EC, July 20, 2018, No M.8837

COMMISSION OF THE EUROPEAN COMMUNITIES

Judgment

BLACKSTONE / THOMSON REUTERS F&R BUSINESS

Subject: Case M.8837 - Blackstone / Thomson Reuters Financial and Risk Business

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 15 June 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which The Blackstone Group ("Blackstone") will acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control over Thomson Reuters Financial and Risk Business ("Thomson Reuters F&R" or "the Target") (the "Transaction") (3). Blackstone is referred to as "the Notifying Party" and Blackstone and the Target together as "the Parties".

1. THE PARTIES

(2) Blackstone is a global asset manager and provider of financial advisory services, headquartered in the US.

(3) The Target is a data and financial technology platform that provides information and data analytics, enables financial transactions, and connects communities of trading, investment, financial, corporate, strategy, treasure and risk professionals. It also provides regulatory and risk management solutions to help customers anticipate and manage risk and compliance.

2. THE OPERATION

(4) For the purpose of the Transaction, private equity funds controlled by Blackstone have formed King (Cayman) Holdings Ltd. ("HoldCo"). Canada Pension Plan Investment Board ("CPPIB") and Suzuka Investment Pte Ltd., an affiliate of GIC Private Limited ("GIC") will invest alongside Blackstone for the Transaction. CPPIB and GIC are together referred to as the Co-investors. Blackstone, CPPIB and GIC are together referred to as the Consortium. The Consortium will acquire a 55% stake in the Target through ownership by the Equity Investor Vehicle (4) (formed pursuant to Sections 2, 3 and 21 of the Equity Funding Arrangement Letters of the Transaction) of 55% of the common shares of HoldCo. Post- Transaction, Thomson Reuters will retain a 45% interest in the Target through ownership of 45% of the common shares of HoldCo. HoldCo will acquire all of the Target's assets.

(5) Blackstone will solely control the Target within the meaning of Article 3(1)(b) of the EU Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (5) (Blackstone [Confidential] in 2016 and the Target [Confidential] in 2017). Each of them has an EU-wide turnover in excess of EUR 250 million (Blackstone [Confidential] in 2016 and the Target [Confidential] in 2017), but they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The notified operation therefore has an EU dimension.

4. COMPETITIVE ASSESSMENT

(7) The Target provides a broad range of financial information products to financial market professionals, including real-time and non-real-time data services.

(8) Blackstone is active in the same markets as the Target only via Ipreo LLC ("Ipreo"), a portfolio company it controls jointly together with the Goldman Sachs group Inc. Ipreo provides software, data and market intelligence products to companies that are active in capital markets. Ipreo's and the Target's activities give rise to horizontal overlaps. (6)

(9) The Transaction also gives rise to limited vertical overlaps between the activities of Target and Blackstone (and its controlled portfolio companies).

4.1. Relevant Markets

4.1.1. Discrete Content Sets, Desktop Services, and Non-Real Time Data Feeds

4.1.1.1. Introduction

(10) The Transaction relates to the financial information industry, namely, the provision of financial information, analytics, and trading capabilities. According to the Notifying Party, the main users of the Parties' products are customers in the financial service industry, such as banks, traders, funds, and corporate customers.

(11) Financial information can be categorized in real-time and non-real time market data. Real-time data consists of indicative or tradable prices for various types of financial instruments such as equities, corporate and government bonds, currency and traded commodities. Real-time data changes rapidly during the day and it is updated every millisecond. It is required by security dealers, foreign exchange dealers, and investment advisers for immediate consumption. Non-real time data is more general financial or economic information which may vary between days and parts of a day, but not every second. It does not satisfy real-time demands and is primarily adapted to research and customer awareness demands.

(12) In the financial information business, there are different methods for the supply of financial information products to customers:

a) Financial information can be delivered by suppliers to customers as "datafeeds" through an application programming interface (API), where the customers obtain their content in a direct or "raw" data format, from which they build their own internal applications or portals; and

b) Financial information can also be integrated into "desktop solutions", namely, retail products, which contain a "front-end" window that enables the user to access the content and functionalities contained in the product on the screen. Such front-end windows can take the form of either a web-delivered solution or a deployed/physical solution. (7)

(13) According to the Notifying Party, the vast majority of suppliers, including the Target, supply their content using both methods (directly to end-users as a datafeed and as a desktop solution).

