Commission, August 29, 2019, No M.9418

EUROPEAN COMMISSION

Judgment

TEMASEK / RRJ MASTER FUND III / GATEGROUP

Subject: Case M.9418 — Temasek/RRJ Master Fund III/Gategroup

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 24 July 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Temasek Holdings (Private) Limited (‘Temasek’) (Singapore) and RRJ Master Fund III, belonging to the group of RRJ Capital (‘RRJ’) (Hong Kong) acquire within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation joint control of gategroup Holding AG (‘Gategroup’) (Switzerland), currently solely controlled by RRJ Capital. (3) Temasek and RRJ Master Fund III are collectively referred to as the ‘Parties.’

1. THE PARTIES

(2) Temasek is an investment company headquartered in Singapore. Temasek has significant shareholdings in two businesses in related markets to Gategroup: SATS and Singapore Airlines. SATS is principally active in ground handling, cargo handling, in-flight catering and the provision of other in-flight services to airlines and is primarily active in the Asia Pacific region, it is not active in the EEA. Temasek also holds a [50-60]% controlling shareholding in Singapore Airlines. Within the EEA, Singapore Airlines offers air transport services, including passenger and freight transport, to airports in Belgium, Denmark, France, Germany, Greece, Italy, the Netherlands, Spain, Sweden, and the United Kingdom.

(3) RRJ is an investment firm based in Hong Kong and Singapore. RRJ undertakes private equity investments in Asia and primarily focuses on growth capital and state- owned enterprises investments. RRJ’s interest in Gategroup is held indirectly by its RRJ Capital Master Fund III.

(4) Gategroup is headquartered in Switzerland and operates in around 60 countries globally, including in contracting countries to the EEA Agreement. It provides various airport and in-flight food and hospitality solutions. Gategroup’s main activities consist of in-flight catering and retail on-board services which it provides primarily through its Gate Gourmet, Servair, gateretail, and Dutyfly brands. (4)

2. THE OPERATION

(5) The notified concentration consists of the acquisition of joint control by Temasek and RRJ of Gategroup, which is currently solely controlled by RRJ (the ‘Transaction’).

(6) More specifically, Temasek intends to acquire 50% of Gategroup’s voting shares from RRJ (which currently controls the entire 100% shareholding of Gategroup) through two instruments. [Information on the transaction structure]. (5) [Information on the transaction structure].

(7) The Transaction will therefore result in Temasek’s acquisition of 50% of Gategroup’s voting shares. Post-Transaction, RRJ will continue to own the remaining 50% of Gategroup’s voting shares.

2.1. Joint control

(8) Temasek and RRJ have undertaken to enter into a Shareholders’ Agreement that will govern the exercise of their interests in Gategroup. [Information on negotiations between Temasek and RRJ]. (6) Specifically, each of Temasek and RRJ is expected to have the following rights.

(9) [Information on the composition of the Gategroup board]. (7) [Information on the composition of the Gategroup board]. (8)

(10) Any decision by the Gategroup board involving a “reserved matter” will require the affirmative vote of one Temasek director and one RRJ director. (9) Reserved matters include, inter alia, the approval and amendment of Gategroup’s business plan and annual budget. (10)

(11) These rights will therefore enable each of Temasek and RRJ to veto decisions which would be essential for the strategic commercial behaviour of Gategroup, including its business plan, budget and the appointment of senior management. Consequently, the Transaction would result in Temasek and RRJ obtaining joint control over Gategroup.

2.2. Full functionality

(12) Following the Transaction, Gategroup would perform all the functions of an autonomous undertaking on a lasting basis.

(13) First, Gategroup would have sufficient resources to operate independently. Gategroup has its own dedicated management and employs over 43,000 personnel. It has assets in excess of EUR 2 500 million, focused around catering facilities that serve airlines at over 200 airports worldwide.

(14) Second, it has activities beyond one specific function for its parent companies. Gategroup is responsible for all operations, sales, and purchases for its in-flight catering, retail on-board, and ancillary activities.

(15) Finally, Gategroup provides services to customers (especially airlines) that are independent of RRJ and Temasek (just ca [0-5]% of Gategroup’s revenues come from sales to Singapore Airlines).

(16) Therefore, the Transaction would result in a concentration within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation.

3. EU DIMENSION

(17) In 2018, the undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (11) [Temasek: EUR […] million, RRJ (excluding the turnover of Gategroup): EUR […] million, Gategroup: EUR 4 277 million]. Each of them has an EU-wide turnover in excess of EUR 250 million, but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. MARKET DEFINITION

(18) Gategroup mainly provides in-flight catering and retail on-board services. Temasek, through its majority shareholding in Singapore Airlines, is active in the downstream market for passenger air transport services.

