Commission, July 17, 2017, No M.8416

EUROPEAN COMMISSION

Judgment

THE PRICELINE GROUP / MOMONDO GROUP HOLDINGS

Dear Sir/Madam,

Subject: Case M.8416 – The Priceline Group / Momondo Group Holdings Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

(1) On 12 June 2017, the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which the undertaking The Priceline Group Inc. ("Priceline", United States) acquires within the meaning of Article 3(1)b of the Merger Regulation sole control over Momondo group Holdings Limited ("Momondo", United Kingdom), by way of purchase of shares ("the Transaction"). (3)

(2) Priceline and Momondo will also be referred to below as the "Parties".

1. THE PARTIES AND THE OPERATION

(3) Priceline is active in the supply of online travel and related services, notably through metasearch sites ("MSS") and online travel agents ("OTAs"), in 224 countries and territories in Europe, North America, South America, the Asia- Pacific region, Middle East and Africa. Its core brands include the MSS brand KAYAK, also operating under the Swoodoo and Checkfelix brands, and the OTA brands Booking.com, priceline.com, agoda.com, Rentalcars.com and Opentable.

(4) Momondo offers services in the online travel sector in 35 international markets with an EEA focus on the Nordic region. It owns two MSS, namely Cheapflights and Momondo.

(5) Priceline will acquire 100% of the issued capital of Momondo through a private acquisition.

(6) Consequently, the Transaction results in the acquisition of sole control within the meaning of Article 3(1)(b) of the EUMR.

2. EU DIMENSION

(7) The Transaction was referred to the Commission under Article 4(5) following the notifying party's request. The Transaction was capable of being reviewed under the national competition laws in Austria, Cyprus, Germany and the UK, which didn't express their disagreement to the request to refer the case. Therefore the concentration is deemed to have an EU dimension.

3. MARKET DEFINITION

3.1. The Parties' activities

(8) Priceline is an integrated group active worldwide in online travel intermediation. In the EEA, Priceline operates MSS for flights, hotels and car rentals under the Kayak, Swoodoo and Checkfelix brands (together "KAYAK"). (4) Priceline also operates OTAs in the EEA: Booking.com, specialising in hotel bookings, and Rentalcars.com, specialising in car rentals.

(9) Priceline's MSS and OTAs also provide commercial affiliate programmes at global level.

(10) Through their commercial affiliate programmes, Priceline's MSS provide access to their search and comparison technology to third party websites, such as other smaller MSS, general travel websites, travel blogs, etc. that wish to offer comparison services to their visitors. Through the commercial affiliate programme, visitors to the affiliate's website can search for and compare flights, hotels and car rentals, as if they were visiting the website of the Priceline MSS that is offering the commercial affiliate programme.

(11) Similarly, Priceline's OTAs provide access to their search, compare and booking functionality to third parties through their commercial affiliate programmes. The affiliates of Priceline's OTAs are notably smaller OTAs and TSPs wishing to combine their offering with other travel services, e.g. airlines wishing to offer hotel accommodation, hotels wishing to offer car rentals, etc. Priceline's OTAs also offer their commercial affiliate programmes to MSS that wish to provide booking functionality on their websites in addition to comparison services. Visitors to the affiliates' websites can search for and book travel services from Priceline's OTAs, as if they were visiting the Priceline websites.

(12) Under their commercial affiliate programmes, Priceline's MSS and OTAs enter into revenue-sharing agreements with their affiliates, whereby Priceline's MSS and OTAs share with the affiliates a percentage of the commission they generate through referrals from the affiliates.

(13) Momondo operates two MSS, both also active in the EEA. Momondo's MSS are active in flights, where they have established their own inventory through cooperation with flights OTAs, airlines etc. Momondo also offers hotels MSS, however this is powered through a commercial affiliate programme offered by HotelsCombined, a hotels MSS. Momondo is not active in the provision of car rental MSS. Instead, it has entered into a commercial affiliate programme provided by CarTrawler, a car rental OTA. Therefore, as regards car rental, Momondo effectively provides OTA services to its users. However, all car rental bookings are re-directed to the CarTrawler website and handled by CarTrawler and not Momondo. (5)

(14) Momondo also offers commercial affiliate programmes for flights MSS.

(15) Therefore, the Transaction would give rise to horizontal overlaps and vertical relationships in the following activities of the Parties: (6)

i. horizontal overlaps in the operation of flights MSS and hotels MSS websites;

ii. horizontal overlaps in the operation of car rental OTAs;

iii. horizontal overlaps in the provision of commercial affiliate programmes for flights MSS;

iv. potential vertical relationship between the operation of MSS for flights, hotels, car rentals and the operation of OTAs for flights, hotels, car rentals;

v. potential vertical relationship between the operation of flights MSS and the provision of flights MSS commercial affiliate programmes, as well as the operation of hotels MSS and the provision of hotels MSS commercial affiliate programmes;

vi. potential vertical relationship between the operation of car rental OTAs and the provision of car rental OTA commercial affiliate programmes.

3.2. Relevant product markets

3.2.1. Online travel intermediation

(16) The Parties are active in the online travel sector. In its previous decision practice, the Commission considered whether online travel markets form part of a broader "dynamic market" comprising the services provided by all suppliers of the travel industry's value chain, i.e. suppliers of different kinds of travel services, tour operators, brick-and-mortar and online travel agents and other travel intermediaries. Ultimately, the Commission left the market definition open. (7)

(17) The online travel sector is characterised by a multitude of players at various levels of the value chain. Among the main ones are:

i. travel service providers ("TSPs"), such as airlines, hotel operators, car rental companies or other transport service suppliers. For the purposes of this Decision, tour operators, which create tourism products by purchasing individual travel products and combining them into package holidays, will also be considered as TSPs;

ii. online travel agents ("OTAs"), namely online retailers which sell one or more types of travel service, supplied by a range of TSPs, such as flights, hotel and other travel accommodation and car rental. OTAs provide, on the one hand, search, compare and booking services to consumers and, on the other hand, marketing services and booking functionality to TSPs; (8)

iii. metasearch sites ("MSS"), namely websites which aggregate information relating to one or more types of travel service. MSS provide, on the one hand, search and comparison services to consumers and allow them to compare offers for the same travel product made by the TSP and/or by one or more OTAs. On the other hand, MSS provide lead generation services to TSPs and OTAs. (9)

(18) The majority of respondents to the market investigation taking a position considered that the distribution of travel services through online channels constitutes a separate market from the distribution of travel services through other channels. (10)

(19) In light of the above, the Commission found evidence pointing towards the existence of a separate market for the online intermediation of travel services. However, as the Parties are only active in online intermediation, and the Transaction would not raise serious doubts under any plausible market definition, for the purposes of this Decision, it may be left open whether the intermediation of travel services online constitutes a separate market from the intermediation of travel services through brick-and-mortar outlets.

(20) Therefore, for the purposes of this Decision, the Commission concludes that it may be left open whether there is a distinct market for the online intermediation of travel services. The Commission will assess the impact of the Transaction only on the narrower possible markets for the intermediation of travel services online, in which the Parties are active.

3.2.2. Distinction between general and specialised search engines

(21) In its prior decision practice, the Commission has concluded that internet general search should be distinguished from specialised search, which focuses on specific segments of online content, such as for example travel search engines. (11)

(22) The Parties also note that, although consumers do use general search to look for travel services, the results thus generated are very different from the comparison services offered by MSS. The Parties view Google's specialised travel services Google Flights and Google Hotels as competing MSS operators and not as part of the general search service provided by Google.

(23) As the Parties only overlap in the operation of specialised search engines focussed on travel, the impact of the Transaction will be assessed on markets for travel search engines.

