Commission, October 22, 2018, No M.9060

EUROPEAN COMMISSION

Judgment

HP / APOGEE

Subject: Case M.9060 – HP / Apogee

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 17 September 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which HP Inc. ("HP", United States) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of Apogee Group Limited ("Apogee", United Kingdom). (3) HP is designated hereinafter as the "Notifying Party" and HP and Apogee are collectively referred to as "Parties".

1. THE PARTIES

(2) HP is a US-based multinational technology company that manufactures and sells electronic devices, including personal computers and printers. HP markets inkjet and laser printers geared towards a range of needs to consumers and businesses. HP's offerings include personal computing and other access devices; and imaging and printing-related products and services.

(3) Apogee is a provider of managed print services ("MPS") to business users primarily in the United Kingdom. Its MPS offering comprises a flexible combination of hardware, consumables, software, maintenance, workflow management, consulting, training and other related services.

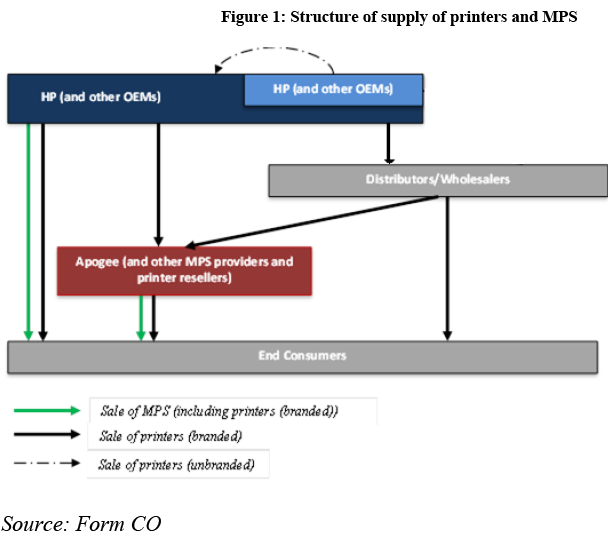

2. THE OPERATION

(4) Pursuant to a sale and purchase agreement entered into on 1 August 2018 ("the SPA"), HP will acquire control of Apogee through the acquisition of an ultimate indirect shareholding of at least 90% of the share capital of Manzana Holdings Limited (the holding company through which the Sellers (4) hold their interest in Apogee) ("the Proposed Transaction"). Following completion of the Proposed Transaction, 100% of the shares in the capital of Manzana Holdings Limited which bear a right to vote will be held by Perigee Midco UK Limited, a wholly owned subsidiary of HP.

(5) The Proposed Transaction will result in Albacore Holdings Jersey Ltd (a private limited company established by HP and incorporated in Jersey) ("Jersey TopCo"), indirectly holding (through Perigee Midco UK Limited) 100% of the shares of Manzana Holdings Limited. [Details relating to the structure of the proposed acquisition].

(6) A shareholders’ agreement will be entered into in relation to the Proposed Transaction upon completion ("the Shareholders’ Agreement"), under which [a direct subsidiary of HP] will have exclusive voting rights. […].

(7) Under the Shareholders’ Agreement, there is no limit on the number of directors on Jersey TopCo’s Board (and therefore the number of directors that HP can appoint). However, the current intention is that at completion there will be […] directors: HP will appoint […] directors while the two current joint-CEOs of Apogee (Robin Stanton-Gleaves and Jason Collins) will be entitled to remain as joint-CEOs and be appointed as directors of Jersey TopCo. This right is personal to […]. Strategic decisions will be taken at board level and voting at board meetings will be made on a simple majority basis, meaning that HP appointed directors will have control of the Board and there are no reserved matters relating to strategic day to day commercial decisions which require greater than simple majority votes to pass. HP is also responsible for [….].

(8) The Proposed Transaction therefore constitutes a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(9) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (5) (HP: EUR 46 868.09 million; Apogee: EUR […] million). Each of them has an EU-wide turnover in excess of EUR 250 million (HP: EUR […] million; Apogee: EUR […] million), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(10) The Proposed Transaction therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

4.1. Structure of supply of printers and MPS

(11) Apogee is active in the provision of MPS direct to its customers, while HP’s focus is on the sale of printers (usually via distributors and resellers). Only a small portion of HP’s business involves direct sales of branded printers to customers and/or the provision of MPS (which is generally limited to large global enterprise customers). As a result, HP is primarily active “upstream” of Apogee, and sells to Apogee the printer hardware that forms part of Apogee’s supply of MPS.