(19) There are, therefore, no horizontal overlaps but vertical links between the activities of Singapore Airlines and the services provided by Gategroup to its customers.

4.1. Upstream market: In-flight catering services

(20) In-flight catering comprises the provision and delivery of food and beverage solutions to airlines, which will be served to passengers on an aircraft during the flight.

4.1.1. Relevant product market

(21) The Parties submit that the relevant product market is in-flight catering as a whole and argue that a segmentation between types of flight or meals is not warranted. (12) They also submit that the exact product market definition can be left open for the purposes of the Transaction, as no competitive concerns arise under any plausible market definition.

(22) In previous cases, the Commission concluded that the relevant product market for in- flight catering comprises the entire range of meals (economy/business/first class) for all types of flights (short-haul/long-haul). (13) The Commission left open whether a distinction should be made as between “traditional” (i.e., airline catering companies that provide the entire range of required meals to meet the different needs of airline companies) and “non-traditional” (i.e., catering companies or other food products suppliers that formally act as suppliers to “traditional” caterers, but also negotiate directly with airlines on quality and price suppliers) catering suppliers. (14)

(23) In line with the Commission’s past decisional practice, the Commission concludes that, for the purposes of assessing the Transaction, the relevant product market for in-flight catering comprises the entire range of meals for all types of flights. As regards a possible segmentation of in-flight catering by a type of catering supplier, it can be left open whether the market for in-flight catering should be segmented between “traditional” and “non-traditional” catering suppliers, since the Transaction would not raise any serious doubts irrespective of the exact product market definition.

4.1.2. Relevant geographic market

(24) The Parties submit that the geographic scope of in-flight catering services is likely to be limited to the local region around an airport. They have provided market share estimates based on the narrowest plausible geographic market, (i.e., the level of individual airports). They also submit that the exact geographic market definition can be left open for the purposes of the Transaction, as no competitive concerns arise under any plausible market definition.

(25) In its most recent case, the Commission concluded that the geographic market for in- flight catering services comprised of at most an airport region. (15) In that case the market investigation found that in-flight catering contracts were agreed either on an airport-by-airport basis, or a catchment area covering multiple airports. Competition between in-flight catering service providers was found to take place at airport level. (16)

(26) In line with the Commission’s past decisional practice, the geographic market for in- flight catering comprises at most a relevant airport region. Nevertheless, for the purposes of the present case, the precise geographic scope of the in-flight catering market can be left open, as the Transaction would not raise any serious doubts irrespective of the exact geographic market definition.

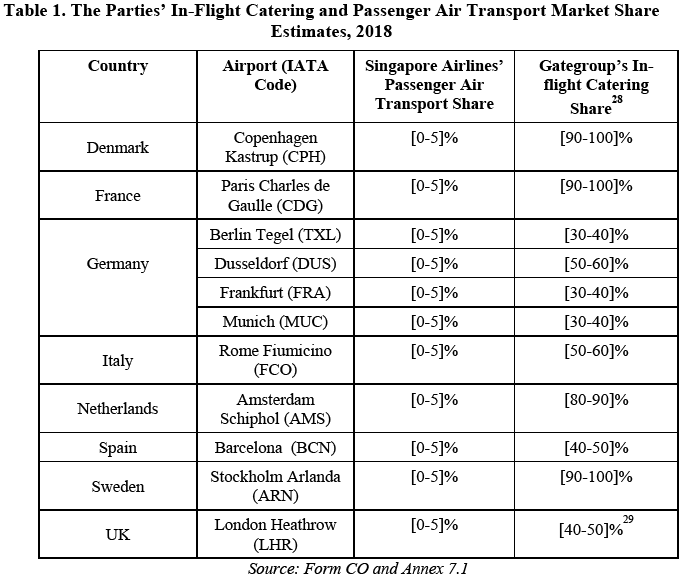

4.2. Upstream market: Retail on-board services

(27) Retail on-board services comprise the provision of shopping services that are made available to passengers during the flight, such as snacks (food and beverages) and duty free goods.