3.2.3. Distinction between MSS and OTAs

3.2.3.1. Commission and national competition authorities' decision practice

(24) The Commission has not defined markets for travel MSS in its past decision practice. MSS were considered in a previous decision, in which the Commission pointed out that MSS aggregate and compare fares, but do not offer booking capabilities, instead channelling consumers to TSPs or travel agents offering the best fares. However, the Commission did not define the market on which MSS operate. (12)

(25) In its previous decision practice, the Commission has considered distinct markets for the provision of travel agency services. (13)

(26) National competition authorities have also looked into the online travel sector. The UK national competition authority has looked into MSS markets in its assessment of the acquisition of KAYAK by Priceline, assessing the impact of the merger on the supply of online travel search services to UK consumers and the supply of online lead generation services to TSPs, without ultimately defining MSS markets. In its assessment, the UK national competition authority considered that MSS and OTAs are both in a vertical relationship and compete with each other, as they both seek to obtain traffic by providing online travel search services to consumers and online lead generation services to TSPs. However, in that decision, the OFT did not conclude on the precise market definition and analysed competition between OTAs and MSS only “on a cautious basis”, finding that, even in a potential market including both OTAs and MSS, an OTA and a MSS “are not in fact close competitors”. (14)

(27) Conversely, in their antitrust decisions assessing most-favoured nation clauses in contracts for the online distribution of hotel accommodation, the German, French, Italian, Swedish and Swiss competition authorities and the Düsseldorf appeal court in Germany treated OTAs specialising in the distribution of hotel accommodation as belonging to a distinct market, implicitly or explicitly excluding MSS. (15)

3.2.3.2. Parties' views

(28) The Parties submit that MSS are active on a two-sided market, offering, on the one hand, online travel search services to consumers and, on the other hand, online lead generation services to TSPs and OTAs.

(29) The Parties argue that MSS are not alternatives to OTAs for either consumers or for TSPs, and should therefore not be included in the same market, for the following reasons.

(30) First, OTAs offer booking functionality to consumers, whereas MSS typically do not. While some MSS, including all KAYAK brands, allow consumers to book through a booking function embedded in the MSS interface, that functionality is actually provided by OTAs or TSPs, and the transaction is in fact completed on the platforms of the latter. Therefore, for TSPs whose website does not include a booking functionality, MSS would not be an alternative to OTAs, as consumers would not be able to complete their booking on the MSS platform.

(31) Second, the payment model adopted by most MSS is different from that of OTAs. MSS typically operate a "pay-per-click model", whereby TSPs and OTAs pay a fee to the MSS for each referral to their own websites, irrespective of whether the referral leads to a booking. OTAs, on the other hand, usually operate a "pay-per- acquisition" model, whereby TSPs pay a fee for each completed booking that is facilitated by the OTA. The payment model used by most MSS entails a higher financial risk for TSPs than that used by OTAs, since the TSP is likely to pay fees for referrals that do not result in actual bookings.

(32) Third, the customer base of MSS is broader, as it includes TSPs and OTAs, whereas OTAs do not list the offerings of rival OTAs on their websites. Moreover, the Parties submit that the majority of MSS revenues is generated through referrals to OTAs.

(33) Fourth, MSS offer consumers the possibility to compare the prices offered by multiple OTAs and TSPs for the same travel service, such as a specific type of hotel room in a particular hotel on a particular date. Conversely, OTAs only display the offers of the TSPs that may be booked through the OTA; they do not display the prices offered by rival OTAs for the same travel service.

3.2.3.3. Commission's assessment

(34) Respondents to the market investigation were rather split as to whether MSS and OTAs should be viewed as belonging to the same market.

(35) When asked whether the services offered by MSS to consumers and to TSPs should be distinguished from those offered by OTAs, respondents were rather split as to whether the services offered by MSS are interchangeable with those of OTAs. (16)

(36) Respondents who considered that MSS should be distinguished from OTAs pointed out that OTAs act as agents of TSPs, whereas MSS act merely as advertisers; that MSS provide the first step in the consumer journey, which is then often completed through a booking on OTA websites; that MSS offer a much broader comparison, displaying offers from multiple distribution channels and enabling consumers to compare prices for the same travel product, whereas OTAs only enable consumers to compare different travel products; that OTAs have a more direct relationship with consumers, providing additional services, such as call centres and after-sales support; and that even when the MSS offer some booking functionality, this is actually still powered by an OTA or TSP.

(37) Moreover, MSS which responded to the market investigation indicated that for an MSS to start offering services similar to an OTA, significant time and investment would be required. The MSS would have to develop a deeper cooperation with TSPs, on the basis of an agency model, invest in software solutions allowing it to process bookings and payments, provide customer service, and in some cases also register as a travel agency and acquire related licences. Some MSS also noted that such a change would not make commercial sense, as MSS' reputation of presenting price comparison results in a neutral way could be compromised, and such a change in the business model would be unlikely to be welcomed by the market. Last, MSS that provided information on their revenue sources appeared to generate most of their income from their relationships with OTAs and only a small share from TSPs. (17)

(38) Respondents who considered that both types of services are interchangeable referred to the fact that both MSS and OTAs compete to attract consumers' attention and lead them to their websites through a variety of channels; that consumers often do not realise that they are not completing their booking on the MSS website, and thus see MSS as interchangeable with OTAs; and that an increasing number of MSS have begun to offer booking functionalities on their websites. However, even respondents who considered that the two types of services are interchangeable from the point of view of consumers pointed out that OTAs offer additional services, such as the completion and management of bookings and payments, after-sales support and other customer services.

(39) In light of the above, the Commission considers that even though MSS and OTAs are both active in the intermediation of travel services online and both aim to attract consumers interested in organising their travel, they appear to offer different services and generally operate on the basis of different business models. As the Transaction would not raise serious doubts, either on the basis of distinct markets for MSS and OTAs or on the basis of a broader market comprising both MSS and OTAs, the exact scope of the product market may be left open for the purposes of this Decision.

3.2.3.4. Conclusion

(40) Therefore, for the purposes of this Decision, the Commission concludes that it may be left open whether there are distinct markets for MSS and OTAs. The Commission will therefore assess the impact of the Transaction both on markets for MSS only and on broader markets comprising both MSS and OTAs.

3.2.4. Segmentation of MSS and OTA markets by type of travel services

3.2.4.1. Commission and national competition authorities' decision practice

(41) In its prior decision practice, the Commission considered that the online distribution of travel services could be further segmented by type of travel products, between flights, hotels, package holidays, etc. though ultimately the exact definition of the product market was left open. (18)

(42) National competition authorities have also distinguished between hotels, flights and car rentals, considering that these are not interchangeable from the consumer's point of view and observing that MSS and OTAs often specialise in one type of travel services, even if there is some complementarity between the different types of travel services from the supply side, as consumers may prefer to organise their entire journey or holiday in a "one-stop" shop. (19)

3.2.4.2. Parties' views

(43) The Parties claim that, even though in the past most online travel intermediaries focussed on a specific type of travel service, such as flights, hotels, car rentals, etc., in recent years, there has been significant convergence in the sector, as MSS and OTAs which originally focussed on one type of travel services have expanded their activities to enable consumers to complete their bookings for multiple travel services on a single website. Therefore, in the Parties' view, the markets for MSS and for OTAs are broader, comprising all types of travel services. (20)

3.2.4.3. Commission's assessment

(44) The majority of respondents to the market investigation consider that the markets for MSS and OTAs should be further segmented by type of travel service, identifying distinct segments for flights, hotels, car rentals and package holidays. (21)

(45) A limited number of respondents who consider that the markets for online travel intermediation should not be further segmented by type of travel services argue that MSS or OTAs specialising in only one type of travel service are in competition with respectively those MSS or OTAs that offer a broader range of travel services; that the business model and technology required to offer online intermediation services for different types of travel services is comparable, and that even though not identical, different types of travel services are complementary and thus likely to be sourced together by consumers.