4.1.1.2. Relevant Product Market

(14) In Thomson/Reuters, the Commission's market investigation indicated that for financial information "discrete content sets represent the appropriate antitrust markets for assessing the impact" of the transaction that was under review. (8) The investigation in that case suggested that the value of the products in the financial information business lies in their functionalities and content. (9) The majority of both customers and competitors considered in that case that "individual content sets are not substitutable for one another". (10) The Commission therefore identified separate relevant markets for each type of data content sets. (11) Regarding non-real time content, the Commission identified separate markets for fundamentals content sets, deals content sets, ownership content sets, and other types of content. (12) The Commission clarified that each of the discrete content sets may be sold/delivered in various modalities: as standalone products (e.g., as databases or datafeeds) or as part of a desktop service. (13)

(15) In the present case, the Notifying Party disagrees with the market delineation in Thomson/Reuters. It submits that relevant markets for financial information products should not be sub-segmented based on discrete content sets because the competitive landscape and the market dynamics have continued to evolve significantly in the 10 years since the Thomson/Reuters decision. According to the Notifying Party, financial information suppliers (including the Target) moved towards packaged solutions (desktop services and datafeeds). For such packaged solutions, competition takes place at the level of the comprehensive packaged desktop or datafeed rather than at the level of discrete content sets or functionalities.

(16) In light of the above, the Notifying Party proposed relevant product markets for (i) desktop services, (ii) non-real-time datafeed services and (iii) real-time datafeed services. However, for the purpose of this transaction real-time datafeed services are not a relevant market as the Parties activities do not overlap for real- time datafeed services:

a) Desktop services. Desktop services include comprehensive integrated desktops, more narrowly focused integrated desktops (a.k.a., workstations or terminals) and content/functionality sold for individual use which can be incorporated or used in/alongside an integrated desktop. The Notifying Party submitted that financial information suppliers typically provide desktop services that comprise multiple sources of different types of financial data. According to the Notifying Party, the various content sets and functionalities in these solutions are not priced separately and cannot be accessed outside of the comprehensive packaged desktop product.

b) Non-real time datafeeds. Non-real time datafeeds combine various types of general financial or economic (historical or archival) information. According to the Notifying Party, non-real time datafeeds do not belong in the same market as real time datafeeds. The characteristics of the two types of datafeeds are very different. For real time datafeeds, timeliness is the most important feature, while for non-real time datafeeds the focus is on completeness and reliability of the information. Real-time datafeeds and non- real time datafeeds also address different types of demand as explained in Section 4.1.1.1 above. The Commission has confirmed in its decisional practice that real time datafeeds belong to relevant markets separate from non- real time datafeeds. (14)

(17) The market investigation did not support the view of the Notifying Party that customers typically only purchase financial information as part of packaged solutions. The vast majority of customers stated that they continue to buy financial information in the form of discrete content sets and not only in packaged solutions. (15) All of the respondents confirmed that when purchasing financial information, they compare the offering of discrete content sets and packaged solutions. (16) Many respondents admitted that packaged solutions lead to cost savings and allow users to be more efficient. (17) But customers also highlighted that they sometimes need to source discrete content sets from different suppliers, for example "to obtain the maximum data coverage and in order to ensure data comparisons for data quality processes" or "if a packaged solution does not contain the data [the customer] need[s]". (18)

(18) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible product market definition (discrete content sets or packaged solutions).

4.1.1.3. Relevant Geographic Market

(19) The Notifying Party submitted that the relevant geographic scope for desktop services is worldwide or at least EEA-wide as both customers and competitors are active globally or at least regionally and the core offering remains the same throughout the world and/or the region. The market investigation confirmed this. (19)

(20) The Notifying Party submitted that the relevant geographic scope for non-real- time datafeeds is worldwide or at least EEA-wide. The market investigation did not bring any element to the Commission's attention which would suggest that the market is narrower than EEA-wide.

(21) The Notifying Party recalled that in Thomson/Reuters, the Commission considered that the relevant geographic scope for discrete content sets was EEA- wide or potentially global in scope. The market investigation in the present case confirmed this. (20)

(22) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible geographic market definition (EEA-wide or worldwide).

4.1.2. Consolidated Real Time Datafeeds

(23) A real time datafeed is a virtual pipeline that supplies continually updated market information. Real-time data feeds can be used in applications developed by banks and financial institutions, for example to allow for electronic or algorithmic trading. (21) There are two types of real time datafeeds: consolidated and direct. Consolidated real time datafeeds involve the aggregation of feeds from various sources into a single source. Direct real time datafeeds involve a more direct connection from an individual exchange to a customer. (22) In Reuters Instrument Codes, the Commission found that consolidated real time datafeeds and direct real time datafeeds belong to different product markets. (23) The Notifying Party submits that it is not necessary to define conclusively the relevant product market.

(24) In Reuters Instrument Codes, the Commission defined the market for consolidated real time datafeeds as worldwide. (24) The Notifying Party submits that it is not necessary to define conclusively the relevant geographic market.

(25) For the purposes of the present case, the Commission considers that there is a separate relevant market for consolidated real time datafeeds, which is worldwide in scope.

4.1.3. Market Data Platform Services

(26) Market data platform services ("MDPs") are "middleware" that receive datafeeds from multiple sources (including real time datafeeds and other sources) as inputs and distribute this information to terminals, applications, wireless devices and the internet. (25), In its decisional practice, the Commission defined a separate market for MDPs. (26) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant product market.

(27) In previous decisions, the Commission has considered the geographic market for MDP to be at least EEA-wide or worldwide, but left the geographic scope open. (27) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant geographic market.

