Commission, July 5, 2018, No M.8855

EUROPEAN COMMISSION

Judgment

Otary / Eneco / Electrabel / JV

Subject: Case M.8855 - Otary / Eneco / Electrabel / JV

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 1 June 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Otary RS NV ("Otary", Belgium), Eneco Wind Belgium NV ("Eneco", part of the Eneco Group NV, The Netherlands) and Electrabel NV ("Electrabel" part of the ENGIE group, France) intend to acquire within the meaning of Articles 3(1)(b) and 3(4) of the Merger Regulation joint control of SeaMade NV ("SeaMade", Belgium).3 Otary, Eneco, and Electrabel are collectively referred to hereinafter as the "Parties" and the concentration as the "Proposed Transaction".

1. THE PARTIES

(2) Otary focuses on the development, construction and operation of three Belgian offshore windfarm projects (Rentel, Seastar and Mermaid), with a combined total capacity of approximately 800 MW. It is jointly owned and controlled by the following 8 companies: Dredging Environmental & Marine Engineering NV (DEME), Green Offshore NV, Elicio NV, S.R.I.W. Environnement SA, Z-Kracht NV, Aspitavi Offshore II NV, Socofe SA, and Power@Sea NV.

(3) Eneco manages onshore and offshore windfarm projects in Belgium. It is part of the Eneco Group active in the production of electricity and supply of electricity and gas to private and business customers in various countries in the EU.

(4) Electrabel is engaged in the generation of electricity and heat, and the supply of electricity and natural gas to customers in Belgium, the Netherlands and Luxembourg. It is part of the Engie group ("Engie", France), a global energy player.

(5) SeaMade (the "Proposed JV") is a joint venture set up for the purpose of developing, constructing and operating the two Belgian offshore windfarm projects Mermaid (235,2 MW) and Seastar (252 MW).

2. THE OPERATION

(6) Pursuant to a Term Sheet entered into on 20 February 2018 (the "Term Sheet"), the offshore wind farm projects Mermaid and Seastar (under development), located in the Belgian North Sea, will be merged into the existing Seastar NV ("Seastar"). Seastar is currently owned and solely controlled by Otary (51%), whereas the eight Otary shareholders each hold a non-controlling minority interest of 6,125%. Mermaid THV ("Mermaid") is currently a contractual non-full function joint-venture between Otary (65%) and Electrabel (35%) holding the domain concession for the development, construction and operation of the Mermaid wind project.

(7) Once the merger between Mermaid and Seastar is completed, Eneco will purchase 12,5% of the shares in Seastar through a share and purchase agreement with Otary. As a result of the Proposed Transaction, Otary will indirectly hold 70% of the voting rights in the Proposed JV,4 Eneco 12.5% and Electrabel 17.5%.

(8) SeaMade's Board of Directors will consist of 11 directors: 8 Otary representatives, 2 Electrabel representatives and 1 Eneco representative. Strategic decisions, including the approval of the business plan and the annual budget, will be approved by the majority of the directors but will always require a positive vote of all Otary directors as well as the positive vote of 1 Electrabel director and the Eneco director. Therefore, Otary, Eneco, and Electrabel will jointly control SeaMade.

3.THE CONCENTRATION

(9) The Parties submit that the Proposed JV is full-function because: (i) it will own, operate and maintain the two offshore windfarm projects, will finance construction through project finance and will have its own management and staff dedicated to day-to-day operation; (ii) it will act as an independent generator and wholesale supplier of electricity on the market; (iii) the electricity generated by the two offshore windfarms will be tendered and awarded at market-compliant terms; and (iv) the Belgian State has granted a 20-year renewable concession for the exploitation of the Mermaid and Seastar windfarms.

(10) On the basis of the information provided in the Form CO and available in the Term Sheet,5 the Commission finds that the Proposed JV will have sufficient resources to operate independently on the market and notes, in addition, that the Proposed JV may recruit its own personnel and that, in any event, seconded personnel will be fully dedicated and act under the authority of the JV management for the development of the offshore windfarm projects in question.

(11) The Commission also finds that the Proposed JV is intended to operate on a lasting basis in view of the duration of the already granted concessions, the fact that the Proposed JV will operate the two windfarms after their development and that the Term Sheet has been entered without limitations in time.

