Commission, June 19, 2017, No M.8360

EUROPEAN COMMISSION

Judgment

IMERYS / KERNEOS

Subject: Case M.8360 – Imerys / Kerneos

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 12 May 2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Imerys SA (‘Imerys’, France) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control over Kerneos SA (‘Kerneos’, France) by way of a purchase of shares ('the proposed Transaction’) (3). Imerys is hereinafter referred to as the ‘Notifying Party’, Imerys and Kerneos are collectively referred to as the ‘Parties’ whilst the undertaking resulting from the proposed Transaction is referred to as ‘the merged entity’.

1. THE PARTIES

(1) Imerys is a French company that mines and transforms minerals, ultimately controlled by Power Corporation of Canada and the Frère-Bourgeois family. Imerys operates in four business groups: (a) Energy Solutions & Specialties, (b) Filtration & Performance Additives, (c) Ceramic Materials, and (d) High Resistance Minerals.

(2) Kerneos is a global supplier of specialty cements for different sectors, in particular the building chemistry and refractory sectors, and also operates a bauxite mining business. Kerneos is ultimately controlled by private equity company Astorg.

2. THE OPERATION

(3) Imerys and the current owners of Kerneos signed a Sale and Purchase Agreement on 26 April 2017, according to which Imerys will acquire all of the shares and voting rights in Kerneos. Imerys will thus acquire sole control of Kerneos.

(4) The notified operation therefore constitutes a concentration pursuant to Article 3(1)(b) of the Merger Regulation.

3. UNION DIMENSION

(5) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 2 500 million (4). In three Member States (Germany, France and the United Kingdom) the combined aggregate turnover of the undertakings concerned is above EUR 100 million and the turnover of each of them is more than EUR 25 million. Each of them has a Union-wide turnover in excess of EUR 100 million, but they do not achieve more than two-thirds of their aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension within the meaning of Article 1(3) of the Merger Regulation.

4. MARKET DEFINITION

4.1. Introduction

(6) The proposed Transaction mainly concerns the refractory value chain where calcium aluminate cement (‘CAC’) and industrial minerals are used in the production of acid monolithic refractories. Kerneos is active in the production and supply of CAC while Imerys is active in the supply of various industrial minerals as well as in the supply of acid monolithic refractories. In addition, Imerys also produced and supplies CAC in India; however, it makes no sales of CAC to third parties in the EEA.

(7) Therefore, the proposed Transaction gives rise to vertically affected markets between Kerneos’ supply of CAC (upstream) and Imerys’ activities in the supply of acid monolithic refractories (downstream).

(8) With regard to industrial minerals, no vertically affected markets arise, but the Commission has assessed any conglomerate effects that could arise due to the addition of CACs into Imerys’ portfolio of products that are used for the production of refractories.

(9) In addition to the refractories value chain, CAC is used in the production of various building chemistry applications. While neither of the Parties is active in building chemistry, Imerys supplies certain industrial minerals that – like CAC – are used in the production of building chemistry products. Therefore, the Commission has assessed any conglomerate effects that could arise due to the addition of CACs into Imerys’ product portfolio with respect to building chemistry applications.

4.2. Relevant product market

4.2.1. Calcium Aluminate Cement (‘CAC’)

(10) CAC is a type of specialty cement. Differently from ‘ordinary’ Portland cement, CAC consists predominantly of hydraulic calcium aluminates rather than calcium silicates. CAC has special properties, is considerably more expensive than ordinary cements and is used in different applications.

(11) CAC is produced with a wide range of alumina contents, from around 40% to 80% alumina. According to the Notifying Party, three types of CAC can be distinguished based on their alumina content: low alumina cement (‘LAC’) (<45%), medium alumina cement (‘MAC’) (ca. 40–60%) with the potential substitute bauxite cement (‘BxC’) (45–55%) (5), and high alumina cement ‘HAC’ (>60%, typically 70–80% (6)).

(12) In addition to different alumina contents, the different subtypes of CAC presented in paragraph (11) are produced from different raw materials and through different production methods: While LAC and MAC can be produced through a fusion- process in a reverbatory kiln or an electric arc furnace, the production of HAC requires sintering in a rotary kiln. As to inputs, red bauxite is used for LAC; white bauxite for MAC; and calcined alumina, which is purer than the bauxites used for lower alumina cements, for HAC.

(13) The Commission has previously considered a separate product market for specialty cements, while also considering the possibility of a narrower market for aluminates-based specialty cements, but ultimately left the precise market definition open. (7) In addition, in past cases dealing with neighbouring industrial minerals, the Commission endorsed a product market definition based on a single mineral employed for a given end-use application. (8) In line with this approach, the product market for CAC could be further segmented by application into the market for CAC for (i) refractory applications, (ii) building chemistry applications and (iii) other applications.