(28) For the purposes of the present case, the Commission considers that there is a separate relevant product market for MDPs. The exact geographic scope of the market can be left open, as no serious doubts arise under an EEA-wide or a worldwide market definition.

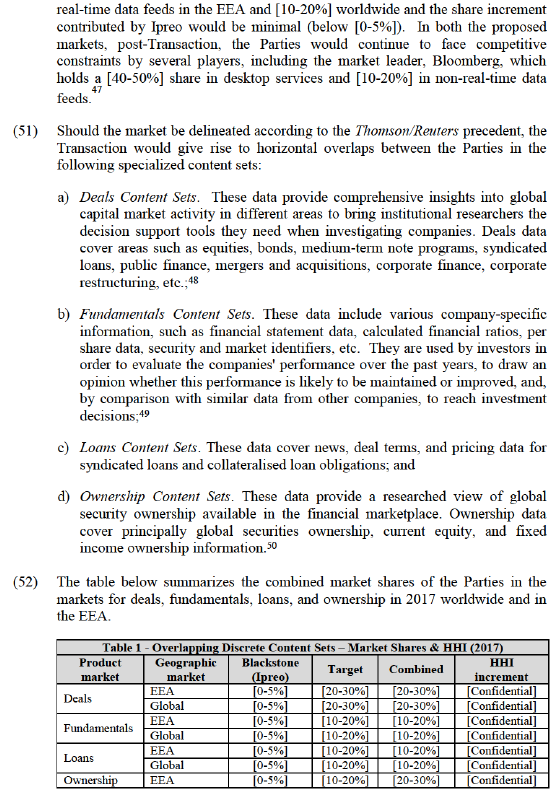

4.1.4. Life Insurance

(29) In its decisional practice, the Commission has made a distinction between three broad categories of insurance products, namely (i) life insurance; (ii) non-life insurance; and (iii) reinsurance. With respect to the life insurance market, the Commission has distinguished between (i) pure protection products; (ii) pension products; and (iii) investment products, but also considered pension and investment products together as part of the same product market. (28) Additionally, the Commission has considered distinguishing between life insurance for individuals and group customers, or between products based on the type of risk covered. Ultimately, the product market definition has been left open. (29) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant product market.

(30) In previous cases, the Commission considered that the market for Life Insurance is national. (30) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant geographic market.

(31) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible product or geographic market definition.

4.1.5. Bulk Annuity Insurance Transactions

(32) Bulk annuity insurance transactions are de-risking transactions that are common in the insurance business, especially in relation to Defined Benefit pension schemes. In a bulk annuity insurance transaction, all of the risk associated with the pension liabilities is transferred to a third party. In its decisional practice, the Commission considered that a separate market exists for bulk annuity insurance transactions. (31) The Commission has also considered a further distinction in the bulk annuity insurance transactions market between buy-in and buy-out transactions, but ultimately left the product market open (32). The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant product market.

(33) In previous cases, the Commission considered that the market for bulk annuity contracts is national in scope. (33) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant geographic market.

(34) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible product or geographic market definition.

4.1.6. Asset management

(35) In its decisional practice, the Commission described asset management as the provision and potential implementation of investment advice. (34) It also considered that asset management may include the creation and managing of mutual funds which are then marketed on an “off-the-shelf” basis, including to retail customers, the provision of portfolio management services to institutional investors (pension funds, institutions and international organisations), and the provision of custody services related to asset management. The Commission also considered the possibility of there being a relevant product market for asset management, which would include the creation and management of mutual funds for retail clients and tailor-made funds for corporate and institutional customers, and portfolio management for private investors, pension funds and institutions. (35) The Commission further considered the possible existence of separate relevant product markets for each of the types of products mentioned above, (36) but ultimately left the product market open. The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant product market.

(36) In previous cases, the Commission considered that the market for asset management is national or EEA-wide in scope. (37) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant geographic market.

(37) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible product or geographic market definition.

4.1.7. Investment banking

(38) Investment banking includes services such as advice on the financial aspects of mergers and acquisitions, initial public offerings and arranging new issues of stocks and bonds, excluding the underwriting of such operations. In its decisional practice, the Commission analysed the market for investment banking as a whole, while identifying the following possible market segments: (i) merger and acquisition advice; (ii) capital markets business such as Initial Public Offering and share issues advice; and (iii) Services relating to arranging new issues as stocks and bonds. (38) The Commission ultimately left the product market open. The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant product market.

(39) In previous cases, the Commission has considered the relevant geographic market to be national or international (EEA-wide or global), but ultimately left the geographic market open. (39) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant geographic market.

(40) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible product or geographic market definition.

4.1.8. Financial market services

(41) Financial market services are provided to institutional investors, corporate clients, and professional traders who lack direct access to financial markets or otherwise value the intermediary services provided by a bank. In its decisional practice, the Commission distinguished within the market for financial market services between the following sub-segments: (i) trading in securities, bonds and derivatives, (ii) foreign exchange trading, (iii) money market operations and (iv) trading of other asset classes (40), but ultimately left the product market open. The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant product market.