(12) In addition, since the Proposed JV will develop and operate new electricity production capacities, it will not take over a specific function within the parent companies' business activities. To the contrary, the Proposed JV will directly tender under market conditions the electricity generated by its windfarms and thus have its own access to the market.

(13) Furthermore, while the Parties are also active in the generation and supply of electricity, the Commission observes that the Proposed JV will tender to the market the entire electricity production of its two windfarms and award it in the form of [Information on the structure that SeaMade will apply in bringing its electricity generation capacity to the market as well as the size of the blocks of electricity], by means of [Information on the duration of the PPAs concluded by SeaMade] Power Purchase Agreements ("PPAs"). Thus, the Proposed JV will not have any dependency on sales to its parents, as all its sales will be done through competitive tenders and, therefore, no production has been committed from the outset to the benefit of the Parties.

(14) Pursuant to section 7 of the Term Sheet, the Parties are entitled to matching rights [Structure and overall size of matching rights offered to the Parties to the Transaction with regard to SeaMade's electricity generation capacity]. However, if matching rights are exercised, it will be at market price calculated by reference to the most competitive bids submitted to reach 100% cumulative output.6 Moreover, […] approximately […]% of production will in any event be awarded to the most competitive bidder, i.e., is not subject to any matching rights.7 As a result, whatever the production acquired by the Parties from the Proposed JV, it will always be valued at normal commercial conditions. Hence, the Commission concludes that the relationship between the joint venture and its parents will be truly commercial in character.8

(15) In view of the above, the Commission finds that the Proposed JV will perform on a lasting basis all the functions of an autonomous economic entity and will therefore be economically autonomous from an operational viewpoint. Hence, the Proposed JV constitutes a concentration within the meaning of Article 3(1)b and Article 3(4) of the Merger Regulation.

4. EU DIMENSION

(16) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million9 [EUR 74 286 million]. Each of them has an EU- wide turnover in excess of EUR 250 million [Otary (and its shareholders) EUR [Otary's (and its shareholders') EU-wide turnover], Eneco (Eneco Group) EUR [Eneco Group's EU-wide turnover], Electrabel (Engie) EUR [Electrabel's

(Engie's) EU-wide turnover]], but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

5.COMPETITIVE ASSESSMENT

(17) The Proposed JV will own, develop, construct and operate two offshore windfarms in the North Sea, based on a 20-year renewable concession awarded by the Belgian State in 2012 following a competitive process. The Proposed JV will therefore engage in the generation and wholesale supply of electricity once it becomes (partly) operational in the third quarter of 2020. In contrast, the Proposed JV will not – [Strategic information regarding SeaMade's activities in the space of the development, construction and operation of wind farms].

5.1.Market Definition

(18) The Proposed JV will be active in the generation and wholesale supply of electricity where the Parties are also active, thus giving rise to a horizontal overlap. The Parties are also active directly or indirectly in the retail supply of electricity in Belgium, which gives rise to a vertical link with the Proposed JV.10

