Commission, December 6, 2017, No M.8687

EUROPEAN COMMISSION

Judgment

PRISKO / OKD NASTUPNICKA

Subject: Case M.8687 - Prisko / OKD Nástupnická

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 30 October 2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (3) by which Prisko a.s. ("Prisko", Czech Republic) will acquire, within the meaning Article 3(1)(b) of the Merger Regulation, control of the whole of OKD Nástupnická a.s. ("OKD", Czech Republic) by way of purchase of 100% of its shares (the "Transaction"). Prisko and OKD are collectively referred to as "Parties".

1. THE PARTIES AND THE OPERATION

(2) Prisko is a State-owned holding company whose shares are wholly owned by the Czech Republic via its Ministry of Finance ("MoF"). Prisko's main activity is the management of assets of the MoF of the Czech Republic.

(3) OKD is a private undertaking active in the market of production and sale of hard coal, and those ancillary activities necessary to it. (4) OKD produces coking and thermal coal that is mined in its four mines located in the Czech Republic. (5)

(4) Pursuant to a share purchase agreement entered into by OKD and Prisko on 6 April 2017, Prisko will purchase 100% of shares in OKD. No holding arrangement, special provisions or other safeguards are in place that would ensure that OKD retains a power of decision that is independent from Prisko after the transaction. Prisko will therefore acquire sole control of OKD within the meaning of Article 3(1)(b) of the Merger Regulation.

2. EU DIMENSION

2.1. Single economic unit

(5) Prisko and OKD on their own do not meet the thresholds set in Article 1 of the Merger Regulation. (6) However, as Prisko is a State-owned enterprise ("SOE") owned by the MoF, the question arises as to whether other SOEs owned by the Czech State should also be taken into consideration for the purpose of turnover calculation.

(6) When dealing with turnover calculation of SOEs, Article 5(4) of the Merger Regulation needs to be read together with Recital 22 of the Merger Regulation which provides that the calculation of turnover of an undertaking concerned must "take account of undertakings making up an economic unit with an independent power of decision, irrespective of the way in which their capital is held or of the rules of administrative supervision applicable to them". Therefore, for the purposes of calculating the turnover of SOEs, account needs to be taken of those undertakings which belong to the same economic unit.

(7) In this case, the Commission must therefore determine the scope of the single economic unit with an independent power of decision within the controlling State. (7) This analysis is conducted to calculate the turnover that is relevant to determine whether the concentration has an EU dimension. Where several SOEs are under the same independent centre of commercial decision-making, then the turnover of those businesses should be considered part of the group of the undertaking concerned for the purposes of Article 5(4). (8)

(8) In previous cases, (9) the Commission has analysed several factors to determine the scope of the single economic unit to be taken into account. The Commission analysed, for instance, the presence of specific holding arrangements, governance provisions and other safeguards ensuring that the entity retains its independent power of decision regarding its strategy, business plan and budget, the legal ability of the State to take decisions for the SOE, the State's right to give instructions to the SOE, its powers of supervision, the possibility of approving amendments of the SOE's by-laws, its ability to appoint board members so as to have the majority of voting rights, etc. Applying these criteria to the present case the Commission will herein determine whether (i) Prisko is taking its strategic decisions independently from the Czech State, and (ii) if this is not the case, which other SOEs are part of the same centre of commercial decision-making, and whose turnover needs to be taken into account for the purposes of Article 5(4) of the Merger Regulation. (10)

2.1.1. Relationship between the Czech State and Prisko

(9) Prisko is owned by the Czech State (100% of shares) and acts as the investment vehicle of the MoF who appoints the members of Prisko's Board of Directors (three members) and of its Supervisory Board (one member, representing the Czech State). Prisko's Board of Directors ultimately requires approval of its business plan and budget by the General Meeting of Shareholders, where only the MoF sits. (11) Therefore, the MoF ultimately controls Prisko. (12)

(10) As Prisko is controlled by the MoF, the question is whether other Czech SOEs can be considered as not having an independent power of decision from the Czech State in the sense of Recital 22 of the Merger Regulation, and in particular from the MoF, and should therefore be considered part of the same single economic unit as Prisko.

2.1.2. Relationship between the Czech State and other SOEs

(11) In addition to Prisko, the MoF also owns nearly 70% of the shares in ČEZ a.s. ("ČEZ"), (13) a company primarily active in the generation of electricity and which purchases hard coal for its power generation. The Commission has analysed whether ČEZ makes up an economic unit with an independent power of decision in the sense of Recital 22 of the Merger Regulation.