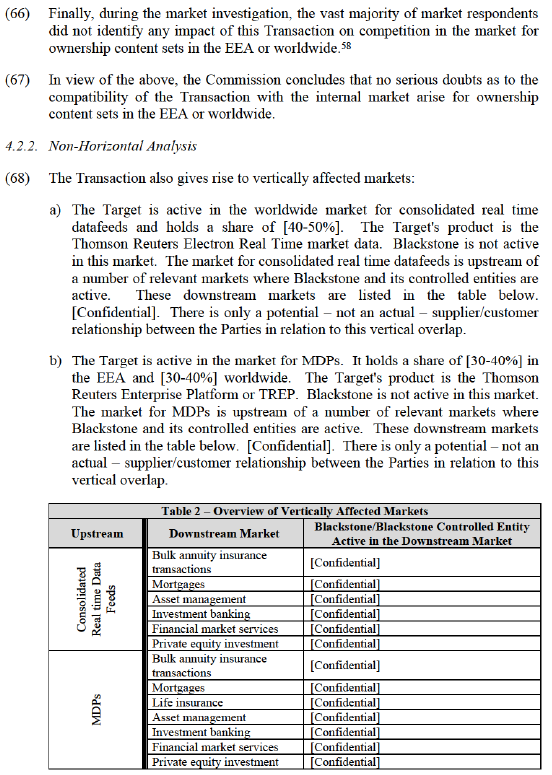

(42) The Commission has considered the relevant geographic market to be national or wider (EEA or global) (41), but ultimately left the geographic market open. The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant geographic market.

(43) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible product or geographic market definition.

4.1.9. Private equity investment

(44) Private equity investment is the investment of equity in unquoted companies (i.e., companies whose shares are not quoted on any public exchange). The supply of funds for equity investment can comprise equity and debt finance. In its decisional practice, the Commission considered a further distinction between the supply of debt and equity finance. (42) The Commission has also considered private equity as a segment of the corporate finance market or asset management services, but ultimately left the market definition open. (43) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant product market.

(45) In previous decisions, the Commission considered the market for private equity investment could be considered either national or wider, but ultimately left the geographic market open. (44) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant geographic market.

(46) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible product or geographic market definition.

4.1.10. Mortgages

(47) As described in recital (46), the Commission has in previous decisions distinguished three segments within the banking market, namely retail banking; corporate banking; and financial market services. The Commission also considered mortgages as a potential market sub-segment within the retail banking market. The exact product market definition has been left open. (45) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant product market.

(48) In previous decisions, the Commission considered the market for retail banking services (including mortgages) to be national in scope, but ultimately left the market open. (46) The Notifying Party submits that for the purpose of the present case it is not necessary to define conclusively the relevant geographic market.

(49) In any event, for the purposes of the present case, the exact market definition can be left open, as no serious doubts arise under any plausible product or geographic market definition.

4.2. Competitive Assessment

4.2.1. Horizontal Analysis

(50) In the market segments that the Notifying Party proposed as horizontally overlapping (i.e., desktop services and non-real time data feeds), the Transaction does not give rise to affected markets worldwide or in the EEA. The combined entity would hold [10-20%] in desktop services in the EEA and [10-20%] worldwide and the share increment contributed by Ipreo would be minimal (below [0-5%]). The combined entity would have a share of [10-20%] in non-

![]()

4.2.1.1. Deals Content Sets

(53) In deals content sets, post-Transaction the Parties will have a combined market share of [20-30%] post-Transaction globally and in the EEA. The share increment contributed by Ipreo is less than [0-5%] (i.e., less than [0-5%] in the EEA and less than [0-5%] worldwide). The HHI increment is minimal. Post- Transaction, the combined entity will continue to face significant constraints from at least five players, i.e., Dealogic, Bloomberg, Acuris, S&P, and FactSet.

(54) Moreover, according to the Parties, the Target and Ipreo are not close competitors. The Target is a "Tier 1" (51) player in this space (alongside Dealogic) while Ipreo has very limited presence.

(55) Finally, during the market investigation, the vast majority of market respondents did not identify any impact of this Transaction on competition in the market for deals content sets in the EEA or worldwide. (52)

(56) In view of the above, the Commission concludes that no serious doubts as to the compatibility of the Transaction with the internal market arise for deals content sets in the EEA or worldwide.

4.2.1.2. Fundamentals Content Sets

(57) In fundamental content sets, the Transaction gives rise to an affected market only at worldwide level (where the combined share of the Parties is [15-25%]). The market is not affected at EEA level. At global level, the share increment contributed by Ipreo is [0-5%]. The HHI increment is minimal. Post- Transaction, the combined entity will continue to face significant constraints from at least eleven competitors, including major players like Bloomberg, FactSet, and S&P Global, as well as other smaller rivals, such as Morningstar, Zacks, Edgar Online, Toyo Keizai, Fitch, Value Line, World'Vest Base, and Mergent.