(14) The Notifying Party submits that CAC can be substituted by other binders in some applications. Furthermore, the Notifying Party argues that different grades of CAC (HAC, MAC and LAC) could be treated as separate product markets but without any further segmentation by end-use since CACs for different applications are generally the same products with differences limited to packaging and branding. The Notifying Party nonetheless acknowledges that there is no or only limited supply-side substitutability between HAC and the lower alumina content cements due to the different production processes.

(15) The Commission's investigation has indicated that customers active in refractories are generally not able to easily substitute CAC by other binders in the production process of acid monolithic refractories.

(16) Moreover, the market investigation suggests that HAC, MAC and LAC each have different chemical properties and end-usage; HAC being primarily used in refractory applications while the lower alumina cements are primarily used for instance in building chemistry, although the division is not completely exclusive. With regard to refractory applications in particular, HAC appears not to be substitutable with lower alumina cements as HAC has higher refractoriness and superior performace. The price of HAC is also higher than the price of lower alumina cements.

(17) As to the different end-uses of refractories, a number of refractory customers indicated in the market investigation that they may not be directly able to use CAC sold for other applications in their production of refractories. Overall, the replies suggest that the market is likely at least differentiated between the different end-uses.

(18) Therefore, taking into account the outcome of the market investigation and all evidence available to it, the Commission considers that, for the purposes of this decision, CAC forms a separate product market from other binders. Furthermore, HAC forms a separate product market from CAC with medium and low alumina content (MAC and LAC). However, whether the markets for CAC should be further delineated between different end-uses can be left open as the outcome of the competitive assessment would remain the same under those alternative product market definitions.

4.2.2. Acid monolithic refractories

(19) Refractories are inorganic nonmetallic materials that can withstand high temperatures without undergoing physical or chemical changes. Refractories are produced by mixing of aggregates (including high alumina silicates) with chemical or hydraulic binders. They are primarily employed as heat buffers or linings in industrial devices such as furnaces, kilns and ovens.

(20) The Commission has previously considered that refractories can be segmented according to their chemical composition and physical form into (i) basic and non- basic (acid) refractories and (ii) shaped and unshaped (monolithic) refractories. (9)

(21) The Notifying Party agrees with these distinctions and submits that the proposed Transaction would only give rise to affected markets with regard to acid monolithic refractories, because CAC is used as an input material almost exclusively for the production of acid monolithic refractories, where Imerys is active.

(22) The Notifying Party further submits that acid monolithic refractories containing CAC may, in limited situations, be substitutable with acid monolithic refractories containing other binders from the demand-side. As to supply-side considerations, the Notifying Party acknowledges that substitution is only possible with regard to acid monolithic refractories containing certain other binders.

(23) However, the market investigation indicates that, from a demand-side perspective, acid monolithic refractories containing CAC cannot be replaced by those that do not contain CAC.

(24) However, for the purpose of this decision, whether the markets for acid monolithic refractories should be further delineated between those that contain CAC and those that do not contain CAC can be left open as the outcome of the competitive assessment remains the same under those alternative product market definitions.

4.2.3. Industrial minerals

(25) Imerys is active in the supply of various industrial minerals that can be used in the production of acid monolithic refractories and/or building chemistry applications, for instance andalusite, mullite and chamottes. In the production of acid monolithic refractories, these minerals are used either as aggregates or additives and they are mixed with HAC that acts as a binder.

(26) In its past practice, the Commission has generally treated each industrial mineral as a separate product market. (10)

(27) The Notifying Party submits that, from a demand-side perspective, alumina- containing minerals could be characterised by their alumina content and that minerals with a similar alumina content are substitutable.

(28) The results of the market investigation do not support the Notifying Party’s submission about interchangeability between minerals containing the same level of alumina.

(29) However, for the purpose of this decision, the exact product market definition of industrial minerals used as aggregates or additives in the production of acid monolithic refractories can be left open as the outcome of the competitive assessment would remain the same under any plausible alternative product market definition.

4.3. Relevant geographic market

4.3.1. Calcium Aluminate Cement

(30) The Commission has previously considered that the geographic markets for various industrial minerals are EEA-wide or worldwide. (11)

(31) The Notifying Party submits that the relevant geographic markets for CACs are at least EEA-wide if not worldwide in scope. The Notifying Party supports its submission by referring to the existence of global trade patterns for CAC, the low levels of import duties (up to 1.7%), the absence of export duties, the high value per tonne of the product and relatively low transport cost ratio.

