Commission, May 26, 2016, No M.7877

EUROPEAN COMMISSION

Judgment

WARBURG PINCUS / GENERAL ATLANTIC / UNICREDIT / SANTANDER / SAM / PIONEER

Dear Sir/Madam,

Subject: Case M.7877 - WARBURG PINCUS / GENERAL ATLANTIC / UNICREDIT / SANTANDER / SAM / PIONEER

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

(1) On 15 April 2016, the European Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which affiliates of Warburg Pincus (“Warburg Pincus”, United States), General Atlantic LLC (“General Atlantic”, United States), Banco Santander, S.A., ("Santander", Spain) and Unicredit S.p.A. ("UniCredit", Italy) combine the asset management businesses of SAM Investment Holdings Limited (“SAM”) and Pioneer Global Asset Management S.p.A. (together with its subsidiaries, but excluding Pioneer Investment Management USA Inc. and its US subsidiaries as well as certain of its other subsidiaries (“Pioneer”)), in a joint venture controlled by Warburg Pincus, General Atlantic, Santander and UniCredit (the "JV"). SAM is currently a joint venture between Santander and affiliates of Warburg Pincus and General Atlantic. Pioneer is currently solely controlled by UniCredit. (3)

(2) Warburg Pincus, General Atlantic, Santander and UniCredit are designated hereinafter as the 'Parties'.

1. THE PARTIES

(3) Warburg Pincus is a member-owned global private equity firm, active through its portfolio companies in a variety of sectors, including energy, financial services, healthcare and consumer, industrial and business services, and technology, media and telecommunications. Warburg Pincus is controlled by the individuals Charles R. Kaye and Joseph P. Landy. (4)

(4) General Atlantic is a member-owned private equity firm, active through its portfolio companies in a variety of sectors, including business services, retail and consumer, financial services, healthcare, internet and technology. […].

(5) Santander is the parent company of an international group of banking and financial companies operating mainly in Europe, the U.S., and Latin America. Santander is not controlled by any other undertaking.

(6) UniCredit is the Italian parent company of a banking group providing banking and financial services in Italy and abroad and is not controlled by any other undertaking.

(7) SAM is an asset management business with operations in Europe and Latin America. SAM is a joint venture between Warburg Pincus, General Atlantic and Santander. (5) SAM’s products are distributed through: (i) Santander’s retail banking network in different countries; (ii) Santander or SAM directly or through sub- advisors to institutional clients; and (iii) third parties, […]. SAM is a full function joint venture owned and controlled by Sherbrooke Acquisition Corp SPC (an investment vehicle jointly controlled by Warburg Pincus and General Atlantic) (“Sponsor Entity”) and Santander. (6)

(8) Pioneer is an asset management business with operations across Europe and in several non-European countries and it is a wholly-owned subsidiary of UniCredit. Pioneer is active in asset management through: (i) Pioneer Investment Management USA Inc. and its group in the U.S.; and (ii) direct and indirect subsidiaries (including joint venture arrangements in certain jurisdictions) in the rest of the world. The proposed transaction does not include Pioneer Investment Management USA Inc. and its US subsidiaries as well as certain of its other subsidiaries. These entities are part of a parallel transaction through which Warburg Pincus, General Atlantic and Unicredit acquire joint control over those entities. That parallel transaction was notified to the Commission separately and was approved unconditionally on 23 March 2016 (Case M.7874 – Warburg Pincus/General Atlantic/Unicredit/Pioneer US).

2. THE CONCENTRATION

(9) The proposed transaction comprises two stages:

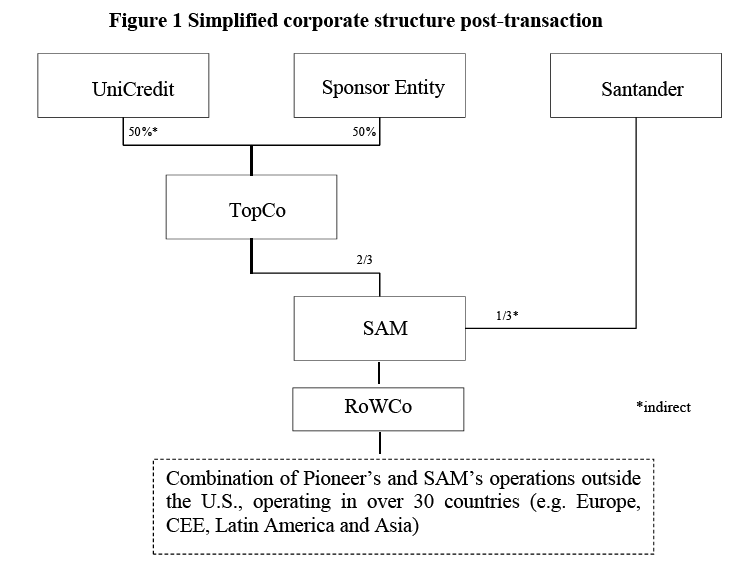

(10) In phase 1, Pioneer will be re-organised internally to separate the US business from the non-US business and certain out-of-scope entities. This includes the incorporation of two new companies (RoWCo and TopCo) with the aim that TopCo will hold the non-US entities of Pioneer through RoWCo.

(11) In phase 2, SAM will acquire 100% of the shares in RoWCo from TopCo in exchange for an issue of shares in SAM to TopCo and cash consideration. As a result, TopCo will hold 1/3 of the shares in SAM. Further, the Sponsor Entity will acquire shares in TopCo in exchange for 100% of its interest in SAM. The Sponsor Entity will then subscribe for additional shares in TopCo in order that it holds a 50% interest in TopCo. The acquisition of the Sponsor Entity’s interest in SAM by TopCo will increase TopCo’s interest in SAM to 2/3. Ultimately, and as set out in Figure 1, Santander, Unicredit and the Sponsor Entity will each indirectly hold 1/3 of the shares in SAM and RoWCo.

(12) As a result, the non-US business of Pioneer and the business of SAM will ultimately be jointly controlled by the Parties. […] each of the Parties will be able to veto […], all of which constitute strategic commercial decisions conferring decisive influence over SAM in accordance with paragraph (69) of the Consolidated Jurisdictional Notice (7).

(13) Based on the information submitted by the Parties, SAM will manage its own portfolio, will act on its own behalf on the market and it will carry out its own sales and marketing functions and hence perform on a lasting basis all the functions of an autonomous economic entity.

(14) In particular, SAM will have a dedicated Board of Directors for its day-to-day operations comprising 11 directors, over 500 members of staff, access to independent financing as well as all assets and resources required to function independently on the market. It will continue its customer facing activities and its activities will go beyond one specific function within the Parties’ business activities as SAM will have its own access to and presence on the market.

(15) It is envisaged that, post-Transaction, Santander and UniCredit will distribute mutual funds created by SAM in certain EU jurisdictions. The Parties estimate that, on an EEA-wide basis, about […]% of SAM's asset management products will be distributed by either Santander or UniCredit. However these distribution relationships will be carried out […]. (8) Also, these relationships will not be exclusive since SAM will be able to appoint third party distributors.

(16) On this basis, the proposed transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(17) Based on the principle to look at the “economic reality of the operation to determine which are the undertakings concerned” laid down in paragraph (145) the Consolidated Jurisdictional Notice, SAM's parent companies should be considered as the real drivers behind the operation due to their significant involvement in the initiation, organization, and financing of the operation. Based on the same principle, the Sponsor Entity's parent companies should be considered as the undertakings concerned since the Sponsor Entity is merely an investment vehicle. Accordingly, each of Warburg Pincus, General Atlantic, Santander and UniCredit constitute undertakings concerned. However, the assessment of the EU dimension of the transaction would remain unchanged if, alternatively, SAM (instead of each of Warburg Pincus, General Atlantic and Santander) or the Sponsor Entity (instead of each of Warburg Pincus and General Atlantic) were to be considered undertakings concerned.

(18) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (9) (General Atlantic: EUR 3 797 million, Warburg Pincus: EUR 14 682 million, Santander: EUR 76 793 million, UniCredit: EUR 21 365 million). Each of them has an EU-wide turnover in excess of EUR 250 million (General Atlantic: EUR 471 million, Warburg Pincus: EUR 1 329 million, Santander: EUR […], UniCredit: EUR 20 108 million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. RELEVANT MARKETS

(19) The proposed transaction gives rise to horizontally affected national markets in Poland for:

(i) the provision of open retail mutual funds;

(ii) the provision of open retail money market funds; and

(iii) a possible product market comprising both these markets, namely the market for overall open asset management for retail clients.

(20) In Poland SAM is active in open asset management for retail clients by offering open retail mutual funds and open retail money market funds via BZ WBK Towarzystwo Funduszy Inwestycyjnych S.A. Pioneer offers both open retail mutual funds and open retail money market funds via Pioneer Pekao Towarzystwo Funduszy Inwestycyjnych S.A.