(46) Among the majority of respondents who consider that narrower markets for each type of travel services should be taken into account, several point out that intermediation for one type of travel service (such as flights) is not substitutable to intermediation for a different type of service (such as hotels); that consumers often search for each type of travel service at different points in time and using different intermediaries; that several MSS and OTAs - including some well-known ones - specialise in only one type of travel service, and that MSS and OTAs use different marketing techniques for each type of travel services.

(47) Moreover, when asked whether they could easily expand their activity from one type of travel service to another, the MSS that responded to the market investigation were rather split. Some respondents noted that they could expand using their current business model and technology, and by establishing commercial relationships (notably through commercial affiliate programmes) with intermediaries already active in the type of travel service into which they wished to expand. Other respondents pointed out that new interfaces, new partners, additional expertise in the new type of product and marketing activities to build a new customer base would be required. (22)

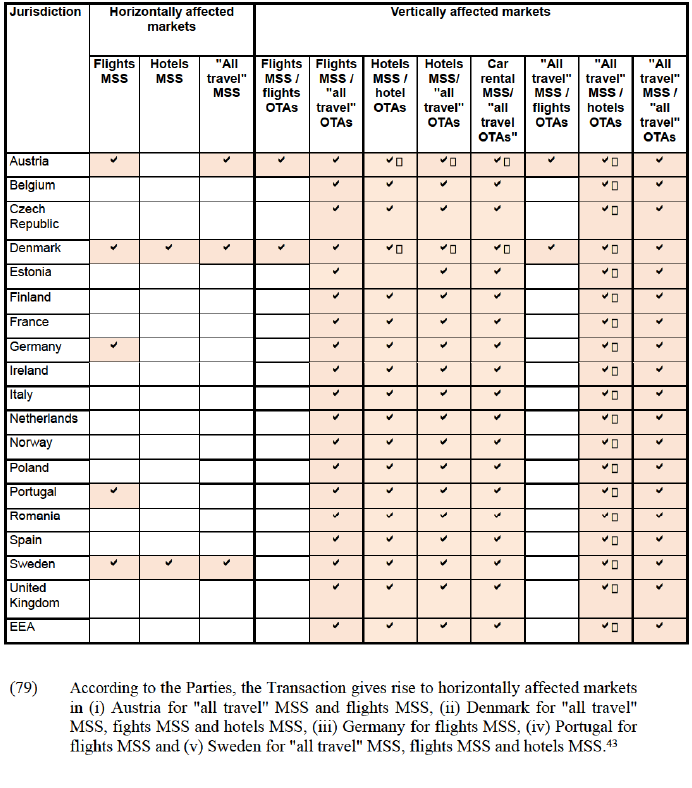

(48) Conversely, the majority of OTAs that responded to the market investigation considered that an expansion of their activities into another type of travel service would be difficult, as expenses would be required to connect to new databases for providing inventory for the new type of service, different technology and a different business model would be required, and product-specific knowledge and market analysis on how to target consumers interested in the new type of travel services would have to be developed. (23)

(49) Last, when asked about the scope of the contracts concluded between MSS and OTAs, the majority of MSS and OTAs that responded to the market investigation indicated that they negotiate separately for each type of travel service, even when both contracting parties provide intermediation for more than one type of travel service. (24)

(50) In light of the above, the Commission considers that segmenting MSS and OTA markets by different types of travel service should be considered. However, as the Transaction would not raise serious doubts, irrespective of whether broader markets comprising "all travel" MSS or OTA services are taken into account, or narrower segments for each of flights, hotels, car rentals and package holidays, the exact delineation of the relevant product markets may be left open.

3.2.4.4. Conclusion

(51) Therefore, for the purposes of this Decision, the Commission concludes that it may be left open whether MSS and OTA markets should be further segmented based on the type of travel service they intermediate. The Commission will therefore assess the impact of the Transaction on markets for flights MSS, hotels MSS, and car rentals MSS and a broader market for "all travel" MSS, as well as on markets for flights OTAs, hotels OTAs, and car rental OTAs and a broader market for "all travel" OTAs.

3.2.5. Commercial affiliate programmes

(52) In its previous decision practice, the Commission has not assessed commercial affiliate programmes in the travel sector.

(53) The Parties submit that commercial affiliate programmes offered by MSS are not in competition with those offered by OTAs. As MSS and OTAs provide their affiliate partners with access to their content and functionalities, the different business models of MSS and OTAs are mirrored in the commercial affiliate programmes they offer. Moreover, the Parties submit that the companies that enter into the commercial affiliate programmes offered by MSS are different from those which enter into the commercial affiliate programmes offered by OTAs. Companies which enter into affiliate programmes offered by MSS wish to offer consumers broad comparison services. These companies are typically general travel websites, travel blogs, small MSS entering new markets, etc. By contrast, companies which enter into affiliate programmes offered by OTAs wish to offer consumers the possibility to complete their travel bookings on a single website, such as TSPs which offer only one type of travel services (e.g. airlines which wish to also offer hotel or car rental bookings), or smaller OTAs wishing to expand, possibly into new travel service segments. Moreover, the Parties consider that commercial affiliate programmes should not be further segmented by type of travel service.

(54) The majority of respondents to the market investigation considered that the provision of commercial affiliate programmes by MSS is part of the overall market for the operation of MSS, notably as they view these programmes as an additional means for MSS to increase traffic to their websites. (25)

(55) Respondents are split as to whether commercial affiliate programmes offered by MSS are interchangeable with commercial affiliate programmes offered by OTAs. Some respondents point out the differences in the type of services offered by MSS and OTAs, whereas others indicate that they considered both OTAs and MSS when selecting the commercial affiliate programme they entered into, or that they have entered into affiliate programmes offered by both MSS and OTAs. (26)

(56) Last, respondents to the market investigation are rather split as to whether commercial affiliate programmes should be further segmented on the basis of the type of travel services they cover, namely between flights, hotels and car rentals. (27)

(57) In any event, the Commission considers that it may be left open whether commercial affiliate programmes constitute a distinct market or are part of broader markets for the operation of MSS and OTAs, Similarly, it may be left open whether potential markets for commercial affiliate programmes should be further segmented, based on whether these are offered by MSS or OTAs, or by type of travel services. This is because the Transaction would not raise serious doubts, irrespective of whether any of these further possible segmentations are taken into account.

3.2.5.1. Conclusion

(58) Therefore, the Commission concludes that, for the purposes of this Decision, whether there are distinct markets for the provision of commercial affiliate programmes by MSS and OTAs and the exact delineation thereof can be left open, as the Transaction does not raise serious doubts under any such plausible product market definition. The Commission will therefore assess the impact of the Transaction on potential markets for commercial affiliate programmes offered by MSS, by OTAs, and on broader potential markets for commercial affiliate programmes offered by both MSS and OTAs. Similarly, the Commission will assess the impact of the Transaction on potential markets for commercial affiliate programmes for flights, for hotels and for car rentals, as well as on broader potential markets for commercial affiliate programmes for all types of travel services.

3.3. Relevant geographic markets

3.3.1. MSS and OTA markets

3.3.1.1. Commission and national competition authorities' decision practice

(59) In its previous decision practice in the travel sector, the Commission has considered that, notably due to language barriers, markets for the distribution of various types of travel services are likely to be national. (28)

(60) National competition authorities in the EEA have also assessed markets for MSS and OTAs on a national basis; several of them, however, with a focus on hotel OTAs. (29)

3.3.1.2. Parties' views

(61) The Parties submit that most major MSS, OTAs and TSPs are active on an EEA or global basis. Moreover, smaller players which originally had a national focus seek to expand their activities also to other EEA regions. Therefore, the Parties consider that the geographic scope of MSS and OTA markets may be broader than national.

