Commission, November 30, 2018, No M.9108

EUROPEAN COMMISSION

Judgment

PEPSICO / SODASTREAM INTERNATIONAL

Subject: Case M.9108 - PepsiCo/SodaStream International Commission decision pursuant to Article 6(1)(b) of Council

Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 24.10.2018, the European Commission received notification of a proposed concentration ('the Transaction') pursuant to Article 4 of the Merger Regulation by which PepsiCo Inc. ('PepsiCo', US) acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of SodaStream International Ltd. ('SodaStream', Israel)3. PepsiCo is also referred to as 'Notifying Party' and PespiCo and SodaStream are collectively referred to as 'Parties'.

1. THE PARTIES AND THE OPERATION

(2) PepsiCo is a global food and beverage company. Through its operations, as well as through authorized bottlers, contract manufacturers and other third parties, it produces, markets, distributes and sells a wide variety of beverages, foods and snacks under a wide portfolio of brands (including Pepsi-Cola, 7Up, Mountain Dew, Doritos, Frito-Lay, Gatorade, Lays, Mirinda, Quaker and Tropicana).

(3) SodaStream manufactures and commercializes home carbonation systems as well as concentrates, syrups and flavours that enable consumers to transform tap water into sparkling water and carbonated soft drinks.

(4) SodaStream is a publicly traded company, at present, not controlled by any of its shareholders. Pursuant to an Agreement and Plan of Merger dated 20 August 2018, PepsiCo will indirectly, through a wholly owned subsidiary, acquire all outstanding shares of SodaStream.

(5) PepsiCo acquiring sole control over SodaStream, the proposed Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

2. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4 (in 2017, PepsiCo: […]; SodaStream: […]). Each of them has an EU-wide turnover in excess of EUR 250 million (in 2017, PepsiCo: […] ; SodaStream: […]), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

3. MARKET DEFINITION

3.1. Introduction

(7) The present case primarily concerns Sodastream's home carbonation systems for home-made sparkling water or home-made carbonated soft drinks. These are systems that are composed of a device that carbonates water by adding compressed CO2 from a replaceable pressurized cylinder to water in a carbonated bottle. Concentrates, syrups and flavours, which are also sold by SodaStream, can be added afterwards to prepare soft drinks. The CO2-cylinders and the related refilling services are the highest value components of the systems.

(8) PepsiCo is active in neighbouring markets such as for beverages, in particular bottled and canned sparkling water and carbonated soft drinks as well as dilutables concentrates, syrups and flavours (but not for final consumers) and also consumer solutions consisting of bottles and pods filled in with dilutables that allow to obtain flavoured water.

3.2. Product Market Definition

3.2.1. Home Carbonation Systems

(9) The Commission did not assess in previous decisions home carbonation systems and their components.

(10) The Notifying Party submits that the relevant product market includes home carbonation systems as a whole, while the single components, namely CO2- cylinders, carbonator bottles as well as the CO2 refilling services should not be considered as separated markets as they only belong to an after-market to that of the sale of home carbonation systems.

(11) The Commission considers that for the purpose of the present decision the exact product market definition can be left open as no serious doubts arise in the markets for the single component of home carbonation systems (sparkling water makers, CO2-cylinders, carbonator bottles as well as the CO2 refilling services) which appear to be the narrowest-possible relevant market among the alternative market definitions discussed above.

3.2.2. Beverages, concentrates, syrups and consumer solution for flavoured water

(12) The Notifying party submits that the relevant product markets as regards beverages, concentrates, syrups and consumer solutions for flavoured water can be left open as the Transaction does not raise serious doubts under any possible market definition for these products.

(13) In previous decisions5, the Commission has identified separate product markets for the production and supply of carbonated and non-carbonated soft drinks. Within carbonated soft drinks, the Commission has considered distinct product markets for cola flavoured and non-cola flavoured carbonated soft drinks6 and, within the market for non-carbonated soft drinks, packaged water, fruit juices, ready-to-drink teas and energy and sports drinks have been considered separately.