(58) Moreover, according to the Parties, the Target and Ipreo are not close competitors. The Target is a "Tier 1" player in this space while Ipreo has very limited presence. Ipreo does not collect or own its own fundamentals database. It is simply a re-distributor of FactSet fundamentals (and estimates) content. (53)

(59) Finally, during the market investigation, the vast majority of market respondents did not identify any impact of this Transaction on competition in the market for fundamentals content sets worldwide. (54)

(60) In view of the above, the Commission concludes that no serious doubts as to the compatibility of the Transaction with the internal market arise for fundamentals content sets worldwide.

4.2.1.3. Loans Content Sets

(61) In loans content sets, the Transaction gives rise to an affected market only at EEA-wide level (where the combined share of the Parties is [10-20%]). The market is not affected at worldwide level. At EEA-wide level, the share increment contributed by Ipreo is [0-5%]. The HHI increment is minimal. Post- Transaction, the combined entity will continue to face significant constraints from at least five competitors, including major players like IHS Markit, S&P Global Market Intelligence (CapIQ), and Bloomberg and other rivals, such as Dealogic, Loan Radar, and Moody's (through its recent acquisition of Bureau Van Dijk).

(62) Finally, during the market investigation, the vast majority of market respondents did not identify any impact of this Transaction on competition in the market for loans content sets in the EEA. (55)

(63) In view of the above, the Commission concludes that no serious doubts as to the compatibility of the Transaction with the internal market arise for loans content sets in the EEA.

4.2.1.4. Ownership Content Sets

(64) In ownership content sets, the Parties will have a combined market share of [20- 30%] in the EEA and [20-30%] globally post-Transaction. The share increment contributed by Ipreo is [0-5%] or less. Post-Transaction, the combined entity will continue to face significant constraints from at least five players, i.e., FactSet, Bloomberg, S&P Global Market Intelligence (CapIQ), Morningstar, and Dealogic.

(65) According to the Notifying Party, Ipreo's and the Targets products do not compete closely. The market investigation confirmed this. The majority of the respondents identified FactSet as the closest competitor to the Target, in terms of scope of the data offered, price, after-sales services, and integration possibilities. (56) The respondents were also asked to rank seven providers of ownership content sets (Ipreo, the Target, FactSet, Bloomberg, CapIQ, MorningStar, and Dealogic) from strongest to weakest taking into account their sales in the EEA in 2017. The majority ranked the Target as the strongest or second strongest and Ipreo only as the weakest or second weakest. (57) The Notifying Party added that Ipreo's and the Target's products do not compete closely because they are delivered to the customers through different channels. Ipreo provides its content either through a standalone web-based solution or via a customer relationship management ("CRM") system. In contrast, the Target is not active in the CRM space, but provides its ownership content either as part of its flagship comprehensive integrated desktop service (Eikon) or as a datafeed which is sold to clients and is then integrated into the client's proprietary software.

(69) The remainder of this Section examines together the vertical links between the same upstream market and the different downstream markets. This is the case because (i) the Target offers the same product (or product family) in the upstream market to all types of downstream customers and it understands that its rivals do the same and (ii) the competitive assessment for each of these vertical links is based on comparable considerations.

4.2.2.1. Consolidated real time datafeeds (upstream) and bulk annuity insurance transactions, mortgages, asset management, investment banking, financial market services, and private equity investment (downstream)

Input Foreclosure

(70) The Notifying Party submitted that post-Transaction the combined entity will not have the ability or the incentive to foreclose downstream competitors, by restricting access to consolidated real time datafeeds for the following reasons. First, the consolidated real time datafeeds are not a necessary input for any of the downstream markets where Blackstone and its controlled entities are active. Second, any input foreclosure strategy would be defeated by the Target's rivals who can satisfy demand in the downstream markets. Third, any potential gains of a hypothetical input foreclosure strategy would be very low in view of the limited market share of Blackstone and its controlled entities in each of the downstream markets, irrespective of their precise delineation.

The Commission considers that post-Transaction, the combined entity would not have the ability to foreclose its downstream rivals. Such an ability exists only when by reducing access to its upstream products, the combined entity negatively affects the overall availability of inputs for the downstream market. This is the case where the remaining upstream suppliers are less efficient, offer less preferred alternatives, or lack the ability to expand output in response to the supply restriction. (59) By contrast, in consolidated real time datafeeds, the Target faces competition by several major players, e.g., Bloomberg (with a share of [20-30%]) and ICE ([0-10%]). These players could expand output to supply consolidated real time datafeeds for any downstream players that the Target might decide to foreclose.

(71) Nor would the combined entity have the incentive to foreclose its downstream rivals. The total consolidated real-time datafeed expenditure of Blackstone and all its controlled entities amounts to USD [confidential], which is less than [0-5%] of the Target's total sales in this market in 2017. Any input foreclosure strategy would likely lead to a loss in consolidated real-time datafeeds that is not commensurate to any possible gain in the downstream markets.