3.3.1.3. Commission's assessment

(62) The majority of MSS that responded to the market investigation considered that competition among MSS takes place at global level. However, several respondents specified that MSS compete both at global level, mainly with other major MSS for brand awareness, and at national level also with domestic MSS to increase their traffic in specific countries. (30)

(63) The majority of MSS that responded to the market investigation also indicated that they differentiate their products between countries. Some respondents noted that they are active only in one or only in some EEA countries. Other respondents, with a broader geographic footprint, explained that they operate in different languages, provide price information in different currencies, cooperate with different TSPs and OTAs, and adjust the results they display according to their relevance for the specific country. (31) Conversely, the majority of respondent OTAs and TSPs indicated that they purchase the same type of MSS services across the EEA, notwithstanding differences in language or in prices and revenue-sharing arrangements.(32)

(64) The majority of OTAs that responded to the market investigation said that they offer the same type of services across the EEA, without differentiating between the various EEA countries. A number of respondents acknowledge, however, that they are active only in some EEA countries, or that they make adjustments to the services they provide, in terms of language, payment systems, ancillary services and inventory. (33)

(65) When asked about their ability to expand to other EEA countries, the majority of MSS that responded to the market investigation said that it would depend on certain factors. On the one hand, such expansion would not require significant investment in terms of the product offered and the technology used. On the other hand, an MSS which wished to begin operating in a new EEA country would have to invest in building relationships with TSPs that serve that country and on advertisement and marketing activities to raise awareness of its brand. (34)

(66) When asked about their ability to expand their activities to other EEA countries, respondent OTAs were rather split, some noting that even if they could start operations, raising awareness of their brand and establishing a customer base in a new country could be challenging. Moreover, they might need to make some further adjustments, such as adapting their payment systems to comply with national regulation, and ensuring local support for customer services. (35)

(67) As regards the contracts between MSS and OTAs, the majority of respondents to the market investigation said that the contracts are global in scope.36 However, when asked about the geographic level at which prices or revenue-sharing arrangements are determined, the majority of respondents noted that these are decided at country level.37 TSPs describe their contracts with MSS and OTAs as global in scope, however their responses are split as regards the geographic scope of the payment arrangements, as some indicate that the same arrangement applies world-wide, whereas others point out that payments are based on a bidding process and therefore amounts may vary significantly or that ad hoc agreements are made for specific countries. (38)

(68) As the Transaction would not raise serious doubts, irrespective of whether global, EEA-wide or national markets are taken into account, the exact delineation of the geographic markets may be left open.

3.3.1.4. Conclusion

(69) Therefore, for the purposes of this Decision, the Commission concludes that the exact geographic scope of MSS and OTA markets may be left open. The Commission will assess the impact of the Transaction at global, EEA-wide and national level.

3.3.2. Commercial affiliate programmes

(70) The Parties submit that markets for commercial affiliate programmes are at least EEA-wide, as travel companies which wish to enter into a commercial affiliate programme are interested in the content and scale of the inventory, and the functionalities offered by the provider of the commercial affiliate programme and not in the provider's market position in a specific EEA country. Moreover, the companies which offer commercial affiliate programmes are often larger companies with a global presence and the agreements they enter into to provide commercial affiliate services usually cover multiple countries, if not the world, as for example the commercial affiliate agreement between Momondo and the OTA HotelsCombined, under which Momondo obtains hotel inventory and booking functionality from HotelsCombined.

(71) The majority of respondents to the market investigation also indicated that the scope of the commercial affiliate programmes they offer or have entered into is global. Some, however, specify that affiliates may choose to restrict the programme only to certain regions. (39)

(72) Therefore, the Commission considers that the geographic scope of any potential market for commercial affiliate programmes would be likely to be global. However, as the Transaction would not give rise to serious doubts under any plausible geographic market definition, the exact geographic delineation may be left open.

3.3.2.1. Conclusion

(73) Therefore, the Commission considers that, for the purpose of this Decision, the geographic scope of potential markets for commercial affiliate programmes may be left open. The Commission will assess the impact of the Transaction at global, EEA-wide and national level.

4. COMPETITIVE ASSESSMENT

4.1. Overview of affected markets

(74) According to the Parties, no reliable and comprehensive public source of market share data is available in the MSS sector. The Parties have therefore provided their best estimates of Priceline's and Momondo's market shares, and the shares of their competitors in the various potential EEA markets for "all travel" MSS and for each of the three types of travel service analysed in this Decision (namely flights, hotel accommodation and car rentals) on the basis of their revenues. (40)

(75) Moreover, the Parties have submitted, in addition to their best estimates as to their own and their competitors market shares on the basis of the turnover generated, information on how frequently various MSS are searched for in Google's general search, their best estimates of the number of visitors to their own and to rival MSS (informing their estimates with Alexa and Comscore data) and a number of industry reports (such as notably reports by Skift and PhocusWright). Even though these data do not allow a precise estimation of the Parties' market shares, they confirm the presence of several competitors on the various EEA markets, and the fact that these competitors enjoy material brand awareness and are perceived as competing with the Parties.

(76) In addition to the estimates provided by the Parties, the Commission has sought to gather data on the revenues generated by and the number of visitors to the Parties' MSS competitors, both for "all travel" MSS services and for each of flights and hotels MSS, at EEA level and in the affected national markets. (41) While the Parties appear to have overestimated the market shares of some of their competitors, the market investigation generally confirmed the existence of alternative players in all the affected markets, as claimed by the Parties.

(77) As regards their market shares on potential OTA markets, the Parties were not able to provide reliable data. However, as Priceline's Booking.com is one of the leading hotel OTAs in most EEA countries and after comparing their […] revenues with the total market size, as estimated in industry reports (42), the Parties have assumed that all potential national markets for hotel OTAs and for "all travel" OTAs would give rise to vertically affected markets.

(78) Table 1 below provides an overview, based on the Parties' estimates, of the horizontally and vertically affected markets which would arise as a result of the Transaction.

(80) Both Parties are active, on the one hand, in the operation of flights and hotels MSS in a number of countries and, on the other hand, Priceline operates OTAs. (44) The Parties' activities would therefore give rise to a number of vertically affected markets, as detailed in Section 4.4 below.

(81) Last, if distinct markets for the provision of commercial affiliate programmes were considered, the Transaction would not result in any horizontally affected market, but would give rise to vertically affected markets between the broader upstream market for the provision of hotels commercial affiliate programmes by MSS and OTAs and the downstream operation of hotels MSS.

4.2. Sectoral overview

(82) In 2016, the EEA MSS sector had an estimated value of around EUR [1-1.5] billion (45) and the sector is generally growing across the EEA. (46)

(83) The Parties' MSS activities in the EEA are geographically complementary: while Priceline's brands are stronger in Austria and Germany, Momondo's brands have a focus in the Nordic region.

(84) In addition to the Parties, other MSS active in the EEA include large global players, such as Skyscanner, Google Flights and Google Hotels, Trivago and TripAdvisor, as well as a number of well-established national players such as Jetcost, Idealo, Liligo, Easyvoyage, Check24.at, and Flyrejser.dk.

(85) At a global level, for "all travel" MSS, on the basis of the Parties' estimates, it appears that Priceline's and Momondo's market shares would be around [5-10]% and [0-5]% respectively. When considering narrower potential MSS markets for particular types of travel service, the Parties' combined global market share would be [10-20]% (increment [5-10]%) for flights, [0-5]% (increment less than [0-5]%) for hotels, and [10-20]% for car rentals (as Momondo operates as an OTA, there is no increment on a car rental MSS market).

(86) On a potential EEA-wide market for "all travel" MSS, on the basis of the Parties' estimates it appears that their combined market share to be around [10-20]%. When considering narrower potential EEA-wide markets for flights MSS, hotels MSS and car rentals MSS, the Parties are stronger in flights MSS, achieving a combined market share of approximately [10-20]%. Competitors operating MSS websites in the EEA for various types of travel services include Google, Trivago, TripAdvisor and Skyscanner, as well as smaller players such as Jetcost, TravelSupermarket, Billiger-mietwagen, Check24 and HotelCombined.

