Commission, October 4, 2019, No M.9426

EUROPEAN COMMISSION

Judgment

3M COMPANY / ACELITY

Subject: Case M.9426 – 3M Company/Acelity

Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 03.09.2019, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation (the “Transaction”) by which 3M Company (“3M”, US, or the “Notifying Party”) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of Acelity, Inc. (“Acelity”, US), by way of a purchase of shares3.

(2) 3M and Acelity are collectively referred to below as the “Parties”.

1. THE PARTIES

(3) 3M is a diversified technology company. Through its health care division, 3M offers a broad range of medical solutions, including advanced wound dressings.

(4) Acelity is primarily active in the development and commercialisation of advanced wound care products, including through its subsidiaries Kinetic Concepts, Inc, Systagenix Wound Management, Limited and Crawford Healthcare Limited.

2.THE OPERATION AND THE CONCENTRATION

(5) The Parties entered into a Stock Purchase Agreement on 1 May 2019. Under the terms of the Stock Purchase Agreement, 3M will acquire the 100% equity interest in Acelity that is currently directly held by Acelity L.P. Inc..

(6) As a result of the Transaction, 3M will obtain sole control over Acelity within the meaning of Article 3(1)(b) of the Merger Regulation.

3.EU DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 2 500 million4. Each of them has an EU-wide turnover in excess of EUR 100 million. In three Member States ([…], […] and […]), their combined turnover exceeds EUR 100 million and the turnover of each undertaking concerned exceeds EUR 25 million in each of these Member States. Neither 3M nor Acelity

achieves more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. The Transaction therefore has an EU dimension pursuant to Article 1(3) of the Merger Regulation.

4.COMPETITIVE ASSESSMENT

(8) The Transaction leads to horizontal overlaps between the activities of 3M and Acelity in relation to the supply of moist advanced wound care products. These overlaps give rise to affected markets only in relation to specific types of wound care products at national level.

(9) In addition, vertically affected markets arise in light of the vertical link between the activities of 3M upstream (film drapes, which are included as consumable products in negative pressure wound therapy (“NPWT”) kits) and Acelity downstream (supply of NPWT kits to hospitals and community customers).

1.1.Horizontal non-coordinated effects - Moist advanced wound care products

1.1.1.Market definition

1.1.1.1.Product market definition

(10) In previous decisions, the Commission concluded that (a) traditional wound care products (e.g., surgical dressings, fixation products and swabs), and (b) advanced wound care products belong to separate product markets as they do not offer the same performance and are not used for the same purpose.5

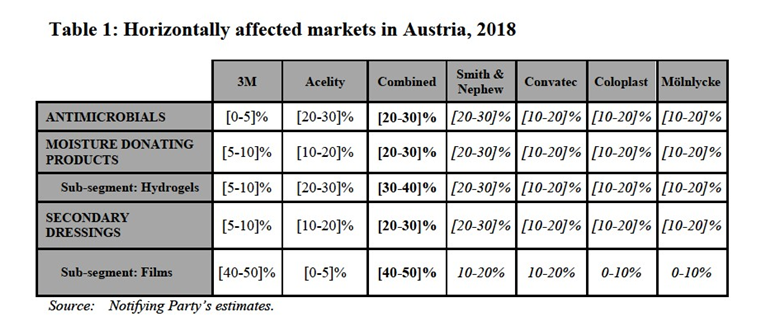

(11) In the market for advanced wound care products, the Commission further differentiated between (i) moist wound care products,6 (ii) active wound care products, and (iii) biological active wound care products.7 Within the segment of moist advanced wound care products (the only segment on which the Parties’ activities overlap) the following sub-segments were also identified: alginates, hydrofibres, foams, hydrocolloids, hydrogels, film dressings, contact layers and silver antimicrobials.8 Ultimately, the Commission left open whether each of these products would constitute a separate product market.

(12) The Commission also considered a potential alternative definition, grouping some moist advanced wound care products into the following categories: (i) a market segment for moisture-absorbing advanced wound care products that includes alginates, foams and hydrofibres, (ii) a market segment for moisture-donation advanced wound care products that includes hydrogels and hydrocolloids, (iii) a market segment for secondary dressings that includes films and contact layers, and (iv) a market segment for silver antimicrobials and other antimicrobials (which include all wound care products in other categories in which silver is incorporated).9 Ultimately, it did not reach a conclusion on this potential definition.

(13) The Notifying Party submits that the relevant product market is the supply of moist advanced wound care products, noting that each wound is unique and at a given time may be treated with more than one of the types of dressing identified above (whether used as substitutes, in combination or in sequence). It also observes that most suppliers are active across the whole range of moist advanced wound care products. To the extent that segmentation by product type is appropriate, the Notifying Party proposes to introduce a new sub-segment of moist wound care products not previously considered by the Commission. Superabsorbent dressings are moisture- absorbing advanced wound care products that are typically used on moderate to highly exudative wounds. As such, the Notifying Party submits they form part of the same product market as alginates, hydrofibres, and foams, with which they are largely substitutable. It also submits that hydrocolloids should not be categorized as “moisture-donating”, but rather as “moisture-absorbing” dressings.

