Commission, July 27, 2018, No M.8880

EUROPEAN COMMISSION

Judgment

OETKER / HENKELL / FREIXENET

Subject: Case M.8880 – Oetker / Henkell / Freixenet

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 22 June 2018, the European Commission received a notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Dr. August Oetker KG (‘Oetker’) intends to acquire — through its wholly-owned subsidiary Henkell International GmbH (‘Henkell’) — within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of Freixenet, S.A. (‘Freixenet’) (3) (Henkell and Freixenet are designated hereinafter as the ‘Parties’).

1. THE PARTIES AND THE OPERATION

(2) Henkell is a subsidiary of Henkell & Co. Sektkellerei KG, which is the parent company of the Oetker Group’s division for sparkling wine, wine and spirits. Oetker is a multinational group with more than 400 companies worldwide, present across several business areas such as food (including Dr. Oetker, Martin Braun and Conditorei Coppenrath & Wiese groups); beer and non-alcoholic beverages (including the Radeberger group), and other interests such as luxury hotels, information technology or banking. Henkell is active in the production and supply of sparkling wines, still wines and spirits, but its core business is within sparkling wines.

(3) Freixenet is the parent company of the Freixenet Group, a Spanish-based group almost exclusively dedicated to the sparkling wine (notably Spanish sparkling wine named Cava) and still wine businesses. The capital of Freixenet is held by members of the founding families of Freixenet.

(4) On 16 March 2018, Henkell signed a contract to purchase 50.67% of the share capital of Freixenet from the family members (the ‘Transaction’). Post completion, […] Henkell will retain […] solely control over Freixenet.

(5) The Transaction therefore constitutes a concentration within the meaning of Artcile 3(1)(b) of the merger Regulation.

2. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world–wide turnover of more than EUR 5 000 million (Henkell: EUR 11 601 million, Freixenet: EUR 501 million) (4). Each of them has an EU-wide turnover in excess of EUR 250 million (Henkell: EUR […], Freixenet: EUR […]). They do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

3. COMPETITIVE ASSESSMENT

3.1. Introduction

(7) Both parties are active in the manufacture and supply of sparkling wines. Sparkling wine refers to wines made effervescent by significant levels of carbon dioxide obtained through a second fermentation process. Under the classical method, used for instance for French Champagne, German Sekt, Italian Spumante and Prosecco or Spanish Cava, the second fermentation takes place in the bottle. Other similar products, like Lambrusco, are manufactured through different methods where the fermentation takes place mainly in tanks. Due to its festive character, the consumption of sparkling wine is associated with the celebration of festivities and events. For that reason, the purchase of sparkling wine presents also a strong seasonality, with sale peaks at the end of the year, as well as around carnival and Easter.

3.2. Relevant Product market

(8) The Transaction concerns essentially sparkling wines as the Parties are both active in the production and supply of sparkling wines, but focus on different product types. While Freixenet is mostly active in Cava from Spain, Henkell focuses on Sekt from Germany, Prosecco from Italy as well as a number of local sparkling wine types.

(9) The Parties commercialize their products through different distribution channels such as the off-trade (sales to retailers etc), the on-trade (sales to bars, clubs and restaurants etc) and the travel retail channels, (5) but the off-trade channel represent the most significant part of their sales (generally above 80%).

3.2.1. Product market definition

3.2.1.1. Commission's precedents

(10) In a previous decision, the Commission has considered that still wines, sparkling wines (other than Champagne), Champagne, fortified wines (such as port and sherry) and light aperitifs constituted a relevant product market for the assessment of the then notified transaction. (6) The Commission has also analysed the possibility of further segmenting the wine market according to colour, origin and price but the exact market definition was ultimately left open. (7)

