Commission, June 5, 2019, No M.9238

EUROPEAN COMMISSION

Judgment

NEOS ENTERPRISES HOLDINGS LIMITED / ASHLAND'S GLOBAL COMPOUND RESIN BUSINESS AND MANUFACTURING FACILITY IN MARL

Subject: Case M.9238 - INEOS Enterprises Holdings Limited / Ashland’s

Global Compound Resin Business and Manufacturing Facility in Marl Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 25 April 2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which INEOS Enterprises Holdings Limited, part of the INEOS group of companies ("INEOS", Switzerland), acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of two distinct businesses of Ashland Global Holdings Inc. ("Ashland", US), namely (i) Ashland’s global composites business as well as (ii) its manufacturing plant located in Marl (Germany) by way of a purchase of shares and assets (“the Transaction”). (3) In this decision, INEOS is also referred to as the “Notifying Party”; INEOS and Ashland are collectively designated hereinafter as the "Parties"; (i) and (ii) are together referred to as the "Target".

1. THE PARTIES

(2) INEOS is a major multinational chemicals company specialized in the manufacture of petrochemicals, specialty chemicals and oil products, globally.

(3) The Target is active globally in the manufacture of vinyl ester resins ("VER"), gel coats, unsaturated polyester resins ("UPR"), benzene and maleic anhydride ("MAN"), which are intermediate chemical products used in the production of composite resins. It is also active in the manufacture, in Marl (Germany), of 1,4- butane-diol ("BDO"), 2-butene-1,4-diol ("B2D"), 2-butyne-1,4-diol ("B3D") and tetrahydrofuran ("THF"), which are input chemicals for engineering plastics, thermoplastic elastomers and specialty solvents.

2. THE TRANSACTION

(4) The Transaction consists in the acquisition of sole control by INEOS of parts of Ashland, namely (i) Ashland’s global composites business as well as (ii) Ashland’s manufacturing plant located in Marl (Germany) through a stock and asset purchase agreement reached on 14 November 2018. The Target is a business with a market presence, to which turnover can be clearly attributed.

(5) The Transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate worldwide turnover of more than EUR 5 000 million (4) (INEOS: EUR [35 000 – 40 000] million; the Target: EUR [900 – 1 000] million). Each of them has an EU-wide turnover in excess of EUR 250 million (INEOS: EUR [20 000 – 25 000] million; the Target: EUR [300 - 350] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(7) The notified operation therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

(8) Within the EEA, the Transaction leads to only minor horizontal overlaps in each of the separate markets for MAN (5), benzene (6), acetylene (7) and formaldehyde. (8) However, none of these markets is horizontally affected by the Transaction under any plausible relevant product and geographic market definitions.

(9) The remainder of the present decision will therefore exclusively focus on several vertically affected relationships, on the one hand, between styrene and VER and, on the other hand, between each of acetylene and formaldehyde with BDO, B2D and B3D.

4.1. Market definitions

4.1.1. Composites product chain

4.1.1.1. Styrene

(10) Styrene is an intermediate chemical used as a base material for the production of polystyrene and as a co-monomer in the production of several polymers and synthetic rubbers. In the context of the present case, the Target uses styrene as an input product for the manufacture of UPRs, gel coats and VERs.

(11) The Notifying Party submits that styrene represents a separate product market due to its physical characteristics and the absence of substitutes in the manufacture of polystyrene and other derivatives. It further submits that the market for styrene is either global or at least EEA-wide in geographic scope.

(12) In previous decisions, the Commission considered styrene as a separate product market (9), whose geographic scope is either global or EEA-wide given that it is traded as a commodity product and that transport costs are low. (10) The Commission’s market investigation did not reveal any evidence suggesting that an alternative market definition should be considered.

(13) Therefore, for the purpose of the present case, the relevant product market is considered to be styrene. As the Transaction does not raise any competition concerns in the market for styrene even under a narrower EEA-wide scope, for the purposes of the present case, the exact geographic scope of the market for styrene can be left open between EEA and global.

