Commission, September 29, 2017, No M.8481

EUROPEAN COMMISSION

Judgment

ABP FOOD GROUP / FANE VALLEY / LINDEN FOODS

Subject: Case M.8481 – ABP FOOD GROUP / FANE VALLEY / LINDEN FOODS

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 25 August 2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which ABP Food Group ("ABP", Ireland) acquires within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation joint control together with Fane Valley Co-Operative Society Limited ("Fane Valley", UK) of the whole of Linden Foods Limited ("Linden", UK), by way of purchase of shares ("the Transaction"). (3) ABP and Fane Valley are designated hereinafter as "the Notifying Parties" and, together with Linden, "the Parties".

1. THE PARTIES

(2) ABP is a privately owned agribusiness company headquartered in Ireland. ABP is active in the slaughtering of cattle and ovine animals (lamb and sheep), the processing of their meat and the collection and processing of associated animal by-products. ABP has 37 plants in total, located in Ireland, UK, Denmark, Poland, Austria, the Netherlands, France, and Spain. It also jointly controls together with Fane Valley the Slaney JV, based in Ireland. (4) In the island of Ireland ("IoI", comprising Ireland and Northern Ireland ("NI")) and in the UK, beyond its interests in the Slaney JV, ABP has 10 plants in England, 1 plant in Scotland and 2 plants in NI.

(3) Fane Valley is a farmer owned cooperative society headquartered in NI, UK. Through its interests in Linden and the Slaney JV, Fane Valley is active in the slaughtering of cattle and ovine animals, the processing of their meat and the collection and processing of animal by-products both in Ireland and the UK. (5) Fane Valley has also non-controlling minority shareholdings (directly and indirectly through Linden) in Linergy, a company based in NI, active in rendering of animal by-products and renewable energy. Fane Valley is also active in the production of breakfast cereals, edible offal and edible fat/protein, and operates retail shops and warehouses.

(4) Linden is currently solely controlled by Fane Valley, and is active in the slaughtering and processing of beef and ovine animals. It has 3 plants in the UK, two in NI (in Dungannon and in Lisnaskea) and one in Great Britain ("GB"), UK. Whilst Linden slaughters and further processes cattle, lamb and sheep at its plant in Dungannon, it does not slaughter these animals at the Lisnaskea plant (it only is engaged in further processing at that plant).

2. THE OPERATION

(5) As part of ABP’s acquisition of a 50% interest in the Slaney JV in 2016, ABP acquired a non-controlling […] interest in Linden. (6) The remaining […] of Linden is currently owned by Fane Valley, which solely controls Linden.

(6) The Transaction involves the purchase by ABP of an additional […] interest in Linden from Fane Valley, resulting in Linden being jointly controlled by ABP and Fane Valley. Each of ABP and Fane Valley will have a 50% interest in Linden and will have a blocking right concerning strategic decisions in relation to it.

(7) The joint venture will therefore result in a change from sole to joint control over Linden, which is Fane Valley's existing business in relation to the slaughtering of cattle and ovine animals, and the processing of their meat. It currently operates, and will continue to operate post-Transaction, as an autonomous economic entity, active on a trade market. Linden will have management dedicated to its day-to- day operations and access to sufficient resources to conduct its business on a lasting basis.

(8) The Transaction therefore constitutes a concentration under Articles 3(1)(b) and 3(4) of the Merger Regulation.

3. EU DIMENSION

(9) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 2 500 million and a combined aggregate EU-wide turnover of more than EUR 100 million in at least three Member States (Ireland, France, Italy, the Netherlands, and the UK). (7) In each of at least three of those Member States, the aggregate turnover of each of ABP and Fane Valley exceeds EUR 25 million. Overall, the aggregate EU-wide turnover of each of ABP and Fane Valley exceeds EUR 100 million, but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(10) The notified operation therefore has an EU dimension according to Article 1(3) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Introduction

4.1.1. Overlaps of the Parties and affected markets

(11) The Transaction gives rise to horizontally affected markets in relation to the purchase of live cattle and ovine animals for slaughter, and the markets for the supply of fresh beef and processed meat to certain retailers.

(12) In addition, the Transaction gives rise to vertically affected markets in relation to the collection and processing of animal by-products.

4.1.2. The Commission's investigation

(13) During pre-notification as well as in the context of the market investigation, the Commission reached out to suppliers of live animals (i.e. farmers and industry associations), competing slaughterhouses, industrial processors, renderers of animal by-products, and retailers. In total, about 200 questionnaires have been sent out and a number of telephone interviews with market participants conducted.

4.2. Purchase of live cattle for slaughter

4.2.1. Product market definition

(14) Cattle could be differentiated either by type or breed. As regards types of cattle, cows, heifers, steers, bulls, and calves can be distinguished. Cows are mature female bovines that have given birth to a calf. A heifer is a female bovine that has not yet had a calf or developed the mature characteristics of a cow. A steer is a male bovine that has been castrated. A bull is a male bovine used for breeding purposes. A calf is a male or female bovine animal under 12 months. (8)

(15) Various cattle breeds and breed variants exist. The most well known include Angus and Hereford in Ireland and Shorthorn and Dexter in the UK. (9)

(16) In the past, the Commission considered (on the basis of the absence of supply- side substitutability) the market for the purchase of live cattle for slaughter as constituting a separate market from the purchase of other live animals for slaughter and from the purchase of live calves for slaughter, without considering further segmentations by type or by characteristics of cattle or by breed. (10)

(17) In a recent decision, the Commission found strong support for a delineation of the market comprising all types and breeds of cattle, in line with past precedents. (11)

(18) The Notifying Parties submit that the relevant product market is the market for the purchase of live cattle for slaughter and that this includes all types of cattle (cows, steers, heifers and young bulls) and breeds of cattle (e.g. Angus, Hereford, etc.). The Notifying Parties also submit that a segmentation of the market into calves and other cattle is not warranted as calves represent less than 3% of all cattle purchased for slaughter in each of NI and GB.

(19) From the supply-side perspective, the vast majority of farmers and associations responding to the market investigation explained that there are no substantial differences in breeding, raising, and finishing of different types of cattle or breed. (12)

(20) In relation to the type of breed, the majority of farmers represented in the investigation explain that it would take time and/or it would be costly for farmers to switch production from one breed of cattle to another and many specify that this would be difficult in particular situations, e.g. if changes in breed specifications are requested by slaughterhouses with short notice or if the demand of a new breed increases by a large scale in a relatively short timeframe. (13) On the other hand, the vast majority of farmers represented in the investigation explain that in general farmers breed and rear several different breeds of cattle rather than specialising. (14) The majority of the responding farmers are also of the opinion that in general, farmers breed and rear all types of cattle. (15) In addition, the vast majority of farmers explain that there are no substantial technical differences in breeding, raising, and finishing of different types or breed of cattle, and thus support the Commission's previous finding that all types and breeds of cattle are comprised within the market for the purchase of live cattle for slaughter. (16)

(21) From the demand-side perspective, nearly all competitors responding to the market investigation explain that there are no substantial differences in the slaughtering or further processing (in terms for instance of special equipment required) of different types of cattle or breed, and thus support the Commission's previous finding that all types and breeds of cattle are comprised within the market for the purchase of live cattle for slaughter. (17)

(22) In light of the above, the Commission considers that for the purpose of this case the market for the purchase of live cattle for slaughter, comprising all types and breeds of cattle, constitutes the relevant product market. (18)

4.2.2. Geographic market definition

(23) In the territory of the IoI, Linden has only one slaughtering plant for bovine animals located in Dungannon, NI. On the IoI, ABP's has eight plants: two are located in NI (in Lurgan and Newry), and six in Ireland.