3.2.1.2. Parties' view

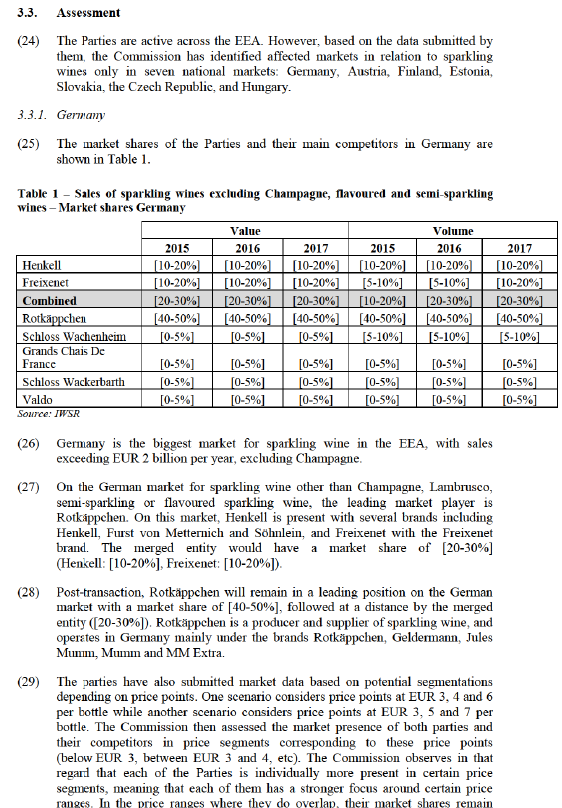

(11) The Parties agree with the delineation whereby the product market consists of sparkling wines other than Champagne, and also propose to consider a product market definition that would exclude from the sparkling wines category Asti, Lambrusco, semi-sparkling or flavoured sparkling wines, i.e. all those products that fall in the category "all others" used by the International Wines and Spirits Report (IWSR).

(12) The Parties' submit that the market should not be further segmented according to price or price ranges. In particular, they argue that sparkling wines form a price continuum, meaning that there is a continuous distribution of prices with no clear break and, therefore, any hypothetical segmentation would be largely subjective depending on the price points considered to establish such segments. The Parties argue that, apart from Champagne which is considered as a separate market due to its premium character and significantly higher price, in general, there is strong price competition between the different categories of sparkling wine bearing in mind that within all of them there are brands with very varied positioning, ranging from premium brands, with more expensive prices, to low value products, with very low prices.

3.2.1.3. Commission's assessment

(13) The vast majority of respondents of the market investigation suggest that Champagne and other sparkling wines are not substitutable from a final consumer perspective, (8) and neither are Lambrusco, semi-sparkling or flavoured sparkling wine. (9)

(14) On that basis, the Commission considers that, for the purposes of this decision, the relevant product market include sparkling wines other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine.

(15) The Commission also investigated whether further criteria would be relevant for the product market segmentation. Some responses of customers and competitors indicate that, as concerns sparkling wines markets, a segmentation based on prices would be conceivable as competition takes place within price segments, but there is no clear consensus on the boundaries of the relevant segments. (10) There were no indications either in these responses that a distintion in the sparking wines markets based on colour or origin would be relevant in the present case.

(16) However, the Commission considers that it can be left open whether the market should be segmented on the basis of the price or price ranges as the Transaction would not give raise to competition concerns under any conceivable alternative market segmentation based on the price or price ranges.

3.2.2. Geographic market definition

(17) The Commission previously considered that the geographic scope of the markets for the production and distribution of spirits and wines are national in scope, mainly because of strong national preferences and consumption behaviours, and despite the fact that some markets, for spirits in particular, could become more international in nature due to the emergence and promotion of brands across many national markets. (11)

(18) The Parties agree with this approach.

(19) Third parties in the market investigation in the present case have confirmed that the markets for sparkling wines other than Champagne, Lambrusco, semi- sparkling or flavoured sparkling wine, are national in geographic scope. (12)

(20) Therefore, the Commission considers that the geographic scope of the sparkling wines other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine is national.