5.1.1.Generation and wholesale supply of electricity

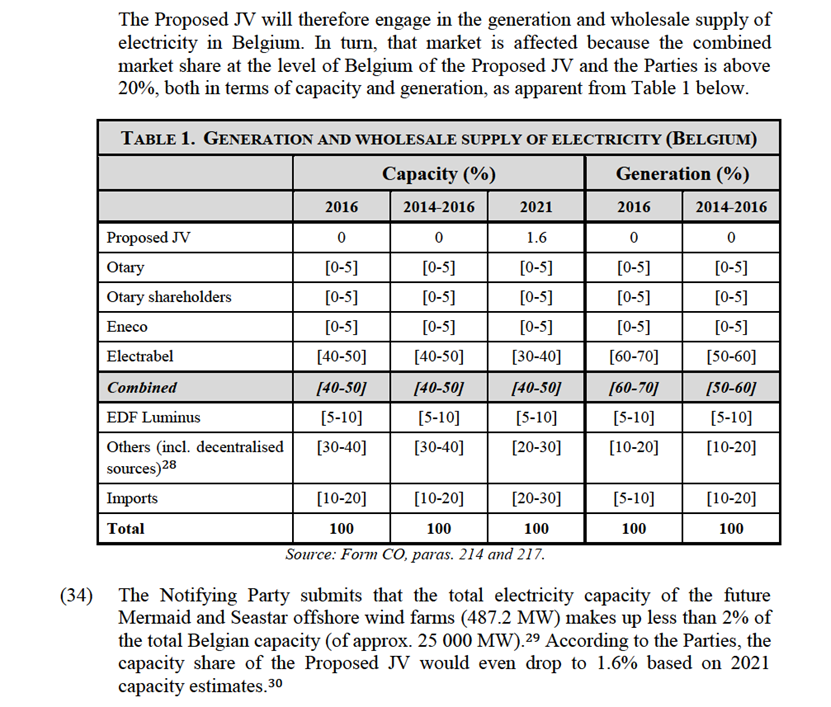

5.1.1.1.Product market definition

(19) The Parties submit that the generation and wholesale supply of electricity constitutes one single relevant product market that: (i) has not and should not be segmented on the basis of the source of electricity generation (e.g., renewable sources); but (ii) should encompass electricity imports and physical and financial trading on organised markets (e.g., Belpex) and OTC.11

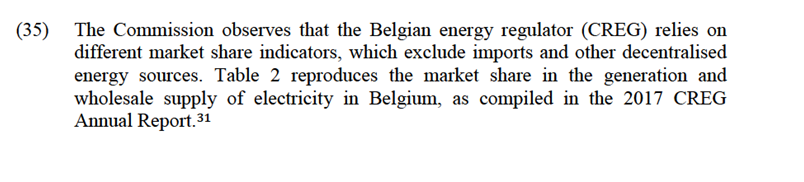

(20) The Commission has consistently defined a relevant product market encompassing both the generation and wholesale supply of electricity, irrespective of the generation sources and trading channels.12 The Commission has also considered in the past whether the financial trading of electricity belonged to the same product market as the generation and wholesale supply of electricity, or to distinct markets.13 Generally, financial trading has been distinguished from wholesale supply due to differences in settlement, duration and overall function since financially settled contracts are about trading risk while physically traded ones are about trading electricity for consumption.14 However, in EDG/Segebel, the Commission concluded in relation to Belgium that the relevant market comprised electricity generation, imports and trading on organised markets or OTC for both physically and financially settled products.15

(21) In the present case, the distinction between physically and financially settled trades can be left open since the Proposed Transaction is unlikely to raise serious doubts on a narrow definition limited to physically traded electricity. Regarding a possible segmentation according to the source of electricity, the question arises whether a dynamic assessment ought not to take into account Belgium's commitment to exit nuclear electricity production. However, that commitment will in any event not materialise before 2025 and implementing measures still need to be adopted and may then be adjusted to ensure security of supply or reflect energy cost developments.16 Moreover, nuclear plants still account for 56% of total electricity production in Belgium.17 Hence, a segmentation according to generation source, and in particular excluding nuclear, does not appear to be a plausible option in the present context.

(22) Overall, the precise market definition can be left open since no serious doubts arise as to the compatibility of the Proposed Transaction with the internal market, even on the narrowest plausible segmentation, which in the context of this case is the generation and wholesale physical supply of electricity irrespective of the source.

5.1.1.2.Geographic market definition

(23) The Parties acknowledge that the market for the generation and wholesale supply of electricity has historically been considered national in scope but submit that, in the present case, it should include the Benelux, France and Germany due to: (i) coupling of day-ahead and intraday markets; (ii) forward markets' price convergence; and (iii) increasing interconnection capacity.18 In any event, the Parties consider that no competitive concerns would arise if one were to consider only a hypothetical Belgian market, and provided data accordingly.19

(24) The Commission has indeed historically defined the market for the generation and wholesale supply of electricity at national level.20 However, the Commission has also recognised the relevance of interconnection capacity between Member States and of pricing relationships across interconnection points. In the present case, the Parties have not submitted evidence supporting their claim that the market should be considered wider than Belgium, except for some high-level references to new interconnection projects.

(25) In any event, the precise geographic market definition may be left open in the present case since no serious doubts arise as to the compatibility of the Proposed Transaction with the internal market even on the narrowest plausible segmentation, which is Belgium.