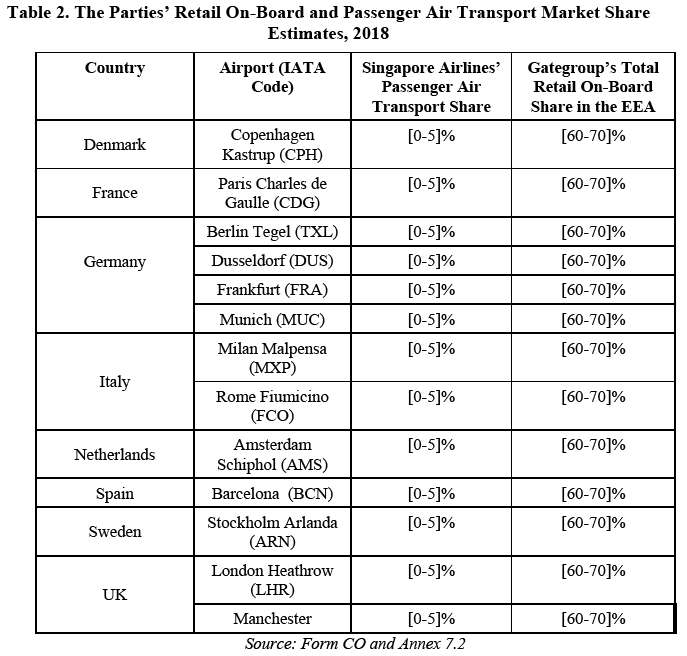

4.2.1. Relevant product market

(28) The Parties refer to the Commission’s past decisional practice, noting that the Commission had considered a separate product market for the provision of third- party retail on-board services. They also submit that the exact product market definition can be left open for the purposes of the Transaction, as no competitive concerns arise under any plausible market definition. (17) The Parties have however provided market share information on the basis of the narrowest plausible product market definition, i.e., retail on-board services segmented into snacks and duty free products.

(29) In previous cases, the Commission considered whether there was a stand-alone market for the provision of third-party retail on-board services, distinct from in-flight catering services and excluding airlines’ own in-house sourcing of retail on-board products. The Commission, has, however, left open the question whether the market may be further segmented into markets for snacks (i.e., the on-board sale of food and beverage products) and duty free products (i.e., the on-board sale of cigarettes, alcohol, perfumes, and other items). (18)

(30) In line with the Commission’s past decisional practice, the Commission concludes that, for the purposes of assessing the Transaction, the market for the provision of retail on-board services is separate from the market for the provision of in-flight catering services. As regards a possible segmentation of retail on-board services by type of product, it can be left open whether the market for retail on-board services comprises both snacking (food and beverage) and duty free products, since the Transaction does not raise any serious doubts irrespective of the exact product market definition.

4.2.2. Relevant geographic market

(31) The Parties provide market share estimates on an EEA-wide basis as the narrowest plausible geographic market. (19) They also submit that the exact geographic market definition can be left open for the purposes of the Transaction, as no competitive concerns arise under any plausible market definition.

(32) In previous cases, the Commission has concluded that the geographic market for retail on-board services is at least EEA-wide, if not global. (20)

(33) In line with the Commission’s past decisional practice, the geographic market for retail on-board services is at least EEA-wide. Nevertheless, for the purposes of the present case, the precise geographic scope of the retail on-board market can be left open, since the Transaction does not raise any serious doubts irrespective of the exact geographic market definition.

4.3. Downstream market: Passenger air transport services

4.3.1. Relevant product market

(34) The Parties refer to the Commission’s past decisional practice, noting that the Commission has defined one overall market for passenger air transport services, when assessing vertical relationships. (21) The Parties argue that this reflects the reality that an airline’s demand for in-flight catering or retail on-board services is a function of total passenger numbers, irrespective of the time-sensitivity of those passengers and their readiness to travel on indirect flights.

(35) In previous vertical cases, the Commission considered that there is an overall market for passenger air transport services, but left open whether this market for passenger air transport services might be further sub-segmented into scheduled and charter flights or into “time-sensitive” and “non-time-sensitive” passengers. (22)

(36) In line with the Commission’s past decisional practice, the Commission concludes that the relevant product market for the purposes of assessing the Transaction is an overall market for passenger air transport services. As regards a possible segmentation of passenger air transport services, it can be left open whether the market for passenger air transport services should be further segmented into scheduled and charter flights or “time-sensitive” and “non-time-sensitive” passengers, since the Transaction does not raise any serious doubts irrespective of the exact product market definition.

4.3.2. Relevant geographic market

(37) The Parties submit that the most appropriate geographic market definition for the assessment of the vertical relationship between Singapore Airlines’ passenger air transport services and Gategroup’s upstream services is an airport-by-airport approach. (23) The Parties provide market share estimates on this basis.

(38) In previous cases involving a vertical relationship between in-flight catering and retail on-board services on the one hand and passenger air transport services on the other hand, the Commission found that airlines procure in-flight catering and retail on-board services on an airport-by-airport basis and not on a route-by-route basis. Therefore, it was considered necessary to look at the market share of the particular airline into the total demand for in-flight catering services and retail on-board services at the relevant airports instead of making a route-by-route assessment. (24)

(39) In line with the Commission’s past decisional practice, the geographic market for the provision of passenger air transport services in this case comprises every route combination between a given point-of-origin airport and a point-of-destination airport. Nevertheless, for the purposes of the present case, the precise geographic scope of the passenger air transport services market can be left open, since the Transaction does not raise any serious doubts irrespective of the exact geographic market definition.