3.2.3. Conclusion

(21) The Commission concludes that, for the purposes of this decision, the relevant product market include sparkling wines other than Champagne, Lambrusco, semi- sparkling or flavoured sparkling wine.

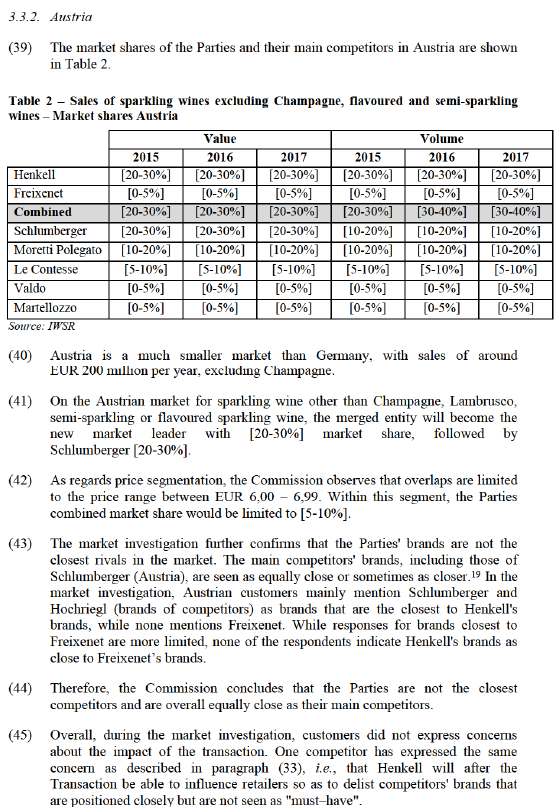

(22) For the purpose of this decision, it can be left open whether the market should be segmented on the basis of the price or price ranges as the Transaction would not give rise to competition concerns under any plausible alternative market segmentation based on the price or price ranges.

(23) The Commission considers that the geographic scope of the for sparkling wines other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine is national.

limited. Henkell is typically stronger in price categories where Freixenet is less present, and vice versa. This shows that the Parties are not the closest competitors, because they are focussing on products belonging to different price segments.

(30) The fact that the Parties are not the closest competitors is confirmed by market studies carried out by external consultant Gfk. These market studies analysed customers’ switching behaviour from Freixenet to other brands. The Commission observes in these studies that while Henkell is close to Freixenet with brands such as Henkell and Fürst von Metternich, competitor Rotkäppchen is nearly as close to Freixenet with its brand Mumm. The closest competitors to Freixenet according to this metric are other Spanish wines, indicating that while sparkling wines of different origins (such as Henkell and Freixenet) compete, those of similar origin might compete more closely.

(31) Overall, during the market investigation, customers did not express concerns about the impact of the transaction. Only one retailer active in Germany (13) claimed that the Transaction would have a negative impact on the market. The retailer claimed that his position in negotiations with sparkling wine suppliers might deteriorate due to the amount of suppliers being reduced from four to three and the concentration of important brands in the hands of a single supplier.

(32) The Commission has therefore assessed whether the Parties market share might underestimate the actual degree of market power as their brands would have such a "must-have" status for retailers. While most retailers identify several brands, e.g. Rotkäppchen, together with Henkell and Freixenet as "must-have products", none of the respondents consider Henkell and/or Freixenet as the only "must-have" products. (14) In that regard, a report from the German Bundeskartellamt of 2014 stated that for sparkling wines, customers' loyalty to a store exceeds their loyalty to a brand. (15) The Commission therefore concludes that Henkell and Freixenet's brands are not "must-have” brands or at least that they do not have a "must-have" status on the German market which is superior to other competing brands.

(33) Some competitors have also expressed concerns on the Transaction. These competitors have, in particular, explained that Henkell will, after the Transaction, expand its portfolio, that would cover most "must–have" brands and would address all basic consumer needs. (16) As a result, Henkell will be able to influence retailers so as to delist competitors' brands that are positioned closely but are not seen as "must-have".