4.1.1.2. VER

(14) VER is a thermoset resin used for its higher heat, structural and corrosion resistant properties. VER is a key component in the production of corrosion resistant pipes and tanks, and is used in several components in boats and other industrial equipment.

(15) The Notifying Party submits that VER constitutes a separate product market as, although it shares certain characteristics with UPRs, it is typically tougher and more resilient. The Notifying Party submits that, given the similarities with UPRs, the relevant geographic scope should equally be at least EEA-wide.

(16) The Commission did not previously assess the market for VER in detail. (11) However, the Commission’s market investigation did not reveal any evidence suggesting that VER are part of a broader relevant product market or further segmented into narrower product markets. For the purpose of the present case, the Commission therefore considers that VER constitutes the relevant product market, in particular due to the particular characteristics of VER, such as increased toughness and resilience, which differentiate them from UPRs. As regards the geographic market definition, however, as the Transaction does not raise any competition issues under any plausible geographic scope (12), the exact geographic market definition can be left open between EEA and worldwide.

4.1.2. Butanediol production chain

4.1.2.1. Acetylene

(17) Acetylene is a gaseous hydrocarbon, which is generally produced by a chemical process where calcium carbide reacts with water, but also from hydrocarbons or as a by-product of ethylene production. Acetylene is usually used for glass (lubrication of moulds) and metalworking (cutting and welding) applications.

(18) The Notifying Party submits that acetylene constitutes a separate product market in light of limited supply-side and demand-side substitutability.

(19) The Commission previously considered industrial gases as separate product markets subdivided by distribution channel (i.e. tonnage, small on-site plants, bulk and cylinders) (13), though it did not consider the existence of a particular distribution channel via pipeline for acetylene specifically. (14) INEOS’ production is predominantly used for captive consumption, with its excess supply of acetylene being sold to a single customer and transported via pipeline (tonnage supply mode). The Commission’s market investigation did not reveal any evidence suggesting that the tonnage supply of acetylene is part of a broader relevant product market or further segmented into narrower product markets. For the purpose of the present case, the Commission therefore considers that the tonnage supply of acetylene constitutes the relevant product market.

(20) In a previous Commission decision, the Commission considered the geographic market for the tonnage supply of a number of industrial gases to be EEA-wide. (15) The Commission’s market investigation did not reveal any elements that would point to a smaller geographic market definition for the tonnage supply of acetylene.

(21) For the purposes of the present case, the Commission therefore considers the relevant market to be the EEA market for tonnage supply of acetylene.

4.1.2.2. Formaldehyde

(22) Formaldehyde is a colourless gaseous compound, which is manufactured from methanol and air. It is used as an input product for various applications in the manufacture of industrial chemicals, resins, plastics or adhesive for the wood industry.

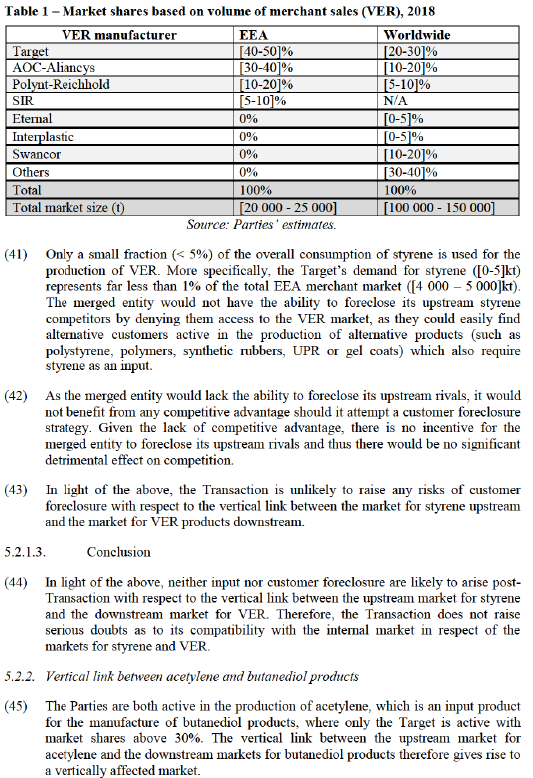

(23) The Notifying Party submits that for the chemical processes used to produce BDO in the Marl plant, formaldehyde is required. The Parties also submit that the relevant geographic market is EEA-wide, or at least regional and comprising Benelux, Germany, Austria, France, Switzerland and Italy.

