Commission, April 12, 2018, No M.8764

EUROPEAN COMMISSION

Judgment

SEDGWICK / CUNNINGHAM LINDSEY

Subject: Case M.8764 - SEDGWICK / CUNNINGHAM LINDSEY

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 6 March 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation whereby Sedgwick, Inc ("Sedgwick", United States), indirectly solely controlled by investment funds affiliated with KKR & Co. L.P. ("KKR", United States), acquires sole control of CL Intermediate Holdings I, B.V. ("Cunningham Lindsey", United States) by way of purchase of shares3. Cunningham Lindsey, Sedgwich and KKR are referred to as "the Parties".

1.THE PARTIES AND THE OPERATION

(2) Sedgwick ("the Notifying Party") is a global provider of risk management solutions. Sedgwick is primarily focused on providing insurance-related services to insurers, self-insured corporations, governmental authorities, etc. On behalf of its customers, Sedgwick manages, processes and audits various claims made by the insured. In the United States, Canada, United Kingdom ("UK") and Ireland, Sedgwick provides Third Party Administrator ("TPA") insurance claims management services and loss adjusting services.

(3) Sedgwick is indirectly solely controlled by investment funds affiliated with KKR, which is a global investment firm. KKR offers a broad range of alternative asset funds and other investment products to investors and provides capital markets solutions for the firm, its portfolio companies, and other clients. Sedgwick operates in the United Kingdom under the name Vericlaim and in Ireland through OSG Outsources Services Group Limited ("OSG Vericlaim"). "Vericlaim" in the present decision therefore refers to Sedgwick subsidiaries

(4) Cunningham Lindsey is a global provider of TPA insurance claims management, loss adjusting, loss consultancy and property reinstatement services. Its customers comprise insurers, reinsurance companies, insurance brokers, self-insured corporations, governmental bodies, etc.

(5) Pursuant to the Share Purchase Agreement Sedgwick acquires 100 % of the issued and outstanding shares of Cunningham Lindsey. The transaction, therefore, constitutes a concentration within the meaning of Article 3(1) of the EUMR.

2.EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4 (KKR: EUR […] million; Sedgwick: […] million; Cunningham Lindsay: EUR […] million). Two of them have an EU-wide turnover in excess of EUR 250 million (KKR: EUR […] million; Sedgwick: […] million; Cunningham Lindsay: EUR […] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

3.RELEVANT MARKETS

(7) The relevant markets to this transaction relate to the provision of outsourced insurance-related services. More specifically, the Parties' activities overlap in loss adjusting services and TPA claims management services in the UK and Ireland. 5

3.1.Product market definition

3.1.1.Loss adjusting

(8) Loss adjusting services involve the provision of inspection services related to claims processing, which typically consist of sending an inspector to the site of the loss to assess whether the insurer is obligated to pay the insured (or a third party on behalf of the insured), to quantify the insurer’s exposure, and to determine whether the insurer can recover payment from a third party. Most field inspections are performed by third party loss adjusters (such as the Parties), but may be performed by an insurer or self-insured corporation using in-house claims inspectors. Claims that require field inspection range from small scale commercial or homeowner claims to large and complex industrial losses stemming from catastrophes and natural disasters.

(9) In a previous case,6 the Commission indicated that from the perspective of supply and demand-side substitutability, loss adjusting services belonged to a separate product market from other insurance-related services. The exact product market definition was however left open because the transaction did not raise serious doubts as to the compatibility with the internal market regardless of the exact market definition.

Distinction by type of claims

(10) The Notifying Party submits that there may be a distinction within loss adjusting services between property and casualty loss adjusting services. Property loss adjusting services relate to property insurance, which is a policy that provides financial reimbursement to the owner or tenant of a structure and its contents, in the event of damage or theft. Property insurance can be written for both personal property (e.g. homeowners and tenants) and commercial property (e.g. factories, goods, retail locations). Casualty insurance is mainly liability coverage of an individual or organisation for negligent acts or omissions.

(11) The market investigation7 showed that the main loss adjusting service providers in the UK and Ireland are active both in casualty and property loss adjusting services, but have different business units to deal with each type of claims. Smaller loss adjusting companies seem to be more specialised. They are generally active either only in property or only in casualty loss adjusting. Overall, the market investigation showed that property and casualty loss adjusting would require different skills, and that the legal and technical frameworks would vary.

(12) Within property loss adjusting services, the market investigation showed that the vast majority of loss adjusting companies are active in both commercial and personal property, but some of them have separate business units for each business line. One competitor pointed to the specificities of commercial property claims, in terms of expertise and customers' preferences.8

Distinction between in-house and external loss adjusting services

(13) The Notifying Party submits that the loss adjusting market should include also in- house supply of these services, which would exert a significant competitive pressure on the merchant market.

(14) The market investigation indicated that the decision to outsource loss adjusting services is mainly driven by costs efficiency and the need of (perceived) independence vis-à-vis the insurer for the insured. Numerous market respondents identified barriers to in-source, such as the need for sufficient volume, risks associated with human resources, lack of expert personnel and IT systems.9 Many customers indicated that they outsource entirely their loss adjusting needs to third parties, and some of them explained that in-sourcing would not be economical.10

Conclusion

(15) In any event, for the purpose of the present case, the precise product market definition for loss adjusting services and in particular whether (i) a distinction should be made between property and casualty loss adjusting services, and within property, between commercial and personal property loss adjusting, and (ii) the relevant market should comprise also in-house loss adjusting services can be left open in this case, since the transaction does not raise serious doubts as to its compatibility with the internal market regardless of the exact product market definition.