(12) A simplified overview of the structure of supply in the markets in which HP and Apogee operate is set out as Figure 1 below:

4.2. Printers

(13) In previous decisions (6), the Commission distinguished the regular format printers which use A3 and A4 papers from the large format printers which function on A2 or larger papers and other supports. (7) The Notifying Party does not disagree with this finding.

(14) Respondents to the market investigation confirmed that this is still a valid distinction due to different applications and sales channels of regular and large format printers. (8)

(15) In line with its previous decisional practice, for the purpose of this decision, the Commission considers that the supply of large format printers should be distinguished from the supply of regular format printers. The following sections discuss any possible further sub-segmentation of the market for regular format printers and large format printers.

4.2.1. Supply of regular format printers

4.2.1.1. Product market definition

(16) In previous decisions, the Commission considered distinctions between single- function and multi-function printers, but ultimately left the product market definition open in this regard. (9) The Commission considered that the supply of mono (black and white) and of colour regular format printers belong to the same relevant product market. (10) As to a further segmentation based on printer speed ranges measured by the output of pages per minute (ppm), the Commission left the exact product market definition open. (11) The Commission also looked into the possible segmentation of printers by page format (that is to say, A3 printers and A4 printers) ultimately leaving the exact product market definition open. (12)

(17) The Notifying Party submits that printers with different speed, colour, functionalities, etc. belong to the same market for regular format printers as the boundaries between the different segments of the regular format printer market are becoming increasingly blurred due to technological developments. In any case, the Notifying Party submits that the exact market definition can be left open as it does not affect the outcome of the assessment of the Proposed Transaction.

(18) The market investigation tested whether any segmentations of regular format printers (e.g. based on single function vs. multifunctional equipment, mono vs. colour format printers, speed ranges, A3/A4 format) would be appropriate. A majority of printer suppliers stated that a further segmentation was not appropriate due to similarities in customer applications. (13)

(19) However, for the purpose of the present decision, the question whether the product market consists of all regular format printers or whether separate markets exist for any segmentations of regular format printers can be left open as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition, including the narrowest possible markets for (i) single function or multifunctional equipment, (ii) mono (black&white) and color regular format printers; (iii) segments based on speed measured by the output of pages per minute (ppm) namely personal devices (speed up to 10 or 20 ppm for mono and up to 20 ppm for colour), office devices (speed between 11-20 and 90 ppm for mono and 20 – 50 ppm for colour) and commercial/production devices (speed over 90 ppm for mono and above 50 for colour); (iv) A3 and A4 regular format printers.

4.2.1.2. Geographic market definition

(20) In HP/Samsung, the Commission considered that there were clear indications that the relevant markets are wider than national or even EEA wide, ultimately leaving the question open.v (14)

(21) The Notifying Party submits that the relevant geographic market should be defined as EEA-wide, given that: (i) OEMs have manufacturing facilities in Asia and other global regions from where they ship their products around the world; (ii) transportation costs are relatively low for worldwide shipping of printers; (iii) there are no import or export quota restraints or other material trade barriers; (iv) major distributors in the EEA resell printers in multiple countries, while some of them also cover the distribution logistics for several countries with one warehouse; (v) OEMs generally price on an EEA or even wider basis following standard price lists; and, (vi) product characteristics of printers do not vary significantly in the EEA or throughout the world.

(22) The market investigation indicated that the geographic scope of the market may be wider than national, as a majority of printer suppliers are able to supply to other countries in the EEA (15) and a majority of customers would consider sourcing printers from a supplier that is active in another country in the EEA. (16)

(23) In conclusion, in spite of the fact that current sourcing patterns for regular format printers are usually at national level, there are clear indications that the relevant markets are wider than national or even EEA wide. However, for the purpose of the present decision the question whether the relevant geographic market definition is national or EEA-wide can be left open as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition, including the narrowest possible national market.

4.2.2. Supply of large format printers

4.2.2.1. Product market definition

(24) Large format printers can be used by customers: (i) to print signage and display items (posters, banners, rigid signs, vehicle and building wraps and packaging); (ii) to print large format photos and posters; (iii) for print proofing; and (iv) for computer aided design (CAD) (17). In addition, large format printers will vary depending on the printing technology used, the type and size of media they can print on, and their printing capacity.