(14) The majority of respondents to the Commission’s market investigation confirmed that moist advanced wound care products should be considered a separate product market from active wound care or biological wound care products, and indicated that it may be appropriate to consider separate markets for moisture-absorbing dressings, moisture-donating dressings, secondary dressings and antimicrobial products.10 The market investigation confirmed that superabsorbers should be considered to be “moisture-absorbing” but was inconclusive on the appropriate categorisation of hydrocolloids.11 The majority of respondents considered that it was not necessary to further sub-segment the market (for example by specific product), though it was noted that in some cases substitutability between specific products is limited.12

(15) In any event, for the purposes of the present case, the Commission considers that it is not necessary to conclude whether the market for moist advanced wound care should be segmented by category (i.e. moisture-absorbing products, moisture-donating products or wound dressings) or whether the individual product types should be considered as separate product markets, since competition concerns are unlikely to arise under any plausible market definition.

1.1.1.2.Geographic market definition

(16) In previous decisions, the Commission has left open whether the market for moist advanced wound care products is EEA-wide or national.13

(17) The Notifying Party submits that the relevant geographic market for moist advanced wound care and its sub-segments is EEA-wide because cross border trade, pan European tenders and regional buyer groups are common, there are no or low regulatory or transport barriers to trade, and because the competitor set is the same across the EEA.

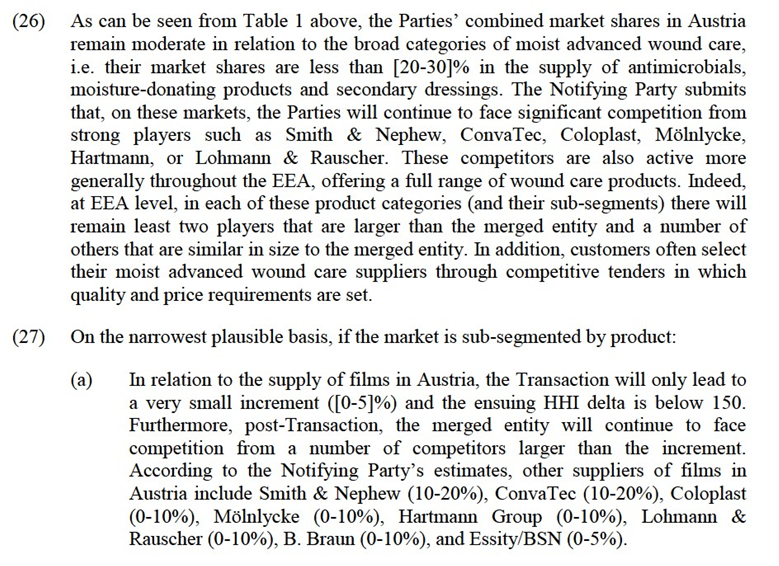

(18) Overall, the market investigation indicated that it may be appropriate to define the relevant geographic market as national. On the one hand, the majority of wound care suppliers confirmed that they are broadly active across the whole of the EEA.14 On the other, the market investigation confirmed that contracts with customers are typically at national or local level, that pricing levels vary between Member States and that there are differences in coverage of moist advanced wound care products (i.e. the extent to which they are reimbursed or are provided by healthcare authorities) between Member States.15

(19) In any event, the Commission considers that the exact geographic market definition can be left open for the purposes of the case at hand, as competition concerns are unlikely to arise under either a national or EEA-wide market definition.

4.1.2.Competitive assessment

(20) Under Articles 2(2) and 2(3) of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position.

(21) A merger can entail horizontal effects. In this respect, in addition to the creation or strengthening of a dominant position, the Commission Guidelines on the assessment of horizontal mergers under the Merger Regulation (“the Horizontal Merger Guidelines”)16 distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede competition, namely non-coordinated and coordinated effects. Non-coordinated effects may significantly impede competition, eliminating important competitive constraints on one or more firms, which consequently would have increased market power, without resorting to coordinated behaviour.

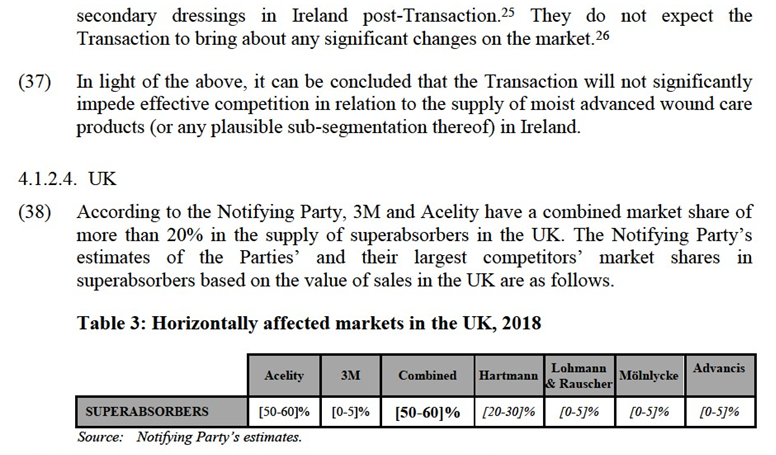

(22) This decision will analyse whether the Transaction is likely to raise serious doubts as to its compatibility with the internal market by the creation of non-coordinated effects in those markets on which the Parties’ activities lead to horizontal overlaps.

