Commission, October 16, 2019, No M.9466

EUROPEAN COMMISSION

Judgment

INFINEON / CYPRESS

Subject: Case M.9466 – Infineon/Cypress

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 11 September 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Infineon Technologies AG (“Infineon” or the “Notifying Party”, Germany) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of Cypress Semiconductor Corporation (“Cypress”, USA) (the “Transaction”). Infineon and Cypress are collectively referred to as the “Parties”.3

1. THE PARTIES

(2) Infineon is active in the design, manufacture and distribution of a wide range of semiconductors and power semiconductors, including, inter alia, transistors, drivers, diodes, microcontrollers (including embedded control, radio-frequency and sensors), for a wide range of applications.

(3) Cypress is active in the manufacture and supply of embedded systems solutions for automotive, industrial, consumer and enterprise end markets. Cypress’ product portfolio includes microcontrollers, analog integrated circuits, wireless and wired connectivity solutions and memory products.

2. THE CONCENTRATION

(4) The Transaction consists of the acquisition by Infineon of the sole control of Cypress. Under the terms of the Agreement and Plan of Merger dated 3 June 2019, Infineon will acquire all of the issued and outstanding share capital of Cypress (which is currently listed on the NASDAQ stock exchange), via a merger with Infineon’s indirectly wholly owned subsidiary IFX Merger Sub Inc.

(5) The Transaction therefore constitutes a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million4 (Infineon: EUR 7.6 billion; Cypress: EUR 2.1 billion). Each of them has an EU-wide turnover in excess of EUR 250 million (Infineon: EUR […] billion; Cypress: EUR […] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

(7) The Transaction concerns the semiconductor industry.

(8) Semiconductors are materials, such as silicon, which act as an insulator, but are also capable of conducting electricity. Semiconductors are at the heart of devices such as diodes, transistors and other electronic components, and can be found in virtually every electronic device today. The end-products that contain semi- conductor devices range from base stations, mobile phones, computers, domestic appliances and cars to medical equipment, identification systems, large-scale industry electronics and aerospace equipment.

(9) Semiconductor devices are rarely bought as end-products by consumers. They are mainly bought by equipment manufacturers in virtually all sectors within the electronic equipment industry.

4.1 Overview of the semiconductor industry

(10) In previous decisions, the Commission considered dividing the market for semiconductors by (i) category of semiconductor and by (ii) end-use application:

i. As to the distinction by category, the Commission considered that it is appropriate to distinguish semiconductors in the categories of (i) integrated circuits (“ICs”), (ii) discretes, (iii) optical semiconductors, and (iv) sensors and actuators.5

ii. As to the distinction by end-use application, the Commission considered that there are six major applications for specific semiconductor devices: (i) communication, (ii) consumer, (iii) computer, (iv) military, (v) industrial, and (vi) automotive. The semiconductors manufactured for each application differ in their function and are not substitutable from one application to another.6

(11) The results of the market investigation in the present case confirmed this general categorization of semiconductors. In particular, all respondents7 to the market investigation agreed that semiconductor devices could be classified into the four distinct categories of (i) ICs, (ii) discretes, (iii) optical semiconductors and (iv) sensors and actuators.8

(12) Considering that the Parties’ activities mainly overlap in ICs, for the purpose of this decision the other categories of semiconductors are not discussed further.

4.1.1 Integrated Circuits

(13) An IC is a semiconductor device composed of diodes, transistors and other electronic components, combined with conductive interconnect material, which controls the current and voltage of electricity running through it. ICs used in electronic devices are called “microchips” or “chips” and contain several billion transistors along with diodes and other electronic components.

(14) In its previous decisions, the Commission found that: (i) digital ICs; and (ii) analog ICs should be considered as separate markets, since this differentiation reflects the structure of customer purchasing categories and is in line with the standard definition provided by World Semiconductor Trade Statistics (WSTS). Semiconductor manufacturers generally classify ICs based on their ratio of digital and analog content. If an IC contains solely digital or analog technology, it is labelled as a digital or analog IC, respectively.9

(15) Within digital ICs, the Commission found three main sub-segments: (i) micro- components; (ii) memory ICs; and (iii) logic ICs, given that these products have different functions and features and do not appear to be readily substitutable with each other.10