(12) Shareholders of ČEZ sit at the General Meeting of Shareholders which appoints the members of the Supervisory Board. Because the MoF owns a majority (70%) of ČEZ's shares, it is entitled to appoint 8 out of the 12 members of ČEZ's Supervisory Board, the remaining 4 members being appointed by the workers' unions. (14)

(13) In turn, ČEZ's Supervisory Board appoints the 7 directors of its Board of Directors. (15) ČEZ's Board of Directors is responsible for setting up the business plan, the budget and for taking the strategic decisions. (16) The other shareholders of ČEZ have no representation at the Supervisory Board or at the Board of Directors.

(14) Therefore, through its majority shares' voting rights in the General Meeting, the MoF is entitled to appoint two thirds of members of the Supervisory Board of ČEZ, which in turn appoints and removes the members of its Board of Directors, giving the MoF the ability to exercise decisive influence over ČEZ's strategic decisions.

(15) ČEZ disagrees and has submitted a number of arguments that in its view show that it should be considered as constituting a separate economic unit with an independent power of decision from the MoF and the Czech State.

(16) First, as regards the applicable test to determine the single economic unit, ČEZ refers to the Commission's decision in M.7850 - EDF/CGN/NNB (China General Nuclear Power Corporation). The Commission notes that it has assessed whether a specific SOE is an economic unit with an independent power of decision not only in the M.7850 - EDF/CGN/NNB decision but also in several other decisions. (17) In each case, the Commission assessed whether, based on the specific situation of the SOE in question, it could be considered as an economic unit with an independent power of decision in the sense of Recital 22 of the Merger Regulation. Although ČEZ argues it constitutes a single economic unit with an independent power of decision, ČEZ does not dispute that the MoF, through its majority shareholding (70%) and exercising its voting rights has the ability to appoint two thirds of the members of the Supervisory Board, which in turn appoint, and remove, the members of the Board of Directors. In this respect, the Commission also notes that certain high ranking officials of the MoF sit in the Supervisory Board of ČEZ. (18)

(17) Furthermore, the Commission has considered whether or not there are safeguards to prevent the sharing of commercially sensitive information among SOEs. (19) In this case, there appears to be no concrete safeguards to prevent sharing commercially sensitive information between Czech SOEs. (20) By being present through representatives or by appointing certain Board members, the MoF has access to all relevant information discussed within both Prisko and ČEZ. (21)

(18) Second, ČEZ explained that [developments on CEZ's corporate structure]". (22)

(19) This argument cannot be accepted. [Commission's analysis of confidential elements on the corporate structure of CEZ]. Therefore, […] does not appear to effectively prevent the MoF from exercising control over CEZ's strategic decisions".

(20) Third, ČEZ argued that its corporate governance rules provide guarantees of independence to its boards. It points out that Article 14(4) of ČEZ's Articles of Association provide that "[n]o one is authorized to instruct the board of directors in the matters related to the company's business management". However, besides the fact that the MoF indirectly controls the composition of the Board of Directors that same provision also states that "directors may request the general meeting to grant instructions regarding business management", which would amount to asking the MoF for instructions, given its 70% shareholding.

(21) Other provisions in the Articles of Association make it even clearer that the boards of ČEZ are not independent from the General Meeting, where the MoF has a majority. Article 14(3) of the Articles of Association provides that "[t]he board of directors must observe the principles and instructions approved by the general meeting, provided that they are in accordance with legal regulations and these Articles of Association." Article 7(1) provides that the General Meeting is the company's supreme body and Article 12(5) provides that the General Meeting decides by a simple majority of votes of attending shareholders, unless provided otherwise by law or the company's Articles of Association. Since the MoF owns nearly 70% of ČEZ's shares it will obtain a simple majority at the General Meeting. Some matters, such as the amendment of the Articles of Association, require a two-thirds majority, but given MoF's shareholding of 70%, the MoF will also easily obtain a two-thirds majority. Only a very limited number of matters (such as a capital increase through in-kind contributions) require a three-fourths majority.

(22) The Articles of Association therefore do not provide sufficient guarantees to establish the existence of an independent power of decision of ČEZ.

(23) This is all the more true when considering that the MoF has the possibility of amending the Articles of Association because of its large majority voting rights at the General Meeting. (23) Consequently, ČEZ's corporate governance structure does not appear sufficient to counterbalance the fact that the MoF has the legal ability to exercise control over it. (24)

(24) Fourth, ČEZ explained that the Czech Business Corporation Act which applies to listed companies such as ČEZ ensures ČEZ's independence from the MoF. (25) However, protections provided by national corporate law are unlikely to counterbalance the MoF's ultimate ability to appoint the Board of Directors. By way of example, ČEZ argued that members of the Board of Directors have to "act with the due care of a prudent manager". However, that obligation applies to all listed companies and to any member of the Board regardless of who appoints them and is not at odds with the fact that in ČEZ's case they are appointed by the MoF. Moreover, the duty of care any member of the Board of Directors has does not prevent a finding that ultimately the company does not act independently from the State.

