Commission, December 21, 2018, No M.9122

EUROPEAN COMMISSION

Judgment

TCCC / COSTA

Subject: Case M.9122 - TCCC / Costa

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 20 November 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which The Coca-Cola Company ("TCCC" or the "Notifying Party", U.S.), acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of Costa Limited ("Costa", UK) by way of purchase of shares ("the Transaction”). (3) TCCC and Costa are together referred to as the "Parties".

1. THE PARTIES

(2) TCCC is a US-based brand owner and licensor of various trademarks used to market and sell non-alcoholic commercial beverages. (4) It produces soft drink concentrate and syrups that it supplies to bottling and canning operations ("Bottlers"), as well as fountain retailers. (5) TCCC also administers Coca-Cola Bottlers' Agreements entered into with the Bottlers to which it sells its concentrates and syrups, and is responsible for the consumer marketing of beverages sold under its trademarks. In certain instances, TCCC produces and sells finished beverages.

(3) Costa operates coffee shops in a limited number of EU Member States. Costa and its affiliated entities engage in this business in the EU through multichannel operations including equity stores and franchise stores. In addition, Costa has a wholesale operations for the sale of packaged, roast and ground ("R&G") coffee and other ingredients. Costa also operates hot beverage vending machines ("express machines") through self-serve Costa Express machines located at its partners' premises.

2. THE OPERATION AND THE CONCENTRATION

(4) The transaction consists in the acquisition of the entire share capital of Costa by TCCC. The SPA was signed on 31 August 2018.

(5) Therefore, the Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (TCCC: 31 345 million, Costa […]). (6) Each of them has a Union-wide turnover in excess of EUR 250 million (TCCC: […], Costa […]), but neither undertaking achieves more than two-thirds of its aggregate Union-wide turnover within one and the same Member State.

(7) The notified operation therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Parties' activities

(8) TCCC owns or licences and markets about 500 non-alcoholic ready-to-drink commercial beverage brands, which can be grouped into the following category clusters: sparkling soft drinks; water; enhanced water and sports drinks; juice, dairy and plant based beverages; and ready-to-drink tea and coffee. (7) (8)

(9) TCCC also owns Chaqwa, a branded hot beverage vending business. TCCC's bottler, Coca-Cola European Partners plc ("CCEP"), owns and operates the machines using product and marketing support supplied by and brand and trademarks licensed from TCCC. Chaqwa machines predominantly dispense hot coffee but also serve other hot beverages (tea and hot chocolate). The Chaqwa machines are currently only supplied in Germany, Belgium, Norway, Sweden and Iceland. (9)

(10) Through the proposed Transaction, TCCC will be adding to its portfolio the following products:

– Costa's coffee shops, mainly in the UK, Ireland and Poland.

– Costa's Proud to Serve ("PtS") products, a suite of ingredients and branded accessories required for a customer to recreate the Costa products out-of-home, such as hospitals, universities, petrol stations and leisure venues. (10) PtS products are currently marketed only in the UK and Ireland.

– Costa's R&G coffee and Tassimo discs. (11) Both products are targeted ultimately toward end customers for use at home. These products are marketed only in the UK and Ireland. (12)

– Costa Express machines, i.e. self-serve hot beverage vending machines located at Costa's partners' premises. Costa operates [8,000 - 8,250] Costa Express machines worldwide, including [7,750 - 8,000] in the EEA, the overwhelming majority of which are in the UK.

4.2. Relevant product market definitions

(11) The Transaction leads to:

(a) Vertical links between the supply by TCCC of non-alcoholic ready-to- drink commercial beverages ("NABs") and Costa's coffee shops; and

(b) Conglomerate links between TCCC's NABs and Costa's PtS products, R&G coffee and Tassimo discs as well as Express machines described at paragraph (10) above.

(12) The Transaction may also give raise to limited horizontal overlaps, which in any event do not result in horizontally affected markets. (13) Therefore, these links will not further be discussed in the present decision.

4.2.1. Supply of non-alcoholic ready-to-drink commercial beverages ("NABs")

Brand ownership and bottling

(13) Commission precedents (14) described the supply of NABs as consisting of two interrelated activities: namely brand ownership upstream and bottling downstream:

(a) Brand ownership typically involves the creation and support of brands, the supply of beverage concentrate, and the authorisation of local bottlers to prepare, package, distribute and sell the beverages. Brand owners usually have primary responsibility for consumer marketing such as television, radio, cinema, and press advertising, as well as sponsorship of activities such as music and sports.

(b) Bottling typically involves preparing, packaging, selling, marketing, and distributing the final product in a territory assigned by the brand owner. Bottlers generally have operational responsibility for marketing closer to the retail level, including promotional discounts and trade marketing. Such efforts are closely coordinated with the brand owner's marketing and support activities. In case of TCCC, authorised bottlers either combine the concentrates with sweeteners (depending on the product), still water and/or sparkling water, or combine the syrups with sparkling water to produce finished beverages. The finished beverages are packaged in authorised containers bearing TCCC's trademarks and are then sold mainly to retailers directly or, in some cases, through wholesalers and distributors.

(14) Bottlers operate in different EEA countries on the basis of their agreements with TCCC, which confer them with an […] licence to market, distribute, bottle and sell TCCC branded beverages in their respective territories.

(15) On the markets affected by the present transaction, TCCC […] and maintains that bottlers are operationally independent from TCCC. However, many aspects of the bottlers’ operations, such as marketing decisions, are influenced by TCCC. In addition, the prices at which concentrate is supplied to bottlers are set by reference to, and as a prescribed percentage of, each bottler's wholesale net sales prices set by the bottler to its customers, thus reducing the business risk a bottler needs to assume on its own. (15)

(16) In addition, certain finished products ([…]) and large and international accounts are directly managed by TCCC and not through the bottlers.