(25) In Canon/Océ, (18) the Commission analysed the transaction by distinguishing between graphic arts (GA) (19) and CAD applications but did not reach any conclusions as to the exact boundaries of the product market.

(26) The Notifying Party submits that there is no need to reach a conclusion as to whether GA and CAD printers are part of separate markets, as the Proposed Transaction will not raise any concerns on any plausible market definition.

(27) During the market investigation a majority of printer suppliers indicated that a segmentation between large format printers for GA and CAD applications is still relevant due to different applications of each segment. (20)

(28) However, for the purpose of the present decision, the question whether the product market consists of all large format printers or whether separate markets exist for any segmentations of large format printers (e.g. for GA and CAD applications) can be left open as the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition, including the narrowest possible markets for GA printers and CAD printers.

4.2.2.2. Geographic market definition

(29) In Canon/Océ (21), the Commission noted that in spite of the fact that sourcing patterns are usually at national level, there are clear indications that the market for office equipment is wider than national if not EEA-wide. Ultimately, the Commission left the precise geographic market definition open.

(30) The Notifying Party submits that the relevant geographic market should be defined as EEA-wide.

(31) The market investigation indicated that the geographic scope of the market may be wider than national, as a majority of printer suppliers are able to supply to other countries in the EEA (22) and a majority of customers would consider sourcing printers from a supplier that is active in another country in the EEA. (23)

(32) In conclusion, in spite of the fact that current sourcing patterns for large format printers are usually at national level, there are clear indications that the relevant markets are wider than national or even EEA wide. However, for the purpose of the present decision the question whether the relevant geographic market definition is national or EEA-wide can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition, including the narrowest possible national market.

4.2.3. Managed Print Services

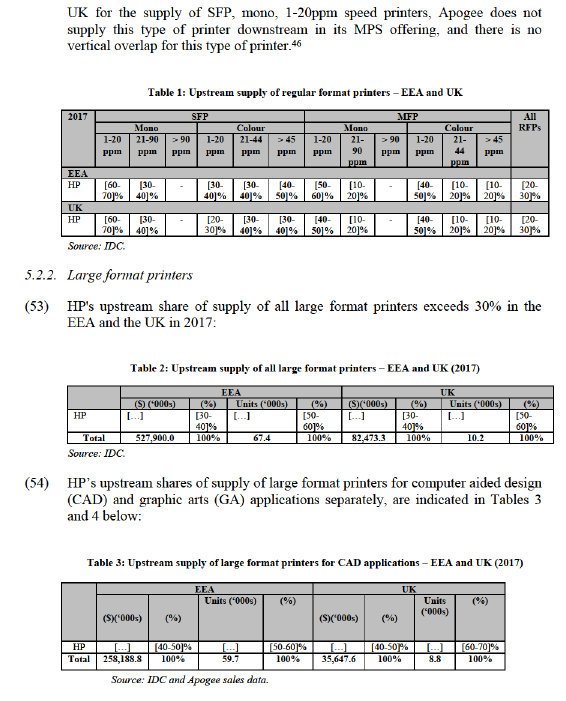

4.2.3.1. Product market definition

(33) MPS offerings cover a broad spectrum of solutions, comprising a flexible combination of hardware, consumables, software, maintenance, workflow management, consulting, training and other related services. These related services may include remote monitoring and management services, audit and advice on fleet management, software supply, outsourced provision of document production, mailroom services, cloud services, etc. Generally MPS providers will enter into multi-year and bespoke agreements with customers to provide some or all of these services depending on customer need and preference, and MPS providers are broadly able to customise the service offering according to the customer’s requirements. At the very least, MPS providers will therefore provide the customer with access to hardware (i.e. the printer and consumables) and then a range of related added-value features, to provide an overall MPS arrangement.