4.1. Overall open asset management for retail clients

4.1.1. Relevant product market

(21) In previous cases, the Commission considered that one may distinguish a relevant product market for (overall) asset management, including the creation and managing of mutual funds for retail clients, the tailor-made funds for corporate and institutional customers, and portfolio management for private investors, pension funds and institutions. (10) The Commission has, however left open the question of whether these individual products constitute separate relevant product markets, with the exception of portfolio management services (i.e. private banking), which have been considered a separate market. (11)

(22) The exact definition of the relevant product market can be left open as in all possible scenarios the proposed transaction does not raise serious doubts as to its compatibility with the internal market.

4.1.2. Relevant geographic market

(23) In previous decisions (12), the Commission considered that certain markets for asset management might be national and others EEA-wide/international in scope.

(24) The exact definition of the relevant geographic market can be left open as in all possible scenarios the proposed transaction does not raise serious doubts as to its compatibility with the internal market.

4.2. Sub-segments of open retail mutual funds and open retail money market funds

4.2.1. Relevant product markets

(25) In a previous case, the Commission found that there are separate markets for (i) open retail mutual funds, (ii) open retail money market funds and (iii) workplace savings schemes. The Commission found that mutual funds and money market funds constituted different markets because mutual funds are used for longer-term investments whereas money market funds are relatively short-term investment vehicles. (13)

(26) The exact definition of the relevant product market can be left open as in all possible scenarios the proposed transaction does not raise serious doubts as to its compatibility with the internal market.

4.2.2. Relevant geographic markets

(27) In a previous case, the Commission considered that the geographic scope of the markets for open retail mutual funds as well as for money market funds was national in scope. (14)

(28) The exact definition of the relevant geographic market can be left open as in all possible scenarios the proposed transaction does not raise serious doubts as to its compatibility with the internal market.

4.3. Possible additional segmentations

(29) The Commission has also discussed the possibility of further segmenting the markets for asset management for institutional clients and retail clients by type of management (active vs. passive). (15) Active asset management consists of strategies in which the investment manager makes specific investments with the goal of outperforming a benchmark, passive asset management consists of strategies which merely seek to replicate the performance of an index and rely more on technology. Passive asset management services therefore normally have lower management fees than active asset management services.(16)

(30) Furthermore, in a previous case the Commission discussed with respect to asset management in France whether products sold within a life insurance “envelope” should form part of the same product market as retail mutual funds sold on a standalone basis. (17)

(31) It can however be left open whether such further segmentations are warranted as even then the proposed transaction does not raise serious doubts as to its compatibility with the internal market.

5. COMPETITIVE ASSESSMENT

(32) The competitive assessment takes into account the affected markets, which are all located in Poland.

(33) For the affected markets in Poland, the Parties provided market share information on the basis of reports from the Polish Chamber of Fund and Asset Management (Izba Zarządzających Funduszami i Aktywami, "IZFiA") and taking into account their own revenues in each relevant market. The IZFiA data comprises the value of assets under management ("AuM") data reported by all Polish asset management companies concerning different asset management products and calculates the total size of the relevant type of asset management products and individual market shares. In the context of the market investigation, the market participants contacted confirmed that the IZFiA data, which the Parties submitted, as well as the corresponding market share information are reliable and provide an accurate indication of the Polish market.

(34) As regards the overall open asset management for retail clients in Poland, SAM and Pioneer had a combined market share of [20-30]% in 2014, measured on the basis of AuM in PLN. Post-transaction, the combined entity would be the largest operator in the Polish market in this segment. The next biggest operator would be PKO with a market share of [10-20]% (by AuM), followed by ING (now named NN) with a share of [10-20]% (by AuM), Union Investment with a share of [5-10]% (by AuM) and PZU with a share of [5-10]% (by AuM).

(35) As regards open retail mutual funds in Poland, SAM and Pioneer had a combined market share of [20-30]% (by AuM) in 2014. Post-transaction, the combined entity would be the largest operator in the Polish market in this segment. The next biggest operator would be ING with a share of [10-20]% (by AuM), followed by PKO with a share of [10-20]% (by AuM) and PZU with a share of [5-10]% (by AuM).

(36) As regards open retail money market funds in Poland, SAM and Pioneer had a combined market share of [20-30]% (by AuM) in 2014. PKO would have an almost identical share of [20-30]% (by AuM), followed by Union Investment with a share of [10-20]% (by AuM) and Millenium with a share of [0-5]% (by AuM).