(17) Therefore, the full independence of the bottlers’ businesses form TCCC’s cannot be established with certainty.

(18) In view of the above and ,taking a precautionary approach, the Commission considers that TCCC's market position should be assessed also including the sales of its products through the bottlers.

Segmentation by type of NAB

(19) In previous decisions, the Commission has considered that, within NABs, carbonated soft drinks (“CSDs”) constitute a separate market from non- carbonated soft drinks (NCSDs). (16) In particular, the Commission has previously considered a narrower market segmentation for cola-flavoured CSDs. (17) In its past decisional practice the Commission also indicated that NCSDs could be segmented into packaged water, fruit juices, ready-to-drink teas and energy and sports drinks, although ultimately left the question on such segmentation open. (18)

(20) Given the absence of any material horizontal overlaps between the operations of the Parties, the Parties do not consider it necessary to reach a definitive view on the scope of the relevant product market.

(21) The Commission considers that, for the purpose of this decision, the exact scope of the product market can be left open since the Transaction does not give rise to serious doubts about its compatibility with the internal market even under the strictest plausible definition of the product market (i.e. the Coca Cola branded products).

Segmentation by distribution channel

(22) Previous Commission’s decisions considered separate product markets according to the distribution channel of NABs distinguishing between the off-premises (retail) and the on-premises consumption market (including, for example, hotels, restaurants, and cafes, known as the"HoReCa" sector). (19)

(23) Respondents to the market investigation confirmed the Commission's findings in previous cases. (20) Therefore, the Commission considers that the effects of the Transaction should be assessed on the two separate product markets for the off- premises channel and the on-premises one.

4.2.2. Operation of coffee shops/informal restaurants

(24) The Commission has not previously defined a relevant product market for the operation of coffee shops specifically, but previous cases indicated that coffee shops are part of a market for informal restaurants. (21) Precedents involving fast food restaurants investigated whether a further segmentation of informal restaurants into "informal restaurants", "informal eating-out restaurants" or "eat-in quick-service restaurants", "(chained) quick service restaurants" and "take away/home delivery" was necessary. (22)

(25) The Notifying Party submits that branded coffee shops, such as Costa, face competition also from independent coffee shops, fast food (quick service) restaurants and other casual dining restaurants that serve hot beverages. Therefore, according to the Notifying Party, the market could be wider than coffee shops alone.

(26) The Commission's market investigation provided a number of indications that coffee shops do compete with informal restaurants (23), while the answers as to whether branded coffee shops competed with the unbranded ones were less conclusive. (24)

(27) The Commission considers that, for the purposes of this decision, the exact scope of the relevant product market can be left open in this respect since the Transaction does not give rise to serious doubts as to its compatibility with the internal market even under the strictest plausible definition of the product market (i.e., branded coffee shops).

4.2.3. Provision of vending services (vending machines)

(28) The Commission has previously considered the provision of vending services, but left open the question of whether the market should be further segmented by the type of food dispensed in (i) hot beverages, (ii) cold drinks and (iii) snacks and food. (25)

(29) The Notifying Party considers that for the purposes of the present Transaction, the relevant market in respect of coffee vending machines should be that for the provision of vending services, i.e. the sale of products and services at an unattended point of sale, using some form of payment. (26)

(30) Respondents to the market investigation confirmed the Commission's description of this products in previous cases, (27) but were not definitive as to a segmentation of vending services by type of beverage/food as well as by type of distribution machine, such as, for example, vending machines, beverage machines used in hotels, restaurants or cafeterias and small capacity machines without payment system designed for office coffee supply. (28)

(31) The Commission considers that, for the purpose of this decision, the exact scope of the product market can be left open since the Transaction does not give rise to serious doubts about its compatibility with the internal market even under the strictest plausible definition of the product market (i.e., vending services for hot beverages only).

4.2.4. Manufacture and sale of coffee and other ingredients

(32) In previous decisions, the Commission has considered that the manufacture and sale of coffee via the "in-home" and "out-of-home" channels form part of separate product markets. In-home encompasses the sale of coffee to consumers via retailers or directly to consumers. Out-of-home encompasses the sale of coffee to hotels, restaurants or cafes (referred to as "HoReCa") but also to offices, hospitals, educational establishments and other work places. (29)

(33) The Commission has also considered that all out-of-home sales belong to the same product market. (30) Conversely, the Commission has segmented the in-home channel into (i) instant coffee, (ii) R&G coffee, (iii) filter pads, (iv) Nespresso compatible capsules, (v) other espresso capsules, and (vi) multi-drink capsules. (31)

(34) The Commission also considered whether R&G coffee in-home was in the same market as whole coffee beans, but ultimately left open the precise product market definition in this respect. (32)

(35) The Notifying Party does not disagree with the Commission's findings in previous cases. (33)

(36) The Commission considers that, for the purpose of this decision, the exact scope of the relevant product market can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market even under the strictest plausible definition of the relevant product market (manufacture and sale of coffee and other ingredients in the out-of-home channel; manufacture and sale of R&G coffee only and Tassimo discs only (34), both in the in-home channel).