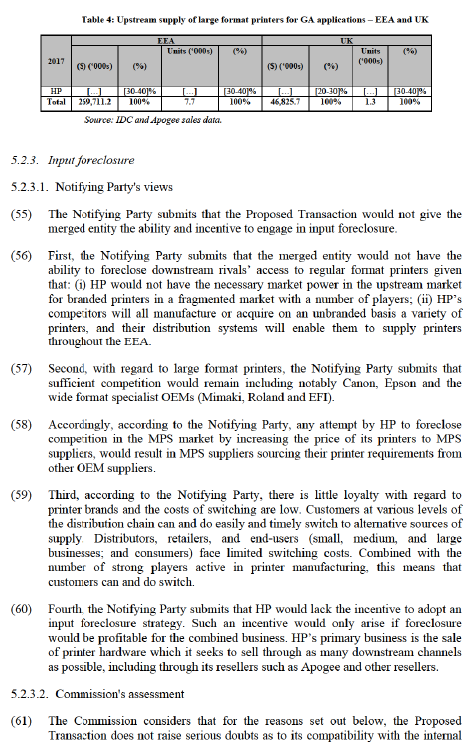

(34) The Notifying Party submits that – even though IDC appears to distinguish between "basic" and a "sophisticated / managed" MPS offerings – it is not appropriate (or indeed possible) to segment MPS by different types of value added services that a customer may choose to contract for. According to the Notifying Party, from a demand side perspective, customers regularly assess their MPS needs and are able to shift between different types of MPS (and vice-versa) depending on their on-going requirements. From a supply side perspective, all MPS suppliers are able to offer a range of services depending on specific customer needs. There is a wide variety of MPS suppliers, and each MPS supplier offers several solution packages depending on customer requirements. For the more sophisticated services, an MPS provider will often partner with specialised companies, like software vendors, which enable them to expand their range of service offerings at little or no incremental cost and time. In each case, the key value that the MPS supplier adds is not so much the individual underlying printers, consumables, and software and systems, but assembling these into a package that acts as a finished ‘solution’ for a client’s printing and document needs, and ensuring that this ‘solution’ remains functional.

(35) During the market investigation a majority of printer suppliers, MPS providers and enterprise customers stated that MPS are different based on the size of the business. (24) Several respondents stated that large enterprise clients need more sophisticated services, such as extensive printer fleet management services. (25)

(36) However, the majority of printer suppliers and MPS providers is able to provide both basic and more sophisticated types of MPS depending on the customer's on- going requirements (26) and a majority of customers is able to shift between these different types of MPS depending on their needs. (27) For this reason, for the purpose of the present decision, the Commission will assses the Transaction in a market encompassing all MPS.

4.2.3.2. Geographic market definition

(37) The Notifying Party submits that the relevant market is that for MPS on an EEA basis as demand for MPS is driven primarily by the range of services required by the customer and the size of a customer’s business. For example, HP and other OEMs enter into MPS agreements that are EEA-wide, if not global, in scope with very large enterprise customers (such as major banks and multinational corporations). According to the Notifying Party, local or mid-sized national businesses are more likely to make purchasing decisions at a regional level, and be concerned about consistency across a regional business (and regional customisation): they are more likely to procure MPS from resellers, such as Apogee, that operate at a national level as well as from certain OEMs, such as Xerox, that have expanded into servicing these types of business either through acquisition or an expansion of their MPS network. Smaller regional MPS providers would be competitively constrained by the national providers, but, in each case, there is competition ‘upwards’ and ‘downwards’ from the different sized suppliers in the market.

(38) The market investigation provided mixed results as to the geographic market for MPS. Different MPS suppliers supply at different geographic levels, i.e. either worldwide, in the EEA or at the national level (28) and only MPS suppliers already active internationally could start supplying in other countries. (29) A majority of printer suppliers who replied during the market investigation supply MPS on EEA-wide basis. (30), and a majority of these printer suppliers also stated that they could not start supplying MPS to end-customers outside the EEA. (31) A majority of enterprise customers purchase MPS from suppliers located in the same EEA Member State where they are located (32) but would consider purchasing from a MPS supplier active in another country in the EEA. (33)

(39) For the purpose of the present decision, the question whether the geographic market for MPS is national or wider can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market, under any plausible geographic market definition, including the narrowest possible national market.

5. COMPETITIVE ASSESSMENT

5.1. Horizontally affected markets (34)

5.1.1. Regular format printers

(40) The Proposed Transaction gives only rise to a horizontally affected market in the supply of regular format printers. (35) The Parties’ combined market share of regular format printers (on the basis of direct sales to end-users) does not exceed [0-5]% on the market for the supply of regular format printers across the EEA and would not exceed [10-20]% for sales in the UK alone. Considering narrower product categories (split by function, speed, colour; and split by A3/A4 and inkjet/laser) no affected markets arise in the EEA or in the UK, except for one sub-segment (SFP, colour, > 45ppm) in the UK, in which however the increment to Apogee’s [30-40]% share is less than [0-5]%: this reflects the fact that HP sold only […] printers directly to end-users in 2017.