3.1.2.TPA claims management

(16) Claims management services involve the administration of insurance claims. TPA claims management service providers replicate all or part of an insurer's internal claims management process, including first notification of loss, initial analysis of claim and distribution to appropriate personnel for processing, negotiation and settlement, payment, providing management information and data, and recovery.

(17) In a previous case,11 the market investigation of the Commission strongly indicated that from both a supply and demand-side substitutability perspective TPA claim management services belong to a separate product market. This was because, according to market participants, TPA claims management services are provided separately from other types of claims-related services.

Distinction by type of claims

(18) The Notifying Party submits that TPA claims management services may be broken down into property (including commercial and personal property), casualty and motor lines, as it would require certain different skills. The Notifying Party however submits that the general process of providing TPA claims management services is similar for casualty, property and motor claims.

(19) The market investigation showed that TPA claims management service providers tend to specialise in each type of claims, casualty, property or motor, and within property, personal or commercial. If some service providers are active in several segments, they will generally have different teams since it would require specific expertise.12

Distinction between in-house and external claims management services

(20) The Notifying Party holds the view that in-house provision of claims management should be considered together with TPA insurance claims management, as it would exert a significant competitive pressure on the merchant market.

(21) The market investigation indicated that the decision to outsource claims management is mainly driven by costs efficiency. Market respondents consistently identified IT tools and expert personnel as necessary capabilities to handle claims in-house.13

Conclusion

(22) In any event, for the purpose of the present case, the exact product market definition for claims management services and in particular whether (i) a distinction should be made between property, casualty and motor claims management services, and within property, between commercial and personal property claims management, and (ii) the relevant market should comprise also in-house claims management services can be left open in this case, since the transaction does not raise serious doubts as to its compatibility with the internal market regardless of the exact product market definition.

3.2.Geographic market definition for loss adjustment and TPA claims management

(23) In its previous decision,14 the Commission considered the markets for insurance claims-related services, among which loss adjusting and claims management, could be national or possibly limited to the UK/Ireland cluster.

(24) The Notifying Party submits that the markets for loss adjusting and TPA claims management are national in scope. The Notifying Party argues that while there are no formal barriers to the movement of staff across national borders from a legal or regulatory perspective, the ability to speak the local language, legal requirements and a knowledge of local insurance law are key requirements for loss adjusting. The Parties consider there is typically a need (for reasons of costs and logistics) to maintain nationally located employees who can liaise locally with the customer and undertake site visits when field inspections are necessary. The Notifying Party adds that their respective entities in the UK and Ireland operate almost entirely as separate business, with different business models commercial strategies.

(25) The results of the market investigation on the geographic dimension of loss adjusting and claims management markets are not conclusive. While the majority of the competitors active in Ireland considers that the competition for loss adjusting and claims management services takes place at the level of the cluster UK and Ireland,15 the majority of UK competitors considers that the competition takes place at the UK level16. The results for customers of loss adjusting and claims management services show that one third of Irish customers purchases these services at the level of the cluster UK and Ireland, followed by a slightly smaller group which purchases them at the level of Ireland.17 The results of the UK customers mirror those of the UK competitors, i.e. a majority of UK customers purchases their loss adjusting services at the level of the UK.18

(26) The market investigation also showed that there may be a distinction between Northern Ireland and the rest of the UK, since Northern Ireland claims are sometimes handled by the Irish organisation of suppliers19 and some customers select their suppliers for the Island of Ireland.20

(27) In any event, for the purpose of the present case, the exact geographic market definition and in particular whether (i) the UK and Ireland should be considered together or separately and (ii) Northern Ireland should be in the same geographic market as the UK or as Ireland can be left open since the transaction does not raise serious doubts as to its compatibility with the internal market regardless of the exact geographic market definition.

4.COMPETITIVE ASSESSMENT

4.1.Loss adjusting

4.1.1. General description of the sector

(28) Loss adjusting services are provided by the Parties mainly to insurers, but also to a lesser extent to brokers, self-insured companies and governmental authorities.21

(29) Loss adjusting services are generally awarded in two ways: (i) providers can compete for a position on a customer’s “panel” of approved providers, or (ii) providers can be selected by a policyholder or broker, known as a “nominated” account.

(30) A panel is a business arrangement whereby a customer, generally an insurer, enters into contracts with a fixed number of suppliers to perform certain loss adjusting work that it has decided to outsource to third party service providers. According to the Parties, insurers select loss adjusters for panel membership by inviting them to the tender process. Membership to a panel typically lasts three to five years before being re-tendered. Membership to a panel is however no guarantee of work.

(31) The Notifying Party adds that, once on the panel, the panel members compete with each other in terms of the service they provide to the insurer. The prices or fees charged by a loss adjuster in a panel would be agreed upon before entering the panel.

(32) The results of the market investigation indicated that the vast majority of panels is set up through tenders22 and that the average duration of such membership is indeed three to five years, with potential prolongations. In the market investigation, customers have suggested that the allocation of work is dependent on the customer. The majority of insurers tend to split the work between panel members as evenly as possible, taking into account several variables such as the expertise of the panel member, the type of claim to be treated, etc23.

(33) On a nominated account, an insured or its broker typically names the specific loss adjusting firm to perform a certain service without that service provider having to be part of the insurer’s relevant panel. As explained by the Notifying Party, an insurance broker or the policy holder typically makes an individual request to the insurer that a particular loss adjusting firm be appointed to manage specific claims (thus “nominating” that firm).