(25) Fifth, ČEZ argued that in a recent ruling the Czech Constitutional Court (26) confirmed the independence of ČEZ from the State. However, the criteria used to conclude on independence in this judgment do not match the criteria used by the Commission to assess whether an SOE has an independent power of decision in the sense of Recital 22 of the Merger Regulation.

(26) Indeed, the Czech Constitutional Court's ruling concerned the application on ČEZ of the obligation of disclosure that falls on public institutions and decided that the majority stake held by the State could not in itself be decisive to consider ČEZ as a public body. The Court evaluated the manner of establishment or dissolution of ČEZ, whether the State is a founder of ČEZ, entities creating ČEZ's bodies and the oversight of the State over ČEZ activities. The Czech Constitutional Court concluded that ČEZ is not a public institution according to Czech rules, which is not equivalent to the notion of an undertaking making up an economic unit with an independent power of decision as analysed by the Commission in its investigation. The Czech Constitutional Court's judgment therefore does not prevent the Commission from finding that ČEZ does not constitute a single economic unit with an independent power of decision-making for the purposes of the Merger Regulation.

(27) In view of the above, with regard to ČEZ's relationship to the MoF, the Commission concludes that the Czech State would have the ability to exercise decisive influence over ČEZ. ČEZ's turnover should therefore be considered together with the turnover of Prisko.

2.2. Thresholds

(28) On this basis, the undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (27) [Prisko: (28) EUR >7 920 million; OKD: EUR 544 million]. Each of them has an EU-wide turnover in excess of EUR 250 million [Prisko: EUR >7 920 million; OKD: EUR 534 million], but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. (29) The notified operation therefore has an EU dimension.

3. MARKET DEFINITION

(29) The activities of the Parties do not overlap horizontally. (30) However, the Transaction gives rise to vertically affected markets between the activities of OKD and ČEZ. OKD is active in the upstream market for the production and sale of hard coal and ČEZ in the downstream market for generation and wholesale supply of electricity. (31)

3.1. Production and sale of hard coal

3.1.1. Product market definition

(30) OKD's activities are concentrated in the production and sale of hard coal (also referred to as black coal). Hard coal is a solid fuel used (i) to produce iron and steel (metallurgical coal) and (ii) for the generation of electricity and heat (thermal coal). Hard coal encompasses all types of coal irrespective of geological properties (anthracite, bituminous and sub-bituminous) except lignite (also known as "brown coal") which constitutes a distinct market.

3.1.1.1. Thermal coal and coking coal

Segmentation by end use

(31) First, in previous decisions, the Commission has found that for most of the users of hard coal it is not possible to replace coal by other fuels in the short term. Therefore hard coal constitutes a distinct market from other fuels. More precisely, lignite and hard coal have been found in the past to belong to different markets in view of their different properties. (32) The increased moisture content of lignite prevents it from been transported over long distances, while hard coal can travel more easily. In addition, calorific values of lignite and hard coal are very different.

(32) Second, within hard coal the Commission has consistently defined separate markets for (i) thermal coal and (ii) metallurgical coal (also referred to as coking coal) in view of the characteristics required depending on the end use: thermal coal for producing electricity and heat and metallurgical coal for the steel industry. (33)

(33) The Notifying Party agrees with the fact that thermal coal and coking coal belong to different product markets and are not substitutable. More precisely, due to their different calorific values and other characteristics they are each suitable for different purposes and the customers' equipment is adapted to either one or the other and cannot be used interchangeably.

(34) Respondents to the Commission's market investigation agree with the fact that hard coal and lignite belong to separate markets. (34)

(35) Similarly, market participants consider that thermal coal is used for power generation while metallurgical coal, understood mainly as coking coal, is used to make steel for its caking properties. They have explained that coking coal has substantially higher monetary value because of those properties that render it suitable for the metallurgical industry. (35) Both types of coal are not substitutable.

(36) As a result, thermal coal and coking coal constitute distinct product markets.

Segmentation by geological properties

(37) As previously explained (see Recital (30)), hard coal can be differentiated according to its geological properties. It can be anthracite, bituminous coal or sub- bituminous coal. While coking coal is bituminous, thermal coal can be any of the three types. A segmentation of thermal coal according to its geological properties has been considered in the past by the Commission but ultimately the question was left open. (36)

(38) The Notifying Party has explained that coking coal is mostly bituminous, while thermal coal, although generally bituminous as well, can also be of different geological content, such as anthracite or sub-bituminous.