5. COMPETITIVE ASSESSMENT

(40) The Transaction does not lead to any horizontally affected markets. (25) However, it gives rise to a number of vertically affected markets in the EEA. More specifically, the Transaction leads to vertically affected markets arising from Gategroup’s supply of in-flight catering upstream and Temasek’s provision of passenger air transport services (via its portfolio company Singapore Airlines) at 11 airports in the EEA. (26)

(41) The Transaction also leads to a vertically affected market between Gategroup’s provision of retail on-board services upstream and passenger air transport services by Temasek downstream (via its portfolio company Singapore Airlines) in the EEA.- (27)

5.1. Market shares

5.1.1. In-flight catering services

(42) The Transaction gives rise to vertically affected markets due to Gategroup’s significant presence in the upstream markets for in-flight catering at a number of major European airports, with market shares ranging from [30-40]% (at Munich (MUC)) to [90-100]% and [90-100]% (at Stockholm Arlanda (ARN) and Copenhagen Kastrup (CHP) respectively), excluding captive sales. However, in all of these vertically affected markets, Singapore Airlines’ market share on the downstream market for passenger air transport services is very low (between [0-5]% and [0-5]%).

(43) More specifically, on the basis of the Parties’ submission, the Transaction gives rise to vertically affected markets for in-flight catering at the following airports in the EEA:

5.1.2. Retail on-board services

(44) The Transaction gives rise to a vertically affected market due to Gategroup’s significant presence on the upstream market for retail on-board services in the EEA. In 2018, Gategroup’s combined market share for its gateretail and Dutyfly brands accounts for approximately [60-70]% on the EEA-wide level. (30)

(45) On a potential narrower market for retail on-board services of snacking, Gategroup’s market share in 2018 amounts to [70-80]% in the EEA. Gategroup’s market share on a potential narrower market for retail on-board services of duty free services in 2018 is [50-60]% in the EEA.

(46) However, as indicated in Table 2 below, in each of the EEA airports where the Parties’ activities overlap, Singapore Airlines’ market share is very low (between [0-5]% and [0-5]%).

5.2. The Parties’ arguments

(47) The Parties submit that the vertical relationships brought about by the Transaction will not lead to input or customer foreclosure for in-flight catering and retail on- board services in the EEA due to the following reasons.

(48) First, Gategroup is only jointly-controlled by Temasek (i.e., the controlling shareholder in Singapore Airlines). The other parent company of Gategroup, RRJ, would not benefit from any input foreclosure strategy and therefore would be likely to block any foreclosure strategy. In addition, given Singapore Airlines’ de minimis presence at all affected airports, any putative input foreclosure strategy would inevitably result in a significant reduction in sales for Gategroup.

(49) Second, there is no commercial rationale for Gategroup to engage in a foreclosure strategy. Gategroup’s business at affected European airports accounts for a small fraction of its overall global business with its airline customers. Any deterioration in price and quality for the European airport contracts would undermine Gategroup’s commercial reputation and could put at risk the entire global relationship.

(50) Third, Gategroup will continue to face significant competition in the supply of in- flight catering, retail on-board, and other related services at all affected airports. The competitive landscape of the affected markets is driven by a competitive procurement process with a number of credible bidders. This will ensure that all future bidding contests remain competitive, while prices under existing contracts remain determined by the competitive parameters of previous bidding contests.

(51) Last, airline customers are sophisticated buyers with significant countervailing power. They are likely to respond to any attempted foreclosure strategy by switching to another supplier and/or make use of “return catering” arrangements, i.e., sourcing meals for both legs of a route at a single airport.

5.3. The Commission’s assessment

5.3.1. Input foreclosure

(52) According to the Non-Horizontal Merger Guidelines, (31) foreclosure occurs when actual or potential rivals’ access to supplies or markets is restricted, thereby reducing those companies’ ability and/or incentive to compete. Such foreclosure may discourage entry or expansion of rivals or encourage their exit. (32)

(53) In order for input foreclosure to be a concern, three conditions need to be met post- merger: (i) the merged entity needs to have the ability to foreclose access to inputs; (33) (ii) the merged entity needs to have the incentive to do so; (34) and (iii) the foreclosure strategy needs to have a likely significant detrimental effect on competition on the downstream market. (35)

5.3.1.1. In-flight catering services

(54) The Commission assessed the vertical relationships between the Parties’ activities in in-flight catering and passenger air transport services and considers that post- Transaction, Gategroup would not have the ability or incentive to foreclose airlines competing with Singapore Airlines downstream from in-flight catering.