(16) Respondents to the market investigation have confirmed the relevance of the distinction between digital and analog ICs and, within digital ICs, between micro- components, memory ICs and logic ICs.11

(17) In its previous decisions, the Commission has also sub-segmented micro- components into: (i) microprocessors (“MPUs”); (ii) microcontrollers (“MCUs”); and (iii) digital signal processors (“DSPs”).12 The results of the market investigation in the present case confirmed this segmentation and in particular that MCUs and MPUs are different products and generally cannot be substituted, both from a supply-side and demand-side perspective.13

(18) Within ICs, the Parties overlap primarily in the design, manufacture and sale of MCUs. Therefore, for the purpose of the present decision, the Commission will not discuss further the other categories of ICs and micro-components.

4.2 MCUs

4.2.1 Product market definition

(19) An MCU is a stand-alone device that performs a dedicated or embedded computing function within an electronic system without the need of other support circuits. An MCU is principally a controlling device, which processes or manipulates data received in real time. This differentiates MCUs from MPUs, which are more powerful processing devices. While MPUs are capable of processing and carrying out several tasks simultaneously, MCUs are, by contrast, dedicated to a single, pre-defined task. The objective of MCUs is to interface with the “real world” (such as processing measurements from sensors) or to supervise and control certain system functions (such as power management, battery charging, actuators or interface to peripherals). MCUs are in general less expensive and less power-consuming than MPUs.

4.2.1.1 The Notifying Party’s view

(20) The Notifying Party submits that MCUs could be sub-divided (a) according to their technical parameters (i.e., number of bits they contain (8, 16 or 32-bits)) or

(b) whether they are either general purpose or used for a specific application.

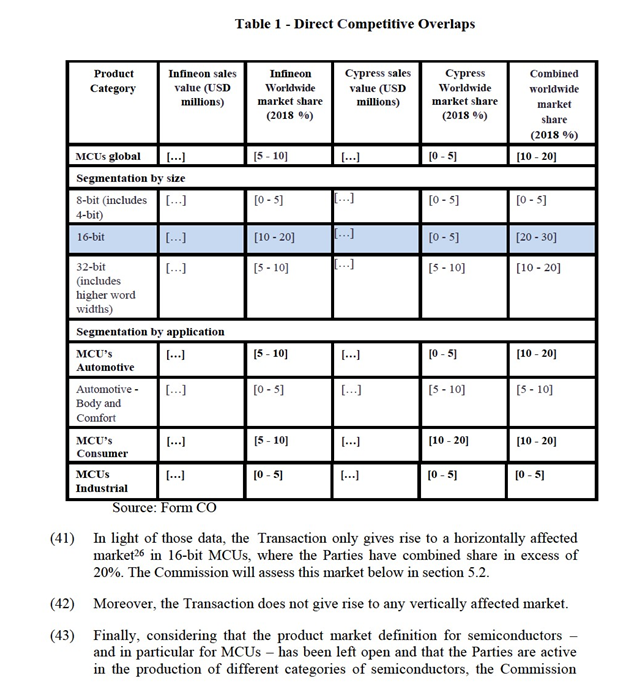

(a) Segmentation by bit-size

(21) The Notifying Party submits that customers select MCUs on the basis of the processing capability required by an application, degree of interfacing needed and the degree of power consumption. An 8-bit MCU would feature a low-gate count, software simplicity and lower complexity, which would make the 8-bit MCU cheaper than other types of controller. 8-bit MCUs would be often designed into low-performance segments where the product lifecycle can be long such as metering, building and home control segments and home appliances.

(22) 16-bit MCUs would provide more precision than 8-bit MCUs, and would be used for applications which require more accuracy, such as industrial robotics. 16-bit MCUs would be more efficient at performing instructions and would have longer timers. Applications requiring high-end processing power (such as video game consoles) would require a 32-bit MCU.

(b) Segmentation by end-use application

(23) Concerning a possible distinction of MCUs based on their end-use, the Notifying Party submits that substitutability among MCUs designed for different applications, although technically feasible, would not be optimal in terms of performance or cost-effectiveness. Substitutability between different MCU types would be dependent on a number of factors, including: (i) the relevant end-use application (automotive, consumer, industrial, etc.); (ii) the maturity of the technology; (iii) whether there is an operating system between the software and hardware elements of the MCU; and (iv) whether the customer wishes the MCU to be cost- and performance-optimised, or rather merely ‘fit-for-purpose’.