(32) However, the Commission's market investigation shows that non-EEA suppliers do not play a significant role in the EEA. (12) Moreover and with respect to HAC, an overwhelming majority of customers only considered suppliers from the EEA as a viable source of HAC for their operations in the EEA, due to in particular transport costs, reliability and lead times. According to customers, the significantly longer lead times from outside the EEA may also negatively affect the quality of HAC. The insignificance of CAC imports in the EEA is a strong indication that CAC volumes produced outside of the EEA do not compete with CAC volumes produced in the EEA for purchase volumes of EEA customers.

(33) Therefore, taking into account the results of the market investigation and all evidence available to it, the Commission considers that the relevant geographic market for CACs is EEA-wide in scope.

4.3.2. Acid monolithic refractories

(34) The Commission has previously considered the relevant geographic market of acid monolithic refractories to be EEA-wide in scope. (13)

(35) The Notifying Party agrees with the Commission’s previous practice.

(36) The Commission's market investigation has not revealed any significant evidence that would contradict its previous finding of an EEA-wide market for acid monolithic refractories.

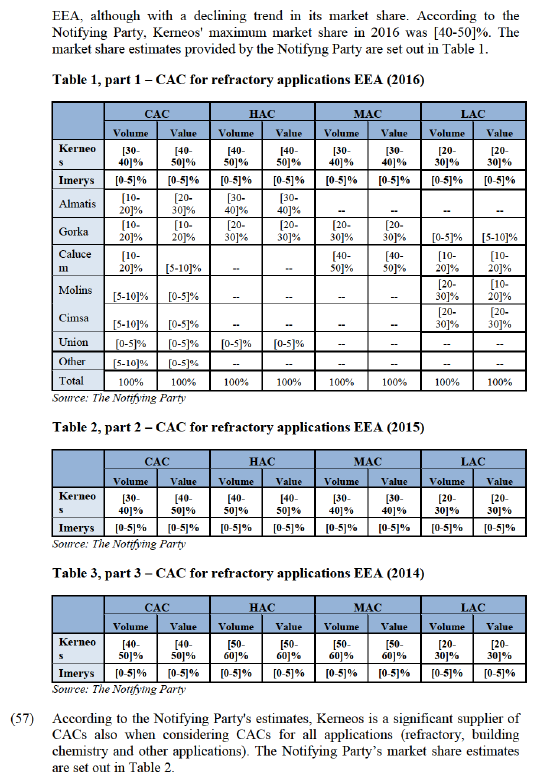

4.3.3. Industrial minerals

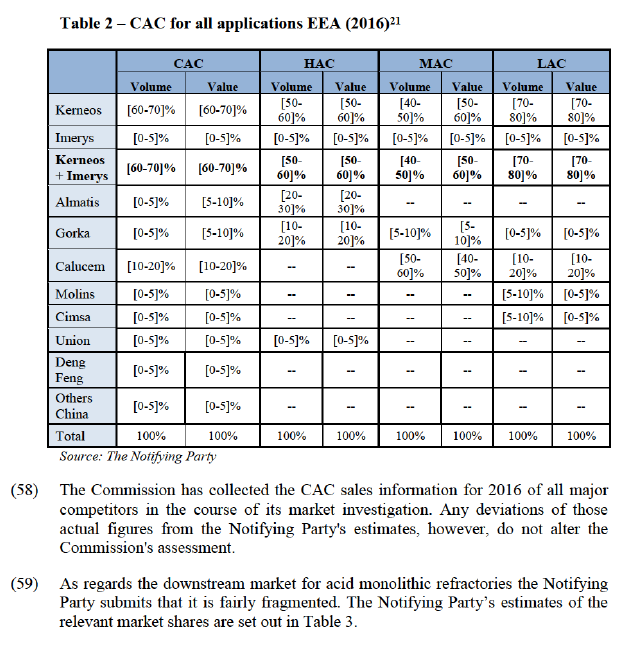

(37) The Commission has previously considered that the geographic markets for various industrial minerals are EEA-wide or worldwide. (14)

(38) The Notifying Party submits that the relevant geographic market for industrial minerals is either worldwide or at least EEA-wide in scope. It supports its submission by referring to, for instance the existence of significant suppliers located all over the world, the ease of transport and significant trade flows.

