Commission, July 23, 2019, No M.9062

EUROPEAN COMMISSION

Judgment

FORTRESS INVESTMENT GROUP / AIR INVESTMENT VALENCIA / JV

Subject: Case M.9062 – Fortress Investment Group/Air Investment Valencia/JV Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 19 June 2019, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004. (3) Fortress Investment Group (USA) and Air Investment Valencia (Spain) acquire, by way of purchase of shares, joint control within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation of a newly created company constituting a joint venture (the “JV”), in which (i) Fortress Investment Group will contribute the business of CityJet and (ii) Air Investment Valencia will contribute the businesses of Air Nostrum (the “Transaction”). The Transaction is accomplished by way of purchase of shares.

(2) CityJet and Air Nostrum are both regional airlines providing – amongst others - wet- leasing services (leasing of aircraft with crew and maintenance services) to other airlines.

1. THE PARTIES

(3) Fortress Investment Group (“Fortress”) is global investment management firm belonging to SoftBank Group (Japan), a group comprising subsidiaries involved in telecommunication products and services, primarily in the USA and in Japan. Fortress is pre-Transaction jointly controlling CityJet, together with CityJet Holdings Ltd. (4) CityJet is a European regional airline based in Dublin, Ireland. It is operating a fleet of 35 aircraft and is providing wet-leasing services to other airlines across Europe. Fortress is also the parent company of Falko Regional Aircraft Limited (Falko), a provider a dry lease and other aviation services to airlines worldwide, including in Europe.

(4) Air Investment Valencia is a holding company indirectly fully owned by Mr Carlos Bertomeu. Through Air Investment Valencia, Mr. Bertomeu pre-Transaction solely controls Air Nostrum. (5) Air Nostrum is a regional airline based in Valencia, Spain, and is operating a fleet of approximately 50 aircraft. It is providing scheduled flight services under a franchise agreement with Iberia. In addition, Air Nostrum is providing charter services, wet-leasing services, crew training and aircraft maintenance services to other airlines. Air Nostrum solely controls Aviatech & Consulting, S.L., a provider of technical services such as flight control and flight operations, and Hibernian Airlines Limited, an airline based in Ireland, which is providing wet-leasing services, currently only to Air Nostrum. Both companies will also be contributed to the JV.

(5) The proposed transaction (6) in essence amounts to the combination of CityJet’s and Air Nostrum’s activities in wet-leasing.

2.THE CONCENTRATION AND THE ACQUISITION OF JOINT CONTROL

(6) The businesses of City Jet and Air Nostrum will be transferred to a newly created joint venture, which will own 100% of the shares in Air Nostrum and 100% of the shares in CityJet. The current shareholders of Air Nostrum (including its controlling parent Air Investment Valencia) will hold 70% of the JV. The remaining 30% of the shares in the JV will be owned by Fortress.

(7) Post-Transaction, the JV will be jointly controlled by Fortress and Air Investment Valencia. (7) Air Investment Valencia is the majority shareholder of the JV, but Fortress has negative joint control together with Air Investment Valencia through certain veto rights conferred to Fortress regarding key business decisions. Fortress and Air Investment Valencia will determine the initial budget and business plan together. In addition, for the first […] years, Fortress will have veto rights regarding the approval of annual budget and business plan, the appointment of the CFO and the termination of contracts with the current CityJet management team. Those veto rights will exist for a period of […] years. According to paragraph 34 CJN, only a relatively short period not exceeding one year will make it unlikely that the joint control period has a distinct impact on the market structure and could be considered as not leading to a change in control on a lasting basis.

(8) As a result, Fortress and Air Investment Valencia will acquire joint control over the JV on a lasting basis.

3. FULL-FUNCTIONALITY OF THE JV

(9) The JV will be full-function within the meaning of Article 3 (4) EUMR since it has sufficient resources, activities beyond one specific function for the parents, access to the market and operates on a lasting basis.

4. EU DIMENSION

(10) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (Softbank Group: EUR […] million, Air Investment Valencia: EUR […] million). Each of them has an EU-wide turnover in excess of EUR 250 million (Softbank Group: EUR […] million, Air Investment Valencia: EUR […] million), but they do not both achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(11) The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

5. MARKET DEFINITION

(12) CityJet provides wet and damp lease (ACMI) services and charter flight services. CityJet’s charter flight services have largely wound down and charter flights are provided only on a very exceptional basis for […]. (8)

(13) Air Nostrum provides franchise services, wet and damp lease services and charter flight services.

(14) Fortress Investment Group is active dry leasing services through its subsidiary Falko.

(15) Dry-leasing, wet and damp leasing and franchise services are used by airlines to increase capacity. Dry-leasing involves the leasing of an aircraft to an airline, without crew, maintenance services and insurance. Wet-leasing to airlines involves the leasing of an aircraft to an airline with crew, maintenance and insurance (‘ACMI’). A damp lease is very similar to a wet lease. The only difference is that with damp leases, the cabin crew are provided by the lessee. Under a franchise agreement, the franchisor airline puts its brand and livery at the disposal of the franchisee for use under the franchise agreement. Charter flights services are flights operated by an airline on behalf of a third party where the airlines quotes an “all-in” cost to the customer. Charter flight services use the flight numbers of the operating airline and all operating costs (fuel, handling, navigation, etc.) are paid for by the airline and “bundled” into the price ultimately charged to the customer. The customer is generally a non-airline customer such as travel agency, a tour operator or a private/corporate entity such as a sports team.