4.3. Geographic market definitions

4.3.1. Supply of non-alcoholic ready-to-drink commercial beverages ("NABs")

(37) The Commission has consistently found that the geographic scope of the supply of NABs is national due to, inter alia, differences in consumption patterns, logistics and distribution networks and marketing strategies. (35)

(38) The Notifying Party agrees with this geographic scope. (36)

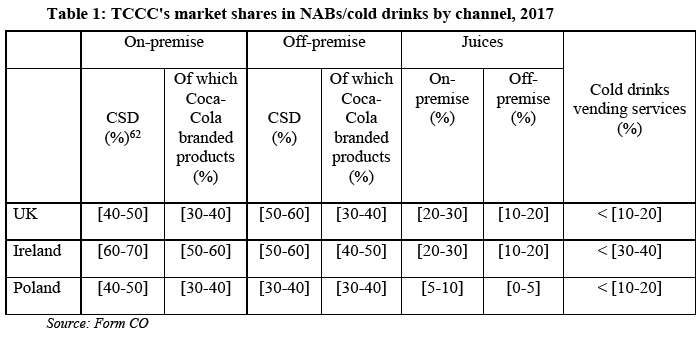

(39) Respondents to the market investigation confirmed the Commission's findings in previous cases. (37)

(40) Based on the above, the Commission will conduct its assessment of the markets for NABs on a national basis.

4.3.2. Operation of coffee shops/informal restaurants

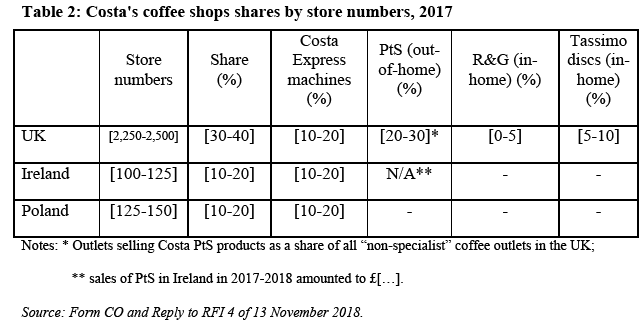

(41) As concerns the market for informal restaurants, Commission precedents considered its geographic scope to be at least national, leaving the precise market definition open. (38)

(42) The Notifying Party submits that also for coffee shops the relevant geographic market should be considered national, as in particular price and product ranges of branded chains are typically determined on a national basis. This is also the case for Costa's equity stores. (39)

(43) The market investigation was not conclusive as to the exact scope of the geographic market. (40)

(44) The Commission considers that, for the purpose of this decision, the exact scope of the geographic market can be left open since the Transaction does not give rise to serious doubts about its compatibility with the internal market even under the strictest plausible definition of the geographic market (national).

4.3.3. Provision of vending services (vending machines)

(45) The Commission has in the past found that the relevant geographic markets for the provision of vending services in general are national in scope due to the absence of EU-wide legislation for the vending industry, the difference in lifestyle and culture between the various European countries and the need for having teams of staff (machine engineers, stockists, operators) available in reasonable proximity. (41)

(46) The Notifying Party therefore submits it would be appropriate to examine the Proposed Transaction by reference to national geographic markets. (42)

(47) Respondents to the market investigation confirmed the Commission's findings in previous cases that the geographic scope of this market is national. (43)

(48) The Commission considers that, for the purpose of this decision, the exact scope of the geographic market can be left open since the Transaction does not give rise to serious doubts about its compatibility with the internal market even under the strictest plausible definition of the geographic market (national).

4.3.4. Manufacture and sale of coffee and other ingredients

(49) The Commission has determined in previous cases that the geographic scope for the markets for the supply of various types of coffee is national. (44) This conclusion was reached on the basis of (i) the high importance of national brands; (ii) the presence of national differences in terms of consumption by consumers; (iii) the divergence in market shares of the relevant suppliers in the different Member States; (iv) the fact that negotiations with retailers regarding supply and pricing of coffee products are national; and (v) the presence of national and regional competitors.

(50) The Commission has not found evidence to contradict its previous findings in this respect and will therefore conduct its assessment on a national basis.

5. COMPETITIVE ASSESSMENT

5.1. Framework of analysis

(51) Article 2 of the Merger Regulation provides that the Commission has to appraise concentrations with a view to establishing whether or not they are compatible with the internal market. For that purpose, the Commission must assess, pursuant to Article 2(2) and (3), whether or not a concentration would significantly impede effective competition, in particular as a result of the creation or strengthening of a dominant position in the common market or a substantial part of it.

(52) The Commission’s assessment of this Transaction focuses on (i) vertical non- coordinated effects due to the creation of vertical links between the Parties as well as (ii) conglomerate non-coordinated effects due to the combination of TCCC's products with Costa's.

Vertical non-coordinated effects

(53) Vertical mergers involve companies operating at different levels of the same supply chain. For instance, a vertical merger occurs when a manufacturer of a certain product merges with one of its distributors.