(41) The Notifying Party submits that the Proposed Transaction does not raise horizontal concerns in the supply of regular format printers at an EEA and UK level since sufficient competition will remain to prevent any harm to competition occurring as a result of the Proposed Transaction. According to the Notifying Party, HP’s closest competitors for the supply of regular format printers are the other OEMs, which are large multinational competitors with established business connections throughout the EEA, including Ricoh, Canon, Konica Minolta, Kyocera, Xerox, Epson and Brother, all of which have shares of over 5% throughout the EEA and exert significant competitive pressure on HP throughout the EEA. The Notifying Party submits that Apogee has a minimal market share in the supply of regular format printers and only sold […] large format printers in the EEA in 2017.

(42) The Commission considers that the Proopsed Transaction does not raise serious doubts as to its compatibility with the internal market in the supply of regular format printers, for the following reasons.

(43) First, as described above (see recital (40)), irrespective of the precise product and geographic market definition, the combined market shares of HP and Apogee lead to an affected market only in a one sub-segment (SFP, colour, > 45ppm) in the UK. The increment to Apogee’s [30-40]% share is less than [0-5]%. Therefore, the competitive conditions that would result from the merger are not materially different from those that would have prevailed absent the merger. This follows from the fact that HP only sells a very limited amount of printers directly to end- users.

(44) Second, the market investigation confirmed that post-Transaction there will be a sufficient number of suppliers of regular format printers to ensure the same level of competition in the market as today and ensure choice for customers, as is confirmed by a majority of competitors and customers. (36) A majority of competitors (37) and customers (38) consider that the likely impact of the Proposed Transaction on the intensity of competition in the market for the supply of regular format printers, will either remain the same or will increase.

5.2. Vertically affected markets (39)

(45) The Proposed Transaction would give rise to several vertical relationships. In particular, HP is primarily active upstream of Apogee and sells to Apogee the printer hardware that forms part of Apogee's supply of MPS.

(46) According to the Non-Horizontal Merger Guidelines, foreclosure occurs when actual or potential rivals’ access to supplies or markets is hampered, thereby reducing those companies’ ability and/or incentive to compete. Such foreclosure may discourage entry or expansion of rivals or encourage their exit. (40)

(47) The Non-Horizontal Merger Guidelines distinguish between two forms of foreclosure: input foreclosure occurs where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input and customer foreclosure occurs where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base. (41)

(48) In order for foreclosure to be a concern, three conditions need to be met post- merger: (i) the merged entity needs to have the ability to foreclose its rivals (42) ; (ii) the merged entity needs to have the incentive to foreclose its rivals (43); and (iii) the foreclosure strategy needs to have a significant detrimental effect on the parameters of competition on the downstream market (input foreclosure) (44) or on consumers (customer foreclosure). In practice, these factors are often examined together since they are closely intertwined. (45)

(49) The Commission examined whether the Proposed Transaction could give rise to a possible risk of input foreclosure for the supply of large and/or regular format HP printers exclusively to Apogee to the detriment of other downstream providers of MPS. In addition, the Commission assessed the risk of a possible customer foreclosure for HP's competitors provided that the merged entity would stop acquiring large and/or regular format printers from other printer suppliers and exclusively rely on the printers provided by HP.

5.2.1. Regular format printers

(50) On the potential market for the supply of all regular format printers to MPS providers that rely on purchasing regular format printers from the OEMs, no vertically affected market arises (neither in the EEA nor the UK) on the basis of value shares (i.e. market shares based on sales value). HP's share is moderate in the EEA and in the UK (at [20-30]% and [20-30]%, respectively). In HP/Samsung the Commission used shares by value as the appropriate metric by which to assess market power in these markets.

(51) However, vertically affected markets arise for the supply of all regular format printers if market power were to be assessed on the basis of volume shares as HP’s share would be [40-50]% (EEA) and [40-50]% (UK).

(52) In addition, in a number of sub-segments for the supply of regular format printers segmented by function, speed and colour, HP has market shares above 30%. Vertically affected markets arise in most of these sub-segments as shown Table 1 below. Although HP’s market share is [60-70]% in the EEA and [60-70]% in the market with respect to potential input foreclosure by which the merged entity would exclusively supplylarge and/or regular format HP printers, regardless of any further segmentation, to Apogee to the detriment of other downstream providers of MPS.