(16) In a previous decision, the Commission considered that dry-leasing, wet-leasing and franchise services constituted three distinct markets, notably because of their different characteristics from a demand-side perspective. (9) The Commission has also considered the market for charter flights as a distinct market from the market for scheduled flights. (10)

(17) The Transaction therefore gives rise to horizontal overlaps with respect to (i) wet and damp lease services and (ii) charter flight services. The Transaction also creates vertical links with respect to (a) dry-leasing services on the one hand and (i) wet and damp leasing services, (ii) franchise services and (iii) charter flight services on the other hand (b) wet-leasing services on the one hand and (i) franchise services and (ii) charter flight services, on the other hand.

5.1. Wet and damp-leasing services

5.1.1. Product market definition

(18) Under a wet-leasing agreement, the lessor operates the flights using its own air operator certificate (AOC) and resources, for which it receives an income from the lessee which is usually a fixed price per block hour. This income would be unrelated to ticket prices and aircraft load factor. The flights are flown under the lessee’s code and it is the lessee who sells the tickets and provides passenger and ground handling services. The commercial risk in a wet lease lies with the lessee, who must generate the revenue to cover the cost of the wet-leasing services and other operating costs. Wet-leasing would allow for an airline to have an aircraft ready turnkey to fly its passengers without investing in the aircraft or crew to operate it. (11)

(19) The Parties submit that a damp lease would be very similar to a wet lease. The only difference would be that with damp leases the cabin crew would be provided by the lessee, not the lessor. The Parties consider damp leases and wet-leases to form part of one wet-leasing market. They state that it would only be in incidental cases that customers ask for damp leases and the Parties would have not experienced a request for a damp lease so far. In addition, the Parties would not be aware of any wet-leasing provider which only focuses on damp-leasing. All wet-leasing providers would be able to provide damp-leasing services if requested by the customer. (12)

(20) In its prior decisional practice, the Commission did not specifically examine damp lease services.

(21) The market investigation in this case has not generated any evidence indicating that wet-leasing and damp-leasing services would not be substitutable from the supply and the demand side. Respondents have not submitted any comment suggesting that a distinction between wet-leasing and damp-leasing would be appropriate. (13) Considering that the Parties have never provided damp-leasing services so far and that no airline solely provides damp-leasing services, the Parties’ market shares in the market for wet-leasing only would not significantly vary. The question of whether wet-leasing and damp-leasing services are part of the same market can be left open, since the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to wet and damp leasing services, under any plausible product market definition. (14) In this decision, the Commission will further assess the effects of the Transaction on the hypothetical narrower segment for wet-leasing services.

(22) The Commission has in a previous case considered that wet-leasing services for cargo air transport services and wet-leasing services for passenger air transport services appear to constitute distinct markets. (15) However, since CityJet and Air Nostrum only provide wet-leasing services for passenger air transport, (16) the Commission will only assess this market segment further in this decision.

(23) In addition, while ultimately leaving the precise market definition open, the Commission has considered in a previous case that the market for the provision of wet-leasing services could be segmented according to aircraft size (seat capacity). The Commission has considered distinctions between regional aircraft (aircraft with around 30-90+ seats and a range of less than 2000 nautical miles) and large commercial aircraft (aircraft with more than 100 seats and a range greater than 2000 nautical miles). With regard to large commercial aircraft, a distinction between wide- body aircraft with 200-400+ seats and narrow-body aircraft with 100-200 seats was considered. Concerning regional aircraft, the Commission considered, but ultimately left open, a distinction between small regional aircraft with 30-50 seats and large regional aircraft with 70-90+seats. (17)

(24) The Parties submit that, while it would be difficult to draw a particular distinction based on aircraft sizes, a possible distinction could be made between small aircraft with a seat capacity between 30-120 seats, middle-sized aircraft with a seat capacity between 121-190 seats and large aircraft with a seat capacity of more than 191 seats. Given the various sizes available, it would not be possible to draw a clear line between regional aircraft and slightly larger narrow-body aircraft with more than 100 seats. In the Parties’ view, while aircraft with a seat capacity of below 50 would be distinct from a demand side perspective, the aircraft sizes above would become substitutable to a significant extent. The Parties explained that, from a demand side perspective, airlines would take into account the total cost of production in their consideration which aircraft size to wet lease. These costs would include the wet lease rate charged by the lessor and all other operating cost for the flight operations. Larger aircraft would have a higher trip cost than a smaller unit, but the cost per seat would be lower and could be more attractive to a lessee. (18)

(25) From a demand side perspective, the market investigation has indicated that customers consider a segmentation between aircraft with a seat capacity of less than 115 and aircraft with a seat capacity of more than 100. Concerning wet-leasing services of regional aircraft, the following three possible ways to divide the market for wet-leasing services of regional aircraft by seat capacity, were considered by customers: (i) under 50 seats; above 50 seats; (ii) 50-70 seats; 70-100 seats and (iii) 30-70 seats; 70-100+ seats. (19)

(26) Considering that the Parties do not operate aircraft of a seat capacity of 50-70, the Transaction would not give rise to an overlap with respect to this hypothetical narrower market. It is therefore not necessary to further assess whether the market for wet-leasing services of regional aircraft should be segmented according to the following seat capacities (i) aircraft with a capacity under 50 seats; above 50 seats; (ii) 50-70 seats; 70-100 seats.

