Commission, September 16, 2019, No M.9452

EUROPEAN COMMISSION

Judgment

GLOBAL PAYMENTS / TSYS

Subject: Case M.9452 – Global Payments / TSYS

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 9 August 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Global Payments Inc. (“Global Payments”, US) enters into a full merger within the meaning of Article 3(1)(a) of the Merger Regulation with Total System Services, Inc. (“TSYS”, US).3 Global Payments and TSYS are designated hereinafter as the “Parties” or the “Notifying Parties”.

1. THE PARTIES

(2) Global Payments is a global provider of payment solutions, which offers services including enterprise and payment management solutions, payment card processing, online payment portal solutions, and merchant acquiring.

(3) TSYS is a global provider of payment solutions, which offers services including payment card processing, merchant acquiring services, and products, such as software for payment card processing.

2. THE OPERATION

(4) On 27 May 2019, Global Payments entered into an agreement and plan of merger with TSYS pursuant to which TSYS will merge with and into Global Payments, with Global Payments being the surviving entity (the “Transaction”). After the proposed Transaction is completed, the separate corporate existence of TSYS will terminate and holders of TSYS common stock will receive 0.8101 shares of Global Payments common stock for each TSYS share. As a result, former holders of TSYS stocks will own approximately 48% and former holders of Global Payments shares will hold approximately 52% of the shares of the combined entity.

(5) The Transaction would therefore give rise to a concentration within the meaning of Article 3(1)(a) of the Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (Global Payments: EUR 3 050 million; TSYS: EUR 3 414 million).4 Each of them has an EU-wide turnover in excess of EUR 250 million (Global Payments: EUR […] million; TSYS: EUR […] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

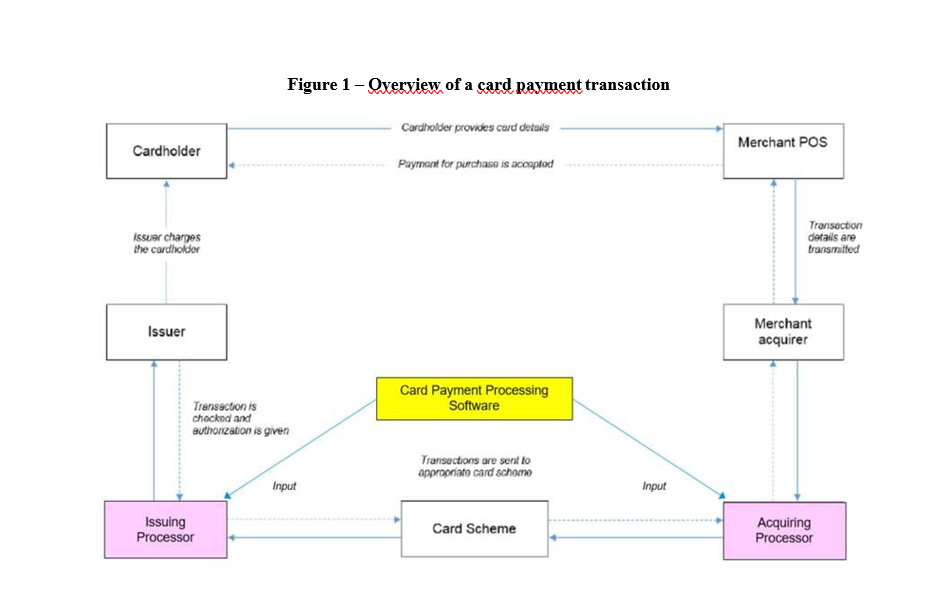

(7) The Transaction combines two providers of payments technology services. The Parties’ activities overlap in relation to card payment systems. Figure 1 below illustrates the key relationships and the main players involved in card-based payment transactions.

(8) Card payment systems allow a cardholder to use a card (e.g., a credit or debit card) to pay for a product or a service without using cash. Card payment systems connect merchants to financial institutions and they cover the whole transaction from the moment the client pays at the point of sale ("POS") until the moment the merchant’s account is credited.

(9) A card payment transaction starts with a purchaser using a payment card to buy goods or services from a merchant, either in a physical shop or online. The merchant seeks authorisation for the transaction. This authorisation request is initiated from the merchant’s physical card reader (a POS terminal for card-present transactions) or at a virtual POS (e.g., a web-based portal which enables similar functionality for card-not-present transactions).