4.3. Horizontal effects

(87) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular as a result of the creation or strengthening of a dominant position.

(88) In the present case, the assessment of the compatibility of the Transaction with the internal market will essentially focus on non-coordinated horizontal effects on potential MSS markets affected by the Transaction (see Table 1 above).

(89) Non-coordinated effects may significantly impede effective competition by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour. The factors listed in paragraphs 27 onwards of the Horizontal Merger Guidelines may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, but not all of these factors need to be present to make significant non-coordinated effects likely, and the list is not exhaustive. (47) The presence of these factors may though have an impact on the degree of horizontal non-coordinated effects arising from the transaction.

(90) The Commission will first present the elements common to the assessment of the Transaction that cut across the different EEA countries (Section 4.3.1), before undertaking a more detailed analysis on a country by country basis (Section 4.3.2).

4.3.1. Elements common to the assessment of the MSS markets in the EEA

(91) The Commission has considered several elements, which are relevant for the assessment of the effects of the Transaction across the EEA countries. These elements include how the Parties negotiate commercial terms with customers (Section 4.3.1.1), closeness of competition between the Parties (Section 4.3.1.2), and the barriers to entry or expansion (Section 4.3.1.3).

4.3.1.1. Negotiation with customers

(92) Respondents to the market investigation indicate that negotiations between MSS and OTAs and TSPs are mainly conducted bilaterally for the full inventory. MSS bargaining power in such negotiations may vary depending on the importance of the OTA or TSP. (48) The main features on the basis of which MSS suppliers are generally selected include (i) the quality of their products, (ii) their volume of traffic and geographic coverage, (iii) the reputation of the MSS and (iv) the prices or cost/revenue-sharing arrangement proposed. (49) While negotiations between large players appear to take place at global level, prices are negotiated at national level and service features, such as language, layout and sometimes content may vary between EEA countries. Finally, the duration of the contract may vary from one to five years, with usually either party having the possibility to terminate the contract at short notice. (50)

(93) The majority of respondents to the market investigation indicate that OTAs and TSPs purchase services from more than one MSS per EEA country, and that this is in line with their commercial policy, notably "not to limit the amount of MSS in each country", "to increase the traffic on their website" and "to ensure brand visibility which is key in the travel industry". (51)

(94) As regards the bargaining power of the MSS and OTAs, while it seems to vary based on the relative market position of the MSS or OTA, respondents to the market investigation point out that it is in the interest of both MSS and OTAs to cooperate with, respectively, several OTAs and MSS. On the one hand, MSS have incentives to contract with as many OTAs as possible, in order to allow their end users to compare a wide range of offers for the travel products they are interested in. On the other hand, OTAs and TSPs also have incentives to contract with as many MSS as possible, to increase the visibility of their offerings and ensure that their prices are shown to as many potential customers as possible. In this respect, "while the main drivers of competition are based on traffic, price and geographic scope, OTAs need to work with all MSS". (52)

(95) The Commission considers that it is unlikely that the Transaction would significantly impact the negotiating power currently held by Parties vis-à-vis their customers. First, the Parties' business model, which is the same as that of most other MSS, will remain unchanged post-Transaction. Second, the Parties' combined market share at global and EEA level is relatively small both for "all travel" MSS as well as when narrower potential MSS markets for particular types of travel services are considered, (53) which means that the merged entity would risk losing its OTA and TSP customers to other MSS, if it changed its negotiating strategy. Third, the increment brought about the Transaction is limited,, therefore the merged entity will not have a materially stronger market position than Priceline or respectively Momondo already have today.

(96) In light of these considerations, the Commission concludes that the proposed Transaction is not likely to significantly increase the Parties' negotiating power towards their OTA and TSP customers in EEA MSS markets.

4.3.1.2. Closeness of competition

(97) According to the Horizontal Merger Guidelines, a merger between close competitors is more likely to have anticompetitive effects and lead to a significant increase in price. The higher the degree of substitutability between the merging firms' products, the more likely it is that the merging firms will raise prices significantly. The purpose of assessing the closeness of competition between the Parties is therefore to determine whether they currently exert a significant competitive constraint on each other which would be removed post-Transaction, and whether other suppliers would be able to sufficiently constrain the Merged Entity. (54)

(98) For the purposes of the present Transaction, it is therefore relevant to assess whether Piceline's and Momondo's brands are close substitutes.

(99) The Commission notes that within the EEA, the Parties' have a different geographic focus and their activities are rather complementary from a geographic point of view and that they are not each other's main competitor in any EEA country. Kayak was originally stronger in the US, whereas Momondo is EEA-based, starting operating in Denmark and remains strongest in the Nordic countries. Therefore, still today in EEA countries where Momondo has a strong market position, Kayak is generally weak and vice versa. (55) Moreover, the range of services offered by the Parties is somewhat different. Whereas Kayak has developed its own inventory in relation to all of flights, hotels and car rental services, Momondo only has its own inventory for flights and relies on commercial affiliate relationships for its hotels and car rental inventory. Therefore, Momondo, unlike Kayak, does not have established relationships with OTAs and TSPs in relation to hotels and car rentals.

(100) The majority of respondents to the market investigation also indicate that the Parties are not close competitors, and that the activities of Priceline and Momondo are rather complementary. (56) Conversely, when asked to identify Priceline's closest competitor in potential markets for "all travel" MSS and for flights MSS in the EEA, the majority of the respondents point to Skyscanner. (57) Skyscanner is also identified as the closest competitor to Momondo by the majority of respondents, followed by Priceline, Trivago, Google, and other national players. (58)

(101) In light of the above, the Commission concludes that the Parties' brands do not compete closely with each other in the EEA in general or in any specific EEA country in particular.

4.3.1.3. Barriers to entry or expansion

(102) When entering a market is sufficiently easy, a merger is unlikely to pose any significant anti-competitive risk. For entry to be considered a sufficient competitive constraint on the merging parties however, it must be shown to be likely, timely and sufficient to deter or defeat any potential anti-competitive effects of the merger. (59) As some mergers could significantly impede competition by enabling the merged entity to make the expansion of smaller firms and potential competitors more difficult, the impact of the Transaction on the Parties' competitors' ability to enter or expand will be assessed. (60)

(103) The Parties claim that there are no significant barriers to entry for a new MSS. The investment costs for entering the MSS market are limited, including creating a website, marketing activities to raise brand awareness, entering into contracts with OTAs and TSPs and obtaining the technology to compare prices. In particular, a MSS could easily enter into an arrangement with a commercial affiliate programme supplier and rely on the contracts and technology of the latter. (61)

(104) A majority of respondents to the market investigation indicate that, in general, barriers to enter in the MSS market are not insignificant. Critical factors for success in the MSS market, as identified by some competitors and customers, include having a well-known brand, financial strength to sustain investments and an effective marketing strategy, since brand awareness is important for MSS to establish relationships and negotiate with OTAs and TSPs and to generate traffic to their websites. (62)

(105) There are, however, examples of recent market entry in MSS markets in the EEA, including Google Hotels and Google Flights and Idealo. There are also examples of expansion by MSS that were active in one type of travel services and have expanded into others, such as TripAdvisor expanding its activity from the hotels segment to the flights segment, and KAYAK expanding from its traditionally […] position in flights also into hotels. (63)

(106) Specifically in relation to Google, even though it is a recent entrant in the EEA, having launched Google Hotels in 2011 and Google Flights in 2013, it already appears well placed to exercise material competitive pressure on other MSS. As the main barrier to entry identified is brand awareness, Google is better placed to grow quickly as opposed to a new operator not known to the market. Moreover, several respondents to the market investigation point out that the main impact currently identifiable on MSS markets is the entry and expansion of Google Hotels and Google Flights rather than the Transaction. (64)

(107) Similarly, respondents to the market investigation also consider that barriers to expansion are lower than barriers to entry, given that the technical investments appear to be much lower and suppliers will likely be able to use their existing customer relationships. In this respect, the market investigation also revealed that a number of competitors are planning expansion projects in the EEA in the coming years. (65)

(108) Finally, the majority of the respondents to the market investigation consider that the Transaction will not have an impact on potential barriers to entry/expansion in the EEA. (66)

(109) Based on the above, the Commission notes that a number of entries in the MSS market have occurred in the EEA over the past years. This indicates that, while barriers to entry and expansion in the MSS market may be material, MSS markets remain attractive for potential and expanding players. As a result, potential new entrants or MSS which are already present and may expand their service offer are likely to exercise a competitive constraint on the merged entity post-Transaction.