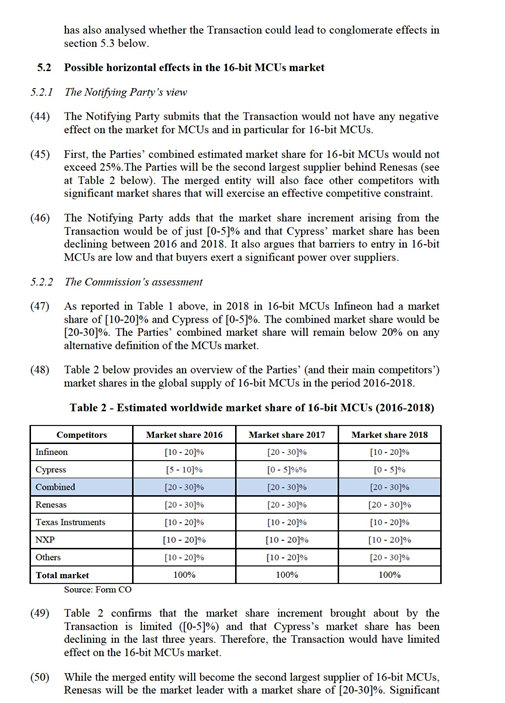

(24) The Notifying Party further submits that application specific MCUs could be segmented into the following product categories: (i) automotive; (ii) ID and smart card; (iii) consumer; (iv) industrial; (v) computers and peripherals; and (vi) wireless communication.

(c) Automotive MCUs

(25) With specific respect to the automotive sector, the Notifying Party, on the basis of a Commission precedent, submits that MCUs could be further segmented on the basis of particular kinds of automotive semiconductors: (i) powertrain; (ii) chassis; (iii) safety; (iv) body and comfort; (v) infotainment; and (vi) security.14

(26) However, the Notifying Party adds that in terms of manufacturing, any supplier of automotive MCUs could manufacture any type of automotive MCUs for a wide range of sub-segments, because the core architecture is often similar across different types of automotive MCUs.

(27) In any case, the Notifying Party submits that the precise scope of the relevant markets can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market irrespective of the market definition adopted by the Commission.

4.2.1.2 The Commission’s assessment

(28) In a past decision, the Commission considered that MCUs could be sub- segmented depending on the number of bits, although in the end it left the market definition open.15 Notably, the Commission considered that MCUs could be distinguished on the basis of the number of bits (8, 16 or 32-bit), as this distinction relates to both their performance and cost.

(29) The vast majority of the respondents to the market investigation has confirmed the relevance of a distinction based on the number of bits. Notably, it has been argued that the heart of an MCU is its computational core, which in itself differs from each other based on the data width it can handle at one time. This difference would create significant variations in the speed and accuracy of the mathematical operations carried out by MCUs. Therefore, a classification based on bits would be relevant.16

(30) In its previous decision the Commission also considered, although ultimately left open, a distinction based on MCUs’ intended use (i.e., whether they are either general purpose or used for a specific application).17 In the present case, the result of the market investigation has confirmed this distinction. Respondents stated that MCUs in general are specifically optimized to carry out limited set of functions. Application-specific MCUs would be customized and optimized for certain applications to enable high performance and quality. They would be used for very specialized functionality, and therefore could not be substituted from both a demand-side and a supply-side perspective.18

(31) The vast majority of respondents to the market investigation also confirmed that application-specific MCUs belong to the following distinct product categories, depending on their application: (i) automotive; (ii) ID and smart card; (iii) consumer; (iv) industrial; (v) computers and peripherals; (vi) wireless communication; and (vii) wired communications.19 Respondents considered that application-specific MCUs of one category would not be substitutable with those of another category, both from a demand side and a supply side perspective. Different applications would require different characteristics, performance and quality levels which would not to be substitutable. For example, MCUs for automotive application would require high reliability and robustness which would need to be qualified by industry standard and by customers.20

(32) With specific respect to automotive MCUs, all respondents to the market investigation confirmed the relevance of the distinction based on specific end- use/application: (i) powertrain; (ii) chassis; (iii) safety; (iv) body and comfort; (v) infotainment; and (vi) security.21 Automotive MCUs would be highly specialized and components needed to perform a specific function would be highly optimized. Therefore, substituting them for other functions would be either inefficient, or cost-ineffective, or plainly impossible.22

4.2.1.3 Conclusion on product market definition

(33) The Commission considers that, for the purposes of this decision, the exact product market definition with regard to MCUs can be left open, as the Transaction does not raise serious doubts as to its compatibility with the internal market irrespective of whether MCUs are segmented on the basis of bit-rate or end-use.