5.1.2.Retail supply of electricity

5.1.2.1.Product market definition

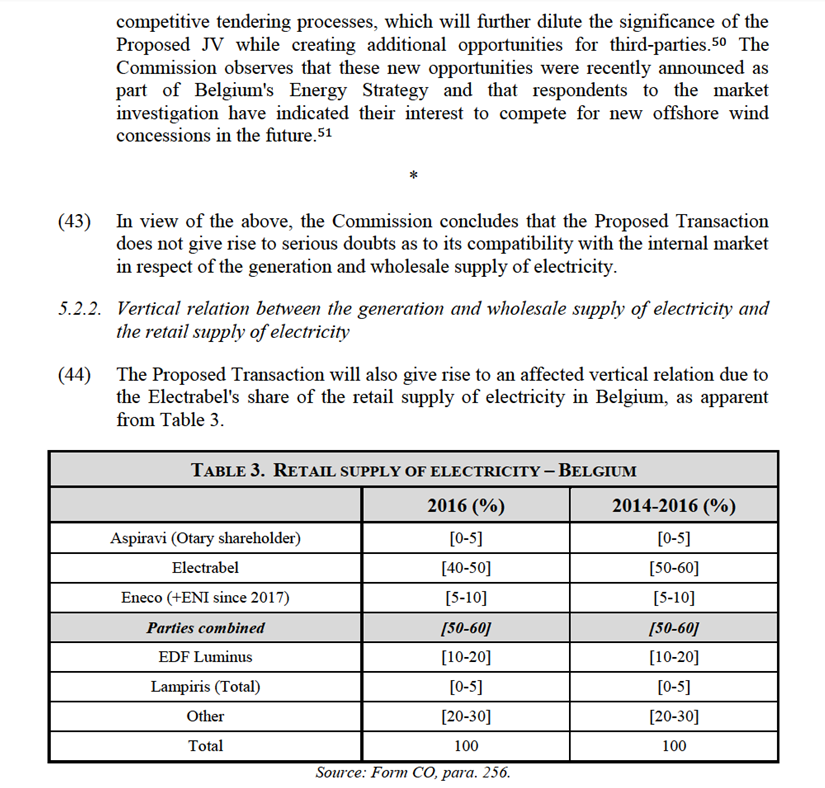

(26) The Parties submit that the definition of the market for the retail supply of electricity and its possible segmentation can be left open since no competition concerns arise irrespective of how the market is defined.21

(27) The Commission has previously considered that the retail supply of electricity constitutes a separate product market from the generation and wholesale supply of electricity, and that potential narrower segments can be distinguished based on factors such as different needs and profiles on the demand side and different services and technologies on the supply side. In this regard, separate product markets have been defined for the retail supply of electricity to: (i) large industrial and commercial customers; (ii) small industrial and commercial customers; and (iii) household customers.22

(28) In the present case, the precise product market definition may be left open since no serious doubts arise as to the compatibility of the Proposed Transaction with the internal market irrespective of the segmentation considered.

5.1.2.2.Geographic market definition

(29) The Parties submit that the definition of the geographic scope of the market for the retail supply of electricity can be left open since no competition concerns arise irrespective of how the market is defined.23

(30) The Commission has historically defined the retail electricity markets as national in scope.24 Under specific conditions, the Commission has also considered broader or narrower definitions. In relation to Belgium, the Commission has in the past excluded wider than national markets and, while considering the possibility of regional markets for household customers, has consistently assessed the retail supply of electricity, irrespective of the relevant segments, at national level.25 In the present case, the Commission has not received indication that retail markets should be considered at a level narrower than Belgium as a whole.

(31) In any event, the precise geographic market definition may be left open since no serious doubts arise as to the compatibility of the Proposed Transaction with the internal market irrespective of the geographic market considered.

5.2.Substantive Assessment

(32) As noted, the Proposed JV gives rise to a horizontal overlap between the Proposed JV and the Parties in the generation and wholesale supply of electricity. Likewise, a possible vertical link arises between the Proposed JV's activities in the generation and wholesale supply of electricity and the Parties' activities in the retail supply of electricity.26

5.2.1.Horizontal overlap in the generation and wholesale supply of electricity

(33) The electricity generated by the Proposed JV will be offered to the market by means of PPAs, subject to approval by the Belgian energy regulator (CREG).27

JV's production, thus limiting the increment that may be allocated to each of them.

