Commission, November 13, 2014, No M.7393

EUROPEAN COMMISSION

Judgment

ALBEMARLE/ ROCKWOOD

Dear Sir/Madam,

Subject:Case M.7393 – Albemarle/ Rockwood

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and article 57 of the EEA agreement

(1) On 9 October 2014, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Albemarle Corporation (Albemarle, US) acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of Rockwood Holdings, Inc. (Rockwood, US) by way of purchase of securities2, hereinafter referred to as "the proposed transaction" or the "Transaction". Albemarle and Rockwood are designated hereinafter as the "Parties".

1.THE PARTIES

(2) Albemarle is a global company which develops, manufactures and markets specialty chemicals across a diverse range of end markets including the petroleum refining, consumer electronics, plastics/packaging, construction, automotive, lubricants, pharmaceuticals, crop protection, food safety and custom chemistry services markets. Albemarle is headquartered in Baton Rouge, Louisiana in the United States, and listed on the New York Stock Exchange.

(3) Rockwood is a global company which develops, manufactures and markets specialty chemicals, in particular lithium and lithium compounds, and surface treatment technologies and solutions, such as corrosion protection/prevention oils and maintenance chemicals. Rockwood is headquartered in Princeton, New Jersey in the United States and listed on the New York Stock Exchange. In 2014, Huntsman Corporation acquired Rockwood's performance additives and titanium dioxide pigments businesses.3

2.THE OPERATION

(4) On 15 July 2014, Albemarle and Rockwood signed an Agreement and Plan of Merger under which Albemarle will acquire sole control of Rockwood. Albemarle Holdings Corporation, a wholly-owned subsidiary of Albemarle, will enter into a full merger with Rockwood, the remaining corporation following the merger (but still a subsidiary of Albemarle). Each outstanding share of Rockwood's share capital will be exchanged for cash and 0.4803 of an Albemarle share. As a result of this share exchange, post- transactions the existing Albemarle and the former Rockwood shareholders (which will become Albemarle shareholders) will own respectively 70% and 30% of Albemarle.

(5) Therefore the proposed transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 2 500 million (Albemarle: approximately EUR 2.0 billion, Rockwood: approximately EUR 1.0 billion)4. Each of them has a EU-wide turnover in excess of EUR 100 million (Albemarle: EUR […], Rockwood: EUR […]).

(7) In each of at least three Member States ([…]), the combined aggregate turnover of all the undertakings concerned is more than EUR 100 million (in […], Albemarle: EUR […], Rockwood: EUR […]; in […], Albemarle: EUR […….], Rockwood: EUR […]; in […], Albemarle: EUR […], Rockwood: EUR […]). In each of these countries each of them has a turnover in excess of EUR 25 million.

(8) The notified operation therefore has an EU dimension within the meaning of Article 1(3) of the Merger Regulation.

4. ASSESSMENT

(9) Albemarle and Rockwood have essentially complementary product portfolios with limited overlaps. Specifically, the Transaction gives rise to one horizontal overlap in specialty chemical catalysts, within the chemical family of magnesium-based organometallics.

(10) In addition, a number of vertical relationships arise as a result of the Transaction. These overlaps relate to different specialty chemicals that one Party produces and the other uses as input in the production of a variety of other chemicals:

·Albemarle produces hydrogen bromide (HBr), while Rockwood uses HBr to produce lithium bromide and caesium bromide;

·Albemarle produces potassium hydroxide (KOH), while Rockwood uses KOH to produce various types of cleaners (such as cleaners for the removal of phosphate layers regarding cold forming, for coil applications or used prior to metal pre-treatment);

·Rockwood produces butyllithium, while butyllithium is an input of Albemarle's production of different types of brominated flame retardants; and

·Rockwood produces various types of Grignard reagents, while Albemarle uses similar Grignard reagents to produce among others organoboron co- catalysts and pharmaceutical chemicals.

4.1.Horizontal effects

(11) Organometallic specialties5 are commonly used as catalysts or co-catalysts6 in a broad range of applications, including in the production of polymers (in particular polypropylene and polyethylene) or synthetic elastomers.

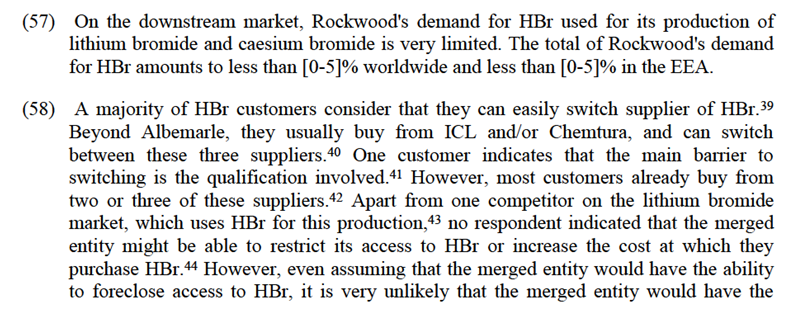

(12) The Parties produce organometallics based on different types of metal bases: aluminium-, magnesium- and zinc-based organometallics for Albemarle and lithium- and magnesium-based for Rockwood. The only overlap therefore arises in relation to magnesium-based organometallics. Within magnesium-based organometallics, both Parties are active in a product category called magnesium dialkyls. However, each Party produces different magnesium dialkyls: Albemarle produces n-butylethylmagnesium ("BEM") and Rockwood produces dibutylmagnesium ("DBM").

4.1.1.Product market definition

(13) This is the first time that the Commission has been called upon to analyse the markets for organometallics.

