Commission, February 27, 2017, No M.8315

EUROPEAN COMMISSION

Judgment

SIEMENS/ MENTOR GRAPHICS

Subject: Case M.8315 - SIEMENS / MENTOR GRAPHICS

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/2004 (1) and Article 57 of the Agreement on the European Economic Area (2)

Dear Sir or Madam,

(1) On 23 January 2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Siemens AG ("Siemens", Germany) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of Mentor Graphics Corporation ("Mentor", United States) by way of purchase of shares (the "Proposed Transaction"). Siemens is referred to as the "Notifying Party" and Siemens and Mentor are collectively referred to as the "Parties".

1. THE PARTIES

(2) Siemens is a German stock corporation headquartered in […] Munich, focusing on electrification, automation and digitalisation. Through its business division Digital Factory, Siemens offers a comprehensive portfolio of seamlessly integrated hardware, software and technology-based services in order to support manufacturing companies worldwide in enhancing the flexibility and efficiency of their manufacturing processes and reducing the time to market of their products. Product Lifecycle Management ("PLM") software, for example, allows companies to develop and optimize new products (from product design and simulation, to manufacturing and maintenance service) on an entirely virtual basis.

(3) Mentor is a publicly held company headquartered in Wilsonville, Oregon, US. It is active in the PLM business and provides electronic hardware and software design solutions, i.e. software, consulting services to support electronic, semiconductor and systems companies.

2. THE OPERATION

(4) The Proposed Transaction consists in the acquisition of sole control by Siemens over Mentor. Pursuant to the Merger Agreement entered into between the Parties and dated 12 November 2016, Siemens Industry, Inc. (US), a Siemens US subsidiary will acquire 100% ownership of Mentor through a merger of a transaction vehicle wholly-owned by Siemens Industry, Inc with Mentor. As a result, all outstanding shares of stock in Mentor will be cancelled, and will be converted into a right to receive merger consideration from Siemens by Mentor's shareholders. The Proposed Transaction will result in Siemens holding 100% of the shares in Mentor and acquiring sole control.

(5) Therefore, the Proposed Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

3. EU DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 2 500 million (3) (Siemens: EUR 79 644 million; Mentor: EUR 1 071 million) and a combined aggregate turnover of more than EUR 100 million in three Member states, namely France (Siemens: EUR […]; Mentor: EUR […]), Germany (Siemens: EUR […] million, Mentor: EUR […]) and the United Kingdom (Siemens: EUR […], Mentor: EUR […]). In each of these three Member States, the aggregate turnover of each of Siemens and Mentor is more than EUR 25 million. Finally, each of them has an aggregate Community-wide turnover in excess of EUR 100 million (Siemens: EUR […]; Mentor: EUR […]), but neither of them achieves more than two-thirds of its aggregate Community- wide turnover within one and the same Member State.

(7) The Proposed Transaction therefore has an EU dimension pursuant to Article 1(3) of the Merger Regulation.

4. RELEVANT MARKETS

(8) The Proposed Transaction concerns the market for the supply of PLM software services. PLM software covers the supply of a wide range of software products and solutions that allow a business to digitally, efficiently and cost-effectively manage information throughout the entire lifecycle of a product. PLM software creates a virtual world for the design, simulation, testing, manufacturing and production of a product and the management of the resulting data at each step of the process.

4.1. Relevant product markets

4.1.1. Introduction

(9) In previous merger decisions (4) the Commission left the product market definition for PLM software supplies open but indicated that: (i) PLM software is a distinct market within the overall category of Enterprise Application Software ("EAS"); and (ii) it may be appropriate to segment the broader PLM market into specific market segments for individual applications, in particular:

· Digital Product Development ("DPD") which comprises:

o Computer-Aided Design ("CAD");

o Computer-Aided Engineering ("CAE"); and

o Computer-Aided Manufacturing ("CAM");

· Digital Manufacturing ("DM"); and

· Product Data Management ("PDM").