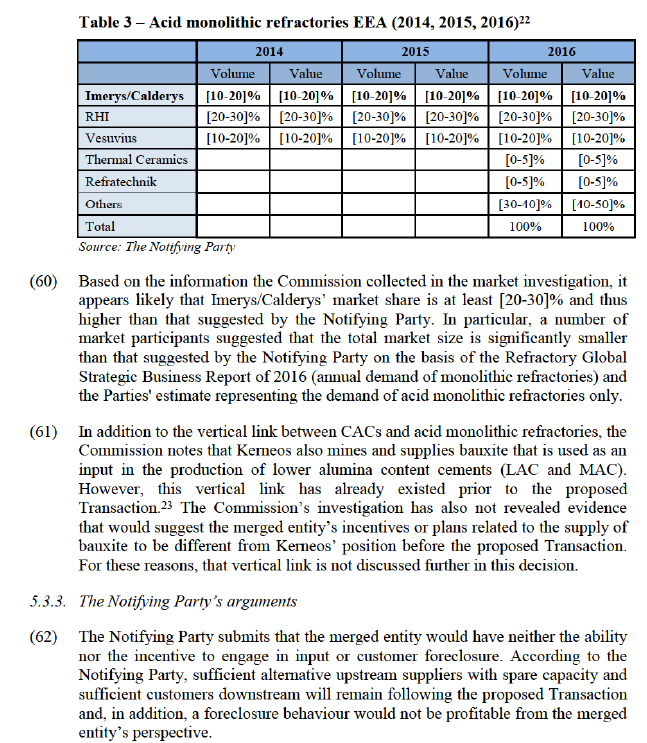

(39) Customers of industrial minerals indicated in the Commission’s market investigation that most of the minerals can be sourced globally.

(40) However, for the purpose of this decision, the exact geographic market definition for industrial minerals can be left open as the outcome of the competitive assessment would remain the same under any plausible alternative geographic market definition

5. COMPETITIVE ASSESSMENT

5.1. Introduction

(41) Under Article 2(2) and (3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(42) In this respect, a merger may entail horizontal and/or non-horizontal effects.

5.2. Horizontal assessment

5.2.1. Analytical framework

(43) As regards horizontal effects, the Commission guidelines on the assessment of horizontal mergers under the Merger Regulation (the ‘Horizontal Merger Guidelines’) (15) distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects. Non-coordinated effects may significantly impede competition by eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour. In that regard, the Horizontal Merger Guidelines consider not only the direct loss of competition between the merging firms, but also the reduction in competitive pressure on non-merging firms in the same market that could be brought about by the merger.

(44) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that a merger would eliminate an important competitive force. That list of factors applies equally if a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects.

(45) This decision will analyse whether the proposed Transaction is likely to raise doubts as to its compatibility with the internal market by the creation on non- coordinated effects in those markets on which the Parties' activities lead to horizontal overlaps.

5.2.2. The Commission’s assessment

(46) Both Kerneos and Imerys (through its subsidiary ACE Calderys in India) produce and sell CAC. However, while Kerneos is the market leader at EEA and global level, Imerys/ACE Calderys sells [most] of its CAC in-house and the [rest] exclusively in India. Imerys sells no CAC to third parties in the EEA.

(47) The Commission’s investigation has also not revealed any plans or attempts by Imerys to enter the EEA-market with CAC prior to the proposed Transaction.

(48) In addition, none of the market participants contacted in the market investigation raised concerns with respect to the horizontal overlap between the Parties' production of CAC.

(49) In light of the results of the market investigation and the evidence available to it, the Commission considers that the proposed Transaction does not raise any concerns as to its compatibility with internal market with respect to the Parties’ overlaps in the production and sale of CACs

5.3. Vertical assessment

5.3.1. Analytical framework

(50) A vertical merger may result in anti-competitive effects due to foreclosure. Foreclosure concerns a situation where actual or potential rivals' access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing these companies' ability and/or incentive to compete. (16)

(51) Two forms of foreclosure can be distinguished in a vertical relationship: input and customer foreclosure. The first is where the merger is likely to raise the costs of downstream rivals by restricting their access to an important input (input foreclosure). The second is where the merger is likely to foreclose upstream rivals by restricting their access to a sufficient customer base (customer foreclosure). (17)

(52) Input foreclosure arises where, post-merger, the new entity would be likely to restrict access to the products or services that it would have otherwise supplied absent the merger, thereby raising its downstream rivals' costs by making it harder for them to obtain supplies of the input under similar prices and conditions as absent the merger. (18)

(53) Customer foreclosure may occur when a supplier integrates with an important customer in the downstream market. Because of this downstream presence, the merged entity may foreclose access to a sufficient customer base to its actual or potential rivals in the upstream market (the input market) and reduce their ability or incentive to compete. In turn, this may raise downstream rivals' costs by making it harder for them to obtain supplies of the input under similar prices and conditions as absent the merger. (19)

(54) For an input or customer foreclosure scenario to raise competition concerns, three cumulative factors need to be taken into account: (i) the ability of the merged entity to engage in foreclosure; (ii) the incentives of the merged entity to do so; and (iii) whether a foreclosure strategy would have a significant detrimental effect on competition in the downstream market. (20)

5.3.2. Afftected markets and market structure

(55) The Transaction gives rise to vertically affected markets in the EEA due to (i) Kerneos' upstream supply of CACs and (ii) Imerys’ downstream supply of acid monolithic refractories through its subsidiary Calderys.