4.1.1.1. Organometallics

(14) Organometallic families based on different materials generally have different chemical properties and are used in different end-applications. However, some organometallics of different families can be used to produce similar downstream products. These are (i) lithium vs. aluminium-based organometallics used in the production of diene-based 3 elastomers; (ii) magnesium vs. aluminium vs. lithium alkylating agents in pharmaceutical applications; and (iii) magnesium vs. lithium metallating agents in pharmaceutical and/or agrochemical applications. Notwithstanding the similarities between the downstream products that can be produced using the organometallic families listed above, the Notifying Party considers that organometallic families based on different materials are not substitutable from a demand-side perspective. According to the Notifying Party, the reason for this is that even within an application where different organometallics can be used, the use of a different organometallic will result in an end product with different properties. Consequently, customer bases and applications of various organometallics are different.

(15) From a supply-side perspective, the Notifying Party considers that there is no substitutability between different organometallics, because the manufacturing processes, technical and safety requirements, know-how and skills required to produce specialty chemicals incorporating diverse metal bases are different.

(16) The results of the market investigation generally support the Notifying Party's view and indicate that organometallics based on different metal bases are overall not substitutable. More specifically, from a demand-side perspective, this is mainly because a change in the type of organometallics used would imply a different chemical process.7 Some customers, in particular manufacturers of pharmaceutical chemicals and of certain agricultural chemicals, also indicate that they cannot easily switch from one specific chemical to another because their manufacturing process was approved by regulatory authorities on the basis of a specific route of synthesis.8

(17) From a supply-side perspective, manufacturers who responded to the market investigation indicated that they often produce organometallics based on various types of metal bases.9 Nevertheless, in view of the large range of products comprised under organometallic chemicals, the equipment and manufacturing process used for the production of various types of organometallics is generally different and the ability of manufacturers to switch from one type of organometallic to another is overall limited.10

4.1.1.2. Magnesium dialkyls

(18) With regard to magnesium-based organometallics, i.e. the family in relation to which Albemarle and Rockwood overlap, a further distinction can be made between two functional product groups (i.e. chemicals undergoing similar chemical reactions): (i) magnesium dialkyls and (ii) Grignard reagents. Magnesium dialkyls are primarily used in the production of Ziegler-Natta catalyst systems for polyolefins and elastomers (i.e. for polymerisation), and can also be employed as alkylating agents in organic synthesis. Unlike magnesium dialkyls, Grignard reagents are not used for polymerisation applications, but in organic synthesis primarily in pharmaceutical applications, as well as agrochemical and electronic applications.

(19) Whilst both Parties are active in the manufacture and supply of magnesium dialkyls, only Rockwood is active in the manufacture and supply of Grignards. Therefore, for the purposes of analysing the horizontal effects of the proposed transaction, the following paragraphs focus on the magnesium dialkyls functional group only.

(20) Within the functional group of magnesium dialkyls there are a number of individual chemical products. Albemarle produces n-butylethylmagnesium ("BEM") while Rockwood produces dibutylmagnesium ("DBM"). The Notifying Party considers that BEM and DBM are poor substitutes for one another from a demand-side perspective. DBM is generally chosen over BEM to achieve certain highly specialised purposes such as specific polymer particle geometry, particle size or polymer molecular weight distribution, which only DBM can perform due to its particular characteristics. BEM is cheaper and due to its higher magnesium content it can be used in smaller quantities to achieve the same magnesium content in a catalyst.

(21) The Notifying Party also considers that there is limited supply-side substitutability between the magnesium dialkyls produced by each Party (BEM and DBM) due to differences in the manufacturing process and the equipment used. Regarding the manufacturing process, BEM requires an additive reducing viscosity, such as aluminium alkyls, which makes the product unsuitable for certain applications. While the production of both DBM and BEM requires the same main production equipment, the primary reactor, the Notifying Party indicates that the auxiliary equipment for purification, product isolation and raw material handling is different.

(22) The results of the market investigation generally supported the Notifying Party’s view as regards further segmentation of a market for magnesium dialkyls into BEM and DBM.

(23) Most customers of magnesium dialkyls who responded to the Commission's market investigation considered that there are no applications where BEM and DBM are substitutable.11 First, from a demand-side perspective, most respondents used only BEM or only DBM for their chemical process. Second, even though some customers acknowledged a degree of substitutability during their product development phase, they emphasized that once the production process is approved, switching would require time, qualification efforts and research and development efforts, which significantly limit the substitutability between them.12 Third, one customer that does purchase both products responded that the reactivity of both products in the chemical process is different for each product, and therefore they cannot be used interchangeably, while another confirmed the existence of a significant price difference between the two products.13 This lack of substitutability on the demand-side was also confirmed by one of the manufacturers that responded to the market investigation.14

(24) From a supply side perspective, the results of the market investigation indicated that generally a company which produces one of these two magnesium dialkyls would not be 5 able to adapt timely and at reasonable cost its manufacturing process in order to switch its production from BEM to DBM and vice versa.15

4.1.1.3.Conclusion

(25) In any event, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the product market for organometallics because even adopting the narrowest definition of the market on which there would be a horizontal overlap between the Parties' activities (i.e. a market for magnesium dialkyls) the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market.

4.1.2.Geographic market definition

4.1.2.1. Organometallics

(26) The Commission has previously considered that the relevant geographic market for some specialty chemicals is at least EEA-wide and may be global by virtue of low transport costs. The Commission has also taken a similar approach in respect of bulk chemicals by reason of the fact that manufacturers are active worldwide and typically ship their products across the world from centralised production facilities.16 The Notifying Party submits that the same reasoning should also apply with respect to organometallics.

