Commission, August 16, 2017, No M.8468

EUROPEAN COMMISSION

Judgment

NORGESGRUPPEN / AXFOOD / EUROCASH

Subject: Case M.8468 - Norgesgruppen/Axfood/Eurocash

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 10 July 2017, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which the undertakings NorgesGruppen ASA ('NorgesGruppen', Norway) and Axfood AB ('Axfood', Sweden) acquire within the meaning of Article 3(1)(b) of the Merger Regulation joint control of the undertaking Eurocash Food AB ('Eurocash', Sweden) by way of purchase of shares ('the Transaction'). NorgesGruppen and Axfood are collectively referred to as 'the Parties'.

1. THE PARTIES

(2) NorgesGruppen is a food retailer active in food procurement, wholesale and retail distribution in Norway. (3) NorgesGruppen is the largest grocery retailer in Norway and operates both through wholly-owned stores and through agreements with store owners (franchise). A total of 1,850 grocery stores are run in Norway under one of NorgesGruppen's brand profiles (Spar, Meny, Joker, Kiwi and Naerbutikken).

(3) Axfood is a food retailer active in food procurement, wholesale and retail distribution in Sweden. Axfood is the third largest grocery retailer in Sweden. The retail business is conducted through the wholly owned store chains Willys and Hemköp, comprising 263 stores.

(4) Eurocash is active in retail distribution in 8 supermarkets located in Sweden at a short distance from the Norwegian border which are primarily aimed at Norwegian consumers crossing the border to buy cheaper daily consumer goods. Eurocash has a turnover of EUR 128 million. 100 per cent of the shares in Eurocash are owned by the holding company NAX.

2. THE CONCENTRATION

(5) On 18 January 2017, NorgesGruppen and Axfood signed two share and purchase agreements and one shareholding agreement that will affect the structure of ownership and control over NAX and consequently Eurocash. After the completion of the concentration Axfood and NorgesGruppen will hold 51% and 49% of the shares in NAX respectively. Pursuant to the shareholders’ agreement, each of the Parties shall appoint two board members and one deputy board member. Under Section 8.3 of the Shareholders Agreement, several Board decisions require unanimity among the board members appointed by the Parties, including strategic issues such as decisions on or amendments to business plans, yearly budget and the company's overall strategy.

(6) As a consequence of the Transaction, NAX and Eurocash will be jointly controlled by NorgesGruppen and Axfood. The Transaction constitutes therefore a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (4) (NorgesGruppen EUR 9,747 million, Axfood EUR 4,410 million, Eurocash EUR 128 million). Two of them have an EU-wide turnover in excess of EUR 250 million (NorgesGruppen EUR 1,233 million, Axfood EUR 4,410 million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. APPLICATION OF THE EEA AGREEMENT

(8) The concentration concerns the distribution of daily consumer goods mainly to Norwegian consumers. Competence of the Commission as regards Norway is defined in the EEA agreement. Article 8(3)(a) of the EEA Agreement states that products falling within Chapters 1 to 24 of the Harmonised Commodity Description and Coding System ("Combined Nomenclature") are not covered by the EEA Agreement, unless such products are listed in Protocol 3 of the said Agreement. Products listed in Chapter 1 to 24 that are not covered by the EEA agreement include in particular meat, fish and seafood, milk and dairy products, eggs, fruit and vegetables, coffee and tea, flour and pastry sugar and cocoa, edible oils, beverages, alcohol and tobacco. Some food products are listed in Protocol 3 and fall therefore within the scope of the EEA agreement such as inter alia sugar and confectionary, pasta, ice cream and mineral water.

(9) Products in the 'non-food' category are included in chapter 25 – 97 of the Nomenclature, and thus fall within the scope of the EEA Agreement and the Commission's jurisdiction. This includes in particular clothes, tableware, electric equipment and batteries, office accessories, domestic appliances, paper and plastic foils, textiles, cleaning products, papers, magazines and books, audio-visual equipment, child care and toys hygiene and sanitary products.