(39) The market investigation has shown that there is limited substitutability between the different types of coal because combustion plants are adapted only to one type and its calorific values. Especially combustion plants designed to burn anthracite will not burn bituminous or sub-bituminous coal. There is however more flexibility between bituminous and sub-bituminous coals. Competitors have explained that customers do not always focus on whether the thermal coal is bituminous or sub-bituminous and can use it interchangeably to a certain extent. Customers have confirmed that bituminous and sub-bituminous coals are at least partially substitutable, while it is not always the case for anthracite coal. (37)

(40) Nevertheless, the large majority of thermal coal in the Central Eastern Europe ("CEE") region in general is bituminous coal (38). Only bituminous coal is produced in Poland and the Czech Republic. (39) There is some production of anthracite coal in Germany, but the only mine producing thermal coal in Germany will close in 2018. Sub-bituminous mostly exists in the United States. OKD itself only sells bituminous coal.

(41) As a result, in this case the question of whether thermal coal should be subdivided according to geological properties can be left open.

3.1.1.2. Pulverised Coal Injection

(42) Coal may be pulverised and injected directly into the base of the blast furnace as a partial replacement for coke in the steelmaking process. This is known as Pulverised Coal Injection ("PCI"). PCI coals provide an additional and cheaper source of carbon and energy to aid iron ore reduction. They are used in the coke- making process, but have no coking properties.

(43) The Commission has considered in past decisions whether PCI should be considered together with coking coal or whether it should be regarded as a distinct market within metallurgical coals. The definition was ultimately left open. (40)

(44) The Notifying Party believes PCI should be included in the same market as thermal coal. According to it, technically PCI cannot be deemed coking coal because it does not have caking properties but is more similar in nature to thermal coal. However, PCI is solely used in the steel industry in order to provide additional heat to speed up the process of the production of iron. The Notifying Party argues that, although the more PCI is used the less coking coal is needed, they are not substitutable. (41)

(45) Despite the fact that PCI is used to increase heat, the market investigation supports that it is not substitutable with thermal coal. From the demand side, only customers active in steelmaking (or coal trading) purchase PCI, while none of the thermal coal customers do. Indeed, even if the purpose of PCI is to increase heat, it is only used in the steelmaking process and thus cannot be considered as thermal coal, as it is not used for power generation. There are also important differences in prices stemming from the fact that PCI has a lower level of impurities and therefore is more costly than thermal coal. As a result, PCI is not substitutable to thermal coal. Conversely, the market investigation suggests that there could be a limited scope for substitutability with coking coal. (42)

(46) Nevertheless, ČEZ only procures thermal coal from OKD and not PCI, therefore the question as to whether PCI is a separate market within metallurgical coal or it forms part of the market of coking coal can be left open.

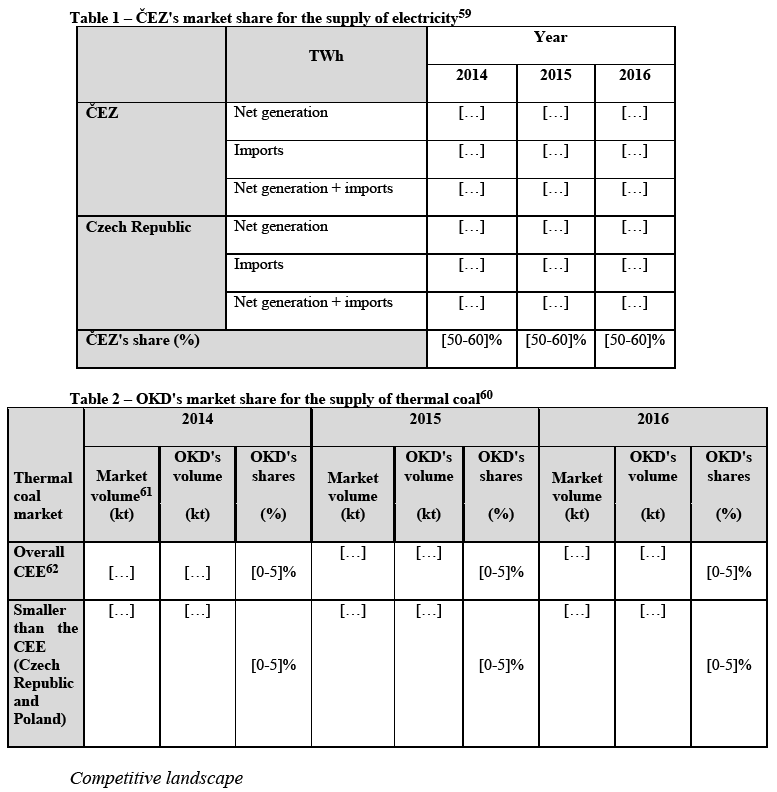

(47) In view of the above, the market for coal is segmented into metallurgical coal and thermal coal. Given that thermal coal is the only type of hard coal procured by ČEZ, the exact definition of metallurgical coal can be left open since it does not constitute a relevant market in this case.