(27) A large majority of respondents to the market investigation indicated that they either purchase organometallics from manufacturers located in the EEA or their purchasing pattern depends on the organometallics product concerned.17 In view of the variety of products considered under organometallics, some of these chemicals face limitations to transportation, in particular technical hurdles. For instance, several customers responded that the temperature sensitivity of some organometallics implies special treatment such as the need for a refrigerated storage or a short shelf life which limits the length of distribution. Other products are classified as hazardous products and are not easily transportable, require expensive, specialised containers, or face restrictions for shipping over sea.18 In addition, although prices of certain organometallics tend to be globally homogeneous, prices for other organometallics vary significantly between different world regions (such as EEA, USA or Asia) and can be impacted by the transport cost.19 6 Transport costs usually vary from 5% to 20% of the final price depending on the product.20

(28) In any event, the questions whether the market for organometallics and its respective sub-segments is national, regional, EEA-wide or wider can be left open since the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative geographic market definitions.

4.1.2.2.Magnesium dialkyls

(29) With respect to magnesium dialkyls, the Notifying party considers that the relevant geographic market is global or at least EEA-wide because the pricing of magnesium dialkyls is global and freight costs are low accounting for approximately 1-5% of the product price depending on destination. In addition, the Notifying Party submits that there are substantial trade flows across the regions, with the same major competitors being active at a global level and the same products being used worldwide. The Notifying Party gives the example that BEM is transported from Albemarle's production facility in Pasadena, Texas to customers in the EEA and worldwide in special portable tanks. These tanks can be loaded into shipping containers for transport by sea21 and transferred onto trucks on land.

(30) From a demand-side perspective, the market investigation indicated that customers buy a large part of their needs of magnesium dialkyls for their European activities in the EEA (often 100%, and all respondents more than 60%).22 Despite these purchasing patterns, respondents to the market investigation also indicate that there are few barriers to transportation of these products, neither technical, regulatory, nor any other trade limitation.23

(31) As to the supply side, although some competitors also sell part of their magnesium dialkyls production globally,24 they provided mixed replies as regards the ease with which magnesium dialkyls, and in particular BEM and DBM, could be transported.25

(32) In light of the above, and on the basis of the information available, the Commission considers that the market for magnesium dialkyls and its respective sub-segments is likely to be at least EEA-wide in scope. However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the geographic market, as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative geographic market definition.

Source: Form CO

(36) [Albemarle's market share decreased from 2012 to 2013 due to customer/product mix changes in the business portfolio.]

(37) Furthermore, the products of the Parties are not close substitutes and therefore the Parties are not close competitors. The results of the market investigation indicated that Albemarle's closest competitors in the market for magnesium dialkyls are Akzo Nobel and Chemtura. Rockwood's closest competitors are also Akzo Nobel, and Chemtura followed by FMC.28 Should the market for magnesium dialkyls be further segmented by BEM and DBM, the proposed transaction would not lead to any overlap.

(38) In light of the above and on the basis of the evidence available to the Commission, the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market as regards organometallics or magnesium dialkyls.

4.2.Vertical effects

(39) The Transaction gives rise to three sets of vertically affected markets. In addition, the Transaction creates one vertical link regarding the potassium hydroxide ("KOH") supplied by Albemarle and used by Rockwood as an input into a number of cleaners. However, this vertical link will be not further examined in this decision as Albemarle's market share is below [0-5]% on the market for KOH both worldwide and in the EEA, while Rockwood's purchases of KOH used for its production of various cleaners represent less than [0-5]% of the worldwide demand for KOH and less than [0-5]% of the EEA demand.

4.2.1.Hydrogen bromide (HBr) as an input into lithium bromide and caesium bromide

4.2.1.1. Product market definition

i. Upstream market for HBr

(40) HBr is – at room temperature – a gas which is primarily used for purified terephthalic acid ("PTA") catalyst preparation but can be used in several other applications such as pharmaceutical, electronics and industrial coolant applications. Rockwood uses aqueous HBr to produce lithium bromide and caesium bromide.

(41) HBr can be sold in various forms, namely in aqueous solution – forming a solution of hydrobromic acid29 – or in anhydrous HBr (also called gaseous HBr). The total merchant market for aqueous HBr is estimated to be […] MT per annum globally, while demand for gaseous HBr is very small: the Notifying Party estimates that global demand for gaseous HBr is approximately […] MT per annum. Aqueous HBr solution is made available in various concentrations. The most common concentration is hydrobromic acid with a 48% concentration level. HBr in acetic acid is made available at a 33% concentration level.10

(42) The Commission has previously considered that different individual industrial, medical and specialty gases (including HBr) constitute separate relevant product markets since each gas has different chemical and physical properties and is therefore not generally substitutable.30 However the Commission has not previously analysed whether different forms of HBr should be considered as part of the same product market.

(43) The Notifying Party considers that HBr, whether as a gas or dissolved in water or acetic acid, should be analysed as a single product market. From a supply-side perspective, according to the Notifying Party, all major producers of HBr can and do produce both aqueous and gaseous HBr, as well as HBr in all concentrations that might reasonably be demanded by a customer because HBr is produced as a gas first and then dissolved in water (or acetic acid) to form aqueous HBr or HBr in acetic acid of the desired concentration. The results of the market investigation generally support the Notifying Party's view. Competitors that responded to the market investigation indicated that they produce different types of HBr for different applications, in particular HBr which is suitable for the production of lithium bromide.31

(44) However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the product market as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative product market definitions.

ii.Downstream markets for lithium bromide and caesium bromide,

(45) The Commission has not previously analysed the markets for lithium bromide and caesium bromide.

(46) Lithium bromide is used for absorption in very specific heating, ventilating, and air conditioning (HVAC) applications due to its very hygroscopic properties. It is also used as a sedative and hypnotic in medicine, in the manufacture of pharmaceuticals and in alkylation processes. It can also be used as brazing and welding fluxes.