(37) If further sub-segmentations of the relevant markets into active and passive asset management were to be made, the Parties' market shares would change only marginally as essentially all open retail mutual funds and open retail money market funds in Poland are active funds. No further affected markets would arise in this segment. The Parties' activities do not overlap in passive asset management and no affected markets would arise in respect of active asset management for institutional clients. Moreover, if products sold within a life insurance “envelope” were considered to form part of the same product market as retail mutual funds sold on a standalone basis, the situation would not change significantly.

(38) The Polish market in all of the affected markets is rather fragmented with a number of additional asset management companies present. A number of these operators are, like the Parties, vertically integrated, meaning that they are part of a larger banking group of companies acting as a distribution channel for asset management products.

(39) Moreover, new market entry occurred in the past years both by national and international players and future entry can be expected. According to the Parties, at least nine companies have entered one or more of the affected markets over the last five years, namely Agio Funds, Altus, Amundi, AXA, BGZ BNP Paribas, BPS, Caspar, EQUES Investments, and Open Finance. In addition, the Parties consider that Goldman Sachs could enter the affected markets, based on information provided in the press. Moreover, Franklin Tempelton and JP Morgan Asset management sell foreign-domiciled retail funds in Poland and both companies could apply for a license to set up a local branch.

(40) As a result, although SAM and Pioneer together would become the largest operator in the Polish market in all of those segments, there are currently no indications that the proposed transaction would result in a significant impediment to effective competition.

(41) The market participants contacted in the market investigation raised no specific concerns as regards the effect of the proposed transaction on competition in Poland. In particular, none of the customers contacted in the market investigation raised any concerns about the transaction.

(42) Likewise, competitors (18) indicated that the merged entity would continue to face competition from other operators, including strong vertically integrated entities.

(43) One of the contacted competitors mentioned that the combination of SAM's and Pioneer's activities may reduce access to distribution networks for independent asset managers (i.e., asset managers that are not part of a larger banking group). (19) However, the market investigation in the Polish market did not substantiate these concerns.

(44) Another contacted competitor stated that the proposed transaction would be unlikely to have significant foreclosure effects based on a possible limitation of access for independent asset managers to distribution networks, pointing out that SAM and Pioneer already distribute their products primarily through their respective own banking networks. (20) This competitor also stated that there are some banking networks in Poland, e.g. Citibank, Deutsche Bank, Raiffeisen, mBank or BÓS, which do not have their own investment fund providers and which therefore generally distribute the asset management products of other companies, including those of independent asset managers. (21)

(45) In light of all the evidence available to it, the Commission considers that the transaction is unlikely to result in foreclosure of independent asset managers or any other competition concerns.

6. CONCLUSION

(46) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 144, 23 April 2016, p. 21.

4 Mr Kaye and Mr Landy do not control any other undertakings outside of the Warburg Pincus group that are active in related businesses.

5 M.6971 – Warburg Pincus/General Atlantic/Santander/Santander Asset Management.

6 M.6971 – Warburg Pincus/General Atlantic/Santander/Santander Asset Management.

7 Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1), "CJN".

8 CJN, paragraph 98.

9 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

10 E.g. M.5384 – BNP Paribas/Fortis, para. 58; M.6812 – SFPI/Dexia, para. 31; M.5580 –

BlackRock/Barclays GIH, para. 9.

11 M.4844 - Fortis/ABN AMRO Assets, para. 68. Open funds do not have any restrictions on the number of investors, whereas closed funds are usually tailor-made for a small group of investors and are not distributed through retail channels.

12 E.g. M.3894 – UniCredito/HVB, para. 42; M.5384 - BNP Paribas/Fortis, para. 75; M.5580 –BlackRock/Barclays GIH, para. 14.

13 M.5728 – Crédit Agricole/Société Générale Asset Management, para. 58.

14 M.5728 – Crédit Agricole/Société Générale Asset Management, para. 84.

15 M.5580 – BlackRock/Barclays GIH, para. 10; M. 5341 – Allianz/Cominvest, para. 15. With respect to retail funds, this was left open.

16 M.5580 – BlackRock/Barclays GIH, footnote 6, and Case No. COMP/M.5728 – Crédit Agricole/Société Générale Asset Management, para. 35.

17 M.5728 – Crédit Agricole/Société Générale Asset Management, para. 82.

18 Confidential minutes of a telephone conference with a competitor of 3 March 2016.

19 Confidential minutes of a telephone conference with a competitor of 2 March 2016.

20 Confidential minutes of a telephone conference with a competitor of 3 March 2016.

21 Confidential minutes of a telephone conference with a competitor of 3 March 2016.