(62) First, with regard to the ability to engage in input foreclosure, the merged entity does not appear to have a significant degree of market power in the upstream market for the supply of regular format printers. Based on the Notifying Party’s submission, other suppliers of branded regular format printers in the EEA, i.e. Ricoh, Canon and Konica Minolta all have shares above 10% in the EEA and the UK, and other significant OEMs have shares between 5% and 10%. The market is fragmented with no player having a share of over 25%. HP’s competitors can all manufacture or acquire unbranded printers, and their distribution systems will enable them to supply printers throughout the EEA. With the established reliance on unbranded printers and good supply-side substitutability, price increases by OEMs can easily be met by increased supply from competitors.

(63) Second, with regard to large format printers, based on the Notifying Party’s submission, there are other competitors such as Canon (with a [20-30]% share at an EEA level and [10-20]% share at a UK level), Epson, and the wide format specialist OEMs, Mimaki, Roland and EFI, with shares of greater than [0-5]% at both the EEA and UK level.

(64) Third, as discussed above, there appear to be a number of competitors to HP's printer business which could provide alternatives to the merged entity, notably Canon which suppies regular format and large format printers. A majority of MPS providers indicated that they already source regular format and large format printers from other manufacturers (such as Konica Minolta, Canon, Ricoh, Kyocera and others). (47)

(65) Fourth, with regard to the incentive to engage in any input foreclosure, the Commssion considers that, based on the Notifying Party’s submission, the combined entity’s share in the MPS market would only be moderate and therefore HP would not be incentivised to implement an input foreclosure strategy that would prevent other resellers from selling HP printers to the market. Furthermore, in accordance with the Notifying Party’s submission, despite HP having a higher share than some of its OEM rivals large format printers, Apogee’s sale of large format printers related to its MPS offering is de minimis (having sold only […] printers in the EEA during 2017) ruling out any potential benefit for HP of by implementing an input foreclosure strategy.

(66) Fifth, during the market investigation, a majority of MPS providers responding to the market investigation consider that the merged entity could or would not engage in input foreclosure. (48) For instance, a competitor indicated that "HP products will be available to a multitude of resellers and dealers". Another competitor indicated that “whilst Apogee is a large reseller, I do not consider it to be large enough to fulfill the requirements of HP, and therefore HP will need to also supply other resellers”. (49)

(67) Based on the above, the Commission concludes that the Proposed Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to input foreclosure in light of the vertical link between the upstream market for regular and large format printers and the downstream market for MPS.

5.2.4.Customer foreclosure

5.2.4.1. Notifying Party's views

(68) The Notifying Party submits that the Parties lack the ability and incentive to foreclose printer suppliers from access to key customers.

(69) First, according to the Notifying Party, the combined entity’s MPS business will not be an important customer on the downstream market for printers, given its low market shares on the downstream market for MPS both a worldwide, EEA and UK level. Moreover, large competitors will continue to place competitive pressure on the combined entity in the EEA and the UK. As […] of Apogee’s printers are sourced from OEMs other than HP/Samsung, if the combined entity purchased 100% of its printers post-Transaction from HP, the impact on the sales of other OEMs would be a reduction of less than [0-5]% of non-HP suppliers’ sales globally, or less than [0-5]% in the UK. Moreover, vertical integration protects competing printer suppliers from any attempted customer foreclosure strategy.

(70) Second, the Notifying Party submits that the merged entity would lack the incentive to cease procuring products from upstream OEM rivals, as it could not capitalise on the increased profits that the combined entity could derive either at the upstream level (i.e. by increasing sales in the MPS market) or at the downstream level (due to lessened competition as a result of the foreclosure strategy) for the following reasons: (i) the combined entity’s share at the downstream level is low and foreclosure is unlikely to lead to higher profits at the upstream level based on a hypothetical increase in sales downstream; and; (ii) the downstream business relies on being able to offer customers a comprehensive ‘print solutions’ offering, which includes access to a broad range of printers, services and value added products that are packaged together to fit a customer’s bespoke MPS requirements.