(10) The Commission's previous decisions considered that PLM software included only the supply of software for the design of mechanical products. Since then, the PLM industry has developed considerably, for example to include software for the design of electronics and embedded software. (5) Against this background, it seems appropriate to consider a sub-division of the overall PLM software activities into the following categories:

Software for the design and verification of products:

· Mechanical PLM ("MPLM") (including certain computational fluid dynamics ("CFD") software related to MPLM, referred to as MPLM CFD);

· Electronic Design Automation ("EDA") (including certain related CFD software, referred to as EDA CFD);

· Architecture, Engineering and Construction ("AEC");

· Embedded Software Engineering ("ESE");

· Application Lifecycle Management ("ALM");

Software for the design of the manufacturing process:

· Digital Manufacturing ("DM");

Software for the execution of the manufacturing process:

· Manufacturing Execution Systems ("MES"); and

Software related to the entire PLM process:

· Collaborative Product Data Management ("CPDM").

(11) The results of the market investigation show indeed that both customers (6) and competitors (7) consider these segments of supply software products as complementary rather than substitutable to each other since they support different business processes, provide different functionalities and satisfy different customer needs. One customer notes that each software product focuses on a different aspect of the product manufacturing process. MPLM tracks use of tangible, mechanical parts; EDA is used to design electrical parts like integrated circuit boards; ESE allows companies to manage what firmware they burn onto ICs used on circuit boards; DM manages bills of material and assembly planning while MES manages production execution. (8)

(12) The market investigation provides inconclusive responses as to whether the two markets for the supply of high end and low end PLM software should be considered separate. (9) While in relation to potential segmentation by industry, most of the respondents indicate that PLM software products for different industries could be considered as substitutes or alternatives due to their similar functionalities and technical requirements. (10)

(13) While the market investigation indicates that MPLM, EDA, AEC, ESE, ALM, DM, MES and CPDM may constitute separate product markets, for the purpose of this decision, the exact product market definition can be left open, since the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definitions for the development and supply of the said products.

4.1.2. MPLM

(14) MPLM is the category within the overall PLM industry that supplies software for the digital design, simulation and testing and manufacture of mechanical products. Mechanical design software differs from software for the design of electronic components because of the different component types’ characteristics, in particular size. Subject to the limited exception of CFD software, software used for MPLM purposes is not suitable for EDA purposes or vice versa.

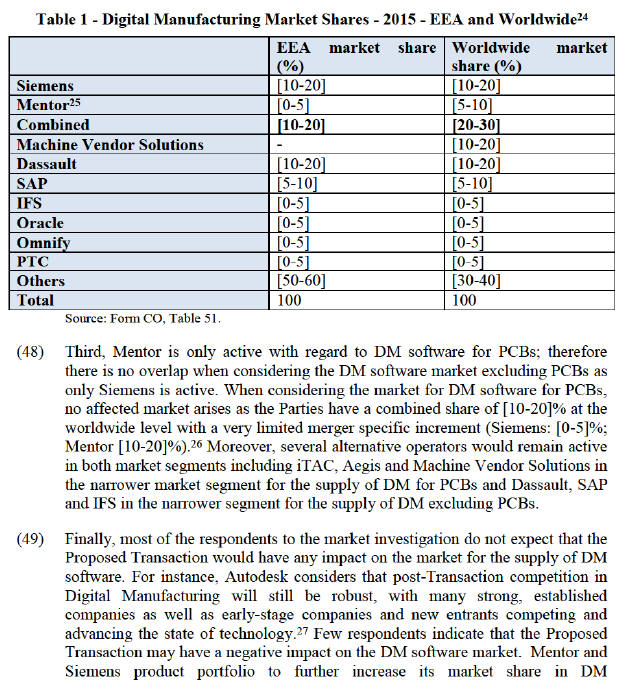

(15) For the purpose of this decision, the exact product market definition can be left open, since the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition for the supply of MPLM software.

4.1.3. EDA

(16) EDA software is used for the design, verification and physical implementation of electronic systems and electronic components (including sensors, displays, wire harnesses, and integrated circuits ("ICs"), and printed circuit boards ("PCBs")).