(38) Secondly, while the Proposed JV is bound to ensure the market-compliant nature of PPAs entered into for the sale of the Seastar and Mermaid windfarms' production, subject to CREG oversight,38 the Commission understands that the Proposed JV is not as such under an obligation to offer and supply that production or a specific percentage thereof, to third-parties. Hence, the Commission disagrees with the submission of a respondent to the market investigation to the effect that, absent the Proposed Transaction, the Parties in general and Electrabel in particular would have had to be treated under the same commercial terms as any third-party bidder (or vice-versa) and, notably, would not have benefited from the matching rights provided for under the Term Sheet.39 To the contrary, the Commission understands that, absent the Proposed Transaction, [Structure and size of priority rights offered to the Parties to the Mermaid THV] [Confidential information with regard to potential business strategies to be deployed by Otary within Seastar NV prior to the establishment of the SeaMade JV], [Confidential information with regard to agreements concluded between Otary and Eneco pre- dating the current Transaction]. In turn, under the Proposed JV marketing arrangement, Electrabel will not have access, […], to a greater amount of electricity offtake compared to the situation prevailing in the absence of the Proposed Transaction.

(39) Against this background, the Parties submit that the Proposed JV aims to create synergies and lower the costs of the completion of the Mermaid and Seastar windfarm development, and of their subsequent operation, in view of the reduction in the guaranteed production support price under the renewable energy certificate scheme recently modified by the Belgian government.40 As a result, according to the Parties, the Proposed JV will enable new capacity to be brought to the market, which is inherently pro-competitive.41 Moreover, under the modified Belgian renewable energy certificate scheme, the Parties are bound to maximize the technical availability of the wind turbines during the period of support, so that they would have no ability and incentive to limit the amount of the Proposed JV's production.42

(40) The market investigation confirmed the Parties' views. In particular, respondents indicated that, inasmuch as it would add capacity on the market, the Proposed JV's "likely impact is that wholesale market prices will on average decrease as more production with low marginal costs enters the market" and thus that it can be expected to have a "depressing effect on the wholesale market", "improve liquidity in the Belgium market" and "help the market to become more competitive".43 One respondent did "not expect this transaction to have an important impact on the competitive market dynamics for the supply for electricity as its impact in terms of volume are relatively low and not constant".44 Such a view also echoes the Parties' contention that the total electricity capacity of the Mermaid and Seastar windfarms remains limited so that, notwithstanding its importance in enabling Belgium to reach renewable energy targets, the overall impact of the Proposed JV will be limited.45

(41) In contrast, one respondent argued that the concentration would lead to a wholesale price increase based on the assumption that the production of the Proposed JV would be channelled to former incumbent Electrabel, thus remaining "captive", and that the addition of wind production would generally increase price volatility and specifically prices on the intra-day and balancing markets, while also raising risk premiums included in the physical day-ahead and financial trading prices.46 The first assumption is inaccurate since the entire production of the Seastar and Mermaid windfarms will be tendered out; the envisioned [Information on the duration of the PPAs concluded by SeaMade] PPAs will be entered into at market terms (under CREG's supervision) and Electrabel's matching rights are [Structure and size of matching rights offered to the Parties to the Transaction with regard to SeaMade's electricity generation capacity]. Moreover, the possible consequences associated with an increase in the share of renewable energy sources in the production mix in Belgium are not specific to the Proposed JV and any possible specific effects were, in any event, not quantified by the respondent in question.47 Conversely, in a subsequent submission, the respondent indicated that the addition of a capacity comparable to that of the Seastar and Mermaid windfarms could have a significant depressing effect on wholesale prices.48

(42) The Parties also submit that other wind park projects are currently under construction (Rentel – 309 MW and Norther – 370 MW) or under development (Northwester II – 224 MW) in Belgium, which will bring additional volumes to the market while equally reducing any increment in their generation portfolio by the time the Proposed JV starts production.49 Moreover, the Parties indicate that the Belgian government recently decided to award concessions for the construction and operation of additional offshore wind farms by means of

on the other hand; (ii) the modest scale of the production of the Seastar and Mermaid windfarms, compared to the total amount of electricity supplied at retail level in Belgium (approx. 2.5%); (iii) the fact that the Parties will each realistically capture only a part of the total production of the Proposed JV; and (iv) the fact that third-party retailers will be invited to compete for the Proposed JV's production, and that approximately […]% of it will in any event be awarded to the most competitive bidder.