(72) The respondents in the market investigation did not raise any concern as regards the potential input foreclosure in the downstream markets for bulk annuity insurance transactions, mortgages, asset management, investment banking, financial market services, and private equity investment by restricting access to the Target's consolidated real time datafeeds.

Customer Foreclosure

(73) The Notifying Party submitted that post-Transaction the combined entity will not have the ability or the incentive to foreclose upstream competitors in consolidated real time datafeeds, by restricting access to Blackstone's demand in the downstream markets. First, even if Blackstone and its controlled entities were to purchase consolidated real-time datafeeds exclusively from the Target, a significant and more than sufficient customer base remains available for the Target's rivals. Second, Blackstone portfolio entities will not start purchasing consolidated real time datafeeds exclusively from the Target, unless this is in the best interests of each entity's investor base. According to the Notifying Party, this in itself prevents a foreclosure strategy.

(74) The Commission considers that post-Transaction, Blackstone would not have the ability to foreclose its upstream rivals in consolidated real time datafeeds. Post- Transaction, sufficient economic alternatives will remain in the downstream market for upstream rivals to sell their output. The total expenditure of Blackstone and its controlled entities on consolidated real time datafeeds represents only [0-5%] of the total worldwide demand for these products in 2017.

(75) According to the Non-Horizontal Guidelines, an ability to foreclose upstream rivals exists only where the merger involves a company which is an important customer with a significant degree of market power in the downstream market. (60) Blackstone and its controlled entities do not have a significant degree of market power in the downstream markets where they are active. According to the Notifying Party, their share never exceeds 30% in any of the downstream markets. (61) Moreover, in each of these markets, Blackstone and its controlled entities face competitive constraints from several large players who likely constitute a significantly large customer base for consolidated real-time datafeeds in the future. (62)

(76) The respondents in the market investigation did not raise any concern as regards the potential customer foreclosure in the upstream market for consolidated real time datafeeds by restricting access to Blackstone's demand for these services.

Conclusion

(77) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the vertical link between Consolidated real time datafeeds (upstream) and bulk annuity insurance transactions, mortgages, asset management, investment banking, financial market services, and private equity investment (downstream).

4.2.2.2. MDPs (upstream) and bulk annuity insurance transactions, mortgages, life insurance, asset management, investment banking, financial market services, and private equity investment (downstream)

Input Foreclosure

(78) The Notifying Party submitted that post-Transaction the combined entity will not have the ability or the incentive to foreclose downstream competitors, by restricting access to MDPs for the following reasons. First, MDPs are not a necessary input for any of the downstream markets where Blackstone and its controlled entities are active. Second, any input foreclosure strategy would be defeated by the Target's rivals who can satisfy demand in the downstream markets. Third, any potential gains of a hypothetical input foreclosure strategy would be very low in view of the limited market share of Blackstone and its controlled entities in each of the downstream markets, irrespective of their precise delineation.

(79) The Commission considers that post-Transaction, the combined entity would not have the ability to foreclose its downstream rivals. Indeed, the combined entity would not be able to affect the overall availability of MDPs for the downstream markets. The share in this (upstream) market barely exceeds 30% and the Target faces competition by several major MDP players, e.g., Bloomberg (with a share of [30-40%] in the EEA and [30-40%] worldwide), Informatica ([20-30%] in the EEA and [20-30%] worldwide), and Solace Systems ([0-10%] in the EEA and [0- 10%] worldwide). These players could expand output to supply MDPs for any downstream players that the Target might decide to foreclose.

(80) Nor would the combined entity have the incentive to foreclose its downstream rivals for two reasons:

a) The total worldwide MDP expenditure of Blackstone and all its controlled entities amounts to [confidential]. This represents [less than 10%] of the Target's total MDP sales worldwide and [20-30]% of the Target's total MDP sales in the EEA in 2017. (63) Any input foreclosure strategy would likely lead to a loss of revenues in the MDPs market that is not commensurate to any possible gain in the downstream markets.

b) The (fixed) cost of developing and updating MDPs is high, while the marginal cost of selling one additional unit is low. MDP suppliers typically seek to spread their fixed costs over a sufficiently large base of customers. The combined entity has no incentive to forego this opportunity by restricting access of third parties to its MDPs.

(81) The respondents in the market investigation did not raise any concern as regards the potential input foreclosure in the downstream market for bulk annuity insurance transactions, mortgages, life insurance, asset management, investment banking, financial market services, and private equity investment by restricting access to the Target's MDPs.

Customer Foreclosure

(82) The Notifying Party submitted that post-Transaction the combined entity will not have the ability or the incentive to foreclose upstream competitors in MDPs, by restricting access to Blackstone's demand in the downstream markets. First, even if Blackstone and its controlled entities were to purchase MDPs exclusively from the Target, a significant and more than sufficient customer base remains available for the Target's rivals. Second, Blackstone portfolio entities will not start purchasing MDPs exclusively from the Target, unless this is in the best interests of each entity's investor base. According to the Notifying Party, this in itself prevents a foreclosure strategy.

