Commission, July 5, 2019, No M.9357

EUROPEAN COMMISSION

Judgment

FIS / WORLDPAY

Subject: Case M.9357 – FIS/Worldpay

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 28 May 2019, the European Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which Fidelity National Information Services, Inc. (“FIS”, US or the “Notifying Party”) will acquire sole control over Worldpay Inc. (“Worldpay”, US or “WP” or the “Target”). FIS and Worldpay are collectively referred to below as the “Parties”.

1. THE PARTIES

(2) FIS is a global provider of financial services technology, offering retail and institutional banking, payments, asset and wealth management, risk and compliance and outsourcing solutions.

(3) Worldpay is a global payments technology company, providing merchant acquiring services and related technology services to merchants.

2. THE OPERATION

(4) On 17 March 2019, FIS, Worldpay, and FIS’ wholly-owned subsidiary Wranger Merger Sub. Inc. entered into a merger agreement, pursuant to which FIS would acquire sole control over the Target by way of a purchase of shares. The proposed concentration will be structured as follows. FIS’ wholly-owned subsidiary, Wranger Merger Sub. Inc., will merge with Worldpay. Worldpay will be the surviving entity in the merger and it will continue as a wholly-owned subsidiary of FIS (the “Transaction”).

(5) The Transaction would therefore give rise to a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (FIS: EUR 7 132 million; Worldpay: EUR 3 324 million). (3) Each of them has an EU-wide turnover in excess of EUR 250 million (FIS: [Confidential] Worldpay: [Confidential]), but none of them achieves more than two- thirds of their aggregate EU-wide turnover within one and the same Member State.

(7) The Transaction therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

(8) The Transaction combines two providers of payments technology services. The Parties’ activities overlap in relation to card payment systems.

(9) Card payment systems allow a cardholder to use a card (e.g., a credit or debit card) in order to pay for a product or a service without using cash. They connect merchants to financial institutions to cover the whole transaction from the moment the client pays at the point of sale ("POS") until the moment the merchant account is credited.

(10) An electronic payment transaction starts with a consumer using his/her payment card to purchase goods or services from a merchant. The merchant then seeks its merchant acquirer’s authorisation for the transaction. This authorisation request is initiated from the merchant’s physical card reader (a POS terminal for card-present transactions) or at a virtual POS (e.g., a web-based portal which enables similar functionality for card-not-present transactions). (4) The authorisation request is then transmitted to the merchant acquirer. The merchant acquirer validates the transaction and forwards it onto the appropriate scheme network for authorisation. The merchant acquirer can carry out this step itself or outsource it to an acquiring processor.

(11) When the card scheme receives the transaction, it determines the appropriate issuer and sends the transaction to the issuer for authorisation. The issuer then determines whether to approve the transaction based on the characteristics of the cardholder account. The issuer can carry out this step itself or outsource it to an issuer processor.

(12) Finally, the transaction response (approved, declined, or other) returns to the merchant. For an approved transaction, the merchant releases the goods or services.

(13) The remainder of this Section discusses market definition in card payment systems markets, which are relevant for the horizontal and non-horizontal analysis of the overlaps between the activities of the Parties.

4.1. Merchant Acquiring

4.1.1. Relevant Product Market Definition

(14) Merchant acquirers offer services that enable merchants to accept card payment transactions by connecting them to a range of card schemes and by providing solutions to process card payment transactions. To offer these services, merchant acquirers have to be licensed with the relevant card schemes (e.g., Visa or Mastercard). In several jurisdictions, merchant acquirers are also required to receive authorisation before they start offering their services. In the UK, merchant acquirers need to receive authorisation from the Financial Conduct Authority (“FCA”).

(15) Merchant acquirers provide three key services: (i) merchant recruitment (i.e., signing up merchants and maintaining the customer relationship); (ii) underwriting transactions (i.e., refunding the card scheme operator when paid goods/services are not delivered and the merchant cannot pay the refund itself); and (iii) merchant processing (i.e., providing the technology platform to connect with card schemes and process card transactions).

4.1.1.1. Previous Commission decisions

(16) The Commission has previously defined the market for merchant acquiring services as separate from the relevant product markets for payment card issuing and payment card processing. (5)

(17) The Commission has also considered possible segmentations of the market for merchant acquiring services, based on: (a) types of payment card schemes (international/domestic); (b) payment card brands (e.g. MasterCard, Visa etc); (c) types of payment card (credit/debit); and (d) platform (physical POS terminals/web- enabled interfaces (e-commerce)). (6)

(18) In its previous decisions, (7) the Commission ultimately decided to leave open the precise scope of the product market definition in merchant acquiring services, since the transaction did not raise serious doubts as to its compatibility with the internal market, whatever the product market definition.

4.1.1.2. Notifying Party's view

(19) The Notifying Party submits that there is a separate market for merchant acquiring services, but it suggested it should not be sub-segmented. Among other reasons, the Notifying Party recalls that merchant acquirers typically provide merchant acquiring services for a range of card schemes (domestic and international) and no merchant acquirers carry out merchant acquiring only for payments of one card brand (e.g., for either Visa or Mastercard).

(20) The Notifying Party submits that in any event, the question of whether the market for the merchant acquiring services should be sub-segmented by type of device can be left open in this case, as the Transaction does not raise concerns under any plausible market delineation.

4.1.1.3. Commission’s assessment

(21) The Commission’s market investigation did not provide any indications that would require the Commission to depart from its precedents on the relevant product market for merchant acquiring services.

(22) In this case, the exact relevant product market definition can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definitions.