(10) The authorisation request is transmitted to the merchant acquirer (a bank or another financial services provider). The merchant acquirer has a contractual relationship with the merchant (who is thus the customer of merchant acquirers) and ensures that merchants are paid for their sales through cards. These services are referred to as merchant acquiring.5

(11) The merchant acquirer receives the authorisation request together with the transaction details. The request and the details are then routed to the relevant card scheme to ensure POS authorisation. These services are referred to as acquiring processing. Merchant acquirers either provide acquiring processing in-house or outsource it to third-party processors.6

(12) The card scheme receives the authorisation request and the details of the transaction from the acquiring processor, identifies the card issuer (usually a bank) and sends the transaction to the issuing processor. The issuing processor requests payment authorisation from the issuer. It also maintains and manages local and international blocking lists, verifies card limits, manages card accounts, and generates cardholder statements and invoices. These services are referred to as issuing processing.7

(13) The issuer then determines whether to approve the transaction based on the characteristics of the cardholder account (e.g., whether the cardholder has sufficient balance). The issuer can carry out issuing processing itself or outsource it to an issuer processor.

(14) Finally, the transaction response (approved, declined, or other) of the issuer returns to the merchant via the issuing and acquiring processors. In case of approval, the merchant releases the goods or services.

(15) To offer acquiring processing services, a merchant acquirer or an acquiring processor may use their own proprietary software or in-license processing software from a card processing software provider. To offer issuing processing services, an issuer or an issuing processor may use their own proprietary software or in-license processing software from a card processing software provider.

(16) The remainder of this Section discusses market definition in card payment systems markets which are relevant for the horizontal and non-horizontal analysis of the overlaps between the activities of the Parties.

4.1 Card Processing

4.1.1 Product Market Definition

(17) Card processing includes all technical services concerning payment card transactions.8 Card processing services include acquiring processing services and issuing processing services. In more detail:

(a) Acquiring processing relates to the merchant-oriented side of technically processing a card payment transaction. It includes the network routing of payments towards the corresponding issuer and the POS authorisation. Merchant acquirers can purchase processing services from third-party processors or source these services in-house;9 and

(b) Issuing processing relates to the issuer-oriented side of technically processing a transaction. It includes payment authorisation requests from the issuer, management of card accounts and credit card limits, and the preparation of cardholder statements and invoices. Issuers can purchase processing services from third-party processors or source these services in-house.10

4.1.1.2 Previous Commission decisions

(18) The Commission previously considered a distinct market for card processing and within that market, it has discussed the existence of separate relevant markets for acquiring processing services and issuing processing services.11 The exact market definition was ultimately left open.12

(19) Within acquiring processing, the Commission has identified a possible further sub- segmentation based on (i) the payment card scheme (national v. international) and (ii) the platform, distinguishing between physical POS terminals and through web- enabled interfaces (e-commerce).13 The exact market definition was ultimately left open.14

(20) With regard to issuing processing, the Commission has not considered any further market sub-segmentation.15

4.1.1.3 Notifying Parties’ view

(21) According to the Parties, there are indications that card processing should be split in two separate relevant markets: acquiring processing and issuing processing. The Parties submit that among other things, acquiring processing and issuing processing services have fundamentally different content and they target different customers; they have a different price structure; and the applicable regulatory framework is not the same.16

(22) The Parties do not consider that it is appropriate to sub-segment further each of the markets for acquiring processing and for issuing processing. Within acquiring processing, the Parties submit that is not necessary to sub-segment the market based on the payment card scheme or based on the platform.17

(23) The Parties also consider that it is not appropriate to distinguish separate markets between in-house card processing services and card processing services to third parties or more narrowly, between in-house acquiring processing services18 and acquiring processing services to third parties nor between in-house issuing processing services19 and issuing processing services to third parties.

(24) In any event, the Parties submit that the precise product market definition can be left open in this case, as the proposed Transaction does not give rise to competition concerns under any plausible (product) market delineation.