(83) The Commission considers that post-Transaction, Blackstone would not have the ability to foreclose its upstream rivals in MDPs. A sufficient number of customers will remain in the downstream markets for upstream rivals to sell their output. The total worldwide expenditure of Blackstone and its controlled entities on MDPs represents less than [0-5%] of the total worldwide demand for these products in 2017 and less than [5-10%] of the total demand in the EEA. (64)

(84) According to the Non-Horizontal Guidelines, an ability to foreclose upstream rivals exists only where the merger involves a company which is an important customer with a significant degree of market power in the downstream market. (65) Blackstone and its controlled entities do not have a significant degree of market power in the downstream markets where they are active. According to the Notifying Party, their share never exceeds 30% in any of the downstream markets. (66) Moreover, in each of these markets, Blackstone and its controlled entities face competitive constraints from several large players who likely constitute a significantly large customer base for MDPs in the future. (67)

(85) The respondents in the market investigation did not raise any concern as regards the potential customer foreclosure in the upstream market for market data platform services by restricting access to Blackstone's demand for these services.

Conclusion

(86) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the vertical link between market data platform services (upstream) and bulk annuity insurance transactions, mortgages, life insurance, asset management, investment banking, financial market services, and private equity investment (downstream).

5. CONCLUSION

(87) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the 'EEA Agreement').

3 Publication in the Official Journal of the European Union No C 228, 29.06.2018, p. 33.

4 [Confidential]. Neither CPPIB nor GIC will obtain any rights in the Target which rise to the level of control as defined by the Merger Regulation.

5 Turnover calculated in accordance with Article 5 of the Merger Regulation.

6 In May 2018, Blackstone agreed to sell Ipreo to IHS Markit Ltd. This transaction is expected to close in the second half of 2018, effectively removing all horizontal overlaps between the Parties. However, by the time the Commission had to adopt a decision on the Transaction, the IHS Markit/Ipreo deal was not completed. For the purposes of the competitive assessment of the Transaction, Ipreo is considered as part of Blackstone.

7 M.4726, Thomson Corporation / Reuters Group, paras. 25-28.

8 M.4726, Thomson Corporation / Reuters Group, para. 43.

9 M.4726, Thomson Corporation / Reuters Group, para. 43.

10 M.4726, Thomson Corporation / Reuters Group, paras. 44-46.

11 M.4726, Thomson Corporation / Reuters Group, para. 61ff.

12 M.4726, Thomson Corporation / Reuters Group, paras. 74ff., in particular, 82ff., 88, and 89.

13 M.4726, Thomson Corporation / Reuters Group, para. 50.

14 See AT.39654 – Reuters Instrument Codes, para. 29 and M.4726, Thomson Corporation / Reuters Group, paras. 65ff. which define markets for consolidated real-time datafeeds and direct real-time datafeeds.

15 See Questionnaire Q1 – Customers, Q3 and Q10.

16 See Questionnaire Q1 – Customers, Q3.4.

17 See Questionnaire Q1 – Customers, Q3.2.

18 See Questionnaire Q1 – Customers, Q3.1.

19 See Questionnaire Q1 – Customers, Q8.1.

20 See Questionnaire Q1 – Customers, Q14.

21 AT.39654, Reuters Instrument Codes, para. 24.

22 M.4726, Thomson Corporation / Reuters Group, para. 66.

23 M.4726, Thomson Corporation / Reuters Group, para. 29.

24 AT.39654, Reuters Instrument Codes, para. 31.

25 M.4726, Thomson Corporation / Reuters Group, para. 68.

26 M.4726, Thomson Corporation / Reuters Group, paras. 62 and 69 and M.3692, Reuters/Telerate, para. 13.

27 M.3692, Reuters/Telerate, para 16 and M.4726, Thomson Corporation / Reuters Group, para 111.

28 M.5075, Vienna Insurance Group / EBV; M.5728, Crédit Agricole / Société Générale Asset Management; M.5384, BNP Paribas / Fortis.

29 M.6883, Canada Life / Irish Life, M.6521, Talanx International / Meiji Yasuda Life Insurance / Warta, M.4701, Generali / PPF Insurance Business, M.4047, Aviva / Ark Life, M.1453 AXA / GRE.