(56) As regards the supply of CAC and its potential subsegments for refractory applications, the Notifying Party submits that Kerneos is the market leader in the

5.3.4. The Commission’s assessment: input foreclosure

5.3.4.1. Ability to foreclose access to inputs

(63) The Notifying Party submits that HAC is significantly more relevant for the production of acid monolithic refractories than the lower alumina content cements MAC and LAC. The Commission's market investigation has confirmed the Notifying Party’s submissions about the importance of HAC in the production of acid monolithic refractories. The concerns expressed by market participants primarily referred to HAC and not to lower alumina content cements or any overall CAC market. The Commission also recalls that, based on the replies of customers in the market investigation, the CAC (including HAC) markets appear at least differentiated based on the end-use of CAC as set out in paragraph (17).

(64) Consequently, the Commission has given emphasis in its investigation particularly to the market position the merged entity will achieve in HAC for refractories. In its assessment, the Commission has examined, among others, whether Imerys’ downstream rivals would be able to turn to alternative suppliers and whether those suppliers have adequate capacity to meet increases in demand.

(65) The merged entity would achieve a significant market share in the supply of HAC for refractory applications ([40-50]% by volume; [40-50]% by value). The Parties’ combined market shares in lower alumina content cements for refractories as well as in the potential overall CAC for refractories market are lower ([30-40]% by volume and [30-40]% by value for MAC, [20-30]% by volume and [20-30]% by value for LAC, and [30-40]% by volume and [40-50]% by value in overall CAC)

(66) Should an overall market for CAC (and for its sub-types HAC, MAC and LAC) for all applications be considered, the merged entity’s market shares would be higher. That is primarily due to Kerneos’ sales to building chemistry applications, where Kerneos is particularly strong when it comes to the lower alumina cements.

(67) There would be two main remaining competitors in the supply of HAC for refractories in the EEA after the Transaction: Almatis ([30-40]% market share by volume and value) and Gorka ([20-30]% market share by volume and value). In the supply of MAC for refractories the number of alternative suppliers is the same, according to the Notifying Party's estimates, while for LAC there are more numerous suppliers.

(68) The Commission’s market investigation has confirmed that CAC suppliers have significant idle capacity for the production of CACs, including HAC. This includes suppliers that are already supplying the refractory industry. In addition, if the merged entity were to divert its third party HAC supplies to own internal use after the Transaction– which is likely considering the Parties' submission and information contained in the the Notifying Party's internal documents – the spare capacity of its upstream competitors would increase correspondingly.

(69) In the light of the results of the market investigation and all evidence available to it, the Commission considers that the competitors could likely meet even significantly increased demand if customers wished to divert from the merged entity. Any foreclosure attempt by the merged entity, for example through substantial price increases, would therefore likely lead customers to switching to one of Kerneos' competitors.

(70) As regards customers' ability to switch to those suppliers, some market participants indicated in the market investigation that HAC sourced from a particular supplier cannot necessarily be automatically replaced by HAC from another supplier but that testing, and potentially some production changes, may be needed. Nonetheless, a significant share of Kerneos’ customers indicated that they either have already approved another supplier or that they could do so if need be. Moreover, although there were some indications from market participants that Kerneos’ quality of HAC is superior, at least Almatis was mentioned to be on par with Kerneos' HAC. As to another competitor, Gorka, market participants noted that it has recently introduced new products to address the gaps in its previous product portfolio.

(71) Some market participants were concerned about the merged entity being able to increase prices of HAC to them, or to offer HAC with lower prices to Imerys’ acid monolithic refractory subsidiary Calderys after the Transaction with adverse effect on their ability to compete with Calderys in acid monolithic refractories. Any such concerns were in general limited to HAC and not expressed for the lower alumina content cements. However, such concerns about HAC were not shared by all market participants. In addition, a number of market participants, including both customers with a large and small presence in acid monolithic refractories, indicated that they could either switch suppliers (24) or that they were otherwise not concerned.

(72) Moreover, Imerys' internal documents at the disposal of the Commission do not indicate that the parties have planned a post-Transaction input foreclosure strategy.

(73) In conclusion, in light of the results of the market investigation and the evidence available to it, the Commission considers that the merged entity would likely not have the ability to engage in input foreclosure after the proposed Transaction.