(27) In any event, the question of whether wet-leasing services should be segmented according to the aircraft capacity can be left open for the purpose of this case, since the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to wet-leasing services, under any plausible product market definition. (20) Nevertheless, considering that the Parties both use regional aircraft of a seat capacity between 88 and 100, the Commission will assess the effects of the Transaction on the following markets: the broader market for wet- leasing services; the segment for wet-leasing services of regional aircraft (with a capacity of 30-90+ seats); the sub-segment large regional aircraft (with a capacity of 70-90+ seats).

5.1.2. Geographic market definition

(28) The Parties consider that the market for wet-leasing services is at least EEA-wide. (21)

(29) In a previous decision, the question of whether the market for wet-leasing services is EEA-wide or worldwide was left open. (22)

(30) The market investigation has indicated that from a supply-side perspective, the main competitors of CityJet and Air Nostrum are only active in the EEA but they could, in principle, offer wet-leasing services worldwide. (23) From a demand-side perspective, airlines purchasing wet-leasing services considered that they would purchase the services from wet-lessors within the EEA for wet-leases with a duration of more than six-seven months because of the current regulatory framework. (24) Article 13(3)(b) of Regulation no 1008/2008 of 24 September 2008 on common rules for the operation of air services in the Community limits wet-leasing arrangements between EU air carriers and third countries to seven months, renewable once.

(31) Based on the above considerations, the Commission considers that the geographic market for wet-leasing services is at least EEA-wide.

(32) The question of whether the geographic market for wet-leasing services is EEA-wide or worldwide can be left open for the purpose of this case, since the Transaction is unlikely to raise serious doubts as its compatibility with the internal market in relation to wet-leasing services if an EEA-wide market is considered, which is in any case the narrower market. (25)

5.2. Charter flight services

5.2.1. Product market

(33) Charter flight is a service where the flight characteristics, such as dates, times, cities of departures and destination, and inflight services, are arranged in accordance with the customer’s needs. Charter flights are thus air transport services that take place outside normal schedules, normally through an arrangement with a particular customer (e.g. a tour operator, a sports team).

(34) In its prior decisional practice, the Commission defined a separate wholesale market for airline seats, in which supply is represented by airlines and demand by tour operators that purchase individual seats, block seats or entire flights and integrate them in their package holidays. The Commission considered but left open whether there is a separate market for the wholesale supply of airline seats by charter airlines. (26) Considering that there might be a market for the wholesale supply of airline seats to tour operators by charter airlines, it could be argued that the market for charter flights could be segmented by customer type. The Parties consider that the exact market definition can be left open, given the small scale of charter services offered by the Parties. (27)

(35) The question of whether charter flight services should be segmented between (i) charter flight services to tour operators and (ii) charter flight services for other types of customers (private individuals or businesses, such as sports clubs) can be left open for the purpose of this case, since the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to charter flight services, under any plausible product market segmentation. (28)

5.2.2. Geographic market definition

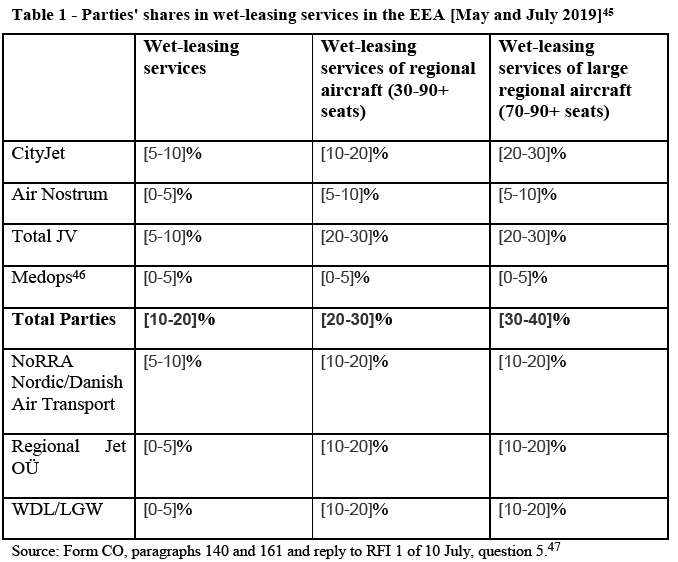

(36) The Parties consider that the market for charter flight services should be defined as at least EEA-wide. (29)

(37) In its decisional practice relating to the wholesale supply of airline seats to tour operators by charter airlines, the Commission considered that the geographic scope was national.30

(38) Considering that there are no regulatory restrictions preventing a charter airline from providing services outside from its own country of establishment, charter flight provider can offer services on any route within the EEA. In addition, the cities of origin and destination for charter flights are defined by the customer, which selects a provider of charter services, indifferent from its country of establishment. In that regard, Air Nostrum and CityJet have provided charter flights to customers in the majority of EEA countries. (31) A respondent to the market investigation that provides charter flights indicated that it provides charter flights on any city-pair within the EEA and therefore considers the market for charter flight services as EEA-wide. (32) There are therefore indications that the geographic scope for charter flight services is EEA-wide.