(10) The concentration thus affects distribution of consumer goods which are within and or outside the scope of the EEA agreement. In cases involving both products falling within and outside the scope of the EEA-agreement, the proper functioning of the EEA mergers rules requires that the entire transaction has to be notified to the competition authority competent to deal with the case under EEA Agreement, namely in the present case to the Commission. (5) Whether the transaction has to be notified to national authorities in the EFTA states depends on national notification rules. (6)

(11) In terms of the substantive analysis to be carried out, the Commission will assess the merger in relation to Norway, with regard to all products falling within the scope of the EEA-agreement. (7) However, in the definition of the relevant markets and their assessment, the Commission applies the established approaches and rules as set out in its guidelines.

5. COMPETITIVE ASSESSMENT

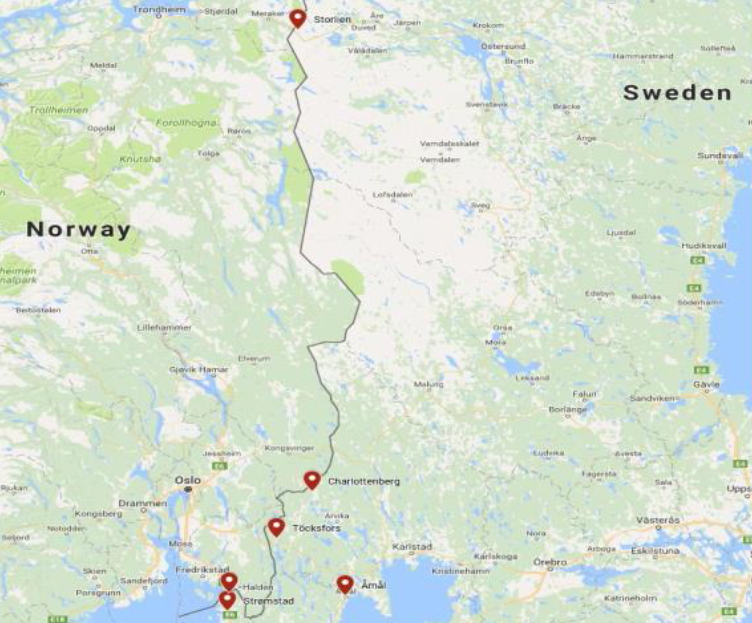

(12) The target business consists of 8 supermarkets located in the Swedish municipalities of Svinesund (one store), Strömstad (two stores), Töcksfors (two stores), Charlottenberg (one store), Storlien (one store) and Åmål (one store). These stores are located in close proximity to the Norwegian border and the vast majority of their customers (between 67% and 95%) are Norwegian – the only exception being the supermarket in Åmål, which is located more than 80 km from the border and whose customer base is predominantly Swedish.

(13) Like other Swedish supermarkets close to the Norwegian border, the business of Eurocash is principally aimed at Norwegian consumers who cross the border from Norway to buy cheaper Swedish groceries, alcohol and tobacco. The product assortment and marketing of Eurocash is primarily aimed at Norwegian consumers, who are also responsible for the major part of the stores’ turnover. The map below shows the location of the Eurocash stores in the border region between Norway and Sweden.

(14) Prior to the acquisition of Eurocash, Axfood had a very limited market presence at the retail level in the municipalities where Eurocash operates and it has no presence in Norway or Denmark. Similarly, NorgesGruppen is not active in Sweden. The only potential overlap between the Parties' and Eurocash activities relate to retail distribution to Norwegian consumers and procurement of daily consumer goods in Norway, where NorgesGruppen and Eurocash are both active.

5.1. Market definition

5.1.1. Product market

5.1.1.1. Retail distribution of daily consumer goods

(15) Cross border shopping in retail distribution is a phenomenon which occurs particularly between countries where there are differences in prices or in range of products. In the case of Norway and Sweden, differences in agricultural policy, custom barriers, cost level and exchange rates contribute to making cross border trade attractive. Price differences between Norway and the other Nordic countries are significant, with Norway being markedly more expensive than its neighbours. Food products and non-alcoholic beverages are in general 22.5 % cheaper in Sweden than in Norway. (8) For milk, cheese and eggs the price level in Sweden is 45-50% lower and for meat 25-30% lower. (9) Alcohol and tobacco are 57% less expensive in Sweden than in Norway. (10)