(54) Pursuant to the Commission Guidelines on the assessment of non-horizontal mergers under the Merger Regulation (the “Non-Horizontal Merger Guidelines”) (45), vertical mergers do not entail the loss of direct competition between merging firms in the same relevant market and provide scope for efficiencies. (46)

(55) However, there are circumstances in which vertical mergers may significantly impede effective competition. This is in particular the case if they give rise to foreclosure. (47)

(56) The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure: input foreclosure, which arises where the merger is likely to raise costs of downstream rivals by restricting their access to an important input, and customer foreclosure, which exists where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base. (48)

(57) Pursuant to the Non-Horizontal Merger Guidelines, input foreclosure arises where, post-merger, the new entity would be likely to restrict access to the products or services that it would have otherwise supplied absent the merger, thereby raising its downstream rivals' costs by making it harder for them to obtain supplies of the input under similar prices and conditions as absent the merger. (49)

(58) For input foreclosure to be a concern, the merged entity should have a significant degree of market power in the upstream market. Only when the merged entity has such a significant degree of market power, can it be expected that it will significantly influence the conditions of competition in the upstream market and thus, possibly, the prices and supply conditions in the downstream market. (50)

(59) Pursuant to the Non-Horizontal Merger Guidelines, customer foreclosure may occur when a supplier integrates with an important customer in the downstream market and because of this downstream presence, the merged entity may foreclose access to a sufficient customer base to its actual or potential rivals in the upstream market (the input market) and reduce their ability or incentive to compete, which, in turn, may raise downstream rivals' costs by making it harder for them to obtain supplies of the input under similar prices and conditions as absent the merger. This may allow the merged entity to profitably establish higher prices on the downstream market. (51)

(60) For customer foreclosure to be a concern, a vertical merger must involve a company which is an important customer with a significant degree of market power in the downstream market. If, on the contrary, there is a sufficiently large customer base, at present or in the future, that is likely to turn to independent suppliers, the Commission is unlikely to raise competition concerns on that ground. (52)

Conglomerate non-coordinated effects

(61) Conglomerate mergers consist of mergers between companies that are active in closely related markets, for instance suppliers of complementary products or of products which belong to a range of products that is generally purchased by the same set of customers for the same end use. (53)

(62) Pursuant to the Non-Horizontal Merger Guidelines, in most circumstances, conglomerate mergers do not lead to any competition problems. (54) However, foreclosure effects may arise when the combination of products in related markets may confer on the merged entity the ability and incentive to leverage a strong market position from one market to another closely related market by means of tying or bundling or other exclusionary practices. (55)

(63) The Non-Horizontal Merger Guidelines distinguish between bundling, which usually refers to the way products are offered and priced by the merged entity and tying, which usually refers to situations where customers that purchase one good (the tying good) are required to also purchase another good from the producer (the tied good). (56)

(64) Within bundling practices, a distinction is also made between pure bundling and mixed bundling. In the case of pure bundling the products are only sold jointly in fixed proportions. With mixed bundling the products are also available separately, but the sum of the stand-alone prices is higher than the bundled price. (57)

(65) Tying can take place on a technical or contractual basis. For instance, technical tying occurs when the tying product is designed in such a way that it only works with the tied product (and not with the alternatives offered by competitors).

(66) While tying and bundling have often no anticompetitive consequences, in certain circumstances such practices may lead to a reduction in actual or potential competitors' ability or incentive to compete. This may reduce the competitive pressure on the merged entity allowing it to increase prices or deteriorate supply conditions in other ways. (58)

(67) In assessing the likelihood of such a scenario, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals (59), second, whether it would have the economic incentive to do so (60) and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers.(61) In practice, these factors are often examined together as they are closely intertwined.

5.2. Market shares

(68) As regards TCCC’s market share in selling NABs in the on-premise channel upstream, TCCC would have more than 40% of the CSD market in the UK, Ireland and Poland based on the Notifying Party's estimates, as illustrated by Table 1 below. The […] of these market shares is represented by Coca-Cola branded products.

(69) In the off-premise market TCCC's share in selling NABs is above 50% in the UK and Ireland and [40-50]% in Poland. As in the on-premise channel, the […] these market shares is represented by Coca-Cola branded products.

(70) Table 1 also shows TCCC’s market share in juices as well as in vending services for cold drinks. The share of TCCC in juices is below 30% in both the on-premise and off-premise channels in each of the three countries considered. The share of TCCC cold drinks vending services is estimated at less than [10-20]% in the UK and Poland and less than [30-40]% in Ireland.

(71) As regards Costa’s market share in operating coffee shops downstream, Table 2 below shows the number and the share of Costa's branded coffee shops in the UK, Ireland and Poland, by number of shops for 2017. If independent coffee shops where included in the relevant market, the Costa's share is would be reduced sizeably. (63)

(72) Table 2 also shows Costa's market shares for the other three lines of Costa's products, namely Costa Express vending machines, PtS and R&G and Tassimo discs in 2017 in the national markets where Costa is present.

5.3. Assessment of vertical non-coordinated effects

(73) Vertically affected markets arise in the UK, Ireland and Poland between TCCC's upstream supply of CSDs and juices for on-premises consumption and Costa's downstream operations of informal restaurants (coffee shops) in these countries.

No input foreclosure effects

(74) The Notifying Party submits that: (1) TCCC does not have the ability to foreclose NAB products to Costa's competitors, as ([…]) the informal restaurants (including coffee shops) generally purchase TCCC products from TCCC's Bottlers or from wholesalers/distributors, and (2) TCCC's Bottlers are operationally independent. (64)

(75) The Notifying Party also submits that TCCC does not have an incentive to foreclose NAB products to Costa's competitors. In the UK, TCCC's sale of NABs to Costa account for […] of its revenues as opposed to TCCC's sales to Costa's competitors that could be lost through input foreclosure. Therefore, according to the Notifying Party, an input foreclosure strategy by TCCC would not to be profitable. (65)

(76) The Notifying Party further explains that NABs are not an important input or core product for Costa that would drive demand, and they are not required for Costa to compete with other coffee shops. For instance, the sale of TCCC's NABs contributes only to [0-5]% of Costa's sales. (66)

(77) The market investigation provided broad support to the Parties' arguments. Although TCCC is one of the leading suppliers of CSDs, the Transaction would be unlikely to significantly impact the market structure, since several suppliers of CSDs will remain available on the market such as: PepsiCo ([30-40]%), A G Barr ([5-10]%) and Britvic ([5-10]%) in the UK; PepsiCo ([20-30]%) and Britvic ([5-10]%) in Ireland; and PepsiCo ([30-40]%) in Poland.