(17) EDA could be further segmented by software for: (i) PCBs; (ii) ICs and (iii) CAE; as customer demand is different in each segment and different technologies and expertise are involved. For example, PCB are designed, verified and physically implemented with a set of EDA tools specifically designed for those PCB related design tasks.

(18) In response to the market investigation, a majority of customers consider EDA software for PCBs, ICs and CAE as complimentary and not alternatives to each other. In particular, one respondent highlights that EDA software for PCBs, ICs and CAE have different functions. IC software helps managing the design and manufacturing process governing a specific integrated circuit, which is often a component of a larger PCB. PCB software helps managing the design and manufacture of the PCB as a whole, which may have several ICs. CAE software is used by manufacturers to analyse and test the functionality of the finished PCB, incorporating any relevant ICs. (11) Most of the competitors responding to the market investigation also consider those software products as mainly complementary. Only one competitor considers the software products as potentially alternatives, and notes that investment in both time and capital can be significant. (12)

(19) The market investigation further indicates that CAE software solutions include the complementary products CFD and Finite Element Analysis ("FEA") software. (13)

(20) For the purpose of this decision, the exact product market definition can be left open, since the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition for the supply of EDA software.

4.1.4. CFD

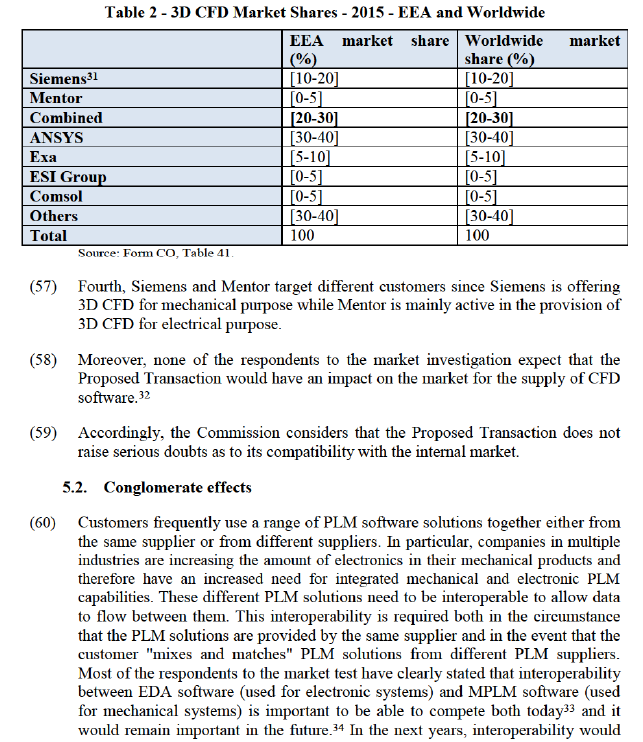

(21) CFD includes PLM software which helps end-users analyse the flow, turbulence and pressure distribution of liquids and gases and their interaction with objects in order to prevent errors before proceeding to production. CFD software is used either as part of MPLM or EDA.

(22) The Commission has previously considered that CFD could be further segmented by type: high-end vs low-end and/or by sub-application type: 1 dimensional ("1D") or 3 dimensional ("3D") applications (14) but ultimately left the market definition open.

(23) The Notifying Party submits that the product market definition can be left open, since no competition concerns arise under any potential market definition.

(24) Most of the respondents to the market investigation indicate that 1D and 3D CFD are mainly complementary and not alternative to each other. Customers may use both 1D and 3D CFD but at different stages of the design process and to solve different problems with different algorithms. In particular, 3D CFD is necessary when analysing fluid flows in more than one dimension. (15)

(25) For the purpose of this decision, the exact product market definition can be left open, since the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition for the supply of CFD software.

4.1.5. Overall MPLM and EDA software for CWH

(26) MPLM and EDA can be complementary products, for the supply of cable wire harness (“CWH”) applications. (16)

(27) The Notifying Party submits that it is not appropriate to look at a potential market comprising MPLM and EDA software for CWH applications since EDA CWH and MPLM CWH are mainly complementary and address different customers' needs.