(39) However, the question of whether the geographic scope of charter flight services is EEA-wide or national can be left open for the purpose of this case, since the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to charter flight services, under any plausible geographic market segmentation. (33)

5.3. Franchise services

5.3.1. Product market

(40) Under a franchise agreement, the franchisee operates with its own aircraft, crew, maintenance, insurance and slots, using the brand and livery of the franchisor. The franchisee bears the commercial risk, including setting fares, but the franchisor markets the route as part of its network and sells the tickets. In return for the use of the brand and for the services provided, the franchisee pays a fee to the franchisor. In contrast with wet-leasing services, franchise services are hence more akin to scheduled services.

(41) In a prior decision, the Commission considered the provision of franchising services to other airlines as an input to the operation of passenger air transport services. (34) For the purpose of the assessment of Transaction, the Commission will consider that dry- leasing services and wet-leasing services are an input to the operation of franchise services.

5.3.2. Geographic market

(42) In a prior decision, the Commission considered that the geographic scope for the provision of franchise services is EEA-wide. (35)

(43) In line with its prior decisional practice, the Commission considers that, for the purpose of this case, the geographic scope for the provision of franchise services is EEA-wide.

5.4. Dry-leasing services

5.4.1. Product market definition

(44) The Commission has, in a previous case considered, while ultimately leaving the precise market definition open, that the market for the provision of dry leasing services should be segmented according to aircraft size (seat capacity). Specifically, the Commission considered distinctions between regional aircraft (aircraft with around 30-100 seats and a range of less than 2000 nautical miles) and large commercial aircraft (aircraft with more than 100 seats and a range greater than 2000 nautical miles). With regard to large commercial aircraft, a distinction between wide- body aircraft with 200-400+ seats and narrow-body aircraft with 100-200 seats was considered. Concerning regional aircraft, the Commission considered a distinction between small regional aircraft with 30-50 seats and large regional aircraft with 70- 90+seats. (36)

(45) The exact product market definition can however be left open for the purpose of this case, since the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to dry-leasing services, under any plausible market segmentation. (37)

5.4.2. Geographic market definition

(46) The Parties consider the market to be worldwide, since most leasing companies would be active and compete with each other globally. Dry lessors could easily reach customers anywhere in the world. Aircraft delivery cost would be minimal and there would be no regulatory restrictions in terms of technical specifications that would limit the use of certain types of aircraft to a particular continent. (38)

(47) The Commission has considered in a previous case that the market for the provision of dry-leasing services is worldwide. (39)

(48) In line with its prior practice, the Commission will assess the effects of the Transaction on a worldwide market for dry-leasing services.

6. COMPETITIVE ASSESSMENT

6.1.Horizontal overlap – wet-leasing services

(49) The Parties’ activities overlap with respect to the provision of wet-leasing services.

(50) CityJet currently offers two aircraft types on its wet-lease services: the Avro RJ85 with 95 seats and the Bombardier CRJ900 with 88/90 seats. (40) Air Nostrum currently offers the following aircraft types on its wet-leases services: […]. (41)

(51) While CityJet currently operates 30 aircraft for wet-leasing services, Air Nostrum operates seven aircraft. In theory, CityJet could use up to […] aircraft for wet-leasing services, while Air Nostrum could use up to […] aircraft for wet-leasing services. (42) Air Nostrum operates most of its fleet (i.e. […] aircraft) under a franchise agreement with Iberia. (43) This agreement was signed in 1997 for an initial duration of […] years. It is automatically renewed for […] periods unless one of the parties states its will to terminate the agreement […] before the expiry of this […] period. The current agreement is valid until […]. The operation under the Iberia franchise agreement constitute the core of Air Nostrum’s business model. (44) By contrast, wet-leasing contracts are usually concluded for shorter periods, [confidential information regarding the Iberia Agreement]. In addition, the terms of the franchise agreement with Iberia require Air Nostrum to use a dedicated fleet with the Iberia livery. [confidential information regarding Air Nostrum’s fleet management] For these reasons, the Commission considers that Air Nostrum cannot rely of the […] aircraft used for the franchise operation to provide wet-leasing or bid for future tenders for wet-leasing services.

(52) The Parties’ market shares post-Transaction on every plausible market where the Parties’ activities overlap are provided in the table below.

(53) Therefore, the Transaction will give rise to affected markets with respect to (i) the supply of wet-leasing services of regional aircraft in the EEA and (ii) the sub- segmentation for wet-leasing services of large regional aircraft with a capacity between 70 and 90+ seats.

(54) However, in both of these affected markets, the combined market share post- Transaction are moderate ([20-30]% in wet-leasing of regional aircraft and [30-40]% in wet-leasing of large regional aircraft) and the increment is also moderate ([5-10]% with respect to wet-leasing of regional aircraft and [5-10]% with respect to wet- leasing of large regional aircraft).

