Commission, February 11, 2020, No M.9641

EUROPEAN COMMISSION

Judgment

SNAM / FSI / OLT

Subject: Case M.9641 – SNAM / FSI / OLT

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 7 January 2020, the European Commission received notification of a proposed concentration (the “Transaction”) pursuant to Article 4 of the Merger Regulation by which SNAM S.p.A. (“SNAM”) and First State Investments International Ltd (“FSI”) acquire joint control, in the meaning of Article 3(1) and 3(4) of the EUMR, over OLT Offshore LNG Toscana S.p.A. (“OLT”; SNAM and FSI are designated hereinafter as the “Notifying Parties” or, together with OLT, the “Parties”).

1. THE PARTIES

(2) SNAM, a company listed on the Italian Stock Exchange, is the holding company of the SNAM group, which is active in the development and integrated management of gas infrastructures and, in particular, in the transmission, regasification and storage of natural gas in Italy as well as in other European Union countries. SNAM is indirectly controlled by the Italian investment bank Cassa Depositi e Prestiti S.p.A. (“CDP”). In turn, CDP is controlled by the Italian Government (namely, the Ministry of Economics and Finance).

(3) FSI, the European brand name of First Sentier Investors (formerly known as Colonial First State Global Asset Management), is a company within the asset management division of Mitsubishi UFJ Trust and Banking Corporation, which is one of Japan’s largest asset managers and a wholly owned subsidiary of Mitsubishi UFJ Financial Group Inc.

(4) OLT is active in the management of a floating storage and regasification unit for liquified natural gas (“LNG”) in Italy. The offshore regasification terminal is located about 22 km off the Tuscan coast between Livorno and Pisa.

2. THE CONCENTRATION

(5) The Transaction consists of the acquisition by SNAM and FSI of joint control of OLT.

(6) Currently OLT is jointly controlled by FSI (via its subsidiary First State SP S.à r.l., “FSI BidCo”) with a participation of 48.24%, and Iren Mercato S.p.A. (“Iren Mercato”), with a participation of 46.79%.3 The remaining part of the capital is held by two minority shareholders (ASA, 2.28% and Golar, 2.69%).

(7) The Transaction will be implemented according to the terms of the following agreements:

a) a Sale and Purchase Agreement, dated 20 September 2019, between Iren Mercato and ASA for the acquisition by Iren Mercato of ASA’s shareholding in OLT. After the implementation of this agreement, Iren Mercato will own a 49.07% shareholding in OLT;

b) a Sale and Purchase Agreement, dated 20 September 2019, between Iren Mercato and SNAM for the purchase by SNAM of a 49.07% shareholding in OLT;

c) an […], which will be executed by SNAM on the closing date of the Transaction, pursuant to which […].

(8) Upon completion of the Transaction, OLT’s shareholding structure will be the following:

Shareholder | % of share capital |

SNAM | 49.07% |

FSI Bidco | 48.24% |

Golar | 2.69% |

(9) […], post-Transaction, […], OLT will be jointly controlled by SNAM and FSI Bidco:

a) OLT shareholders’ meetings would be validly constituted, and its resolutions validly taken, respectively, with the presence and the favourable vote of as many shareholders as represent the percentage of capital required under applicable law that will have to include, in any case, the presence and the favourable vote of both SNAM and FSI BidCo;

b) OLT’s board of directors consists of […] members, […] of whom will be appointed by SNAM and […] by FSI BidCo. Board meetings are validly convened, and resolutions validly passed, with the majorities required by applicable law that must, in any case, include the attendance and favourable vote of […] SNAM and […] FSI BidCo. More specifically, all resolutions for the approval of strategic decisions, […], are taken by the board of directors by simple majority, provided that […].

c) The chairman of the board will be appointed upon designation by […];

d) OLT’s […] CEOs will be designated […];

e) OLT’s Chief Financial Officer will be […] designated by […]

(10) Therefore, upon completion of the Transaction, OLT will be jointly controlled by SNAM and FSI within the meaning of Article 3(1)(b) of the Merger Regulation.

(11) OLT is and will continue to be a full-function joint venture, active on the market as any other players in the same sector. OLT has its own management and personnel and has access to sufficient resources including finance, staff, and assets (tangible and intangible) in order to conduct on a lasting basis its business activities in the LNG regasification service market. OLT has and will continue to have its own presence in the market and does not have relevant sales/purchase relationships with the parent companies. Therefore, OLT will be active as a fully functional joint venture.

(12) The Transaction, therefore, constitutes a concentration pursuant to Articles 3(1)(b) and 3(4) of the Merger Regulation.

3. UNION DIMENSION

(13) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (SNAM […] million, FSI […] million, OLT […] million). Each of SNAM and FSI has an EU-wide turnover in excess of EUR 250 million (SNAM […] million, FSI […] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(14) The Transaction therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Introduction

(15) Natural gas originates in oilfields or natural gas fields. After being processed and purified at a treatment plant, natural gas can be supplied either in gaseous form through pipelines or in liquid form, as LNG. When supplied as LNG, natural gas is converted in liquid form in a liquefaction plant, transported in specially-designed LNG tankers and then delivered for regasification at a receiving terminal at the point of destination or used directly as LNG for certain specific applications. Once regasified, LNG is transported in the pipeline network where it is mixed with "piped" natural gas. It is then distributed and supplied to end customers.

(16) In the previous decisional practice of the Commission,4 the gas markets have been segmented into i) the production and exploration for natural gas, ii) gas wholesale supply, iii) gas transmission (via high pressure systems), iv) gas distribution (via low pressure systems), v) gas storage, vi) gas trading, vii) gas supply to end customers5 and viii) the market for infrastructure for gas imports.