4.1.2.1. Overview of horizontally affected markets

(23) The Parties overlap in the supply of moist advanced wound care products in the EEA. They are active across all product categories (moisture-absorbing products, moisture-donating products, secondary dressings and antimicrobial products) and in each of the individual products belonging to these categories. However, the Transaction would not give rise to any horizontally affected markets at EEA level under any plausible product market definition (i.e. whether the product market is considered to be moist advanced wound care, the abovementioned product categories, or the individual products belonging to these categories).

(b) In relation to the supply of hydrogels in Austria, 3M adds a limited increment of [5-10]% (representing sales of less than €[...]) to Acelity’s share of [20- 30]%. Furthermore, post-Transaction, the merged entity will continue to face competition from a number of competitors larger than or similar in size to the increment. According to the Notifying Party’s estimates, other suppliers of hydrogels in Austria include Smith & Nephew ([20-30]%), ConvaTec ([10- 20]%), Coloplast ([10-20]%), Mölnlycke ([10-20]%), Hartmann Group (0- 10%), Lohmann & Rauscher (0-10%), B. Braun (0-10%), and Essity/BSN (0- 5%).

(28) More generally, the results of the market investigation confirmed that the Parties are not particularly close competitors. The majority of market participants responding to the market investigation identified only one of the Parties among the top three suppliers for each of the affected product categories (or their sub-segments) in Austria. Overall, it appears that each of the Parties compete more closely with other suppliers, rather than between themselves, both in relation to the specific product considered (e.g. hydrogels) and in relation to the product categories to which they belong.17

(29) In addition, the market investigation revealed that it is relatively easy for customers to change suppliers at the end of the contract or change procurement patterns during a contract since (i) customers usually select more than one supplier,18 and (ii) the products are generally procured through competitive bidding processes (in which price requirements can be set by customers).19 Therefore, there are no or low barriers to switching.

(30) Finally, the vast majority of respondents to the market investigation confirmed that they will continue to have a number of alternative suppliers from which to procure each of these products post-Transaction.20 They do not expect the Transaction to bring about any significant changes on the market.21

(31) In light of the above, it can be concluded that the Transaction will not significantly impede effective competition in relation to the supply of moist advanced wound care products (or any plausible sub-segmentation thereof) in Austria.

4.1.2.3.Ireland

(32) According to the Notifying Party, 3M and Acelity have a combined market share of more than 20% in the supply of secondary dressings in Ireland (secondary dressings are a category of products comprising contact layers and films). The affected market in the overall category of secondary dressings arises primarily from Acelity’s [50- 60]% market share in the supply of contact layers in Ireland. There is, however, no overlap in this sub-segmentation as 3M only supplies films, but not contact layers, in

(42) Finally, the vast majority of respondents to the market investigation confirmed that they will continue to have a number of alternative suppliers from which to procure superabsorbers in the UK post-Transaction.30 They do not expect the Transaction to bring about any significant changes on the market.31

(43) In light of the above, it can be concluded that the Transaction will not significantly impede effective competition in relation to the supply of moist advanced wound care products (or any plausible sub-segmentation thereof) in the UK.

4.1.3.Conclusion on horizontal non-coordinated effects

(44) For the reasons set out in Section 4.1, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market in the markets for the supply of moist advanced wound care products under any plausible product and geographic market definitions due to horizontal effects.

4.2. Vertical overlaps between the supply of film drapes (3M, upstream) and the production of NPWT kits (Acelity, downstream)

(45) Vertically affected markets arise in light of the vertical link between the activities of 3M upstream (film drapes, which are included as consumable products in NPWT kits) and Acelity downstream (supply of NPWT kits to hospitals and community customers).32

4.2.1.Market definition - Negative Pressure Wound Therapy devices (“NPWT”)

4.2.1.1.Product market definition

(46) NPWT technology promotes healing in complex wounds by applying controlled negative pressure (sub-atmospheric or “vacuum” pressure) to a wound site through a specially sealed dressing. The negative pressure removes excessive exudate to allow wound healing, reduce edema, and increase metabolic activity in the cells. This promotes blood flow to the area and leads to growth of healthy granular tissue, which fills the wound bed.

(47) In Apax/Kinetic Concepts,33 the Commission considered that NPWT devices belong to the active wound care products category. While the Commission assessed market shares both in the broader market for active wound care products and in the narrowest possible product market for NPWT devices, it ultimately left the precise market definition open.

(48) The Notifying Party submits that the relevant product market is the supply of active wound care products and that NPWT products do not form a separate product market.

(49) In any event, in the present case, the product market definition can be left open, as competition concerns are unlikely to arise under the narrowest product market definition (i.e. NPWT devices), where the Parties’ market shares are at their highest.34

4.2.1.2.Geographic market definition

(50) As regards the geographic market, the Commission has so far left open the question of whether the market for advanced wound care products is national or EEA-wide.35

(51) The Notifying Party submits that the relevant geographic market is EEA-wide, noting inter alia that NPWT products are the same across the EEA, intra-EEA transportation costs are very low, and NPWT suppliers ship their products across the EEA from a few manufacturing plants.