(47) Caesium bromide is an ionic compound of caesium and bromine. It is a colourless, crystalline powder with a melting point of 636°C and soluble in water. It is used in niche industrial/chemical processes, such as the production of radiation detectors and other measuring devices.

(48) Lithium bromide and caesium bromide are different chemical products, used for different applications. The Notifying Party therefore submits that lithium bromide and caesium bromide should be considered as separate markets.

(49) However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the product market as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative product market definitions.

incentive to do so in view of Rockwood's limited market share on the downstream market (below [0-5]%) and of the size of its HBr requirements (below [0-5]% of the demand) both at the European and worldwide level. Competitors also confirmed that the Transaction would not impact their ability to sell HBr, since either they do not sell to Rockwood or they indicate being able to easily find alternative customers.45 Therefore, the merged entity would not have the abilities and the incentives to foreclose its downstream competitors from access to HBr.

(59) Rockwood is also present in the caesium bromide market, which is a downstream market related to HBr. The market size worldwide is estimated at [between EUR 150 000 and EUR 250 000], and at [below EUR 10 000] in the EEA. Caesium bromide is used in niche industrial/chemical processes. Given the limited value of this market and the very specific usage, the vertical relationship created by the Transaction would not give rise to foreclosure effects. Indeed, in view of Albemarle's market share in the market for HBr and Rockwood's very limited demand for HBr, any potential competitor in the market for caesium bromide would be able to source HBr from other manufacturers than Albemarle.

(60) In light of the above, and on the basis of the evidence available to it, the Commission considers that the Parties do not have the ability or incentive to engage in input foreclosure of their downstream competitors as a result of the proposed transaction.

(61) Therefore, the Commission considers that the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market due to vertical relationships for HBr as an input for lithium bromide and caesium bromide.

4.2.2.Butyllithium as input to brominated flame retardants

4.2.2.1.Product market definition

i.Upstream market for butyllithium

(62) Butyllithium is a lithium-based organometallic widely used as a polymerisation initiator in the production of elastomers such as polybutadiene or styrene-butadiene- styrene ("SBS") and also as a strong base in organic synthesis. It is also used in pharmaceutical applications, primarily in the synthesis of prostaglandins and antibiotics. Albemarle uses butyllithium as […] in the manufacture of [...] (not available on the merchant market) which is then incorporated into […] brominated flame retardants.

(63) The Commission has not previously analysed the market for butyllithium.

(64) Butyllithium is commercially available in a number of forms: normal ("n- butyllithium"), secondary ("sec-butyllithium"), tertiary ("tert-butyllithium" or "t- butyllithium") and iso-butyllithium. The type refers to the location in the molecule where the lithium metal is bonded to the carbon. The difference in the location of the carbonlithium bond can result in subtle differences in the compound's properties and, as a result, how the butyllithium is used. However, all these forms of butyllithium have the same chemical formula (C4H9Li) and can be used in all the applications listed above.16 The vast majority of demand is for n-butyllithium. Albemarle uses only n-butyllithium in the manufacture of all its downstream products which incorporate butyllithium, including in the manufacture of […] incorporated into flame retardants.46

(65) The Notifying Party submits that various forms of butyllithium are produced by running very similar chemical reactions. All suppliers of butyllithium therefore would produce or be able to produce any form of butyllithium in response to customer demand. Hence the Notifying Party considers butyllithium to be a separate relevant market, without the need for further segmentation according to the form of butyllithium (i.e. n- butyllithium, sec- butyllithium, ort- butyllithium).

(66) However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the product market as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative product market definitions.

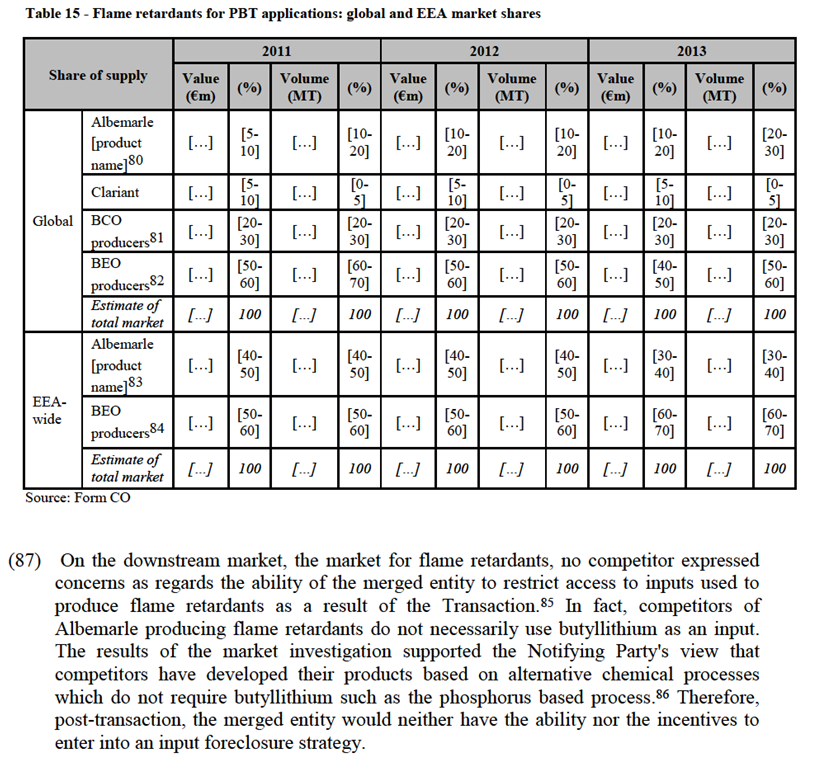

ii.Downstream market for flame retardants

(67) Flame retardants are compounds added to manufactured materials, such as plastics and textiles, and surface finishes and coatings that inhibit, suppress, or delay the production of flames to prevent the spreading of fire. They may be mixed with the base material (additive flame retardants) or chemically bonded to it (reactive flame retardants).