(24) In the past, the Commission left the potential geographic scope of markets for the purchase of live cattle for slaughter open, assessing the transactions on the basis of different catchment areas around slaughtering plants and the national level. (19)

(25) In a recent case, the Commission assessed the market for purchase of live cattle for slaughter in Ireland and concluded that the market was not wider than national (i.e. Ireland) as live cattle were generally not exported while imports were limited due to veterinary restrictions and labelling requirements. In view of the results of the market investigation in that case the Commission has assessed the transaction applying a 60 miles radius from cattle processing plants in Ireland. (20)

(26) In relation to the merger of two slaughterhouses active in the UK, the UK competition authority has suggested, in a past case, that GB and NI could be distinct markets, as there is limited supply of cattle between the two due to difficulties in transporting live animals over sea. (21)

(27) The Notifying Parties consider that the relevant geographic market is national in scope encompassing the whole UK (i.e. NI and GB). While there are differences in the prices of cattle in NI and GB, the differential is not significant, and prices in NI generally track those in GB. In their view, this reflects the fact that cattle may be transported between NI and GB. In any event, the Notifying Parties explain that if a catchment area of 60 miles is considered in NI, given the limited size of the territory, this supports the view that the market is least NI-wide. This, according to them, is further supported by the homogeneity in prices for live cattle across the NI territory.

(28) Most of slaughterhouses responding to the market investigation believe that the market for purchase of live cattle for slaughter is not wider than national. (22) The main reason why cattle are not transported between Ireland and NI are in general labelling requirements in relation to the origin of the meat and customers' preferences for national meat. (23) In general, also farmers explain that the national origin of the meat is important for customers and thus labelling requirements limit cross-border movement of cattle. (24)

(29) The majority of slaughterhouses and farmers responding to the investigation also confirmed the Commission's precedent that the maximum distance cattle travel is 150-200 miles and that the typical distance cattle travel is up to 60 miles. However, a significant part of respondents also believe that the average distance is actually larger than that. (25) Competitors have also explained during pre- notification calls that there is limited supply of cattle between NI and GB due to the difficulties and costs associated with transporting live animals over sea. (26)

(30) The Commission notes that NI is a relatively small geographic area, measuring about 86 miles by 82 miles. Therefore, when a 60 miles catchment areas is applied to the Parties' NI plants, this results in a number of overlapping catchment areas that comprise the entire territory of NI. The only exception would be the catchment area around ABP's plant in Newry. As regards that catchment area, two plants of competing slaughterhouses (Foyle and WD Meats) which are located in the very northern part of NI would be excluded by just a few miles. However, a delineation of the market on that basis would constitute a rather artificial delineation and would not reflect real market dynamics.

(31) The market investigation did not reveal that cattle movement is restricted within the territory of NI and shows that no differences in prices paid/received for cattle exist in different areas or regions of NI according to slaughterhouses and farmers active in the region, respectively. (27)

(32) In light of the above, the Commission considers that, for the purposes of the assessment of this case, the market for the purchase of live cattle for slaughter comprises the whole territory of NI.

4.3. Purchase of live lambs and live sheep for slaughter

4.3.1. Product market definition

(33) The Commission has assessed the potential market(s) for the purchase of live lambs and/or sheep for slaughter for the first time last year, in relation to case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods.

(34) In that case, the Commission has left open whether either the purchase of live lambs and/or live sheep for slaughter constitute separate product markets, and whether there is an overall market for the purchase of live lambs and sheep. (28)

(35) The results of the market investigation confirm the findings of case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods that slaughterhouses are able to process and market all different types of sheep and lambs without significantly need to adjust their assets or incurring in significant time delays. (29)

(36) In any event, given the fact that the Transaction does not raise serious doubts under any plausible market definition, for the purpose of this case, the product market definition can be left open.

4.3.2. Geographic market definition

(37) The Commission has considered in a recent previous decision that the geographic scope of the market(s) for the purchase of live lamb and/or lamb for slaughter is the IoI. (30)

(38) The Notifying Parties agree with these recent findings as prices for lambs and sheep on both sides of the Irish border are very similar while there is considerable movement of live ovine animals between Ireland and NI. While the same origin labelling requirements apply to lamb and sheep as for cattle, they do not restrict the cross-border movement of ovine animals as there is little preference for Irish or British lamb or sheep for downstream customers.

(39) The market investigation largely confirmed the Commission's precedent. Most slaughterhouses explained that ovine animals do travel across the Irish border and that prices are very similar between Ireland and NI. (31) Moreover, slaughterhouses confirmed that cross-border trade of sheep and lamb is more common than for cattle due to "less stringent customer demand on country of origin." (32)

(40) In light of the above, the Commission considers that, for the purposes of the assessment of this case, the market(s) for the purchase of live lamb and/or sheep for slaughter is the IoI.

4.4. Sale of fresh beef meat

4.4.1. Product market definition

(41) In the past, the Commission has concluded that fresh meat includes both fresh and frozen meat (including minced meat) which is not further processed in any way, i.e. no other ingredients or spices have been added, nor has the meat been cooked, smoked or dried. (33) The Commission has, in previous decisions, defined separate product markets for the sale of various types (pork, veal, etc.) of fresh meat, including fresh beef. (34)

(42) The Commission has previously assessed the market for the sale of fresh beef meat on the basis of the following segmentation by distribution channel: (i) sales to retailers, further divided into sales to (a) supermarkets and (b) butchers; (ii) sales to caterers (such as restaurants, government institutions, and ship and airport handlers); and (iii) sales of fresh beef to industrial processors (such as producers of sausages, hamburgers and canned food). (35)

(43) In case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods the Commission has also found that while the results of the market investigation have provided certain indications that characteristics such as country of origin, certain breeds, types of the animal and premiumising techniques are of importance for the sale of fresh beef meat, these indications alone do not appear to be sufficiently strong to warrant further sub-segmentation of the fresh beef meat markets on that basis. (36)

(44) The Notifying Parties agree with the assessment in the above Commission's decisions.

(45) The results of the market investigation largely confirmed the previous findings of the Commission. In particular, the respondents to the market investigation confirmed that the market for fresh meat includes meat that has not undergone further processing and that a separate market for the sale of fresh beef exists. (37) Retailers and meat processors responding to the investigation also confirmed that a segmentation based on the distribution channel appears appropriate. (38) Finally, characteristics such as country of origin or the breed are of importance for the sale of fresh beef meat, but there are not sufficiently strong indications that these would need to be considered separate product markets. In particular, most of slaughterhouses and retailers explain that despite customers' tendency to prefer national beef, fresh beef of British origin competes with beef of other countries, and in particular with Irish beef. (39) Other elements (such as the breed) contribute to the overall quality of the meat, which would affect the price of the meat, suggesting that different quality breeds compete with each other. (40)

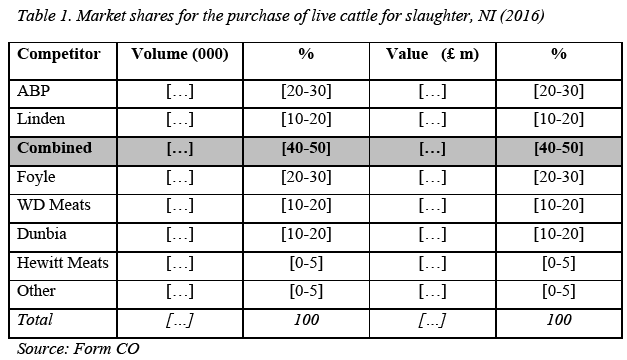

(46) In light of the above, the Commission considers that for the purpose of this case, the product markets that are relevant for the assessment of the transaction consist of the (distinct) markets for the sale of fresh beef to i) supermarkets; ii) industrial processors; iii) caterers; iv) butchers.