5.3.4.2. Incentive to foreclose acces to inputs

(74) The Notifying Party submits that the merged entity would not have the incentive to engage in input foreclosure as such a strategy would not be profitable because (i) upstream losses would be substantial given Kerneos' important upstream position, (ii) downstream gains would be limited as HAC only represent 5% of the total costs of monolithic products, (iii) margins and profit upstream are higher than downstream, and (iv) Calderys' downstream position is not sufficiently strong.

(75) As regards upstream and downstream margins, in relative terms, the upstream input HAC indeed generates higher margins than the downstream product, acid monolithic refractories. However, in absolute terms, the margins generated downstream are higher.

(76) As regards HAC input costs, the market investigation indicates that the cost represented by HAC in the price of acid monolithic refractories, is indeed moderate (less than or equal to 10%). In order to cause meaningful competitive harm on the downstream market, upstream prices would need to increase substantially. For instance, in order for Kerneos to impose an input price increase on producers of acid monolithic refractories that would correspond to a range between 2.5% and 5.0% of the downstream price, Kerneos would have to increase the price of HAC by up to 50% after the proposed Transaction. This does not appear to be the most likely scenario. While there is some product differentiation between different suppliers of HAC for certain uses, and hence substitutability is not perfect for all uses, customers can and do switch between upstream suppliers and have done so in the past. Moreover, a price increase of this order of magnitude is likely to make it profitable for customers to qualify additional suppliers and for competitors to work with customers to provide the desired specifications of HAC. Furthermore, competitors could potentially consider expanding capacities where necessary in the case of such price increase.

(77) As regards effects on downstream competitors, most large producers of acid monolithic refractories, i.e. Calderys' competitors, indicated in the market investigation that it is unlikely that they would be affected by the proposed Transaction as they could source HAC from competitors and qualify additional alternative suppliers if required. Since the main potential targets of a putative foreclosure strategy (Calderys' large refractories competitors) are not concerned of an input foreclosure strategy, critical effects for the competitiveness of the downstream market as such are less likely to arise. Moreover, many market participants point out that the share of HAC as an input cost is not decisive as a component of the overall production cost, and thus subsequently the price of acid monolithic refractories.

(78) In addition, prior to the proposed Transaction, the Notifying Party has already controlled a number of other critical inputs that are necessary for the production of acid monolithic refractories. Imerys' market shares with respect to some of these inputs are even higher than those that the merged entity would achieve in CAC, or HAC, after the Transaction (see paragraph (91)). Despite such high market shares, the market investigation confirms that, in the past, Imerys has not engaged in foreclosing behaviour with regard to Calderys' competitors on the acid monolithic refractories market, irrespective of the size of the competitor.

(79) Therefore, in light of the results of the market investigation and the evidence available to it, the Commission considers that even if the merged entity had the ability to foreclose input, it is unlikely that it would have sufficient incentive to do so.

5.3.4.3. Conclusion on input foreclosure

(80) On the basis of the arguments set out in paragraphs (63) to (79) and in light of the results of the maket investigation and the evidence available to it,the Commission concludes that the proposed Transaction would not give rise to competition concerns related to input foreclosure of CAC, and in particular of HAC, due to lack of sufficient ability and incentives to engage in such foreclosure strategy.

5.3.5. The Commission’s assessment: customer foreclosure

(81) The Notifying Party has submitted that Imerys/Calderys’ share of purchasing of the various qualities of CAC for refractory applications in the EEA in 2016 was [10-20]% for LAC, [10-20]% for MAC and [10-20]% for HAC.

(82) As discussed in paragraph (60), the Commission considers that Imerys/Calderys’ market share in the downstream markets for acid monolithic refractories is likely higher than the share suggested by the Notifying Party. Nonetheless, the market investigation has not revealed evidence that would suggest Imerys/Calderys to be a particularly significant purchaser of CAC from third parties.

(83) Imerys’ role as a purchaser of CAC is limited by the fact that it sources part of its needs captively from its Indian operations. In addition, it sources a significant share of its needs from Kerneos already prior to the Transaction. With regard to HAC, the type of CAC most commonly used in refractory production, Imerys sourced approximately half ([…]%) of its needs in the EEA from Kerneos in 2016 and a significant volume captively ([…]%).

(84) Thus, the Commission considers that the merged entity would not have the ability to engage in customer foreclosure.

(85) The results of the market investigation support the absence of customer foreclosure concerns as upstream CAC competitors consider that a sufficiently large customer base will remain available after the Transaction.

(86) Therefore, in light of the results of the market investigation and the evidence available to it, the Commission concludes that the proposed Transaction would not give rise to competition concerns related to customer foreclosure for CAC.

5.3.6. Conclusion on vertical effects

(87) In light of the considerations in Sections 5.3.4 and 5.3.5, the Commission concludes that the Transaction does not give rise to serious doubts about its compatibility with the internal market due to input or customer foreclosure as regards the CAC and acid monolithic refractories markets.