(14) In a previous decision7, the Commission did consider concentrates and syrups sold to bottling and canning operators, but it did never assess whether concentrates, syrups and flavours sold directly to final consumers constitute a separate market from other soft drinks. Finally, consumer solutions for flavoured water were not considered in any previous Commission's decision.

(15) During the market investigation, a majority of customers indicated that concentrates syrups and flavours for home carbonation systems compete with carbonated soft drinks.8 However, some customers also specify that these products are only partial substitutes.9 During the market investigation, several customers also indicated that concentrates, syrups and flavours to be used in connection with home carbonation systems present certain specific characteristics, but the elements reviewed do not allow the Commission to reach a conclusion as to whether concentrates, syrups and flavours to be used in connection with home carbonation systems, or consumer solutions for flavoured water form separate markets.10

(16) However, for the purposes of this decision, the Commission considers that the exact product market definitions might ultimately be left open as no serious doubts arise in the market for cola flavoured and non-cola flavoured soft drinks nor in a market for concentrates, syrups and flavours to be used in connection with home carbonation systems which appear to be the narrowest-possible relevant markets among the alternative market definitions discussed above.

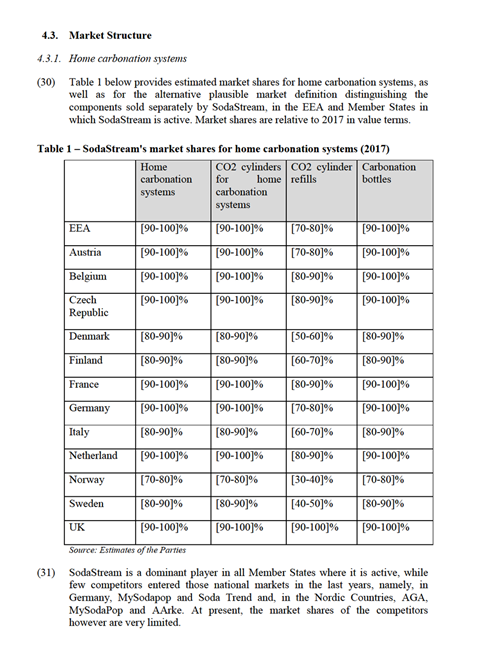

3.3. Geographic Market Definition

(17) As regards the geographic scope of the relevant markets, the Commission has in the past found that the relevant geographic markets for consumers' goods, including home appliances, beverages or syrups and concentrates, are national in scope due to differences in consumption patterns, logistics and distribution networks as well as marketing strategies.11

(18) In its submission, the Notifying Party does not take position on the geographic scope of the relevant product markets as the Transaction would not raise serious doubts under any relevant geographic market definition.

(19) The responses to the market investigation have not provided any indication that it would be warranted for the Commission to depart from its previous practice for defining the geographic scope of the relevant product markets in the present case.

(20) For the purposes of this decision, the Commission considers, in line with its practice, that all the relevant product markets are national.

4. COMPETITIVE ASSESSMENT

4.1. Activities of the Parties

(21) PepsiCo produces, markets, distributes and sells bottled or packaged (e.g., in cans) carbonated and non-carbonated soft drinks and water and it is a brand owner and licensor of various trademarks used to market and sell non-alcoholic beverages (Pepsi, 7Up, Mirinda, Bubly, Mountain Dew; Kas, Schwip Schwap, Tropicana, Aquafina and Drinkfinity). Through an international joint venture together with Unilever, PepsiCo also markets ready-to-drink tea products (under the Lipton brand name).

(22) In addition, PepsiCo produces soft drink concentrates and syrups that it supplies to hotels, restaurants and catering services. These concentrates and syrups are mixed together with water and CO2 in specialized dispensing machines (soft drink dispensing machines visible in the counters of fast food restaurants).