4.4.2. Geographic market definition

(47) In the past, the Commission has left open whether the markets for the sale of fresh beef to supermarkets, butchers, caterers, and industrial processors are national or wider (cross-border regional or EEA) in scope. (41)

(48) The majority of slaughterhouses responding to the questionnaire explain that the market is at least national in scope and that in general there are no barriers to export fresh beef to other EEA countries. (42) Retailers mostly believe that the market for the sale of fresh beef is either national or regional (comprising both the territory of the UK and Ireland) in scope. (43)

(49) Based on the results of the market investigation, the Commission considers that the exact geographic market definition of the relevant markets for sale of fresh beef to each of supermarkets, butchers, caterers, and industrial processors can be left open (national, cross-border regional, or EEA-wide) since the Transaction does not raise competition concerns under any possible geographic delineation of the relevant markets.

4.5. Sale of processed meat

4.5.1. Product market definition

(50) The Commission has in previous cases defined a market for processed meat products, which is separate from the markets for sale of fresh meat. Processed meat products have been defined as pork, beef or poultry meat containing external ingredients such as salt or spices, being raw, dried smoked or cooked. Processed meat products include a wide range of different products that differ in terms of the raw material used (i.e. pork, beef, poultry), ingredients used (spices, water content), heat treatment (smoked or boiled), portion, packaging and temperature (chilled or canned). (44)

(51) The Commission has distinguished between (i) processed pork products, (ii) processed beef products, and iii) processed poultry products. Moreover it has grouped processed meat into the following categories and has distinguished according to sales channel (i.e. retail and catering), although the exact scope of the market has been left open: i) raw cured products, ii) processed meat for cold consumption (cold cuts or charcuterie), iii) canned meat; iv) cooked sausages; v) pâtés and pies, vi) ready-prepared dishes and components for these (i.e. convenience products). In addition raw cured pork could be divided into bacon and raw sausages. (45)

(52) Based on the above distinctions, the Transaction would give rise to an affected market for convenience products. However, it appears that the overlap would affect only two segments of such market: processed beef burgers and processed meat balls sold to retailers. The competitive assessment in this decision will therefore focus on these two segments as the narrowest-possible relevant product markets.

4.5.2. Geographic market definition

(53) In terms of the geographic scope of the market for processed meat products the Commission has previously considered national as well as wider than national delineation of the market and its potential segments, ultimately leaving the exact geographic market definition open. (46)

(54) For purpose of this decision, the exact geographic market definition (national or wider than national) can be left open since the Transaction does not raise competition concerns under any possible geographic delineation of the relevant markets.

4.6. Animal by-products

4.6.1. Product market definition

(55) The Commission has considered in previous cases that animal by-products can be differentiated based on their risk category. (47) Category 1 by-products are high risk materials that are not fit for human consumption. Category 2 material consists of fallen animals died of natural causes. In Ireland as well as the UK, no dedicated category 2 treatment plants exists and all category 2 material is treated as category 1 material. Category 3 products are not intended but fit for human consumption; these are typically used for other purposes like pet food and should be considered separately.

(56) The Parties claim that separate markets exist for the collection and processing of category 1 and 2 products on the one hand and category 3 products on the other hand.

(57) The results of the market investigation confirm the previous finding of the Commission that animal by-products have to be treated differently, depending on their risk category. (48) In addition, the market investigation showed that farmers and slaughterhouses typically pay for the disposal of category 1 and 2 materials while they can sell category 3 material for further processing. (49)

(58) In light of the above, and for the purpose of this decision, the Commission distinguishes between separate product markets comprising on the one hand the collection and processing of category 1 and 2 animal by-products and on the other hand the collection and processing of category 3 animal by-products.

4.6.2. Geographic market definition

(59) In previous decisions, the Commission left the precise geographic scope of the markets for the collection and processing of animal by-products open but found indications that the market for high risk material (category 1 and 2) are likely to be national in scope. (50)

(60) In a previous decision, the UK Competition and Markets Authority ("CMA") found that the geographic market for the collection and processing of category 3 material is wider than NI and includes Ireland and Scotland. (51)

(61) The Parties claim that the relevant market for all animal by-products is at least the IoI but would most likely also include Scotland and other parts of the UK because material travels across borders and the Irish Sea.

(62) The results of the market investigation show that rendering facilities receive category 1 and 3 material from NI and Ireland, regardless of their specific position on the IoI. Category 2 material which consists mainly of fallen stock (i.e. animals died of natural causes) provided by farmers seems to be rather restricted to national borders due to veterinary requirements.- (52)

(63) As regards typical travel distance for animal by-products, the market investigation revealed estimates between 100 and 200 miles but also showed that maximum travel distances are significantly larger. (53) The majority of slaughterhouses also explain that no restrictions exist to exporting animal by-products cross border from NI to Ireland or vice versa.

(64) In light of the above, and for the purpose of this decision, the Commission considers that the markets for collection and processing of animal by-products in category 1 and 2 may be confined by national borders while collection and processing of category 3 material is wider than that and contains at least the whole of the IoI (it can be left open whether it also includes parts of GB, especially Scotland).

5. COMPETITIVE ASSESSMENT – HORIZONTAL OVERLAPS

5.1. Introduction

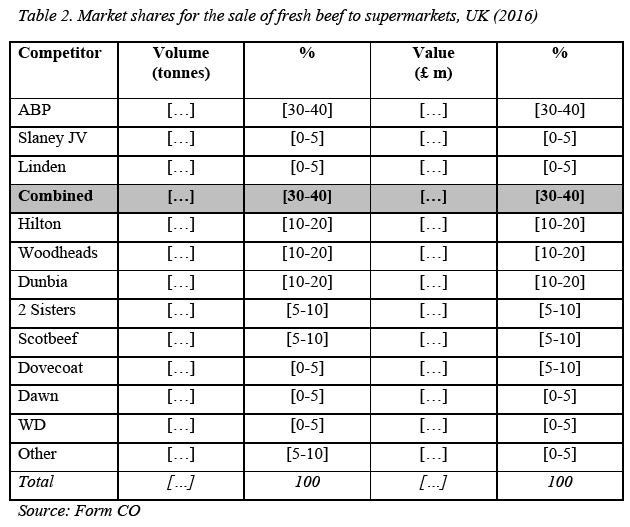

(65) Before the present case was notified to the European Commission on 25 August 2017, a transaction related to the merger between other two meat processors operating in Ireland and the UK (Dawn Meats and Dunbia) was notified to the Irish Competition and Consumer Protection Commission and the UK Competition and Markets Authority. (54)

(66) In light of the above, the assessment of the present case will take into account the proposed merger between Dawn Meats and Dunbia, and in particular will consider the hypothetical scenario in which the two meat processors will become a single entity for the purposes of the competitive assessment, where relevant.