(16) Cross-border shopping between Sweden and Norway is particularly relevant because of the long common border and the fact that a large part of the Norwegian population lives close to this border. In 2015 Norwegians spent approximately EUR 1,430 million on cross border shopping on day trips to Sweden (which includes more than only grocery shopping). (11) The total sales of groceries sales in the Swedish border municipalities are estimated to be approximately EUR 1,206 million, which represents approximately 6 per cent of Norwegians' total grocery spend. (12) The vast majority of the consumers who cross the border to shop reside in the south-eastern part of Norway (including the Oslo area) and the average travel distance for those cross-border trips is 83.4 km. (13)

(17) The Commission has in previous cases considered that there is a distinct relevant product market for the retail sale of daily consumer goods mainly carried out by retail outlets such as supermarkets, hypermarkets and discount chains. (14) The Norwegian Competition Authority has taken the same approach in a recent case. (15) However, neither the Commission nor national competition authorities have previously assessed a merger where cross border shopping is as significant as at the border between Norway and Sweden.

(18) The Parties take the view that for Norwegian consumers cross-border shopping in Sweden does not belong to the same antitrust market as regular shopping in Norway. On the demand side, cross-border shopping has a lower frequency. Furthermore, the average shopping basket is larger and includes a more significant share of alcohol and tobacco. On the supply side, retailers in border areas mainly set their prices based on competition locally from competing Swedish grocery chains and conversely Norwegian retailers do not take into account Swedish border shops when setting their prices and marketing policies.

(19) Respondents to the market investigation have not confirmed that cross-border shopping is not in competition with traditional grocery shopping. These respondents indicated that Norwegians tend to shop for everyday consumption in Sweden, although probably in greater proportions to benefit from lower prices. (16) Frequency of shopping trips goes from once a month to once a week for consumers depending on the distance to be travelled to the border. (17)

(20) On the supply side, the border grocery stores in Sweden advertise through Norwegian newspapers and media (including social media) to attract consumers. The advertisement is directed towards consumers living close to the border, but also further away from the border regions such as in the Oslo area. In addition, Norwegian national newspapers do general surveys on the price level in the Swedish border grocery stores up against Norwegian grocery stores. Consequently, Norwegian grocery stores tend to take cross-border competition into account when setting prices and developing marketing policies. (18)

(21) Consequently the Commission takes the view that regular trips to shop in Sweden may substitute to some extent daily shopping in Norway for Norwegian consumers living relatively close to the border (see below for a discussion of the relevant geographic market) and that for these customers border shops in Sweden constitute alternatives from Norwegian stores. The issue can however be left open since the Transaction does not lead to serious doubts as to its compatibility with the internal market and the EEA Agreement even if shopping in border stores in Sweden by Norwegians is deemed to fall into the same relevant product market as shopping in Norwegian retail stores.

5.1.1.2. Procurement of daily consumer goods

(22) In its previous practice, the Commission considered a distinct market for the procurement of daily consumer goods by retailers and wholesalers from producers and upstream suppliers.

(23) The Commission – although it has ultimately left the exact product market definition open in its previous cases – has considered that the procurement market for daily consumer goods should be defined with reference to different product groups given the limited supply-side substitutability. (19) The Parties agree with this approach.

5.1.2. Geographic market

5.1.2.1. Retail distribution of daily consumer goods

(24) The Commission has in its practice delineated the geographic market for retail sale of daily consumer goods, according to demand side considerations, by the boundaries of a territory where the outlets can be reached easily by consumers (radius of approximately 20 to 30 minutes driving time). (20) The Commission has stressed that the delineation of each local area should be undertaken on a case by case basis by taking into account specific local circumstances. In the Coop/ICA decision, the Norwegian Competition Authority defined a radius of 10 to 20 minutes driving time but stressed that the precise delimitation of the local markets would vary in each area based on local factors such as topography, demography and the stores' relative location.

(25) With respect to cross-border trade , the average travel distance for the cross-border shopping trips is 83.4 km, meaning that a proportion of the customers travel even further (up to 120 km) and this has been confirmed by respondents to the market investigation. (21) It appears therefore fair to assume that in relation to cross-border shopping, a driving time of maximum 30 minutes is a less suitable parameter to assess competition for Norwegian consumers.