(24) In its previous decisions, the Commission considered formaldehyde to constitute a separate product market. (16) As regards the geographic dimension, the Commission previously assessed that the relevant geographic market is at most regional, depending on the location of the production plant. (17) The Commission’s market investigation did not reveal any evidence suggesting that formaldehyde is part of a broader relevant product or geographic market.

(25) Hence, for the purpose of the present case, the relevant product market is considered to be formaldehyde. As regards the geographic market definition, however, as the Transaction does not raise any competition concerns, each at the narrowest plausible national geographic level and at any relevant broader regional level, the exact geographic definition can be left open between regional and national markets.

4.1.2.3. Butanediol Products (BDO, B2D, B3D)

(26) BDO is a straight-chain molecule, with a high reactivity, easy to incorporate into polymer chains. BDO is used either to act as a chain extender or to confer flexibility to polymer chains. It is mainly use for the production of polymers such as polyesters, polyurethanes, PTMEG or THF. (18)

(27) Beside BDO products, the Target further produces B3D and B2D products, which the Parties consider to belong to niche markets within the broader market for butanediol products. The Target uses a specific manufacturing process (the “Reppe method”) which yields either B2D or BDO from the common precursor B3D, itself a product of acetylene and formaldehyde (19). B3D is mainly applied in metal finishing or flame retardants, while B2D is used as a raw material for vitamins and agrochemicals.

(28) The Notifying Party submits that each of B3D, B2D and BDO can be considered to be separate product markets given the different applications and end-uses for each product. However, it also notes that, as B3D is a precursor to BDO, there is significant supply-side substitutability among them, and the Parties are not aware of any B2D competitor who does not also produce BDO. The Notifying Party submits that each of the geographic markets for B3D, B2D and BDO are global, but that the precise geographic scope can be left open for the purpose of the present case.

(29) The Commission previously considered BDO to be a separate product market. (20) The possible markets for B3D and B2D have never been previously addressed by the Commission. The Commission’s market investigation confirmed that, from a demand-side perspective, these products could belong to separate product markets due to their different properties and suitability to different end-use applications. However, from a supply-side perspective, the market investigation suggested a strong level of supply-side substitutability between BDO, B2D and B3D. The question as to whether these constitute separate relevant product markets can be left open for the purpose of the present case, as the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible market definition (see sections 5.2.2 and 5.2.3).

(30) Concerning the geographic market definition, the Commission previously considers the market for BDO to be EEA-wide in geographic scope. (21) B2D and B3D have not been previously assessed by the Commission, but the Commission’s market investigation did not reveal any evidence suggesting that the geographic markets for B2D and B3D are part of a broader or narrower relevant geographic market than that of BDO. Therefore, for the purpose of the present case, the Commission considers that the relevant geographic markets for BDO, B2D and B3D are EEA-wide in scope.