(78) In addition, a key competitor of Costa's coffee shops explained that, other than limited purchases from Innocent juices, which is a TCCC affiliate, it does not buy any other TCCC products (including Coca Cola). (67) This suggests that TCCC branded NABs may not be necessary for Costa's competitors in order to successfully compete. Therefore, even if TCCC foreclosed its branded NABs to other coffee shops, this would likely have no impact on competition on the market for informal restaurants including coffee shops.

(79) Moreover, the Commission's investigation also showed that a possible input foreclosing strategy would potentially be unprofitable as Costa's coffee shops account for only a limited portion of TCCC total sales of NABs. Therefore, any losses incurred to TCCC by foreclosing NABs to Costa’s competitors would not be compensated by increased turnover at Costa’s.

(80) Finally, in the course of the market investigation, no substantiated concerns were raised by market participants as to the impact of the transaction on their businesses or on the market. (68)

(81) In light of the above and the evidence available to the Commission and in view of the outcome of the market investigation, it appears unlikely that the Parties would have the ability and/or incentive to engage in an input foreclosure strategy after the Transaction.

No customer foreclosure effects

(82) The Notifying Party explains that Costa would have neither the ability nor the incentive to foreclose TCCC's competitors in the upstream market for the supply of NABs. Although Costa is the largest branded coffee shop chain operator in the UK, Costa is a relatively minor distribution channel for suppliers of NABs. (69)

(83) The Notifying Party also submits that any such attempt to foreclose would not materially affect the upstream competitors' business, whereas it could negatively affect Costa, since for the success of its own business it has an interest to choose its NABs’ offering on the basis of their appeal to customers, regardless of their origin. (70)

(84) The market investigation provided broad support to the Parties' arguments. Although Costa is the largest branded coffee shop chain operator in the UK, with [2,250 – 2,500] stores, including franchise shops (and [30-40]% market share), followed by Starbucks, [750-1,000] shops ([10-20]%) and Caffè Nero, [250-500] shops ([5-10]%), Costa still represents a minor distribution channel for suppliers of NABs. (71) This suggests that, should TCCC decide to foreclose its competitors from Costa, TCCC's competitors will retain access to the vast majority of the downstream market.

(85) Moreover, in the course of the market investigation, no substantiated concerns were raised by market partipants as to the impact of the transaction on their businesses or on the market. (72)

(86) In light of the above and the evidence available to the Commission and in view of the outcome of the market investigation, it appears unlikely that the Parties would have the ability and/or incentive to engage in a customer foreclosure strategy after the Transaction.

5.4. Assessment of conglomerate non-coordinated effects

(87) The Transaction leads to conglomerate links between:

(a) TCCC's NABs (and Coca-Cola products specifically) and Costa’s PtS products which are sold to customers for on-premise/out-of-home consumption,

(b) TCCC's NABs (and Coca-Cola products specifically) and Costa’s Tassimo discs and R&G products which are sold to retailers for off-premise/in- home consumption, and

(c) TCCC's cold drinks vending services (including Coca-Cola products specifically) and Costa’s Express machines which are sold to customers who have vending machines on their premises, such as large supermarkets, hotel chains, restaurants and large corporate organizations. (73)

(88) The Commission’s assessment of conglomerate non-coordinated effects therefore focusses on:

(a) the potential leveraging of TCCC’s position in NABs/Coca-Cola for on premise/out-of-home consumption in the UK and Ireland to foreclose Costa’s on-premise/out-of-home coffee competitors in the same countries; (74)

(b) the potential leveraging of TCCC’s position in NABs/Coca-Cola off premise/retail in the UK and Ireland to foreclose in-home coffee competitors in the same countries; (75) and

(c) the potential leveraging of TCCC’s position in cold drinks vending services/Coca-Cola in the UK, Ireland and Poland to foreclose competitors in vending services (vending machines) in the same countries. (76)

Leveraging of TCCC’s position in NABs/Coca-Cola on premises (out-of- home) in the UK and Ireland to foreclose out-of-home coffee competitors in the same countries

(89) The Notifying Party submits that TCCC does not have the ability to bundle or tie or otherwise condition its sale of Coca-Cola products in the on-premise/out-of- home sales channel on the purchase of Costa's products, as customers, if they purchase both, purchase NABs and coffee products separately. (77)

(90) The Notifying Party further argues that both businesses (TCCC’s and Costa’s) are operated by independent companies: the sale of TCCCs products is carried out through […] bottlers and a bundling strategy could jeopardise their NAB sales. (78)

(91) In addition, the Notifying Party submits that many large TCCC on-premises customers (e.g. fast food chains) have a clear preference for unbranded coffee and have sufficient bargaining power to resist any bundling strategy. (79)

(92) The Notifying Party also submits that TCCC does not have the incentive to engage in a bundling or tying strategy, as the turnover that can be achieved through the sales of PtS products is far inferior compared to the significance of the TCCC NAB business. (80)

(93) In any event, the Notifying Party is of the view that such a bundling strategy would not have an effect on the market. (81)

(94) The market investigation provided broad support to the Notifying Party's arguments. While acknowledging that TCCC holds a strong market position in NABs with brands that are considered to be particularly important, the majority of customers who responded to the Commission's market investigation indicated that NABs and coffee products, such as Costa’s PtS, are generally purchased separately by on-premises/out-of-home customers and are typically not part of the same buying decision. (82) To this end one customer noted that "For hot coffee then there is no cross over of decision making and the decision is entirely separate from NAB". (83)