4.1.2.Loss adjusting, Ireland Market shares

(34) The Parties and their main competitors' market shares for loss adjusting in Ireland are presented in the table below.

by customers as Vericlaim and/or Cunningham Lindsey's closest suppliers in terms of capabilities and expertise.27

Alternative suppliers

(38) According to the Notifying Party, the transaction will not impede effective competition as there are numerous alternative service providers.

(39) The market investigation indicated that sufficient alternative service providers will remain post-transaction. Thornton, Davies and ProAdjust, among others, have been identified as credible alternative suppliers.28 These three companies are active in all market segments, including property (personal and commercial).29

(40) The market investigation indicated that the smaller loss adjustment providers also exercise a certain degree of competitive pressure. While capacity is important for customers and may be required to handle large volume loss adjusting works (for example in relation to severe weather events)30, half of the customers include in the panels loss adjusting service providers irrespective of their size31, so that the panels comprise small and large companies32. Customers say that small loss adjusting service providers are also encouraged to apply for panel contracts and that they ultimately select the providers based on their expertise, the service offering, quality of service delivery, etc. In this respect, small players can be niche providers with specialist expertise addressing specific needs like for example related to high-risk casualty loss adjustment33.

(41) The market investigation showed that customers' panels composition vary, although several of the main players in Ireland are generally present.34 One competitor noted that "[the merger] will not have an impact on price and very few panels all have the same adjusters but a mix of all 6 firms operating in Ireland. Insurers with smaller panels who currently use both Cunningham Lindsey and OSG Vericlaim have a choice to use another firm or substitute an adjuster".35

(42) The market investigation also suggested that the Parties' competitors might increase their turnover post-transaction as customers generally multi-source through panels, so that post-transaction customers purchasing currently from both Parties may allocate more works to alternative suppliers. Competitors noted for instance that the transaction may have a positive impact for them as "we compete for panel positions where Cunningham Lindsey and OSG Vericlaim are chasing the same business"36 and "we think that some of the combined work of OSG and Cunningham Lindsey will become available for other companies".37 The market investigation indicated that a very significant proportion of loss adjusting works are awarded through panels38 and when asked whether they would need to organise a new tender should the transaction be completed, customers generally considered that it may not be necessary either because competition will remain within their panel or because the quality of the sevices provided by the current panel members should not be impacted by the transaction.39 Customers generally considered that the transaction should not impact the expertise or quality of services of the two companies (be they nominated or on a panel), while expertise and quality of services are being consistently identified as the most important capabilities.40 Quite the contrary, some customers considered that the merger will combine the Parties' skillsets and may therefore increase the companies' quality of services.41

(43) The vast majority of customers considered that the transaction will not impact their purchases nor competition on the loss adjusting market as there is a sufficient number of credible alternative suppliers. The overall view is that "there is a good strength, depth and volume of alternative providers".42 On the personal property market more specifically, one customer noted that "Irish personal property market has evolved in recent years with introduction of higher policy excesses and introduction of no claims bonus leading to reduction in volume of smaller claims. Merger of Vericlaim & Cunningham Lindsey will have little impact on Irish market. Overall Irish market is small and served well by small number of providers".43

(44) Only one competitor and one customer (out of 39 market respondents) identified a possible negative impact of the transaction on competitition or prices, mainly due to a reduction of choice. The competitor considers that there will be a reduction from 3 to 2 nationwide players. The customer considered that there could be a negative impact on prices as both Parties are among the (only) four loss adjusting service providers that participated to its last tender process for personel loss adjusting services. However, as explained above, the market investigation identified at least three other alternative suppliers of similar size and business model as the Parties, in particular for property (commercial and personal) loss adjusting services, namely Thornton, Davies and ProAdjust. The other competitive features of the loss adjusting markets detailed below further indicate that the transaction will not significantly impede effective competition for loss adjusting in Ireland.

Barriers to entry and ability of competitors to expand their activities

(45) The Notifying Party submits that barriers to enter and expand in the loss adjustment business are relatively low. There are no barriers associated with intellectual property, research and development, network effects or access to source of supply. The Notifying Party adds that scale is also not a barrier to entry, since being a credible loss adjusting service provider depends more on expertise and reputation.

(46) The market investigation indicated that to be successful it is essential for loss adjusters to hire expert personnel. Having dedicated and experienced personnel seems to be the key criterion to be selected by customers.44 For this reason, if competitors were willing to expand their activities from casualty to property loss adjusting for instance, they would need to build some expertise and have resources to hire competent personnel. In that respect, the market investigation did not point to any restriction on staff movement. Local presence, scale or having historical datasets were consistently considered to be less crucial than expertise.45

(47) In view of the above, the market investigation did not identify high barriers to entry or expansion in the loss adjusting business, except for the resources needed to hire expert personnel.

Barriers to switching

(48) The Notifying Party considers that customers can easily switch suppliers, as the latter do not have any guaranteed volumes under their contracts. In addition, customers regularly organise new bidding processes. Vericlaim and Cunningham Lindsey argue that respectively […]% and […]% of their turnover from loss adjusting is annually up for rebid in Ireland.