(17) OLT is active in the market for infrastructure for gas imports in Italy. It owns and operates an offshore regasification terminal located about 22 km off the Tuscan coast between Livorno and Pisa, with a storage capacity of 137,100 cubic meters of LNG and a maximum annual regasification capacity of 3.75 billion cubic meters.

(18) […].

(19) SNAM is also active in the market for infrastructure for gas imports in Italy via a regasification terminal in Panigaglia (La Spezia) and via pipelines. In addition, SNAM is present in the following related markets in Italy: (i) gas transmission (via high-pressure systems) and (ii) gas storage.

4.2. Product market definition

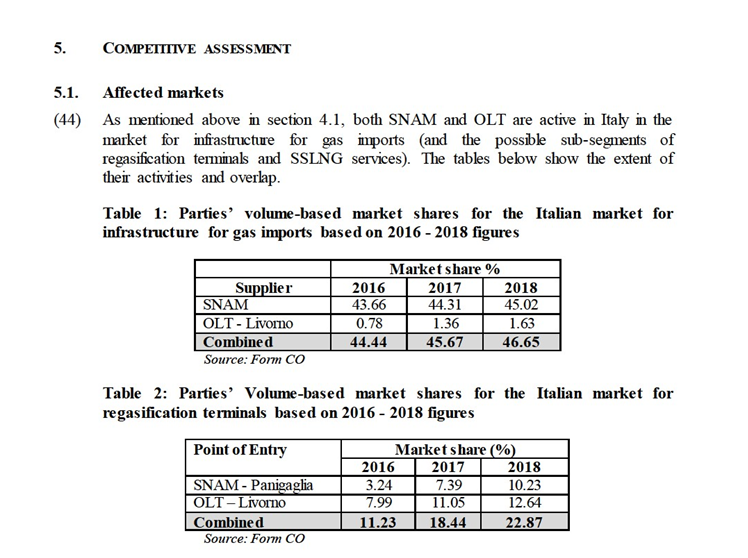

4.2.1. Infrastructure for gas imports

(20) In previous decisions, the Commission considered the question whether the market for infrastructure for gas imports could be sub-segmented into the following markets: (i) regasification services for the import of liquid natural gas; (ii) interconnection points with international gas pipelines; and (iii) underground gas storage.6 The Commission ultimately left open the exact market definition. However, in another decision, the Commission concluded that underground gas storage represented a separate market.7

(21) The Notifying Parties submit that the exact market definition can be left open as, in their view, the Transaction does not raise competition concerns regardless of the market definition adopted.

(22) The results of the market investigation conducted in the present case indicated that entities that import gas in Italy do so by using both pipelines and regasification terminals. The majority of the respondents to the market investigation8 consider that regasification terminals and pipelines are interchangeable facilities in order to carry out the import of gas.9 However, a number of respondents consider the two types of infrastructures to be more complementary than substitutable solutions.10 Some respondents have indicated that the costs associated to pipelines and regasification terminals are different and planning gas imports shall take into account different timelines, depending on the infrastructure chosen. Also, minimum capacity requirements may be provided for in contracts for the utilisation of pipelines, which do not apply in the case of regasification terminals.11 Other respondents have mentioned that some substitutability exists, but they have not substantiated their position or they have indicated that this substitutability would nevertheless be limited, only for short-term gas import. Different regulatory regimes applicable to the two types of infrastructure may also impact the level of substitutability between the two types of infrastructure.12

(23) The Commission considers that, for the purposes of this decision, it may be left open whether pipelines and regasification terminals belong to the same relevant product market or belong to separate relevant product markets, as the Transaction does not lead to serious doubts as to its compatibility with the internal market, regardless of the market definition adopted. With respect to gas storage and consistently with previous Commission’s practice,13 for the purposes of this decision, the Commission considers gas storage as a separate market.

SSLNG services

(24) The Notifying Parties submitted that all regasification terminal operators are considering to start offering Small-scale LNG services (SSLNG). Such services consist in processing LNG delivered by large cargoes in order to sell it as a fuel to LNG-fuelled trucks or ships. SSLNG can also be used to divide large LNG shipments in smaller LNG loads to deliver through smaller ships (for example to local networks in Sardinia). According to the Notifying Parties, all projects relating to SSLNG are still at a very preliminary stage and there is no market for SSLNG services yet, distinct from the market for infrastructure for gas imports or from the possible regasification service segment.

(25) With respect to the question whether the services of SSNLG, which are still in development in Italy, are substitutable with ordinary regasification services, the results of the market investigation are inconclusive. On the one hand, the majority of respondents to the market investigation have indicated that SSLNG services are distinct from the traditional regasification services offered by LNG terminals.14 One respondent submitted that SSLNG services are very different from conventional LNG services in terms of market, logistic costs, operations, etc.15 On the other hand, another respondent submitted that it is too early in the development of the SSLNG market in Italy to provide an opinion on the differences between SSLNG services and traditional services provided by regasification terminals.16 In general, respondents to the market investigation confirmed that this is a nascent market, not yet sufficiently developed, and therefore it could be difficult to provide a final view.

(26) However, for the purpose of this decision, the Commission considers that it may be left open whether SSLNG services belong to the same product market as regasification terminals services (or, under a broader product market definition, to the overall market for infrastructure for gas imports) or are part of a separate product market, as the Transaction does not raise serious doubts as to its compatibility with the internal market, regardless of the market definition adopted.