(55) First, while Gategroup’s upstream market share is high ranging from [30-40]% (at Munich (MUC)) to [90-100]% (at Paris Charles de Gaulle (CDG)) and [90-100]% (at Copenhagen Kastrup (CPH)), (36) in-flight catering cannot be considered an important input for the downstream market for passenger air transport services. As demonstrated by the Commission’s market investigation, in-flight catering services account for a very low proportion (on average around 5%) of the total costs of providing passenger air transport services. (37) It is also ancillary to the core service of providing passenger air transport services.

(56) Second, the majority of respondents to the Commission’s market investigation were of the view that it is not likely that Gategroup will restrict access to or increase prices of its in-flight catering services as this would have a detrimental effect on its position and encourage customers to switch to other service providers. (38) Indeed, one market participant responding to the Commission’s market investigation noted that due to their global footprint large airlines are able to leverage their buyer power and negotiate certain discounts. (39)

(57) At the same time, the Commission’s market investigation showed that an airline’s current in-flight catering provider may have an advantage compared to competing players due to, for example, its knowledge of the airline’s service needs and preferences. This may reduce the airlines’ willingness to switch to other in-flight catering providers. Indeed, some respondents considered that potential delays related to getting accustomed with the internal procedures of the airline, staff training, logistics costs associated with the change of a supplier might limit the possibilities of switching. (40) On the other hand, more than half of the airlines responding to the Commission’s market investigation confirmed that they had switched their in-flight catering provider at least once in the last five years. (41) However, as noted by a market respondent, changing in-flight catering suppliers at the hubs is much more difficult, because “the requirements to tender and change suppliers are higher” (42) and that typically the existing supplier is “the only [one] having enough capacity to fulfil all needs of the customer without having to build any additional infrastructure [whereas] other suppliers […] will have to invest in new buildings, equipment and hire hundreds of people”. (43) On balance, the Commission considers that if Gategroup restricted access to or increased prices of its in-flight catering services post- Transaction, customers would have some alternatives for in-flight catering services from other competing providers such as LSG Sky Chefs or smaller players such as DO & CO or Newrest (see paragraph (59) below).

(58) Third, Gategroup will have a limited ability to negatively affect market prices and conditions to customers post-Transaction due to the bidding type of in-flight catering market. Indeed, airlines typically select their suppliers at airports based on a regular competitive tender process in which they invite as many suppliers as can potentially respond. (44) The in-flight catering contracts are typically concluded on average for a period of 2 to 5 years with extension and termination possibilities. (45) In order to remain competitive, Gategroup will have to maintain competitive price/quality of its services. Such market dynamics also makes it unlikely for Gategroup to increase prices or reduce service quality of in-flight catering services despite its considerable shares at a given airport and will constrain Gategroup’s ability to affect market prices and conditions.

(59) Last, while Gategroup is the largest in-flight catering provider in the EEA having by far the highest market share in the majority of the affected airports in the EEA, (46) it will continue to face competition from a number of in-flight catering providers, in particular from the second largest provider LSG Sky Chefs that is active in 7 out 11 affected airports in the EEA (47) with a market share estimate ranging from [5-10]% (at Amsterdam Schiphol (AMS)) to [40-50]% (at Berlin Tegel (TXL)) and [40-50]% (at Frankfurt (FRA)). (48) Other competitors include smaller in-flight catering providers such as Newrest (active in 4 out 11 affected airports in the EEA) (49) and DO & CO (active in 5 out of 11 affected airports in the EEA) (50) as well as other suppliers.

(60) In terms of new market entry, the Commission’s market investigation showed that there exist a number of barriers to entry in the market for in-flight catering related to the logistics set up and required investment in infrastructure and equipment. (51) For instance, one market participant noted that “[t]he in-flight catering services are dominated by a few big payers covering […] many airports and only some few minor players” (52) adding that “due to large investments to enter the market not many new entrants are seen”. (53) Nevertheless, in recent years there have been some instances of smaller players expanding their footprint at various airports in the EEA. For example, DO & CO has expanded in London Heathrow (LHR), (54) while Newrest has sought to expand to new locations in the EEA. (55) Also, Inflight International Logistics started operations in 2015 in the Nordic region (56) and a new player has started operations at Copenhagen Kastrup recently. (57)

(61) The Commission therefore considers that it is unlikely that Gategroup could engage in an input foreclosure strategy in in-flight catering post-Transaction.

5.3.1.2. Retail on-board services

(62) Post-Transaction, the Parties will have an EEA-wide combined market share of [60-70]% in the upstream market for retail on-board services (and [70-80]% on a potential market for snacking only, and [50-60]% for a potential market for duty free only). The respondents to the Commission’s market investigation noted that there were limited providers in this market, noting for example that there were “only 3 significant suppliers Gate Retail and Retail in Motion, which both together have more than 70% of the market, and Tourvest.” (58) A majority of respondents also indicated that switching to other providers was difficult, (59) noting for example that “the business model is very integrated into the airlines operation and daily business” (60) and while there are “many suppliers of logistics services […] last mile suppliers within the restricted safety areas in an airport are limited due safety issues.” (61) However, on the downstream market, Singapore Airlines’ market share however is very low, ranging from [0-5]% to [0-5]%.