(49) In Ireland, customers generally grant contracts of a limited duration (3 to 5 years) to several suppliers, after a competitive tendering process.46 The market investigation also indicated that being on a panel or having a contract is not a guarantee of work. Within panels, customers generally have latitude on how to allocate work within the panel47 and reserve their right to purchase outside of that panel.48 Customers therefore generally remain free to decide which company they want to use for each claim or to appoint new loss adjusting service providers as they wish.

(50) In view of the above, the market investigation showed that customers can easily and swiftly switch between loss adjusting suppliers in Ireland.

Negotiating power of customers

(51) The Notifying Party submits that loss adjusting customers in Ireland are sophisticated buyers that dictate price to their service providers.

(52) The market investigation seems to indicate that a limited number of large insurance companies represents a high proportion of the Irish demand for loss adjusting services.49

(53) In addition, as indicated above, a large proportion of the market is attributed through panels, after a competitive tendering process. The market investigation indicated that through this process, insurance companies can compare the proposed loss adjusters' prices against each other, and may obtain a similar fee scale for all panellists.50 As detailed above, customers can also generally appoint (new) loss adjusting companies other than their preferred supplier(s).

(54) These competitive dynamics tend to confirm that the Parties' ability to raise prices post-transaction would be rather limited.

(55) The competitive assessment of the market for loss adjustment in Ireland above remains the same irrespective of whether or not Northern Ireland should be considered as part of the same geographic market as Ireland because (i) the market shares of the parties do not materially change, and (ii) the same competitive dynamics are observed.

Conclusion

(56) In light of all the above, and in particular in view of the alternative loss adjusting service providers who will remain post-transaction and the competitive dynamics on the demand-side, the Commission concludes that the transaction does not raise serious doubts as to its compatibility with the internal market for loss adjusting services in Ireland. The same conclusion applies if loss adjusting services in the United Kindgom are included in the same geographical market as Ireland because, as further explained in the part 4.1.3 below, (i) the market shares of the Parties would be lower and (ii) the same competitive dynamics are observed.

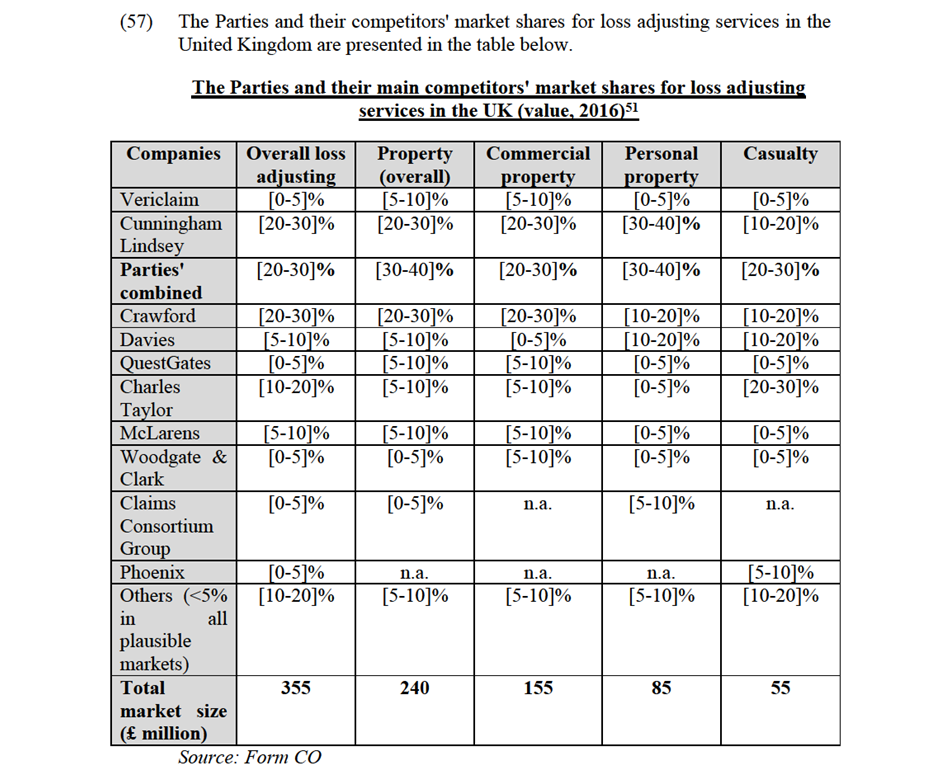

4.1.3.Loss adjusting, United Kingdom Market shares

investigation also indicated that Vericlaim is a smaller player, which would be more specialised in high value/low volume claims.53

(60) To support their claim that the Parties are not close competitors in the United Kingdom, the Notifying Party adds that of all the panels ([…]) in which either of the Parties participated, only in […] both of them were present. The Notifying Party specified that the same is true when the panels are considered separately for each of the subsegments. The market investigation did not identify the Parties as being particularly close competitors to each other. When asked to define the closest competitor to the each of the Parties, only a minority of customers refers to the Parties as each other closest competitors and Crawford is often mentioned as Cunningham Lindsey's closest supplier54.

Alternative suppliers

(61) According to the Notifying Party, the transaction will not impede effective competition as there are numerous alternative service providers.

(62) The market investigation indicated that sufficient credible alternative suppliers would remain. The vast majority of UK customers does not foresee an impact of the proposed Transaction on the loss adjusting services purchased by their company in the UK55, or on the loss adjustment market in the UK in general56. The vast majority of UK customers indicated that even post transaction, sufficient alternative loss adjusters would remain available on the market. When asked whether they would launch a new tender to try and select an additional panel member (if both Parties are current panel members), the majority of customers responded that it is currently not being considered57.