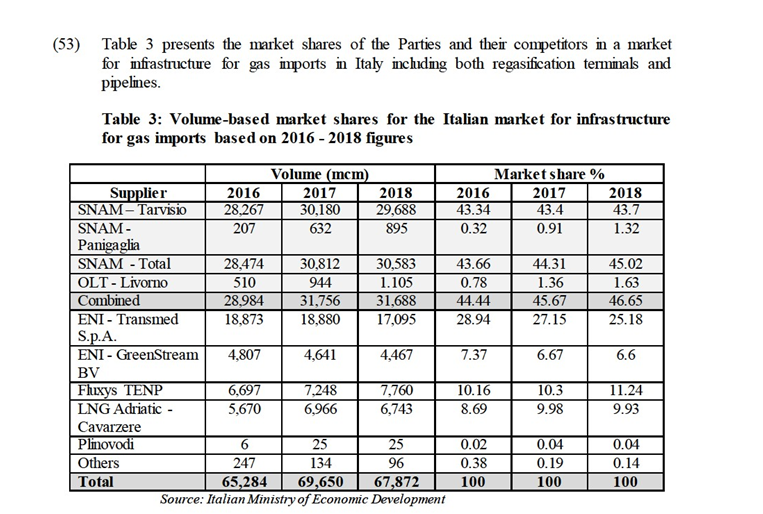

4.2.2. Gas transmission

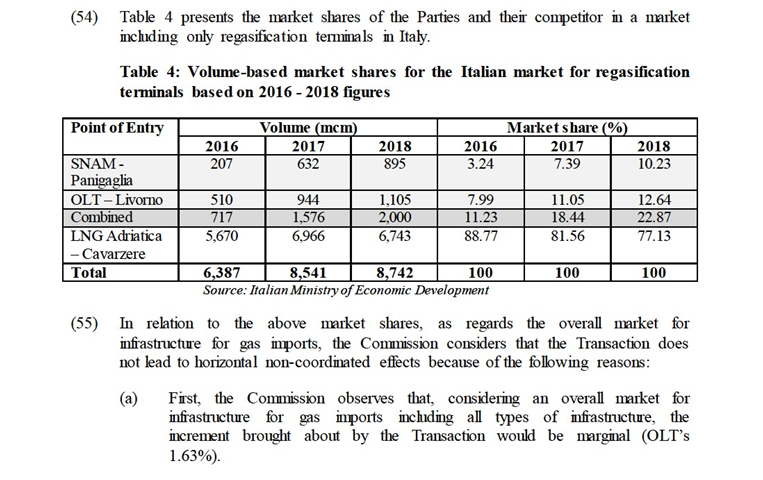

(27) The transmission of natural gas consists of physical gas transportation services via high-pressure pipelines to gas wholesale suppliers that aim to resell their gas either to other gas wholesalers, to distributors, or to large industrial customers that are directly connected to the gas transmission network.

(28) In its decisional practice, the Commission has consistently considered gas networks as natural monopolies.17 The Notifying Parties do not challenge this conclusion.

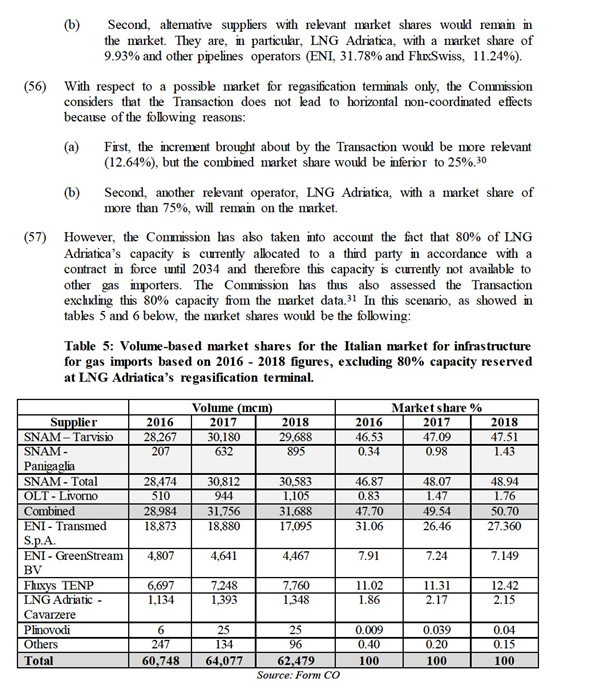

(29) The results of the market investigation confirm that the conclusions reached by the Commission in its previous practice are still valid for Italy today.18 The Commission therefore considers that gas networks for the transmission of gas are natural monopolies and each of them constitute a distinct product market.

4.2.3. Gas storage

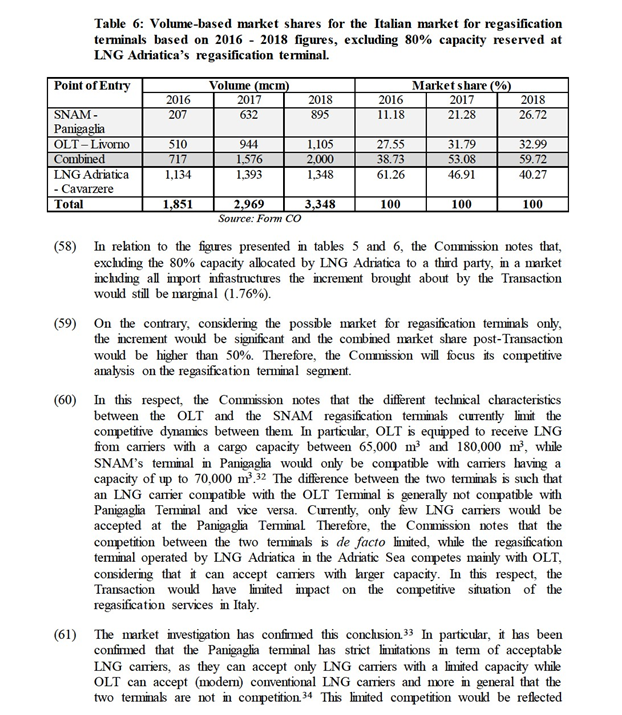

(30) In previous decisions, the Commission has defined a separate relevant product market for the storage of natural gas, while considering a further distinction between pore and cavern storage facilities as well as between storage facilities suited for the storage of high calorific value (H-gas) and storage facilities suited for the storage of low calorific value (L-gas).19 The Commission has however ultimately left the latter questions open.