(95) When asked how customers would react to a hypothical tie/bundle of TCCC's NABs with Costa's PtS products, some customers answered that they would not accept such link between the products/purchasing decisions, that such strategy would even be counter productive and that it would have very limited effects. (84) To this end, one customer observed that "As of today the two markets are considered not linked and remain separate, maybe we will not see any relevant effect in these markets". (85)

(96) More generally, TCCC/Costa’s customers raised no substantiated concerns as to the impact of the transaction on their businesses or on the market. (86)

(97) In light of the above and the evidence available to the Commission and in view of the outcome of the market investigation, it appears unlikely that the Transaction would significantly impede effective competition in the market for the manufacture and sale of coffee and other ingredients in the out-of-home channel in the UK and Ireland as a result of conglomerate non-coordinated effects deriving from the leveraging of TCCC’s position in NABs/Coca-Cola in the on- premises/out-of-home channel in the same countries.

Leveraging of TCCC’s position in NABs/Coca-Cola in the off-premise/retail channel in the UK and Ireland to foreclose in-home coffee competitors in the same countries

(98) The Notifying Party submits that TCCC does not have the ability to bundle or tie or otherwise condition its sale of Coca-Cola products on the purchase of Costa's products, as off-premises/retail customers, such as supermarkets, purchase NABs and coffee products separately, in the context of separate purchasing decisions. (87)

(99) The Notifying Party adds that many of the Parties' competitors are also in a position to offer such bundles, either through their existing product portfolios or through teaming up, if they wanted to, and that therefore competition can also take place at the level of the bundle. (88)

(100) The Notifying Party argues that off-premises customers are large, with significant bargaining power and could counter any bundling strategy by TCCC. (89)

(101) The Notifying Party also reasons that TCCC does not have an incentive to pursue a commercially hazardous strategy in the off-premises channel, as it represents a critically important sales channel, […] times larger than the on-premises channel. (90)

(102) The Notifying Party is of the view that, in any event, such a bundling strategy would not have an effect on the market. (91)

(103) The market investigation provided broad support to the Parties' arguments. While acknowledging that TCCC holds a strong market position in NABs with brands that are considered to be particularly important, the majority of customers who answered the Commission's questionnaire indicated that NABs and coffee products are generally purchased separately and are typically not part of the same buying decision. (92) To this end one leading retail chain noted that "we purchase NAB and hot drinks separately from each other". (93)

(104) When asked how customers would react to a hypothical tie/bundle of TCCC's NABs with Costa's coffee, some customers answered that such strategy would have very limited effects. (94) To this end, one leading retail chain noted that "There would be no or very few impacts". (95)

(105) More generally, TCCC/Costa’s customers raised no substantiated concerns as to the impact of the transaction on their businesses or on the market. (96)

(106) In light of the above and the evidence available to the Commission and in view of the outcome of the market investigation, it appears unlikely that the Transaction would significantly impede effective competition in the market(s) for the manufacture and sale of R&G coffee and Tassimo discs in the in-home channel in the UK and Ireland as a result of conglomerate non-coordinated effects deriving from the leveraging of TCCC’s position in NABs/Coca-Cola in the off premise channel in the same countries.

Leveraging of TCCC’s position in cold drinks vending services/Coca-Cola or supplies of NABs/Coca-Cola in the UK, Ireland and Poland to foreclose competitors in vending services (vending machines) in the same countries

(107) The Notifying Party argues that TCCC would not have the ability to bundle or tie Costa’s vending machines (the Costa Express) with its own vending machines or more in general with its supplies of NABs/Coca-Cola, for the following reasons:

(108) First, the Notifying Party explains that customers usually take purchasing decisions concerning vending machines for NAB and vending machines for coffee separately. (97)

(109) Second, the Notifying Party notes the presence of a large number of competitors (e.g. PepsiCo, Britvic, Nespresso, Dolce Gusto, Starbucks, Lavazza and others) which would not have any capacity or other constraints preventing them from undermining any hypothetical bundling strategy, whether alone or in combination. (98)

(110) Third, TCCC already operates vending machines for coffee, Chaqwa. Therefore, the Costa Express vending machines are not a new addition to TCCC's portfolio of products. (99)

(111) Fourth, the Notifying Party argues that the practical ability of TCCC to implement any bundling/tying strategy for Costa Express and chilled NAB vending machines is limited, as it would require coordination across multiple commercially and operationally independent entities. (100)

(112) The market investigation provided broad support to the Notifying Party's arguments. First, the results of the Commission's market investigation show that in all the countries where Chaqwa is present, namely Germany, Belgium, Norway, Sweden and Iceland, the number of customers that have on their premises both TCCC chilled NAB vending machines and Chaqwa machines are very limited. (101)

(113) As a result of this, Chaqwa's share of supply is less than [0-5]% in Germany, and is similarly low in the other countries where it is present. (102) This suggests that (1) TCCC has not been successfull to leverage any potential strength in NABs to increase their Chaqwa's share, and (2) TCCC would possibly not have the ability to do so with Costa Express. Any hypothetical bundling strategy of Costa Express and TCCC's cold drinks vending services/Coca-Cola is therefore unlikely to result in foreclosure of TCCC's or Costa's rivals.