5.2.4.2. Commission's assessment

(71) The Commission considers that for the reasons set out below, the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market with respect to potential customer foreclosure by which the merged entity would stop acquiring large and/or regular format printers from other printer suppliers and exclusively rely on the printers provided by HP for the provision of MPS.

(72) First, with regard to the ability to engage in any potential customer foreclosure strategy, the merged entity does not appear to have a significant degree of market power in the downstream market for the provision of MPS, irrespective of the precise geographic market definition.

(73) Second, there are other MPS competitors which will continue to exert competitive constraint on the merged entity post-Transaction. The market investigation results confirmed that MPS customers consider that Apogee’s market share is low and that "less choice in the market will inevitably lead to increased competition” amongst the remaining players on the market. (50)

(74) Third, based on the Notifying Party's submission, even if the merged entity would source printers exclusively from HP, the impact on the sales of other OEM providers would not be significant.

(75) Fourth, during the market investigation a competitor expressed the view that "HP cannot only resell through Apogee as their sales and market coverage through resellers is much bigger". (51) Another competitor responding to the market investigation indicated that that there is limited incentive for the merged entity to employ a possible foreclosure strategy as it would restrict the market on which it would operate and thereby reduce sales. (52) A majority of competitors responding to the market investigation consider that the merged entity would not have the ability and incentive to degrade the terms and conditions of the supply of regular format and/or large format printers. (53)

(76) Fifth, with regard to the incentive to engage in any potential customer foreclosure, the Commission considers that the combined MPS offerings of the merged entity would be impeded if they attempt a foreclosure strategy, while MPS competitors would remain free to offer customers HP printers and services as well as a range of other branded printers from HP’s OEM competitors and an assortment of bundled services (some proprietary and some contracted from other providers such as document software providers).

(77) A majority of MPS providers responding to the market investigation consider that the merged entity will not have an incentive to engage in a customer foreclosure strategy because the one supplier approach would limit their market opportunities. (54) For instance, one competitor expressed the view that "the company Apogee is a service provider and the success of the company is among others the great manufacturer portfolio, The customers who need an appropriate solution will certainly also get the right products offered in the future for their requirements. Therefore, [we] think that in the future Apogee will focus more on HP products but will also continue to market the other manufacturers with appropriate solutions". (55)

(78) Based on the above, the Commission concludes that the Proposed Transaction does not give rise to serious doubts as to its compatibility with the internal market in relation to customer foreclosure in light of the vertical link between the upstream market for regular and large format printers and the downstream market for MPS.

6. CONCLUSION

(79) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 340, 24.09.2018, p. 13.

4 The Sellers are Euroblue Investments Limited, certain funds ("the Equistone Funds") managed by Equistone Partners Europe Limited ("Equistone") and various other management and employee sellers ("the Sellers"). The Equistone Funds are: Equistone Partners Europe Fund V "A" L.P., Equistone Partners Europe Fund V "B" LP, Equistone Partners Europe Fund V "C" L.P., Equistone Partners Europe Fund V "D" L.P., Equistone Partners Europe Fund V "E" L.P., Equistone Partners Europe Fund V "F" L.P., Equistone Partners Europe Fund V "G" L.P., Equistone V Excess L.P., and Europe Equity V.

5 Turnover calculated in accordance with Article 5 of the Merger Regulation.

6 Commission decision of 22 December 2009 in Case M.5672 Canon/Océ, paragraphs 13 and 14; Commission decision of 4 April 2017 in Case M.8254 HP/Printer Business of Samsung Electronics, paragraph 16.

7 In HP/Samsung, the Commission considered that the supply of branded office automation equipment belongs to a separate relevant market than that of the supply of unbranded office automation equipment. As Apogee is neither a manufacturer nor a buyer of unbranded printers, this market will not be considered further in this decision.

8 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 4.

9 Commission decision of 4 April 2017 in Case M.8254 HP/Printer Business of Samsung Electronics, paragraph 28. The Commission also considered that a distinction could be made between single function office equipment (SFPs) and multifunctional peripherals (MFPs), in Commission decision of 22 December 2009 in Case M.5672 Canon/Océ, paragraphs 16 to 19 and Commission decision of 19 January 2010 in Case COMP/M.5666 Xerox/ Affiliated computer services, paragraphs 20-29. With regard to the distinction between single function devices, the Commission considered that photocopiers, printers and fax machines may constitute three distinct product markets in Case M.4434 Ricoh/Danka of 8 December 2006.