4.3.2. Market-specific analysis of affected markets

4.3.2.1. Introduction

(110) According to the Horizontal Merger Guidelines, "the larger the market share, the more likely a firm is to possess market power. And the larger the addition of market share, the more likely it is that a merger will lead to a significant increase in market power... Although market shares and additions of market shares only provide first indications of market power and increases in market power, they are normally important factors in the assessment." (67)

(111) When replying to the market investigation, some competitors claim that post- Transaction the merged entity will have a significant market position in a number of EEA countries and that competition will be reduced.

(112) The Commission considers that Transaction will not give rise to competition concerns, for the following reasons.

(113) First, the Parties are small players in the travel MSS market across Europe and, although in some national markets the Parties' combined market share is significant (that is in Austria and Denmark), the increment brought about the Transaction is limited, both at EEA and at national level, even when considering a possible narrower segmentation of MSS markets by type of travel service.

(114) Second, the Parties' activities are geographically complementary: at national level, in EEA countries in which Momondo's brands have a stronger position (that is in the Nordic region), Priceline is much weaker, with a market share estimated as no more than [0-5]%. Conversely, in EEA countries where Priceline's brands have a stronger position (such as Austria and Germany), Momondo's brands are much weaker, with a market share of approximately [5-10]% or less.

(115) Third, as also shown by the market investigation, the Parties will continue to be constrained by a number of major MSS that are active globally and in the affected markets, such as Skyscanner, Google with its specialised search MSS Google Flights and Google Hotels, Trivago and TripAdvisor, as well as a number of well- established national players such as Jetcost, Idealo, Liligo and Easyvoyage. Google has become a major competitor to existing travel MSS in recent years. Google has already become the market leader in the US, where its two MSS brands were launched in 2011, and a comparable strengthening of its market position is likely to materialise also in Europe. As also noted by an industry report, Google is on the cusp of being one of the globe’s most important metasearch companies. (68)

(116) Finally, the majority of respondents to the market investigation, including MSS, OTAs and TSPs, did not raise any competition concerns with respect to the Parties' position in the EEA or at national level. (69)

4.3.2.2. Austria – markets for "all travel" MSS and MSS for flights

Parties' activities

(117) On the basis of the Parties' estimates, it appears that Priceline's and Momondo's combined market share would be moderate for "all travel" MSS in Austria, amounting to around [30-40]%, with an increment of [0-5]%.

(118) On a narrower potential market for flights MSS, the Parties' combined market share amounts to [60-70]%. However, the increment is marginal and amounts to [0-5]%.

Commission's assessment

(119) Even though the market for "all travel" MSS and the narrower potential market for flights MSS in Austria would be affected, the increment brought about by the Transaction would be limited, as Momondo generated EUR […] of turnover in Austria in 2016, EUR […] of which through its flights MSS. (70) Therefore, there would be no material Transaction-specific effect in Austrian MSS markets.

(120) Multiple competitors remain in the "all travel" MSS market in Austria, such as Trivago, TripAdvisor, Google, and Skyscanner. In addition, the merged entity will continue to face competition from a number of smaller MSS, including Check24.at, Billiger-mietwagen, Idealo.at and Jetcost.

(121) Several competitors will also continue to significantly compete in flights MSS in Austria, such as Skyscanner, with a market share materially higher than that of Momondo. TripAdvisor, Idealo, and Jetcost are also active on the Austrian market for flights MSS, with market shares comparable to that of Momondo. Moreover, Google Flights entered the Austrian market in 2015 and is expected to further strengthen its market position, especially in light of consumer awareness of the Google brand.

(122) The existence of additional competitors as well as the marginal presence of Momondo for flights MSS in Austria is also confirmed by Google Trend data. In particular, Checkfelix (a KAYAK brand) is the most searched for MSS in Austria, consistent with its market position, followed by Skyscanner, which has been steadily growing in popularity over the past five years, and has overtaken Swoodoo (a KAYAK brand) which has been declining in popularity over time. Searches for Google Flights have also started to grow rapidly since the beginning of 2015 and have overtaken all the remaining MSS. (71)

(123) Similarly, when looking at the frequency with which different MSS appear in the first page of the search results generated on Google in Austria in response to popular flight-related searches, KAYAK's brand Checkfelix is second in terms of average ranking, just behind Google Flights, appearing on the first page of the results in 90% of the searches and in the top three results in 85% of the searches. The OTA Opodo and the TSP Swiss have higher ranking than any MSS in flights related searches. Skyscanner appears on the first page in 90% of searches and in the top three results 15% of the time. Momondo does not appear in the top three results at all and appears on the first page in just 10% of searches. (72)

(124) As regards barriers to entry, the analysis in Section 4.3.1.3. above is also applicable in Austria. While barriers to entry may not be insignificant, the MSS market in Austria remains attractive for potential players that can use a brand known in other sectors/activities as demonstrated by the recent entry of Google Flights and TripAdvisor. Respondents to the market investigation also confirmed that the expansion of an already active MSS supplier would be easier as "the technical investment is much lower" and "an existing MSS would have a certain advantage in that their brand may be known to end users". In this respect, a number of competitors confirmed their interntion to enter or expand in a number of EEA countries and that their plans would not change because of the merger. (73)

(125) Finally, the majority of respondents to the market investigation considers that the Transaction will not have a negative impact on the "all travel" MSS market in Austria or on the flights MSS segment in Austria. (74)

Conclusion

(126) The Commission thus concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in respect of the market for MSS in Austria, under any plausible segmentation.

4.3.2.3. Denmark – markets for "all travel" MSS, MSS for flights and MSS for hotels

Parties' activities

(127) On the basis of the Parties' estimates, it appears that Priceline's and Momondo's combined market share would amount to [50-60]% for "all travel" MSS in Denmark, with an increment of less than [0-5]%.

(128) On a narrower potential market for flights MSS, the Parties' combined market shares is estimated at [60-70]%. However, the increment is marginal and amounts to less than [0-5]%.

(129) On a narrower potential market for hotels MSS, the Parties' combined market shares is estimated at [20-30]%, with an increment of less than [0-5]%.

Commission's assessment

(130) The increment brought upon by the Transaction for "all travel" MSS, flights MSS and hotels MSS would be very limited, as KAYAK generated approximately EUR […] across all travel in Denmark in 2016, of which EUR […] in flights. (75) Therefore, there would be no material Transaction-specific effect in these markets.

(131) Multiple competitors continue to significantly compete in the market for "all travel" MSS, such as Google, which recently entered (in 2014) and is expected to quickly strengthen its market position, Travelmarket, TripAdvisor, Skyscanner, Trivago and Flyrejser. The Parties submit that all of these MSS rivals have a market share greater than that of KAYAK in Denmark.

(132) Several competitors will also continue to significantly compete in flights MSS, such as Skyscanner, Flyrejser, Jetcost, Google Flights, TripAdvisor and Travelmarket.

(133) As regards hotels MSS, other important MSS that will continue to significantly compete post-Transaction are Trivago, TripAdvisor, Travelmarket, Skyscanner and Google Hotels.