5.2. Purchase of live cattle for slaughter

5.2.1. Non-coordinated effects

(67) As regards the market for the purchase of live cattle for slaughter, the Transaction leads to an affected market in NI. The Parties’ combined market shares post- Transaction will be slightly above [40-50]% both in volume and value. (55)

(68) The Notifying Parties submit that there are several strong competitors in NI (notably, Foyle, WD Meats and Dunbia) to which the Parties would lose volumes swiftly if they attempted to reduce prices to farmers post-Transaction.

(69) Moreover, the Notifying Parties submit there is significant excess capacity in NI. Therefore, any reduction in the Parties’ current prices for cattle could be readily offset by these competing slaughterhouses increasing their purchases and utilising their spare capacity.

(70) The Notifying Parties argue that the Parties are not closer competitors with each other than with other slaughterhouses in NI. All slaughterhouses can process and market all different types and specifications of cattle. Geographically speaking, Linden is not the closest competitors to ABP’s NI plants. The closest competitors to both ABP’s plants in NI is Oakdale’s Lurgan plant, while Dunbia’s Dungannon plant is the next nearest to ABP Newry and Lakeview Farm Meat’s plant is the next nearest to ABP Lurgan.

(71) Finally, the Notifying Parties submit that farmers can and do switch with ease between competing slaughterhouses as there are no long-term supply agreements and the costs of doing so are low. Moreover, transport costs in NI are not significant and do not prevent farmers from supplying cattle to slaughterhouses across N, and thus do not restrict switching.

(72) Starting the assessment by looking at the market shares of the Parties as a proxy of their likely market power, the Commission notes that while the Parties will become the market leader post-Transaction, a number of strong alternative players will remain present on the market; in particular: Foyle (which has a market share very similar to ABP pre-Transaction, of about [20-30]%), WD Meats (market share of about [10-20]%) and Dunbia (about [10-20]%). (56)

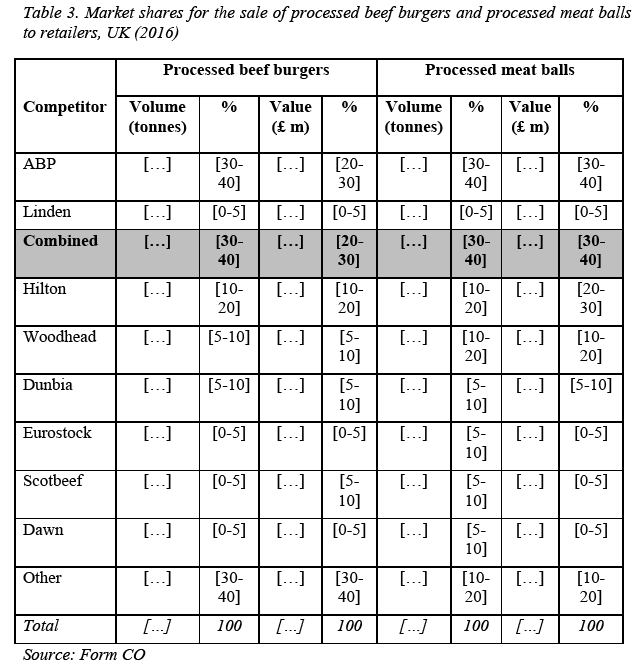

(73) The market investigation revealed that the main competitors of the Parties’ in NI do have spare capacity to slaughter more cattle, and this is in general readily available. (57) Moreover, some slaughterhouses explain that they can also easily increase their processing activity in a short time by “slaughtering at weekends”, for example. Given the ability of competitors to take additional volumes, a price reduction by the Parties would likely result in the Parties losing revenues from downstream beef sales, which would be counterproductive.

(74) The market investigation revealed that in general slaughterhouses do not have written contracts with farmers, but rather verbal agreements, which are not considered to be binding and can easily change. (58) All slaughterhouses responding to the market investigation explain that farmers are free to contact different slaughterhouses and generally do so by comparing prices offered by different processors when getting offers from them. (59) Many farmers confirmed that they sell their live cattle to more than one slaughterhouse and that in order to get price quotes for their cattle, they generally contact multiple slaughterhouses. (60)

(75) Therefore, in line with the findings of case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods, there are no particular barriers to switch for farmers. Transport costs typically represent only about 1-2% of the total price of the cattle in NI and thus do not restrict farmers’ ability to switch. (61)

(76) The majority of competitors responding to the market investigation do not expect the Parties to be able to achieve lower prices when purchasing animals post- Transaction. For example, one explains that “Farmers would simply switch supply to another abattoir.” Another underlines the fact that there is “huge structural capacity, especially in beef”, and therefore no effect on prices will likely occur post-Transaction. (62) One competitor submits that the Parties will achieve a market share above [40-50]% in NI, but does not substantiate any negative effect arising from the Transaction.

(77) Moreover, the majority of farmers responding to the market investigation do not expect any negative impact to arise from the Transaction. Some even mention what they consider to be pro-competitive effects of the deal. For example, one farmer explains that “[…].” (63) An association representing a large number of farmers explained that while it can be difficult to forecast the impact of the Transaction and some farmers are concerned about the possibility of an adverse impact on prices on the markets for live animals (in general), “there are also those in the industry who argue that the processing sector needs to consolidate and become more efficient. This could reduce costs, improve investment in the sector, supply greater consistency to new and existing markets, advance research and development.” The association does not ultimately take a definitive position in this respect and does not elaborate on any particular negative impact that could arise from the Transaction.

(78) Based on the reasons above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to non-coordinated effects on the market for the purchase of live cattle for slaughter in NI.

5.2.2.Coordinated effects

(79) As also explained in case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods, in theory, slaughterhouses could coordinate in two different ways. First, they could agree on a price they pay to farmers and, second, they could divide the farmers by their geographic location and agree to only deal with farmers in their respective region. As to the latter, the Commission considers coordination based on the geographic location of farmers unlikely, in particular in light of the possibility for farmers to easily switch, the limited transport costs for bringing own cattle to more distant slaughterhouses, and the availability of price quotes to all farmers since cattle prices offered by slaughterhouses are published weekly in local newspapers. (64)

(80) As to the former, the market investigation did not reveal any evidence of likely coordination. While the Transaction will reduce the number of market participants, it will also decrease symmetry among them. (65) In particular, the Parties will become larger than the runner-up Foyle (by about [10-20] percentage points) and other smaller competitors. Therefore, the Transaction is unlikely to make it easier for competitors to enter into coordination.

(81) Moreover, as also underlined in the context of case COMP/M.7930 - ABP Group/ Fane Valley Group / Slaney Foods, the demand of slaughterhouses is highly dependent on the demand of retailers, industrial processors and caterers downstream, which is influenced by a number of factors and make it relatively unstable. Such changes in demand make coordination on price relatively difficult in practical terms. (66)

(82) Based on the reasons above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to coordinated effects on the market for the purchase of live cattle for slaughter in NI.