(31) The Notifying Parties consider that the product market definition can be left open as, in their view, the Transaction does not raise competition concerns regardless of the market definition adopted.

(32) The results of the market investigation confirm that gas storage facilities belong to a separate product market.20 As to the possible distinction between (i) pore and cavern and (ii) facilities for the storage of L-gas and H-gas, the market investigation indicated that such distinctions are irrelevant for Italy, as there would not be cavern storage facilities and no L-gas grids/storages.21

(33) In view of the above, the Commission considers that storage facilities belong to a separate market, while any possible segmentation can be left open, as the Transaction does not lead to serious doubts as to its compatibility with the internal market regardless of the market definition adopted in this respect.

4.3. Geographic market definition

4.3.1. Infrastructure for gas imports

(34) In past decisions, the Commission considered that the market for infrastructure for gas imports, including LNG regasification terminals, was national in scope but ultimately left open whether the geographic scope was national or wider. 22

(35) The Notifying Parties submit that the exact market definition can be left open as the Transaction would not give rise to competition concerns regardless of the geographic scope. With respect to the possible segment of regasification services, the Notifying Parties submit that a sub-national definition would be inappropriate, as the specific geographic location of an LNG terminal would not play a role in the decision of gas importers.

(36) The results of the market investigation indicate that the geographic scope of the market for infrastructure for gas imports in general, and for regasification terminals in particular, is national.23 The majority of the respondents to the market investigation also confirmed that the different regasification terminals in Italy are substitutable, irrespective of their different locations in Italy.24 Therefore, for the purpose of this decision, the Commission considers that the market for infrastructure for gas imports (possibly split between pipelines and regasification terminals) is national.

(37) With respect to SSLNG services, the Notifying Parties submit that a future potential separate market for SSLNG services provided by LNG terminals would most likely have a geographic dimension broader than national. The results of the market investigation are mixed, with some respondents pointing to a national dimension of the market and other respondents to a supra-national dimension, dependent on the specific location of the different SSLNG terminals.25 In any case, and consistently with the geographic dimension of the market for infrastructure for gas imports, the Commission will base its assessment on the most narrow plausible market definition, i.e. national.

4.3.2. Gas transmission

(38) In its past decisional practice, the Commission has generally considered the market for gas transmission to be national, although noting that the region covered by the physical infrastructure grid constitutes the narrowest possible delineation of the geographic market. 26

(39) The Notifying Parties submit that, for the purposes of the Transaction, the geographic market may be considered national and limited to the Italian territory.

(40) Based on the results of the market investigation,27 the Commission considers that the market for gas transmission can be considered national in scope, in line with its decisional practice.

4.3.3. Gas storage

(41) The Commission has previously defined the geographic scope of the market for the storage of natural gas to be either national or regional, while keeping account of a potential broadening in view of the liberalization of this sector in Europe. 28

(42) The Notifying Parties submit that, for the purposes of the Transaction, the geographic market may be considered national.

(43) Based on the results of the market investigation,29 the Commission considers that the market for gas storage can be considered national in scope, in line with its decisional practice

(48) Moreover, both the OLT and the Panigaglia (SNAM) terminals would operate under a Third Party Access (TPA) regulated regime, i.e. they provide their regasification capacity to all interested market participants under transparent and non- discriminatory conditions. Pursuant to Article 24(1) of the Legislative Decree 164/2000 (adopted to implement EU gas directives), companies operating gas network infrastructures and LNG terminals have a general duty to grant access (in a non-discriminatory manner) to who so requests (subject to the compliance with the access technical requirements). This non-discrimination obligation has been further strengthened by the Italian Gas and Electricity Authority (ARERA) in an integrated text on access to regasification services, adopted in 2017. This text provides that LNG operators must allocate their available regasification capacity on the basis of transparent and non-discriminatory tenders to be held in light of the criteria set out in the text itself and in the operators’ respective regasification codes. The auctions are carried out through an IT platform made available by Gestore dei Mercati Energetici S.p.A. (“GME”), indirectly wholly owned by the Ministry of Economy and Finance. The tariffs for the provision of the regasification services are calculated according to criteria set out by ARERA resolutions. Both OLT and Panigaglia have adopted regasification codes that confirm and implement those provisions. According to the Notifying Parties, this stringent regulatory framework would prevent the Parties from exercising any form of market power.

(49) Furthermore, the Notifying Parties submit that the different characteristics between the OLT and the SNAM regasification terminals limit the competitive dynamics between them. In particular, OLT is equipped to receive LNG from carriers with a cargo capacity between 65,000 m3 and 180,000 m3, while Panigaglia would only be compatible with carriers having a capacity of up to 70,000 m3. Currently, only five LNG carriers would be accepted at the Panigaglia Terminal.

(50) As for SSLNG services, the Notifying Parties submit that the market is still inexistent in Italy and in any case OLT’s and SNAM’s SSLNG plans would address two different segments of the potential market: OLT would load LNG onto bunker/feeder vessels, while Panigaglia would load it onto tanker trucks. Moreover, such services would already be offered by most of the European LNG regasification terminals (some of which having material impact on the Italian market due to their location in the Mediterranean basin) and would be offered by various operators which are either building or developing merchant SSLNG facilities. Finally, ARERA has adopted a specific resolution, applicable to both the OLT and the Panigaglia terminals, ensuring a transparent and non-discriminatory offer of SSLNG services to all concerned shippers.