4.1.2. Relevant Geographic Market Definition

4.1.2.1. Previous Commission decisions

(23) In past decisions, the Commission has considered the market for merchant acquiring to be likely national or at most EEA-wide in scope, irrespective of the type of card, the card scheme or the card brand that merchant acquiring services concern. (8) The Commission confirmed this approach in more recent decisions, such as Advent International/Bain Capital/ICBPI and Worldline/Equens/Paysquare for merchant acquiring services and all possible sub-segments of this market except for merchant acquiring services related to e-commerce payments, where the relevant market was found to be likely EEA-wide. (9)

4.1.2.2. Notifying Party's view

(24) The Notifying Party submits that the relevant geographic market for the provision of merchant acquiring services can be left open as no concerns arise even on the basis of the narrowest plausible geographic market definition, i.e., at national level. (10)

4.1.2.3. Commission’s assessment

(25) The Commission’s market investigation did not provide any indications that would require the Commission to depart from its precedents on the geographic scope of the market for the supply of merchant acquiring services.

(26) In any event, for the purposes of this Decision, the exact geographic scope of the market for merchant acquiring services can be left open, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market even on the basis of the narrowest plausible geographic market definition, i.e., at national level.

4.2. Provision of POS Terminals and Related Services

4.2.1. Relevant Product Market Definition

(27) A POS terminal is the electronic device used to process card payments at the merchant's location. It is a necessary element for physical card based transactions. POS terminals are either sold or leased to merchants. POS terminals are supplied either together with the merchant acquiring services or separately on a standalone basis. The supply of POS terminals typically includes services contracts for related services (i.e., maintenance and updates). (11) The remainder of this Section will refer to the supply of POS terminals as including related services.

(28) There are different types of POS terminals: traditional POS terminals and mobile POS (or “mPOS”) card readers. Traditional POS terminals connect to the merchant acquirer’s system through the merchant’s fixed telephone line or through broadband (via fixed cable or WiFi) or through the mobile telephone network. (12) mPOS card readers connect to the merchant’s smartphone or tablet via Bluetooth and an app on that smartphone or tablet then connects to the merchant acquirer. (13)

4.2.1.1. Previous Commission decisions

(29) In Worldline/Equens/Paysquare, the Commission considered that the market for the provision of POS terminals may be distinct from the market for the provision of merchant acquiring services. (14) The market investigation in that case showed that several customers procure POS terminals from a provider different from their merchant acquirer. This is typically the case for large retailers, while small and medium-sized enterprises (“SMEs”) appeared to opt for packaged solutions, including both the POS terminal and merchant acquiring services. (15)

(30) In Worldline/Equens/Paysquare, the Commission ultimately left open the question of whether a separate market can be defined for POS terminals (i.e., distinct from merchant acquiring services). (16)

(31) The Commission did not further consider the market for the supply of POS terminals by type of device or type of customer. However, the market investigation in Worldline/Equens/Paysquare did indicate that POS purchasing strategies may differ between merchants, depending on their size. (17)

4.2.1.2. Notifying Party's view

(32) The Notifying Party agrees with the definition of a relevant market for the supply of POS terminals as separate from the relevant market for merchant acquiring services.

(33) The Notifying Party also considers a possible sub-segmentation of the market for the supply of POS terminals by type of device (e.g., between traditional POS and mPOS). The Notifying Party recalls the UK Competition and Markets Authority’s (“CMA”) finding in PayPal/iZettle that in the UK, providers of traditional POS and mPOS compete in the same relevant market for the provision of offline card payment services to merchants. (18) The Notifying Party submits that in any event, the question of whether the market for the supply of POS terminals should be sub-segmented by type of device can be left open in this case, as the Transaction does not raise concerns under any plausible market delineation.

(34) As for a possible sub-segmentation of the market by customer size, the Notifying Party considers three categories of POS terminal customers, taking into account CMA’s recent PayPal/iZettle decision and the customer categories that the Parties use internally:

a) smaller merchants (including all merchants with an annual total payments volume (“TPV”) below GBP 380 000);

b) medium-sized merchants (including all merchants with an annual TPV between GBP 380 000 and GBP 1 million); and

c) large merchants (including all merchants with an annual TPV exceeding GBP 1 million).

(35) The Notifying Party takes the view that there are no clear boundaries between these three customer segments. According to the Notifying Party, FIS and Worldpay serve customers of all sizes, with Worldpay offering the same POS terminal models to customers regardless of their size and with its pricing for hire of POS terminals being standard across the board. The Notifying Party submits that in any event, the question of whether the market for the supply of POS terminals should be sub- segmented by customer size can be left open in this case, as the Transaction does not raise concerns under any plausible market delineation.

4.2.1.3. Commission’s assessment

(36) The Commission’s market investigation did not provide any indications that would require the Commission to depart from its precedents on the market for the supply of POS terminals.

(37) In particular, none of the respondents to the Commission’s market investigation took a clear position as to whether a possible relevant market for the supply of POS terminals should be sub-segmented further by type of POS device or based on the size of the POS terminal customers.

(38) In any event, the exact product market definition can be left open, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definitions.

4.2.2. Relevant Geographic Market Definition

4.2.2.1. Previous Commission decisions

(39) In Worldline/Equens/Paysquare, the Commission considered there were strong indications that the relevant geographic market for the supply of POS terminals should be national, or at least regional. Nevertheless, on the basis of the results of the market investigation in that case, the Commission left open the question of whether the relevant geographic market should be defined at national or broader level. (19)

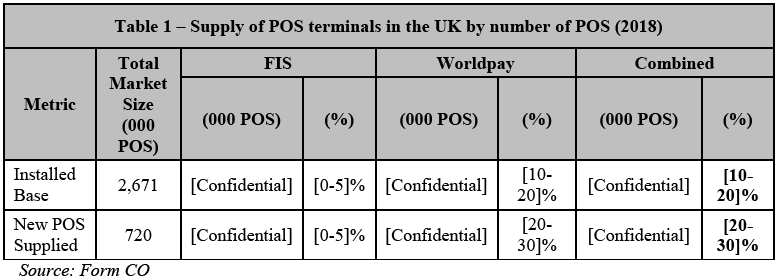

4.2.2.2. Notifying Party's view

(40) The Notifying Party submits that the relevant geographic market for the supply of POS terminals can be left open, as no concerns arise even on the basis of the narrowest plausible geographic market definition, i.e., at national level. (20)

4.2.2.3. Commission’s assessment

(41) For the purposes of this Decision, the exact geographic scope of the market for the supply of POS terminals can be left open, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market even on the basis of the narrowest plausible geographic market definition, i.e., at national level.