(63) The Commission considers that Gategroup would not therefore have the ability or incentive to foreclose airlines competing with Singapore Airlines downstream from retail on-board services.

(64) In particular, while Gategroup’s upstream market share is high ([60-70]% and [70-80]% for snacking and [50-60]% for duty free), retail on-board services cannot be considered an important input for the downstream market for passenger air transport services. For example, retail on-board services accounts for a very low proportion (less than 5%) of total costs of providing passenger air transport services. (62) It is also ancillary to the core service of providing air transport services.

(65) Furthermore, all market participants who responded to the market investigation indicated that, in their view, Gategroup would not have an incentive to pursue an input foreclosure strategy. (63) The Commission’s market investigation showed that post-Transaction, any attempt to foreclose competitors downstream would result in loss of sales for Gategroup, but that it would not result in a corresponding diversion of demand to Singapore Airlines due to the fact that, as noted by a market participant, “on-board retail part not decisive” (64) and would not therefore be profitable. The same market participant does however go on to note that “[l]ogistics at the airport is [a] bottleneck.” (65)

(66) In addition, Gategroup is jointly controlled by Temasek and RRJ. Any input foreclosure strategy would entail loss of sales for Gategroup. RRJ, which is not active in the downstream passenger air transport services market, would not benefit from this strategy and it would be in RRJ’s economic interest to block it. (66) The Commission does not therefore consider that it is not likely that the Transaction will lead to increased prices in the downstream market for passenger air transport services. (67)

(67) The Commission therefore considers that it is unlikely that Gategroup could engage in an input foreclosure strategy in retail on-board services (or in retail on-board snacking, or retail on-board duty free) post-Transaction.

5.3.2. Customer foreclosure

(68) According to the Non-Horizontal Merger Guidelines, customer foreclosure may occur when a supplier integrates with an important customer in the downstream market. (68)

(69) The Non-Horizontal Merger Guidelines acknowledge that customer foreclosure may be of concern if a vertical merger involves a company that is an important customer with a significant degree of market power in the downstream market, as only then does an integrated firm have a potential ability to foreclose access to a sufficient customer base. No such concerns arise, however, where a sufficiently large customer base is likely to turn to alternative suppliers, as this would provide upstream competitors with sufficient economic alternatives. (69)

5.3.2.1. In-flight catering services

(70) The Commission assessed the vertical relationships between the Parties’ activities in in-flight catering and passenger air transport services and considers that Gategroup would not have the ability or incentive to foreclose access of Gategroup’s competitors to Singapore Airlines’ demand of in-flight catering services.

(71) First, while Gategroup’s in-flight catering market share exceeds 30% at 11 European airports (namely, Copenhagen Kastrup (CPH), Paris Charles de Gaulle (CDG), Berlin Tegel (TXL), Dusseldorf (DUS), Frankfurt (FRA), Munich (MUC), Rome Fiumicino (FCO), Amsterdam Schiphol (AMS), Barcelona (BCN), Stockholm Arlanda (ARN), and London Heathrow (LHR)), Singapore Airlines’ downstream share on the market for passenger air transport services at all of these airports is very low, ranging between [0-5]% and [0-5]%. Given the de minimis market share of Singapore Airlines at the affected airports, it cannot be considered an “important customer” within the meaning of the Commission’s Non-Horizontal Guidelines. (70) Even if Singapore Airlines were to purchase its in-flight catering services exclusively from Gategroup, the overwhelming majority of customer demand for in- flight catering services at any given airport would remain available to other upstream in-flight catering suppliers, providing them with sufficient alternatives to avoid being foreclosed. (71)

(72) Second, neither the market investigation nor the evidence submitted by the Parties provide strong indication that post-Transaction Gategroup would have the incentive to engage in customer foreclosure. Indeed, any such strategy would be unsuitable to increase the costs of its upstream competitors. The Commission considers that following the Transaction, the upstream suppliers will continue to have economic alternatives to avoid being foreclosed.

(73) The Commission therefore considers that it is unlikely that Gategroup could engage in a customer foreclosure strategy in in-flight catering post-Transaction.