(34) The Commission assessed whether suppliers of sparkling wine such as the merged entity would be able to influence retailers on the brands to delist or to keep on the shelves as claimed by these competitors. However, as explained above in paragraph (32), the Parties' brands are not "must-have" brands, a retailer is not bound to keep the Parties' products on the shelves and is able to diversify to the Parties' competitors.

(35) Moreover, in its report of 2014 mentioned above in paragraph (32) describing the competitive dynamics between suppliers and retailers in sparkling wine, the German Bundeskartellamt explained that suppliers of sparkling wine are significantly dependent on off–trade retail. Unlike other markets, such as spirits, beer or soft drinks, the off-trade channel in Germany amounts for more than 80% of sparkling wine sales. In Germany, Henkell's top five off-trade customers represent […] of its sales in 2017. For Freixenet, almost […] of its German sales in 2017 are concentrated at its top four off-trade customers.

(36) The fact that sparkling wine suppliers are dependent on a limited amount of off- trade customers is exacerbated by the fact that sales of sparkling wine are strongly driven by promotional activities and by its seasonal character (promotions mainly take place during the last three montshs of the year). The market investigation shows that prices and promotions are among the main drivers of competition, and are more important than for instance brand recognition. (17) This is also recognised in the 2018 report of consultant IWSR, which states that "[…] it continues to be driven by promotional mechanics." (18) It is the retailers who decide when and to what extent promotional activities are performed. The Parties to this extent submit that the promotions are not decided by the retailers' purchase department but by their sales department and they are often not informed of promotional activities until after they have already been introduced by the retailer.

(37) In the light of the above, it does not appear that suppliers of sparkling wine such as the merged entity would be able to influence retailers on the brands to delist or to keep. Consequently, the Transaction would have no impact on the choice of brands by the retailers.

(38) On the basis of the above, the Commission considers that the Transaction does not raise serious doubts as regards its impact on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine in Germany, irrespective of any further plausible market segmentation based on the price or price ranges.

(46) However, concentration of the customer base in Austria is also significant. The Parties submit that 88% of the market share in grocery retail in Austria is held by three players. This is in line with the concentration of the customers of Henkell, for which the largest four represent […] of its Austrian sales, (20) and for Freixenet, for which the largest three represent […] of its Austrian sales. (21)

(47) Moreover, as explained above in paragraph (36), the balance of power in negotiations for sparkling wine lies with retailers. Sparkling wine producers are dependent on these retailers and have few alternative outlets. Given that these retailers, through their control of promotional activities, have a significant influence over the main driver of sales, it is unlikely that the merged entity would be able to influence the choice of brands by the retailer.

(48) On the basis of the above, the Commission considers that the Transaction does not raise serious doubts as regards its impact on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine in Austria, irrespective of any further plausible market segmentation based on the price or price ranges.

3.3.3. Estonia

(49) In Estonia, sales of sparkling wine, excluding Champagne, accounted for EUR 32 million in 2017.

(50) On the Estonian market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine, Henkell is mostly active with its brand Törley and, to a lesser extent, with other brands such as Mionetto and Henkell Sekt, while Freixenet is active with the Freixenet brand. Henkell is the market leader, while Freixenet is n°3, with sales under EUR […].

(51) The merged entity would remain market leader with a combined market share of [40-50%] (Henkell: [30-40%], Freixenet: [5-10%]) followed by SPI ([10-20%]). Other players active in Estonia are Grand Chais De France and Zonin (between [5-10%] and [5-10%]), Castel and Codorniu.

(52) In the market investigation, customers and competitors were overall not concerned about the Transaction. One retailer indicated that the Transaction might impact the competition between Prosecco and Cava. The Commission however notes that Henkell is only active in Prosecco with its brand Mionetto, which accounts to only […] of Henkell's sales in Estonia. (22) There are a multitude of other Prosecco brands from competitors remaining on the market post– Transaction. This is also illustrated by Henkell's share in Prosecco in Estonia amounting to […]. There are also several Cava brands of competitors remaining on the market, including those of Cordoniu and García Carrión.