(114) More generally, TCCC/Costa’s customers raised no substantiated concerns as to the impact of the transaction on their businesses or on the market. (103)

(115) In light of the above and the evidence available to the Commission and in view of the outcome of the market investigation, it appears unlikely that the Transaction would significantly impede effective competition in vending services (vending machines) in the UK, Ireland and Poland as a result of conglomerate non-coordinated effects deriving from the leveraging of TCCC’s position in cold drinks vending services/Coca-Cola in the same countries.

6. CONCLUSION

(116) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 429, 28.11.2018, p. 7.

4 Non-alcoholic commercial beverages is a broad category of non-alcoholic beverages, otherwise known as "soft drinks", including packaged water, still drinks, iced teas, fruit juices, sports and energy drinks and other soft drinks (see e.g. Form CO, paragraph 107).

5 Fountain retailers are outlets, such as restaurants and convenience stores, which use dispensing equipment to mix the syrups with sparkling or still water at the time of purchase to produce finished beverages that are served in cups or glasses for immediate consumption.

6 Turnover calculated in accordance with Article 5 of the Merger Regulation.

7 Form CO, paragraph 70.

8 TCCC's non-alcoholic ready-to-drink commercial beverages (NABs) portfolio also includes a ready- to-drink coffee, marketed under the Honest brand in the UK and Spain. Moreover, TCCC has a licensing agreement with Illy, […]. The main flavours are Illy Caffe Latte, Illy Caffe Vanilla Affogato, Illy Issimo Cafe Espresso, Illy Issimo Caffe Tiramisu and Illy Issimo Latte Macchiato. These are only sold in Cyprus, Czech Republic, Greece, Romania, Slovakia and Slovenia. Given that these are non- carbonated drinks, sold in aluminium cans and PET bottles at ambient or cold temperature, the Commission considers that these products do not lead to a horizontal overlap with Costa products.

9 Form CO, paragraphs 80-86.

10 PtS includes various coffee ingredients (beans, ground and filter coffee), takeaway cups and lids, porcelain cups, saucers and glasses, scoops, beakers, thermometers and other coffee-making equipment, snacks, and cleaning products.

11 Tassimo discs are designed for use within compatible espresso coffee machines. R&G coffee is also designed for consumption at home (but does not require an espresso machine). […].

12 Costa also manufactures […] of R&G retail packs […], which it sells through its own stores in the UK and in a number of other EEA countries.

13 Both TCCC and Costa overlap in vending services for hot beverages at the national level in Germany. However, this does not lead to affected markets as TCCC share is ca. [5-10]% and Costa has only [15- 20] Costa Express machines in Germany.

14 See, e.g., Case IV/M.794 - Coca-Cola/Amalgamated Beverages GB, paragraph 23; Case IV/M.833 - TCCC/Carlsberg A/S, paragraphs 25-30; Case COMP/M.1683 - The Coca-Cola Company/Kar-Tess Group (Hellenic Bottling), paragraphs 11-12; Case COMP/M.5632 - PepsiCo/Pepsi Americas, paragraph 9; Case COMP/M.5633 - PepsiCo/The PepsiCo Bottling Group, paragraph 8, Case M.7763– TCCC/COBEGA/CCEP.

15 TCCC calls this pricing model towards bottlers "incidence pricing".

16 Case M.5633 - Pepsico/The Pepsico Bottling Group, paragraphs 10-12; Case M.833 - The Coca-Cola Company/Carlsberg A/S, paragraph 42; Case M.2276 - The Coca-Cola Company/Nestle/JV, paragraph 17; Case M.6924 - Refresco Group/ Pride Foods, paragraph 15.

17 Case IV/M.1065 – Nestle/San Pelegrino, paragraph 17; Case IV/M.794 – Coca-Cola/Amalgamated Beverages GB, paragraphs 26, 30-94; M.2504 – Cadbury Schweppes/Pernod Ricard, paragraphs 10.

18 Case M.2276 - The Coca-Cola Company/Nestle/JV, paragraph 17; Case M.6924 - Refresco Group/Pride Foods, paragraph 16.

19 Case M.2504 – Cadbury Schweppes/Pernod Ricard, paragraphs 7-14.

20 See replies to Q5 of the Questionnaire to competitors and of the Questionnaire to customers.

21 Case M.4220 – Food Service Project/Tele Pizza, paragraphs 7-13. Informal restaurants” include quick-service restaurants, plus a wide selection of chained and independent informal restaurants, pizzerias, cafes, coffee shops, sandwich bars as well as take-away and home delivery outlets..

22 Cases COMP/M.2940 – TPG Advisors III/Goldman Sachs/Bain Capital Investors/Burger King, paragraphs 12-23; COMP/M.4220 – Food Service Project/Tele Pizza, paragraphs 7-13; and COMP/M.6895 – 3G Special Situations Fund III/ Berkshire Hathaway/ H J Heinz Company, paragraphs 21-23.

23 See replies to Q8 of the Questionnaire to competitors and of the Questionnaire to customers.

24 See replies to Q9 of the Questionnaire to competitors and of the Questionnaire to customers.

25 Case M.8454 – KRR/Pelican Rouge; Case M.6857 – Crace Co/MEI Group.

26 Form CO, paragraph 116.

27 See replies to Q6 of the Questionnaire to competitors and of the Questionnaire to customers.

28 See replies to Q7 of the Questionnaire to competitors and of the Questionnaire to customers.

29 Case M.7292 - DEMB/Mondelez/Charger OPCO, paragraph 43.

30 Case M.7292 - DEMB/Mondelez/Charger OPCO, paragraph 44.

31 Case M.7292 - DEMB/Mondelez/Charger OPCO, paragraph 103, paragraph 107, paragraph 112, paragraph 123, paragraph 136 and paragraph 151.