4.3. Independent Service Organisation Services

4.3.1. Relevant Product Market Definition

(42) As explained above, one of the key services of merchant acquirers is merchant recruitment. (21) Merchant acquirers often outsource this service to third parties, which are called Independent Service Organisations (“ISOs”). A merchant acquirer may use one or more ISOs to recruit merchants. Sometimes, merchant acquirers use ISOs while they also recruit merchants directly themselves. The contractual relationship for the provision of merchant acquiring services remains between the merchant and the merchant acquirer. ISOs have a contractual relationship with and are remunerated by the merchant acquirer – not the merchant directly.

(43) The ISO does not play any role in the underwriting, processing or settlement of the payment transaction. Unlike merchant acquirers, ISOs do not need to be licensed with card schemes (22) like Visa or Mastercard. They also do not need to be authorised by public authorities, including the FCA in the UK. (23)

4.3.1.1. Previous Commission decisions

(44) The Commission has not previously analysed the relevant product market for the provision of ISO services in relation to merchant acquiring.

4.3.1.2. Notifying Party's view

(45) The Notifying Party submits that the market for the provision of ISO services should not be further sub-segmented by the type of merchant acquiring services a merchant signs up for, as described in paragraph (17) above. All ISOs are able to serve all merchant acquirers, irrespective of the exact type and content of services that the merchant acquirers offer. (24)

4.3.1.3. Commission’s assessment

(46) The question of whether ISO services have to be sub-segmented by type of associated merchant acquiring services can be left open. The Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition.

4.3.2. Relevant Geographic Market Definition

4.3.2.1. Previous Commission decisions

(47) The Commission has not previously analysed the geographic market for ISO services related to merchant acquiring.

4.3.2.2. Notifying Party's view

(48) The Notifying Party submits that the relevant geographic market can be left open, as the Transaction does not raise competition concerns even on the narrowest plausible geographic market definition, i.e., at national level. (25)

4.3.2.3. Commission’s assessment

(49) For the purposes of this Decision, the exact geographic scope of the market for the provision of ISO services can be left open, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market even on the narrowest plausible geographic market definition, i.e., at national level.

4.4. Payment Terminal Testing Solutions

4.4.1. Relevant Product Market Definition

(50) A merchant acquirer needs tools to test and validate its payment technology and processing capabilities. These are payment terminal testing solutions (“PTTS”). PTTS are software productivity tools, which simulate a virtual transaction with a merchant using the software and the equipment of the merchant acquirer. A virtual transaction that goes through successfully confirms that the solution of the merchant acquirer works without problems. PTTS offer an automated testing service that historically had to be undertaken manually.

4.4.1.1. Previous Commission decisions

(51) The Commission has not previously analysed the relevant product market for the provision of PTTS to merchant acquirers and other users.

4.4.1.2. Notifying Party's view

(52) The Notifying Party submits that the market for PTTS should include not only the tools offered to merchant acquirers but also to other customers, such as POS manufacturers and card scheme operators. According to the Notifying Party, the underlying technology and functionality is very similar for providing PTTS across these three customer groups, and many providers of PTTS (e.g., UL, Iliad Solutions, FIME Testing and Certification, and Galitt) offer their services to all three customer groups.

4.4.1.3. Commission’s assessment

(53) The question of whether there is a separate market for PTTS to merchant acquirers or whether the market includes PTTS to merchant acquirers, card scheme operators, and POS manufacturers can be let open. The Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition.

4.4.2. Relevant Geographic Market Definition

4.4.2.1. Previous Commission decisions

(54) The Commission has not previously analysed the geographic market for PTTS, including related to merchant acquiring.

4.4.2.2. Notifying Party's view

(55) The Notifying Party submits that the relevant market for the provision of PTTS is likely to be at least EEA-wide if not worldwide, as merchant acquirers can obtain such solutions from businesses located worldwide. However, the Notifying Party submits that the relevant geographic market definition can be left open as no concerns arise even on the basis of the narrowest plausible market definition, i.e. at national level. (26)

4.4.2.3. Commission’s assessment

(56) For the purposes of this Decision, the exact geographic scope of the market for the provision of PTTS can be left open, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market even on the narrowest plausible geographic market definition, i.e., at national level.

5. COMPETITIVE ASSESSMENT

5.1. Introduction

(57) Article 2 of the Merger Regulation requires the Commission to examine whether notified concentrations are compatible with the internal market, by assessing whether they would significantly impede effective competition in the internal market or in a substantial part of it, in particular, as a result of the creation or strengthening of a dominant position.

(58) A merger giving rise to significant impediment of effective competition may do so as a result of the creation or strengthening of a dominant position in the relevant market(s). Moreover, mergers in oligopolistic markets involving the elimination of important constraints that the parties previously exerted on each other, together with a reduction of competitive pressure on the remaining competitors, may also result in a significant impediment to effective competition, even in the absence of dominance. (27)

(59) In fact, the Commission Guidelines on the assessment of horizontal mergers under the Merger Regulation (the “Horizontal Merger Guidelines”) (28) describe horizontal non-coordinated effects as follows: “A merger may significantly impede effective competition in a market by removing important competitive constraints on one or more sellers who consequently have increased market power. The most direct effect of the merger will be the loss of competition between the merging firms. For example, if prior to the merger one of the merging firms had raised its price, it would have lost some sales to the other merging firm. The merger removes this particular constraint. Non-merging firms in the same market can also benefit from the reduction of competitive pressure that results from the merger, since the merging firms’ price increase may switch some demand to the rival firms, which, in turn, may find it profitable to increase their prices. The reduction in these competitive constraints could lead to significant price increases in the relevant market.” (29)

(60) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force. (30) That list of factors applies equally regardless of whether a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of these factors need to be present for significant non-coordinated effects to be likely. The list of factors, each of which is not necessarily decisive in its own right, is also not an exhaustive list. (31)

(61) Finally, the Horizontal Merger Guidelines describe a number of factors, which could counteract the harmful effects of the merger on competition, including the likelihood of buyer power, the entry of new competitors on the market, and efficiencies.