4.1.1.4 Commission’s assessment

(25) In this case, the exact product market definition can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition (including all card processing services; all issuing processing services; card processing services to third parties; issuing processing services to third parties).20

4.1.2 Geographic Market Definition

4.1.2.1 Previous Commission decisions

(26) The Commission has previously left open the question whether the provision of card processing services is national or EEA-wide in scope.21 When looking more narrowly into acquiring processing and issuing processing, the Commission also left the geographic market definition open, indicating that the relevant markets could be national or EEA-wide in scope.22

4.1.2.2 Notifying Parties’ view

(27) The Parties submit that each of the markets for acquiring processing and issuing processing is EEA-wide. In any event, the Parties add that the Transaction would not give rise to any competition concerns even if it was assessed on the narrowest plausible market definition, i.e., at national basis.23

4.1.2.3 Commission’s assessment

(28) The Commission’s market investigation did not provide any indications that would require the Commission to depart from its precedents on the geographic scope of the market for card processing.24

(29) In any event, for the purposes of this Decision, the exact geographic scope of the market for card processing can be left open, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition (i.e., at EEA-wide level or at national level).

4.2 Provision of card processing software

4.2.1 Product Market Definition

(30) Card processing software is an application and office software designed for and licensed to merchant acquirers and issuers (respectively enabling them to offer acquiring and issuing processing services in-house). Card processing software can also be licensed to acquiring and issuing processors who use the software to offer issuing and acquiring processing services to third parties.

4.2.1.1 Previous Commission decisions

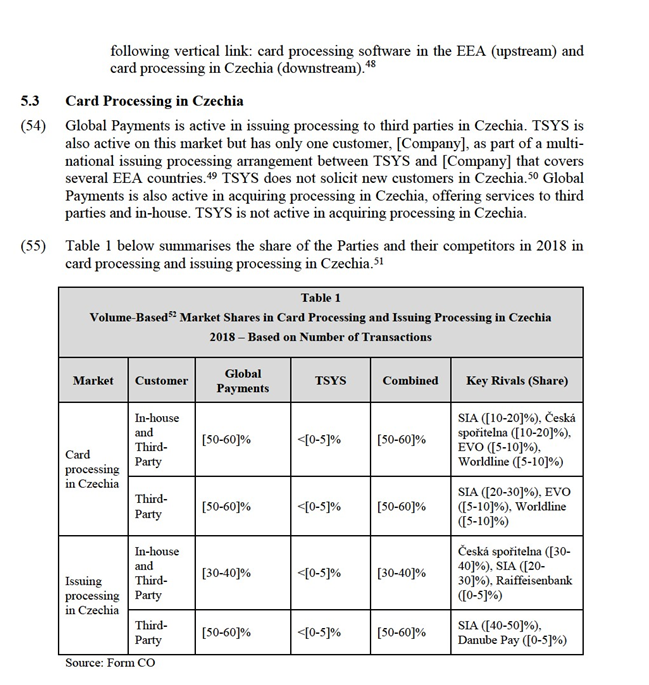

(31) The Commission has defined software markets based on criteria such as functionality, sector, and end-use of the software in question, further sub-segmented in some cases by application or level of sophistication.25 The Commission has not previously considered a market for the provision of card processing software.26

4.2.1.2 Notifying Parties’ view

(32) The Parties submit that there is one single product market including the provision of all types of card processing software. The Parties take the view that within this market, there are no separate markets for the provision of acquiring processing software and issuing processing software, because of supply-side substitutability. Most players designing and licensing card processing software offer both acquiring and issuing processing software.27

(33) That said, the Parties also acknowledged that there are “differences in the functionality depending on the intended use [of the software] such that a licensee who is using [software] only for acquiring processing could not use the product licensed for... issuing processing. Reflecting the difference in functionality, license fees differ depending on whether the software is used for acquiring processing, issuing processing, or both”.28

(34) In any event, the Parties add that the Transaction would not give rise to any competition concerns even if assessed on the basis of the all plausible market segments (i.e., provision of card processing software; provision of acquiring processing software; provision of issuing processing software).

4.2.1.3 Commission’s assessment

(35) In this case, the exact product market definition can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition (i.e., a single market including the provision of all card processing software or two separate markets, one for the provision of acquiring processing software and one for the provision of issuing processing software).

4.2.2 Geographic Market Definition

4.2.2.1 Previous Commission decisions

(36) In its decisional practice, the Commission took the view that the relevant geographic markets for application and office software, including software used in the banking and financial sector, are generally at least EEA-wide or worldwide in scope, because the solutions were offered on an EEA, or even on a global basis.29 The exact geographic market definition was left open.30

(37) The only exception in payment systems software is Worldline/Equens/Paysquare, where the Commission examined the relevant market for the software used by NSPs in Germany. As the software in that case was specifically meant to serve German card payment systems, the Commission found that the market was likely national in scope but in any event, the precise geographic scope of the market was left open because serious doubts arose under any plausible geographic market definition.31

4.2.2.2 Notifying Parties’ view

(38) The Parties submit that the relevant geographic market for card processing software is EEA-wide or global in scope.