4.2.2 Geographic market definition

4.2.2.1 The Notifying Party’s view

(34) In line with Commission’s previous decisions, the Notifying Party considers that the geographic market for semiconductors (and sub-segments) is global because: (i) customers are large companies that purchase semiconductors on a worldwide basis; (ii) there are no national quotas, tariffs or technical specifications; (iii) there are no significant price differences between countries; (iv) transport costs are very low; and (v) suppliers compete at a worldwide level.

4.2.2.2 The Commission’s assessment

(35) In NXP/Freescale, the Commission found that the geographic scope of the semiconductor markets was likely worldwide in scope, as competition between suppliers is worldwide, transport costs are very low, and price differences among regions are small. The exact market definition was, however, ultimately left open.23

(36) In Qualcomm/NXP, the Commission concluded that the geographic scope of the semiconductor product markets at issue in that case, including semiconductors for automotive applications, was likely worldwide.24

(37) The results of the market investigation in the present case confirm that the geographic scope of the semiconductor markets is likely to be worldwide. Respondents to the market investigation have submitted that the semiconductor industry has a global footprint, with supply chain spanning across multiple countries and in relatively free market conditions. Suppliers would be generally able to compete with each other across geographical boundaries.25

4.2.2.3 Conclusion on geographic market definition

(38) For the purposes of this decision, the Commission therefore concludes that the geographic scope of the semiconductor product markets relevant in this case, notably MCUs (and sub-segments), is likely worldwide.

5. COMPETITIVE ASSESSMENT

5.1 Affected Markets

(39) According to the Notifying Party, the Parties are mainly active in the manufacture and supply of distinct semiconductor products. Infineon’s focus would be on power semiconductors, whereas Cypress’ focus would be on connectivity products and MCUs.

(40) As already mentioned above in section 4, the Parties overlap primarily in the design, manufacture and sale of MCUs. The following table is based on the data provided by the Notifying Party and relates to the different segments where the Parties’ activities overlap:

competitors, like Texas Instruments (with a market share of [10-20]%) and NXP ([10-20]%) will also continue to provide viable supply alternatives to customers.

(51) On all alternative market definitions in the MCUs sector, market share data provided by the Notifying Party shows that the Parties’ combined market share will remain below 20% and that several significant competitors, with market shares higher than that of the merged entity, will remain active on the market.27

(52) The results of the market investigation confirms that the Parties are not close competitors for MCUs in general and 16-bit MCUs in particular. The majority of respondents considers that, after the merger, there will be sufficient supply alternative and that the merged entity will face competitive constraints from other suppliers with respect to 16-bit MCUs and MCUs in general.28 With specific reference to the 16-bit segment, the majority of respondents indicates that the Transaction will not change competitive dynamics considering that, while Infineon is a key player, Cypress has a more limited role.29 Similar views have been expressed with respect to the automotive segment: a reasonable line-up of suppliers would remain in terms of capacity, technological and commercial competition. Furthermore, the Parties’ products are considered to be mainly complementary.30

(53) In light of the above, the Commission concludes that the Transaction does not give rise to serious doubts with regard to its compatibility with the internal market as a result of possible horizontal effects in the 16-bit MCUs market.