5. COMPETITIVE ASSESSMENT

5.1. Introduction

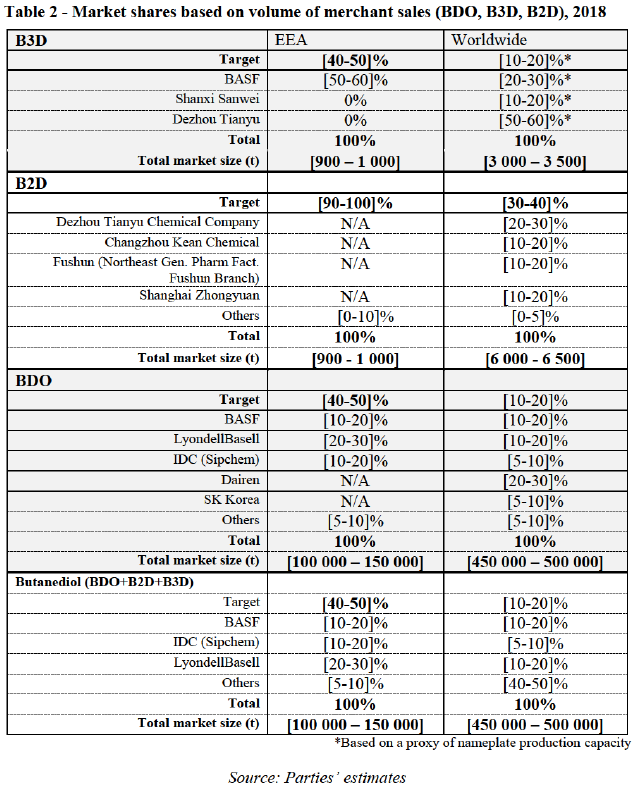

(31) The Transaction does not give rise to any horizontally affected markets.

(32) Conversely, the Transaction gives rise to several vertically affected relationships between, on the one hand:

a. the upstream market for styrene, where INEOS is present; and

b. the downstream market for VER, where the Target enjoys an important market share,

and, on the other hand:

c. the upstream markets for acetylene (where both Parties are present in the production but the Target has no merchant sales) and formaldehyde (where each Party has a small merchant activity); and

d. the downstream markets for butanediol products (BDO, B2D and B3D), where the Target enjoys significant market shares.

(33) The following sections assess every relevant vertically affected links identified above.

5.2. Vertical effects

5.2.1. Vertical link between styrene and VER

(34) INEOS is active in the manufacture of styrene, which is an input product for the manufacture of VER, where the Target enjoys a market share above 30% in the EEA, thus giving rise to a vertically affected link.

5.2.1.1. Input foreclosure

(35) Input foreclosure is highly unlikely to arise in the present case, given INEOS’s limited EEA ([10-20]%) and worldwide (less than [0-5]%) market shares in the upstream market for styrene. In fact, the merged entity would not enjoy a sufficient degree of upstream market power in order to be able to engage in an input foreclosure strategy.

(36) In any event, INEOS does not currently supply styrene to any EEA VER manufacturer and several alternative suppliers will remain active in the EEA market for styrene post-Transaction (e.g. Royal Dutch/Shell ([10-20]%), LyondellBasell/Covestro ([10-20]%), Repsol SA ([5-10]%) and BASF ([5-10]%) and on the global market (e.g. Royal Dutch/Shell ([5-10]%), LyondellBasell ([5- 10]%), SABIC ([5-10]%), Total Group ([5-10]%) and CNPC ([0-5]%). Therefore, the merged entity will have no ability to foreclose access to inputs to its downstream competitors in the market for VER.

(37) As the merged entity would lack the ability to foreclose its downstream rivals, it would not benefit from any competitive advantage should it attempt an input foreclosure strategy. Given the lack of competitive advantage, there is no incentive for the merged entity to foreclose its downstream rivals and thus there would be no significant detrimental effect on competition.

(38) In light of the above, the Transaction is unlikely to raise any risks of input foreclosure with respect to the vertical link between the market for styrene upstream and the market for VER products downstream.

5.2.1.2. Customer foreclosure

(39) Despite the Target’s strong position in the downstream EEA market for VER, where the Target enjoys a [40-50]% market share, customer foreclosure is unlikely to arise post-Transaction, given the limited demand for styrene that the Target accounts for in the EEA (22).

(40) Market shares in the downstream market for VER are shown in Table 1 under the two alternative plausible geographic market definitions as defined in section 4.1.1.2. The vertical link between the upstream market for styrene and the downstream market for VER only arises under the narrower geographic market definition of an EEA-wide market for VER.