(47) In view of the above, the Commission concludes that the Proposed Transaction does not give rise to serious doubts as to its compatibility with the internal market in respect of the retail supply of electricity.

5.2.3.State aid aspects

(48) In its assessment, the Commission took into account the grant of State aid to the Seastar and Mermaid projects,53 notably the grant of renewable energy certificates (REC) entitling the Proposed JV to benefit from a guaranteed production support price. In that connection, the Belgian REC scheme was approved by the Commission by decision dated 8 December 2016 in case SA.45867, according to which Belgium will notify the aid to be granted to the Seastar and Mermaid projects.54. Generally, though, the Commission considers that the benefit of the support scheme in question and the potential State aid aspects thereof are not inherent to the Proposed Transaction but rather attached to the production of electricity by each of the Seastar and Mermaid (and other) windfarms. In any event, the potential aid would not alter the outcome of the merger control assessment of the Proposed Transaction, as set forth under sections 5.2.1 and5.2.2 above.

6.CONCLUSION

(49) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the Agreement on the European Economic Area. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the Agreement on the European Economic Area.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 SeaMade is the most likely name of the joint venture, but the final name may be different.

4 Otary will indirectly hold its shares in SeaMade through an intermediate holding company, Otary Bis NV, in which Otary will hold a controlling stake of 51% and the individual Otary shareholders will each hold a 6.125% non-controlling stake.

5 Form CO, section 3.6.

6 Form CO, paras. 135-148; Reply of the Parties to the request for information of 18 June 2018.

7 Contrary to the submission of a respondent to the market investigation, the Proposed JV can be considered to deal with its parents at arm's length commercial terms even though the most competitive bid may possibly be submitted by one of the Parties (Reply of a third-party to the request for information of 4 June 2018, and follow-up correspondence of 14 June 2018).

8 The Commission also notes that the Belgian energy regulator ("CREG") has the statutory obligation to review the market conformity of the PPA prices and to approve the concluded PPAs, as well as the right to order the adjustment of the correction factor applicable to the LCOE (Levelized Cost of Electricity) used for the calculation of the minimum price per MWh of produced electricity guaranteed under the applicable renewable energy certificate (REC) scheme (see Article 14, §1ter, 1° of the Royal Decree of 16 July 2002 aimed to establish mechanisms designed to promote the production of electricity from renewable sources). Form CO, paras. 124- 125 and reply of the CREG to the request for information of 19 June 2018.

9 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

10 The Parties contend that the vertical link in question is only potential in view of the fact that the electricity retailers (including Electrabel and Eneco) will not acquire electricity directly from the Proposed JV but rather from its off-takers (Form CO, para. 162). However, the Parties also indicate that if they were to acquire electricity under PPAs from the Proposed JV (and thus actually become off-takers themselves) [Strategic information regarding the Parties' (future) activities in the segments of the wholesale and retail supply of electricity] (Form CO, para. 151).

11 Form CO, paras. 177-179.

12 See cases COMP/M.7927 – EPH/ENEL/SE, paras. 9-12; COMP/M.6984 – EPH/Stredoslovenska Energetika, para. 15; M.3268 – Sydkraft/Graninge, paras. 19-20; COMP/M.8660 – Fortum/Uniper, paras. 18-21.

13 See cases COMP/M.5549 – EDF/Segebel, paras. 79-83; COMP/M.3868 – DONG/Elsam/Energi E2, paras. 241-246; COMP/M.8660 – Fortum/Uniper, para. 19-21.

14 See case e.g. COMP/M.3868 – DONG/Elsam/Energi E2, para. 252; COMP/M.8660 – Fortum/Uniper, paras. 43-48.

15 Case COMP/M.5549 – EDF/Segebel, para. 21.

16 Belgium Federal Energy Strategy, 30 March 2018:

http://www.presscenter.org/files/ipc/media/source6892/Federale energiestrategie.pdf.