5.2.2. The Commission’s assessment

(51) As noted in section 1, OLT operates an offshore regasification terminal located about 22 km off the Tuscan coast between Livorno and Pisa, with a storage capacity of 137,100 cubic meters of LNG and a maximum annual regasification capacity of 3.75 billion cubic meters.

(52) SNAM operates a regasification terminal in Panigaglia, near La Spezia (Liguria) with regasification capacity of 3.5 billion cubic metres of gas per year. Furthermore, SNAM operates an entry point through a pipeline at Tarvisio (North Italy).

in different pricing, as the Panigaglia Terminal would offer the most convenient tariffs, due to the capacity constraint in the accepted carriers. 35

(62) Moreover, the Commission observes that the activity of the regasification terminals is subject to specific sectoral regulation aimed at (i) ensuring free access to all users of the network with equal conditions, (i) the impartial and neutral use of LNG terminals and gas transport networks under normal market conditions, and (iii) determining the main obligations of the subjects involved in the gas transport or operating LNG terminals. With specific regard to LNG regasification activities, the ARERA has adopted an integrated text on access to regasification services, which is aimed at setting out the criteria ensuring the freedom of access, neutrality and non- discrimination in the provision of regasification services.36 With reference to the allocation of LNG regasification capacity, the integrated text provides that operators must allocate their available regasification capacity on the basis of transparent and non-discriminatory tenders to be held in light of the criteria set out in the text and in their respective regasification codes. A competitive mechanism has been introduced for the allocation of regasification capacity: (i) an ascending clock auction algorithm for the allocation of annual and multi-annual regasification capacity and (ii) pay-as- bid auctions for the allocation of regasification capacity for periods of less than one year. A dedicated IT platform is provided for the management of the allocation procedures (PAR – Platform for the Allocation of Regasification capacity) – which regasification companies can voluntarily join to in order to allocate their regasification capacity. The functioning of this platform is defined in accordance with requirements set out in the integrated text.

(63) Following the adoption of the integrated text, both OLT and SNAM have adopted regasification codes that confirm and implement those provisions for their respective regasification terminals. With specific respect to OLT, the regasification code adopted states that allocation capacity is allocated as follows:

(a) multi-annual and annual regasification capacity is made available through an open ascending clock auction mechanism;

(b) capacity during the thermal year is allocated via “pay as bid” auctions; and

(c) any short-term capacity that may still be unsold after the performance of the aforementioned procedure will then be available on a “first-come-first- served” basis.

(64) Finally, the tariffs for the provision by OLT of the regasification services are calculated according to the criteria set out by ARERA resolutions and are approved periodically by ARERA.

(65) In the above respect, all respondents to the market investigation have indicated that TPA regulation and other regulatory measures adopted by the ARERA are effective in ensuring level playing field competition in access to regasification terminals.37 In particular it has been submitted that the current regulation ensures that all market operators can access the essential gas infrastructures, including regulated regasification terminals, on non discriminatory terms and based on transparent and predictable tariffs / economic conditions defined by the Italian Regulatory Authority. Moreover, the market-based mechanism for regasification capacity allocation guarantees to any operator the possibility to access the auction mechanism. 38

(66) Similarly, the vast majority of the respondents has also indicated that, in their opinion, TPA regulation and other regulatory measures adopted by the ARERA are effective in preventing regasification terminals’ operators from exercising any form of market power in relation to the access to their facilities.39

(67) In addition, the Commission notes that no respondent to the market investigation has expressed any concern about the impact that the Transaction could have on the market for infrastructure for gas imports and on the market for regasification terminal.40 Some respondents have also submitted that the Transaction can have a positive impact on those markets. In particular, it has been underlined that SNAM's core business is investing in gas infrastructures. Also,it is expected that this Transaction could be a first step for potential investments in increasing the regasification capacity in Italy, increasing in the meantime the possibilities of a diversification of supply and a consequent increase of security.41 It has also been submitted that the experience of SNAM in the gas sector could lead to a more efficient management of the regasification terminals and all buyers could benefit of this. 42

SSLNG services

(68) With respect to SSLNG services, the result of the market investigation has been mixed. First, the majority of respondents submitted that when SSLNG will be offered, SNAM (Panigaglia) and OLT will compete for customers, although with certain limitations (only for vessels and not for trucks, OLT being an offshore terminal).43 However, the majority of respondents submitted that the Transaction will have a positive or neutral impact on SSLNG services in Italy. 44

(69) A respondent submitted that the Transaction could have a negative effect on the provision of SSLNG services, because SNAM would be the only operator that has the possibility in Italy to offer SSLNG services for road and maritime transport directly from a regasification terminal. Other operators in Italy would need to build a coastal deposit to offer the same services. 45 Similarly, another respondent submitted that SNAM will control the two terminals that in the near future are likely to offer SSLNG services in the Tyrrhenian Sea. 46

(70) In this regard, first of all the Commission notes that currently neither SNAM nor OLT offer SSLNG services in Italy. OLT plans to start offering SSLNG services in […], while SNAM (Panigaglia) foresees to start offering SSLNG services in […].47 Other operators are currently either building or developing merchant SSLNG facilities that should be able to offer such services in the near future, in particular coastal deposits designed to allow both reloading of LNG on tanker trucks and on feeder/bunker vessels.48 A respondent to the market investigation confirmed that in 2021 it will complete the construction of the first coastal deposit on mainland Italy and will be able to offer SSLNG services to the Italian market. Other coastal deposits would be under construction or under authorization process in Sardinia and mainland Italy.49 Moreover, some respondents to the market investigation confirmed that SSLNG services are already offered by other European LNG regasification terminals (some of which having a material impact on the Italian market due to their location in the Mediterranean basin).50