5.4. Conglomerate assessment

5.4.1. Analytical framework

(88) According to the Non-Horizontal Merger Guidelines, in most circumstances, conglomerate mergers do not lead to any competition problems. (25)

(89) However, foreclosure effects may arise when the combination of products in related markets may confer on the merged entity the ability and incentive to leverage a strong market position from one market to another closely related market by means of tying or bundling or other exclusionary practices. The Non- Horizontal Merger Guidelines distinguish between bundling, which usually refers to the way products are offered and priced by the merged entity (26) and tying, usually referring to situations where customers that purchase one good (the tying good) are required to also purchase another good from the producer (the tied good). Tying can take place on a technical or contractual basis. For instance, technical tying occurs when the tying product is designed in such a way that it only works with the tied product (and not with the alternatives offered by competitors). While tying and bundling have often no anticompetitive consequences, in certain circumstances such practices may lead to a reduction in actual or potential competitors' ability or incentive to compete. This may reduce the competitive pressure on the merged entity allowing it to increase prices. (27)

(90) In assessing the likelihood of such a scenario, the Commission examines, first, whether the merged firm would have the ability to foreclose its rivals, (28) second, whether it would have the economic incentive to do so (29) and, third, whether a foreclosure strategy would have a significant detrimental effect on competition, thus causing harm to consumers. (30) In practice, these factors are often examined together as they are closely intertwined.

5.4.2. Industrial minerals for refractories

(91) While Kerneos is the leading CAC supplier, Imerys is already active in a number of industrial minerals used in the production of refractories, including those used in the production of acid monolithic refractories and therefore purchased by the same set of customers. According to the Notifying Party, its market shares in those minerals are notable in the EEA, the highest market share being achieved in mullite ([70-80]%), andalusite ([60-70]%) and chamottes ([40-50]%). At the global level, only the market market share in andalusite ([60-70]%) is above 20%.

(92) In the market investigation, a minority of market participants expressed concerns related to the fact that Imerys would add a further industrial mineral to its portfolio of minerals that can be used in the production of refractories, and in particular in acid monolithic refractories. However, the view was not shared by the majority of market participants who were not concerned about the addition of another industrial mineral to Imerys' portolio. Market participants also indicated that they negotiate sourcing of each mineral separately and Imerys' portfolio still lacks a number of important minerals.

(93) The Commission's market investigation has not revealed any significant existing bundling strategies in the markets. Market participants confirmed that Imerys has not engaged in bundling practices in the past, irrespective of the size of the customer and downstream rival, despite already having a broad portfolio of industrial minerals. Market participants also indicated that at least Almatis is able to supply a wide portfolio of industrial minerals as well.

(94) Therefore, in light of the results of the market investigation and the evidence available to it, the Commission concludes that the proposed Transaction would not give rise to competition concerns with respect to potential conglomerate effects in the market for industrial minerals for refractories.

5.4.3. Industrial minerals for building chemistry

(95) According to the Notifying Party, the merged entity would achieve a market share of approximately [60-70]% in CACs for building chemistry applications in the EEA and [20-30]% globally.

(96) Prior to the Transaction, Imerys has already been supplying some industrial minerals for building chemistry. However, according to the Notifying Party, its market shares are negligible in all minerals (at most [0-5]%) except for bentonite where its market share could amount to [20-30]% in the EEA and to [0-5]% globally.

(97) The Commission notes that, due to the rather limited portfolio of industrial minerals that Imerys currently offers to building chemistry customers and the low market shares of Imerys in the supply of minerals for building chemistry, conglomerate effects are unlikely.

(98) The market investigation has not revealed any substantiated competition concerns related to conglomerate effects in industrial minerals for building chemistry.

(99) Therefore, in light of the results of the market investigation and the evidence available to it, the Commission concludes that the Transaction would not give rise to competition concerns with respect to potential conglomerate effects in the markets for industrial minerals and CAC for building chemistry.

5.4.4. Conclusion on conglomerate effects

(100) In light of the considerations in paragraphs (91) to (99), the Commission concludes that the proposed Transaction would not give rise to serious doubts about its compatibility with the internal market due to conglomerate effects.

6. CONCLUSION

(101) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the ‘Merger Regulation’). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (‘TFEU’) has introduced certain changes, such as the replacement of ‘Community’ by ‘Union’ and ‘common market’ by ‘internal market’. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the ‘EEA Agreement’).

3 Publication in the Official Journal of the European Union No C 157, 19.05.2017, p. 20.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 BxC is primarily produced and used outside of the EEA and its importance in Europe is limited. According to the Notifying Party, the Parties’ combined market share in BxC in the EEA is at most 9%. BxC is therefore not discussed further in this decision.