(26) Assuming a maximum distance of 120 km, the catchment area for the Eurocash stores in the south of Sweden (Svinesund, Strömstad, Töcksfors and Charlottenberg) includes Norwegian consumers residing in South Eastern Norway, i.e. in the regions Oslo, Ostfold and Akershus and the southern parts of Hedmark and Oppland, as well as parts of Vestfold, Telemark and Buskerud. A similar assumption can be made for the catchment area for the Eurocash store in Storlien which includes Norwegian customers residing in the Trøndelag region, including northern parts of Hedmark and Oppland, as a proxy. NorgesGruppen is also present in these regions with its network of stores. The activities of the Parties therefore overlap in large stretches of the Norwegian territory.

(27) Respondents to the market investigation have confirmed that due to their attractiveness to Norwegian consumers living up to 120 km from the border, the catchment areas of Eurocash stores cover the Norwegian regions mentioned above. For the purpose of this decision, the Commission will therefore assess the impact of the Transaction in retail distribution of daily consumer goods in all these regions. (22)

5.1.2.2. Procurement of daily consumer goods

(28) The Commission has previously considered the scope of the procurement market as national (23) and the Parties agree with this approach.

5.2. Assessment (24)

5.2.1. Retail distribution of daily consumer goods

(29) If, in line with the Parties ‘arguments, for Norwegian consumers cross-border shopping in Sweden does not belong to the same relevant product market as regular shopping in Norway, there is no overlap between Norgesgruppen and Eurocash’activities.

(30) If on the contrary for some consumers located in Norway cross-border shopping and regular grocery shopping constitute alternatives, they may choose between shopping for these products in Norway or take a special longer trip to one of the grocery stores in Sweden close to the border aimed at Norwegian clients, there is an overlap between Norgesgruppen and Eurocash for these consumers. The question here is to determine whether these border stores exert on Norgesgruppen’s stores a competitive constraint on Norgesgruppen’stores – and if the elimination of this constraint would have a detrimental effect on competition, in the absence of relevant alternatives.

(31) The Parties have therefore identified all 622 NorgesGruppen stores which are within 120 km (the assumed maximum travel distance) from any of the eight Eurocash stores. The Parties subsequently provided market shares for retail distribution in the 622 catchment areas around each store and took into account the sales made by the Eurocash stores within 120 km from them. (25)

(32) The results of this analysis show that 595 out of these 622 catchment areas will be horizontally affected as a result of the Transaction, with combined market shares ranging from 20.4% to 78.6%. In 535 of these catchment areas, the combined share is above 40% and in 185 of these catchment areas, the combined share is above 50%.

(33) However, in each of these 595 catchment areas, the increment would be less than 3.5% and in all the catchment areas where the combined share is more than 40%, the increment is systematically below 3%. The competitive constraint exerted by Eurocash stores or Norgesgruppen’s supermarkets appear therefore relatively limited with modest overlaps brought by the border stores

(34) It appears moreover that in three of the four Swedish towns where Eurocash stores are located, other retail stores targeting mainly Norwegian consumers are active and could therefore provide a suitable alternative for these consumers, reflecting the dynamic character of these cross-border markets.

(35) In Svinesund-Strömstad (three Eurocash stores), there are 96 catchment areas where the combined share is above 40% but three other stores are active in this border region. These three stores belong to Coop Sweden and two of them achieve a turnover which is three times higher than the Eurocash stores together. These border stores will continue to exert on Norgesgruppen a competitive constraint post- transaction.

(36) In Töcksfors (two Eurocash stores), there are 381 catchment areas where the combined share is above 40% but two other stores are present in this border region and one more has been opened by Swedish retailer ICA in 2017. These two stores belong to Swedish retailers Coop Sweden and Bergendahl and one of them achieve a turnover which is higher than the Eurocash stores together. These border stores will continue to exert on Norgesgruppen a competitive constraint post-transaction.