3.1.2. Geographic market definition

(48) The Commission has in the past defined the seaborne market for coal as global, given the low costs of transportation by sea. (43) However, the Transaction concerns production of coal in the Czech Republic which is not part of the seaborne market, thus the geographic scope for landborne coal has to be analysed.

(49) The Notifying Party considers that the market for production and sale of thermal coal, as well as coking coal, is not broader than CEE. This would be mainly explained by the characteristics of the region which only allow transportation through rail services. Rail transportation implies, first, higher costs in longer distances (as costs are directly proportional to the distance over which the product is transported, unlike maritime transport), and secondly, higher total costs when compared with Europe's coastal regions.

(50) This is supported by OKD's own activities. OKD sells a majority of its coal in the Czech Republic, Poland, Slovakia, Austria and Germany. To a lesser extent, it also has sales in the Balkan Peninsula, but does not sell beyond those countries. Similarly, OKD's competitors also sell thermal coal in CEE countries or nearby, with most of production staying in Poland and in the Czech Republic. (44)

(51) Traditionally, customers of thermal coal are located in the vicinity of the mines so costs of transport, which usually consists on rail, can be minimised. The market investigation has showed that most customers of thermal coal located in the Czech Republic or neighbouring countries indeed source most of their needs of thermal coal in the Czech Republic and Poland. (45) Customers of OKD have also stated that they would source from Poland in case they would need to find alternative suppliers.

(52) This is consistent with the fact that Czech Republic and Poland are also the main producers of hard coal, and thermal coal, in the EU. Together, they account for 80% of the EEA production of thermal coal and 100% in the CEE. (46) Similarly, both countries export some of their coal but have very limited imports of hard coal, due to both their own indigenous production and the fact that they are locked in the European continent. (47) In 2016 Czech Republic imported 1556kT of thermal coal from Poland, which accounted for 94% of imports, with the remaining 6% coming from Russia. (48)

(53) In view of the above, the geographic scope for the landborne market of thermal coal is not global. This market is likely to be rather CEE wide in scope (with possibly Russia included), (49) however, the exact market definition can be left open since the Transaction raises no competitive concerns even on the narrowest possible definition which covers at least Poland and the Czech Republic.

(54) To conclude, for the purposes of this case the relevant upstream affected market of thermal coal will be assessed at the narrowest possible level, Czech Republic and Poland.

3.2. Generation and wholesale supply of electricity

3.2.1. Product market definition

(55) ČEZ is active in the generation and wholesale supply of electricity. This market comprises electricity generated in power stations, traded on the wholesale market as well as electricity physically imported via interconnectors. (50)

(56) In previous decisions concerning the electricity sector, the Commission has considered that the generation and wholesale supply of electricity is a different product market from the transmission, distribution and retail supply, as these activities correspond to distinct market conditions and structures. (51)

(57) The Notifying Party is in line with the Commission's past practice.

3.2.2. Geographic market definition

(58) In previous decisions, the Commission has considered the electricity wholesale market to be national in scope. (52) Moreover, the Commission, in line with the decision of the Czech NCA (Office for the Protection of Competition), (53) has defined the geographic scope of this market as national and not wider than the Czech Republic. (54)

(59) The Notifying Party agrees with the Commission's practice. However, ČEZ has submitted that the market could be wider in scope, including both the Czech Republic and Slovakia.

(60) The existence of market coupling with Slovakia since 2009 could imply the existence of a wider geographic market, however, there are indicators that both markets remain distinct.

(61) First, prices still differ between both countries. (55) Traditionally, Czech wholesale electricity prices are lower than Slovak prices, which reduces the scope for imports.

(62) Second, in terms of flows, while there is interconnection capacity, the Czech transmission system operator ("TSO") has reported large amounts of unplanned flow on the grid which threatens grid stability and limits commercial trade. (56)

(63) Third, on the supply-side, the activities of electricity wholesalers are different in both countries. Slovakia's main electricity producer is Slovenské elektrárne with 69% market shares on its national market, while it has only minor activities in the Czech Republic. (57) Similarly, in the Czech Republic, ČEZ is the largely dominant player.v(58)

(64) Finally, for the purpose of this case, the assessment will be carried out on the basis of the narrowest possible market, namely the Czech Republic. If Slovakia were to be considered to be part of the same market, ČEZ' market share would only be diluted due to the presence of other strong competitors.

(65) In any case, despite indications that markets are national, the exact geographic market definition can be left open given no competition concerns arise even on the narrowest market definition, namely the Czech Republic.

4. COMPETITIVE ASSESSMENT

4.1. Market dynamics

Market shares

(66) While ČEZ has a strong presence in the downstream market ([50-60]%), OKD has a limited presence on the upstream market ([0-5]% in both the CEE and considering only Poland and the Czech Republic).