30 M.6521, Talanx International / Meiji Yasuda Life Insurance / Warta; M.5075, Vienna Insurance Group / EBV and M.5057, Aviva / UBI Vita, M.6883, Canada Life/ Irish Life

31 M.8257, NN Group / Delta Lloyd, para 88; M.7204, Rothesay Life / Metlife Assurance.

32 M.8257, NN Group / Delta Lloyd, para 88

33 M.8257, NN Group/Delta Lloyd, para. 91 and M.7204, Rothesay Life / Metlife Assurance, para. 28.

34 M.8257, NN Group / Delta Lloyd, para. 108.

35 M.6812, SFPI / Dexia, M.3894 Unicredito/HVB, M.8257, NN Group / Delta Lloyd.

36 M.8257, NN Group/Delta Lloyd, para. 110.

37 M.8257, NN Group / Delta Lloyd, para. 110.

38 M.5384, BNP Paribas / Fortis, M.6168, RBI / EFG EUROBANK / JV, M.4692, Barclays / ABN AMRO, M.3894, Unicredito / HVB.

39 M.5726, Deutsche Bank / SAL Oppenheim, M.5384, BNP Partibas / Fortis, M.7044, Blackstone / Goldman Sachs / Rothesay.

40 M.3894, Unicredito / HVB, M.4692, Barclays / ABN AMRO, M.5384, BNP Paribas / Fortis, M.5726,

Deutsche Bank / SAL Oppenheim, and M.6168, RBI/EFG Eurobank / JV.

41 M.3894, Unicredito / HVB, M.4692, Barclays / ABN AMRO, M.5384, BNP Paribas / Fortis, M.5726,

Deutsche Bank / SAL Oppenheim; and M.6168, RBI / EFG Eurobank / JV.

42 M.2577, GE Capital / Heller Financial.

43 M.6738, Goldman Sachs / KKR / QMH, M.6832, Goldman Sachs / TPG Lundy / Ainscough, M.6841,

Goldman Sachs / TPG Lundy / Tulloch Homes Group Limited.

44 M.2577, GE Capital / Heller Financial.

45 M.5384, BNP Paribas / Fortis, M.4844, Fortis / ABN Amro assets, M.8553, Banco Santander / Banco Popular, M.6405, Banco Santander / Rainbow.

46 M.5384 BNP Paribas / Fortis, M.4844 Fortis/ABN Amro assets, M.8553 Banco Santander/Banco Popular, M.6405 Banco Santander/Rainbow.

47 Both worldwide and in the EEA

48 M.4726, Thomson Corporation / Reuters Group, para. 89.

49 M.4726, Thomson Corporation / Reuters Group, para. 82.

50 M.4726, Thomson Corporation / Reuters Group, para. 88.

51 Tier 1 suppliers offer broader and deeper coverage than Tier 2 suppliers for fundamental content sets. Examples of Tier 1 suppliers for fundamental content sets are Bloomberg, FactSet, S&P Global and The Target. Examples of Tier 2 suppliers are Morningstar, Zacks, Edgar Online, Toyo Keizai, Fitch, Value Line; World'Vest Base, Mergent and other smaller suppliers.

52 See Questionnaire Q1 – Customers, Q20.

53 See https://ipreo.com/targeting-services/.

54 See Questionnaire Q1 – Customers, Q18.

55 See Questionnaire Q1 – Customers, Q18.

56 See Questionnaire Q1 – Customers, Q11.

57 See Questionnaire Q1 – Customers, Q12.

58 See Questionnaire Q1 – Customers, Q20.

59 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 265, 18.10.2008, p. 7 ("Non-Horizontal Merger Guidelines"), para. 36.

60 Non-Horizontal Merger Guidelines, para. 61.

61 See Notifying Party's submission of 18 July 2018, "Addendum to Additional Submission of 18 July 2018".

62 According to the Notifying Party, key rivals of Rothesay Life Limited in bulk annuity insurance transactions include L&G, PIC, Scottish Windows, Phoenix Live, JRP, Aviva, and Canada Life; key rivals of the Northview Group in mortgages (in the UK) include Lloyds Banking Group, Nationwide BS, Royal Bank of Scotland, Santander UK, Barclays, HSBC Bank, Coventry BS, Virgin Money, Yorkshire BS, and TSB Bank; key rivals of Blackstone and First Eagle Management in asset management include Barclays, Allianz, AXA, and ING; key rivals of Blakcstone in investment banking and financial market services include Goldman Sachs, JP Morgan Chase, Morgan Stanley, and Credit Suisse; and key rivals of Blackstone in private equity investment include Blackrock, Lazard, Citigroup, and Deutsche Bank.

63 This figure is overstated, as it compares the total worldwide MDP expenditure of Blackstone and its controlled entities with the total MDP sales of the Target in the EEA. The total MDP expenditure of Blackstone and its controlled entities in the EEA was not available to the Notifying Party.

64 This figure is overstated, as it compares the total worldwide MDP expenditure of Blackstone and its controlled entities with the total demand for MDP products in the EEA. The total MDP expenditure of Blackstone and its controlled entities in the EEA was not available to the Notifying Party.

65 Non-Horizontal Merger Guidelines, para. 61.

66 See Notifying Party's submission of 18 July 2018, "Addendum to Additional Submission of 18 July 2018".

67 See fn. 62 above. According to the Notifying Party, key rivals of The Lombard Group in life insurance (in the UK) include Cardif, Swiss Life, La Mondiale, Allianz, Generali and AXA.