(37) In Charlottenberg (one Eurocash store), there are 56 catchment areas where the combined share is above 40% but three larger supermarkets directly targeting Norwegian consumers are also present. These supermarkets also belong to Bergendahl and Coop Sweden and they achieve higher turnover than the Eurocash stores. These border stores will continue to exert on Norgesgruppen a competitive constraint post-transaction

(38) In the region of Storlien however, Norwegian consumers have only one cross-border alternative, which is an ICA store. The potential customers of Eurocash Storlien, from the Norwegian side of the border, are most likely to come from the regions of Nord- or Sør-Trøndelag. However, NorgesGruppen's presence is more limited in these areas as their rivals Coop and Rema 1000 traditionally have a stronger market presence in Nord- and Sør-Trøndelag. In none of the catchment areas around Storlien the combined entity has a share of more than 25%. The only exception relates to consumers located in the Norwegian city of Selbu, which is located at a 109 km of Storlien, and where the combined entity would hold a share of [60-70]%, albeit with a limited overlap of [0-5]%.

(39) In the light of the above, the Transaction does not raise serious doubts as regards its compatibility with the internal market and the EEA Agreement with respect to its impact on competition on the market for retail distribution of daily consumer goods.

5.2.2. Procurement of daily consumer goods

(40) Some respondents to the market investigation have expressed concerns regarding the impact of the Transaction on the procurement market of daily consumer goods in Norway.

(41) In particular, these respondents submitted that Norgesgruppen is by far the leader in the Norwegian procurement market. In addition to holding an overall 42.3 % market share in the Norwegian procurement market, Norgesgruppen is also a significant player as a wholesaler and within the hotel, restaurant and catering market through its subsidiary ASKO Norge AS according to the respondents.

(42) Further, the respondents report that Norgesgruppen has signed in 2016 a purchasing collaboration with Bunnpris, a small Norwegian retail chain. Through the joint purchasing cooperation, NorgesGruppen conducts the negotiations with suppliers on behalf of both parties for the product groups covered by the agreement. (26) As a result, the respondents submit, Norgesgruppen would hold a market share of more than 50% in the procurement market in Norway.

(43) According to these respondents, holding a strong position in the upstream market could potentially result in raising barriers for Norgesgruppen’s competitors to get access to the products and develop effective relations with the suppliers. Being the gateway to the Norwegian grocery market, Norgesgruppen would be likely the first mover in negotiations with central suppliers and would be able to dictate terms for competitors' relations to the suppliers. The respondents submit that the acquisition of Eurocash would further strengthen its already significant purchasing power in Norway which would in turn reinforce its position in the downstream markets because of increased barriers to entry and expansion for its competitors. (27)

(44) The Commission has assessed Norgesgruppen's market position in the procurement markets in Norway. Depending on the product groups, Norgesgruppen holds a market share in the procurement market between 45 and 50% (except for home products at [30-40]%). Coop Norway holds shares between 24 and 30% (except home products 38%) and Rema holds shares between 23 and 28%.

(45) It appears therefore that the procurement market in Norway has an oligopolistic structure, with only three major players and Norgesgruppen being the clear leader. The impact of this concentrated market structure on the possibilities of entry and expansion by retail rivals is uncertain but the Commission notes that German retailer Lidl withdrew from the Norwegian market in 2007 (it is still present in Sweden and Denmark) after only three years of operation and that Swedish retailer ICA has sold its Norwegian operations to Coop Norway in 2015. (28) The Norwegian retail market is therefore characterized by a recent history of exits and withdrawals having led to the current concentrated market structure.

(46) However, the Commission does not consider that the current merger will have an impact on Norgesgruppen's market position in the procurement market for daily consumer goods in Norway for the following reasons.

(47) First, the procurement of Eurocash (roughly EUR 88 million) represents much less than 1 per cent of the total procurement in the Norwegian retail market (EUR 18 billion). Even if one presumes that NorgesGruppen will negotiate on behalf of Eurocash and that NorgesGruppen can leverage all of Eurocash' volume in the negotiations with suppliers in Norway, it is unlikely that the incremental increase will have any negative effects on Norwegian suppliers or competing grocery chains.

