure, it should be borne in mind that flat stainless steel products are, at the upstream level, traded on at least an EEA- wide market where Hernandez Edelstahl only represents a small share of the total demand. To add, Outokumpu is already Hernandez Edelstahl’s clearly biggest supplier and satisfies up to […] % of all Hernandez Edelstahl’s current demand. That share has lately been on the increase, […]. (35) Outokumpu also already supplies Hernandez Edelstahl with the widest product portfolio of any of its suppliers, being the sole supplier for some types of products. Hernandez Edelstahl is therefore at present not a significant customer to any of the other stainless steel manufacturers at the EEA-level.

(60) Following the proposed transaction, a number of alternative distributors for stainless steel flat products would remain, including both the manufacturers’ own distribution arms as well as third-party distributors. The Commission has also earlier found that barriers to entry and expansion in the distribution markets are moderate at most. (36) Moreover, in the present case, market participants have indicated that SSCs competing with the parties have excess capacity and could increase their sales. (37)

(61) Producers of flat stainless steel products would therefore continue to have access to a number of alternative customers. This finding was also supported in the market investigation where the majority of the respondents indicated that there are enough alternative distributors for stainless steel products of Outokumpu’s upstream competitors. (38)

(62) The submitted internal documents of Outokumpu and the agreements (39) support the view that Hernandez Edelstahl would continue to distribute products from suppliers other than Outokumpu as well. While the agreements oblige Hernandez Edelstahl to source a minimum share of its total requirements from Outokumpu, that share is below Outokumpu’s present share. The obligatory purchase share for the benefit of Outokumpu shall also gradually decrease in the years following the proposed transaction. (40) Moreover, the internal documents of Outokumpu estimate that the actual sourcing share from Outokumpu by Hernandez Edelstahl will not be significantly higher than the obligatory sourcing share and that it would be below the present sourcing share. (41)

(63) Finally, it is unlikely that any attempted customer foreclosure by the merged entity would significantly harm customers of flat stainless steel products as a number of alternative distributors will remain. Should Hernandez Edelstahl stop distributing the products of Outokumpu’s upstream rivals, customers could turn to alternative distributors to get such supplies and to have another source if Outokumpu attempted to raise prices significantly.

Conclusion on non-horizontal effects

(64) In light of the above and the evidence available to it, the Commission concludes that the proposed transaction does not give rise to serious about its compatibility with the internal market and the functioning of the EEA due to non-horizontal effects.

5. CONCLUSION

(65) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (‘the Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p.3 (‘the EEA Agreement’).

3 Publication in the Official Journal of the European Union, OJ C388, 21.11.2015, p. 18.

4 The shares will be transferred to Outokumpu Nirosta GmbH, part of the Outokumpu Group.

5 Turnover calculated in accordance with Article 5 of the Merger Regulation.

6 Furthermore, the Parties have a combined market share of [20-30]% (2014) in the United Kingdom. That market share is nonetheless fully due to Outokumpu’s sales there, Hernandez Edelstahl having made only […] tonnes of sales in 2014 in a market the Parties estimate to be […] tonnes. In light of this, the horizontal overlap is not discussed further in this decision.

7 See, for instance M.7155 – SSAB / Rautaruukki, paragraphs 22 and 25; M.7138 – ThyssenKrupp / Acciai Speciali Terni / Outokumpu VDM, paragraph 7; and M.6741 – Outokumpu / Inoxum, paragraphs 116–7.

8 See, for instance M.6471 – Outokumpu / Inoxum, paragraphs 47–51.

9 See, for instance M.7138 – ThyssenKrupp / Acciai Sepciali Terni / Outokumpu VDM, paragraphs 7–9; and M.6471 – Outokumpu/Inoxum, paragraphs 126–9 and 209.

10 M.6471 – Outokumpu/Inoxum, paragraph 136.

11 M.6471 – Outokumpu/Inoxum, paragraph 209. Hernandez Edelstahl does not distribute precision strip.

12 See, for instance M.7138 – ThyssenKrupp / Acciai Sepciali Terni/ Outokumpu VDM, paragraphs 10–1; and M.6471 – Outokumpu / Inoxum, paragraphs 214 and 221.