32 Case M.7292 - DEMB/Mondelez/Charger OPCO, paragraph 136.

33 Form CO, paragraph 122.

34 Case M.7292 - DEMB/Mondelez/Charger OPCO, paragraph 92. In this case the Commission concluded that consumables for the various single-serve systems, such as the Tassimo system, belong to different markets.

35 Case M.2276 – The Coca-Cola Company/Nestlé/JV, paragraph 23

36 Form CO, paragraph 111.

37 See replies to Q10 of the Questionnaire to competitors and of the Questionnaire to customers.

38 Case M.4220 – Food Service Project/Tele Pizza, paragraphs 14-17; Case No COMP/M.6895 - 3G Special Situations Fund III/Berkshire Hathaway/H J Heinz Company, paragraphs 24-25.

39 Form CO, paragraph 99.

40 See replies to Q12 of the Questionnaire to competitors and of the Questionnaire to customers.

41 Case M.8454 – KRR/Pelican Rouge, paragraphs 17-19.

42 Form CO, paragraph 118.

43 See replies to Q11 of the Questionnaire to competitors and of the Questionnaire to customers.

44 Case M.7292 - DEMB/Mondelez/Charger OPCO, paragraph 157.

45 OJ C 265, 18.10.2008, p. 6.

46 Non-Horizontal Merger Guidelines, paragraph 13.

47 Non-Horizontal Merger Guidelines, paragraph 18.

48 Non-Horizontal Merger Guidelines, paragraph 30.

49 Non-Horizontal Merger Guidelines, paragraph 31.

50 Non-Horizontal Merger Guidelines, paragraph 35.

51 Non-Horizontal Merger Guidelines, paragraph 58.

52 Non-Horizontal Merger Guidelines, paragraph 61.

53 Non-Horizontal Merger Guidelines, paragraph 91.

54 Non-Horizontal Merger Guidelines, paragraph 92.

55 Non-Horizontal Merger Guidelines, paragraph 93.

56 Non-Horizontal Merger Guidelines, paragraph 97.

57 Non-Horizontal Merger Guidelines, paragraph 96.

58 Non-Horizontal Merger Guidelines, paragraph 93.

59 Non-Horizontal Merger Guidelines, paragraphs 95 to 104.

60 Non-Horizontal Merger Guidelines, paragraphs 105 to 110.

61 Non-Horizontal Merger Guidelines, paragraphs 111 to 118.

62 TCCC's share NCDS is [10-20]% in the UK and less than [5-10]% in Ireland and Poland.

63 For example, including independents and non-specialist operators would increase the total market size to around 24,061 stores in the UK for 2017 (an increase from around 7,476 of branded coffee shops), resulting in Costa's share of all coffee shops in the UK being approximately [10-20]%.

64 Form CO, paragraphs 130-131.

65 Form CO, paragraph 132.

66 Form CO, paragraph 131.

67 See replies to Q3.1 of the Questionnaire to competitors.

68 See replies to Q28-Q30 of the Questionnaire to competitors and replies to Q23-Q25 of the Questionnaire to competitors.

69 Form CO, paragraph 134-135.

70 Form CO, paragraph 137.

71 In this regard, the Notifying Party submits that in any case the off-premises sales of NABs are almost 10 times as high as all on-premises sales channels together in the UK.

72 See replies to Q28-Q30 of the Questionnaire to competitors and replies to Q23-Q25 of the Questionnaire to competitors.

73 See reply to Request for Information of 27 November 2018.

74 In relation to a possible leveraging from Costa to TCCC, Costa does not seem to have the ability to leverage its position in PtS for lack of market power as illustrated by its low market shares as set out in Table 2.

75 In relation to a possible leveraging from Costa to TCCC, Costa does not seem to have the ability to leverage its position in R&G and Tassimo discs for lack of market power as illustrated by its low market shares as set out in Table 2.

76 In relation to a possible leveraging from Costa to TCCC, Costa does not seem to have the ability to leverage its position in vending services (Costa Express) for lack of market power as illustrated by its low market shares as set out in Table 2.

77 Form CO, paragraph 140.

78 Form CO, paragraph 140.

79 Form CO, paragraph 140(c).

80 Form CO, paragraph 142.

81 Form CO, paragraph 143.

82 See replies to Q23 of the Questionnaire to customers.

83 See replies to Q23.1 of the Questionnaire to customers.

84 See replies to Q29 of the Questionnaire to customers.

85 See replies to Q29.2 of the Questionnaire to customers.

86 See replies to Q28-Q30 of the Questionnaire to customers.

87 Form CO, paragraph 144 (c).

88 Form CO, paragraph 144 (a).

89 Form CO, paragraph 144(b).

90 Form CO, paragraph 145(a).

91 Form CO, paragraph 146.

92 See replies to Q23 of the Questionnaire to customers.

93 See replies to Q30 of the Questionnaire to customers.

94 See replies to Q29 of the Questionnaire to customers.

95 See replies to Q29.2 of the Questionnaire to customers.

96 See replies to Q28-Q30 of the Questionnaire to customers.

97 See response to Request for Information of 23 November 2018, paragraph 3.

98 See response to Request for Information of 23 November 2018, paragraph 2.

99 See response to Request for Information of 23 November 2018, paragraph 5.

100 See response to Request for Information of 23 November 2018, paragraph 3(b).

101 See response to Request for Information of 27 November 2018.

102 Form CO, paragraph 120.

103 See replies to Q28-Q30 of the Questionnaire to customers.