(52) In any event, in the present case, the geographic market definition can be left open, as competition concerns are unlikely to arise under either a national or EEA-wide market definition.

4.2.2.Market definition - Film drapes

4.2.2.1.Product market definition

(53) Film drapes are transparent, airtight, adhesive polyurethane film dressings. Film drapes are used with NPWT devices to seal the wound and to prevent entry of air and bacteria, creating a “vacuum seal.” The film drape covers the dressing and secures the foam, allowing negative pressure to be maintained evenly at the wound site. Film drapes are included in NPWT kits sold to customers and are also sold independently (either by themselves or, more commonly, as part of dressings kits for use with particular NPWT devices).36

(54) Film drapes produced for NPWT use have two relevant stages of production. They typically start as bulk rolls of uncut, non-adhesive film drapes (“uncut film”). Uncut film is then “converted” into finished film drapes for NPWT use (“finished film drapes”) through a process that involves adding an adhesive, backing layers, and handling bars which assist with applying the finished film drape onto patients and cutting the film to specification for the specific NPWT dressing.

(55) The Commission has not assessed film drapes in the past. The Notifying Party submits that the relevant product market in this case is the upstream supply of film drapes appropriate for NPWT use. The Notifying Party submits that any further segmentation, for example between uncut film and finished film drapes, is not appropriate.

(56) The market investigation indicated that it may be appropriate to distinguish between the supply of uncut film and finished film drapes appropriate for NPWT use. While uncut film has a number of applications, including use with NPWT after conversion,37 finished film drapes can generally only be used with the specific NPWT device for which they have been approved. However, the market investigation also revealed that the equipment used to produce finished film drapes can also be used to produce wound care dressings for many other applications.38

(57) In any event, the question of whether uncut film drapes appropriate for use with NPWT and finished film drapes for use with NPWT devices constitute separate markets can be left open, as competition concerns are unlikely to arise under either plausible market definition.

4.2.2.2.Geographic market definition

(58) The Notifying Party submits that the market for the upstream supply of film drapes appropriate for NPWT use is global in scope since the product is highly commoditized and transportation costs are low.

(59) The majority of respondents to the market investigation confirmed that suppliers based outside the EEA can and do compete to supply film drapes to customers in the EEA.39 Indeed, 3M supplies film drapes to […] in […] from 3M’s film drape manufacturing facility in […]. Likewise, […] supplies film drapes to […] in […] from its manufacturing facility in […].

(60) In any event, the geographic market definition can be left open in the present case, as competition concerns are unlikely to arise under either an EEA-wide or worldwide market definition.

4.2.3.Competitive assessment

(61) According to the Non-Horizontal Guidelines,40 non-coordinated effects may significantly impede effective competition as a result of a vertical merger if such merger gives rise to foreclosure. Foreclosure occurs where actual or potential competitors' access to supplies or markets is hampered or eliminated as a result of the merger, thereby reducing those companies' ability and/or incentive to compete.41 Such foreclosure may discourage entry or expansion of competitors or encourage their exit.42

(62) The Non-Horizontal Guidelines distinguish between two forms of foreclosure. Input foreclosure occurs where the merger is likely to raise the costs of downstream competitors by restricting their access to an important input. Customer foreclosure occurs where the merger is likely to foreclose upstream competitors by restricting their access to a sufficient customer base.43

(63) With regard to input foreclosure, in assessing the likelihood of an anticompetitive foreclosure scenario, the Commission examines, first, whether the merged entity would have, post-Transaction, the ability to substantially foreclose access to inputs, second, whether it would have the incentive to do so, and third, whether a foreclosure strategy would have a significant detrimental effect on competition downstream.44

(64) With regard to customer foreclosure, in assessing the likelihood of an anticompetitive foreclosure scenario, the Commission examines, first, whether the merged entity would have the ability to foreclose access to downstream markets by reducing its purchases from its upstream rivals, second, whether it would have the incentive to reduce its purchases upstream, and third, whether a foreclosure strategy would have a significant detrimental effect on consumers in the downstream market.45

(65) The Notifying Party submits that vertically affected markets arise in light of Acelity’s market shares on the market for NPWT devices,46 in which the Notifying Party estimates that Acelity holds a share of [30-40]% in the EEA and up to [80- 90]% at national level.47 3M is not active in the supply of NPWT devices.

(66) Respondents to the market investigation confirmed that Acelity is the largest supplier of NPWT kits by a considerable margin, and indicated that its EEA-wide market shares may be higher than the Notifying Party’s estimates.48

(67) On the upstream markets, the Notifying Party estimates that 3M holds a market share of less than [5-10]% on the market for uncut film and finished film drapes, both in the EEA and worldwide. The Notifying Party notes that once uncut film has been converted to finished film drapes for use with a particular NPWT device, it can only be used with the specific NPWT device for which it has been manufactured and approved.