13 See, for instance M.7138 – ThyssenKrupp / Acciai Sepciali Terni/ Outokumpu VDM, paragraphs 12–5; and M.6471 – Outokumpu/Inoxum, paragraphs 215–231.

14 Replies to questions 4 and 5 of Q1 – Questionnaire to stainless steel suppliers, and replies to questions 4 and 5 of Q2 – Questionnaire to distributors of stainless steel. A great majority of suppliers and distributors pointed out that SSCs – in contrast to steelworks – offer shorter lead times, additional processing possibilities and deliver smaller volumes, however at higher price levels.

15 M.6471 – Outokumpu/Inoxum, paragraphs 238–243 and 260. See also, for instance M.7138 – ThyssenKrupp / Acciai Speciali Terni / Outokumpu VDM, paragraph 16.

16 Replies to question 6 of Q1 – Questionnaire to stainless steel suppliers, and replies to question 6 of Q2 – Questionnaire to distributors of stainless steel.

17 See, for instance M.7138 – ThyssenKrupp / Acciai Speciali Terni / Outokumpu VDM, paragraphs 18–9, and M.6471 – Outokumpu/Inoxum, paragraphs 274–7.

18 Replies to question 8 of Q2 – Questionnaire to stainless steel distributors.

19 Market shares are the Parties’ best estimates that are based on the Parties’ actual sales figures and publicly available data on total market sizes.

20 Market shares are the Parties’ best estimates for 2014.

21 In Outokumpu / Inoxum, that Commission noted that the geographic market was likely wider than Hungary. That would only dilute the parties’ combined market share. See, M.6471 – Outokumpu / Inoxum, paragraph 935. In the present case, some German SSCs also replied they could serve Hungary from Germany, see replies to question 7 of Q2 – Questionnaire to distributors of stainless steel flat products.

22 Market shares are the Parties’ best estimates for 2014.

23 See, for instance M.7138 – ThyssenKrupp / Acciai Speciali Terni / Outokumpu VDM, paragraph 38.

24 See, for instance confirmed minutes of a conference call on 1 December 2015 with a distributor that indicated that competitors could easily make up Hernandez Edelstahl’s volumes in full..

25 Replies to questions 8 and 9 of Q1 – Questionnaire to stainless steel suppliers; questions 11 and 12 of Q2 – Questionnaire to distributors of stainless steel flat products; and questions 7 and 8 of Q3 – Questionnaire to customers of SSCs for flat stainless steel products.

26 See, for instance replies to questions 12 and 13 of Q3 – Questionnaire to customers of SSCs for flat stainless steel products.

27 See confirmed minutes of a conference call on 30.11.2015 with a distributor.

28 The Parties have confirmed that Outokumpu’s market share are similar to the figures given herein in any of the potential sub-segments of hot rolled and cold rolled flat stainless steel products that Hernandez Edelstahl distributes.

29 Hernandez Edelstahl made sales of only […] tonnes of sales in 2014 in the UK distribution market, which the Parties estimate to be […] tonnes.

30 See, for instance paragraph 30 of the Commission Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 265, 18.10.2008, p. 7 (‘Non-Horizontal Guidelines’).

31 See, for instance paragraphs 32 and 59 of the Non-Horizontal Guidelines.

32 See, for instance replies to questions 15 and 18 of Q2 – Questionnaire to distributors of stainless steel flat products, and minutes of a phone call with an SSC on 30 November 2015.

33 See, for instance minutes of a phone calls with distributors on 30 November 2015.

34 See M.6471 – Outokumpu / Inoxum, paragraphs 173 and 209.

35 In 2014, Outokumpu satisfied above […] % of Hernandez Edelstahl's total demand. Other suppliers in 2014 included […] and […].

36 See, for instance M.7138 – ThyssenKrupp / Acciai Speciali Terni / Outokumpu VDM, paragraph 38.

37 See, for instance confirmed minutes of a conference call on 1 December 2015 with a distributor that indicated that competitors could easily make up Hernandez Edelstahl’s volumes in full...

38 See, for instance replies to question 11 of Q1 – Questionnaire to stainless steel suppliers.

39 See Annexes 5.1–5.4d to the Form CO.

40 See Section 2.2

41 See, for instance document titled […], pages 10–1 and 26, where the actual share of sourcing is estimated at […]% by 2018.