5.3 Possible conglomerate effects in semiconductors markets

5.3.1 Introduction

(54) In the majority of circumstances, conglomerate mergers do not lead to any competition problems but in certain specific cases there may be harm to competition.31 The main concern in the context of conglomerate effects is that of foreclosure.32 Conglomerate mergers may allow the merged entity to combine products in related markets and this may confer on the merged entity the ability and incentive to leverage a strong market position from one market to another by means of tying or bundling, or other exclusionary practices.33

(55) In assessing the likelihood of conglomerate effects, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals, second, whether it would have the economic incentive to do so and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers. In practice, these factors are often examined together as they are closely intertwined.34

(56) As expressly submitted by the Notifying Party, the key strategic rationale of the Transaction is to combine two complementary product portfolios to enable the merged entity to offer a broad suite of solutions to its customers. Currently, Infineon’s key focus is the manufacture and supply of power semiconductors and security solutions. By contrast, Cypress is focused on the supply of MCUs and connectivity products. Accordingly, the Commission has examined whether the Transaction would give rise to conglomerate effects by foreclosing competitors in one or more of the semiconductors markets.

5.3.2 The Notifying Party’s view

(57) The Notifying Party submits that the Transaction would not give rise to any conglomerate concerns.

(58) First, the Parties would have no ability to foreclose competitors considering that their respective market shares do not exceed 30% in relation to any of the neighbouring markets on which they are active.

(59) Furthermore, following the Transaction, the merged entity will continue to face stringent competition from a large number of international and local suppliers. Post-Transaction, Infineon will be the eighth largest global semiconductor supplier and many of its competitors would have a similar range of products as the merged entity.

(60) The Notifying Party further submits that although the merged entity may cross- sell, bundle or integrate the enlarged portfolio, it would have no incentive to attempt to foreclose competitors. Given the size, strength and international presence of the Parties’ competitors, any attempt by the merged firm to force them out of a particular product market would likely be met by a counter-strategy.

(61) In addition, the Parties’ customers would have sufficient buyer power to deter anticompetitive foreclosure. The market would be characterised by countervailing buyer power of large, sophisticated, well informed Tier 1 suppliers, OEMs and distributors, which would not accept any bundling practices which would not suit their interests and would purchase standalone components from rival suppliers (following a “mix-and-match” approach).

(62) Finally, the Notifying Party submits that in no circumstances the integrated products or bundled solutions would represent the only offering provided by the merged entity. In all cases, the individual products will remain available as standalone products (in line with customers’ tender processes expectations).

5.3.3 The Commission’s assessment

5.3.3.1 Ability to foreclose

(63) In order to have the ability to foreclose rivals, the merged entity must have a significant degree of market power in at least one of the markets concerned. That is, at least one of the Parties’ products must be viewed by many customers as particularly important and there must be few relevant alternatives for that product.35

(64) In this respect, the Commission notes that the merged entity would have a market share of [20-30]% in the market for 16-bit MCUs. Moreover, there are at least two significant competitors with a comparable market position (Renesas and Texas Instruments) and a third competitor with a market share close to 15%. The Commission is therefore of the view that based on its position in the market for 16-bit MCUs, it is unlikely that after the Transaction the merged entity will have the ability to leverage its position into other neighbouring markets. Moreover, the Parties’ combined market share in other MCU markets will remain below 20%.

(65) The Notifying Party has also provided the Parties’ and competitors’ market shares for other semiconductors products that the merged entity envisage to [details on strategy] to obtain the planned synergies. According to those market data, the merged entity’s estimated market shares will not exceed 30% in any of those semiconductors markets and significant competitors will remain active in each market.36

(66) The results of the market investigation confirm that the Parties do not sell any product that would be difficult to source from alternative suppliers. Respondents thus indicated that alternatives would remain on the market for each product of the respective product portfolio and that other competitors would have capability to supply equivalent or similar products.37

(67) Few respondents expressed concerns with respect to the automotive sector and submitted that through the offering of a large range of automotive semiconductors, the merged entity would have an advantage over its main competitors.38 However, the majority of respondents to the market investigation confirmed that customers would be able to procure automotive semiconductors from the Parties’ competitors and mix-and-match them as an alternative to the merged entity’s bundle.39 In particular, it has been argued that while bundled solutions are attractive from an end customer perspective, as they allow the simplification of the supply chain and possibly cost savings, they would not preclude sophisticated customers like automobile manufacturers from negotiating separate deals with alternative suppliers to replace one or more of the bundled products. Most of automotive customers would have internal engineering resources to mix-and-match different products from different sources.40

(68) Based on the above, the Transaction is unlikely to confer the merged entity with the ability to leverage its market position in the automotive MCUs markets to foreclose competitors in closely related markets.