(62) In addition, the Commission Guidelines on the assessment of non-horizontal mergers under the Merger Regulation (the "Non-Horizontal Merger Guidelines") distinguish between two main ways in which vertical mergers may significantly impede effective competition, namely input foreclosure and customer foreclosure. (32)

(63) For a transaction to raise input foreclosure competition concerns, the merged entity must have a significant degree of market power upstream. (33) In assessing the likelihood of an anticompetitive input foreclosure strategy, the Commission has to examine whether (i) the merged entity would have the ability to substantially foreclose access to inputs; (ii) whether it would have the incentive to do so; and (iii) whether a foreclosure strategy would have a significant detrimental effect on competition downstream. (34)

(64) For a transaction to raise customer foreclosure competition concerns, the merged entity must be an important customer with a significant degree of market power in the downstream market. (35) In assessing the likelihood of an anticompetitive customer foreclosure strategy, the Commission has to examine whether (i) the merged entity would have the ability to foreclose access to downstream markets by reducing its purchases from upstream rivals; (ii) whether it would have the incentive to do so; and (iii) whether a foreclosure strategy would have a significant detrimental effect on consumers in the downstream market. (36)

5.2. Overview of Affected Markets

(65) Both FIS and Worldpay supply POS terminals to merchants in the UK. The Proposed Transaction gives rise to a horizontally affected market regarding the supply of POS terminals in the UK.

(66) In addition, FIS offers ISO services and PTTS to merchant acquirers in the UK. Worldpay is active in merchant acquiring in the UK. The Transaction gives rise to affected markets regarding the following vertical links in the UK: (i) ISO services (upstream) and merchant acquiring services (downstream), and (ii) PTTS (upstream) and merchant acquiring services (downstream). (37)

5.3. Supply of POS Terminals in the UK

(67) FIS offers traditional POS terminals to merchants in the UK (not mPOS). FIS does not offer merchant acquiring services in the UK. It providers POS terminals (and related services) that are merchant acquirer agnostic, which means that merchants can use POS terminals supplied by FIS with their chosen third-party merchant acquirer. FIS is responsible for supplying the POS terminal (with associated software) and for providing maintenance and/or support services for the POS terminals. FIS does not manufacture the POS terminals it supplies to merchants. Rather, it sources them from Verifone and Ingenico.

(68) Worldpay offers traditional POS and mPOS terminals to merchants in the UK. Worldpay supplies POS terminals only to merchants for which it carries out merchant acquirer services. Worldpay does not manufacture the POS terminals it supplies to merchants. Rather, it sources them from Verifone, Ingenico, and Miura.

(69) The market for the supply of POS terminals in the UK is only affected based on the number of new POS terminals supplied in the country in 2018. As shown in Table 1 below, taking into account the installed base of POS terminals in the UK as of 2018, the Transaction would not result in an affected market in this relevant market.

(70) The Transaction does not give rise to serious doubts as to its compatibility with the internal market regarding a possible market for the supply of POS terminals in the UK for the following reasons.

(71) First, following the Transaction, the combined entity would have a share of [20- 30]% in this market (in terms of new POS terminals supplied). In terms of all POS terminals installed in the UK in 2018, the combined entity would only have a share of [10-20]%. According to the Horizontal Merger Guidelines, (38) combined market shares below 25% may indicate that the concentration is not likely to impede effective competition.

(72) Second, the share increment contributed by FIS remains below [0-5]%, regardless of the metric used for the estimation of market shares in the relevant market. In terms of new POS terminals supplied, the HHI delta would be below 75, which again is unlikely to indicate competition concerns. (39)

(73) Third, the combined entity will continue to face competition constraints by at least 10 competitors including POS terminal manufacturers (such as Ingenico and Verifone), merchant acquirers (such as Barclaycard and Global Payments), payments facilitators (such as PayPal/iZettle and Square), ISO providers (such as Paymentsense and Retail Merchant Services), and independent software vendors (such as Shopkeep and Lightspeed). Third party reports suggest that there have been at least 15 new entrants (40) that started offering POS terminals in the EEA in the past 5 years. (41) Many of these suppliers provide both traditional and mPOS in the UK, such as First Data, YouTransactor, Datecs, Feitian Tech, and BBPOS.

(74) Fourth, the Parties are not each other’s closest competitors. FIS supplies merchant acquirer agnostic POS terminals on a standalone basis. In contrast, Worldpay offers POS terminals only to merchants that are using its merchant acquiring services. In this sense, Worldpay competes more closely (not with FIS but) with merchant acquirers who offer POS terminals, such as Barclaycard and Global Payments. Moreover, each of FIS and Worldpay focus on different customer segments. Approximately [70-80]% of POS terminals installed by Worldpay are provided to small and medium-sized merchants, while [the majority] of FIS’ installed base at the end of 2018 were provided to large merchants with multiple retail branches. (42)

(75) Fifth, the vast majority of respondents in the market investigation did not raise any competition concerns in relation to the proposed Transaction in a possible market for the supply of POS terminals in the UK. (43)

(76) The Transaction also does not give rise to serious doubts as to its compatibility with the internal market, even if the supply of POS terminals in the UK were to be sub- segmented by type of POS device. In this context, the activities of the Parties would overlap only in traditional POS, given that FIS does not supply mPOS. In a possible market for the supply of traditional POS terminals in the UK, the combined entity would have a share of less than [20-30]% and the share increment of FIS would remain low, namely below [0-5]%. (44) The combined entity will continue to face competition by several suppliers of traditional POS terminals, such as Verifone, Ingenico, Barclaycard, and Global Payments. The market investigation did not reveal any substantiated competition concerns in relation to the proposed Transaction in a possible market for the supply of traditional POS terminals in the UK.