5.3. Purchase of live lambs and live sheep for slaughter

5.3.1. Non-coordinated effects

(83) The Parties' activities overlap only in relation to the purchase of live lambs for slaughter, given the fact that Linden is not active in the purchase of live sheep for slaughter in the IoI. (67)

(84) The market for purchase of live lambs for slaughter in the IoI has recently been assessed by the Commission in the context of case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods. Given the fact that Linden, target of the present Transaction, was already solely controlled by Fane Valley at the time of the assessment of that case, the overlap between ABP and Fane Valley (including Linden) in relation to the purchase of live lambs for slaughter has been already assessed in the context of case COMP/M.7930 - ABP Group / Fane Valley Group/ Slaney Foods. As will be explained in more detail below, the present transaction does not change anything in this respect.

(85) The market investigation conducted in the context of the present case revealed that no particular change in the competitive landscape has occurred in the market in relation to the IoI. (68) In particular, the market shares of the Parties and their competitors overall appear not to have substantially changed from those of 2015, included in the Commission's assessment of case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods. (69) The potential change in the competitive dynamics of the market concerned would be the proposed merger between Dawn Meats and Dunbia, recently notified and currently under review by the national competition authorities of Ireland and the UK.

(86) However, the potential merger between Dawn Meats and Dunbia would not have such an effect on the competitive landscape that a different assessment of the present Transaction (with respect to the Commission’s assessment performed last year in case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods) could be justified. In particular, post-Transaction, Dawn Meats and Dunbia will reach a combined market share between 10% and 20%, and will stay within the same range of the other two main competitors active on the market, Kildare and Kepak. Therefore, through the Dawn Meats/Dunbia proposed merger a rather stronger competitor to its peers (Kepak and Kildare) and the market leader (the Parties combined) will emerge on the market.

(87) The market investigation in the present case, which was launched when the proposed merger between Dawn Meats and Dunbia was already in the public domain and notified to two national competition authorities, did not reveal particular concerns in relation to the present Transaction.

(88) The majority of competitors responding to the market investigation confirmed that they do not expect the Parties to be able to influence prices paid to farmers or volumes bought for ovine animals post-Transaction, but rather expect these to stay the same. (70) In addition, the vast majority of farmers responding to the market investigation did not report any expected negative impact. (71) An association representing a large number of farmers acknowledges that there is a trend of increasing consolidation in the market for the purchase of live ovine for slaughter in the IoI. The submission appears to relate particularly to the purchase of live sheep for slaughter, regarding which the present Transaction does not lead to any overlap. Moreover, concerns voiced related to the purchase of live sheep for slaughter appear to extend to external factors beyond industry consolidation:

“There is a concern that because of the joint venture progressed by Slaney Foods, Irish Country Meats, ABP and Linden Foods, and also the proposed merger of Dawn Meats and Dunbia, a rapid level of consolidation in the sheep processing sector is occurring. These companies currently procure the majority of lambs produced in NI and are slaughtered in both NI and Ireland. If these businesses complete their proposals, the only remaining large competitor will be Kepak in the west of Ireland. This is particularly concerning in the context of Brexit as we do not know what trading conditions there will be between NI and Ireland. If there [were] economic trade barriers for cross border trade this will devastate the NI sheep sector.” (72)

(89) Therefore, the association of farmers appears to express more general concerns in relation to the ovine market which are not fully merger specific. Furthermore, and in any event, the observations made by the association do not substantiate a negative view of the Transaction and its likely effects.

(90) In general, the market investigation confirmed the findings of case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods that farmers can easily switch between slaughterhouses and that these latter have sufficient spare capacity to take on additional volumes should there be any decrease in prices offered to farmers post-Transaction. (73)

(91) Based on the reasons above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to non-coordinated effects on the market for the purchase of live lambs for slaughter in the IoI.

5.3.2. Coordinated effects

(92) In view of what explained in the section above, the Commission refers to its assessment of case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods for potential coordinate effects related to the market of live lambs for slaughter in the IoI.

(93) The only element which differs from the assessment performed in case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods is the proposed merger between Dawn Meats and Dunbia. While if Dawn Meats and Dunbia were to merge, their market shares would increase and would bring their position close to Kepak’s and Kildare’s positions, a significant gap with the market leader (i.e. the Parties, with a market share of about [40-50]%) will remain. Therefore, even if the number of market participants decreases (should the proposed Dawn Meats/Dunbia merger take place), the asymmetry in market shares will remain present, which renders coordination on the market unlikely. (74)

(94) Based on the reasons above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to coordinated effects on the market for the purchase of live lambs for slaughter in the IoI.

5.4. Sale of fresh beef meat

(95) As regards the market for the sale of fresh beef meat, the Transaction leads to an affected market only in relation to the sale of fresh beef to supermarkets in the UK. (75) The Parties’ combined market shares post-Transaction will be about [30- 40]% (in volume and value) on that market in 2016, with a small increment brought by the Transaction (up to [0-5]% in volume and value). No substantial change in market shares have occurred with respect to 2015 and 2014. (76)

(96) The Notifying Parties submit that the increment brought by the Transaction is very small and therefore the Transaction will not significantly alter the Parties' market shares or market power. Moreover, the Notifying Parties explain that the market is not otherwise concentrated and a number of competitors with sufficient size will constraint the Parties' activities post-merger.

(97) In addition the Notifying Parties submit that imports impose a competitive constraint as they are a chief source of supply for large supermarkets in the UK. Finally, the Notifying Parties explain that supermarkets have significant countervailing buying power due to their size, commercial significance and ability to switch to alternative suppliers with ease.

(98) Starting the assessment by looking at the market shares of the Parties as a proxy of their likely market power, the Commission notes that post-Transaction the merged entity will remain the market leader due to ABP's strong position on the market pre-Transaction, and that the increment brought by the operation is very small (about [0-5]% in volume and [0-5]% in value). Therefore the Transaction will not materially alter the market structure, where a number of significant competitors with market shares above 5% will remain on the market: Hilton, Woodheads, Dunbia, 2 Sisters, Scotbeef, Dovecoat.

(99) The proposed merger between Dawn Meats and Dunbia does not impact the present assessment as the increment that would be brought by that merger on the market is small (up to 3%) since Dawn is a rather small player. Therefore, even if Dawn Meats and Dunbia were to merge, all the competitors mentioned in the paragraph above will remain present.

(100) Competitors responding to the market investigation explain that the sale of fresh meat to supermarkets generally occurs in the context of competitive tendering procedures and that supermarkets have significant buyer power against suppliers, especially in view of their ability to easily switch. (77)

(101) On the demand side, retailers indicate that they would be able to switch to other suppliers, and that they do mention their readiness to switch in the context of commercial negotiations with fresh meat providers in order to leverage their position. (78)

(102) Overall, retailers do not expect any negative impact to arise from the Transaction, especially in view of the existence of alternatives on the market to which they could turn in case the merged entity were to increase prices post-Transaction. (79) Competitors do also not expect any negative impact to arise post-Transaction. (80)

(103) Based on the reasons above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for the sale of fresh beef to supermarkets in the UK.

5.5. Sale of processed meat

(104) The Parties are primarily producers of fresh meat (beef and lamb). Whilst they both sell processed meat products, this does not represent a material part of their business. [Description of Linden’s activities in relation to processed meat].

(105) Therefore, as explained in section 4.5, the Transaction gives rise to affected markets only under very narrow market definitions, i.e. the sale of processed beef burgers to retailers in UK and the sale of processed beef meat balls to retailers in UK.