(71) Second, SSLNG services would be ancillary for a regasification operator such as OLT and would represent a limited part of its activity. The provision of SSLNG service would be mainly used to optimize OLT’s Terminal activity, especially during inactivity periods. Although, due to the early stage of development of the SSLNG sector, it is not possible to properly analyse the demand for SSLNG services (since there is currently no actual market for SSLNG services for vessels in Italy), according to an OLT forecast for the future SSLNG sector, the share of the demand that the OLT Terminal would address would range from […] (in case of moderate demand growth) to […] (in case of stronger demand growth, as estimated by Italian authorities).51

(72) Furthermore, it is worth noting that the OLT and the Panigaglia terminals would offer two different kinds of SSLNG services: in accordance with the request submitted to the Italian authorities in order to obtain the authorization to provide SSLNG services, OLT will be enabled to discharge LNG exclusively on feeder/bunker vessels (OLT, being an offshore facility, cannot provide any direct SSLNG service for loading LNG onto tanker trucks). LNG loaded onto feeder/bunker vessels may be transported to any port for direct bunkering (Ship-to- Ship) to LNG fuelled ships. Conversely, SNAM’s current business plan for Panigaglia foresees to offer SSLNG services for loading exclusively onto tanker trucks. LNG loaded onto tanker trucks is transported to small local stations where it serves the demand of LNG as a fuel for the terrestrial transportation. Therefore, there would be little, if any, substitutability between OLT’s and other SNAM’s SSLNG services.

(73) Finally, although in general SSLNG services are (and will be) offered at market terms and conditions, specific provisions apply to the offer of SSLNG services by certain infrastructure operators (including OLT and Panigaglia).52 In particular, the relevant provisions state that SSLNG capacity shall be allocated on the basis of transparent and non-discriminatory procedures. The economic conditions for the provision of SSLNG services are defined by each operator in compliance with the principles of transparency and equal treatment between users. Operators are required to publish, in a transparent manner, the technical and economic conditions for the provision of additional SSLNG services and to offer such services in a non- discriminatory manner.

5.2.3. Conclusion on horizontal non-coordinated effects

(74) Based on the foregoing, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to horizontal non-coordinated effects.

5.3. Horizontal coordinated effects in the market for infrastructure for gas imports

5.3.1. The Notifying Parties’ view

(75) The Notifying Parties submit that the Transaction will not give rise to horizontal coordinated effects on the market for infrastructure for gas imports or on hypothetical markets for regasification services, for the following reasons:

(a) tariffs applied by both OLT and SNAM are extensively regulated and both parties are subject to third-party access obligation;

(b there is no past history of collusion in the market for infrastructure for gas imports in Italy;

(c) post-Transaction, the market shares of the operators will be totally asymmetric, for all market definitions;

(d) the main operators will remain differentiated, implying a limited risk of coordination;

(e) the Transaction will not change the competitive structure on the market, as OLT is active only to a very limited extent and the Parties will continue to face competition from strong suppliers;

(f) the Transaction will not alter the existing degree of transparency in the market;

(g) no credible deterrent mechanism or reaction of outsiders will be possible, because SNAM and OLT, as well as their competitors, will have no option but to apply the prices approved by the national authority.

5.3.2. The Commission’s assessment

(76) As set out in the Horizontal Merger Guidelines,53 to find coordinated effects evidence is needed that the horizontal merger changes the nature of competition in such a way that firms that previously were not coordinating their behaviour are now significantly more likely to coordinate and raise prices or otherwise harm effective competition. A merger may also make coordination easier, more stable or more effective for firms that were coordinating prior to the merger.54

(77) As regards the overall market for infrastructure for gas imports, the Commission considers that the Transaction does not lead to horizontal coordinated effects because (i) the increment brought about by the Transaction will be marginal (less than 2%); and (ii) a series of operators, with different market shares and different infrastructures (pipelines, regasification terminals) will remain active in the market. The Transaction will not change the nature of competition and the competitors would remain differentiated, implying a limited risk of increased coordination.

(78) With respect to a possible market for regasification services, the Commission considers that coordinated effects can be excluded for the following reasons.

(79) First, there is only limited substitutability (if any) between the regasification services offered by the Parties, due to the different capacity of the LNG carriers accepted by OLT and Panigaglia respectively (see above section 5.2.2). In this respect, the Transaction would have limited impact on the nature of competition in the market for regasification services in Italy. For the same reason, the Transaction could increase the asymmetry between the two remaining operators on the market, as SNAM will be able to accept vessels of all sizes (either in Panigaglia or via OLT), while LNG Adriatica would not be able to accept smaller vessels.

(80) Second, the Transaction would not significantly alter the existing degree of transparency on the market either, as already today tariffs and commercial conditions applied by the regasification terminals operating under TPA rules (as OLT and Panigaglia) are public. Therefore, the Commission considers that any possible impact of the Transaction on transparency will not materially change the existing ability of firms to monitor deviations.

(81) Third, also the sectoral regulation described in previous section 5.2.2 – in accordance with which all operators must allocate their available regasification capacity on the basis of transparent and non-discriminatory tenders and with tariffs calculated according to the criteria set out by ARERA – suggests that the possibility to coordinate the competitive behaviour in the regasification service market would not increase substantially following the Transaction, as the particular allocation mechanisms will remain unchanged irrespective of the number of operators in the market.

(82) Finally, any coordinated effects have to be excluded also in a hypothetical market for SSLNG services. First, as explained above, OLT and SNAM will provide different services on this market (LNG loading, respectively, onto bunker/feeder vessels and tanker trucks) and therefore the Transaction would not change substantially the nature of (future) competition. Second, a series of other coastal deposits (designed to allow reloading of LNG on both tanker trucks and on vessels) and small-scale liquefaction units have been built/are under development by several third parties in Italy and will enter into service in the coming years.55 The Commission considers that changes in demand and supply are an element to be taken into consideration in the assessment of any possible coordinated effects, especially in a nascent market as the SSLNG services one where the growth rate is expected to be exponential.56 Therefore, demand conditions do not look sufficiently stable to make coordination likely.