(77) Finally, the Transaction does not give rise to serious doubts as to its compatibility with the internal market, even if the supply of POS terminals in the UK were to be sub-segmented by customer size.

a) In a possible market for the provision of POS terminals to smaller customers in the UK, the Parties confirmed that their combined market share would not exceed [30-40]% (based on the number of merchants served). (45) The share increment contributed by FIS would remain very low, i.e., less than [0-5]%. Post-Transaction, the combined entity will likely face competition by at least five competitors (Barclaycard, PayPal/iZettle, Global Payments, Elavon, and First Data), each holding a share of 5% or more. The combined entity will face strong competition in this space in particular from mPOS terminals suppliers (PayPal/iZettle, Square, SumUp) who are specifically targeting smaller merchants. (46) The market investigation did not reveal any competition concerns in relation to the Transaction in a possible market for the supply of POS terminals to smaller merchants in the UK.

b) In a possible market for the provision of POS terminals to medium-sized customers in the UK, the combined entity would hold a share of less than [20-30]% and the share increment contributed by FIS will remain low (less than [0-5]%). In this possible segment, the merged entity will continue facing strong competition from several players, including POS terminal manufacturers (such as Ingenico and Verifone), merchant acquirers (such as Barclaycard and Global Payments), ISO providers (such as Paymentsense and Retail Merchant Services), and independent software vendors (such as Shopkeep and Lightspeed). (47) The market investigation did not reveal any competition concerns in relation to the Transaction in a possible market for the supply of POS terminals to medium-sized merchants in the UK.

c) In a possible market for the provision of POS terminals to large customers in the UK, the combined entity would hold a share of less than [20-30]% and the share increment contributed by FIS will remain low, namely less than [0- 5]%. In this possible segment, the merged entity will continue to face strong competition from several players, including POS terminal manufacturers (such as Ingenico and Verifone), merchant acquirers (such as Barclaycard and Global Payments), ISO providers (such as Paymentsense and Retail Merchant Services), and independent software vendors (such as Shopkeep and Lightspeed). (48) In particular, Verifone and Ingenico will likely exert strong competitive constraints on the merged entity in this space, as they supply POS terminals on a standalone basis and large retailers often buy the POS terminal separately from the merchant acquiring services. (49) The market investigation did not reveal any competition concerns in relation to the Transaction in a possible market for the supply of POS terminals to large merchants in the UK.

(78) In light of the above considerations supported by evidence collected over the course of the market investigation, the Commission concludes that the Transaction does not give rise to serious doubts as to its compatibility with the internal market as regards its impact on competition in the possible market for the supply of POS terminals in the UK (and its plausible sub-segmentations in terms of type of device and size of customer).

5.4. ISO Services in the UK (upstream) – Merchant Acquiring Services in the UK (downstream)

(79) FIS offers ISO services in the UK only to one merchant acquirer, Elavon, on a non- exclusive basis. On top of recruiting merchants directly, Elavon is using at least one ISO other than FIS, namely, Retail Merchant Services. As Worldpay offers merchant acquiring services in the UK, a vertical link arises between the markets for ISO services in the UK (upstream) and merchant acquiring services in the UK (downstream).

5.4.1. Input Foreclosure

(80) The Transaction is unlikely to give rise to input foreclosure concerns. The combined entity would not have the ability to foreclose its downstream competitors in merchant acquiring by restricting access to its ISO services for the following reasons.

a) Input foreclosure may raise competition problems when it is essential for the downstream product, e.g., when that product could not be manufactured or effectively sold on the market without the input. (50) Based on the market investigation, today ISO services do not seem to be essential for merchant acquirers to enter and succeed in the UK market. Merchant acquirers can sign up merchants and maintain the customer relationships as an in-house activity, instead of outsourcing it to an ISO.

b) For input foreclosure to be a concern, the combined firm must have a significant degree of market power in the upstream market. (51) However, FIS has a very limited position in ISO services in the UK. FIS only offers ISO services to one merchant acquirer in the UK, Elavon. Elavon does not rely significantly on FIS for merchant recruitment. Merchants recruited by FIS represent approximately [a very small proportion] of Elavon’s customer base (in terms of transaction volume) and [a very small proportion] (in terms of value). (52) In addition to recruiting merchants directly, Elavon is using at least one ISO other than FIS, namely Retail Merchant Services, which has recruited approximately five times more merchants for Elavon than FIS has. (53)

c) The merged entity would have the ability to foreclose downstream competitors if, by reducing access to its own upstream products and services, it could negatively affect the overall availability of inputs in the market. (54) Yet, FIS only holds a share of less of [0-5]% (by value of transactions) and [0-5]% (by transaction volume) in ISO services in the UK. There are much larger players in ISO services in the UK, including Paymentsense, Payment Merchant Services, Handepay, Payzone, and Retail Merchant Services. These five players account for 66% of merchants recruited via ISOs in the UK. (55) In the course of the Commission’s market investigation, one merchant acquirer stated that it had not even been aware that FIS provided ISO services in the UK. (56) Post-Transaction, Elavon and other merchant acquirers could switch to one of these alternative suppliers of ISO services, assuming the combined entity were to restrict access to its own ISO services. (57)

d) When assessing input foreclosure, the Commission considers whether there are effective and timely counter-strategies that downstream rivals can deploy e.g., to be less reliant on the input. (58) In this case, downstream rivals could counter any attempt of the combined entity to restrict access to ISO services by recruiting more merchants directly, i.e., making more use of their in-house sales force.

(81) None of the respondents in the Commission’s market investigation raised concerns regarding foreclosure of access to ISO services that could exclude merchant acquirer rivals of the combined entity.