(106) The Parties' combined shares on the potential market for the sale of processed beef burgers would be about [30-40]% in volume and [20-30]% in value, with a very small increment brought by the Transaction of less than [0-5]%. In relation to the potential market for the sale of processed meat balls, the Parties' combined shares would be around [30-40]% in volume and, similarly, [30-40]% in value, with an insignificant increment brought by the Transaction of less than [0-5]%. (81)

(107) The Notifying Parties submit that the Transaction will lead to a very minor change in these markets in the UK since [Description of Linden’s activities in relation to processed beef burgers and processed meat balls], while there are numerous other suppliers of each product that will continue to impose a competitive constraint on the Parties post-Transaction.

(108) Starting the assessment by looking at the market shares of the Parties as a proxy of their likely market power, the Commission notes that post-Transaction the merged entity will remain the market leader on both markets due to ABP's strong position pre-Transaction, and that the increment brought by the operation is either very small (less than [0-5]% for processed beef burgers) or insignificant (less than [0-5]% for processed beef meat balls). Therefore the Transaction will not materially alter the market structure, where a number of significant competitors with market shares above [5-10]% will remain on the market, including Hilton, Woodhead, and Dunbia. Moreover, many smaller competitors (which collectively hold about [30-40]% of the processed beef burgers market and about [10-20]% of the processed beef meat balls market) will remain present.

(109) As explained in relation to the market for the sale of fresh beef, the proposed merger between Dawn Meats and Dunbia does not impact the present assessment as the increment that would be brought by that merger on both potential markets is small (up to about 5%). Therefore, even if Dawn Meats and Dunbia were to merge, many other competitors, as mentioned in the paragraph above, will remain present.

(110) As already mentioned in relation to the market for the sale of fresh beef, retailers have buyer power against suppliers and can easily switch between several meat providers present on the market. (82)

(111) Overall, the market investigation (including pre-notification calls) did not reveal any negative concern in relation to these markets neither from competitors nor retailers. (83)

(112) Based on the reasons above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the market for the sale of fresh beef to supermarkets in the UK.

6. COMPETITIVE ASSESSMENT – VERTICAL RELATIONSHIPS

6.1. Animal by-products

(113) Meat processors and slaughterhouses have to dispose their animal by-products that result from their activities. Therefore, a vertical relation exists between the upstream markets for slaughtering of live animals and the downstream markets for the collection and processing of animal by-products.

(114) On the downstream markets, ABP is active with two plants in Ireland but none in NI. Specifically, it operates the Munster Protein category 3 plant in Tipperary and a category 1 plant in Waterford. In addition, Fane Valley and ABP jointly control Slaney JV which operates a category 3 processing plant in Wexford, also located in Ireland.

(115) While Linden does not operate any processing plants for animal by-products, it holds minority shareholdings in Linergy. Linergy operates two processing plants in NI, one for category 3 products and the other for category 1 and 2 material. It is not active in Ireland. Fane Valley is also a minority shareholder in Linergy, in addition to Linden. (84)

(116) The proposed merger between Dawn Meats and Dunbia will not affect the present assessment given the fact that Dunbia is not active in the rendering business on the IoI; only Dawn Meats is (through Western Proteins).

6.1.1. Input foreclosure

(117) Input foreclosure concerns could only arise if the merged entity had the ability and incentive to prevent downstream competitors (i.e. other renderers) from access to relevant inputs. Currently, ABP processes all its category 3 material from its slaughterhouses on the IoI in its own facilities. Given that ABP is not active as a supplier of other third party renderers, it does not have any ability to foreclose competing processors of category 3 materials in the relevant markets.

(118) The situation is comparable in relation to category 1 products. Almost the totality of ABP's category 1 materials are processed in its own facilities, with only [5-10]% of the material from its Newry's plant being processed by Linergy. Given Linergy's total capacity, this amounts to less the [0-5]% of Linergy's processing of these material.

(119) Linden provides all of its animal by-products to Linergy. Therefore, no other rendering facility could be foreclosed. A potential foreclosure of Linergy seems also unlikely, given that Linden's input account for about [5-10]% of Linergy's total capacity for the processing of animal by-products (both in relation to category 1 and category 3 material). Therefore, Linden would not have the ability to effectively foreclose Linergy.

(120) In addition, and taking into account Linden's shareholdings in Linergy, it seems unlikely that the merged entity would have any incentive to foreclose Linergy. This is even more the case giving the physical distance between the Parties facilities. A favouring of ABP's rendering plants in the southern part of Ireland at the expense of the Linergy plants (located in Northern Ireland, in proximity to Linden's slaughtering plants) would lead to additional transport costs.

(121) Based on the reasons above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to this vertical link.

6.1.2. Customer foreclosure

(122) A customer foreclosure strategy would require the ability and incentive of the merged entity to restrict competing slaughterhouses from accessing processors of animal by-products. Such a strategy requires market power on the downstream market for collection and processing of animal by-products.

(123) In the market for collection and processing of category 1 and 2 products, ABP is not active in Northern Ireland but only in Ireland. On a such defined geographic market, it reaches market shares of [30-40]%, being the second largest processor behind College Proteins. In addition, Dublin By-Products is also active and has market shares of more than [20-30]%.

(124) The Parties estimate spare capacity across all rendering facilities to be approximately 35% in the industry. The market investigation did not reveal any information contradicting this estimation overall. (85) In addition, all meaningful replies to the market investigation confirm that in general, spare capacity for processing of category 1 and 2 material exists in Northern Ireland as well as in Ireland. (86)

(125) In light of the lack of market power and the availability of spare capacity of competing rendering facilities, the merged entity would not be in a position to foreclose access of competing slaughterhouses to rendering facilities for category 1 and 2 animal by-products.

(126) In relation to category 3 material, ABP and Slaney reach market shares of slightly above [30-40]% on an IoI-based market. Other large competitors like College Proteins, Western Proteins, Linergy, and Dublin By-Products are also active on the market and make up the remaining [70-80]% of the total market size.

(127) The market investigation indicated that overall sufficient spare capacity is readily available for the collection and processing of category 3 material so that competitors could easily move to other providers should the Parties try to lower prices paid for category 3 material. (87)

(128) Based on the reasons above, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to this vertical link.

7. ARTICLE 2(4) ASSESSMENT (POSSIBLE SPILL-OVER EFFECTS)

(129) Under Article 2(4) of the Merger Regulation, to the extent that the creation of a JV that constitutes a concentration pursuant to Article 3 has as its object or effect the coordination of the competitive behaviour of undertakings that remain independent, the Commission must assess such coordination in accordance with the criteria of Article 101(1) and (3) TFEU, with a view of establishing whether or not the operation is compatible with the common market.

(130) In making this assessment, the Commission must take into account, in particular, whether two or more parent companies retain, to a significant extent, activities in the same market as the joint venture or in a market that is downstream or upstream from that of the joint venture or in a neighbouring market closely related to this market. In addition, the Commission has to take into account whether the coordination which is the direct consequence of the creation of the joint venture affords the undertakings concerned the possibility of eliminating competition in respect of a substantial part of the products or services in question. A restriction of competition under Article 101(1) TFEU is established when the coordination of the parent companies' competitive behaviour is likely and appreciable and results from the creation of the joint venture. (88)

(131) Given the fact that Linden constitutes the existing slaughtering and processing business of Fane Valley, ABP and Fane Valley will not individually have activities in any market where Linden in active.