(39) According to the Parties, card processing software can be sourced globally;32 the product offered does not differ between EEA countries and between the EEA and other regions;33 license fees do not differ materially between regions; and after-sales support can be provided remotely.34

(40) The Parties distinguish the geographic market definition for card processing software and the geographic market definition for software used by NSPs (considered in Worldline/Equens/Paysquare). Unlike card processing software which is sourced by merchant acquirers, acquiring processors, issuers, and issuing processors around the world, the software used by NSPs was tailored to German card payment systems.35

(41) The Parties add that the Transaction would not give rise to any competition concerns even if it was assessed on the basis of the narrower plausible geographic market definition, i.e., at EEA-wide level.

4.2.2.3 Commission’s assessment

(42) The Commission’s market investigation did not provide any indications that would require the Commission to depart from its precedents on the geographic scope of the markets for application and office software (including software used in the banking and financial sector).

(43) Card processing software is typically offered to different types of customers around the world (merchant acquirers, acquiring processors, issuers, and issuing processors) and it is not developed specifically for payment card transactions in one country. In this sense, the market for provision of card processing software differs from the market for provision of software for the activities of German NSPs, which the Commission considered as likely national in scope in Worldline/Equens/ Paysquare.36

(44) For the purposes of this Decision, the exact geographic scope of the market for card processing software can be left open, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under the narrower plausible geographic market definition (i.e., at EEA-wide level).

5. COMPETITIVE ASSESSMENT

5.1 Introduction

(45) Article 2 of the Merger Regulation requires the Commission to examine whether notified concentrations are compatible with the internal market, by assessing whether they would significantly impede effective competition in the internal market or in a substantial part of it, in particular as a result of the creation or strengthening of a dominant position.

(46) A merger giving rise to a significant impediment of effective competition may do so as a result of the creation or strengthening of a dominant position in the relevant market(s). Moreover, mergers in oligopolistic markets involving the elimination of important constraints that the parties previously exerted on each other, together with a reduction of competitive pressure on the remaining competitors, may also result in a significant impediment to effective competition, even in the absence of dominance.37

(47) The Commission Guidelines on the assessment of horizontal mergers under the Merger Regulation (the “Horizontal Merger Guidelines”)38 describe horizontal non- coordinated effects as follows: “A merger may significantly impede effective competition in a market by removing important competitive constraints on one or more sellers who consequently have increased market power. The most direct effect of the merger will be the loss of competition between the merging firms. For example, if prior to the merger one of the merging firms had raised its price, it would have lost some sales to the other merging firm. The merger removes this particular constraint. Non-merging firms in the same market can also benefit from the reduction of competitive pressure that results from the merger, since the merging firms’ price increase may switch some demand to the rival firms, which, in turn, may find it profitable to increase their prices. The reduction in these competitive constraints could lead to significant price increases in the relevant market.”39

(48) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force.40 That list of factors applies equally regardless of whether a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of these factors need to be present for significant non-coordinated effects to be likely. The list of factors, each of which is not necessarily decisive in its own right, is also not an exhaustive list.41

(49) Finally, the Horizontal Merger Guidelines describe a number of factors, which could counteract the harmful effects of the merger on competition, including the likelihood of buyer power, the entry of new competitors on the market, and efficiencies.

(50) In addition, the Commission Guidelines on the assessment of non-horizontal mergers under the Merger Regulation (the "Non-horizontal Merger Guidelines") distinguish between two main ways in which vertical mergers may significantly impede effective competition, namely input foreclosure and customer foreclosure.42

(51) For a transaction to raise input foreclosure competition concerns, the merged entity must have a significant degree of market power upstream.43 In assessing the likelihood of an anticompetitive input foreclosure strategy, the Commission has to examine whether (i) the merged entity would have the ability to substantially foreclose access to inputs; (ii) whether it would have the incentive to do so; and (iii) whether a foreclosure strategy would have a significant detrimental effect on competition downstream.44