5.3.2.2. Retail on-board services

(74) As noted above in Section 5.3.2.1, based on the Parties’ estimates, Singapore Airlines has a very low downstream share on the market for passenger air transport services at all of these airports is very low, ranging between [0-5]% and [0-5]%. Given the de minimis market share of Singapore Airlines at the affected airports, it cannot be considered an “important customer” within the meaning of the Commission’s Non-Horizontal Guidelines. (72) Even if Singapore Airlines were to purchase its demand of retail on-board services exclusively from Gategroup, the overwhelming majority of customer demand for such services at any given airport would remain available to other upstream suppliers of retail on-board services, providing them with sufficient alternatives to avoid being foreclosed. (73)

(75) The Commission therefore considers that it is unlikely that Gategroup could engage in a customer foreclosure strategy in retail on-board services (or in retail on-board snacking, or retail on-board duty free) post-Transaction.

5.4. Conclusion on competitive assessment

(76) In light of the outcome of the market investigation and the evidence submitted by the Parties, the Commission concludes that it is unlikely that the combined entity could engage in either an input or customer foreclosure strategy post-Transaction.

(77) The Commission therefore concludes that the Transaction does not raise serious doubts about its compatibility with the internal market or the functioning of the EEA Agreement as regards its impact on competition for the markets for in-flight catering in Copenhagen Kastrup (CPH), Paris Charles de Gaulle (CDG), Berlin Tegel (TXL), Dusseldorf (DUS), Frankfurt (FRA), Munich (MUC), Rome Fiumicino (FCO), Amsterdam Schiphol (AMS), Barcelona (BCN), Stockholm Arlanda (ARN), and London Heathrow (LHR) airports and on retail on-board services (and in retail on- board snacking, or retail on-board duty free) in the EEA on the basis of vertical effects.

6. CONCLUSION

(78) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C 257, 31.07.2019, p. 17.

4 In addition, Gategroup is active in in-flight catering equipment, airport lounge services, and to a more limited extent in airport retail and contract catering services.

5 [Information on the transaction structure] RRJ acquired 100% of Gategroup’s share capital from HNA on April 3, 2019. See Gategroup’s press release on April 3, 2019, available at: https://www.gategroup.om/en-gb/media/gategroup-announces-completion-of-change-in-ownership.

6 See Form CO, Annex 5.1.3 – 3 (the “Call Option Agreement”), Article 3.5(a).

7 Ibid., Schedule 3, Section 3.1 (page 17).

8 Ibid., Schedule 3, Section 3.2 (page 18).

9 Ibid., Schedule 3, Section 3.3 (page 18).

10 Ibid., Schedule 3, Section 3.4(a) (page 18).

11 Turnover calculated in accordance with Article 5 of the Merger Regulation.

12 Form CO, paragraph 6.12.

13 Case M.8104 - HNA Group/Gategroup, paragraph 17, Case M.8137 – HNA Group/Servair, paragraph 42

14 Case M.8137 – HNA Group/Servair, paragraph 42.

15 Case M.8104 – HNA Group/Gategroup, para. 23, Case M.8137 – HNA Group/Servair, paragraph 50.

16 Case M.8137 – HNA Group/Servair, paragraphs 46-50. See also Case M.8104 – HNA Group/Gategroup, paragraphs 20 to 22.

17 Form CO, paragraph 6.16.

18 Case M.8137 – HNA Group/Servair, paragraph 26.

19 Form CO, paragraph 6.24.

20 Case M.8137 – HNA Group/Servair, paragraph 33.

21 Form CO, paragraph 6.9.

22 Case M.8104 – HNA Group/Gategroup, paragraph 35, Case M.8137 – HNA Group/Servair, paragraph 58.

23 Form CO, paragraph 6.29.

24 See Case M.8137 – HNA Group/Servair (2018), paragraph 61. See also Case M.8104 – HNA Group/Gategroup (2018), paragraph 35.

25 To a limited extent, the Parties overlap in the management of airport lounges at London Heathrow (LHR) airport. Given that there are no affected markets with respect to airport lounges (see footnote 43 of the Form CO), this aspect is no longer discussed in this decision.

26 See section 5.1.1 below.

27 See section 5.1.2 below.

28 For their estimate of the total market size at each relevant airport, the Parties provided data that excludes captive sales from Air Chef to Emirates Airlines; KLM Catering Services (KCS) to KLM; and LSG to Lufthansa Group Airlines (Lufthansa, Swiss, and Austrian Airlines) as in-house supply. See Form CO, Annex 7.1.

29 British Airways (the largest airline active at London Heathrow (LHR)) will switch from Gategroup to DO & CO in 2020, therefore, according to the Parties, the stated Gategroup’s market share overstates its competitive position. See Form CO, Annex 7.1.

30 All retail on-board services market shares exclude captive sales. Gategroup based its own retail on-board market shares on the actual 2018 revenues and provided estimates for the rest of the market based on its market intelligence. See Form CO, Annex 7.2.

31 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 265, 18.10.2008, p. 6, (the “Non-Horizontal Merger Guidelines”).