(82) As the Commission found that the combined entity would have no ability to foreclose merchant acquirers in the UK, it is not necessary to assess in detail whether there is an incentive to foreclose or the overall impact of the transaction on competition.

5.4.2.Customer Foreclosure

(83) The Transaction is unlikely to give rise to customer foreclosure concerns. The combined entity would not have the ability to foreclose its upstream competitors in ISO services by foreclosing access to a significant customer base for the following reasons.

a) When assessing customer foreclosure, the Commission examines whether there are sufficient economic alternatives in the downstream market for the upstream rivals to sell their output to (59). Worldpay’s share in merchant acquiring services in the UK is [30-40]% (by value of transactions) and [30-40]% (by transaction volume) (60). While Worldpay is the leading player in merchant acquiring in the UK today, post-Transaction the merged entity will face strong competition from several players, including Barclaycard ([20- 30]% by value of transactions and [20-30]% by volume of transactions), Global Payments ([10-20]% by value of transactions and [10-20]% by transaction volume), Cardnet ([10-20]% by value of transactions and [5-10]% by transaction volume), Elavon and First Data (each [5-10]% both by value of transactions and by transaction volume), and others. Post-Transaction, ISOs will be able to continue offering services to each of these players and also to the many new merchant acquirers that regularly enter the market in the UK (61).

b) Customer foreclosure is less likely when the combined entity is not an important customer for the upstream product. (63) Worldpay makes only limited use of ISO services today. Merchants recruited by ISOs on behalf of Worldpay accounted for approximately [0-5]% of Worldpay’s transactions by value and [0-5]% of its transactions by volume in 2018. Merchants recruited by ISOs for Worldpay represented only [10-20]% of the total value of transactions involving ISO-recruited merchants in the UK in 2018. (64)

(84) Nor would the combined entity have an incentive to foreclose upstream rivals by discontinuing its purchases of ISO services. The market investigation suggested that merchant acquirers typically use more than one ISOs to maximise their opportunities for merchant recruitment. For example, this is the case with Worldpay, Elavon, and other merchant acquirers today. (65) Post-Transaction, the combined entity would have the incentive to continue working with several third-party ISOs to make sure its customer reach is as broad as possible.

(85) None of the respondents in the Commission’s market investigation raised concerns regarding foreclosure of access to the downstream market of merchant acquiring for upstream ISO rivals of the combined entity.

(86) As the Commission found that the combined entity would have no ability to foreclose ISO rivals in the UK, it is not necessary to assess in detail whether there is an incentive to foreclose or the overall impact of the transaction on competition.

5.4.3. Conclusion

(87) In light of the above considerations and the evidence collected in the course of the Commission’s market investigation, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as a result of either input or customer foreclosure on the markets for ISO and merchant acquiring services in the UK.

5.5. PTTS in the UK (upstream) – Merchant Acquiring Services in the UK (downstream)

(88) In the UK, FIS offers PTTS [Business Secret], which is active in the market for merchant acquiring. Worldpay also sources PTTS from [Business Secret]. A vertical link arises between the markets for PTTS in the UK (upstream) and merchant acquiring services in the UK (downstream).

5.5.1. Input Foreclosure

(89) The Transaction is unlikely to give rise to input foreclosure concerns. The combined entity would not have the ability to foreclose its downstream competitors in merchant acquiring by restricting access to PTTS for the following reasons:

a) The combined entity will not hold a significant degree of market power in the upstream market of PTTS in the UK. (66) FIS holds a market share that is less than 5% in the narrowest possible market for PTTS to merchant acquirers in the UK. (67) With such a limited position in the upstream market, the combined entity would have no ability to foreclose its downstream competitors.

b) The combined entity would not be in a position to affect the overall availability of PTTS in the UK market post-Transaction. (68) Today, FIS does not supply [Business Secret] in the UK. In the course of the Commission’s market investigation, one merchant acquirer stated that it had not even been aware that FIS provided PTTS in the UK. (69) Post-Transaction, downstream competitors could continue purchasing PTTS from the same source as they do today, in case the combined entity were to decide to restrict access to its PTTS.

(90) None of the respondents in the Commission’s market investigation raised concerns regarding foreclosure of access to PTTS that could exclude merchant acquirer rivals of the combined entity.

(91) As the Commission found that the combined entity would have no ability to foreclose merchant acquirers in the UK, it is not necessary to assess in detail whether there is an incentive to foreclose or the overall impact of the transaction on competition.

5.5.2. Customer Foreclosure

(92) The Transaction is unlikely to give rise to customer foreclosure concerns. The combined entity would not have the ability to foreclose its upstream competitors in PTTS by foreclosing access to a significant customer base for the following reasons:

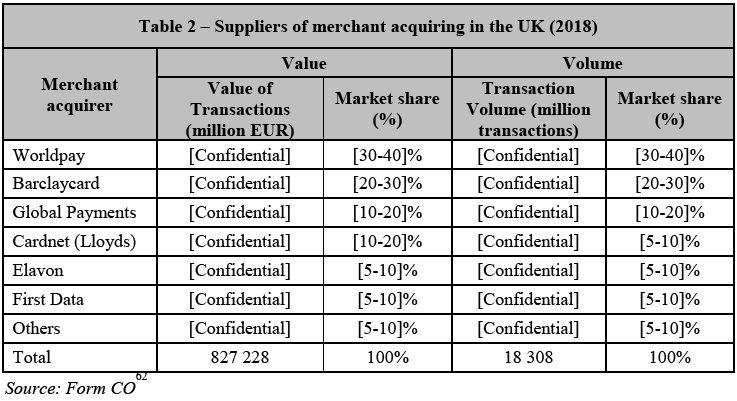

a) As shown in Table 2 above, Worldpay faces significant competition in the market for merchant acquiring services in the UK by at least five rivals with shares exceeding 5%. Post-Transaction, PTTS providers will be able to continue offering services to each of these players and also to the many new merchant acquirers that regularly enter the market in the UK. (70)

b) When assessing customer foreclosure, the Commission takes into account the existence of different uses for the upstream product. These can ensure that a sufficiently large customer base remains for that product post-merger. (71) Merchant acquirers are not the only purchasers of PTTS. The Notifying Party estimates that in 2018 in the UK, merchant acquirers represented approximately 30-40% of the total demand for PTTS. (72) POS manufacturers and card scheme operators also buy PTTS and according to the Notifying Party, they represented approximately 30-50% of the demand for PTTS in the UK in 2018. Post-Transaction, upstream rivals could compete to supply PTTS to card scheme operators and POS manufacturers, assuming the combined entity were to stop purchasing these services from third parties. (73)

(93) None of the respondents in the Commission’s market investigation raised concerns regarding foreclosure of access to the downstream market of merchant acquiring for upstream PTTS rivals of the combined entity.