(63) Small loss adjusting service providers also exercise a certain degree of competitive pressure. While capacity is important for customers and may be required to handle large volume loss adjusting works, approximately one third of the customers include loss adjusting service providers in their panels irrespective of their size. Customers say that they ultimately select the providers based on their expertise, the service offering, quality of service delivery, etc. In this respect, small players can be niche providers with specialist expertise58.

(64) Only two competitors and two customers (out of 53 market respondents) identified a possible negative impact of the transaction on competition and on prices. One customer considered that the choice of large providers might be limited post-transaction and the other customer pointed to the risk that other competitors may have difficulties to compete with the (large) combined entity. The two competitors considered that the transaction may reduce capacity and competition, narrowing choice for customers.59 However, one of the competitors referring to a potentially reduced choice for customers also indicated that they considered it likely for Vericlaim to focus more on high volume claims, effectively providing opportunities for smaller emerging firms. Furthermore, as indicated above, the market investigation identified several credible alternative suppliers, including one of the same size as the combined entity, Crawford. More importantly, the market investigation showed that Vericlaim's presence is limited and the Parties' activities are rather complementary. The other competitive features of the loss adjusting markets detailed below further indicate that the transaction will not significantly impede effective competition for loss adjusting in the United Kingdom.

Barriers to entry and ability of competitors to expand their activities

(65) In analogy with the loss adjustment market in Ireland, the Notifying Party submits that barriers to entry and expansion in the UK loss adjustment business are relatively low. There are no barriers associated with intellectual property, research and development, network effects or access to source of supply. The Notifying Party adds that scale is also not a barrier to entry, since being a credible loss adjusting service provider depends more on expertise and reputation.

(66) The market investigation indicated that to be successful it is essential for loss adjusters to hire expert personnel. Having dedicated and experienced personnel seems to be the key criterium to be selected by customers.60 For this reason, if competitors were willing to expand their activities from casualty to property loss adjusting for instance, they would need to build some expertise and have sufficient resources to hire competent personnel. Local presence, scale or having historical datasets were generally considered to be less crucial than expertise.61

(67) In view of the above, the market investigation did not identify high barriers to entry or expansion in the loss adjusting business, except for the resources needed to hier expert personnel.

Barriers to switching behaviour

(68) The Notifying Party submits that working with panels allows customers to easily re-allocate panel work and/or add additional providers to these panels if they would have concerns about the merged entity's market position. The Parties also argue that, due to the fact that prices charged by the different panel members are relatively similar, insurers are indifferent when awarding work.

(69) The results of the market investigation seem to suggest that the prices within a panel are relatively similar for the same type of work. If specialist work is required, different pricings can be agreed62. The market investigation also suggests that insurers try to split the work as evenly as possible between panel members, unless specific characteristics of the claims (such as geographical location of the claimant, expertise needed to address the claim, etc.) does not allow for such an even split. It should also be noted that next to working with panels, customers can also appoint additional loss adjusters to do loss adjustment work outside of a panel, creating additional competition for the panel members. According to the results of the market investigation, the majority of customers actively purchases loss adjusting services from suppliers outside of their approved panels.63

(70) In view of the above, the market investigation showed that customers can easily and swiftly switch between loss adjusting suppliers in the United Kingdom.

Negotiation power of customers

(71) The Notifying Party submits that the Parties do not have the ability to raise prices, referring to customers' possibilities to discipline attempted price increases or reductions in service levels by switching supplier or threathening to do so.

(72) As described above, the majority of panels is composed through the use of tenders. In such a tender process, loss adjusters have to submit an offer in the tender process, describing the services to be provided and a price range. The customers then engage in negotiations with the loss adjusters before selecting their final panel members. The market investigation has shown that the majority of customers considers prices for comparable tasks are rather similar among the loss adjusters represented in their panels.64

(73) The market investigation has also shown that customers consider that price changes are rather infrequent and in the majority of cases dependent on the inclusion of additional services. However, when a loss adjuster proposes new prices, customers tend to engage in negotations with the loss adjuster. One customer indicated that "should a supplier initiate the discussion with an expectation of raising the price, then we would expect a detailed business case as a starting point to any discussion", while another customer stated that "any request for more substantive fee rises will be subject to open book analysis and negotiation (including rejection)"65.

(74) Since alternative suppliers are active in the UK market, customers may have the possibility to discipline price increases, either by reallocating work among panel members or by simply attracting a completely new supplier of loss adjusting services.

(75) These competitive dynamics tend to confirm that the Parties' ability to raise prices post-transaction would be rather limited.

(76) The competitive assessment of the market for loss adjustment in the United Kingdom above remains the same irrespective of whether or not Northern Ireland should be considered as part of the same geographic market as the rest of the United Kingdom because (i) the market shares of the Parties do not materially change, and (ii) the same competitive dynamics are observed.

Conclusion

(77) In light of the above, and in particular in view of the alternative loss adjusting service providers who will remain post-transaction, the Commission concludes that the transaction does not raise serious doubts as to its compatibility with the internal market for loss adjusting services in the United Kingdom. As indicated the conclusion above for loss adjusting services in Ireland, the same conclusion applies if Ireland and the United Kingdom are considered to form part of the same geographical market for loss adjusting services.

4.2.TPA claims management

4.2.1.General description of the sector

(78) TPA claims management present different competitive features compared to loss adjusting services.