4.2.3.1.Input foreclosure

(68) The Notifying Party submits that 3M’s position in the supply of film drapes appropriate for use with NPWT devices (be it uncut film or finished film drapes) is marginal with a market share of less than [5-10]% both in the EEA and worldwide. Post-Transaction many alternative suppliers of film drapes will remain active on the market.

(69) The market investigation confirmed that competing NPWT producers will continue to have sufficient sources of supply for film drapes appropriate for use with NPWT devices.49 In addition, already pre-Transaction, 3M is not a material supplier of film drapes to any of Acelity’s NPWT competitors,50 so the Transaction will not bring about any significant change in the market.

(70) In light of the above, the Commission considers that the merged entity would not have the ability to engage in an input foreclosure strategy and that it is unlikely that the Transaction would lead to input foreclosure risks in relation to the supply film drapes in the EEA or globally.

4.2.3.2.Customer foreclosure

(71) The Notifying Party submits that the merged entity will not have the ability to engage in a customer foreclosure strategy. Acelity currently procures […]. The Notifying Party submits that 3M […]. The Notifying Party further explains that it is necessary to design, test and obtain regulatory approval for the finished film drapes to be used in a particular NPWT kit, which may take […] to complete. Therefore, it argues that the merged entity will not have the ability to […]. Moreover, it considers that […]. Finally, it argues that there will continue to be a number of NPWT suppliers to whom film drape suppliers can sell post-Transaction.

(72) As regards uncut film, the respondents to the market investigation confirmed that uncut film is used for a wide range of applications other than with NPWT devices and that post-Transaction a number of suppliers will continue to sell uncut film for NPWT use and other applications.51 This supports the Notifying Party’s estimates that only around [10-20]% of uncut film is ultimately used with NPWT devices. Consequently, Acelity only represents a small proportion of the overall demand for uncut film.52 Therefore, post-Transaction, suppliers of uncut film will have a large array of customers to turn to. In light of this, it seems unlikely that the merged entity would have any ability to foreclose uncut film suppliers (upstream) by attempting a customer foreclosure strategy.

(73) As regards finished film drapes more specifically, once uncut film has been converted into finished film for use with a particular NPWT device (for which the finished film is approved), it can only typically be used together with that device. Acelity is the largest NPWT player by some margin and so for some suppliers of uncut film drapes it is an important customer with a significant degree of market power in the downstream market. In addition, Acelity is responsible for seeking authorisation for the finished film drapes to be used together with its NPWT devices and consequently can determine which supplier’s finished film drapes can be used with its NPWT devices. The respondents to the market investigation indicated that film drape suppliers have limited opportunities to sell finished film drapes for use with NPWT devices when their products are not approved for use with the particular device.53 Therefore, while the merged entity would need to design, test and obtain regulatory approval to use 3M’s finished film drapes in all of Acelity’s NPWT devices and increase its conversion capacity, which would require some time and investment, it cannot be excluded that the merged entity would have the ability to foreclose access to the downstream markets in the medium-term. However, it is not necessary for the Commission to conclude on whether the merged entity would have this ability, as in any event such a strategy would be unlikely to have an adverse impact on the downstream market.

(74) As regards incentives, respondents to the market investigation considered that in the medium-term the merged entity may have the incentive to reduce purchases from third parties and vertically integrate its film drape and NPWT activities.54 However, it is not necessary for the Commission to conclude on whether the merged entity would have this incentive, as in any event such a strategy would be unlikely to have an adverse impact on the downstream market.

(75) Even if the combined incentive had the ability and incentive to foreclose customers, it is unlikely that a customer foreclosure strategy would have an adverse impact in the downstream market.

(76) First, the market investigation confirmed that the rotary die presses used to convert uncut film into finished film drapes for use with NPWT devices can be used to produce other wound dressings and disposable medical products.55 Reconfiguration of the equipment can be done relatively easily and with limited cost or time required.56 Therefore, there are effective and timely counter-strategies that film drapes suppliers can deploy over time to mitigate a reduction in demand and it appears likely that these finished film drape suppliers will continue to be able to meet existing or new demand from NPWT suppliers.

(77) Second, respondents to the market investigation confirmed that post-Transaction there will remain a number of NPWT competitors and that at least some of these currently source finished film drapes from third parties.57 Conversely, respondents to the market investigation expect that these NPWT competitors will continue to have sufficient sources of supply for finished film drapes post-Transaction.58

(78) Third, it is unlikely that such a strategy would impact competing NPWT providers to such an extent as to allow the merged entity to profitably raise prices or reduce output downstream. The cost of converting uncut film into finished film drapes is low; according to the Notifying Party, conversion represents less than […]% of the total cost of producing NPWT kits. In addition, some competing NPWT producers already convert uncut film to finished film drapes for use in their NPWT kits in- house and would not be affected by such a foreclosure strategy. The market investigation indicated that the costs for an existing wound care manufacturer to begin converting uncut film in-house for use with its own NPWT devices, while not immaterial, are not prohibitive (and that this can be an attractive investment for wound care manufacturers as they can also use the equipment for other purposes).59

(79) In light of the above, the Commission considers that it is unlikely that the Transaction would lead to customer foreclosure risks in relation to the supply of film drapes in the EEA or globally.