(68) There are various types of flame retardants, in particular mineral flame retardants (which are typically additives) and chemical flame retardants (such as organohalogen and organophosphorus compounds which can be either reactive or additive). Of commercialised chemical flame retardants, brominated flame retardants (a type of organohalogen compounds) are the most widely used.

(69) Albemarle produces flame retardants using butyl lithium which are used in: (i) high temperature polyamides47 ("HTPA"); (ii) polyamides ("PA"); and (iii) polybutylene terephthalate ("PBT").

(70) The Commission has not previously examined the market for flame retardants, although it has considered specific chemicals which can be used as flame retardants.48

(71) The Notifying Party submits that certain end uses require flame retardants to have particular properties such as flow, colour and thermal stability. For example, flame retardants incorporated into high temperature polyamides require higher specifications than those incorporated into polyamides. The flame retardant that Albemarle mostly sells for high temperature polyamides application is called [product name]. This product could also be used in nylon production but it is cheaper to use [product name] or [product name] (which does not contain butyllithium). [Product name] is a different product that is only suitable for use in PBT applications (not nylon applications). Due to these differences in specifications for different applications, the Notifying Party submits that the relevant product markets are flame retardants segmented by end use, i.e. for use in HTPA, PA and PBT.17

(72) The results of the market investigation were inconclusive on the question whether and which types of flame retardants should be considered as substitutable from a demand- side perspective. However, respondents to the market investigation indicated that different types of flame retardants are generally used by customers in different applications and their technical characteristics differ at least partially.49 The results of the market investigation indicated that flame retardants can differ depending on the inputs used (e.g. halogen-based, phosphorus-based which are halogen free and mineral flame retardants) or on the basis of the application (e.g. flame retardants for thermoplastics which encompass polyamides and polyesters like PET/PBT, flame retardants for coatings, flame retardants for textiles, flame retardants for the production of foams, etc.).50 From a supply-side perspective, however, the results of the market investigation indicated that manufacturers of flame retardants can use different inputs to achieve flame retardants to compete with Albemarle's products.51

(73) On the basis of the evidence before it, the Commission considers that the market for flame retardants could potentially be further segmented per type of flame retardants. However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the product market as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative product market definitions.

4.2.2.2.Geographic market definition

i.Butyllithium

(74) In respect of the geographic market definition, in the absence of relevant precedents, the Notifying Party submits that the relevant market in relation to butyllithium is EEA wide due to the unstable nature of the product (risk of fire upon contact with air and moisture) and the lack of trade flows and substantial price differences across the regions. Rockwood produces butyllithium in Germany, USA and Taiwan. It is primarily transported via road and rail. Rockwood's main European customers are located in [Western Europe], and it also sells in other European countries such as [Eastern Europe] via distributors.

(75) A majority of respondents to the market investigation indicate that trade flows are regional.52 This is also supported by customer purchasing patterns: according to the results of the market investigation, almost all customers of butyllithium buy 100% of their needs for their European production facilities in Europe.53 In addition, transport costs represent on average 10% of the final price according to respondents to the market

18 on other inputs than butyllithium, such as phosphorus. For the applications for which Albemarle supplies butyl-lithium based flame retardants, these alternative manufacturing processes represent [60-90]% of the market depending on the application. According to the Notifying Party, the only competitor of Albemarle downstream to whom Rockwood currently supplies limited quantities of butyllithium is […], however these are supplies for another application than flame retardants.

18 on other inputs than butyllithium, such as phosphorus. For the applications for which Albemarle supplies butyl-lithium based flame retardants, these alternative manufacturing processes represent [60-90]% of the market depending on the application. According to the Notifying Party, the only competitor of Albemarle downstream to whom Rockwood currently supplies limited quantities of butyllithium is […], however these are supplies for another application than flame retardants.

(84) The results of the market investigation were inconclusive regarding the switching of butyllithium supplier.65 Customers active in particular in the pharmaceutical and agricultural industries66 indicate that a change in their supplier would require engaging in qualification efforts due to regulatory constraints.67

(85) A large manufacturer of butyllithium indicated that it produces normal butyllithium, secondary butyllithium and tertiary butyllithium, as well as varieties using different solvents and with different concentration of active material.68 In addition, it does not know producers of flame retardants which use butyllithium to produce flame retardants apart from Albemarle.69

(86) Even though the main suppliers of butyllithium in the EEA might consider that it would be difficult to find alternative customers to Albemarle, as the customer base for butyllithium is limited70, Albemarle's purchases represent a small part of the global and European demand, and of other manufacturer's sales71, as it already purchases [50-80%] of its needs from Rockwood. While butyllithium producers could use their free capacity to produce other compounds, their butyllithium equipment is usually dedicated equipment, therefore retrofitting this equipment may not make economic sense.72 Nevertheless, in view of [Albemarle's geographic purchases], the merged entity could not foreclose suppliers in the EEA. The limited purchases worldwide (less than [0-5]% of the global demand73) and the limited purchases of Albemarle from other producers […] (less than [0-5]% of aggregated global sales of other competitors74) lead to conclude that there would be no ability nor incentive to enter into a customers' foreclosure strategy.

(89) Therefore, the Commission considers that the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market due to vertical relationships for butyllithium as input to brominated flame retardants.