(132) Moreover, ABP and Fane Valley will not both retain significant activities in a market which is upstream or downstream from the markets in which Linden is active.

(133) First, ABP and Fane Valley will be active in the collection and processing of animal by-products, which is a downstream market in relation to Linden's activities in the market for the purchase of live animals. However, Fane Valley is only active on the by-products market through the Slaney JV, which serves practically only its parents rather than the merchant market. Moreover, the relevant vertical links arising from the Transaction have already been discussed in the context of the competitive assessment of the Transaction (see section 6.2) and thus will not be further considered. Finally, there is no evidence that the creation of the joint venture will increase the likelihood of coordination of the Parties' competitive behaviour in the market for the collection and processing of animal by-products.

(134) Second, ABP and Fane Valley will both retain activities in the supply of beef dripping in the UK, a market which is downstream of Linden's slaughtering activities. (89) The Commission has not previously considered a potential market for beef dripping. In any event, the Notifying Parties will not retain significant activities in this potential market, having estimated combined market shares in the UK of less than [10-20]% (Fane Valley: [10-20]%; ABP [0-5]%). In light of the asymmetric position of the Notifying Parties on this potential market and the relatively low combined market shares, the Commission considers that spill-over effects are unlikely and, in any event, unlikely to be appreciable in relation to the market for beef dripping. Moreover, there is no evidence that the creation of the joint venture will increase the likelihood of coordination of the Parties' competitive behaviour in this market.

(135) There are no neighbouring markets closely related to the markets where Linden is active in which ABP and Fane Valley will both retain activities to a significant extent.

(136) Finally, the Transaction will not significantly alter the existing relationship between ABP and Fane Valley, which are already parent companies to the joint venture Slaney JV, itself subject to Commission's merger clearance last year. (90) There is no reason to believe that the Transaction will lead to any higher likelihood of coordination of the Parties' competitive behaviour in markets where Linden is not present than which already exists in their current relationships.

(137) Therefore, the Commission considers that the Transaction does not give rise to any potential spill-over effects.

8. CONCLUSION

(138) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 290, 01.09.2017, p. 13.y

4 On 7 October 2016, the Commission unconditionally cleared the transaction whereby ABP acquired joint control over the Slaney JV together with Fane Valley (COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods). The Slaney JV is a full-function joint venture jointly controlled by ABP and Fane Valley. It is active in the slaughtering of cattle and ovine animals, the processing and sale of their meat and the collection and processing of animal by-products. Slaney JV has 1 bovine and 2 ovine slaughtering plants in Ireland. The Slaney JV also further processes bovine in its Ireland ovine slaughtering plants. The Slaney JV also has a lamb processing plant in Belgium.

5 Fane Valley does not control any other slaughtering/processing plants beyond those of Linden and the Slaney JV.

6 See COMP/M.7930 – ABP Group / Fane Valley Group / Slaney Foods.

7 Turnover calculated in accordance with Article 5 of the Merger Regulation.

8 Commission decision of 7 October 2016 in case M.7930 – ABP Group / Fane Valley Group / Slaney Foods, paragraph 79.

9 Commission decision of 7 October 2016 in case M.7930 – ABP Group / Fane Valley Group / Slaney Foods, paragraph 80.

10 Commission decision of 20 August 2010 in case M.5935 – Vion/ Weyl, paragraphs 10-11; Commission decision of 21 December 2005 in case M.3968 – Sovion/ Südfleisch, paragraph 12; Commission decision of 19 March 2004 in case M.3337 – Best Agrifund/ Nordfleisch, paragraph 17; Commission decision of 9 March 1999 in case M.1313 – DanishCrown/ Vestjyske Slagterier, paragraphs 20-21.

11 Commission decision of 7 October 2016 in case M.7930 – ABP Group / Fane Valley Group / Slaney Foods, paragraph 93.

12 See replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – question 6.

13 See replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – question 9.

14 See replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – question 8. For example, "[Farmers produce] different breeds to meet different market requirements."

15 See replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – question 7.

16 See replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – question 6.

17 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 10-12.

18 The inclusion or exclusion of calves in such an overall market does not materially impact the outcome of the assessment in this case as calves represent only less than 3% of all cattle purchased for slaughter in each of NI and GB in 2016.

19 Commission decision of 9 March 1999 in case M.1313 – DanishCrown/ Vestjyske Slagterier, paragraphs 66 to 73; Commission decision of 19 March 2004 in case M.3337 – Best Agrifund/ Nordfleisch, paragraphs 18 to 21; Commission decision of 21 December 2005 in case M.3968 – Sovion/ Südfleisch, paragraphs 35-36; Commission decision of 20 august 2010 in case M.5935 – Vion/ Weyl, paragraphs 14 to 19.

20 Commission decision of 7 October 2016 in case M.7930 – ABP Group / Fane Valley Group / Slaney Foods, paragraph 106.

21 OFT ME/5251/11 – Completed acquisition by ABP Food Group of RWM Food Group Holdings Limited.

22 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 29.

23 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 30. Origin labelling requirements mean that an animal can only be called and its meat marketed as Irish or British, for example, if it is born, raised and slaughtered in that country; it cannot change origin labelling by being finished or slaughtered in a different jurisdiction.

24 See replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – questions 13-14 and 31-32. For example one farmer explains that "one is Irish, the other is UK." Another explains that "Irish beef must be sold as Irish beef. British beef must be sold as British beef."

25 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 33-34, and replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – questions 15-16. For example, one slaughterhouse explains that "[The distance cattle travel is] likely to be more like 80 miles given the improvement in national road networks"; another "Cattle can travel up to 8 hours."

26 Teleconference with [Anonymous] on 17 July 2017.

27 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 35; and replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – question 17.

28 Commission decision of 7 October 2016 in case M.7930 – ABP Group / Fane Valley Group / Slaney Foods, paragraph 114.

29 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 15.

30 Commission decision of 7 October 2016 in case M.7930 – ABP Group / Fane Valley Group / Slaney Foods, paragraph 123.

31 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 39-42; and replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – questions 20-23. For example, one slaughterhouse explains that "There is no restriction on the movement of live lambs and sheep between Ireland and NI." Famers also explained that "The Irish market for live lambs is hugely important for the NI sheep industry. Approx. 40% of NI lambs are exported for processing in Ireland […]." "[…] [there are] well established cross border routes to [the] market."

32 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 40.

33 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 124; Commission decision of 20 August 2010 in case M.5935 - Vion/ Weyl, paragraphs 36 and 39; Commission decision of 9 March 1999 in case M.1313 - Danish Crown/ Vestjyske Slagterier, paragraph 34.

34 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 124; Commission decision of 20 August 2010 in case M.5935 - Vion / Weyl, paragraph 36; Commission decision of 8 December 2004 in case M.3535 - Van Drie/ Schils, paragraphs 18-19; Commission decision of 19 March 2004 in case M.3337 - Best Agrifund/ Nordfleisch, paragraph 23.

35 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 148; Commission decision of 20 August 2010 in case M.5935 - Vion/ Weyl, paragraph 37; Commission decision of 21 December 2005 in case M.3968 - Sovion/ Südfleisch, paragraph 62; Commission decision of 19 March 2004 in case M.3337 - Best Agrifund/ Nordfleisch, paragraph 24.