(53) As regards other types of sparkling wine, the Parties are mainly active within different price categories. While Henkell's main brand Törley, accounting for […] of its sales in Estonia, is sold at an average price of EUR […], Freixenet is sold at EUR […]. (23) This price difference shows that the Parties are relatively distant competitors in Estonia.

(54) On the basis of the above, the Commission considers that the Transaction does not raise serious doubts as regards its impact on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine in Estonia, irrespective of any further plausible market segmentation based on the price or price ranges.

3.3.4. Finland

(55) In Finland, sales of sparkling wine, excluding Champagne, accounted for EUR 87 million in 2017.

(56) On the Finnish market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine, Henkell is mostly active with its brands Mionetto, Henkell Sekt and Törley, while Freixenet is mostly active with its Freixenet brand and Castellblanch. Freixenet is the market leader, while Henkell is n°4. Off–trade retail is dominated by Alko Ab, the state monopoly on retail of alcoholic beverages above 5.5% alcohol content.

(57) The merged entity would remain market leader with a combined market share of [20-30%] (Freixenet: [10-20%], Henkell: [5-10%]), followed by Cordoniu ([5-10%]), Altia ([5-10%]) and Grands Chais De France ([5-10%]). Other players are Bernard Massard and Val D'Oca. In Finland, the parties are active in the same price ranges, and overlap in the price range EUR 7 to 15, where there combined market share is [20-30%] (Freixenet: [20-30%], Henkell: [5-10%]).

(58) However, the market investigation has not revealed any competition concerns arising from the Transaction in Finland.

(59) On the basis of the above, the Commission considers that the Transaction does not raise serious doubts as regards its impact on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine in Finland, irrespective of any further plausible market segmentation based on the price or price ranges.

3.3.5. Czech Republic

(60) On the Czech market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine, Henkell is present with a local flagship brand Bohemia Sekt in the Czech Republic. Freixenet sells the Freixenet brand. Freixenet does not have a sales organisation in the Czech Republic and operates through third-party distributors specialised in the (alcoholic) beverages sector.

(61) The Transaction gives rise to affected market in the Czech Republic, where the Parties would hold a combined share of [60-70%]. However the increments brought by Freixenet are particularly small: less than [0-5%]. In light of this limited increase, it is unlikely that the increment might be significant under any plausible market segmentation based on the price or price ranges. The Transaction will therefore not substantially modify the market structure in the Czech Republic.

(62) The market investigation has not, in general, revealed any competition concerns arising from the Transaction. However, one competitor currently active in Czech Republic explained that Freixenet's market share is not large today [0-5%], but could be increased post-merger through Henkell's distribution network. According to this competitor, it cannot be excluded that this increase would occur at the expense of other small competitors active in the Czech market.

(63) The Commission has carefully considered this statement. At this stage, it is however unclear how the more widespread distribution of Freixenet in the Czech Republic could hinder the development of small brands, as claimed by this competitor. No evidence in the market investigation suggests that Henkell attempted in the past to use its strong marker position to foreclose its rivals in the Czech Republic.The addition of Freixenet's turnover is very small (EUR […] compared to EUR […] for Henkell) and it therefore seems unlikely that the Transaction will change the ability of the merged entity to engage in a foreclosure strategy.

(64) On the basis of the above, the Commission considers that the Transaction does not raise serious doubts as regards its impact on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine in the Czech Republic, irrespective of any further plausible market segmentation based on the price or price ranges.

3.3.6. Slovakia

(65) Henkell is present with a local flagship brand, Hubert, in Slovakia. Freixenet sells the Freixenet brand. Freixenet does not have a sales organisation in Slovakia and operates through third-party distributors specialised in the (alcoholic) beverages sector.