(48) Second, [40-50]% of the products sold in Eurocash are supplied by Axfood. It is not likely that Axfood would accept that NorgesGruppen should act as wholesaler instead of them for the whole range of products supplied by Axfood, given that Axfoods will hold 51% of Eurocash and joint control in relation to the day-to-day management of Eurocash's operations.

(49) Third, among the products which are not supplied by Axfood, most of them are procured from Sweden and there are a limited number of Norwegian brands and products which are sourced from Norway. For example, meat produce are mainly bought from local producers and international suppliers. None of the meat products sold in Eurocash derive from Norway, due to the differences in custom barriers and production costs.

(50) In the light of the above, the Transaction does not raise serious doubts as regards its compatibility with the internal market and the EEA Agreement with respect to its impact on competition on the market for procurement of daily consumer goods in Norway.

6. CONCLUSION

(51) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 In addition to its grocery retail business in Norway, NorgesGruppen has joint control over the Danish grocery retail chain Dagrofa.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 See, by analogy, the Judgment of the EFTA Court in case E-1/16, Synnove Finden, at para 63.

6 In this case, under the Norwegian merger rules, the Parties have no obligation to notify in Norway because only one undertaking has a turnover exceeding NOK 100 million.

7 See cases M.2337 Nestlé/Ralston Purina, M. 2544 Masterfoods/Royal Canin, M.6753 Orkla/Rieber & Son.

8 Eurostat: Price level index for food and non-alcoholic beverages 2015.

9 See officials Norwegian statistics at https://www.ssb no/priser-og-prisindekser/artikler-og- publikasjoner/norge-har-europas-hoeyeste-matvarepriser.

10 Eurostat: Price level index for food and non-alcoholic beverages 2015.

11 See official Norwegian statistics at https://www.sb.no/en/varehandel-og tjenesteyting/statistikker/grensehandel.

12 Dagligvarerapporten 2016 (The Daily Consumer Goods Report 2016), power-point presentation, slide 5.

13 NILF-memorandum 2012-17 Grensehandel – utvikling, årsaker og virkning (Border trade – developments, causes and effects) available here:http://nilfno/publikasjoner/Notater/2012/grensehandelutvikling_arsaker_og_virkning.

14 Decisions in cases IV/M.1221 REWE/Meinl of 3 February 1999, IV/M.1684 Carrefour/Promodes of 25 January 2000 and COMP/M.4590 Rewe/Delvita of 25 April 2007.

15 Decision V2015/4 Coop/ICA of 4 March 2015.

16 Reply to Q5 of questionnaires to competitors.

17 Reply to Q4 of questionnaires to competitors.

18 Reply to Q9 of questionnaires to competitors.

19 Decision in COMP/M.4590 Rewe/Delvita.

20 Decision in case COMP/M.7702 Koninklijke Ahold/Delhaize Group of 22 October 2015.

21 Reply to Q11 of questionnaires to competitors.

22 Reply to Q11 of questionnaires to competitors.

23 Decision in case IV/M.1684 Carrefour/Promodes.

24 The competitive assessment in this section is conducted in line with what is described in paragraph (11) above. Therefore, the Commission is not limited in its determination of the relevant markets and their assessment by the scope of application of the EEA Agreement.

25 The Parties have calculated these shares with two major alternative methodologies: In the first analysis, they have assumed that customers living in Norwegian provinces which are "far" from the Swedish border (for example in Oslo) spend the same amount per annum as those living closer to the border. The second analysis weighs the turnover of Eurocash stores in a given Norwegian province by the distance of this province from the border. There are no major differences between the final results of these two alternative methodologies.

26 Through the agreement, Bunnpris also has access to NorgesGruppens portfolio of private label brands.

27 No specific comments were voiced in relation to the combination of the procurement activities of Eurocash and Axfood in Sweden (Eurocash already sources 45% of its needs from Dagab, which is a subsidiary of Axfood).

28 As the merger led to lessening of competition in some catchment areas, Coop had to divest 93 of ICA's stores. 43 of these store were sold to Bunnpris and 50 to Norgesgruppen. See http://www.konkurransetilsynet no/en/news/news-archive/20152/coops-acquisition-of-ica-norge-cleared- with-remedies/.