36 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 142.

37 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 17-18; and replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – questions 6-7. For example one retailer explains that "Fresh meat meets a different consumer demand. From a supply side perspective fresh meat is only subject to the mechanical process of cutting and cleaning, no heat or curing is applied."

38 See replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – question 11.

39 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 20; and replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – question 16.

40 See replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – question 20. For example, one retailer explains that "More premium breeds e.g. Angus [cost more]."

41 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 156; Commission decision of 20 August 2010 in case M.5935 - Vion / Weyl, paragraphs 40 and 42; Commission decision of 21 December 2005 in case M.3968 - Sovion/ Südfleisch, paragraph 65; Commission decision of 21 December 2004 in case M.3605 - Sovion/HMG, paragraphs 68-70.

42 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 46-47.

43 See replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – question 25.

44 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 185; Commission decision of 17 July 2015 in case M.7565 - Danish Crown / Tican, paragraphs 21-25 and 32; Commission decision of 19 March 2004 in case M.3337 - Best Agrifund / Nordfleisch, paragraphs 39-40, 44 and 46.

45 Commission decision of 17 June 2004 in case M.3401 – Danish Crown / Flagship Foods.

46 Commission decision of 7 October 2016 in case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 185; Commission decision of 17 July 2015 in case M.7565 - Danish Crown / Tican, paragraphs 21-25 and 32; Commission decision of 19 March 2004 in case M.3337 - Best Agrifund / Nordfleisch, paragraphs 39-40, 44 and 46.

47 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 188.

48 See replies to Q3 Questionnaire to Rendering facilities and other processors of animal by-products – question 7 and Q1 Questionnaire to slaughterhouses – Question 26. In particular, category 1 material is high risk material which has to be processed by rendering facilities with the outputs having to be incinerated. In Ireland and UK, category 2 material is downgraded and processed as category 1 material. Category 3 material does not need to be incinerated but is rather processed into other products (e.g. pet food).

49 See replies to Q3 Questionnaire to rendering facilities and other processors of animal by-products – question 9; and replies to Q1 Questionnaire to slaughterhouses – question 28; and replies to Q2 Questionnaire to farmers and farmers' associations – question 37.

50 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 197; Commission decision of 14 February 2002 in case M.2662 - Danish Crown / Steff-Houlberg, paragraph 88; Commission decision of 9 march 1999 in case M.1313 - Danish Crown / Vestjyske Slagterier, paragraphs 98-99.

51 CMA final report on Linergy Limited and Ulster Farm By-Products Limited, 6. January 2016.

52 See replies to Q02 Questionnaire to farmers and farmers' associations of 28 August 2017 – questions 27-28. For example: "It is more likely that there is a cross border trade for animal by products from processing plant [rather than for fallen stock]." "Veterinary restrictions to the export of fallen stock between NI and Ireland [exist]."

53 See replies to Q3 Questionnaire to rendering facilities and other processors of animal by-products – questions 14-15.

54 This transaction was notified to the Irish Competition and Consumer Protection Commission on 16 June 2017 (M/17/035 – Dawn Meats / Dunbia) and to the UK Competition and Markets Authority on 10 August 2017.

55 No substantial change in the market shares of the Parties and their competitors have occurred with respect to 2015 and 2014.

56 Given the fact that Dawn Meats is not active in NI in relation to the purchase of live cattle for slaughter, the proposed merger between Dawn Meats and Dunbia does not affect in any way the present assessment.

57 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 5, 62, 65.

58 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 58; and replies to Q02 Questionnaire to farmers and farmers’ associations of 28 August 2017 – question 34.

59 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 59. For example, one explains that “Farmers will typically phone around for the best price and will often claim that competitors are offering more money in order to negotiate a better price.”

60 See replies to Q02 Questionnaire to farmers and farmers’ associations of 28 August 2017 – questions 29 and 33.

61 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 38.

62 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 60.

63 See replies to Q02 Questionnaire to farmers and farmers’ associations of 28 August 2017 – questions 41-42.

64 See replies to Q02 Questionnaire to farmers and farmers’ associations of 28 August 2017 – question 32.

65 Horizontal Merger Guidelines, paragraph 48: "Firms may find it easier to reach a common understanding on the terms of coordination if they are relatively symmetric, especially in terms of cost structures, market shares, capacity levels and levels or vertical integration. […]"

66 Commission decision of 7 October 2016 in case M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 321.

67 Linden had very minimal activities on the market for the purchase of live sheep in the IoI in 2015 (purchase of […] tonnes).

68 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 54.

69 Reference to case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods, paragraph 330. See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 5.

70 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 60, 66, 67.

71 See replies to Q02 Questionnaire to farmers and farmers’ associations of 28 August 2017 – question 35.

72 See replies to Q02 Questionnaire to farmers and farmers’ associations of 28 August 2017 – question 20.

73 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 60 and 62-64.

74 Horizontal Merger Guidelines, paragraph 48: "Firms may find it easier to reach a common understanding on the terms of coordination if they are relatively symmetric, especially in terms of coordination if they are relatively symmetric, especially in terms of cost structures, market shares, capacity levels and levels or vertical integration. […]"

75 Technically, outside the UK, the market for the sale of fresh beef to supermarkets in Ireland would be an affected market, but the Parties' market shares exceed 20% […] (2016). Moreover, this market was examined by the Commission in the context of case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods, and ABP's share has subsequently reduced since 2015. As the Transaction will not alter the position on this market since the Commission's previous assessment, this market will not be further discussed.

76 The only relatively relevant variation being an increase in Dunbia's market shares from about [5-10]% in 2014 to about [10-20]% in 2016.

77 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – questions 9, 70. For example, one competitor explains that "[Buyer power] is due to the level of excess capacity that exists within the processing sector. It is very easy for a customer to switch suppliers (irrespective of sales channel)." Another explains that "yes they do [have buyer power] as there is a lot of competition."

78 See replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – questions 37-38.

79 See replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – questions 38-40.

80 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 71.

81 The data is related to 2016. There are no indications that substantial changes in the market shares of the Parties and their competitors have occurred with respect to 2015 and 2014.

82 See replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – questions 37-38.

83 See replies to Q01 Questionnaire to slaughterhouses of 28 August 2017 – question 79, 81; and replies to Q04 Questionnaire to retailers and meat processors of 28 August 2017 – questions 38-41.

84 The facts on file, including Linergy's corporate governance rules, indicate that the Parties would not be in a position to impose or block strategic decisions of Linergy. In line with the Commission's findings in the context of case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods, the Commission considers that the Parties do not control Linergy.

85 See replies to Q04 Questionnaire to rendering facilities and other processors of animal by-products of 28 August 2017 – question 21.

86 See replies to Q04 Questionnaire to rendering facilities and other processors of animal by-products of 28 August 2017 – question 22.

87 See replies to Q04 Questionnaire to rendering facilities and other processors of animal by-products of 28 August 2017 – question 23.

88 Merger Regulation, Article 2(5).

89 Beef dripping is a refined animal fat that can be used by the food service and catering sectors for cooking (e.g. for frying food). The Notifying Parties submit that beef dripping is supplied across the UK (thus including NI) by suppliers on the same terms.

90 See case COMP/M.7930 - ABP Group / Fane Valley Group / Slaney Foods.