4.2.4.Conclusion

(80) In light of the above, the Transaction does not raise serious doubts as to its compatibility with respect to the vertical relationships between 3M’s supply of film drapes (upstream) and Acelity’s production of NPWT kits (downstream) under any plausible market definition.

4.3.Conglomerate effects

(81) The Transaction does not give rise to any conglomerate effects or concerns for the following reasons.

4.3.1.Conglomerate effects between different categories of moist advanced wound care products.

(82) Both Parties are already active in most moist advanced wound care segments and have not engaged in tying or bundling. The Transaction will not affect the Parties’ ability or incentive to tie/bundle moist advanced wound care products since (i) the Parties are constrained by a number of strong and active competitors in each segment and across the EEA, (ii) the Parties’ market shares and/or the increment are generally moderate and there are limited affected markets on the narrowest plausible basis, (iii) these products are often sold in response to tenders and the market investigation confirmed that the tenders are often for the individual types of moist advanced wound care product,60 and (iv) the market investigation confirmed that it is generally the customer (and not the supplier) that determines the specific products or combinations of products for which it will seek quotes.61

4.3.2.Conglomerate effects between NPWT and moist advanced wound care products.

(83) Acelity is already active in most moist advanced wound care segments and has not engaged in tying or bundling. The Transaction will not affect the Parties’ ability or incentive to leverage Acelity’s position in NPWT into moist advanced wound care products since (i) the Parties are constrained by a number of strong and active competitors in each moist advanced wound care segment and across the EEA, (ii) 3M is not active in the supply of NPWT products and so the Transaction does not change Acelity’s ability to leverage from NPWT into moist advanced wound care as there is no increment in NPWT, (iii) the market investigation confirmed that NPWT and moist advanced wound care products are generally procured separately62, and (iv) the market investigation confirmed that it is generally the customer (and not the supplier) that determines the specific products or combinations of products for which it will seek quotes.63

4.3.3.Conglomerate effects between NPWT and film drapes sold independently of NPWT kits.

(84) Customers of NPWT devices procure finished film drapes either (i) as part of a NPWT kit containing the consumables necessary for use with the NPWT device included in the kit, or (ii) independently from a NPWT kit but for use with the particular NPWT device for which its use has been approved (either as part of a pack of dressings including film drapes or, less commonly, as finished film drapes only). The Transaction is unlikely to have any material impact on customers’procurement of finished film drapes independently of NPWT kits. This is because even when film drapes are procured independently from NPWT kits, they are typically procured from the NPWT supplier (and not directly from the manufacturer of finished film drapes). In the case of Acelity, its third party converters do not supply finished film drapes directly to end customers. Already pre-Transaction, it is Acelity (and not the converter) that sells finished film drapes independently of NPWT kits. Therefore, the Transaction has no impact on any plausible market for the supply of finished film drapes independently of NWPT kits.

5.CONCLUSION

(85) For the above reasons, the European Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement.

1 OJ L 24, 29.1.2004, p. 1 (the “Merger Regulation”). With effect from 1 December 2009, the Treaty on the Functioning of the European Union (“TFEU”) has introduced certain changes, such as the replacement of “Community” by “Union” and “common market” by “internal market”. The terminology of the TFEU will be used throughout this decision.

2 OJ L 1, 3.1.1994, p. 3 (the “EEA Agreement”).

3 Publication in the Official Journal of the European Union No C 308, 12.09.2019, p. 7.

4 Turnover calculated in accordance with Article 5 of the Merger Regulation.

5 See Cases COMP/M.7323 - Nordic Capital/GHD Verwaltung, decision of 08.08.2014; COMP/M.4367 - APW/APSA/Nordic Capital/Capio, decision of 16.03.2007; COMP/M.5190 - Nordic Capital/ConvaTec, decision of 15.07.2008; COMP/M.3816 - Apax/Mölnlycke, decision of 15.06.2005; COMP/JV.54 - Smith&Nephew/Beiersdorf, decision of 30.01.2001.

6 The Commission noted that the common functionality of moist advanced wound care products that differentiates them from other advanced wound care products is that they provide a moist environment that can be beneficial for healing. See e.g. Case COMP/M.7323 - Nordic Capital/GHD Verwaltung, decision of 08.08.2014.

7 The Commission noted that the functions performed by each of these product categories are distinct: (i) moist wound care products maintain optimum conditions for tissues to repair themselves; (ii) active wound care products encourage better healing by interacting with the tissues at a physiological and cellular level, and (iii) biologically active wound care products either deliver bioactive compounds or are constructed from material having endogenous activity. See Case COMP/M.3816 - Apax/Mölnlycke, decision of 15.06.2005.

8 See Cases COMP/M.7323 - Nordic Capital/GHD Verwaltung, decision of 08.08.2014; COMP/M.4579 - Investor/Morgan Stanley/Mölnlycke, decision of 27.03.2007; COMP/M.4229 - APHL/L&R/Netcare/General Healthcare Group, decision of 25.07.2006; COMP/M.3816 - Apax/Mölnlycke, decision of 15.06.2005.