(28) Respondents to the market investigation indicate that PLM software for CWH system applications are not substitutable with PLM software for non-CWH applications since the use cases are different and they serve different purposes. (17)

(29) The market investigation further indicates that there could be separate sub- segments for EDA CWH and MPLM CWH software given that the two tools are used together to complete the CWH design process. Despite interdependencies between the two types of software, they represent pretty unique functionalities since MPLM CWH software has a more material/assembly function while EDA CWH software is used for electrical definition. (18)

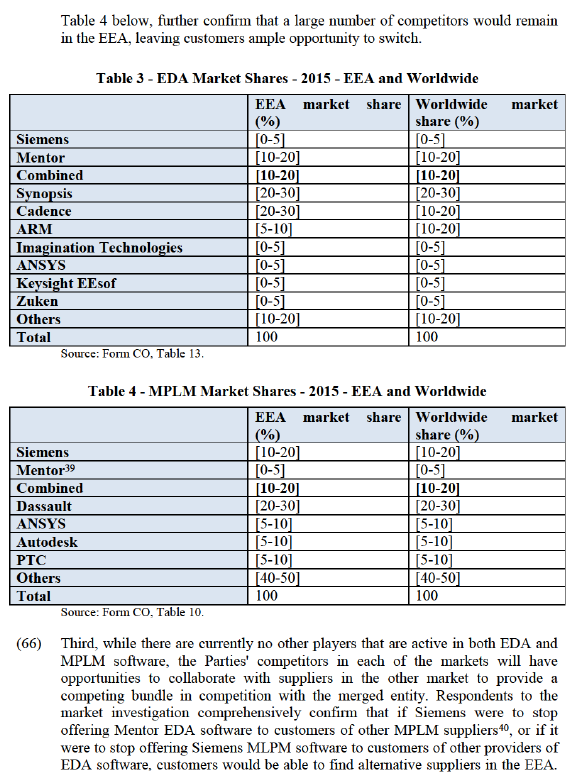

(30) For the purpose of this decision, the exact product market definition can be left open, since the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition for the supply of MPLM and EDA software for the supply of CWH applications.

4.1.6. DM

(31) DM software designs the manufacturing process. The use of these software tools allows manufacturing engineers to create the complete definition of the manufacturing process in a virtual environment, including tooling, assembly lines, work centres, facility layout, ergonomics and resources.

(32) The Notifying Party submits that within DM, a distinction should be made between: (i) DM for PCBs; and (ii) DM excluding PCBs; but that the product market definition can be left open, since no competition concerns arise under any potential market definition.

(33) For the purpose of this decision, the exact product market definition can be left open, since the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition for the supply of DM software.

4.1.7. CPDM

(34) CPDM is the use of software to manage product data and process-related information in a single, central system. At its core, a CPDM system provides solutions for secure data management, process enablement, and configuration management. CPDM can be divided into data management in relation to a particular domain (e.g. IC, PCB, or CWH) or across a whole company or factory floor based on data feeds from different domains (i.e. enterprise level). CPDM at an enterprise level can apply to both mechanical and electronic applications.

(35) For the purpose of this decision, the exact product market definition can be left open, since the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition for the supply of CPDM software.

4.2. Relevant geographic market

(36) In previous decisions (19) the Commission has considered that the geographic scope of the market for the supply of PLM software could be global or at least EEA wide but has ultimately left the definition open.

(37) The Notifying Party submits that the market for PLM software and any potential sub-categories are worldwide since the product, the suppliers and the large customers are the same throughout the world.

(38) The market investigation supports this argument with the vast majority of respondents replying that there are no significant differences in sourcing patterns or product requirements between the EEA and the rest of the world (20) and that they are equally able to procure/source PLM software in the EEA as in the rest of the world. (21)

(39) For the purpose of this decision, the exact geographic market definition can be left open, since the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition for the supply PLM software.