(134) The existence of active competitors as well as the marginal presence of Kayak for flights MSS in Denmark is also confirmed by Google Trend data. While Momondo has consistently been the most searched for MSS on Google in Denmark in the last five years, consistent with its market position, TripAdvisor and Skyscanner are the second and third most searched-for MSS in Denmark, and their popularity has remained broadly the same over the last five years. Searches for Flyrejser have decreased during this period, although it still remains number four overall. Very few consumers search for KAYAK, and it is by far the least popular MSS in terms of consumer searches in Denmark. (76)

(135) Similarly, the Parties estimate on the basis of Alexa data how traffic to flights MSS, namely number of unique visitors, is distributed among the various providers in Denmark. While Momondo receives [30-40]% of the overall traffic, Google Flights (as estimated by the Parties) and TripAdvisor also receive a significant proportion of the overall traffic, namely [20-30]% and [10-20]% respectively, followed by Travelmarket and Skyscanner receiving [5-10]% and [5-10]% of the overall traffic respectively. KAYAK by contrast receives only a [0-5]% of the overall traffic. (77)

(136) As regards barriers to entry, the analysis in Section 4.3.1.3. above is also applicable to Denmark. While barriers to entry may not be insignificant, the MSS market in Denmark remains attractive for potential players, as demonstrated by the recent entry of for example for Google (in 2013) and Idealo (in 2014). A number of competitors also confirmed their intention to enter or expand in a number of EEA countries, including the Nordic countries and that their plans would not change because of the merger. (78)

(137) Finally, the majority of respondents to the market investigation considers that the Transaction will not have a negative impact on the market for "all travel" MSS or the flights MSS or hotels MSS segments in Denmark. (79)

Conclusion

(138) The Commission thus concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in respect of the market for MSS in Denmark, under any plausible segmentation.

4.3.2.4. Germany - MSS for flights

Parties' activities

(139) On the basis of the Parties' estimates, it appears that Priceline's and Momondo's combined market share would be [20-30]% for flights MSS in Germany, with an increment of [5-10]%.

Commission's assessment

(140) The increment brought about by the Transaction on the German market for flights MSS is not significant, around [5-10]%, and the Parties' combined market share is well below [30-40]%, so that there would be no material Transaction-specific effect in this market.

(141) Additional competitors are active and will remain present in the flights MSS market, such as Skyscanner, Google Flights, and Idealo. A number of smaller MSS are also present such as TripAdvisor and Liligo.

(142) Finally, the majority of respondents to the market investigation considers that the Transaction will not have a negative impact with respect to flights MSS in Germany. (80)

Conclusion

(143) The Commission thus concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in respect of the market for flights MSS in Germany.

4.3.2.5. Portugal – MSS for flights

Parties' activities

(144) On the basis of the Parties' estimates, Priceline's and Momondo's combined market share would be [20-30]% on a market for flights MSS in Portugal, with an increment of [0-5]%.

Commission's assessment

(145) The increment brought upon by the Transaction for flights MSS is only [0-5]% and the Parties' combined market share is well below [30-40]%, so that there would be no material Transaction-specific effect in this market.

(146) Additional competitors are and will remain active in flights MSS in Portugal, such as Google Flights, Skyscanner, Jetcost, and TripAdvisor.

(147) Finally, the majority of respondents to the market investigation considers that the Transaction will not have a negative impact on the market for flights MSS in Portugal. (81)

Conclusion

(148) The Commission thus concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in respect of the market for flights MSS in Portugal.

4.3.2.6. Sweden – "all travel" MSS, MSS for flights and MSS for hotels

Parties' activities

(149) On the basis of the Parties' best estimates, Priceline and Momondo's combined market share would be [20-30]% for "all travel" MSS in Sweden, with an increment of [0-5]%.

(150) On a narrower potential market for flights MSS, the Parties estimate their combined market share as [20-30]%, with an increment of less than [0-5]%.

(151) On a narrower potential market for hotels MSS, the Parties estimate their combined market share as [20-30]%, with an increment of less than [0-5]%.

Commission's assessment

(152) The increment brought upon by the Transaction is very small (around [0-5]%) and the Parties' combined market share also remains below [30-40]% under all plausible market definitions, so that there would be no material Transaction- specific effect in these markets.

(153) Additional competitors are and will remain active in a market for "all travel" MSS, as well as in the potential narrower MSS markets for flights and hotels, such as Google, TripAdvisor, Skyscanner, Trivago, Roseguiden and Destination.

(154) Finally, the majority of respondents to the market investigation considers that the Transaction will not have a negative impact the market for "all travel" MSS, flights MSS or hotels MSS in Sweden.

Conclusion

(155) The Commission thus concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in respect of the market for MSS in Sweden, under any plausible segmentation.

4.3.3. Conclusion

(156) In view of the above, the Commission considers that the Transaction does not raise any serious doubts as regards its compatibility with the internal market, as regards the Parties' horizontal overlaps.

4.4. Vertical effects

(157) As indicated in Section 4.1 above, the Transaction gives rise to two types of vertical relationships between the Parties, namely: (i) between the Parties' MSS activities upstream and OTA activities downstream and (ii) between the provision of commercial affiliate programmes by the Parties' MSS and OTAs upstream and the operation of flights and hotels MSS downstream.

4.4.1. Vertical link between MSS upstream and OTAs downstream

(158) Both Parties are active in the operation of MSS in a number of EEA countries and operate MSS offering different types of travel services, namely flights, hotels and, for Priceline only, also car rentals.

(159) Priceline is already vertically integrated, as it also operates OTAs. In the EEA, it is active through its hotels OTA, Booking.com, which has a material market position in all EEA countries and with its car rental OTA, Rentalcars.com. In flights OTA, Priceline has a very limited activity through its OTA Priceline.com. Priceline.com is heavily focused on US markets and is almost unknown in the EEA. Momondo is only active in car rental OTAs.

(160) To the extent that OTAs purchase lead generation services from MSS, paying MSS a commission or fee to be listed on the MSS website together with other competing offers, there exists a vertical relationship between MSS upstream and OTAs downstream.

(161) In light of the various possible delineations of the relevant markets, as set out in Section 3, the Parties' activities would give rise to a number of potential vertically affected markets, as detailed below:

a. The Parties estimate that their combined market share on a flights MSS market would exceed 30% in Austria and Denmark (namely [60-70]% in Austria and [60-70]% in Denmark); therefore, vertically affected markets would arise between the operation of flights MSS by the Parties and the operation of flights OTAs by Priceline in Austria and Denmark, where Priceline's estimated market shares are below 1%. The only flights OTA operated by the Parties is Priceline.com, the content of which is not available in any language other than English, […]. If OTA product markets were considered broader in scope, comprising "all travel" OTAs, the Parties estimate their combined market share as exceeding [20-30]%, mainly as a result of the presence of Priceline's Booking.com. Therefore, vertically affected markets would exist between the operation of flights MSS by the Parties and the operation of OTAs in the EEA and in all EEA countries, in which Momondo is active, namely in Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Romania, Spain, Sweden and the UK.

b. The Parties estimate that on markets for "all travel" MSS, their combined market share would exceed 30% in Austria and Denmark (namely [30-40]% in Austria and [50-60]% in Denmark); therefore vertically affected markets would exist between the operation of MSS by the Parties and (i) the operation of flights OTAs by Priceline in Austria and Denmark (with the market shares of Priceline.com being estimated at less than 1%); (ii) the operation of hotels OTAs by Priceline in the EEA and in all EEA countries, in which Momondo is active (where Priceline estimates that its market share would exceed [20-30]%, mainly through the activities of Booking.com) and (iii) the operation of car rental OTAs by the Parties in Austria and Denmark, where the Parties estimate their market shares as lower than [20-30]%. If OTA product markets were considered broader in scope, comprising "all travel" OTAs, vertically affected markets would exist between the operation of MSS by the Parties and the operation of OTAs in the EEA and in all EEA countries, in which Momondo is active, since the Parties estimate their combined market share as exceeding [20-30]%, mainly through the activities of Booking.com.