(52) For a transaction to raise customer foreclosure competition concerns, the merged entity must be an important customer with a significant degree of market power in the downstream market.45 In assessing the likelihood of an anticompetitive customer foreclosure strategy, the Commission has to examine whether (i) the merged entity would have the ability to foreclose access to downstream markets by reducing its purchases from upstream rivals; (ii) whether it would have the incentive to do so; and (iii) whether a foreclosure strategy would have a significant detrimental effect on consumers in the downstream market.46

5.2 Overview of Affected Markets

(53) On the basis of the above market definitions, and the Parties' activities, the Transaction results in the following affected markets:

(a) Both Parties are active in issuing processing services in Czechia. Global Payments is also active in acquiring processing services in Czechia. The proposed Transaction gives rise to a horizontally affected market in card processing in Czechia;47 and

(b) TSYS develops and licenses its card processing software for acquiring and issuing processing in several EEA countries. The card processing software market is upstream to the Parties’ activities in card processing (downstream). The proposed Transaction gives rise to affected markets regarding the

(56) Taking into account services provided in-house and to third parties, in Czechia, the combined market share of the Parties in card processing (including both acquiring and issuing processing) would be [50-60]%. The Parties’ combined market share would be [30-40]% in issuing processing. In both cases, TSYS would contribute an increment of less than [0-5]% to the share of the combined entity. Taking into account services provided only to third parties, in Czechia, the combined market share of the Parties in card processing (including both acquiring and issuing processing) would be [50-60]%. The Parties’ combined market share would be [50- 60]% in issuing processing. In both cases, TSYS would contribute an increment of less than [0-5]% to the share of the combined entity.

(57) The Transaction does not give rise to serious doubts as to its compatibility with the internal market regarding the plausible markets for card processing (in-house and third-party or third-party only) or issuing processing (in-house and third-party or third-party only) in Czechia for the following reasons.

(58) First, under all plausible market definitions, the market position of TSYS remains minor. The share increment from TSYS remains always less than [0-5]%. Thus, the proposed Transaction is unlikely to cause significant change in the competitive landscape of card processing or issuing processing in Czechia.53

(59) Second, the combined entity will continue to face competitive constraints from several competitors active in card processing in Czechia, including SIA, Česká spořitelna, EVO, Worldline, and Danube Pay. Each of these players has a much higher share than TSYS in card processing and issuing processing in Czechia.

(60) Third, the Parties do not compete closely in card processing in Czechia:

(a) Global Payments offers card processing services both in-house and to third parties while TSYS offers card processing services only to third parties;

(b) Global Payments offers both issuing and acquiring processing, while TSYS only offers issuing processing; and

(c) Global Payments holds a significant market position in card processing in Czechia as a result of its 2004 acquisition of the previously state-owned central payment processor in the country. Global Payments serves many different third parties and proactively bids for new customer opportunities in the country. In contrast, TSYS offers issuing processing services only to one customer in Czechia, namely, [Company]. This is in the context of TSYS’ multi-national client relationship with [Company], covering several EEA countries.54 The Parties are not aware of any company other than TSYS that offers issuing processing services to [Company] in Czechia today.55 TSYS currently does not compete closely with Global Payments in the market for card processing or issuing processing in Czechia, as it does not proactively solicit customers in the country.

(61) In light of the above considerations, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in terms of its competition impact in the plausible markets for card processing or issuing processing in Czechia.

5.4 Card Processing Software in the EEA (Upstream) – Card Processing in Czechia (Downstream)

(62) TSYS licenses its card payment software (called Prime) for issuing processing in Bulgaria, Cyprus, Denmark, Estonia, Finland, Greece, Lithuania, Norway, Poland, Romania, Sweden, and the UK and for acquiring processing in Bulgaria, Germany, Greece, Lithuania, Poland, and Romania. The Parties submitted that TSYS’ market share is less than 10% in the upstream market for provision of card processing software in the EEA.56

(63) Card payment software is an important input for the services offered in the card processing market.57 Global Payments and TSYS are active in card processing in several EEA countries. The Parties submitted that their combined share exceeds 30% in card processing (or in any of its sub-segments) only in Czechia.58

(64) Thus, the Transaction results in one set of vertically affected markets: (i) card payment software in the EEA (upstream) and (ii) card processing in Czechia (downstream).59

5.4.1 Input Foreclosure

(65) The Transaction is unlikely to give rise to input foreclosure concerns. The combined entity would not have the ability to foreclose its downstream competitors in card processing in Czechia (under all plausible market delineations) by restricting access to card payments software in the EEA for the following reasons:

(a) Input foreclosure may raise competition problems when the upstream input is essential for the downstream product, e.g., when that product could not be manufactured or effectively sold on the market without the input.60 Based on the market investigation, in-licensing card payment software is not an essential input for entering and succeeding in the card processing market. Several issuers, issuing processors, merchant acquirers, and acquiring processors are active in this space having developed their own proprietary software in-house. This is the case with Global Payments in Czechia which uses its own proprietary software for the acquiring and issuing processing services it offers to third parties;61

(b) For input foreclosure to be a concern, the combined entity must have a significant degree of power in the upstream market.62 However, TSYS has a very limited position in card processing software in the EEA. In 2018, TSYS’ share in this market was [5-10]% (in terms of revenues63 from provision of card processing software).64 Moreover, TSYS competes with five other key rivals in this market (namely ACI Worldwide, RS2, Openway, Fiserv/First Data and HPS) and at least two competitors have a much higher share than TSYS in the EEA, namely, ACI Worldwide (which holds 17-50% in terms of revenues from provision of card processing software) and RS2 (which holds [10-20]% in terms of revenues from provision of card processing software);65 and

(c) The combined entity would not have the ability to foreclose downstream competitors, as it cannot negatively affect the overall availability of inputs for the downstream market.66 TSYS does not license its card processing software to any customer in Czechia as of 2019 (be it to a card processor; a merchant acquirer; or an issuer). In 2018, TSYS’ software was used for the issuing processing of [0-5]% of card transactions and the acquiring processing of [0- 5]% of card transactions in Czechia.67 TSYS would thus have no ability to foreclose downstream competitors in this country, by restricting access to its card processing software.

(66) As the Commission found that the combined entity would have no ability to foreclose card processing players in Czechia (under any plausible market delineation), it is not necessary to assess in detail the incentives of the combined entity or the overall impact of the Transaction on competition.

5.4.2 Customer Foreclosure

(67) The Transaction is unlikely to give rise to customer foreclosure concerns. The combined entity would not have the ability to foreclose its upstream competitors in provision of card processing software in the EEA by foreclosing access to a significant customer base for the following reasons:

(a) When assessing customer foreclosure, the Commission takes into account the existence of different uses for the upstream product. These can ensure that a sufficiently large customer base remains for that product post-merger.68 Card processors in Czechia are not the only purchasers of card processing software. According to the ECB, the volume of transactions processed in Czechia represents approximately 1.44% of the transactions processed in the EEA.69 Post-Transaction, there will remain several downstream players to whom upstream rivals can sell card processing software. These include (i) card processors outside Czechia,70 given that the card processing software market is at least EEA-wide and (ii) customers in Czechia and in other EEA countries who are not card processors, e.g., merchant acquirers and issuers who also license card processing software to conduct processing in-house. Customers who are not card processors represent a significant percentage of the demand for card processing software today, as reflected in the customer base of TSYS for card processing software. Across the EEA, today, TSYS only provides its card processing software to two processors ([…], […]). The revenues from these licences represent less than [5-10]% of the total revenues that TSYS obtained in 2019H1 from licensing its card processing software in the EEA; and

(b) Customer foreclosure is less likely when the combined entity is not an important customer for the upstream product.71 This is the case here, as Global Payments is currently not purchasing third-party card processing software but uses its own in-house software to process card payments (both for acquiring and for issuing processing).

(68) As the Commission found that the combined entity would have no ability to foreclose card processing software suppliers in the EEA, it is not necessary to assess in detail the incentives of the combined entity or the overall impact of the Transaction on competition.

5.4.3 Conclusion

(69) In light of the above considerations, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as a result of either input or customer foreclosure on the markets for card processing software in the EEA (upstream) and card processing in Czechia (downstream).

6. CONCLUSION

(70) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C 281, 20.08.2019, p. 24.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 14.

6 Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, Commission decision of 20 April 2016, paragraph 14; M.7241 - Advent International/Bain Capital Investors/Nets Holding, Commission decision of 8 July 2014, paragraph 32.

7 Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 14.

8 See Case M.5968, Advent/Bain Capital/RBS Worldpay, Commission decision of 14 October 2010, paragraph 11.

9 See Case M.7873, Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 14.

10 See Case M.7873, Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 14.

11 Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 33; M.7241 - Advent International/Bain Capital Investors/Nets Holding, Commission decision of 8 July 2014, paragraph 32.