5. COMPETITIVE ASSESSMENT

(40) As noted above, Siemens and Mentor are both active in the provision of PLM software but are mainly focused in different sub-segments. While the Parties' activities overlap with regard to DM and CPDM products, as well as in the supply of (i) MPLM and EDA; (ii) MPLM CWH and EDA CWH; and (iii) MPLM CFD and EDA CFD, should these be considered together to be markets, the Proposed Transaction gives rise to only two horizontally affected markets:

a. Supply of software services for DM (section 5.1.1); and

b. Supply of software services for 3D CFD, a sub-segment of the MPLM CFD and EDA CFD segments (section 5.1.2).

(41) The Commission has also considered, in section 5.2 below, the question of whether the Proposed Transaction would raise conglomerate concerns as certain customers need both MPLM software (where Siemens is active) and EDA software (where Mentor is active) since a degree of interoperability is required between these two types of PLM software.

(42) Finally, the Proposed Transaction also gives rise to a vertically affected market with regard to EDA software for PCBs which is discussed in section 5.3 below.

5.1. Horizontal unilateral effects

5.1.1. DM

(43) Both Siemens and Mentor are active with regard to the supply of DM software.

(44) The Notifying Party submits that no competition concerns can be expected to arise in this market post-Transaction given that: (1) the Parties combined share is limited, with a small increment; (2) a large number of competitors would remain in the market, and in each of its sub-segments, leaving customers ample opportunity to switch; (3) the Parties' products do not compete as Siemens’ DM software is not considered by customers as a substitute for the Mentor suite of DM software for the electronics industry and that the market for DM software should in fact be segmented according to DM for PCBs and DM excluding PCBs; and (4) purchasers of DM software include large corporations which have strong buyer power and the ability to play suppliers off against each other.

(45) The Commission considers that for the reasons set out below, the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market with respect to DM software, regardless of any possible segmentation of the market for the supply of DM software.

(46) First, the Parties’ combined market share in 2015 is [20-30]% at worldwide and [10-20]% at EEA level and the increment brought by the Proposed Transaction, which corresponds to Mentor's market share, is approximately [5-10]% worldwide and only [0-5]% at EEA level. When responding to the market investigation, only one customer and no competitors consider Mentor to be a top 5 provider of DM software. (22)

(47) Second, there are a large number of competitors that will remain in the market post-Transaction including Machine Vendor Solutions, Dassault, and SAP. The market shares of the Parties and their competitors can be seen in Table 1. Most of the respondents to the market investigation consider that there will be a sufficient number of players remaining the market post-Transaction. (23)

manufacturing. (28) In this regard, the Commission notes that several alternative operators would remain active in the market. (29)

(50) Accordingly, the Commission considers that the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market.

5.1.2. 3D CFD

(51) Both Siemens and Mentor are active with regard to the supply of 3D CFD software. (30)

(52) The Notifying Party argues that no competition concerns can be expected to arise in this potential market post-merger for the following reasons: (1) the Parties have a low combined market share; (2) ANSYS will continue to be the leading supplier of 3D CFD software and a number of other players will also remain post- Transaction; and (3) the Parties are not close competitors for CFD.

(53) The Commission considers that for the reasons set out below, the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market with respect to 3D CFD software, regardless of any possible segmentation.

(54) First, the Parties do not have a significant share of the market. When considering all CFD software, the Parties have a combined market share in 2015 worldwide of [10-20]% (Siemens: [10-20]%; Mentor: [0-5]%) and in the EEA of [10-20]% (Siemens: [10-20]%; Mentor: [0-5]%). When considering the market for just 3D CFD software, the Parties have a combined market share in 2015 both worldwide and at EEA level of [20-30]% (Siemens: [10-20]%; Mentor: [0-5]%).

(55) Second, the Parties have a combined market share of [20-30]% with a very limited increment brought by the Proposed Transaction attributable to Mentor (Siemens: [10-20]%; Mentor [0-5]%).

(56) Third, the Parties will continue to be constrained by other players in the market. In particular, ANSYS will continue to be the leading supplier with 3D CFD segment share of more than 30% and a large number of competitors will remain in the market post-Transaction including Exa, and ESI Group. The market shares of the Parties and their competitors can be seen in Table 2.

remain important due to the increasing relevance of mechatronics (35) and the need to integrate mechanical and electrical design.