9 See Cases COMP/M.7323 - Nordic Capital/GHD Verwaltung, decision of 14.08.2014, and COMP/M.5190 - Nordic Capital/ConvaTec, decision of 15.07.2008.

10 Replies to question 4 of Q1 – questionnaire to advanced wound care competitors and replies to question 3 of Q2 – questionnaire to customers.

11 Replies to questions 5.1 and 5.2 of Q1 – questionnaire to advanced wound care competitors and replies to questions 4.1 and 4.2 of Q2 – questionnaire to customers.

12 Replies to questions 5.3 and 7 of Q1 – questionnaire to advanced wound care competitors and replies to questions 4.3 and 5 of Q2 – questionnaire to customers.

13 See e.g. Cases COMP/M.7323 - Nordic Capital/GHD Verwaltung, decision of 14.08.2014; COMP/M.4367 - APW/APSA/Nordic Capital/Capio, decision of 16.03.2007 and COMP/M.3816 - Apax/Mölnlycke decision of 15.06.2005. In case COMP/M.5190 – Nordic Capital/ConvaTec, decision of 15.07.2008, the Commission however defined the geographic market for advanced wound care products as national for the purposes of that specific case.

14 Replies to questions 8 and 8.1 of Q1 – questionnaire to advanced wound care competitors.

15 Replies to questions 9, 9.1, 10, 10.1 and 10.2 of Q1 – questionnaire to advanced wound care competitors and replies to question 6 of Q2 – questionnaire to customers.

16 Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings, OJ C 31, 5.2.2004 p.5.

17 Replies to questions 11 and 13 of Q1 – questionnaire to advanced wound care competitors and replies to question 9 of Q2 – questionnaire to customers.

18 Replies to questions 7 and 7.1 of Q2 – questionnaire to customers.

19 Replies to question 8 of Q2 – questionnaire to customers.

20 Replies to question 16 of Q1 – questionnaire to advanced wound care competitors and replies to question 10 of Q2 – questionnaire to customers.

21 Replies to question 29 of Q1 – questionnaire to advanced wound care competitors and replies to question 11 of Q2 – questionnaire to customers.

22 Replies to questions 11 and 17 of Q1- questionnaire to advanced wound care competitors and replies to question 14 of Q2-questionnaire to customers.

23 Replies to questions 12 and 12.1 of Q2- questionnaire to customers.

24 Replies to questions 13 of Q2- questionnaire to customers.

25 Replies to questions 20 of Q1- questionnaire to advanced wound care competitors and replies to question 16 of Q2-questionnaire to customers.

26 Replies to questions 29 of Q1- questionnaire to advanced wound care competitors and replies to question 16 of Q2-questionnaire to customers.

27 Replies to questions 11 and 21 of Q1- questionnaire to advanced wound care competitors and replies to question 19 of Q2-questionnaire to customers.

28 Replies to questions 12 and 12.1 of Q2- questionnaire to customers.

29 Replies to questions 13 of Q2- questionnaire to customers.

30 Replies to question 24 of Q1 – questionnaire to advanced wound care competitors and replies to question 15 of Q2 – questionnaire to customers.

31 Replies to question 29 of Q1 – questionnaire to advanced wound care competitors and replies to question 16 of Q2 – questionnaire to customers.

32 For completeness, barrier film would technically be an additional vertically affected market in light of the link between 3M’s supply of barrier film upstream and Acelity’s supply of NPWT kits downstream. Barrier films are a polymeric solution, which upon application to intact or damaged skin forms a waterproof film acting as a protective interface between the skin and bodily wastes, fluids, adhesive products, and friction. Barrier films are widely used in many clinical settings, including with NPWT technology to improve the seal created by a film drape. Barrier films are typically sold separately from NPWT kits but in some limited cases are included in the kits. In any event, no vertical competition concerns arise in light of this link as the Transaction will not bring about any change in the market: (i) input foreclosure is implausible as already pre-Transaction 3M does not supply barrier film to any of Acelity’s competitors, and (ii) customer foreclosure is implausible as already pre-Transaction Acelity purchases the entirety of its barrier film needs from 3M. Moreover, no specific concern was raised in this respect during the market investigation. In light of the above, the Commission considers that the Transaction does not raise serious doubts as regards this vertical relationship between barrier film and NPWT, which will not be assessed further in this decision.

33 See Case COMP/M.6343 - Apax/Kinetic Concepts, decision of 7 October 2011. Note that Kinetic Concepts is a predecessor company to Acelity.

34 See paragraph 65 and footnote 47 below.

35 See Case No. COMP/M.6343, Apax/Kinetic Concepts, decision of 7 October 2011.

36 The components of Acelity’s NPWT kits include: (i) the NPWT device, (ii) film drapes, (iii) a foam or gauze (compressible, open and porous material, which is placed in the wound to ensure that the negative pressure is applied across the entire wound), (iv) a drainage tube used to remove excess exudate from the wound and drain it to the collection canister, (v) a connection pad which connects the drainage tube to the wound dressing, and (vi) barrier films, which are an optional component of the kits used as skin preparatory products to aid in ensuring a reliable seal.