(67) The market investigation has demonstrated that Polish coal producers exert strong competitive pressure on OKD. In 2015, Poland's thermal coal production was 10 times larger than OKD's production. (63) In addition, the Polish mines are the main producers of thermal coal in Europe.

(68) As it was submitted by the Notifying Party, (64) the two main hard coal suppliers are Jastrzębska Spółka Węglowa ("JSW"), the largest producer of coking coal in Europe and Polska Grupa Górnicza ("PGG"), one of the largest producers of thermal coal in the CEE, (65) both located in Poland. The majority of customers that responded to the market investigation consider them as credible alternative suppliers in the Czech Republic. (66) The majority of competitors that responded to the market investigation listed JSW and PGG as their main competitors. (67)

(69) In addition to strong competitors in Poland, the market for the production and sale of coal is characterised by the existence of trading companies that provide customers with additional sources of supply. Weglokoks for example, exported from Poland around 3 579 kt of thermal coal in 2016. (68) Weglokoks and other trading companies such as EP Coal Trading supply thermal coal in the Czech Republic. (69) Moreover, some customers have explained that alternatively, they could also eventually source coal from the major coal hub ARA (Amsterdam-Rotterdam-Antwerp). (70)

(70) It should also be noted that it is publicly known that OKD will gradually close its mines between 2017 and 2023. (71) For this reason, customers are already starting to plan for other sources.

(71) In short, there are strong alternatives to OKD that would impede any foreclosure attempt by the merged entity. The Commission has further analysed whether the merged entity could potentially engage in foreclosure strategies both on the upstream and downstream market.

4.2. No input foreclosure

(72) The Commission has analysed whether post-Transaction, the merged entity could restrict its supply to downstream rivals of ČEZ.

(73) The Commission's Non Horizontal Guidelines (72) explain that "for input foreclosure to be a concern, the vertically integrated firm resulting from the merger must have a significant degree of market power in the upstream market. It is only in these circumstances that the merged entity can be expected to have a significant influence on the conditions of competition in the upstream market and thus, possibly, on prices and supply conditions in the downstream market." (emphasis added)

(74) As explained in paragraph (66), even on the narrowest possible geographic market definition (Czech Republic and Poland), OKD's shares in thermal coal are too small for the merged entity to exercise any type of market power that would have an effect on downstream producers of electricity.

(75) Moreover, in case the merged entity would still attempt to restrict the supply of coal to other electricity suppliers, as demonstrated in paragraph (67) to (71), there exist readily available competitors to OKD, especially in view of the important capacity from the Polish suppliers and the large quantities of imports coming into the Czech Republic from Poland.

(76) Therefore, downstream players would be able to defeat any attempt by the merged entity to increase prices or restrict supply of coal by sourcing from OKD's competitors. The merged entity will not have the ability to engage in input foreclosure.

(77) In addition, there is no incentive for the merged entity to restrict access to coal to downstream electricity suppliers as the downstream market is defined at national level. Any attempt to restrict access to coal in other countries, e.g. in Poland, would not result in profits in the downstream market, i.e. the Czech Republic.

(78) Finally, even attempts to restrict access to coal to other electricity suppliers than ČEZ in the Czech Republic would not result in profits for the merged entity. Indeed, as electricity is a homogeneous product and only a small part of it is generated using coal, electricity suppliers using other sources of power generation would remain unaffected by any foreclosure attempts.

(79) In view of the above, the Commission has concluded that the merged entity will not have the ability or the incentive to engage in input foreclosure post- Transaction.

4.3. No customer foreclosure

(80) The Commission has analysed whether post-transaction, the new entity would have the ability or incentive to foreclose OKD's competitors.

(81) While ČEZ enjoys an important position on the downstream market for generation and supply of electricity in the Czech Republic (see paragraph 66), it appears that ČEZ already sources most of its coal from OKD so that even if it would increase its sourcing from OKD it would not result in a significant loss for other suppliers.

(82) ČEZ operates 12 power plants, 10 of which use lignite. The remaining two plants, Dětmarovice and Vítkovice, are fuelled with thermal coal and are currently already largely supplied by OKD. As a result, there is no scope for ČEZ and OKD to engage in customer foreclosure given there is currently a small proportion of ČEZ needs that are sourced from other suppliers. Furthermore, the volumes ČEZ purchases from OKD are actually expected to decrease by half in 2018, rather than increase. (73)

(83) Moreover, as explained in paragraph (70) above, it is publicly known that OKD plans to gradually close its mines between 2017 and 2023. The merged entity's supply capacity will therefore gradually decrease, thereby preventing any attempt to foreclose OKD's competitors. (74)

(84) Both the Dětmarovice and the Vítkovice plants are supplied from OKD's mines of Darkov, Lazy and CSM. Darkov and Lazy are expected to close in 2018. CSM will be the last mine of OKD to close, in 2023. (75) As a result, ČEZ will have no incentive or possibility to source all of its coal from OKD, rather it has the incentive to secure supplies from other mines.