5.2.2.1. Input foreclosure

(46) Input foreclosure is highly unlikely to arise in the present case as the merged entity would have a limited upstream market share of only [10-20]% in the EEA market for the tonnage supply of acetylene. In fact, while both Parties are active in the manufacture of acetylene, only INEOS is active in the merchant market with pipeline sales to a single customer, [Customer name], itself active in the bottling and resale of acetylene. By contrast, the Target’s entire production is destined for captive consumption (23). Therefore, the merged entity does not enjoy any particular market power in the upstream market for acetylene.

(47) Moreover, none of the Parties directly sells acetylene to downstream butanediol competitors of the Target. In fact, players active in the markets for butanediol products are independent from the Parties and already have access to sufficient input acetylene from alternative, well-established players in the industrial gas industry such as Linde, Air Liquide, Air Products, AGA or Messer (24).

(48) While, in practice, some of INEOS’s acetylene sold to [Customer name] could be sold to third-party butanediol manufacturers in acetylene cylinders, INEOS has no visibility over [Customer name's] sales of acetylene (25) and therefore does not have the ability to selectively deny the access to acetylene for downstream butanediol competitors of the Target. Given the existence of alternative suppliers and the lack of visibility over [Customer name's] sales in the merchant market, the merged entity would lack the ability to foreclose its downstream rivals.

(49) As the merged entity would lack the ability to foreclose its downstream rivals, it would not benefit from any competitive advantage should it attempt an input foreclosure strategy. Given the lack of competitive advantage, there is no incentive for the merged entity to foreclose its downstream rivals and thus there would be no significant detrimental effect on competition.

(50) In light of the above, risks of input foreclosure are unlikely to arise post-Transaction with respect to the vertical link between the market for acetylene upstream and each of the plausible downstream EEA or worldwide markets for BDO, B2D and B3D.

5.2.2.2. Customer foreclosure

(51) Despite the relatively high downstream market shares of the Target, in particular in the EEA market for B3D ([40-50]%), EEA and worldwide markets for B2D ([90- 100]% and [30-40]% respectively), EEA market for BDO ([40-50]%) and EEA market for BDO, B2D and B3D products ([40-50]%), customer foreclosure is unlikely to arise in the present case, as the Target is fully vertically integrated with respect to its sourcing of acetylene for its production of butanediol products. In other words, as it does not currently rely on any upstream manufacturer of acetylene, it is unable to reduce the merchant demand for acetylene.

(52) Market shares of the Target are shown in Table 2 under every plausible relevant alternative product and geographic market definition as defined in section 4.1.2.3.

(53) Currently, the Target does not purchase acetylene from any third-party acetylene producer for its production of BDO, B2D and B3D. Even if the Target were to rely on third-party sales of acetylene, the Transaction is unlikely to raise any risks of customer foreclosure as the butanediol industry only represents a very limited fraction of the overall demand for acetylene (<5% in the EEA). Risks of customer foreclosure are highly unlikely to arise post-Transaction as the merged entity does not have the ability to foreclose upstream competitors in the acetylene market by denying them access to an important customer active in the downstream markets for butanediol products.

(54) As the merged entity would lack the ability to foreclose its upstream rivals, it would not benefit from any competitive advantage should it attempt a customer foreclosure strategy. Given the lack of competitive advantage, there is no incentive for the merged entity to foreclose its upstream rivals and thus there would be no significant detrimental effect on competition.

(55) In light of the above, the Transaction is unlikely to raise any risks of customer foreclosure with respect to the vertical link between the market for acetylene upstream and each of the plausible downstream EEA or worldwide markets for BDO, B2D and B3D.

5.2.2.3. Conclusion

(56) In light of the above, neither input nor customer foreclosure are likely to arise post- Transaction with respect to the vertical link between the upstream EEA market for the tonnage supply of acetylene and each of the plausible downstream EEA or worldwide markets for BDO, B2D and B3D. Therefore, the Transaction does not raise serious doubts as to its compatibility with the internal market in respect of the markets for the tonnage supply of acetylene and each of the markets for BDO, B2D and B3D.