(55) In addition, the Parties will continue to face significant competition from other established wet-leasing services providers such as NoRRA Nordic, Regional Jet and WDL/LGW, whose market share in wet-leasing services of large regional aircraft are respectively [10-20]%, [10-20]% and [10-20]%. (48)

(56) There is a significant number of wet-leasing services suppliers in the EEA (78 suppliers of wet-leasing services to third parties, in addition to approximately 20 providers of in-house wet-leasing services). (49) These suppliers of wet-leasing services can provide wet-leases across the EEA, considering that there is no regulatory barrier for EEA airlines to provide wet-leasing services in the EEA. (50)

(57) Barriers to entry into the market for wet-leasing services market and related costs are relatively low for airlines already operating scheduled, franchise or charter services, since they already possess the necessary resources for the provision of wet-leasing services. For a new airline wishing to enter the market for wet-leasing services, the barriers to entry are lower than those for entering the market for scheduled passenger air transport services, given that there is no need to have customer-facing services (e.g. sales and marketing services). In that respect, Regional Jet entered the market for wet-leasing services of regional aircraft in 2016, following the demise of Estonian Airlines, and currently provide wet-leasing services to five different airlines, operating 19 aircraft.(51)

(58) From the demand-side, there are no significant barriers to switching between wet- lessors. Switching costs seem to be low and most contracts have a limited duration (of up to 3 years). (52) Airlines can purchase wet-leasing services from approximately 78 providers of wet-leasing services in the EEA. (53) The market investigation confirmed that airlines tend to have different suppliers of wet-leasing services (54) and would have no difficulty in switching suppliers. (55)

(59) In addition, customers indicated that they consider that the Transaction is unlikely to have a negative impact on the competitive situation of the markets for wet-leasing services. (56) Some customers indicated that the impact of the Transaction might even be positive for their companies, as the Transaction might create synergies and potentially allow the merged entity to charge lower prices due to cost efficiencies. (57) Competitors indicated that generally, they do not consider that theTransaction would have a negative impact on their companies. (58) Some competitors indicated that they might have a disadvantage in case an airline launches a tender for a high number of aircraft, to which the merged entity would be the only wet-lessor able to respond. (59) However, these competitors indicated that tenders for a high number of aircraft are infrequent. (60)

(60) In light of the above considerations, the Commission concludes that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to wet-leasing services, under any plausible market definition.

6.2. Horizontal overlap – charter flight services

(61) The Parties submit that CityJet and Air Nostrum currently have very limited activities and only a couple of aircraft in use for conducting charter services. While Air Nostrum uses […] aircraft for charter services focusing on customers in Spain, CityJet’s charter flight services have largely wound down and charter flights are provided only on a very exceptional basis (a few flights per year) for [name of customer]. (61)

(62) In order to adopt a conservative approach, the Commission will consider that CityJet is active in charter flight services.

(63) If the geographic market is defined as EEA-wide, the Parties’ activities overlap on the broader market for charter flight services and the narrower market for charter flight services for private individuals and businesses (e.g. sports teams). However, the Parties’ combined market share post-Transaction will remain below [0-5]%. (62)

(64) If the geographic scope for charter flight services is defined as national, the Parties’ activities would not overlap given that CityJet is not active in charter flight services in Spain (where Air Nostrum mainly operates) or in any of the other countries where Air Nostrum is active. (63)

(65) The Transaction will therefore not result in any horizontally affected markets and is unlikely to raise competition concerns.

(66) In light of the above considerations, the Commission concludes that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to charter flight services, under any plausible market definition.

6.3. Vertical relationships – dry-leasing services

(67) Fortress Investment Group, through its subsidiary Falko, is active on the market for dry-leasing services while the JV will be active on the downstream markets for charter flights and wet-leasing services. (64)

(68) Therefore, the Transaction gives rise to potential vertical relationships between Falko’s activities in the upstream market for dry-leasing services, on the one hand, and the Parties’ activities in the downstream markets for (i) charter flight services and (ii) wet-leasing services, on the other hand.

6.3.1.Overview of Falko’s activities and market shares in dry-leasing services

(69) Falko has a fleet of […] aircraft available for dry-leasing services, focusing on regional aircraft. Its fleet comprises different regional aircraft types with a seat capacity between 50 (for Bombardier CRJ100/200 aircraft) to 118 (for the Embraer E195 aircraft). (65)

(70) Falko dry-leases […] aircraft to customers in the EEA. Approximately […] of these aircraft have a capacity between 70 and 90 seats, the remaining aircraft having a capacity between 90 and 120 seats. (66)

(71) Falko’s share in dry-leasing services worldwide is below [0-5]%. (67) Its share would be well below [5-10]% in any plausible segmentation of dry-leasing services of regional aircraft. (68)

6.3.2.Vertical relationship between the Parties’ activities in dry-leasing services and wet- leasing services

(72) As explained in section 6.1 above, the Parties’ combined share in wet-leasing services only exceeds 30% in one plausible delineation for wet-leasing services (namely wet-leasing services of large regional aircraft with a capacity of 70-90+ seats). Falko’s market share in dry-leasing services under any plausible market delineation is also well below 30%. (69)

(73) Considering that Falko’s market share in the upstream market for dry-leasing services of regional aircraft would be low (below [5-10]%), the Commission considers that the merged entity could not have the ability to restrict access to regional aircraft (input foreclosure) to airlines providing wet-leasing services in the EEA. Considering that the Parties’ market share in the downstream market for wet- leasing services of regional aircraft would be moderate (not exceeding [30-40]% under any plausible market delineation) and that numerous airlines provide wet- leasing services in the EEA, the merged entity would not represent a significant customer base for dry-leasing services of regional aircraft post-Transaction. Furthermore, Air Nostrum dry-leases [number of aircraft] from a third party dry lessor. Air Nostrum’s demand thus represents [less than 10]% of the EEA or worldwide market for dry-leased aircraft. (70) As a result, there is no risk that the merged entity will restrict access of dry-lessors to the downstream markets for wet- leasing services post-Transaction (customer foreclosure).