(89) Therefore, the Commission considers that the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market due to vertical relationships for butyllithium as input to brominated flame retardants.

4.2.3.Grignard reagents as input into organoboron co-catalysts and pharmaceutical chemicals

4.2.3.1.Product market definition

i.Upsteam market for Grignard reagents

(90) Grignard reagents are a functional group within magnesium organometallics. Grignard reagents are used in organic synthesis in primarily pharmaceutical applications, as well as agrochemical and electronic applications.

(91) Albemarle uses two types of Grignard reagents that it has previously purchased from Rockwood: iPrMgBr and MMC. Further, Albemarle purchases small quantities of […] additional types of Grignard reagents that Rockwood produces, and [another compound] (aggregate value of total purchases in 2013 of approximately […]).

(92) iPrMgBr is principally used in pharmaceutical, electronic and agrochemical applications. It is used primarily to add an isopropyl group to carbonyl groups, but can also be used as a strong base in aprotic solvents. Albemarle uses it in the synthesis of organoboron compounds, which subsequently become part of a polymerisation catalyst system.

(93) MMC is used primarily in pharmaceutical, electronic and agrochemical applications to add a methyl group to carbonyl groups, such as aldehydes and ketones, providing synthetically useful routes to alcohols. It can also be used as a strong base in aprotic solvents. Albemarle uses MMC to produce three pharmaceutical chemicals: […].

(94) The Notifying Party considers that the market for Grignard reagents comprises all types of Grignard reagents due to the strong supply-side substitutability. Grignard reagents are produced in multi-purpose chemical facilities in production "campaigns". Rockwood's portfolio of Grignard reagents is produced according to a production schedule which is optimised in order to coincide with customer demand and delivery requirements. Likewise, producers of Grignard reagents are able to easily adapt their production plan to produce more or less of a particular product.

(95) Customers that responded to the market investigation considered that the different types of Grignard reagents are not substitutable from a demand-side perspective.87 From a supply-side perspective however, the results of the market investigation indicated that manufacturers are usually able to supply a large range of Grignard reagents.88 One of the main producers of Grignard reagents explains that the chemical process is similar for all Grignard reagents. Differences in the process relate more to the state of the raw material (i.e. liquid or gaseous halide) and to the fact that the manufacturer has or not a licence to 26 handle the raw materials and/or is willing or not to handle certain solvents such as diethyl ether.89

(96) Based on the above it follows that the market for Grignard reagents could be segmented per type of agent, due to the limited demand side substitutability. However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the product market as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative product market definitions.

ii.Downstream markets for organoboron co-catalysts and pharmaceutical chemicals

Organoboron co-catalysts

(97) Albemarle uses Grignard reagents for the synthesis of organoboron co-catalysts ([…]) which subsequently become part of a polymerisation catalyst system. The primary purpose of a co-catalyst is to improve the activity of the primary catalyst. In particular, boron-based co-catalysts are important cationic activators for metallocene catalyst systems (and can also be used to reduce the electron density of a metallocene complex). Metallocene catalysts are used on a silica support to produce drop-in catalysts for use in slurry and gas-phase units to make metallocene polyethylenes ("mPE"s).

(98) The Notifying Party submits that not all organoboron co-catalysts contain Grignard reagents. Albemarle also produces […] and […] which do not contain Grignard reagents.

(99) According to the Notifying Party, there is limited demand-side substitutability between different organoboron co-catalysts. Individual organoboron products are often custom- made for customers and are not interchangeable within catalyst systems. Customers use specific organoboron co-catalysts to produce a specific olefin polymer, depending on the application and polymer properties they desire.

(100) On the supply-side, the Notifying Party submits that the majority of organoboron co- catalysts are custom made and tend to be produced in small volumes via batch processes. The same equipment required to manufacture one organoboron co-catalyst (reaction vessels, distillation columns, purification systems, etc.) can easily be used to produce multiple different types, provided the supplier has the correct formula and undertakes the requisite requalification process. Lastly, the Notifying Party considers switching between the production of different types of organoboron co-catalysts would only take a few weeks.

(101) However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the product market as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative product market definitions.27

Pharmaceutical chemicals

(102) Albemarle also uses Grignard reagents in the production of three active pharmaceutical ingredients: […].

(103) The three pharmaceutical chemicals are used in the manufacture of final products having different therapeutic indications and based on different active ingredients (molecules). […] is an […] non-steroidal anti-inflammatory drug […]. […] is a non- steroidal anti-inflammatory drug […]. […] is [a] muscle relaxing drug […].

(104) However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the product market as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative product market definitions

4.2.3.2.Geographic market definition

i.Upstream market for Grignard reagents

(105) The Notifying Party submits that the geographic market for Grignard reagents is worldwide or at least EEA-wide due to similar global prices, low freight costs and same competitors active globally.

(106) The results of the market investigation do not, however, support the Notifying Party's view. Customers that responded to the market investigation indicated that trade flows are generally regional.90 The main transport limitations are the need for dedicated containers.91 Certain Grignard reagents require temperature control and, therefore, specific measures need to be taken in order to transport the product.92 Other Grignard reagents are considered as hazardous materials, which leads to certain restrictions applied to their transportation.93 Likewise, competitors that responded to the market investigation also indicated that trade flow of Grignard reagents are regional,94 because of the flammability of certain products or the need for some Grignard reagents to be transported at a certain temperature to avoid precipitation.95

(107) In light of the above, and on the basis of the information available to it, the Commission considers that the market for Grignard reagents is likely to be regional in scope. However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the geographic market, as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative geographic market definition.28

ii.Downstream markets for organoboron co-catalysts and pharmaceutical chemicals

Organoboron co-catalysts

(108) The Notifying Party considers that organoboron co-catalysts can be shipped in a variety of containers (pressurized portable tanks, cone drums, trailers, and railcars) by cargo air, railroad, road and ship. The delivery costs associated with these products can vary depending on the product specifications and the ship-to destination, however freight costs remain relatively low, approximately 1% of delivered cost.