5.2.3. Vertical link between formaldehyde and butanediol products

(57) In the EEA, both INEOS and the Target produce and sell formaldehyde, which is an input for the production of B3D, B2D and BDO, where only the Target is active with market shares above 30%. The Transaction therefore gives rise to a vertically affected link between the upstream market for acetylene and the downstream markets for butanediol products.

5.2.3.1. Input foreclosure

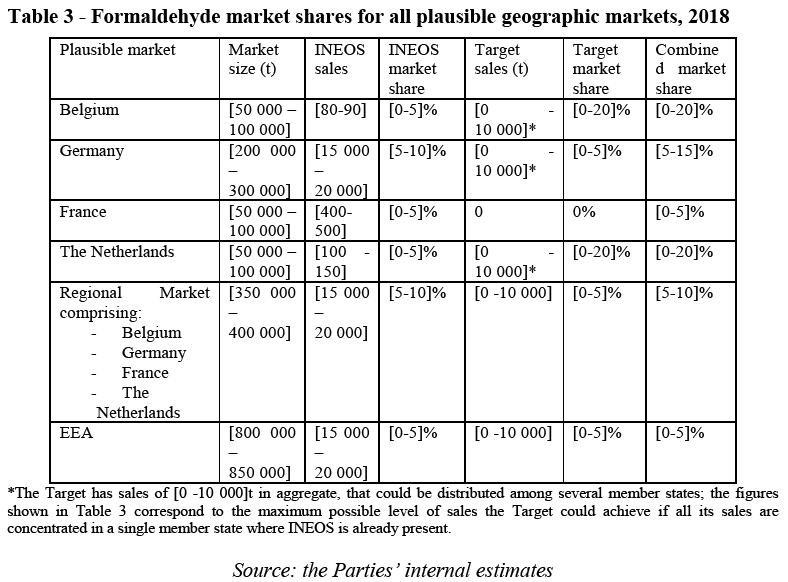

(58) Input foreclosure is highly unlikely to arise in the present case as the merged entity would have limited upstream market shares under every plausible geographic market definition. The Parties’ market shares in the formaldehyde market are shown in Table 3.

(59) The Parties’ combined market shares in the upstream market remain limited regardless of the geographic scope. Even in the most restrictive region (i.e. Germany, where the Parties’ assets are located and the three neighbouring countries where INEOS has sales, namely France, Belgium and the Netherlands), combined market shares for the merchant market remain low at a maximum of [5-10]%. If the region were to be expanded to other member states following the Parties’ proposed regional scope (i.e. including Italy, Austria, and Luxembourg), the Parties’ combined market shares would be even lower as they do not have any merchant sales in these markets. At the narrowest possible national level, market shares would be slightly higher in Germany (up to [10-20]%), provided that all of the Target’s sales are allocated to Germany, which the Parties have confirmed is not likely to be the case. Therefore, under any plausible geographic market definition, the Parties’ combined market share in the upstream market for formaldehyde remains fairly limited, and in any event below 20%.

(60) In any event, neither INEOS, nor the Target currently supply formaldehyde to other EEA-based suppliers in the markets for butanediol products and numerous alternative suppliers of formaldehyde will remain active in this highly fragmented market post-Transaction (e.g. Metadynea, Caldic, Kronochem, Hexion), including specifically in Germany (with Kronochem and Hexion). Downstream competitors for BDO, B2D and B3D therefore already currently have access to sufficient formaldehyde to cover their needs before the Transaction, whether internally through captive production or on the merchant market. Therefore, the merged entity will have no ability to foreclose access to inputs to its downstream competitors in the markets for butanediol products, as these competitors do not currently rely on INEOS or the Target and are able to source formaldehyde from alternative manufacturers.

(61) As the merged entity would lack the ability to foreclose its downstream rivals, it would not benefit from any competitive advantage should it attempt an input foreclosure strategy. Given the lack of competitive advantage, there is no incentive for the merged entity to foreclose its downstream rivals and thus there would be no significant detrimental effect on competition.