(66) The Transaction gives rise to affected market in Slovakia, where the Parties would hold a combined share of [80-90%] on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine. However the increments brought by Freixenet are particularly small: less than [0-5%]. In light of this limited increase, it is unlikely that the increment might be significant under any plausible price market segmentation.The Transaction will therefore not substantially modify the market structure in Slovakia.

(67) The Commission has also considered whether the more widespread distribution of Freixenet in Slovakia could hinder the development of small brands. No evidence in the market investigation suggests that Henkell attempted in the past to use its market power to foreclose its rivals in Slovakia. As the addition of Freixenet's turnover is very small (EUR […] compared to EUR […] for Henkell), it seems unlikely that the Transaction will change the ability or the incentive of the merged entity to engage in a foreclosure strategy.

(68) On the basis of the above, the Commission considers that the Transaction does not raise serious doubts as regards its impact on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine in Slovakia, irrespective of any further conceivable market segmentation based on the price or price ranges.

3.3.7. Hungary

(69) Henkel is present with a local flagship brand, ie Törley, in Hungary. Freixenet sells the Freixenet brand. Freixenet does not have a sales organisation in these countries and operates through third-party distributors specialised in the (alcoholic) beverages sector.

(70) The Transaction gives rise to affected market in Hungary, where the Parties would hold a combined share of [60-70%] on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine. However the increments brought by Freixenet are particularly small: less than [0-5%]. In light of this limited increase, it is not likely that the increment might be significant under any plausible price market segmentation. The Transaction will therefore not substantially modify the market structure in Hungary.

(71) The Commission has also considered whether the more widespread distribution of Freixenet in Hungary could hinder the development of small brands. No evidence in the market investigation suggests that Henkell attempted in the past to use its market power to foreclose its rivals in Hungary. As the addition of Freixenet's turnover is very small (EUR […] compared to EUR […] for Henkell), it seems unlikely that the Transaction will change the ability of the merged entity to engage in a foreclosure strategy.

(72) On the basis of the above, the Commission considers that the Transaction does not raise serious doubts as regards its impact on the market for sparkling wine other than Champagne, Lambrusco, semi-sparkling or flavoured sparkling wine in Hungary, irrespective of any further plausible market segmentation based on the price or price ranges.

4. CONCLUSION

(73) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 230, 2.7.2018, p. 11.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 See Case M.5114 – Pernod Ricard/V & S (2008), paragraph 15.

6 Case M.5114 – Pernod Ricard/V & S (2008), paragraph 40.

7 Case M.5114 – Pernod Ricard/V & S (2008), paragraph 35, 38 and 39.

8 Questionnaire to customers, question 6; and Questionnaire to competitors, question 6.

9 Questionnaire to customers, question 7; and Questionnaire to competitors, question 7.

10 Questionnaire to customers, question 8; and Questionnaire to competitors, question 8.

11 See Commission Decision in Case M.5114 – Pernod Ricard/V & S (2008), paragraphs 42-43.

12 Questionnaire to customers, questions 11-12; and Questionnaire to competitors, questions 11-12.

13 Questionnaire to customers, question 36.

14 Questionnaire to customers, question 15.2.

15 Bundeskartellamt – Sektoruntersuchung Lebensmitteleinzelhandel, September 2014.

16 Call with a competitor on 10 July 2018; Call with a competitor on 12 July 2018.

17 Questionnaire to customers, question 13; and Questionnaire to competitors, question 13.

18 Annex 7.2 to the Form CO, IWSR report on German market 2018.

19 Questionnaire to customers, question 16 and 17.

20 The Notifying Parties' response of 18 July to the Commission's request for information.

21 The Notifying Parties' response to question 28 of the Commission's second request for information.

22 Annex RFI2-H-3 to the Form CO.

23 The Notifying Parties' response to question 1 of the Commission's second request for information.