(94) As the Commission found that the combined entity would have no ability to foreclose PTTS suppliers in the UK, it is not necessary to assess in detail whether there is an incentive to foreclose or the overall impact of the transaction on competition.

5.5.3.Conclusion

(95) In light of the above considerations and the evidence collected in the course of the Commission’s market investigation, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as a result of either input or customer foreclosure on the markets for PTTS and merchant acquiring services in the UK.

6. CONCLUSION

(96) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Turnover calculated in accordance with Article 5 of the Merger Regulation.

4 For the purposes this decision, “POS terminals” refers to physical POS terminals and not to virtual POS.

5 Case M.7241 - Advent International/Bain Capital Investors/Nets Holding, recital 12 with references to earlier cases.

6 Case M.7873 - Worldline/Equens/Paysquare, recitals 19-32. This follows from the Commission’s previous decisions in e.g. M.7241 – Advent International/Bain Capital Investors/Nets Holding; Case M.7711 – Advent International/Bain Capital/ICBPI; Case M.6956 – Telefonica/Caixabank/Banco Santander; Case M.5241 – American Express/Fortis/Alpha Card.

7 Case M.8073 – Advent International/Bain Capital/Setefi Services/Intesa Sanpaolo Card, paragraph 21 and Case M.7950 – EGB/GP, paragraph 26.

8 See e.g. Case M.4316 – Atos Origin/Banksys/BCC; Case M.5241 – American Express/Fortis/Alpha Card; Case M.6956 – Telefonica/Caixabank/Banco Santander; Case M.7241 – Advent International/Bain Capital Investors/Nets Holding.

9 Case M.7711 – Advent International/Bain Capital /ICBPI, recital 30 (where the Commission ultimately left open the question regarding the market for merchant acquiring services related to e-commerce payments) and Case M.7873 – Worldline/Equens/Paysquare, recital 108.

10 Form CO, paragraph 169.

11 Case M.7873, Worldline/Equens/Paysquare, paragraph 55.

12 Traditional POS terminals can be further sub-divided into two categories: integrated POS terminals and portable POS terminals. Integrated POS terminals are static devices often combining a pin entry device (or “PED”) with a cash register. Portable POS terminals connect via WiFi or mobile telephone network can be mobile in that they can be carried around the premises by staff and they do not have to be fixed to the sales desk and attached via a cable. See CMA Final Report, PayPal/iZettle, 12 June 2019, paragraph

2.30. See also Juniper Research, POS and MPOS Terminals: Vendor Strategies, Innovation, and Market Forecasts 2018-2023, p. 10, provide as Annex 7.2 to the Form CO.

13 See CMA Final Report, PayPal/iZettle, 12 June 2019, paragraph 2.30.

14 Case M.7873, Worldline/Equens/Paysquare, paragraph 68.

15 Case M.7873, Worldline/Equens/Paysquare, paragraphs 62ff.

16 Case M.7873, Worldline/Equens/Paysquare, paragraph 69.

17 Case M.7873, Worldline/Equens/Paysquare, paragraph 66 and fn. 37.

18 Form CO, paragraph 127. See also Final Report, PayPal/iZettle, 12 June 2019, paragraph 6.35.

19 Case M.7873, Worldline/Equens/Paysquare, paragraphs 128-134.

20 Form CO, paragraph 143.

21 See recital (15) above.

22 Card schemes typically require their licensed merchant acquirers to register the ISOs they use with the card scheme.

23 Form CO, paragraph 82.

24 Form CO, paragraphs 162 and 163.

25 Form CO, paragraph 169.

26 Form CO, paragraphs 186 and 187.

27 Horizontal Merger Guidelines, paragraph 25.

28 OJ C 31, 5.2.2004, p. 5.

29 Horizontal Merger Guidelines, paragraph 24.

30 Horizontal Merger Guidelines, paragraphs 27 and following.

31 Horizontal Merger Guidelines, paragraphs 24-38.

32 OJ L 24, 29.1.2004, p. 1.

33 Non-horizontal Merger Guidelines, paragraph 35.

34 Non-horizontal Merger Guidelines, paragraph 32.

35 Non-horizontal Merger Guidelines, paragraph 61.

36 Non-horizontal Merger Guidelines, paragraph 59.

37 The Transaction results in these vertically affected markets, as Worldpay’s share exceeds 30% in merchant acquiring services in the UK. See paragraph (83)(a) below.

38 Horizontal Merger Guidelines, paragraph 18.

39 Horizontal Merger Guidelines, paragraph 19.

40 Namely, UIC (2014); YouTransactor, Nayax, NewNote, FlyPOS (2015); Datecs, Centerm, Telepower Comm, Vanstone, Feitian Tech, BBPOS, and WizarPOS (2016); and Newland, Dspread Tech, Sunyard Tech, and First Data (2017).

41 See Nilson Report 1043, June 2014 (provided as Annex 8.2.a to the Form CO); Nilson Report 1067, July 2015 (provided as Annex 8.2.b to the Form CO); Nilson Report 1095, September 2016 (provided as Annex 8.2.c to the Form CO); Nilson Report 1114, July 2017 (provided as Annex 8.2.d to the Form CO).