(74) In light of the above considerations, the Commission concludes that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to the vertical effects in the market for dry-leasing services and wet-leasing services, under any plausible market definition.

6.3.3. Vertical relationship between the Parties’ activities in dry-leasing services and franchise services

(75) The Parties’ combined share in franchise services are below 30% under any plausible market delineation. (71) Falko’s market share in dry-leasing services under any plausible market delineation is also well below 30%. (72)

(76) The Transaction will therefore not result in any vertically affected markets with respect to dry-leasing services and franchise services.

(77) In light of the above considerations, the Commission considers that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to the vertical effects in the markets for dry-leasing services and franchise services, under any plausible market definition.

6.3.4.Vertical relationship between the Parties’ activities in dry-leasing services and charter flight services

(78) As explained in section 6.2 above, the Parties’ combined share in charter flight services are below 30% under any plausible market delineation. Falko’s market share in dry-leasing services under any plausible market delineation is also well below 30%. (73)

(79) The Transaction will therefore not result in any vertically affected markets with respect to dry-leasing services and charter flight services.

(80) In light of the above considerations, the Commission considers that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to the vertical effects in the markets for dry-leasing services and charter flight services, under any plausible market definition.

6.3.5.Conclusion

(81) In light of the above considerations, the Commission concludes that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market due to the vertical links between the activities of Fortress Investment Group in the market for dry-leasing services, on the one hand, and the JV’s activities in the markets for (i) wet-leasing services, (ii) franchise services and (iii) charter flight services, on the other hand.

6.4. Vertical relationships – wet-leasing services

(82) CityJet and Air Nostrum are active in wet-leasing services, while the JV will be active on the downstream markets for franchise services and charter flights.

(83) Therefore, the Transaction gives rise to potential vertical relationships between the Parties’ activities in the upstream market for wet-leasing services, on the one hand, and the Parties’ activities in the downstream markets for (i) franchise services and (ii) charter flight services, on the other hand.

6.4.1. Vertical relationship between the Parties’ activities in wet-leasing services and franchise services

(84) As explained in section 6.1 above, the Parties’ combined share in wet-leasing services only exceeds 30% in one plausible delineation for wet-leasing services (namely wet-leasing services of large regional aircraft with a capacity of 70-90+ seats). The Parties’ combined share in franchise services are below 30% under any plausible market delineation. (74)

(85) Considering that the Parties’ combined market shares in the upstream market for wet-leasing services would be moderate (not exceeding [30-40]% under any plausible market delineation) and that numerous airlines provide wet-leasing services in the EEA, the merged entity could not have the ability to restrict access to wet- leasing services (input foreclosure) to airlines providing franchise services in the EEA. Considering that the Parties’ market share in the downstream market for franchise services would be moderate (below 30% under any plausible market delineation) and that Air Nostrum only purchases wet-leasing services to cover ad hoc specific capacity needs that may arise in the context of the Iberia franchise agreement, the merged entity would not represent a significant customer base for wet-leasing services post-Transaction. (75) As a result, there is no risk that the merged entity will restrict access of wet-lessors to the downstream markets for franchise services post-Transaction (customer foreclosure).

(86) In light of the above considerations, the Commission concludes that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to the vertical effects in the market for wet-leasing services and franchise services, under any plausible market definition.

6.4.2. Vertical relationship between the Parties’ activities in wet-leasing services and charter flight services

(87) As explained in section 6.1 above, the Parties’ combined share in wet-leasing services only exceeds 30% in one plausible delineation for wet-leasing services (namely wet-leasing services of large regional aircraft with a capacity of 70-90+ seats). As explained in section 6.2 above, the Parties’ combined share in charter flight services do not exceed [0-5]% under any plausible market delineation.

(88) Considering that the Parties’ combined market shares in the upstream market for wet-leasing services would be moderate (not exceeding [30-40]% under any plausible market delineation) and that numerous airlines provide wet-leasing services in the EEA, the merged entity could not have the ability to restrict access to wet- leasing services (input foreclosure) to airlines providing charter flight services in the EEA. Considering that the Parties’ market share in the downstream market for charter flight services are low (not exceeding [0-5]%) and that numerous airlines provide charter flight services in the EEA, the merged entity would not represent a significant customer base for wet-leasing services post-Transaction. (76) As a result, there is no risk that the merged entity will restrict access of wet-lessors to the downstream markets for charter flight services post-Transaction (customer foreclosure).

(89) In light of the above considerations, the Commission concludes that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market in relation to the vertical effects in the market for wet-leasing services and charter flight services, under any plausible market definition.