(109) However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the geographic market, as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative geographic market definition.

Pharmaceutical chemicals

(110) The Notifying Party considers that the market for pharmaceutical chemicals is likely to be global or at least regional, (i) since customers purchase globally, (ii) freight costs are low as a component of delivered price, (iii) the products are transported in small volumes and easily, and (iv) competitors are located globally.

(111) However, for the purposes of the present decision, it is not necessary to conclude on the exact scope of the geographic market, as the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market under any alternative geographic market definition.

4.2.3.3.Competitive assessment

(112) Post-transaction, it is unlikely that the merged entity would have the ability or the incentive to enter into a customers' foreclosure strategy, or no input foreclosure strategy.

(113) On the upstream market for Grignard reagents Rockwood has a market share of [30- 40]% in value ([20-30]% in volume) in the EEA and [20-30]% in value ([10-20]% in volume) globally.

foreclosure of their downstream competitors as a result of the proposed transaction. Therefore, the Commission considers that the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market due to vertical relationships in respect of Grignard reagents as inputs for organoboron co-catalysts or pharmaceutical chemicals.

foreclosure of their downstream competitors as a result of the proposed transaction. Therefore, the Commission considers that the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market due to vertical relationships in respect of Grignard reagents as inputs for organoboron co-catalysts or pharmaceutical chemicals.

4.2.4.Conglomerate effects

(118) Some respondents to the market investigation raised potential conglomerate effects that could arise from the proposed transaction due to the strong market positions that Albemarle and Rockwood hold in different markets.

(119) One customer indicated that the addition of DBM to the portfolio of Albemarle would lead to increased negotiating power.96 Nevertheless, customers usually do not purchase the two products together since they use either one or the other in their applications. Therefore any bundling strategy appears unlikely. Second, customers have at least two strong alternatives to each of Rockwood's and Albemarle's respective products: for BEM, there are Akzo Nobel and Chemtura, and for DBM, there are Akzo Nobel and FMC. The latter exports the majority of its DBM to Europe.97 Third, Akzo Nobel also manufactures both products DBM and BEM and would be able to exert competitive constraints over the merged entity.98

(120) In addition, one competitor considered that the merged entity could limit access to some customers by selling Grignard reagents at a low price with other chemicals at a higher price and therefore harm its ability to compete.99 However, such a bundling strategy appears unlikely since customers do not necessarily purchase several chemicals from the same provider.

(121) In light of the above, and on the basis of the evidence available to it, the Commission considers that the proposed transaction does not give rise to serious doubts as to its compatibility with the internal market with regard to any potential conglomerate effects.

5.CONCLUSION

(122) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 ('the Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 Publication in the Official Journal of the European Union No C 368, 17 October 2014, p. 16.

3 The transaction was examined by the Commission under the case COMP/M.7061 Huntsman Corporation/Equity interests held by Rockwood Holdings.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 Organometallic specialties are chemical compounds which contain at least one bond between a carbon atom of an organic compound and a metal. The metal is typically lithium, magnesium, aluminium or zinc, although transitional metals, lanthanides, actinides, semimetals and elements such as boron, silicon, arsenic and selenium can also be used.

6 A catalyst is a chemical substance which initiates, accelerates or selectively directs a chemical reaction without being consumed. A co-catalyst is either of a pair of cooperative catalysts that improve each other’s catalytic activity.

7 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 7 and 7.2.

8 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 7.2 and 13.1.

9 Replies to Questionnaire Q2 – Competitors, Questions 3 and 7.

10 Replies to Questionnaire Q2 – Competitors, Questions 5 and 6.

11 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 9 and 58.

12 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 9.

13 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 9.

14 Reply to Questionnaire Q2 – Competitors, Question 11.

15 Replies to Questionnaire Q2 – Competitors, Questions 9, 9.1, 10 and 10.1.

16 See, for example, M. 5424, Dow/Rohm and Haas, decision of 8 January 2009, paragraph 210 on biocides, M.3344, Bain Capital/Interfer/Brenntag, decision of 21 January 2004, paragraphs 13 to 16 on bulk chemical business.

17 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 22.

18 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 22.2; reply to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 33; reply to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 38; replies to Questionnaire Q2 – Competitors, Questions 23 and 23.1.

19 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 22.

20 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 23; replies to Questionnaire Q2 – Competitors, Question 24.1.

21 In compliance with regulations of the International Maritime Dangerous Goods ("IMDG") code. Some large tanks have a frame around them and can be loaded as a container (isotanks).

22 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 23.1.

23 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 28 and 28.1.

24 Replies to Questionnaire Q2 – Competitors, Questions 26 and 28.

25 Replies to Questionnaire Q2 – Competitors, Questions 29 and 29.1.

26 Comprising magnesium dialkyls and Grignards.

27 Comprising magnesium dialkyls and Grignards.

28 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 56 and 57; replies to Questionnaire Q2 – Competitors, Questions 46 and 47.

29 HBr can also be sold in an acetic acid solution. According to the Parties, demand for this product in Europe is extremely small (less than [0-5]% of global HBr merchant supply) and is primarily used to produce agricultural chemicals.

30 Case COMP/ M.4141 - Linde/BOC, paragraphs 20 to 23, case COMP M.1641-Linde/AGA, paragraphs 14 to 21, case COMP/M.1630 - Air Liquide/BOC, paragraphs 12 to 19; and case COMP/ M.3314 - Air Liquide/Messer, paragraphs 14 to 16.