12 Cases M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, M.7241 - Advent International/Bain Capital Investors/Nets Holding, Commission decision of 8 July 2014, M.7078 - Santander Consumer Finance/El Corte Ingles/Financiera El Corte Ingles, Commission decision of 29 January 2015, M.5241 - American Express/Fortis/Alpha Card, Commission decision of 3 October 2008.

13 Cases M.8073 – Advent International/Bain Capital/Setefi Services/Intesa Sanpaolo Card, Commission decision of 10 August 2016, paragraph 25; and M.7241 - Advent International/Bain Capital Investors/Nets Holding, Commission decision of 8 July 2014, paragraphs 35-36.

14 Cases M.8073 – Advent International/Bain Capital/Setefi Services/Intesa Sanpaolo Card, Commission decision of 10 August 2016, paragraph 27; and M.7241 - Advent International/Bain Capital Investors/Nets Holding, Commission decision of 8 July 2014, paragraph 36.

15 Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 34.

16 Form CO, paragraphs 6.53 and 6.60.

17 Form CO, paragraphs 6.54ff.

18 This is the case when a merchant acquirer processes in-house the transactions of its merchants.

19 This is the case when an issuer processes in-house the transactions based on the cards it has issued.

20 These markets are discussed in detail in Section 5 below. The following plausible markets are not affected by the proposed Transaction: all acquiring processing services; acquiring processing services for national card schemes; acquiring processing services for international card schemes; acquiring processing services for POS transactions; acquiring processing services for transactions through web- enabled interfaces; acquiring processing services to third parties and in-house acquiring processing services; in-house card processing services; and in-house issuing processing services.

21 Cases M.8073 – Advent International/Bain Capital/Setefi Services/Intesa Sanpaolo Card, Commission decision of 10 August 2016, paragraph 36; M.5968 – Advent/Bain Capital/RBS Worldpay, paragraph 12; M.4814 – AIB/FDC/JV, paragraphs 19-20; M.4316 – Atos Origin/Banksys/BCC, paragraphs 26-27.

22 Regarding acquiring processing, see Case M.7950 – EGB/GP, Commission decision of 19 April 2016, paragraphs 39-43. In Case M.7241 - Advent International/Bain Capital Investors/Nets Holding, Commission decision of 8 July 2014, the Commission recognized that acquiring processing for web- enabled transactions could be EEA-wide but ultimately left the issue open (see paragraph 40). Regarding issuing processing, see Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 112-114.

23 Form CO, paragraph 1.25.

24 Including for narrower plausible markets for acquiring processing and issuing processing services.

25 Case Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 78.

26 In Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, the Commission defined a separate relevant market for the software used by network service providers (“NSPs”) in Germany. This software was described as a "toolbox" for German NSP functionalities including routing, clearing, authorisation, communication protocol ZVT, routing of credit card transactions and some terminal management functions. This software was “tailored to the German card payment systems, specifically for the needs of German NSPs” (Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 138). Therefore, this software is different from card processing software (such as TSYS’ Prime), which is purchased around the world by merchant acquirers, acquiring processors, issuers, and issuing processors.

27 Form CO, Table 6.5.

28 Form CO, paragraph 6.67.

29 Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 136.

30 Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraph 136 with references to earlier decisions.

31 Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraphs 138- 140.

32 For example, TSYS’ card processing software is licensed for use in 80 countries.

33 For example, TSYS’ card processing software is licensed with EEA Member State languages preloaded and does not need to be specifically adapted to the language of each country.

34 Form CO, paragraph 6.71.

35 See Form CO, paragraph 6.72.

36 See Case M.7873 - Worldline/Equens/Paysquare, Commission decision of 20 April 2016, paragraphs 70ff and 135ff. The Commission ultimately left open the relevant geographic market definition for provision of software for the activities of German NSPs.

37 Horizontal Merger Guidelines, paragraph25. 38 OJ C 31, 5.2.2004, p. 5.

39 Horizontal Merger Guidelines, paragraph 24.

40 Horizontal Merger Guidelines, paragraphs 27 and following.

41 Horizontal Merger Guidelines, paragraphs 24-38.

42 OJ L 24, 29.1.2004, p. 1.

43 Non-horizontal Merger Guidelines, paragraph 35.

44 Non-horizontal Merger Guidelines, paragraph 32.

45 Non-horizontal Merger Guidelines, paragraph 61.

46 Non-horizontal Merger Guidelines, paragraph 59.

47 The Parties’ activities do not overlap horizontally in any other EEA country. Outside Czechia, Global Payments offers acquiring and issuing processing services also in Latvia, Romania, and Slovakia and TSYS offers issuing processing services in Finland, Germany, Hungary, Ireland, Italy, the Netherlands, Norway, Poland, Sweden, and the UK.