32 Non-Horizontal Merger Guidelines, paragraphs 29 to 30.

33 Non-Horizontal Guidelines, paragraphs 33 to 39.

34 Non-Horizontal Merger Guidelines, paragraphs 40 to 46,

35 Non-Horizontal Merger Guidelines, paragraphs 47 to 57.

36 Excluding captive sales, see Form CO and Annex 7.1

37 Replies to Q1 – questionnaire, question 11.

38 Replies to Q1 – questionnaire, questions 12 and 12.1.

39 This, however, applies only to those airports where more than one in-flight catering providers are active. Replies to Q1 – questionnaire, question 5.

40 Replies to Q1 – questionnaire, questions 9; 9.1 ; 10; and 10.1.

41 Market respondents noted various reasons for the switch, including lack of capacity, inadequate service of the previous service provider, better commercial conditions, and the fact that there existing in-flight services provider had been acquired by a larger player. Replies to Q1 – questionnaire, questions 7 and 7.1.

42 Customer/Competitor’s Reply to Q1 – questionnaire, question 7.1.

43 Customer/Competitor’s Reply to Q1 – questionnaire, question 10.1.

44 Form CO, paragraph 7.3 and Replies to Q1 – questionnaire, question 5.

45 Form CO, paragraph 7.3 and Replies to Q1 – questionnaire, question 6.

46 With the exception of Berlin Tegel (TXL), Frankfurt (FRA), and Munich (MUC) airports where Gategroup is the second largest in-flight catering provider after LSG Sky Chefs (Lufthansa Group) and Barcelona (BCN)where it is a close second in-flight catering provider after Newrest. See market share information submitted by the Parties in Annex 7.1 of the Form CO.

47 Namely, Berlin Tegel (TXL), Dusseldorf (DUS), Frankfurt (FRA), Munich (MUC), Rome Fiumicino (FCO), Amsterdam Schiphol (AMS), and London Heathrow (LHR) airports.

48 Excluding captive sales. See market share information submitted by the Parties in Annex 7.1 of the Form CO.

49 Namely, Paris Charles de Gaulle (CDG), Amsterdam Schiphol (AMS), Barcelona (BCN), and London Heathrow (LHR) airports.

50 Namely, Berlin Tegel (TXL), Dusseldorf (DUS), Frankfurt (FRA), Munich (MUC) and London Heathrow (LHR) airports.

51 Replies to Q1 – questionnaire, questions 8 and 10.1.

52 Customer’s Reply to Q1 – questionnaire, question 8.

53 Ibid.

54 Customer’s Reply to Q1 – questionnaire, question 8. See also Form CO, paragraph 7.3.

55 Customer’s Reply to Q1 – questionnaire, questions 8 and 25.

56 Competitor’s Reply to Q1 – questionnaire, questions 1 and 8. However, based on the Parties estimates, Inflight International Logistics’ market shares have remained very low, namely [0-5]% in Copenhagen Kastrup (CPH) and [0-5]% in Stockholm Arlanda (ARN), see Form CO, Annex 7.1.

57 Customer/Competitor’s Reply to Q1 – questionnaire, question 8.

58 Competitor’s Reply to Q1 – questionnaire, question 17.1. Gateretail is one of Gategroup’s retail on-board services brands and Retail inMotion is a Lufthansa Group’s subsidiary. Another respondent also mentioned a recent market entrant in on-board retail services, see a Competitor’s Reply to Q1 – questionnaire, question 16.

59 Replies to Q1 – questionnaire, question 17.

60 Customer/Competitor’s Reply to Q1 – questionnaire, question 17.1.

61 Customer/Competitor’s Reply to Q1 – questionnaire, question 17.1.

62 Replies to Q1 – questionnaire, question 19.

63 Replies to Q1 – questionnaire, question 20.

64 Customer/Competitor’s Reply to Q1 – questionnaire, question 20.1.

65 Customer/Competitor’s Reply to Q1 – questionnaire, question 20.1.

66 As noted in the Non-Horizontal Merger Guidelines, paragraph 45 (footnote), “in cases where two companies have joint control over a firm active in the upstream market, and only one of them is active downstream, the company without downstream activities may have little interest in foregoing input sales.”

67 Non-Horizontal Merger Guidelines, paragraph 47.

68 Non-Horizontal Merger Guidelines, paragraph 58.

69 Non-Horizontal Merger Guidelines, paragraphs 58 to 74.

70 Non-Horizontal Merger Guidelines, paragraphs 58 and 61.

71 Non-Horizontal Merger Guidelines, paragraph 61.

72 Non-Horizontal Merger Guidelines, paragraphs 58 and 61.

73 Non-Horizontal Merger Guidelines, paragraph 61.