(23) PepsiCo has also recently started to commercialize and develop consumer solutions for flavoured water.

(a) In 2018, PepsiCo launched a specific branded solution (Drinkfinity) comprising a special bottle and flavor pods, whereby pods can be pierced and their content can be compressed out and into a bottle.

(b) According to information provided by the Notifying Party, PepsiCo is also in the final stages of the creation and commercialization of a new sport drink product platform – called “Gx” – that consists of a special bottle, or “vessel” (where the water is stored), and consumable “pods” of a given flavour and hydration formula.

(24) PepsiCo has not been active in the home carbonation system market prior to the transaction in the EEA. Only in the US, SodaStream and PepsiCo entered into an arrangement whereby PepsiCo would supply Pepsi- and Sierra Mist-branded pods of dilutable concentrates and syrups for consumers’ use with home carbonation systems. […].

(25) SodaStream is specialized in home carbonation systems and manufactures different type of devices as well as carbonation bottles and CO2-cylinders. […].

(26) SodaStream also sells concentrates, syrups and flavours for the preparation of carbonated soft drinks.

4.2. The Notifying party's view

(27) The Notifying party submits that the Transaction does not lead to any horizontal overlaps between the Parties in any plausible relevant market. The main products of the Parties, PepsiCo’s packaged carbonated soft drinks and SodaStream’s home carbonation systems, would not be substitutable, but rather complementary in the overall beverages industry.

(28) Further, the Notifying Party claims that they do not compete in the sector of concentrates, syrups and flavours to be diluted into water. SodaStream’s offering in this sector consists of bottled concentrates, syrups and flavours that are intended to be mixed with water after being carbonated with home carbonation system, while PepsiCo does not produce or market any such bottled concentrates or syrups to the retail market or to end consumers in the EEA.

(29) The Notifying party holds the view that the Transaction does not lead to any conglomerate relationship as there would be no link between sales of home carbonated appliances and sales of sparkling water or soda in the EEA. In particular the Notifying party submits that the Parties could not limit the ability of consumers to purchase any carbonated soft drink, any home carbonation system and any dilutable, for their own different purposes and that there are numerous competitors active in all three sectors, particularly regarding carbonated soft drinks and dilutable concentrates, syrups and flavours, which are highly fragmented and characterized by a large number of players.

4.3.2. Beverages, concentrates, syrups and consumer solution for flavoured water

(32) PepsiCo is an important player in the beverage market. According to the estimates of the Parties, PepsiCo has market shares below 30% under all plausible market definitions, with the exception of cola flavoured carbonated soft drinks and ready to drink tea on certain national markets.

(33) As to cola flavoured carbonated soft drinks, PepsiCo has market shares above 30% in Finland ([30-40]%), Norway ([30-40]%), Poland ([30-40]%), Romania ([30-40]%) and the UK ([30-40]%). However, in these national markets, PepsiCo follows at distance CocaCola that is the clear market leader with market shares respectively of [50-60]% in Finland, [50-60]% in Norway, [40-50]% in Poland, [50-60]% in Romania and [60-70]% in the UK.

(34) As to ready to drink Tea, PepsiCo – through the brand Lipton – has market shares exceeding 30% in Belgium ([60-70]%), France ([50-60]%), Greece ([40-50]%), the Netherlands ([40-50]%), and the UK ([70-80]%) and is the market leader in these national markets.

(35) SodaStream has limited sales of dilutables and estimates its market share of approximately [0-5]% at EEA level while at national level its market shares would not exceed 5% in any national market, as they range between under [0-5]% (e.g., Netherlands, Denmark) and [0-5]% (Germany).

4.4. The Commission's assessment

(36) On the basis of the product and geographic relevant markets defined above in section 3, the Commission will assess whether Transaction leads to any horizontal overlaps or vertical relationships between the activities of the Parties.

(37) Further, in light of the fact that the Parties are active on closely related markets, the Commission will also assess possible conglomerate effects arising from the Transaction.