c. The Parties estimate that on markets for hotels OTAs, Priceline's market share would exceed [20-30]% in the EEA and in all EEA countries, mainly through the activities of Booking.com. Therefore, vertically affected markets would exist between the operation of hotels MSS by the Parties (where the Parties estimate their combined market shares as below 30% in the the EEA all EEA countries, in which both Parties are active) and Priceline's hotels OTA activities, at EEA level and in all EEA countries in which Momondo is active.If MSS product markets were considered broader in scope, comprising "all travel" MSS, vertically affected markets would exist between the operation of "all travel" MSS by the Parties (where the Parties' market shares are estimated at [30-40]% in Austria and [50-60]% in Denmark) and Priceline's hotels OTA activities at EEA level and in all EEA countries in which Momondo is active.

d. The Parties estimate that on markets for "all travel" OTAs, Priceline's market share would exceed [20-30]% in the EEA and in all EEA countries, mainly through the presence of Booking.com. Therefore, vertically affected markets would exist between, on the one hand, the operation of flights MSS and hotels MSS by the Parties and the operation of car rental MSS by Priceline and, on the other hand, Priceline's "all travel" OTA activities at EEA level and in all EEA countries in which Momondo is active.

If MSS product markets were considered broader in scope, comprising "all travel" MSS, vertically affected markets would exist between the operation of "all travel" MSS by the Parties and Priceline's "all travel" OTA activities, at EEA level and in all EEA countries in which Momondo is active.

(162) In assessing these vertical relationships, it is appropriate to consider whether the Parties could pursue a strategy of input foreclosure, whereby they would delist from their MSS OTAs which compete with them on potential downstream OTA markets. It is also appropriate to consider whether the Parties could pursue a strategy of customer foreclosure, whereby they would withdraw their OTAs from rival MSS upstream and list their OTAs only on the Parties' own MSS.

4.4.1.1. Input foreclosure

(163) According to the Non-horizontal Merger Guidelines, in order to assess the likelihood of the merged entity following an input foreclosure strategy, the merged entity should have the ability and the incentive to adopt such strategy. Moreover, for an input foreclosure strategy to be anti-competitive and raise serious doubts as to the compatibility of the Transaction with the internal market, such strategy would have to produce anti-competitive results. (82)

(164) For the merged entity to be able to adopt an input foreclosure strategy, it would need to have a significant degree of market power on the upstream MSS market that would allow it to restrict access to or raise the cost of its lead generation services to rival OTAs. (83) Therefore, such strategy could only be followed in Austria and Denmark, where the Parties' flights MSS and "all travel" MSS have a material market position.

(165) Downstream, the markets that are primarily vertically related are the markets for flights OTAs. Depending on the market definition considered, the number of affected markets is greater, as seen in the Table in para. 77 above, as broader markets comprising "all travel" OTAs would also be vertically related. Similarly, if broader markets for "all travel" MSS in Austria and Denmark are considered, markets for hotels OTAs, car rental OTAs and "all travel" OTAs would also be vertically affected. However, any foreclosure of lead generation services would originate from flights MSS, since this is the market segment in which the merged entity would have a strong market position and potentially exert some market power. Consequently, even on a broader market for "all travel" OTAs, what would be impacted by such input foreclosure strategy would be the traffic directed to flights OTAs. Therefore, the input foreclosure analysis will mainly focus on the relationships between flights MSS and flights OTAs.

(166) When asked on whether the merged entity would have the ability to restrict OTAs' access to MSS lead generation services or increase the cost of such services, respondents to the market investigation were rather divided. Whereas some respondents do not exclude that the merged entity will have the ability to display its own OTAs in a more favourable way, other respondents point out that there will be sufficient competition to prevent the merged entity from increasing the cost of advertising and that in a business where transparency to consumers is key, this type of foreclosure will not occur. (84)

(167) The Parties compete with a number of other MSS operators in Austria and Denmark, such as Skyscanner - which has a market position stronger than, respectively, Momondo and Priceline, Google Flights - a recent entrant with significant growth potential, TripAdvisor and others. OTAs in Austria and Denmark would thus still have the possibility to still advertise their services on other MSS and would not be fully reliant on the Parties. Already today, OTAs purchase lead generation services from multiple MSS; the majority of respondents to the market investigation indicating that OTAs (as well as TSPs) purchase services from more than three MSS per EEA country, in order to increase traffic to their websites and reach as many consumers as possible. (85)

(168) Moreover, MSS are not the only source of traffic for OTAs. Consumers may also reach OTA websites through direct visits, to the extent that the OTA is known to them, by following advertisments on blogs, travel websites, etc., through general search e.g. on Google or Bing, or through other sources, such as e-mail marketing, marketing on social media, etc. OTAs responding to the market investigation estimate that approximately half of their traffic comes through MSS referrals, whereas the other half is split among the other channels. (86)

(169) In relation to Austria, even if the Parties have a material market position in flights MSS markets, the increment of the Transaction is rather limited, amounting, according to the Parties' estimation, to market shares of [0-5]%. Therefore, the merged entity's market position, and consequently also its ability to follow an input foreclosure strategy, will not be materially increased relative to that of Priceline already today in the Austrian market. Priceline currently has a market share of [60-70]% on flights MSS in Austria and is vertically integrated, also operating flights OTAs; yet there is no evidence of Priceline attempting to restrict or increase the cost of rival OTAs' access to its MSS lead generation services.

(170) The situation is different in Denmark, where the market share of the already integrated Priceline on MSS markets is very limited, estimated as approximately [0-5]%, and Momondo is the market leader on flights MSS, with a market share estimated at [60-70]%. Therefore, post-Transaction, the position of the merged entity on the upstream and downstream markets will be comparable to the current position of Priceline on the upstream and downstream markets in Austria.

(171) In light of the above, it cannot be excluded that the merged entity would have the ability to follow a input foreclosure strategy. However, it appears unlikely that the merged entity would have the incentive to do so.

(172) Respondents to the market investigation are rather split as to whether they consider that the merged entity would have the incentive to adopt an input foreclosure strategy, some mentioning that some change in the display of search results on the Parties' MSS may occur, whereas others point out that any such incentives would exist already, that MSS markets are competitive and that a foreclosure strategy could restrict the attractiveness of the Parties' MSS. (87)

(173) The Commission however considers unlikely that the merged entity would have incentives to foreclose its input, as it appears unlikely that such strategy would be profitable to it.

(174) On the downstream market for flights OTAs, the Parties have a marginal presence in the EEA through Priceline.com. Priceline.com is focused in the US, is not available in German, Danish or any EEA language other than English and […]. Priceline.com generated less than EUR […] million in 2016 in the EEA, corresponding to less than […]% of its total revenues. In Austria, it generated EUR […] and in Denmark EUR […] in the same period.

(175) On the upstream market for flights MSS, the Parties rely primarily on OTAs for their revenues: OTAs account for at least […]% of KAYAK's flights MSS revenues in the EEA and for […]% of Momondo's flights MSS revenues. By relying exclusively on TSPs and on Priceline's flights OTAs, the activities of which are marginal in the EEA, the Parties' MSS would thus in all likelihood incur losses. Similarly, by raising prices that would risk reducing the attractiveness of its MSS to OTAs and incentivising the latter to switch to other suppliers, the merged entity would forgo a material part of its revenues.

(176) It is therefore unlikely that the Parties would risk their flights MSS revenues, amounting to EUR […] million in Austria and EUR […] million in Denmark, to favour Priceline.com, which generates only a fraction of those revenues in the EEA.