5.3.3.2 Incentive to foreclose

(69) The Commission has also assessed whether the merged entity will have an incentive to engage in bundling of different semiconductors, to foreclose rivals from effectively competing for customers who purchase different products.

(70) The merged entity will continue to face several credible competitors, many of which are able to offer the same range of products (as single solutions or bundles) as the Parties. These suppliers would thus be able to respond to the merged entity bundling initiatives by offering equally attractive solutions. Accordingly, the market investigation confirms that, after the Transactions, by integrating their respective product portfolios, the Parties will not gain a competitive advantage on their main competitors, but rather achieve the same breadth of offer.41

(71) The possible sale of bundles at a discount by the merged entity would therefore unlikely lead to the marginalisation of competitors, who will be able to replicate the offers and/or to propose different discounts on other bundles.

(72) Consistently with this view, the majority of the participants to the market investigation submitted that the merged entity, through the offering of bundles including different products, would not have the incentive to foreclose competing operators in the MCUs segment.42

(73) Based on the above, the Commission considers that the merged entity is unlikely to have the incentive to foreclose competitors in semiconductors markets by bundling different products post-Transaction.

5.3.3.3 Impact on effective competition

(74) Regardless of whether the merged entity has either the ability or the incentive to foreclose rivals in the semiconductors markets by bundling different products, the Commission considers that such strategy would not have an appreciable impact on competition.

(75) Any potential impact of such bundling strategy would be mitigated by the ability of competitors to react to such strategy by (i) lowering the price of single products, or (ii) offering similar or other bundles based on their portfolio. This could be particularly the case with respect to the Parties’ main competitors (NXP, Renesas, Texas Instruments, etc.), that have a similar market presence and comparable products portfolios.

(76) The results of the market investigation confirm the limited effect of the Transaction. Notably the vast majority of the participants to the market investigation submitted that the Transaction would either positively impact the markets for MCUs, 16-bit MCUs or automotive MCUs or not affect these markets at all.43 Similarly, the vast majority of respondents submitted that the Transaction would not have a negative impact on their activity.44

5.3.3.4 Conclusion on conglomerate effects

(77) In light of the above, the Commission considers that the Transaction does not give rise to serious doubts with regard to its compatibility with the internal market as a result of conglomerate effects in the semiconductors markets.

6. CONCLUSION

(78) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the ‘Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (‘TFEU’) has introduced certain changes, such as the replacement of ‘Community’ by ‘Union’ and ‘common market’ by ‘internal market’. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the ‘EEA Agreement’).

3 Publication in the Official Journal of the European Union No C 314, 18.09.2019, p. 15.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

5 Commission decisions of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 14 and of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, recital 33.

6 Commission decision of 24 June 2002 in case M.2820 - STMicroelectronics/Alcatel Microelectronics, paragraph 11. A similar conclusion was reached in Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraphs 44- 45.

7 Throughout this decision, when the Commission refers to the (number of) respondents in relation to a given question of the market investigation, this excludes all respondents that have not provided an answer to that question or replied “I do not know”, unless stated otherwise. For example, “a majority of respondents” means a majority of respondents having replied to a given question and not having ticked “I do not know”.

8 See replies to Commission questionnaires Q1 to competitors and customers, question 3.

9 Commission decisions of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 38 and of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, recital 33.

10 Commission decisions of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraphs 39 and 46, and of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, recital 33.

11 See replies to Commission questionnaires Q1 to competitors and customers, question 4.

12 Commission decisions of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraphs 39-40 and 46, and of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, recital 33. See also Commission decisions of 02 December 2009 in case M. 5535 - Renesas Technology/NEC Electronics and of 26 January 2011 in case M.5984 - Intel/Mcafee, paragraphs 23-30.

13 See replies to Commission questionnaires Q1 to competitors and customers, question 5.

14 Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, recital 30.

15 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 46.

16 See replies to Commission questionnaires Q1 to competitors and customers, questions 6 and 6.1.

17 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraphs 44-45.