No horizontally or vertically affected markets

(38) The Commission observes that, in light of the activities of the Parties, the Transaction does not give rise to any horizontal overlap as the products of the Parties are highly differentiated. PepsiCo sells ready to go sparkling water and soft drinks, while SodaStream commercializes devices that ultimately allow to fulfil the same needs, but require a higher investment at the beginning and the beverage produced is mostly suitable for domestic use.12

(39) The only potential overlap arise in relation to concentrates, syrups and flavours sold to final consumer for dilution in sparkling or still water as both Parties are active in this sector. However, the consumer solution for flavoured water sold by PepsiCo under the Drinkfinity brand is a nascent system which only achieved very limited sales ([…]), and is only available on-line ([…]). The product also appears to have a different functioning from SodaStream's dilutables. 13 As regards Gx, it is not yet available in the EEA and it is meant for the production of non-carbonated energy beverages.

(40) The Transaction does not give rise to any vertical relationships.

Conglomerate effects

(41) Overall, during the market investigation, customers did not express concerns about the impact of the transaction on any of the relevant product markets. However, comments of a competitor14 suggest that the merged entity could use its financial and portfolio strength to limit the access of competitors or impose worse contractual conditions on retailers. Therefore, the Commission has carefully assessed possible conglomerate effects.

(42) During the market investigation, several market participants indicated that, contrary to the submission of the Parties, there could be links between home carbonated appliances, dilutables, bottled sparkling water and soft drinks15 and it also results from internal documents, […].16

(43) However, it must be noted that in the assessment of conglomerate effects a distinction must be drawn between a pure portfolio effect understood as an incentive on customers to buy the range of products from a single shop (one-stop- shopping) rather than from many suppliers and a strategic use of the portfolio and financial leverage resulting from a strong market position from one market to another by means of tying or bundling or other exclusionary practices.17 Pure portfolio effects, although conferring a competitive advantage on suppliers, are not necessarily regarded as anticompetitive in merger control.18 Conglomerate effects may only result in a significant impediment to competition when the new entity decides to use its market power in one market by conditioning sales in a way that links the products in the separate markets in a particular and strategic way in order to disadvantage its competitors or potential entrants.19

(44) Non-horizontal mergers pose no threat to effective competition unless the merged entity has a significant degree of market power in at least one of the markets concerned.20 The effects of bundling or tying can only be expected to be substantial when at least one of the merging parties' products is viewed by many customers as particularly important and there are few relevant alternatives for that product.21

(45) As explained above under section 4.3.1, this condition is fulfilled at least for SodaStream that is the clear market leader on the home carbonation systems market, with estimated market shares above [90-100]% at EEA level between [60-100]% at national level. As concerns PepsiCo, it has also a strong market position on certain national market with its brands Lipton, as indicated above under paragraph (34) and several of its brands might be considered as important by retailers

(46) Moreover, from the market investigation it results, as indicated above under paragraph (31), that there are only a limited number of competing products on the market for home carbonation systems.

(47) However, it needs further to be assessed whether the merged entity may be able to use its market power to foreclose competitors in another market by conditioning sales in a way that links the products in the separate markets together, by tying or bundling.22 In general, the specific characteristics of the products may be relevant for determining whether any of these means of linking sales between separate markets are available to the merged entity.23

(48) First, technical tying is possible only in certain industries as it occurs where a product can be designed in such a way that it only works with the tied product and not with the alternatives offered by competitors.24

(49) The market investigation confirmed the submission of the Parties that from a technical point of view it does not appear possible to tie the use of home carbonation systems and dilutable concentrates, syrups and flavours. Even assuming that Sodastream would launch in the consumer markets dilutables with the brands Pepsi, Tropicana or Lipton, from a technical point of view, consumers cannot be prevented from using any additive dilutable from any brand with water after it has been carbonated with a SodaStream's device. Vice-versa consumers could not be prevented from using any PepsiCo additive dilutable also in connection with soda makers of other brands.25