(61) The Notifying Party will be the first company to offer a broad range of both EDA and MPLM products. The Commission has therefore assessed the extent to which, post-Transaction, Siemens could foreclose MPLM-only or EDA-only rivals by hampering interoperability with its products.

(62) The Notifying Party submits that the merged entity will have neither the ability nor the incentive to foreclose competition in any neighbouring market, including the EDA and MPLM segment for the following reasons: (1) the PLM software products offered by Siemens and by Mentor are open systems and interoperable with applications provided by other companies; (2) customer bargaining power is such that providers of PLM software are generally required to offer interoperability between PLM solutions; (3) Siemens intends to maintain its open architecture policy post-merger, as it has following all previous acquisitions in the PLM space; and (4) Siemens would not have market power on any relevant market to raise prices for integrated mechanical and electronic services.

(63) The Commission considers that for the reasons set out below, the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market with respect to conglomerate effects as the merged entity would have neither the ability, nor it is likely to have the incentive, to foreclose competitor by reducing interoperability between its products and the PLM solutions of its rivals.

(64) First, neither Party has a strong position in EDA or MPLM software. With regard to MPLM, Siemens has a market share of [10-20]% at both the worldwide and EEA level whereas Mentor (36) is not active. (37) With regard to EDA software, Mentor has a market share of [10-20]% at the worldwide level and [10-20]% at an EEA-wide level whereas Siemens is not active. The Notifying Party submits that the only potential sub-segment of the EDA market where Mentor has a market share of 30% or more is EDA for PCB applications.

(65) Second, in each market (MPLM and EDA) customers will have alternatives to switch to which will act as a constraint on the merged entity post-Transaction. Both competitors and customers responding to the market investigation confirm that post-Transaction there would remain a sufficient number of competitors in both the MPLM and EDA markets. (38) Moreover, the market shares of the Parties and their competitors in the EDA and MPLM markets, presented in Table 3 and

Only one customer highlighted that switching EDA provider could be difficult in the short term. (41)

(67) Fourth, the market investigation is supportive of the Parties argument that the merged entity would have no incentive post-Transaction to reduce the levels of interoperability with products from other suppliers. (42) The views of competitors were mixed with some respondents, such as SAP, considering that the merged entity would have the incentive to reduce interoperability and cross-sell their software solutions among their combined installed bases and others, such as PTC noting that this would not be a practical strategy because customers would strongly oppose such efforts. (43) The latter view is confirmed by the market investigation since most of the customers did not consider that Siemens would have the incentive to degrade or exclude the interoperability of its PLM software solutions with the PLM software solutions of other providers, either for Mentor's EDA competitors or Siemens MPLM competitors. Fiat Chrysler Automobiles ("FCA") notes that either degrading or excluding integration would put Siemens at risk to loose PLM customers. Ericsson further considers that such a strategy would only shrink Siemens' addressable market. By excluding interoperability with other suppliers, Siemens would be able to sell only to those customers already using Mentor's EDA software. (44)

(68) Moreover, both Siemens and Mentor appear to have a business strategy of fostering interoperability. In particular, both Siemens and Mentor currently have long term bilateral interoperability agreements with other players in the PLM market in order to be able to provide solutions for customers. Siemens has in recent years undertaken multiple accretive acquisitions in the PLM industry and has maintained interoperability following each of these acquisitions. Moreover, both Siemens and Mentor participate in industry initiatives to support interoperability. (45) There is no evidence on the Commission's file that would indicate that Siemens would alter this strategy post-Transaction.

(69) Finally, most of the respondents to the market investigation do not expect that the Proposed Transaction would have any impact on the PLM software market and in any other potential segment. (46) Few respondents indicate that the Proposed Transaction may have a negative impact on the PLM software market. Two competitors note that the Proposed Transaction may have a negative impact on the market arguing that the merged entity will increase its financial power and market presence, and that the merged entity could foreclosure Mentor's competitors from supplying to Siemens (the second concern related to vertical relationships between Siemens and Mentor will be discussed in Section 5.3 below). (47) Moreover, one customer considers that its terms of agreement with Mentor would become less favourable after the Proposed Transaction. (48) A number of respondents also consider that the Proposed Transaction may have a positive impact by enhancing software functionalities and push other MPLM and EDA competitors to improve their software interoperability. (49)

(70) Accordingly, the Commission considers that the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market.