6.4.3. Conclusion

(90) In light of the above considerations, the Commission concludes that the Transaction is unlikely to raise serious doubts as to its compatibility with the internal market due to the vertical links between the activities of the Parties in the market for wet-leasing services, on the one hand, and the JV’s activities in the market for (i) franchise services and (ii) charter services, on the other hand.

7. CONCLUSION

(91) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 OJ L 24, 29.1.2004, p. 1 (the ‘Merger Regulation’).

4 CityJet Holdings Ltd. is owned by three natural persons. [Information on strategic decision making rights and economic activities of the relevant individuals] he is not considered to be a natural person controlling CityJet in accordance with paragraph 12 CJN.

5 Air Nostrum has several shareholders. Mr Carlos Bertomeu holds both individually and through Air Investment Valencia 58,71% of Air Nostrum’s shares. Carlos Bertomeu, through Air Investment Valencia, solely controls Air Nostrum (Form CO, paragraph 33).

6 This decision is without prejudice to any potential future state aid enquiry into financing of Air Nostrum’s aircraft.

7 Post-Transaction, CityJet Holdings will either cease to exist or it may continue to be used as a holding company under the indirect ownership of Fortress; in any case, it will not be jointly controlling the JV.

8 Form CO, paragraph 105.

9 Case M.9287 – Connect Airways/Flybe, paragraph 211-213 (to be published).

10 In decisions related to scheduled air transport services, the Commission considered, while ultimately leaving the question open, that charter flights were not part of the same market as scheduled flights (see e.g. cases M.8869 – Ryanair/Laudamotion, paragraph 154; M.6447 – IAG/bmi, paragraph 74).

11 Form CO, paragraph 57 et seq. and 76.

12 Form CO, paragraph 59 et seq.

13 See agreed non-confidential minutes of a conference call of 28 June 2019 with a competitor; agreed non- confidential minutes of a conference call of 8 July 2019 with a competitor; agreed non-confidential minutes of a conference call of 12 July 2019 with a competitor; agreed non-confidential minutes of a conference call of 20 June with a customer; agreed non-confidential minutes of a conference call of 26 June with a customer; agreed non-confidential minutes of a conference call of 1 July with a customer; agreed non-confidential minutes of a conference call of 2 July with a customer.

14 See sections 6.1, 6.3.2, 6.3.5 and 6.3.6 below.

15 Case M.9287 – Connect Airways/Flybe, paragraph 223 (to be published).

16 Reply to RFI 1 of 10 July 2019, question 3.

17 Case M.9287 – Connect Airways/Flybe, paragraph 229 (to be published).

18 Form CO, paragraph 152.

19 See agreed non-confidential minutes of a conference call of 20 June with a customer, paragraph 7; agreed non-confidential minutes of a conference call of 26 June with a customer, paragraph 5; agreed non- confidential minutes of a conference call of 1 July with a customer, paragraph 5; agreed non-confidential minutes of a conference call of 2 July with a customer, paragraph 10.

20 See sections 6.1, 6.3.2 and 6.4 below.

21 Form CO, paragraph 96.

22 Case M.9287 – Connect Airways/Flybe, paragraph 232 (to be published).

23 See agreed non-confidential minutes of a conference call of 28 June 2019 with a competitor, paragraph 6 and agreed non-confidential minutes of a conference call of 8 July 2019 with a competitor, paragraph 6.

24 See agreed non-confidential minutes of a conference call of 1 July with a customer, paragraph 5 and agreed non-confidential minutes of a conference call of 2 July with a customer, paragraph 10.

25 See sections 6.1, 6.3.2 and 6.4 below.

26 See e.g. Case M.8046 – TUI/Transat France, paragraph 73.

27 Form CO, paragraph 95.

28 See sections 6.2, 6.3.3 and 6.4.2 below.

29 Form CO, paragraph 100.

30 See e.g. Case M.8046 – TUI/Transat France, paragraph 88.

31 Form CO, paragraph 100.

32 See agreed non-confidential minutes of a conference call of 12 July with a competitor, paragraph 10.

33 See sections 6.2, 6.3.3 and 6.4.2 below.

34 Case M.9287 – Connect Airways/Flybe, paragraph 233 (to be published).

35 Case M.9287 – Connect Airways/Flybe, paragraph 235 (to be published).

36 Case M.9287 – Connect Airways/Flybe, paragraphs 215-219 (to be published).

37 See sections 6.3 below.

38 Form CO, paragraph 99.

39 Case M.9287 – Connect Airways/Flybe, paragraph 221 (to be published).

40 Form CO, paragraph 179.

41 Form CO, paragraphs 150 and 185.

42 Form CO, paragraph 164.

43 As indicated in paragraphs 3 and 4 above, CityJet and Air Nostrum have a fleet of respectively 35 and approximately 50 aircraft. The Parties submit that the number of CityJet’s aircraft available for wet- leasing operations corresponds to its total fleet minus some backup aircraft necessary to guarantee CityJet’s overall operations. The number of Air Nostrum’s aircraft available for wet-leasing services corresponds to its total fleet minus the aircraft necessary for the Iberia franchise operations, its charter flights operation and backup aircraft necessary to guarantee Air Nostrum’s operations (Form CO, paragraph 164).