6 60% alumina content CACs are not common and, for instance, Kerneos does not produce any.

7 M.4157 – Wendel Investissement/Groupe Materis, paragraphs 24-25.

8 M.619 – Gencor/Lonrho, paragraph 23; M.774 – Saint-Gobain/Wacker-Chemie/NOM, paragraph 41; M.1381 – Imetal/English China Clays; M.1693 – Alcoa/Reynolds, paragraphs 9-11; M.3796 – Omya/Huber PCC, paragraph 235; M.4827 – Rio Tinto/Alcan, paragraph 17; M.6189 – Imerys/Rio Tinto Talc Business, paragraph 24; M.7456 – Imerys/S&B Minerals, paragraph 11. Similarly in the not yet published M.8130 – Imerys/Alteo certain assets.

9 M.4961 – Cookson/Foseco, paragraphs 10–17. Similarly in the not yet published M.8130 – Imerys/Alteo certain assets.

10 M.1381 – Imetal/English China Clays, paragraph 34; Similarly in the not yet published M.8130 –Imerys/Alteo certain assets.

11 Cases M.774 – Saint-Gobain/Wacker-Chemie/NOM (for silicon carbide) paragraph 109; M.1381 – Imetal/English China Clays (for kaolin, fused silica, high value refractory clays, paragraphs 48, 52, 56; M.1693 – Alcoa/Reynolds, paragraph 18; M.4441 – EN+/Glencore/Sual/UC Rusal, paragraphs 20, 22; M.4827 – Rio Tinto/Alcan, paragraph 19; M.6189 – Imerys/Rio Tinto Talc Business, paragraph 32; M.7456 – Imerys/S&B Minerals, paragraph 30; Similarly in the not yet published M.8130 – Imerys Alteo certain assets.

12 For instance, the level of imports of HAC for refractory applications appears to be below 10%.

13 M.4961 – Cookson/Foseco, paragraphs 27-30; M.472 – Vesuvius/Wuelfrath, paragraphs 22 – 24, Similarly in the not yet published M.8130 – Imerys Alteo certain assets.

14 Cases M.774 – Saint-Gobain/Wacker-Chemie/NOM (for silicon carbide) paragraph 109; M.1381 – Imetal/English China Clays (for kaolin, for fused silica for high value refractory clays, paragraphs 48, 52, 56; M.1693 – Alcoa/Reynolds, paragraph 18; M.4441 – EN+/Glencore/Sual/UC Rusal, paragraphs 20, 22; M.4827 – Rio Tinto/Alcan, paragraph 19; M.6189 – Imerys/Rio Tinto Talc Business, paragraph 32; M.7456 – Imerys/S&B Minerals, paragraph 30; Similarly in the not yet published M.8130 – Imerys/Alteo certain assets.

15 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 31, 5.2.2004, p. 5.

16 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 265, 18.10.2008, p. 6 (‘Non-Horizontal Guidelines’), paragraphs 29–30.

17 Non-Horizontal Guidelines, paragraphs 29–30.

18 Non-Horizontal Guidelines, paragraph 31.

19 Non-Horizontal Guidelines, paragraph 58.

20 Non-Horizontal Guidelines, paragraphs 32, 59.

21 The Notifying Party submits that Kerneos’ market shares have been roughly similar through 2014-2016.

22 The market shares only include acid monolithic refractories that contain CAC. The Notifying Party has submitted that it only produces limited volumes of other kinds of acid monolithic refractories and has confirmed that its market share would not be materially higher if considering an overall acid monolithic market.

23 Imerys has also previously had a mine in Southern Europe that used to produce bauxite suitable for CAC production. However, Imerys has confirmed that the mine has been closed as itw as nbot profitable and that Imerys has already also lost the mining rights related to the site.

24 Customers replying to the market investigation in general expressed that they would not prefer to change their HAC supplier. However, the majority of the respondents that produce acid monolithic refractories indicated that there are alternative suppliers they could turn to in case of a price increase imposed by Kerneos.

25 Non-Horizontal Guidelines, paragraph 92.

26 Within bundling practices, the distinction is also made between pure bundling and mixed bundling. In the case of pure bundling the products are only sold jointly in fixed proportions. With mixed bundling the products are also available separately, but the sum of the stand-alone prices is higher than the bundled price.

27 Non-Horizontal Guidelines, paragraphs 91, 93.

28 Non-Horizontal Guidelines, paragraphs 95-104.

29 Non-Horizontal Guidelines, paragraphs 105-110.

30 Non-Horizontal Guidelines, paragraphs 111-118.