17 CREG Annual Report 2017, p. 47.

18 Form CO, para. 182.

19 Form CO, para. 183.

20 See cases COMP/M.5979 – KGHM/TAURON Wytwarzanie/JV, para. 24; COMP/M.5711 – RWE/Ensys, para. 21; COMP/M.4180 – GDF/Suez, para. 726.

21 Form CO, para. 203.

22 See, e.g., in relation to Belgium case COMP/M.5549 – EDF/Segebel, para. 132.

23 Form CO, para. 202.

24 See cases COMP/M.6984 – EPH/Stredeoslovenska Energetika, para. 18; COMP/M.5827 – Elia/IFM/50 Hertz, para. 24; COMP/M.5496 – Vattenfall/ Nuon Energy, para. 15; COMP/M.5467 – RWE/Essent, paras. 283-284.

25 Case COMP/M.4180 – Gaz de France / Suez, paras. 738-743; Case COMP/M.5549 – EDF/Segebel, para. 138.

26 For the sake of completeness, the Commission notes that [Confidential information with regard to the structure and the development of the Seastar and Mermaid offshore wind farms]. Moreover, a number of similar projects are underway in Belgium and abroad, and will still be awarded in the future. Likewise, ENGIE is a supplier of offshore substations linking the windfarm to the transmission grid, but is only one potential supplier of that type of equipment to the Proposed JV.

27 In addition, the CREG has the statutory obligation to periodically review the market conformity of the PPA price. If this review reveals a difference between the PPA price and an average nomitated price, the aforementioned correction factor will be adjusted by the CREG (see Form CO, para.124).

28 Decentralised energy sources generally refer to generation close to consumption sites that is fed into the distribution guid.

29 Form CO, para 123. The share is around 2.3% if imports are discount.

30 Form CO, para 214. The share is around 2% if imports are discount.

31 CREG Annual Report, p40. The Commission notes that production data per power source contained in the same annual report (p47) do include decentralised sources.

32 CREG Annual report 2017, pp.40 and 47.

33 Replies of third-parties to the request for information of 4 june 2018 (and follow-up correspondance).

34 Form CO, para 121 see also reply of the CREG to the request for information of 19 June 2018.

35 Term sheet section 7.1 ; Form CO paras.138-140.

36 Form CO, paras 143-144.

37 Reply to the requests for information of 29 June 2018 and 2 July 2018.

38 See footnote 7 above.

39 Reply of a third-party to the request for information of 4 June 2018, and follow-up correspondence.

40 Form CO, paras. 28 and 119. The scheme was modified by a Royal Decree of 9 February 2017 with a view to ensuring compliance with the Commission Guidelines on State aid for environmental protection and energy 2014-2020 (see CREG 2017 Annual Report, p. 11).

41 Form CO, paras. 120.

42 Form CO, paras. 129-130. The Commission has been able to verify that this obligation is part of the LCOE Agreement entered into on 27 October 2017 between the Parties and the Belgian Minister for Energy and the North Sea (see Annex 4 to the Term Sheet). Moreover, the Commission notes that the production of the Proposed JV will in any event be marketed by means of [Information on the duration of the PPAs concluded by SeaMade] PPAs, thus leaving it limited scope, if any, to vary the production level of the Seastar and/or Mermaid windfarms.

43 Replies to question 3 of the request for information of 4 June 2018.

44 Reply to question 3 of the request for information of 4 June 2018.

45 Form CO, para. 123.

46 Reply to question 3 of the request for information of 4 June 2018.

47 The Commission notes that other respondents also alluded to the challenges associated with the increase in renewable – in particular wind – production, including in relation to price volatility, balancing costs and grid investments. These challenges are well-known to the industry and all stakeholders as being part of the energy transition process.

48 Reply to the request for information of 4 June 2018 and following correspondence of 14 June 2018.

49 Form CO, para. 123.

50 IDEM

51 Respectively ; (i) Belgium Federal Energy Strategy, 30 March 2018, and (ii) Replies to question 1 of the request for information of 4 june 2018.

52 Form CO, paras. 257-258.

53 Case T-156/98, RJB Mining plc v Commission [2001] ECR II-337, para. 114.

54 Decision of the Commission in Case SA.45867 (2016/N) – Belgium, para. 25.