31 Replies to Questionnaire Q2 – Competitors, Questions 17, 17.1 and 18.

32 COMP case M/4141-Linde/BOC, paras 80-81.

33 Including amongst, Shandong Tianyi Chemicals Co Ldt Weifang Weisenge Chemicals Co Ltd, Shandong Brother Science & Technology Co Ltd and Shandong Haihua Group.

34 Including, amongst others, Solaris Chemtech Industries Limited and Agrocel Industries Limited.

35 Including amongst, Shandong Tianyi Chemicals Co Ldt Weifang Weisenge Chemicals Co Ltd, Shandong Brother Science & Technology Co Ltd and Shandong Haihua Group.

36 Including, amongst others, Solaris Chemtech Industries Limited and Agrocel Industries Limited.

37 Asian (predominantly Chinese and Indian players, including Neogen and Shuangliang) and FMC.

38 Asian (predominantly Chinese and Indian players, including Neogen and Shuangliang) and FMC.

39 Replies to Questionnaire Q1-Competitors (downstream markets) and customers, Question 62.

40 Replies to Questionnaire Q1-Competitors (downstream markets) and customers, Question 60 and 62.1.

41 Replies to Questionnaire Q1-Competitors (downstream markets) and customers, Question 62.1.

42 Replies to Questionnaire Q1-Competitors (downstream markets) and customers, Question 60.

43 Replies to Questionnaire Q2-Competitors Question 62.1.

44 Replies to Questionnaire Q1-Competitors (downstream markets) and customers, Question 81.

45 Replies to Questionnaire Q2 – Competitors, Questions 52, 53 and 53.1.

46 Albemarle, reply to request for information (RFI) dated 17 October 2014.

47 Polyamides are more commonly known as nylons.

48 Case M.5406- IPIC/MAN Ferrostaal AG, paragraph 9, Case M.1663- Alcan, paragraph 11.

49 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 17.

50 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 18 and 18.1. submission of a competitor, reply to Questionnaire Q1 – Competitors (downstream markets) and customers.

51 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 16; submission of a competitor, reply to Questionnaire Q1 – Competitors (downstream markets) and customers.

52 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 36; reply to Questionnaire Q2 – Competitors, Question 40.

53 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 34.

54 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 37.1.

55 Reply Questionnaire Q2 – Competitors, Question 38.

56 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 38.

57 Reply Questionnaire Q2 – Competitors, Question 42.1.

58 Reply Questionnaire Q2 – Competitors, Question 41.

59 Reply Questionnaire Q2 – Competitors, Question 42.

60 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 43 and 44.1.

61 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 46.1.

62 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 46.

63 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 43 and 44.1.

64 Rockwood understand that demand in China is for n-buytllithium. As such, although Chinese producers or Ganfeng could produce the other types of butyllithium, these estimates assume that their 2011, 2012 and 2013 production was all n-butyllithium.

65 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 68.

66 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 5 and 13.1.

67 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 68.

68 Reply to Questionnaire Q2 – Competitors, Questions 15.1 and Question 37.

69 Reply to Questionnaire Q2 – Competitors, Question 16.

70 Replies to Questionnaire Q2 – Competitors, Questions 57 and 57.1.

71 Replies to Questionnaire Q2 – Competitors, Question 56.

72 Replies to Questionnaire Q2 – Competitors, Question 57.2.

73 Form CO, Annex 7.

74 Calculations based on Form CO, Annex 7; Replies to Questionnaire Q2 – Competitors, Question 56.

75 Albermarle has provided market shares split by its […] products which compete in this application – [ product name] (which contains butyllithium) and [product name] (wich does not contain butyllithium).

76 Albermarle has provided market shares split by its […] products which compete in this application – [ product name] (which contains butyllithium) and [product name] (wich does not contain butyllithium).

77 The figure for [product name] aove actually includes [product names] (i.e […] Albermanle’s brominated flame retardants serving this application which contain butyllithium.

78 Albermarle has provided market shares split by its […] products which compete in this application – [ product name] (which contains butyllithium) and [product name] (wich does not contain butyllithium).

79 The figure for [product name] aove actually includes [product names] (i.e […] Albermanle’s brominated flame retardants serving this application which contain butyllithium.

80 [product name]

81 Chemtura and other Asian suppliers.

82 Including, but not limited to, Woojin Chemical Co, Ltd Kaimei Chemical Science and Technology (Nantong) Co, Ltd, Sakamoto Yakuhim Kogyo Co, Ltd and DIC Corporation.

83 [product name]

84 Including, but not limited to, Woojin Chemical Co, Ltd Kaimei Chemical Science and Technology (Nantong) Co, Ltd, Sakamoto Yakuhim Kogyo Co, Ltd and DIC Corporation.

85 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 16, 79, 79.1 and 82.1.

86 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 16 and 64.

87 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 12.

88 Replies to Questionnaire Q2 – Competitors, Questions 12 and 14.

89 Reply to Questionnaire Q2 – Competitors, Question 14.1.

90 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Questions 29 and 31.

91 Replies to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 33.

92 Reply to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 33.

93 Reply to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 33.

94 Replies to Questionnaire Q2 – Competitors, Question 34.

95 Replies to Questionnaire Q2 – Competitors, Question 35.

96 Reply to Questionnaire Q1 – Competitors (downstream markets) and customers, Question 53.

97 Reply to Questionnaire Q2 – Competitors, Question 25.

98 Reply to Questionnaire Q2 – Competitors, Question 9.

99 Reply to Questionnaire Q2 – Competitors, Question 43.1.