(85) In any case, if ČEZ were to single source from OKD, the remaining suppliers would have no issue in supplying other customers in the Czech Republic or in Poland.

(86) In view of the above, the Commission has concluded that the merged entity will not have the ability or the incentive to engage in customer foreclosure post- Transaction.

5. CONCLUSION

(87) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 OJ L 24, 29.1.2004, p. 1 (the "Merger Regulation").

4 See Form CO paragraphs 7-8.

5 More specifically in the Moravian-Silesian Region (Karviná, Darkov, ČSM and Paskov mines).

6 Prisko achieves EUR 168 715 both worldwide and in the EEA.

7 What constitutes the single economic unit is further developed in Recitals 192-194 of the Consolidated Jurisdictional Notice ("CJN"). For completeness, Recitals 52, 53 and 153 of the CJN also relate to turnover calculation of SOEs.

8 CJN, Recital 194.

9 See, e.g., cases M.7850 – EDF/CGN/NNB Group of companies, paragraph 30; M.5508 – Soffin/Hypo Real Estate; M.5861 – Republic of Austria/Hypo Group Alpe Adria; M.6815 – SFPI/Dexia.

10 This test has been applied in previous cases, such as M.7850 – EDF/CGN/NNB Group of companies; M.5508 – Soffin/Hypo Real Estate; M.5861 – Republic of Austria/Hypo Group Alpe Adria; M.6815 – SFPI/Dexia.

11 See also Prisko's reply to RFI 02 dated 03.07.2017 where it explains that the Board of directors of "Prisko is obliged to submit the business plan, the financial plan and business strategy to the Czech State for an approval".

12 Reply to question 2(a) of RFI 01 in case C.1593 – Prisko/ OKD, submitted on 3 July 2017.

13 More precisely, the MoF holds 69.78% of shares in ČEZ, private investors hold 29.52% and ČEZ 0.7%. For completeness, the 29.52% of shares owned by private investors and the additional 0.7% of shares held by ČEZ itself have no personal presence in the Board of Directors and Supervisory Board.

14 See Article 8(1)(d) of ČEZ's Articles of Association.

15 See Article 15(2) of ČEZ's Articles of Association.

16 See Article 14(10) of ČEZ's Articles of Association.

17 See e.g. M.5508 – Soffin/Hypo Real Estate; M.5861 – Republic of Austria/Hypo Group Alpe Adria; M.6815 – SFPI/Dexia.

18 One example relates to Ondřej Landa, Vice-Chairman of the Supervisory Board who is currently also one of the Deputy Ministers of the MoF (see: http://www.mfcr.cz/en/about-ministry/organisation- chart/section-02-legal/ondrej-landa - Accessed on 23.11.2017).

19 See e.g. M.6082 - China National Bluestar/Elkem, paragraph 11: "[i]n order to assess whether the State has the power to coordinate the commercial conduct of companies, the Commission has previously taken into account factors such as the degree of interlocking directorships between entities owned by the same entity or the existence of adequate safeguards ensuring that commercially sensitive information is not shared between such undertakings".

20 [ČEZ analysis of corporate provisions].

21 It is also noted that [Name of representative] is currently the sole representative of the MoF sitting at the Supervisory Board of Prisko and at the same time the sole representative of the MoF at the General Meeting of ČEZ (Reply to question 3 of RFI 6 to the Parties).

22 Reply to question 4 of RFI to ČEZ dated 3 October 2017 in C.1593 – Prisko/OKD.

23 See Article 12(6) of ČEZ's Articles of Association.

24 See paragraph 22 of CJN.

25 See paragraph 22 of CJN.

26 Ruling IV. US 1146/16 and Ruling Ref. No. I. US 260/06.

27 Turnover calculated in accordance with Article 5 of the Merger Regulation and the CJN.

28 The above turnover aggregates Prisko and ČEZ turnovers, which is enough to meet the thresholds. ČEZ by itself achieves EUR 7 920 million turnover worldwide and in the EEA.

29 OKD achieves approximately 50% of its turnover in the Czech Republic while the rest is achieved in sales in nearby countries as explained hereunder (Recital (50)).

30 For completeness, ČEZ also extracts mining, but no horizontal overlap exists as ČEZ only produces brown coal or lignite, while OKD produces only hard coal.

31 For completeness, OKD also provides waste management services for fly ash (a by-product of electricity generation) produced by its customers of thermal coal. OKD provides this service only in the Czech Republic and for its customers. The dynamics of the waste management market will closely follow the ones of the production and sale of coal. The only revenue from OKD for the treatment of fly ash that is not achieved with one of its coal customers is with [Name of customer] and is marginal.