5.3.3. Conclusion on horizontal coordinated effects

(83) In light of the above considerations, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to horizontal coordinated effects.

5.4. Non-horizontal effects

(84) Customers of regasification terminals (i.e. LNG gas importers), once their LNG loads are processed and converted back to a gaseous state, need transmission and/or storage capacity, in order to deliver the commodity to their customers. Therefore, the Transaction will bring about a vertical relationship in Italy between the upstream market for infrastructure for gas imports (and its possible sub-segments including regasification terminals and SSLNG), where OLT and SNAM are both active, and the downstream markets for (i) gas transmission and (ii) gas storage, where SNAM is active.

5.4.1. The Notifying Parties’ view

(85) The Notifying Parties submit that the Transaction would not have any vertical negative effect, mainly because access to the Italian gas transportation network and storage services is subject to a strict regulatory framework – including third-party access at tariffs defined on the basis of the criteria established by the Italian Regulatory Authority – which would eliminate any risk of foreclosure.

(86) The Notifying Parties submit that their arguments as to the absence of any ability to foreclose are supported by the conclusions of the Italian Antitrust Authority in the case Cassa Depositi e Prestiti/SNAM. In fact, according to the Authority’s decision in this case, the pervasive and consolidated regulatory framework of activities in the markets for gas transportation, storage and distribution would make impossible any distorting use of vertical integration.57

(87) Furthermore, SNAM is not active in the production and commercialization of natural gas58 (in compliance with the full-ownership unbundling model envisaged by EU law) and, therefore, the decision to opt for SNAM or other competitors in a related market (for example, in the gas storage market) will rest upon the shippers concerned and could not be influenced by SNAM.

5.4.2. The Commission’s assessment

(88) Non-horizontal effects may principally arise when mergers give rise to foreclosure. A merger is said to result in foreclosure where actual or potential rivals' access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing these companies' ability and/or incentive to compete.59 Such foreclosure may discourage entry or expansion of rivals or encourage their exit. Such foreclosure is regarded as anti-competitive where the merging companies — and, possibly, some of its competitors as well — are as a result able to profitably increase the price charged to consumers.60

(89) In the gas transmission market, SNAM is the main transmission system operator in Italy and has a natural monopoly over its network. Considering the whole Italian gas network, SNAM has a market share of [90-100]% in volume (gas handled) and of [90-100]% in value (based on 2018 figures). The remaining competitors are operators of small local networks.

(90) In the gas storage market, SNAM is active through its subsidiary Stogit, which manages nine active storage facilities in Italy. SNAM has a market share of [90- 100]% in volume (gas handled, natural gas year 2018/2019) and [90-100]% in value (2018). The only other operator is Edison Stoccaggio (with a market share of [0-5]% in volume and [5-10]% in value).

(91) Regardless of SNAM’s market shares in the gas transmission market and in the gas storage market, the Commission considers that the Transaction will not raise serious doubts as to its compatibility with the internal market with respect to non-horizontal effects, for the reasons explained below.

(92) First, both the market for gas transmission and the market for gas storage are subject to sector-specific regulation in Italy (adopted to implement the corresponding EU sectoral law), which prevents gas operators from refusing access to their facilities and from charging excessive tariffs. In particular:

(a) With respect to gas transmission, pursuant to Legislative Decree No 164/2000, natural gas transportation and dispatching services are subject to regulation by ARERA, in order to guarantee all users of the network the freedom of access on equal terms to such markets (as well as impartiality and neutrality of the services). The regulation has been detailed by ARERA Resolution no. 137/02 and subsequent amendments, on the basis of which gas transportation companies have adopted their own network codes;

(b) As regards the gas storage, Legislative Decree No 164/2000 provides for a general third-party access regime to storage services and gives ARERA the power to define the criteria and the economic conditions for the provision of storage services.

(93) Second, respondents to the market investigation have confirmed the relevance of the sectoral regulation in order to limit the ability of the Parties to foreclose access to the relevant markets. The vast majority of the respondents submitted that SNAM’s position in gas transmission and/or storage in Italy would not provide any advantage to OLT after the Transaction, notably because of the extensive regulation of the relevant markets.61 Similarly, the vast majority of the respondents submitted that, even taking into account SNAM's position in gas transmission and storage, it does not consider that OLT would have either the ability or the incentive to foreclose its competitors in the market for infrastructure for gas imports, again thanks to the regulated regime of the relevant markets.62

(94) Third, more general, the vast majority of the respondents to the market investigation confirmed that in their opinion the sectoral regulation applicable in Italy to gas transmission and gas storage is effective in preventing SNAM from exercising any form of market power following the Transaction.63 One respondent confirmed that sectoral regulation would provide a clear framework that would not highlight any evident risks to increase SNAM’s ability to exercise market power as a result of the Transaction.64

(95) In light of the above, the Commission considers that the merged entity would not have the ability to foreclose its rivals.

(96) Moreover, considering that, in accordance with the described regulatory framework, SNAM would not have any possibility to discriminate between operators with respect both to access to the facilities and to the applicable tariffs, and also considering that OLT is not active in Italy in the production, supply and distribution of natural gas, the Commission considers that the merged entity would not have any incentive to foreclose its rivals.

5.4.3. Conclusion on non-horizontal effects

(97) In light of the above considerations, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to non-horizontal effects.