37 Replies to question 4.2 of Q3 – questionnaire to film drape competitors and Non-confidential minutes of a conference call with a NPWT supplier on 18 September 2019.

38 Replies to question 4.3.1 of Q3 – questionnaire to film drape competitors and Non-confidential minutes of a conference call with a NPWT supplier on 18 September 2019.

39 Replies to question 8 of Q3 – questionnaire to film drapes competitors and to question 28 of Q1 – questionnaire to advanced wound care competitors.

40 Guidelines on the assessment of non-horizontal mergers under the Council Regulation on the control of concentrations between undertakings ("Non-Horizontal Guidelines"), OJ C 265, 18.10.2008, p. 6-25.

41 See Non-Horizontal Guidelines, paragraph 18.

42 See Non-Horizontal Guidelines, paragraph 29.

43 See Non-Horizontal Guidelines, paragraph 30.

44 See Non-Horizontal Guidelines, paragraph 32.

45 See Non-Horizontal Guidelines, paragraph 59.

46 For completeness, Acelity’s primary active advanced wound care product is NPWT. Its market share in a broader market for active advanced wound care products would be less than 30% across the EEA. While Acelity’s share may exceed 30% on some national markets for active advanced wound care products, in all cases its share in this broader category is driven by and lower than its market share for NPWT. As the vertical link between 3M’s film drapes is with NPWT (and not other active advanced wound care products sold by Acelity), the broader category of active advanced wound care products is not considered further.

47 In particular, Acelity’s market share is 30% or more in Austria ([80-90]%), Belgium ([60-70]%), Cyprus ([60-70]%), France ([30-40]%), Germany ([60-70]%), Ireland ([60-70]%), Luxembourg ([40-50]%), Slovenia ([50-60]%), Sweden ([50-60]%), and the UK ([30-40]%).

48 Non-confidential minutes of a conference call with a wound care supplier, 30 August 2019; Non- confidential minutes of a conference call with a wound care supplier, 17 September 2019; Non- confidential minutes of a conference call with a wound care supplier, 18 September 2019; and Non- confidential minutes of a conference call with a film drape supplier, 5 September 2019.

49 Non-confidential minutes of a conference call with a wound care supplier, 30 August 2019; Non- confidential minutes of a conference call with a wound care supplier, 17 September 2019; and Non- confidential minutes of a conference call with a wound care supplier, 18 September 2019.

50 3M […]. 3M only supplies […] amount of uncut film drapes to […] – 3M’s sales to […] amounted to less than €[…] in 2018.

51 Replies to question 6.1 of Q3 – questionnaire to film drapes competitors. Non-confidential minutes of a conference call with a wound care supplier, 30 August 2019; Non-confidential minutes of a conference call with a wound care supplier, 17 September 2019; Non-confidential minutes of a conference call with a wound care supplier, 18 September 2019; and Non-confidential minutes of a conference call with a film drape supplier, 5 September 2019.

52 The Notifying Party submits that Acelity’s demand for uncut film appropriate for NPWT use would be less than [10-20]% of the total demand for uncut film drapes appropriate for NPWT use at global level.

53 Non-confidential minutes of a conference call with a wound care supplier, 18 September 2019. For example, hospitals may be reluctant to purchase non-approved finished film drapes for use with NPWT devices.

54 Replies to question 10 of Q3 – questionnaire to film drapes competitors. Non-confidential minutes of a conference call with a film drape supplier, 5 September 2019.

55 Replies to question 6.1 of Q3 – questionnaire to film drapes competitors. Non-confidential minutes of a conference call with a wound care supplier, 17 September 2019; and Non-confidential minutes of a conference call with a wound care supplier, 18 September 2019.

56 Non-confidential minutes of a conference call with a wound care supplier, 17 September 2019; and Non- confidential minutes of a conference call with a wound care supplier, 18 September 2019.

57 Responses to question 26 of Q1 – questionnaire to advanced wound care competitors. Non-confidential minutes of a conference call with a wound care supplier, 17 September 2019; and Non-confidential minutes of a conference call with a wound care supplier, 18 September 2019.

58 Non-confidential minutes of a conference call with a wound care supplier, 30 August 2019; Non- confidential minutes of a conference call with a wound care supplier, 17 September 2019; and Non- confidential minutes of a conference call with a wound care supplier, 18 September 2019.

59 Non-confidential minutes of a conference call with a wound care supplier, 18 September 2019.

60 Non-confidential minutes of a conference call with a wound care supplier, 18 September 2019, replies to questions 14, 18 and 22 of Q1 – questionnaire to advanced wound care competitors and replies to questions 8, 13 and 18 of Q2 – questionnaire to customers.

61 Non-confidential minutes of a conference call with a wound care supplier, 30 August 2019.

62 Non-confidential minutes of a conference call with a wound care supplier, 18 September 2019, replies to questions 14, 18 and 22 of Q1 – questionnaire to advanced wound care competitors and replies to questions 8, 13 and 18 of Q2 – questionnaire to customers.

63 Non-confidential minutes of a conference call with a wound care supplier, 30 August 2019.