(50) Second, contractual tying or bundling usually refers to the way products are offered and priced by the merged entity and is very unlikely to be possible if products are not bought simultaneously or by the same customers.26

(51) The products of the Parties, ie SodaStream's home carbonations systems and PepsiCo's beverages, are not bought simultaneously and there is a large common pool of customers for the individual products concerned. The Parties' customers are retailers and final consumers. In relation to retailers, even for retailers buying both home carbonated appliances and sodas, purchases are managed by different buyers. For final consumers bottled and canned beverages are alternatives to the use of home carbonations systems. On the other hand, as concerns dilutables like concentrates, syrups and flavours to be used in connection with home carbonation systems, during the market investigation, competitors and customers indicated that home carbonation systems such as those of SodaStream are used mainly for home-made sparkling water and it is not expected that in the future consumers would use these devices predominantly for home-made carbonated soft drinks. Hence, the use of home carbonation systems is largely independent from the use of dilutable concentrates, syrups and flavours.27

(52) In addition, the Commission observes that there is no evidence that the Parties would have the incentive to engage in any foreclosure strategy. In particular, there is no evidence in internal strategic documents that the Parties would envisage a strategy of bundling and tying post-Transaction, […].

(53) As the characteristics of the Parties’ products and use do not differ between the different national markets, this reasoning apply to all EEA national markets where the Parties are active.

(54) For the reasons set out above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as regards any conglomerate effects of the concentration between, on the one hand, the manufacturing of home carbonation systems and, on the other hand, the sales of sparkling water, soft drinks or dilutables concentrates, syrups and flavours.

5. CONCLUSION

(55) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 395, 31.10.2018, p. 23.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

5 See eg Commission decision in Case M.8244, The Coca-Cola Company/Cocacola Hbc/Neptuno Vendenys, paras 18-23.

6 See Commission decisions in Case No IV/M.794 - Coca-Cola/Amalgamated Beverages GB, Case M.6522, Groupe Lactalis/Skanemejerier, paras 8-10; Case M.2504, Cadbury Schweppes/Pernod Ricard, paras 9-14; Case M.2276, The Coca-Cola Company/Nestle/JV, paras 17-22.

7 Commission decision in Case M.5633, PepsiCo/The Pepsi Bottling Group

8 Replies to question 6 of Q2 to customers.

9 Replies to question 6.1.of Q2 to customers.

10 Replies to question 5 of Q2 to customers.

11 See eg Commission decision in case M.8224, The Coca-Cola Company / Coca-Cola HBC / Neptuno Vandenys, paras 25-27.

12 See eg the reply of a Customer to question 6.1. of Q2 to customers.

13 The Drinkfinity system comprises a special bottle and flavour pods, whereby pods can be pierced and their content can be compressed out and into a bottle, which is different from SodaStream's syrup where the disposable bottles content are poured and diluted into water.

14 Minutes of the call with a competitor on 10 October 2018.

15 Replies to questions 12 and 13 of Q2 to customers.

16 See slide 20 of Annex 5.4.a.2. to the Form CO and slide 11 of Annex 5.4.a.5 to the Form CO..

17 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings, JO C 265, 18.10.2008 (non-horizontal guidelines), para 93.

18 See non-horizontal guidelines, para. 104.

19 Non-horizontal guidelines, para. 95.

20 Non-horizontal guidelines, para. 23.

21 Non-horizontal guidelines, para. 99.

22 Non-horizontal guidelines, para. 95.

23 Non-horizontal guidelines, para. 98.

24 Non-horizontal guidelines, para. 97.

25 Replies to question 22 of Q2 to customers.

26 Non-horizontal guidelines, para. 98.

27 Replies to questions 21 and 21.1 of Q1 to competitors; and to questions 21 and 21.1 of Q2 to customers.