6. CONCLUSION

(98) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Case M.9341 - First State Investment International / Iren Mercato / Olt Offshore LNG Toscana.

4 M.3440 ENI/EDP/GDP, M.3294 EXXONMOBIL/BEB, M.3293 Shell/BEB, M.4180 Gaz de France/Suez, M.3868 DONG/Elsa m/ Energi E2.

5 This market can be further subdivided according to different types of users (big and industrial, small and medium enterprises, households, etc.).

6 M.5649 - RREEF FUND/ ENDESA/ UFG/ SAGGAS , paras. 11-15; M.8771 - Total/Engie, paras. 23-27.

7 M. 1383 – Exxon / Mobil, recital 69.

8 Throughout this decision, when the Commission refers to the (number of) respondents in relation to a given question of the market investigation this excludes all respondents that have not provided an answer to that question or replied "I do not know", unless stated otherwise. For example, "a majority of respondents" means a majority of respondents having replied to a given question and not having ticked "I do not know".

9 See replies to question 7 in questionnaire Q1 of 8 January 2020 to competitors and customers.

10 See replies to question 7.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

11 See, for example, replies by Enel and A2A to question 6 in questionnaire Q1 of 8 January 2020 to competitors and customers.

12 See replies to questions 10 and 10.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

13 M.5549 EDF/Segebel; M.3696 E.ON/MOL; M.3410 Total/Gaz de France.

14 See replies to questions 11 and 11.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

15 ENEL, reply to question 11.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

16 Terminale GNL Adriatico, reply to question 11.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

17 M.6984 - EPH/ STREDOSLOVENSKA ENERGETIKA, para. 25; M.3696 E.ON/MOL, recital 97.

18 See replies to questions 12 and 12.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

19 M.5467 RWE Essent; M.3410 Total / Gaz de France.

20 See replies to questions 13 and 13.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

21 See replies to questions 14 and 14.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

22 M.5649 - RREEF FUND/ ENDESA/ UFG/ SAGGAS , paras. 16-18; M.8771 - Total/Engie, paras. 35-37.

23 See replies to questions 16, 16.1, 17 and 17.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

24 See replies to questions 18, 18.1, 19 and 19.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

25 See replies to questions 20 and 20.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

26 M.6984 - EPH/ STREDOSLOVENSKA ENERGETIKA, para. 25; M.3696 E.ON/MOL, recital 126.

27 See replies to questions 21 and 21.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

28 M.6984 - EPH/ STREDOSLOVENSKA ENERGETIKA, para. 24; M.3696 E.ON/MOL, recitals 128-130.

29 See replies to questions 22 and 22.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

30 Guidelines on the assessment of horizontal mergers, para 18.

31 The Notifying Parties submit that the capacity reserved by LNG Adriatica should not be excluded from the market data, because it is not captive but destined to a third party. The Commission considers that, irrespespective of the party to which this capacity is allocated, as a matter of fact 80% of the capacity of the terminal would not be available to other importers until 2034 and therfore it is necessary to verufy the competitive scenario taking into account the real regasification capacity on the market (i.e. capacity availabe for all operators).

32 This difference is mainly due to the fact that OLT is an offshore terminal while Panigaglia is a costal one, with very shallow water depth and realized between 1967-1970 taking into account the standard size of existing LNG carriers at that time.

33 See replies to questions 24 and 24.1 in Q1 of 8 January 2020 to competitors and customers.

34 Terminale GNL Adriatico and DXT Commodities, reply to question 24.1 in Q1 of 8 January 2020 to competitors and customers.

35 See replies to questions 25 and 25.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

36 Resolution 660/2017/R/gas, Integrated text of the provisions on guarantees of free access to the regasification service of liquefied natural gas.

37 See replies to questions 26 and 26.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

38 ENI, reply to question 26.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

39 See replies to questions 27 and 27.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

40 See replies to questions 36.1 and 36.2 in questionnaire Q1 of 8 January 2020 to competitors and customers.

41 A2A, reply to question 38 in questionnaire Q1 of 8 January 2020 to competitors and customers.

42 See replies to question 32.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

43 See replies to questions 30 and 30.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

44 See replies to question 36.3 in questionnaire Q1 of 8 January 2020 to competitors and customers.

45 Edison, reply to questions 36.4 and 37.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

46 Societa’ Gasdotti Italia, reply to question 36.4 in questionnaire Q1 of 8 January 2020 to competitors and customers.

47 […].

48 Form CO, table 4 (SSLNG infrastructures).

49 Edison, reply to question 31, in questionnaire Q1 of 8 January 2020 to competitors and customers.

50 A2A, reply to question 30.1 and Societa’ Gasdotti Italiani, reply to question 31 in questionnaire Q1 of 8 January 2020 to competitors and customers.

51 Annex 6.48 to the Form CO – […].

52 Resolution No. 168/2019/R/gas of ARERA.

53 Horizontal Merger Guidelines, paragraphs 22, 39 et seq.

54 Horizontal Merger Guidelines, paragraph 22(b).

55 See above paragraph 70.

56 Annex 6.48 to the Form CO – SSLNG Market Outlook.

57 Italian Antitrust Authority, decision of 8 August 2012, case C11695 - Cassa Depositi e Prestiti/SNAM, para. 84.

58 SNAM has a 13.5% minority participation without any rights of control in Italgas, a company listed on the Italian Stock Exchange and active as gas distributor in Italy.

59 Non-horizontal Merger Guidelines, paragraph 29.

60 Non-horizontal Merger Guidelines, paragraph 29.

61 See replies to questions 32 and 32.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

62 See replies to questions 33 and 33.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

63 See replies to questions 34 and 34.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.

64 Società Gasdotti Italia, reply to question 34.1 in questionnaire Q1 of 8 January 2020 to competitors and customers.