(62) In light of the above, risks of input foreclosure are highly unlikely to arise post- Transaction with respect to the vertical link between the market for formaldehyde upstream and each of the plausible downstream EEA or worldwide markets for BDO, B2D and B3D.

5.2.3.2. Customer foreclosure

(63) As shown in Table 2, the Target enjoys important to significant downstream market shares in the EEA market for B3D ([40-50]%), EEA and worldwide markets for B2D ([90-100]% and [30-40]% respectively), EEA market for BDO ([40-50]%) and EEA market for BDO, B2D and B3D products ([40-50]%). Nevertheless, customer foreclosure is unlikely to arise in the present case given the Target’s limited demand for formaldehyde products on the merchant market.

(64) Despite the Target’s high market shares in the downstream markets for BDO, B2D and B3D, the quantity of formaldehyde required by the butanediol industry in general represents only a limited fraction of the overall consumption of formaldehyde at EEA level (<3%). In any event, as the Target does not currently purchase formaldehyde on the merchant market for its production of BDO, B2D and B3D, the merged entity would not have the ability to foreclose its upstream formaldehyde competitors by denying them access to the niche markets of BDO, B2D and B3D.

(65) As the merged entity would lack the ability to foreclose its upstream rivals, it would not benefit from any competitive advantage should it attempt a customer foreclosure strategy. Given the lack of competitive advantage, there is no incentive for the merged entity to foreclose its upstream rivals and thus there would be no significant detrimental effect on competition.

(66) In light of the above, the Transaction is unlikely to raise any risks of customer foreclosure with respect to the vertical link between the market for formaldehyde upstream and each of the plausible downstream EEA or worldwide markets for BDO, B2D and B3D.

5.2.3.3. Conclusion

(67) In light of the above, neither input, nor customer foreclosure are likely to arise post- Transaction with respect to the vertical link between the upstream market for formaldehyde, irrespective of its precise geographic market definition at regional or national level, and each of the downstream EEA markets for BDO, B2D and B3D. Therefore, the Transaction does not raise serious doubts as to its compatibility with the internal market in respect of the markets for formaldehyde and each of the markets for BDO, B2D and B3D.

6. CONCLUSION

(68) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 151, 03.05.2019, p. 14.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

5 Both Parties manufacture MAN in the US and have only a de minimis presence in the EEA. The Parties’ combined market share would remain [0-5]% at global level and less than [5-10]% at EEA level.

6 The Target produces de minimis quantities of benzene. The Parties’ combined market share would remain, in any event, well less than [10-20]% at global level and [0-5]% at EEA level.

7 See section 5.2.2.1 of the present decision.

8 See section 5.2.3.1 of the present decision.

9 COMP/M.8015 - Synthos / INEOS Styrenics, paragraph 26.

10 COMP/M.8015 - Synthos / INEOS Styrenics, paragraph 27.

11 In COMP/M.8059 - Investindustrial / Black Diamond / Polynt / Reichold, footnote 5, the Commission mentioned the market for VER but did not assess it in detail as that concentration did not lead to an affected market under any plausible market definition.

12 See section 5.2.1.

13 COMP/M. 8480 - Praxair / Linde, paragraph 91.

14 COMP/M. 8480 - Praxair / Linde, paragraph 34.

15 COMP/M. 8480 - Praxair / Linde, paragraph 105

16 COMP/M.1813 - Industri Kapital (Nordkem) / Dyno, paragraph 34; COMP/M.2396 - Industri Kapita / Perstorp (II), paragraph 29.

17 COMP/M.2396 - Industri Kapital / Perstorp (II), paragraph 48.

18 Form CO, paragraph 87.

19 Form CO, paragraph 171-173.

20 COMP/M.2314 - BASF/ Eurodiol / Pantochim, paragraph 18.

21 COMP/M.2314 - BASF/ Eurodiol / Pantochim, paragraph 58.

22 See recital 41 for figures on styrene demand from VER producers.

23 Form CO, paragraph 168.

24 Form CO, paragraph 227.

25 Form CO, paragraph 244.3.