(79) First, customers seem to in-source more often, at least partially66 and the decision on whether to outcource certain claims is essentially based on costs and hiring expert personnel but not on considerations such as the need for (perceived) impartiality67.

(80) In addition, TPA claims management contracts are generally granted with an exclusivity clause for a specific book of claims (as opposed to allocation of work within loss adjusting panels). Customers generally award TPA claims management contracts by tenders or nomination.68 Such contracts typically range from six months to five years in length, or may be open-ended.

4.2.2.TPA claims management, Ireland Market shares

(81) The Parties and their main competitors' market shares for TPA claims management in Ireland are presented in the table below.

"Cunningham Lindsey’s TPA offering in Ireland is not of a size that it would have a significant impact on the TPA market." 70

(84) As to Vericlaim's market position, the Notifying Party noted that TPA insurance property claims management merchant market in Ireland is very small, EUR 3 million (approximately 90% of the claims would be managed in-house) and that there is a high degree of customer concentration. This means that current market shares cannot be taken in isolation to assess the competitive strength of a supplier. In 2016 more than […]% of Vericlaims's turnover from property TPA claim management services was generated by […] customers. The same levels of customers concentration would exist on potential subsegments for TPA commercial property claims management and for TPA personal property claims management, in the latter with […] accounting for […]% of Vericlaim's total personal property claims management turnover. Losing […] customers to any of the Parties' competitiors would therefore result in a significant loss of market share for Vericlaim.

(85) The market investigation indicated that the market size is relatively limited, as customers insource TPA claims management to a large extent. Only three of the Irish customers entirely outsource TPA claims management.71 A vast majority of customers (around 70%) outsource only partially, meaning that they manage TPA claims also in-house.72

Alternative suppliers

(86) The Parties claim that despite the high combined market shares post-transaction, the customers will continue to have ample choice of TPA claims management service providers and the merged entity will continue to face competition from significant remaining competitors.

(87) The market investigation indicated that despite the Parties' high combined market shares, sufficient choice would remain for all types of TPA claims management. The majority of the customers considered that there would be a sufficient number of credible alternative providers.73 Other competitors for TPA claims management often cited by customers include Thornton and Davies.74 In addition, the small TPA claims management service providers also exercise a degree of competitive pressure. While resource capacity and systems capabilities are required for handling high volume contracts (i.e. contracts with a large number of claims) 75, important criteria based on which customers select their provider are the specific expertise ans staff competency, quality of service and price. In this respect, small providers can also be competitive as niche players76. Customers did not point out any impact of the transaction on their own purchases.

(88) Only one competitor and one customer (out of 21 market respondents) identified a possible negative impact of the transaction on competition. The competitor mentioned a reduction in capacity and competition. The customer considered that the market will lose a significant player (this customer does not currently purchase from Cunningham Lindsey). However, as explained above, the market investigation showed that alternative credible suppliers will remain in Ireland, and in particular Thornton which is of a similar size as Vericlaim for commercial TPA claims management, and that these alternatives would be sufficient in light of the small size of the Irish market. The other competitive features of the TPA claims management market detailed below further indicate that the transaction will not significantly impede effective competition for TPA claims management in Ireland.

Barriers to entry and ability of competitors to expand their activities

(89) The Notifying Party submits that barriers to enter and expand in the TPA claims management sector are low and that competitors recently expanded their presence in Ireland. In particular, DWF which was active in the UK acquired Triton to expand its presence in Ireland.

(90) The market investigation indicated that the most important cababilities for TPA claims management are expertise, experience and good claims handling systems.77 For this reason, if competitors were willing to expand their activities from casualty to property TPA claims management for instance, they would need to build some expertise and hire competent personnel. As to geographical expansion, the market investigation pointed out to some regulatory specificities in Ireland, where the market is regulated to the Central Bank of Ireland. Several customers and competitors nevertheless indicated that they purchase or compete for TPA claims management at the level of both the UK and Ireland together.78

(91) In view of the above, the market investigation did not identify high barriers to entry or expansion in TPA claims management, except for having good claims handling systems and resources to hire expert personnel.

Negotiating power of customers, barriers to switch and ability to in-source

(92) The Notifying Party submits that TPA claims management customers in Ireland are sophisticated buyers that do most of their claims handling in house and can effectively discipline price to their service providers. The Notifying Party specifies that in Ireland approximately 90% of claims would be managed in- house. The Notifying Party adds that customers can easily switch suppliers, as the the contracts are usually subject to termination with short notice (thirty or ninety days) and not subject to penalties. In Ireland, Vericlaim estimates that […]% of its annual turnover from TPA claims management up for rebid annually. Given the relatively small size of the market in Ireland, even where some works is moved to a competitor, the incumbent would be likely to continue serving the same customer for other portfolios.

(93) The market investigation indicated that the vast majority of customers at least partially insource claims management and some insurers fully insource claims management.79 Several customers stated that the higher value or more complex claims would preferably be dealt with internally, while high volume/low value claims would be outsourced.80 In addition, one customer indicated that it recently moved certain claims to another TPA claims management service provider.81

(94) The customers' ability to in-source or change supplier tend to further limit the Parties' ability to raise prices post-transaction.

(95) The competitive assessment of the market for TPA claims management in Ireland above remains the same irrespective of whether or not Northern Ireland should be considered as part of the same geographic market as Ireland because (i) the market shares of the Parties do not materially change, and (ii) the same competitive dynamics are observed.