32 See Cases: M.6541 - Glencore/Xstrata, and IV/M.402 - PowerGen/NRG Energy/Morrison Knudsen/Mibrag, paragraph 10.

33 See, for example: Case ECSC.1316 - RAG/Burton, ECSC.1331 - Anglo American/Shell; M.2413 BHP/Billiton; M.6541 - Glencore/Xstrata.

34 Replies to question 2(a) of RFI to trade associations, competitors and customers.

35 Reply to question 2(b) of RFI to trade associations, competitors and customers.

36 See Case M.6541 - Glencore/Xstrata.

37 Reply to question 2(c) of RFI to trade associations, customers and competitors.

38 The CEE in this analysis includes Czech Republic, Slovakia, Poland, and Austria.

39 Reply to question 2 of RFI 02 to Euracoal.

40 M.6541 - Glencore/Xstrata.

41 Reply to question 1 of RFI 03 to Parties.

42 Replies to questions 1(a) and 2(c) of RFI to trade associations, customers and competitors.

43 M.6541 - Glencore/Xstrata.

44 Replies to questions 3(a) (b) and (c) of RFI to trade associations, customers and competitors.

45 Replies to questions 3(a) and (b) of RFI to trade associations, customers and competitors.

46 Reply to question 1 of RFI 02 to Euracoal, based on OECD International Energy Agency (IEA) 2016 statistics.

47 Reply to questions 3(c) of RFI to Euracoal.

48 Reply to question 1 of RFI 02 to Euracoal.

49 Some respondents to the market investigation indicated that it would also be feasible to procure coal from beyond the CEE, for instance from the Antwerp/Rotterdam/Amsterdam hub (Replies to questions 3(b) and 3(c)ii of RFI to customers).

50 Case M.6984 - EPH/Stredoslovenska Energetika.

51 Case M.5978 – GDF Suez/International Power, paragraph 12; M.5224 EDF/British Energy, paragraph 10ff; M.5467 RWE/Essent, paragraph 23.

52 Case M.5978 – GDF Suez/International Power, paragraphs 24, 42 or 70; M.5549 – EDF/Segebel, paragraph 38; M.8270 – EDF/CDC/RTE.

53 S4.92/2011/KS - ČEZ/Energotrans (2012).

54 Case AT.39727 – ČEZ (2013).

55 See fluctuations of prices of futures from Power Exchange Central Europe at http://www.pxe.cz/?language=english, last visited on 23/11/2017 at 11h07.

56 "National Report of the Energy Regulatory Office on the Electricity and Gas Industries in the Czech Republic in 2016", ERO, 2016.

57 See https://www.seas.sk/slovak-energy-sector, last visited on 23/11/2017.

58 Source: Form CO.

59 Source: Reply to question 5 of RFI 01 to ČEZ.

60 Source: Reply to question 1.c of RFI 06 to Parties, based in Eurostat and internal data about OKD's sales.

61 The commission made its own estimations on the size of the market based in Eurostat data and its results did not differ significantly from those presented by the Parties.

62 Overall CEE in this analysis includes Czech Republic, Slovakia, Poland and Austria. If Germany would be included OKD's shares would dilute, representing [0-5]%, [0-5]% and [0-5]% in each of the relevant years respectively.

63 Polish thermal coal production in 2015 reached 59 191 kt. Reply to question 1 of RFI 02 to Euracoal, based on OECD International Energy Agency (IEA) 2016 statistics.

64 Reply to question 14 of RFI 02 to Parties.

65 "Coal Industry across Europe", 6th Edition, Euracoal, 2017. Pages 37-38. Available in: https://euracoal.eu/library/publications/ last visited: 24 November 2017.

66 Replies to question 4(c) of RFI to customers.

67 Replies to questions 4(b) of RFI to competitors.

68 Reply to question 3(b)(i) of RFI to Weglokoks.

69 Replies to question 3(b)(i) and (iii) of RFI to Weglokoks and 2(b) to EP Coal Trading.

70 The major suppliers of ARA appear to be supplied by coal suppliers situated in South Africa, Russia, the US, etc. See reply to question 2 of RFI 01 to ČEZ.

71 See for instance: OKD plans to close all mines by 2023, Prague Daily Monitor, http://praguemonitor.com/2017/07/14/okd-plans-close-all-mines-2023

72 See paragraph 35 of the Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (2008/C 265/07).

73 Reply to question 2 of RFI 06 to Parties.

74 Reply to question 9 of RFI 02 to Parties. OKD owns the mines of Paskov, Darkov, Lazy, CSA and CSM. Paskov was already closed in March 2017.

75 Reply to question 9 of RFI 02 to Parties. CSA mine will close in 2021.