48 The Parties are active in card processing in many EEA countries other than Czechia (see fn. 47 above) but their combined share in below 30% under any plausible product market definition. TSYS' market share in the upstream market for provision of card processing software is below 10% in the EEA. See Section 5.4.

49 In addition to Czechia, TSYS offers issuing processing services to [Company] in the following EEA countries : the UK, Hungary, Poland, Finland, Norway, and Sweden.

50 Form CO, paragraph 6.90(i)(a).

51 In 2018, the combined share of the Parties would not exceed 20% in the EEA-wide card processing market and in an EEA- wide issuing processing market (including in-house and third-party or third-party only). As such, these markets are not horizontally affected.

52 The shares in Table 1 are calculated based on the number of transactions processed. The Parties confirmed that these market shares are commensurate with market shares based on the value of the transactions processed (see reply to RFI 3, 29 August 2019, questions 1 and 2).

53 In particular regarding issuing processing in Czechia, the HHI delta is […] (i.e., below 150); the post- merger HHI is […]; and the combined share of the Parties does not exceed 50%. The proposed Transaction is thus unlikely to give rise to horizontal competition concerns as per the Horizontal Merger Guidelines, paragraph 20.

54 In addition to Czechia, TSYS offers issuing processing services to American Express in the following EEA countries: the UK, Hungary, Poland, Finland, Norway, and Sweden.

55 See RFI 4, Parties’ Reply of 11 September 2019.

56 Form CO, Table 6.4. The Parties confirmed that their share does not exceed 10% in the plausible upstream markets for provision of acquiring processing software in the EEA and the provision of issuing processing software in the EEA.

57 Card payment software is also an important input for merchant acquiring services and issuing services. Global Payment offers merchant acquiring services in the EEA but its share does not exceed 30% in any EEA country. TSYS does not offer merchant acquiring services in the EEA. Global Payments does not offer issuing services in the EEA.

58 See Table 1 above.

59 The analysis in paragraphs 60ff. applies also to potential vertical links between upstream card payment software in the EEA and downstream: card processing in Czechia (in-house and third-party); card processing in Czechia (third-party only); issuing processing in Czechia (in-house and third-party); and issuing processing in Czechia (third-party only).

60 Non-horizontal Merger Guidelines, paragraph 34.

61 Form CO, paragraph 6.102. The Parties submitted that the following players in the downstream market for card processing in Czechia may use a combination of in-house and third-party software solutions: Worldline and EVO for acquiring processing; and Česká spořitelna, Raiffeisen Bank and Sberbank for issuing processing. See RFI 4, Parties’ Reply of 11 September 2019.

62 Non-horizontal Merger Guidelines, paragraph 35.

63 In 2018, TSYS held less than [0-5]% in the EEA-wide market for provision of card processing software based on the value and volume of transactions processed.

64 This conclusion would not change if the market were to be sub-segmented by type of card processing software. The Parties confirmed that their share does not exceed 10% in the plausible upstream markets for provision of acquiring processing software in the EEA and the provision of issuing processing software in the EEA.

65 Other key competitors include Openway, Fiserv/First Data, and HPS. See Form CO, Table 6.4.

66 Non-horizontal Merger Guidelines, paragraph 36.

67 In 2018, TSYS licensed its software to only one customer in Czechia, namely [Company], […]. See Form CO, paragraph 6.102. [Company] used TSYS’ software for in-house issuing and acquiring processing. TSYS’ software was not used at all in Czechia for issuing processing or acquiring processing services to third parties in 2018.

68 Non-Horizontal Merger Guidelines, paragraphs 61 and 66.

69 See Form CO, Table 6.1, based on ECB Payments data 2018, available at https://www.ecb.europa.eu/stats/payment statistics/payment services/html/index.en html.

70 Cf. Case M.8073, Advent International/Bain Capital/Setefi Services/Intesa Sanpaolo Card, Commission decision of 10 August 2016, paragraph 51.

71 Non-horizontal Merger Guidelines, paragraph 61.