42 Form CO, paragraphs 231-233.

43 In the market investigation, only one customer expressed the concern that post-Transaction the combined entity could bundle in the UK (i) FIS-legacy POS terminals and associated payment processing services and (ii) Worldpay-legacy merchant acquiring services. According to this customer, merchants (in particular large retailers) today benefit from the flexibility of FIS’ standalone merchant acquirer agnostic POS offering (which includes Verifone and/or Ingenico hardware). According to the same customer, a merchant that sources today POS terminals from FIS could possibly consider switching to the combined entity’s merchant acquiring services. In that sense, the respondent suggested that in the long run, the proposed Transaction could foreclose rivals of the combined entity in merchant acquiring services in the UK (Minutes of call with customer, 17 June 2019, paragraph 8). The Commission takes the view that it is unlikely that the combined entity would have the ability to foreclose competitors in merchant acquiring services in the UK, by leveraging FIS’ minimal position in POS terminals in the UK. First, post- Transaction, the combined entity could leverage only FIS’ standalone offering of POS terminals, because Worldpay already today supplies POS terminals only to merchants for which it carries out merchant acquirer services. FIS’ standalone offering of POS terminals represents less than [0-5]% of the relevant market in the UK. Second, the vast majority of respondents to the market investigation did not submit that FIS’ POS terminals have a “must have” status. Third, rival merchant acquirers could deploy effective and timely counter-strategies, offering their services together with POS hardware from either Verifone or Ingenico. According to the Notifying Party, merchant acquirers like Barclaycard and Global Payments offer POS terminals from both Verifone and Ingenico. Post-Transaction, merchants could turn to one of these providers to counter a possible bundling strategy from the combined entity. This conclusion would not change, if the relevant market for POS terminals in the UK was further sub-segmented by type of device or type of customer, because the position of the combined entity would not be significantly different in any of the narrower market segments, as explained in paragraphs (76)-(77) below.

44 Notifying Party’s reply to RFI 5, 28 June 2019, reply to question 3.

45 Form CO, paragraph 240.

46 Final Report, PayPal/iZettle, 12 June 2019, paragraphs 8.5 and 8.15.

47 Notifying Party’s reply to RFI 5, 28 June 2019, reply to questions 1-2.

48 48 Minutes of call with customer, 17 June 2019, paragraph 8 and Notifying Party’s reply to RFI 5, 28 June 2019, reply to questions 1-2.

49 49 Case M.7873, Worldline/Equens/Paysquare, paragraph 66.

50 50 Non-horizontal Merger Guidelines, paragraph 34.

51 Non-horizontal Merger Guidelines, paragraph 35.

52 Estimated based on Form CO, paragraphs 252, 258, and 336.

53 Form CO, paragraph 336.

54 Non-horizontal Merger Guidelines, paragraph 36.

55 Form CO, paragraph 335.

56 Minutes of call with competitor, 24 May 2019, paragraph 10.

57 This conclusion would not change, if the relevant market for ISO services were to be sub-segmented by the type of merchant acquiring services a merchant signs up for, as described in paragraph (17) above. According to the Notifying Party, all ISOs are able to serve all types of merchant acquirers in the UK. This means merchant acquirers could switch to any of the alternative suppliers of ISO services in the UK, if the combined entity decided to restrict access to ISO services for merchant acquiring services concerning a specific type of card scheme; payment card brand; payment card type; or platform.

58 Non-horizontal Merger Guidelines, paragraph 39.

59 Non-horizontal Merger Guidelines, paragraph 61.

60 The Parties confirmed that Worldpay’s position would not be significantly different in any of the potential narrower sub-segments of merchant acquiring described in paragraph (16) above. For the purposes of this decision, therefore, all these potential sub-segments will be assessed together. Worldpay’s share does not exceed [40-50]% in possible UK markets for merchant acquiring services related to international card schemes, for merchant acquiring services related to domestic card schemes, for merchant acquiring services related to Visa cards, for merchant acquiring services related to Mastercard cards. In a possible market for merchant acquiring services related to debit cards, Worldpay’s share in the UK is [30-40]% (by value of transactions) and [30-40]% (by transaction volume). In a possible market for merchant acquiring services related to credit cards, Worldpay’s share in the UK is [30-40]% (by value of transactions) and [40-50]% (by transaction volume). Finally, in a possible market for merchant acquiring services for payments through POS terminals, Worldpay’s share in the UK is [30-40]% (by value of transactions) and [30-40]% (by transaction volume) and in a possible market for merchant acquiring services for payments through web-enabled interfaces, Worldpay holds [20-30]% (by value of transactions) and [30-40]% (by transaction volume). Source: Form CO, Annex 7.7. In all of these market segments, a sufficiently large customer base will remain that is likely to turn to independent suppliers for ISO services, if the combined entity restricted access to its ISO offering.

61 See paragraph (73) above.

62 All EUR figures converted from GBP using the ECB’s average exchange rate for 2018.

63 Non-horizontal Merger Guidelines, paragraph 61.

64 Form CO, paragraphs 250 and 340.

65 Regarding Worldpay and Elavon, see Form CO, paragraphs 341 and 336, respectively. Source regarding other merchant acquirers: minutes of call with competitor, 24 May 2019, paragraph 10.

66 Non-horizontal Merger Guidelines, paragraph 35.

67 Based on the value of services provided.

68 Non-horizontal Merger Guidelines, paragraph 36.

69 Minutes of call with competitor, 24 May 2019, paragraph 13.

70 See paragraph (73) above.

71 Non-horizontal Merger Guidelines, paragraph 61 and 66.

72 See Notifying Party’s reply to RFI 4, question 2.

73 This conclusion stands irrespective of whether there is a separate market for PTTS to merchant acquirers or whether the market includes PTTS to merchant acquirers, card scheme operators, and POS manufacturers.