10 HP/Samsung, paragraph 36.

11 HP/Samsung, paragraph 44.

12 HP/Samsung, paragraph 51.

13 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 5.

14 HP/Samsung, paragraph 59.

15 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 8.

16 Replies to questionnaire Q3 – Questionnaire to enterprise customers of 19 September 2018, question 5.

17 Typical CAD applications are technical line drawings, maps, (architectural) renderings and illustration, supporting photographs (to a limited extent) as well as (mainly indoor) posters.

18 Commission decision of 22 December 2009 in Case M. 5672, Canon/Océ, para 39.

19 Typical applications include display materials, advertising material and signage

20 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 6.

21 Canon/Océ, paragraph 47.

22 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 8.

23 Replies to questionnaire Q3 – Questionnaire to enterprise customers of 19 September 2018, question 5.

24 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 11; Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 4; Replies to questionnaire Q3 – Questionnaire to enterprise customers of 19 September 2018, question 8.

25 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 11.1; See also Replies to questionnaire Q3 – Questionnaire to enterprise customers of 19 September 2018, question 8.1.

26 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 12; Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 5.

27 Replies to questionnaire Q3 – Questionnaire to enterprise customers of 19 September 2018, question 9.

28 Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 6.

29 Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 7.

30 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 9.

31 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 10.

32 Replies to questionnaire Q3 – Questionnaire to enterprise customers of 19 September 2018, question 6.

33 Replies to questionnaire Q3 – Questionnaire to enterprise customers of 19 September 2018, question 7.

34 The market shares in this section are based on the Parties' direct sales to end-consumers.

35 The Proposed Transaction does not give rise to a horizontally affected market in the supply of large format printers. The Parties’ combined share printers (on the basis of direct sales to end-users) does not exceed [5-10]% on the market for the supply of large format printers across the EEA or the UK. For printers for CAD applications, the Parties’ combined share does not exceed [5-10]% across the EEA and would not exceed [5-10]% in the UK. For printers for GA applications, the Parties’ combined share is below [0-5]% across the EEA or the UK. In addition, in both the EEA and the UK, the share of Apogee is below [0-5]% (reflecting the fact that it sold a total of […] large format printers over the three year period 2015-2017). The horizontal overlap in the supply of large format printers will therefore no longer be discussed in this Section. Similarly, the Proposed Transaction does not give rise to a horizontally affected market in the supply of MPS. The Parties’ combined share on this market (on the basis of direct sales to end-users) does not exceed [5-10]% on the market for the supply of MPS across the EEA (HP: [0-5]%; Apogee: [0-5]%) and would be below [10-20]% for sales in the UK alone (HP: [0-5]%; Apogee: [10-20]%). The horizontal overlap in the supply of MPS will also not be discussed further in this Section.

36 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 17 and 18; Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 5.

37 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, questions 14 and 15.

38 Replies to questionnaire Q3 – Questionnaire to enterprise customers of 19 September 2018, questions 11 and 12

39 The market shares in this section are based on the HP's total sales of regular and large format printers in the EEA and the UK through all routes to market (i.e. its "upstream" sales or direct/indirect sales to end-users). This includes sales of HP printers made through resellers, such as Apogee.

40 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentration between undertakings (the Non-Horizontal Merger Guidelines) OJ C 265/6, 18.10.2008, paragraphs 29-30.

41 See Non-Horizontal Merger Guidelines, paragraph 30.

42 See Non-Horizontal Merger Guidelines, paragraphs 33 to 39 and 60 to 67.

43 See Non-Horizontal Merger Guidelines, paragraphs 40 to 46 and 68 to 71.

44 See Non-Horizontal Merger Guidelines, paragraphs 47 to 57.

45 See Non-Horizontal Merger Guidelines, paragraphs 72 to 77.

46 Similarly, in the relation to HP’s upstream supply of RFPs when distinguished by A3/A4 and laser/inkjet, while HP has a higher market share (above 30%) for A4 inkjet printers, Apogee does not supply these printers downstream and so there is no vertical overlap for this type of printer

47 Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 2.

48 Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 11.

49 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 20.

50 Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 10.

51 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 20.

52 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 20.

53 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 21.

54 Replies to questionnaire Q2 – Questionnaire to providers of managed print services of 19 September 2018, question 11.

55 Replies to questionnaire Q1 – Questionnaire to printer suppliers of 19 September 2018, question 22.