18 See replies to Commission questionnaires Q1 to competitors and customers, questions 7 and 7.1.

19 See replies to Commission questionnaires Q1 to competitors and customers, questions 9 and 9.1. One respondent to the market investigation just added that in its opinion “Consumer” would be a broad category and that a large number of general purpose MCUs could serve as ‘consumer’ MCUs. Moreover, there would be other minor categories of application-specific MCUs based on specific use-cases or sectors, such as, motor control MCUs, smart metering MCUs, healthcare-optimized MCUs, smart appliance MCUs, defence MCUs, space MCUs, aerospace MCUs, etc. (NXP and MicroChip, replies to question 9.1).

20 See replies to Commission questionnaires Q1 to competitors and customers, questions 8 and 8.1.

21 Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, recital 35.

22 See replies to Commission questionnaires Q1 to competitors and customers, questions 10 and 10.1.

23 Commission decision of 17 September 2015 in case M.7585 - NXP Semiconductors/Freescale Semiconductor, paragraph 58.

24 Commission decision of 18 January 2018 in case M.8306 - Qualcomm/NXP Semiconductors, recital 242.

25 See replies to Commission questionnaires Q1 to competitors and customers, questions 11 and 11.1.

26 Where this decision makes reference to "affected markets" it refers to instances where: for horizontal overlaps, both Parties are engaged in business activities in the same relevant market and where the concentration will lead to a combined market share of 20% or more; for vertical relationships, where one or more of the Parties are engaged in business activities in a relevant market which is upstream or downstream of a relevant market in which any other party to the concentration is engaged, and any of their individual or combined market share at either level is 30% or more, regardless of whether there is any existing supplier / customer relationship between the Parties. See section 6.3 of Annex I (Form CO relating to the notification of a concentration pursuant to regulation (EC) No 139/2004) of Commission Implementing Regulation (EU) No 1269/2013 of 5 December 2013 amending Commission regulation (EC) No 802/2004 implementing Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings (OJ L 336, 14.12.2013, P.1-36).

27 Form CO, paragraph 143.

28 See replies to Commission questionnaires Q1 to competitors and customers, questions 13.1 and 13.2.

29 See replies to Commission questionnaires Q1 to competitors and customers, question 13.2.1.

30 See replies to Commission questionnaires Q1 to competitors and customers, question 13.3.1.

31 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings (“Non-Horizontal Merger Guidelines”), OJ C 265, 18.10.2008, paragraph 92.

32 Non-horizontal Merger Guidelines, paragraph 93.

33 Non-horizontal Merger Guidelines, paragraph 93.

34 Non-horizontal Merger Guidelines, paragraph 94.

35 Non-horizontal Merger Guidelines, paragraph 99.

36 Form CO, paragraphs 105-138, 161 and 171-2, Table 4. Notably the Notifying Party has provided market information for the following products: (i) Non automotive MEMS - microelectromechanical systems – sensors, (ii) Security ICs, (iii) Automotive MCUs – ADAS, (iv) Power transistors and thyristors, (v) Gate driver ICs, (vi) Power ICs, (vii) Small signal and discretes,

(viii) IoT MCU, (ix) Connectivity ICs – Wi-Fi, (x) Connectivity ICs – Bluetooth, (xi) Connectivity ICs – BLE, (xii) NOR flash memory semiconductors.

37 See replies to Commission questionnaires Q1 to competitors and customers, questions 16 and 16.1. It is worth noting that of the only two respondents who stated that the Parties have “must-have” products, one did not give any further explanation and the other confirmed that the market would be competitive but once a product is designed into a particular product, it could be difficult to change (Avnet, question 16.1).

38 See replies to Commission questionnaires Q1 to competitors and customers, questions 17, 17.1 and 20.1.

39 See replies to Commission questionnaires Q1 to competitors and customers, questions 19 and 19.1.

40 NXP’s and Renesas’ replies to Commission questionnaires Q1 to competitors and customers, question 19.1.

41 This is particularly true for automotive components, see replies to Commission questionnaires Q1 to competitors and customers, question 17.1.

42 See replies to Commission questionnaires Q1 to competitors and customers, questions 20.1, 20.2, and 20.3.

43 See replies to Commission questionnaires Q1 to competitors and customers, questions 22.1, 22.2 and 22.3. The only negative replies were connected to the possible bundling in the automotive MCUs sector, on which see previous paragraph (67).

44 See replies to Commission questionnaires Q1 to competitors and customers, questions 23 and 23.1.