5.3. Vertical effects

(71) Mentor is active on the market with regard to the supply of EDA software for PCBs where it has a market share above 30%. Siemens is a customer in this market since it purchases EDA software.

(72) The Notifying Party submits that no competition concerns can be expected to arise given the limited vertical relationship.

(73) The Commission considers that for the reasons set out below, the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market with respect to potential foreclosure of Mentor's EDA software for PCBs, regardless of any possible segmentation.

(74) As regards potential concerns related to customer foreclosure, in 2015 Siemens' EDA software purchases worldwide from all software providers accounted for approximately EUR […] million (50) which corresponds to [0-5]% of the EDA software market. Therefore, in the event that post-merger Siemens were to source all its EDA software from Mentor, it would not materially change the competitive dynamics on the EDA market. Moreover, Siemens has entered in long-term agreements with a number of Mentor's competitors which cannot be terminated in the short-term.

(75) As regards potential concerns related to input foreclosure, the merged entity would not have any incentive to foreclose access to Mentor's EDA software. As described in paragraph (74) above, Siemens' EDA software purchases are limited while Mentor's revenue in the market are approximately USD […] million worldwide and USD […] million per year in Europe. By foreclosing access to Mentor's EDA, Siemens would not be able to compensate the reduction of sales in the EDA market.

(76) Finally, as discussed at paragraph (69) above, most of the respondent to the market investigation do not expect the Proposed Transaction to have any impact on the EDA market. (51) Only one respondent notes that the merged entity may have the incentive to foreclose competing Mentor's ESE suppliers from providing their software to Siemens. On this regard, the Commission notes that, first, Siemens does not have significant market power in the upstream market under any potential market definition (52); second, in 2015 Siemens' ESE software purchases worldwide from all software providers accounted for EUR […] million (53) which corresponds to [0-5]% of the ESE software market. Therefore, in the event that post-merger Siemens were to source all its ESE software from Mentor, it would not materially change the competitive dynamics on the ESE market.

(77) Accordingly, the Commission considers that the Proposed Transaction does not raise serious doubts as to its compatibility with the internal market.

6. CONCLUSION

(78) For the above reasons, the European Commission has decided not to oppose the Proposed Transaction and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the "Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the "EEA Agreement").

3 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, 16.4.2008, p. 1).

4 Commission decision of 27 April 2007 in Case M.4608 – Siemens/UGS Corporation, paragraph 10; Commission decision of 29 March 2010 in Case M.5763 – Dassault Systèmes/IBM DS PLM Software Business, paragraph 16.

5 In addition, the reach of PLM software has extended beyond the design of the manufacturing process to the actual execution of the manufacturing process. Further, what was at the time of the Commission’s previous decisions considered to be DPD would now appear to include software for the design of all types of products i.e. mechanical, electronic, software, as well as architecture and construction software and embedded software incorporated into the design of products.

6 See responses to Question 6 of Q2 – Questionnaire to customers.

7 See responses to Question 6 of Q1 – Questionnaire to competitors.

8 See Microsoft's responses to Question 6 of Q2 – Questionnaire to customers.

9 See responses to Question 8 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

10 See responses to Question 7 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

11 See responses to Question 9 of Q2 – Questionnaire to customers.

12 See responses to Question 9 of Q1 – Questionnaire to competitors.

13 See responses to Question 10 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

14 Commission decision of 29 March 2010 in case M.5763 – Dassault Systèmes/IBM DS PLM Software Business, paragraphs 17 - 19.