44 In 2017, […]% of Air Nostrum’s revenues were generated through the franchise agreement with Iberia (email of the Parties dated 16 July 2019).

45 The Parties submitted that they do not have reliable market data on the number of competitors’ aircraft available for wet-leasing services. On a conservative basis, the Parties’ market shares are calculated based on their own total number of aircraft available to use for wet-leasing services, while the size of the market is determined based on the number of aircraft actually used for wet-leasing services. The Parties’ market shares would necessarily be lower, if the size of the market was based on the number of aircraft available for wet-leasing services (Form CO, paragraphs 162 et seq). The Parties’ available capacity takes account of their potential future plans to lease/acquire aircraft (reply to RFI 4 of 16 July 2019).

46 Mediterranean Aviation Operations Company, Ltd. (“Medops”) is an airline jointly controlled by Air Investment Valencia active in the operation of air routes between Europe and Africa. Medops is focused on providing air transportation services to gas and oil companies, corporate clients and humanitarian organizations, mainly through charter flight and wet-lease services. In particular, Medops provides wet- lease services third parties (3 aircraft) (Form CO, footnote 2).

47 The Parties have provided market shares based on data from ch-aviation database retrieved on 29 May 2019 and 12 July 2019.

48 Reply to RFI 1, question 5.

49 Form CO, paragraph 193.

50 Form CO, paragraph 194.

51 Form CO, paragraph 205.

52 Form CO, paragraphs 199 and 212.

53 Form CO, paragraph 193.

54 See agreed non-confidential minutes of a conference call of 26 June with a customer, paragraph 2; agreed non-confidential minutes of a conference call of 2 July with a customer, paragraph 2; agreed non- confidential minutes of a conference call of 28 June 2019 with a competitor, paragraph 10.

55 See agreed non-confidential minutes of a conference call of 1 July with a customer, paragraph 8.

56 See agreed non-confidential minutes of a conference call of 20 June with a customer, paragraph 10; agreed non-confidential minutes of a conference call of 26 June with a customer, paragraph 9; agreed non- confidential minutes of a conference call of 1 July with a customer, paragraph 7; agreed non-confidential minutes of a conference call of 2 July with a customer, paragraph 15.

57 See agreed non-confidential minutes of a conference call of 1 July with a customer, paragraph 7; agreed non-confidential minutes of a conference call of 2 July with a customer, paragraph 14.

58 See agreed non-confidential minutes of a conference call of 8 July 2019 with a competitor, paragraph 8; agreed non-confidential minutes of a conference call of 28 June 2019 with a competitor, paragraph 10.

59 See agreed non-confidential minutes of a conference call of 8 July 2019 with a competitor, paragraph 8; agreed non-confidential minutes of a conference call of 12 July with a competitor, paragraph 11.

60 See agreed non-confidential minutes of a conference call of 8 July 2019 with a competitor, paragraph 8.

61 [Further information on customer and the routes flown]. Form CO, paragraph 105 and reply to RFI 1 of 10 July 2019, question 1.

62 Form CO, paragraph 105 and reply to RFI 2 of 11 July 2019, question 2. Based on the Parties’ estimates, approximately 288 airlines provide charter flight services, using 5,469 aircraft. Air Nostrum only uses a couple of aircraft for charter flight services. The Parties’ are unable to provide estimates of their market shares with respect to the sub-segment for charter flight services to private individuals and businesses. In any event, the combined market share and the increment would be very limited.

63 Form CO, paragraph 106 and reply to RFI 2 of 11 July 2019, question 2. For the sake of completeness, the Parties confirmed that there would be no overlap on a route-by-route basis.

64 For the sake of completeness, the Parties indicated that Air Investment Valencia subsidiary Saimer provides dry leasing services to other Air Investment Valencia subsidiaries (Form CO, paragraph 222).

65 Form CO, paragraph 109 et seq. and reply to RFI 1 of 10 July 2019, question 2 and reply to RFI 2 of 11 July 2019, question 1.

66 Form CO, paragraph 105 and reply to RFI 2 of 11 July 2019, question 2.

67 Form CO, paragraph 109.

68 Replies to QP 1 of 8 February 2019, question 8 and RFI 2 of 11 July 2019, question 1. The Parties indicated that Falko’s share in dry-leasing aircraft with a size between 70 and 90+ seats would be below [5-10]% in a geographic market defined as EEA-wide. The Parties submitted that Falko’s share in the worldwide market is necessarily lower.

69 Form CO, paragraph 109 and reply to RFI 2 of 11 July 2019, question 1.

70 Form CO, paragraph 110.

71 Reply to RFI 3 of 15 July 2019, question 2.

72 Form CO, paragraph 109 and reply to RFI 2 of 11 July 2019, question 1.

73 Form CO, paragraph 109 and reply to RFI 2 of 11 July 2019, question 1.

74 Reply to RFI 3 of 15 July 2019, question 2.

75 See email of the Parties dated18 July 2019. In addition, customers of wet-leasing services are not confined to airlines providing franchise services, but also airlines providing scheduled passenger air transport and charter flight services.

76 In addition, customers of wet-leasing services are not confined to airlines providing charter flight services, but also airlines providing scheduled passenger air transport and wet-leasing services.