Conclusion

(96) Taking into account Cunningham Lindsey's small market position, the number of alternative service providers available and the competitive dynamics on the demand side, the Commission concluded that the transaction does not raise serious doubts as to its compatibility with the internal market for TPA claims management services in Ireland. The same conclusion applies if TPA claims management services in the United Kindgom are included in the same geographical market as Ireland because, as further explained below, (i) the market shares of the Parties would be lower and (ii) the same competitive dynamics are observed.

4.2.3.TPA claims management UK

(97) For TPA claims management in the United Kingdom, based on the Notifying Party's estimate, the transaction leads to only one affected market for the sub- segment of commercial property TPA insurance claims management.

(98) The combined market share of the Parties commercial property TPA insurance claims management is [20-30]% in value in 2016) and the increment brought by Vericlaim's market share is small ([0-5]% in value in 2016).82

(99) Other competitors for commercial property TPA insurance claims management include the market leader Crawford, and Davies which is close to Cunningham Lindsey in terms of market share.

(100) The market investigation has indicated that the Parties will face competition from many alternative suppliers post-transaction and that they are not particularly close competitors to each other. When asked about their views on the closest competitors to the Parties, customers' replies show that there are no clear closest competitors in the market for TPA insurance claims management83. Nearly all of the customers consider that sufficient alternatives for TPA insurance claims management would remain available in the market post-transaction.84 The vast majority of customers does not foresee an impact on the TPA insurance claims market in the UK in general, nor on the TPA insurance claims they purchase.85.

(101) In light of the above, and in particular in view of the Parties' limited market position and the presence of alternative TPA claims management providers, the Commission concludes that the transaction does not raise serious doubts as to its compatibility with the internal market for claims management services in the United Kingdom.

5. CONCLUSION

(102) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 95, 13.3.2018, p. 22.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

5 Cunningham Lindsey is also active in loss adjusting and TPA claims management in Belgium, France, Germany, Italy, Netherlands, Spain and Sweden where Vericlaim is not present. Vericlaim may however refer claims of global customers in these countries to partners companies (not controlled by or affiliated with any of the Parties) within a network called "the VRS Network". The overlaps between Cunningham Lindsey and the claims referred by Vericlaim however do not lead to any affected markets.

6 See M.6752 - CVC/Cunningham Lindsey Group (para. 10-14).

7 Replies to questions 5 and 43 of Q1 - Questionnaire to Competitors.

8 A reply to question 44.1.1 of Q1 - Questionnaire to Competitors.

9 Replies to question 8 of Q1 - Questionnaire to Competitors.

10 Replies to questions 4 and 43 of Q2 - Questionnaire to Customers.

11 See M.6752 CVC/Cunningham Lindsey (para. 15-19).

12 Replies to questions 26 and 43 of Q1 - Questionnaire to Competitors as well as replies to questions 27 and 44 of Q1 - Questionnaire to Competitors.

13 Replies to questions 32 and 73 of Q2 - Questionnaire to Customers.

14 See M.6752 CVC/Cunningham Lindsey (para. 38-40).

15 Replies to questions 11 and 33 of Q1 - Questionnaire to Competitors.

16 Replies to questions 49 and 70 of Q1 - Questionnaire to Competitors.

17 Replies to questions 9 and 31 of Q2 - Questionnaire to Customers.

18 Replies to questions 48 and 71 of Q2 - Questionnaire to Customers.

19 Replies to question 1 of Q1 - Questionnaire to Competitors.

20 Replies to question 1 of Q2 - Questionnaire to Customers.

21 In Ireland, insurers represent respectively […]% of Vericlaim's property TPA revenue, […]% of its property loss adjustment revenue and […]% of its casualty loss adjusing revenue. For Cunningham, the insurers make up respectively […]%, […]% and […]% of the described business lines revenue. In the UK, insurers represent respectively […]% of Vericlaim's property TPA revenue, […]% of its property loss adjustment revenue and […]% of its casualty loss adjusing revenue. For Cunningham, the insurers make up respectively […]%, […]% and […]% of the described business lines revenue.

22 Replies to questions 5 and 44 of Q2 - Questionnaire to Customers.

23 Replies to questions 17 and 57 of Q2 - Questionnaire to Customers.

24 The Parties and their main competitors’ market shares are similar (i) over the last three years and (ii) even if Northen Ireland is included. These figures exclude in-house loss adjusting. If in-house loss adjusting was to be part of the same product market as external loss adjusting. The Partie’s market shares would be lower and the conclusion as to the absence of serious doubts as to the compatibility with the internal market would remain the same.

25 Replies to questions 21 to 23 of Q1-Questionnaire to Competitors and questions 20 to 22 of- Q2-Questionnaire to Custoners. Also minutes of a conference call with a competitor dated 16 February 2018.