15 See responses to Q 10.2.1 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

16 MPLM software for CWH determines where wires need to physically pass through a product and where the necessary holes and fixtures need to be located and installed. EDA software for CWH on the other hand determines which devices are interconnected with each other and how the necessary signals are passed through the CWH. Data from EDA software systems for CWH and data from MPLM software for CWH is exchanged during the design process.

17 See responses to Questions 11 and 11.1 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

18 See responses to Question 11.2 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

19 Commission decision of 29 March 2010 in case M.5763 – Dassault Systèmes/IBM DS PLM Software Business, paragraph 21; and Commission decision of 27 April 2007 in Case M.4608 – Siemens/UGS, paragraph 11.

20 See responses to Question 12 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

21 See responses to Question 13 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

22 See responses to Question 17.3 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

23 See responses to Question 15 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

24 Source : Mentor Graphics and Siemens actual revenue and Siemens internal estimates based on the CIMData Report and market intelligence. European shares for competitors estimated by reference to published revenue by geographic region.

25 These figures include 100% of the revenues attributable to Frontline in this market. Frontline PCB Solutions is a 50/50 joint venture between Mentor and Orbotech active in relation to Digital Manufacturing for PCBs.

26 The Parties are not able to provide market share estimates at the EEA level but submit that the worldwide market shares are representative of the shares in the EEA.

27 See responses to Question 15 and 17.3of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

28 See responses to Question 26.1 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

29 See responses to Question 15 of Q1 – Questionnaire to competitors.

30 No affected market arises when considering a market for 1D CFD software alone as the Parties have a combined market share of [5-10]%.

31 Including 100% of the revenues attributable to CD Adapco in this market which Siemens acquired in April 2016.

32 See responses to Question 26.1 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

33 See responses to Question 18 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

34 See responses to Question 19 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

35 Mechatronics is as “a multidisciplinary field of science that includes a combination of mechanical engineering, electronics, computer engineering, telecommunications engineering, systems engineering and control engineering.

36 Mentor’s revenues in relation to CFD are allocated to its EDA revenues. However even if Mentor's CFD sales (with the exception of its CFD software which is suitable for electronics only) were allocated to MPLM, Mentor’s share of total MPLM sales in 2015 would be approx. [0-5]%.

37 When considering a combined market for MPLM and EDA software together, the Parties have a combined market share of [10-20]% worldwide (Siemens: [5-10]%; Mentor [5-10]%); and [10- 20]% in the EEA (Siemens: [5-10]%; Mentor [5-10]%).

38 See responses to Question 15.1 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers. The only exception to this is one customer that responded that it did not know whether there would be a sufficient number of competitors remaining in the EDA market.

39 Mentor’s revenues in relation to CFD are allocated to its EDA revenues. However even if Mentor’s CFD sales (with the exception of its CFD software which is suitable for electronics only) were allocated to MPLM, Mentor’s share of total MPLM sales in 2015 would be approx. (0-5)%.

40 See responses to Question 23 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

41 See responses to Question 24.1 of Q2 – Questionnaire to customers.

42 See responses to Question 21 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

43 See responses to Question 21 of Q1 – Questionnaire to competitors.

44 See responses to Question 21 of Q2 – Questionnaire to customers.

45 See for example: (1) Siemens public declaration of its commitment to interoperability: http://www.plm.automation.siemens.com/en us/about us/facts philosophy/open.shtm; (2) Siemens support of the worldwide initiative "Code of Openness -http://www.prostep.org/en/cpo.html; and (3) Mentor's Opendoor program which provides access to Mentor's software and includes over 100 partners.

46 See responses to Question 26 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

47 See responses to Question 26.1 of Q1 – Questionnaire to competitors.

48 See responses to Question 26.1 of Q2 – Questionnaire to customers.

49 See responses to Question 26.1 of Q2 – Questionnaire to customers.

50 See Notifying Party's response to question 4 of RFI N.1 of 8 February 2017.

51 See responses to Question 26 of Q1 – Questionnaire to competitors and Q2 – Questionnaire to customers.

52 See Notifying Party's response to question 1 of RFI N.2 of 10 February 2017.

53 See Notifying Party's response to question 4 of RFI N.1 of 8 February 2017.