26 Replies to question 1 of Q1-Questionnaire to Competitors.

27 Replies to question 22 of Q2 – Questionnaire to Customers.

28 Replies to question 20 of Q2 - Questionnaire to Customers. Also minutes with a competitor dated 22 February 2018.

29 Replies to questions 5 and 6 of Q1 - Questionnaire to Competitors.

30 Replies to question 12 of Q2 - Questionnaire to Customers and question 15.2 of Q2 - Questionnaire to Customers.

31 Replies to question 15 of Q2 - Questionnaire to Customers.

32 Replies to question 15.1 of Q2 - Questionnaire to Customers.

33 Replies to question 15.1 of Q1 - Questionnaire to Competitors.

34 Replies to question 16 of Q1 - Questionnaire to Competitors.

35 A reply to question 25 of Q1 - Questionnaire to Competitors.

36 Replies to question 24.1.1 of Q1 - Questionnaire to Competitors.

37 Replies to question 24.2.1 of Q1 - Questionnaire to Competitors.

38 Replies to question 14 of Q2 – Questionnaire to Customers.

39 Replies to question 25 of Q2 - Questionnaire to Customers.

40 Replies to questions 12 and 13 of Q2 – Questionnaire to Customers.

41 Replies to question 24.1 and 24.2 of Q2 – Questionnaire to Customers.

42 A reply to question 23.1 of Q2 - Questionnaire to Customers.

43 A reply of a customer to question 24.1 of Q2 - Questionnaire to Customers.

44 Replies to question 9 of Q1 – Questionnaire to Competitors and questions 11, 12 and 13 of Q2 – Questionnaire to Customers.

45 Replies to question 5 of Q1 – Questionnaire to Competitors.

46 Replies to question 16 of Q2 – Questionnaire to Customers and question 17 of Q1 – Questionnaire to Competitors.

47 Replies to question 18 of Q1 - Questionnaire to Competitors and question 17 of Q2 - Questionnaire to Customers.

48 Replies to question 20 of Q1 - Questionnaire to Competitors and question 19 of Q2 - Questionnaire to Customers.

49 The Top 5 customers represent a high proportion of loss adjusters' revenues (replies to question 4.1 of Q1 - Questionnaire to Competitors). Also minutes of a conference call with a competitor dated 16 February 2018.

50 Replies to question 19 of Q1 - Questionnaire to Competitors and question 18 of Q2 - Questionnaire to Customers.

51 The parties and their main competitors market shares are similar (i) over the last three years and (ii) even if Northen Ireland is excluded. These figures exclude in-house loss adjusting. If in-house loss adjusting was to be part of the same product market as external loss adjusting. The Parties market shares would be lower and the conclusion as to the absence of serious doubts as to the compatibility with the internal market would remain the same.

52 Replies to question 60 of Q2 – Questionnaire to Customers. Also minutes of a conference call with a customer dated 20 February 2018.

53 Replies to questions 60 and 61 of Q2 – Questionnaire to Customers. Also minutes of conference calls with customers dated 20 February 2018 and 22 February 2018.

54 Replies to question 62 of Q2 - Questionnaire to Customers.

55 Replies to question 64.1 of Q2 - Questionnaire to Customers.

56 Replies to question 64.2 of Q2 - Questionnaire to Customers.

57 Replies to question 65 of Q2 - Questionnaire to Customers.

58 Replies to question 52, 55, 55.1 and 55.2 of Q2 - Questionnaire to Customers.

59 Replies to questions 63 and 64 of Q2 – Questionnaire to Customers and question 61 of Q1 – Questionnaire to Competitors.

60 Replies to question 47 of Q1 – Questionnaire to Competitors and questions 51, 52 and 53 of Q2 – Questionnaire to Customers.

61 Replies to question 47 of Q1 – Questionnaire to Competitors.

62 See question 58 and subquestions of Q2 – Questionnaire to Customers.

63 See question 59 of M.8764 – Q2 – Questionnaire to Customers.

64 Replies to question 58 and subquestions of Q2 - Questionnaire to Customers.

65 See question 58.3 of M.8764 – Q2 – Questionnaire to Customers.

66 Replies to questions 26 and 66 of Q2 - Questionnaire to Customers.

67 Replies to questions 26.2 and 66.2 of Q2 - Questionnaire to Customers.

68 Replies to question 67 of M.8764 – Q2 – Questionnaire to Customers. The preferred selection method of customers differs on the type of customer (e.g. an insurance company compared to a self-insured company or a government agency) or in general with the customers' preference for one method over the other.

69 The Parties and their main competitors market shares are similar (i) over the last three years and (ii) even if Norhen Ireland is included. These figures exclude in-house loss adjusting. If in-house claims management was to be part of the same product market as TPA claims management, the Parties market shares would be lower and the conclusion as to the absence of serious doubts as to the compatibility with the internal market would remain the same.

70 A reply to question 40.2.1 of Q2 - Questionnaire to Customers.

71 Replies to question 26 of Q2 - Questionnaire to Customers.

72 Repies to question 26 of Q2 - Questionnaire to Customers.

73 Replies to question 39 of Q2 - Questionnaire to Customers. Only one customer considered that competition may be be reduced post- transaction.

74 Replies to question 36 of Q2 - Questionnaire to Customers.

75 Reply to question 31.1 of Q1 - Questionnaire to Competitors.

76 Replies to question 34 of Q2 - Questionnaire to Customers.

77 Replies to question 30 of Q1 – Questionnaire to Competitors and questions 33, 34 and 35 of Q2 – Questionnaire to Customers.

78 Replies to 33 of Q2 – Questionnaire to Customers.

79 Replies to question 26 of Q2 – Questionnaire to Customers.

80 Replies to question 26.3 of Q2 – Questionnaire to Customers.

81 Replies to question 29.1 of Q2 – Questionnaire to Customers.

82 The Parties' market shares are similar (i) over the last three years and (ii) even if Northern Ireland is excluded. The Parties' market shares would be even lower if in-house claims management figures were included.

83 Replies to question 79 of Q2 - Questionnaire to Customers.

84 Replies to question 80 of Q2 - Questionnaire to Customers

85 Replies to questions 81.1 & 81.2 of Q2 - Questionnaire to Customers